Abdul Rahman Shaik*![]() | Shaiku Shahida Saheb

| Shaiku Shahida Saheb![]() | Ibrahim Alnour Ibrahim Abdulmajeed

| Ibrahim Alnour Ibrahim Abdulmajeed![]() | Salim Mohammed Bafaqeer

| Salim Mohammed Bafaqeer![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The objective of education for sustainable development is to incorporate concerns of sustainable development in teaching and learning, hence enabling the Higher Education Institutions (HEIs) to achieve Sustainable Development Goals (SDGs). The current study explores the incorporation of SDGs into the accounting programs of higher educational institutions in Saudi Arabia. The study uses quantitative research for analysis. A structured questionnaire was designed to incorporate different aspects of demography and various factors related to incorporating SDG 4 (ensuring quality education) and SDG 8 (decent work and economic growth) into the accounting curriculum. The study population consisted of Saudi Arabian Universities, and the study sample comprised students at different levels of the accounting program at Prince Sattam bin Abdulaziz University. The final study sample consisted of 91 responses. The study has selected accounting courses that are significant for incorporating SDGs, ranking them based on the responses received. Further, the study estimated two models using simple regression where SDG 4 (quality education) and SDG 8 (economic growth and productive employment) are employed as dependent variables alternatively. At the same time, student willingness and student perception were the independent variables. The results indicate that students believe sustainability concepts should be integrated into all the accounting courses examined in the studies, such as Intermediate Accounting, Managerial Accounting, Advanced Accounting, and Auditing, with particular emphasis on Managerial Accounting (based on the assumption of 20.9% students). Further, the empirical findings reveal that accounting students are interested in integrating accounting courses with Sustainability and favor incorporating the SDGs into the accounting curriculum (the coefficients of student willingness and student perception were 0.19 and 0.57, respectively, significant at less than 5% and 1% level of significance). Based on the quantitative findings, the study recommends incorporating SDG 4 and SDG 8 into the accounting curriculum at Prince Sattam bin Abdulaziz University.

sustainable development, higher educational institutions, accounting, SDG-4 quality education, SDG-8 decent work and economic growth, Saudi Arabia

Globalization and technology are often recognized as primary forces driving economic upsurge [1]. In recent times, sustainable development has garnered considerable attention due to several key factors that underscore the potential for economic growth for individuals and communities through sustainable, uninterrupted, and comprehensive economic upswing worldwide [2]. This economic upswing has paved the way for many challenges in achieving sustainable development, especially regarding the environment and society. Consequently, the stakeholder nations of the UN have adopted the Sustainable Development Agenda for 2030, which defines 17 SDGs and their associated targets. The UNECE on Education for Sustainable Development strategy presents education as an essential tool for attaining sustainable development because it enables individuals to make informed decisions and choices that support sustainability [3]. The objective of education for sustainable development is to incorporate concerns of sustainable development in teaching and learning, hence enabling the Higher Education Institutions (HEIs) to achieve SDGs. Indeed, the purpose of SDG 4 is to ensure quality education, with targets that focus on achieving quality technical education and learning relevant skills for employment and business.

HEIs, including universities, should recommend the SDGs and implement quality assurance systems to track and assess their progress. They should develop a lifelong learning plan for students and motivate them to embrace innovative methods by providing valuable skill-building opportunities [4]. Further, the implementation and evaluation of SDGs should be part of the University's vision. Furthermore, university programs can support the achievement of the SDGs by utilizing diverse teaching and learning methods and integrating them into the curriculum. Implementing the SDGs in universities relies on the pragmatic approach to teaching and learning across undergraduate and graduate programs, professional training, executive education, electronic learning, and student extracurricular activities [5, 6].

As previously stated, providing quality education is a key SDG in developing nations [7]. Accounting literature debates the approaches accounting faculty use to shape students' perspectives, enabling them to contribute meaningfully to SDGs [8]. According to Pit-Watson [9], this contribution is linked to environmental accounting, integrated reporting, sustainability reporting, carbon accounting, etc. Further, the accounting faculty must recognize the driving forces of change in higher education. However, it is concerning that, so far, most new undergraduate and graduate accounting programs or modifications to existing accounting curricula have adhered mainly to traditional models [8, 10]. Therefore, the International Sustainable Standards Board (ISSB) has developed two sustainability disclosure standards: disclosure of sustainability-related financial information and disclosures related to climate change. The accounting faculty and professionals need to incorporate these standards into the accounting curriculum to bring in a model more suitable for sustainable development in terms of economic, social, and governance (ESG). Cho and Mäkelä [11] observe that the sustainability disclosure standards proposed by ISSB put the accounting academia in a dilemma regarding incorporating sustainability into accounting courses and curricula. Further, they observed that education on sustainability disclosures required practical knowledge and skills on corporate accountability and performance. Therefore, incorporating Sustainability into accounting curricula poses a significant challenge for the accounting faculty and practitioners. The other challenge is the perception of accounting students incorporating Sustainability into the existing accounting courses and curricula. Education, regardless of specialization, presumes to some extent that students from diverse societal backgrounds who become leaders will gain a deeper understanding of the environment and society, ensuring their actions align with this awareness [12].

The Ministry of Education in the Kingdom of Saudi Arabia is committed to realizing its vision for SDGs by promoting continuous economic growth while preserving the nation's natural and environmental resources. It is dedicated to achieving societal, economic, and environmental Sustainability. The Ministry's SDG objectives include providing inclusive and high-quality education for all segments of society, promoting lifelong learning, and developing higher education infrastructure. The ministry has initiated efforts to support this by building a knowledge-driven society through a knowledge-based economy. Therefore, considering discussions of previous research on Sustainability and the commitment of MoE to achieving the SDGs on education, it becomes significant for the current study to examine the incorporation of Sustainability into the accounting curriculum of Saudi Arabian Universities. Moreover, past research has examined the embedding of SDGs in HEIs, and very few are primarily related to accounting. Furthermore, the current study will be the first to explore the incorporation of Sustainability into the accounting curriculum of Saudi Arabian Universities.

2.1 SDGs in higher education institutions

Crespo et al. [3] examined the experience of SDGs in HEIs by evaluating students' assignments using 17 SDGs as a rubric. They found that social and technical aspects mostly follow the environmental aspect of sustainable development. Fleaca et al. [2] studied the capacity of Higher Educational Institutions to incorporate the SDGs into teaching and learning using a scoping diagram and the SIPOC method. They found the scoping diagram approach to be the most suitable model to report the extent of incorporation of Sustainability towards achieving SDGs. Albareda-Tiana et al. [13] studied the SDG implementation at the University level using semi-structured interviews. They identified different perceptions, challenges, and difficulties in implementing SDGs at the University level. Franco et al. [14] studied the responsibility of HEIs in equipping the students with the required skills for achieving the SDGs through distinct methodological techniques. They reported incorporating higher education for sustainable development in the curriculum and policies by understanding the gaps and differences of the HEfSD plan. Filho et al. [6] studied the benefits of incorporating SDGs into teaching at the university level, which can motivate students to study the concepts of Sustainability. They collected data from universities worldwide through a survey. They found that HEIs are engaged in incorporating SDGs and recommended more engagement in their teaching and learning. Argento et al. [15] examined the representation and engagement of HEIs in incorporating Sustainability into their curriculum through a case study on one Swedish University. They found that HEIs need to put more regular effort into incorporating sustainability by joining networks that initiate and help educational institutions achieve the SDGs. Miotto et al. [16] investigated the different strategies adopted by the world business schools in addressing the criticisms of their stakeholders regarding SDG achievement in their sustainability reports. They used content analysis to analyze the data and highlighted that the business schools are engaged in the social responsibility strategy, giving importance to economic, social, and environmental issues. Kioupi and Voulvoulis [17] assessed the contribution of educational programs of HEIs in achieving the SDGs. They developed a tool on eight sustainable attributes and used it through multi-criteria analysis. The findings show that the HEI programs face drawbacks regarding these eight attributes, and the environmental program is not exceptional. Heleta and Bagus [18] investigate the adoption of SDGs by the HEIs in low-income countries. The study critically evaluated SDG 4 in terms of low-income countries, saying that some targets provide opportunities in higher education to a specific group of people to study in universities of advanced nations. They suggested that the SDGs should prioritize strengthening the local higher educational institutions. Filho et al. [19] examined the introduction of SDGs in the programs offered by the HEIs. They used survey methods to collect the data. They developed a framework for the HEIs to implement SDGs in their programs. This framework, which includes personal, thematic, structural, and institutional aspects, is of significance in introducing SDGs into the programs of HEIs. Chankseliani and McCowan [20] examined the association between higher education and SDGs. This special issue is discussed by incorporating different authors' research on the role of higher educational institutions in achieving the SDGs. They report that the HEIs performed three main functions: education, research, and engagement, before incorporating SDGs. Caputo et al. [21] evaluated sustainability reporting by observing the role played by the HEIs in achieving SDGs using content analysis. They found that the HEIs focused more on social and environmental issues, as disclosed in their reports, and the involvement of their stakeholders was large. Elmassah et al. [22] studied the responsibility of HEIs in achieving Sustainability through a case study analysis in three countries: Egypt, Germany, and Japan. The data was collected through semi-structured interviews, and HEIs' SD framework analysis was used. They reported that the HEIs of Germany and Japan are practicing sustainable development. In contrast, the former is ahead of the latter, while the HEIs of Egypt need to follow both in practicing sustainable development. Ferrer-Estévez and Chalmeta [23] examined the implementation of SDGs in HEIs by evaluating 160 articles published in the past 10 years. The results report recommends six SDG research categories and proposes an efficient framework for implementing SDGs in HEIs. Abad-Segura and Gonzalez-Zamar [24] studied sustainable economic development in HEIs. They conducted a bibliometric analysis and found that most articles published on sustainable development achievement were from the US, UK, and China. The themes studied include environment, education, economy, recycling, and other related topics. Stukalo and Lytvyn [4] identified the quality assurance mechanism of HEIs in achieving the SDGs. The qualitative data were collected through questionnaires and observations. They reported that to ensure quality in HEIs, the SDGs should be incorporated into teaching, learning outcomes, curriculum development, and other relevant areas. This should be done at the program, institutional, and national levels. De Iorio et al. [25] analyzed the elements of SDG disclosure in HEIs at a cross-country level using a regression technique. They found a positive influence of HEIs and the elements of SDG disclosure. Cottafava et al. [26] examined the significance of research in HEIs towards achieving SDGs as a regular contribution to sustainable development using novel multi-step techniques. They employed different methodologies to report the results. They successfully developed an Interdisciplinary Sustainability Index to identify and quantify interdisciplinary SDG research in HEIs. Serafini et al. [27] studied the SDGs in HEIs conceptually by examining the published articles. They have selected 45 articles with cases from Scopus and WoS databases. They identified various studies employing different approaches to address the alignment between HEIs and SDGs. However, there is still no consensus on the proper beginning and end of SDG implementation. Ashida [28] studied the role of HEIs in incorporating SDGs. They reported and suggested forming a society consisting of different stakeholders. Furthermore, stakeholders, particularly researchers, should be educated about SDG 4, which focuses on education and establishing research institutions to achieve the SDGs. Leal Filho et al. [29] examined the engagement of HEIs in incorporating SDGs in developed countries using survey methods. They reported that the HEIs consider incorporating SDGs to be significant. Further, they suggested that HEIs incorporate the SDGs in teaching and the curriculum. Adams et al. [30] examined the effect of sustainable development on education. This can be achieved by mapping the SDGs to the program curriculum through a survey of academic staff dealing with the curriculum. In this regard, they developed SDG keywords to check the coverage level in the program curriculum. Ocaña-Zúñiga et al. [31] examined the role of HEIs in integrating SDGs through research and program curricula, analyzing articles from the Scopus database. They found some concerning results and suggested that the HEIs incorporate the SDGs into research and academic activities as per the SDG guidelines. Gehlot et al. [32] conducted a bibliometric analysis of incorporating SDGs in higher education by reviewing 580 published papers in different journals. They found that Indian educational institutions have adopted the SDGs in research and academics. Still, the adoption rate is very slow, and institutions should be motivated by awareness campaigns to adopt the SDGs. De Villiers et al. [33] studied the components of SDG reporting by the HEIs. This paper intends to present a conceptual framework explaining the association between teaching, research, and service by the HEIs. They reported that SDG reporting enhances the quality of teaching and research, thereby engaging universities with their stakeholders. Handayani et al. [34] examined the integration of SDGs into the HEIs' programs. Hence, they developed instruments to measure it using quantitative research methods. They found a moderate level of implementation of SDGs in the Indonesian HEIs and suggested prospective areas for improvement.

2.2 SDGs in accounting

Bebbington et al. [35] studied the thoughts and approaches of accounting and sustainable development. They intended to encourage accountants on social and environmental issues, scholars of critical accounting, and those who understand sustainable development scholarship. Bebbington and Unerman [36] examined the role of research in accounting in achieving the United Nations SDGs. They reported that accounting research serves as a link between SDGs and accounting specialization. Saliba [1] examined the role played by the accounting profession in achieving the SDGs by collecting data from accounting professionals through qualitative interviews. The study used grounded theory methodology to generate the results. The results report that the accounting professionals in the Malta region are engaged in achieving SDGs through adaptive, conservative, and visionary methods. Bebbington and Unerman [37] investigated the devotion of research in accounting to achieving the UN SDGs. They used the study published in the last five years to address this issue. They found that scholars in accounting are very slow in addressing the SDGs, while the world is on track to achieve them. Frizon and Eugénio [38] examined the recent phenomena of research in SDG incorporation in management and accounting programs of HEIs using bibliometric content analysis. They found that HEIs worldwide engaged in incorporating SDGs in their curriculum, teaching, and learning. Mohammed et al. [39] investigated the association between the level of disclosure of integrated reporting and the salient features of Malaysian Universities using different methods. They found an increasing trend in the integrated reporting level of the Universities. Further, there is a positive relationship between the integrated reporting level and the features of Malaysian Universities. Alakkas et al. [40] studied the role of sustainable accounting as a significant method in incorporating SDGs using a panel data approach. They found that companies consider environmental accounting a key factor in environmental performance. Further, firms with strong environmental performance have higher productivity. Falivena and Gulluscio [41] examined the incorporation of SDGs in accounting programs of Italian HEIs using content analysis. The results indicate that HEIs should better integrate SDGs into their accounting programs and other courses. Al-Hazaima et al. [8] studied the implementation of SDGs into accounting programs and the role of stakeholders in this regard in Jordanian Universities using semi-structured interviews. They report that the implementation of SDGs into accounting is significant, but stakeholders are unable to incorporate them due to their role in decision-making. Therefore, the stakeholders would like to be provided with the government's decision-making power to integrate SDGs into the educational courses of HEIs.

2.3 SDGs and student perception

Seva-Larrosa et al. [12] studied the perception of students regarding SDGs and the benefits the companies derive from their implementation on a sample of 178 students at the University of Spain using a structured questionnaire. They employed the PLS method to analyze the data. They found that university students assume that companies' commitment to SDGs is a significant component. Cachero et al. [42] explored the changing perceptions in terms of SDGs among the university students in Spain. They aligned 17 SDGs with different academic disciplines. They found that the grasp of SDGs by the students is low; however, the students of Social-Legal sciences assume the impact of SDGs is moderate to high on their lives. Abowardah et al. [43] examined the students' perception in HEIs of Saudi Arabia through an online survey. They reported that the students associate SDGs with the environment and have no knowledge about other aspects of SDGs, such as poverty, gender equality, quality education, etc. Novieastari et al. [44] studied the understanding and perception of SDGs among the students from different disciplines of a public university in Indonesia. They found that 77 percent of students know the SDGs, and 74 percent of the students have a positive perception towards the SDGs, while 42 percent of the students are unaware of the SDGs.

2.4 Research gap

The objective of education for sustainable development is to integrate sustainability concerns into teaching and learning, thereby enabling HEIs to advance the SDGs. Among these, the provision of quality education remains a critical goal, particularly for developing countries. Within the accounting literature, scholars have examined how faculty influence students’ perspectives to prepare them for meaningful contributions toward the SDGs. The present study reviews prior literature on the association of SDGs with HEIs, accounting, and students’ perceptions regarding their adoption in higher education. Findings indicate that the integration of SDGs within HEIs is still at a nascent stage: while some institutions recognize their importance, others remain uncertain about embedding them into teaching and learning. Moreover, there is no clear consensus on the appropriate framework for initiating and completing SDG implementation. In accounting education, research reveals a slow pace of adoption. Although integrated reporting is increasingly practiced, and environmental accounting has emerged as a significant measure of environmental performance, overall engagement with SDGs in the accounting field remains limited. Similarly, studies exploring students’ perceptions of SDG adoption in higher education show inconsistent trends.

In summary, this review identifies a significant gap in examining the incorporation of SDGs into higher education curricula, particularly within accounting education. Notably, research addressing this issue in the context of Saudi Arabia is scarce, with no prior studies specifically investigating the integration of SDGs into accounting curricula.

2.5 Hypotheses

The following are the hypotheses formulated to examine the incorporation of SDGs into the accounting curriculum.

H1: Students' perception and willingness to integrate SDG 4 into the accounting curriculum are positive.

H2: Students' perception and willingness to integrate SDG 8 into the accounting curriculum are positive.

The current study examines the perception of students majoring in accounting specialization regarding integrating SDGs into the accounting curriculum of Saudi Arabian Universities. The study uses quantitative research for analysis. In this regard, a structured questionnaire was designed in Google Forms, consisting of demographic profile questions, student willingness to incorporate SDGs into the accounting curriculum, student perception of SDGs, quality education (SDG 4), and economic growth and productive employment (SDG 8). The questions of student willingness and perception are structured based on a five-point Likert scale, while the questions of SDG 4 and SDG 8 are structured based on different sustainable concepts, ranging from 1 to 5.

The study population was Saudi Arabian universities, and the sample consisted of students at different levels of the accounting program at Prince Sattam bin Abdulaziz University. A stratified random sampling method was employed to construct the sample, dividing the students based on their year. A pilot study was conducted after the design of a structured questionnaire in October 2024. Later, the questionnaire was sent to more than 300 students during October and December 2024, of which 91 responses were received. There were no missing data or data errors. Hence, the final study sample was equal to the responses received, i.e., 91.

Table 1. Factors with their reliability values

|

Factor/Variable |

Reliability Value Cronbach Alpha/Mean Inter-Item Correlation |

|

Quality Education (SDG 4) |

0.16 |

|

Productive Employment (SDG 8) |

0.64 |

|

Student Willingness |

0.86 |

|

Student Perception |

0.15 |

Nevertheless, the sample size is small; it reflects the characteristics of the study population, i.e., it is representative of the students of the accounting program in different Saudi Arabian Universities. The study constructed variables of student willingness, student perception, SDG 4, and SDG 8 based on reliability measurement. Reliability was measured using Cronbach's Alpha and Mean Inter-item Correlation (for the variables of Cronbach's Alpha less than 0.60). The study considered those variables whose Cronbach's Alpha is more than or equal to 0.60 [45, 46] or Mean Inter-item Correlation of more than or equal to 0.15 [47]. Table 1 displays the factors (variables) with their reliability values.

The study has chosen accounting courses that are significant in incorporating sustainability concepts, such as Intermediate Accounting, Managerial Accounting, Advanced Accounting, and Auditing. These courses will be ranked from 1 (highest percentage) to 5 (lowest percentage) based on the rate of responses received. The data collected shall be analyzed using descriptive statistics, correlation analysis, and simple regression.

Table 2 displays the dependent and independent variables to estimate the simple regression.

Table 2. Dependent and independent variables

|

Factor/Variable |

Dependent/Independent Variable |

|

Quality Education (SDG 4) |

Dependent Variable |

|

Productive Employment (SDG 8) |

Dependent Variable |

|

Student Willingness |

Independent Variable |

|

Student Perception |

Independent Variable |

The current study estimates two models using simple regression. In one model, SDG 4 (quality education) and SDG 8 (economic growth and productive employment) are alternatively dependent variables, while student willingness and perception are the independent variables. The study is primarily interested in examining the impact of student willingness and student perception on SDG 4 and SDG 8; therefore, it excluded control variables.

$\mathrm{QE}=\alpha+\beta_1 \mathrm{Wlg}+\beta_2$ Perc $+\varepsilon$ (1)

$\mathrm{PE}=\alpha_0+\beta_1 \mathrm{Wlg}+\beta_2$ Perc $+\varepsilon$ (2)

where, QE = Quality Education (SDG 4); PE = Economic Growth and Productive Employment (SDG 8); Wlg = Student Willingness; Perc = Student Perception; $\varepsilon$ = error term.

The collinearity between the variables shall be examined using the Durbin-Watson test statistics and the Variance Inflation Factor (VIF). Further, the goodness of fit of these two models shall be explained using the Adjusted R2 and the F-statistic.

The current study examined the integration of SDGs into the accounting curriculum of Saudi Arabian Universities. Initially, the study presents demographic profile results, such as gender, age, and year of study, followed by the ranking of accounting courses that require sustainability concepts, the alignment of sustainability concepts to different accounting courses, and, ultimately, the results of simple regression.

4.1 Demographic profile results

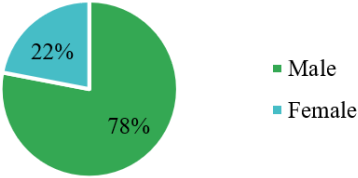

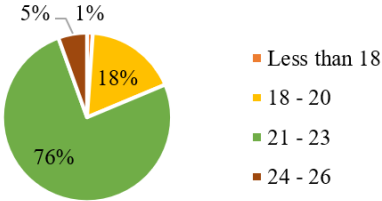

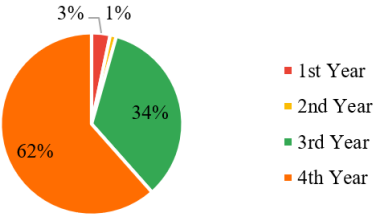

The study presents the results of the demographic profile of respondents (i.e., the students) in terms of age, gender, and year in which they are currently studying. The demographic profile indicates that 78% of the students were male, 22% were female, and the majority were between 21 and 23 years old, accounting for 76%. The study shows that 62% of male and female students are in the fourth year, 34% are in the third year, and the remaining are in the first and second years. This has been shown in Figures 1-3.

Figure 1. Gender of respondents

Figure 2. Age of respondents

Figure 3. Study level

4.2 Ranking of accounting courses based on sustainability concepts

The accounting courses of the accounting program offered at Prince Sattam bin Abdulaziz University were ranked by the students studying at different levels based on sustainability concepts. Table 3 shows the ranking of accounting courses. Students assume Managerial Accounting is the best course to include sustainability concepts, followed by Intermediate Accounting, Advanced Accounting, and Auditing. Besides, 46.2% of students consider including sustainability concepts in all the accounting courses.

Table 3. Ranking of accounting courses based on sustainability concepts

|

Accounting Course |

Student Assumption on Suitability to Include Sustainability (in %) |

Ranking |

|

Intermediate Accounting |

16.5% |

2 |

|

Managerial Accounting |

20.9% |

1 |

|

Advanced Accounting |

8.8% |

3 |

|

Auditing |

7.7% |

4 |

|

All the above courses |

46.2% |

No rank |

4.3 Alignment of accounting courses to different sustainability concepts

Table 4 shows the alignment of some important sustainability concepts to the accounting courses of the accounting program of Prince Sattam bin Abdulaziz University. The concepts such as sustainability development, IASB and SASB guidelines on sustainability reporting, and ESG reporting are aligned with Intermediate Accounting. It will be significant to incorporate these concepts into the syllabus of Intermediate Accounting. Furthermore, incorporating the concepts of SDGs into financial reporting, the integrated reporting framework and its application, and non-financial reporting practices will be significant in the Advanced Accounting and Auditing syllabus. Furthermore, incorporating the concepts of Environmental Management Accounting, SDGs under management accounting, SRI, SROI, SBS, and Sustainable Management Accounting into the Management Accounting syllabus in Saudi Arabia will be significant.

Table 4. Sustainability concepts and accounting courses alignment

|

S. No. |

Sustainability Concepts |

Managerial Accounting |

Intermediate Accounting |

Advanced Accounting |

Auditing |

|

1. |

Sustainable Development |

|

√ |

|

√ |

|

2. |

Sustainability Reporting & IASB Guidelines |

|

√ |

|

|

|

3. |

Sustainability Reporting & SASB Guidelines |

|

√ |

|

|

|

4. |

ESG Reporting |

|

√ |

|

√ |

|

5. |

SDGs on Financial Reporting |

|

|

√ |

√ |

|

6. |

Integrated Reporting Framework (IRF) |

|

|

√ |

√ |

|

7. |

Application of IRF in Saudi Arabia |

|

|

√ |

√ |

|

8. |

Non-financial Reporting Practices |

|

|

√ |

√ |

|

9. |

Environmental Management Accounting |

√ |

|

|

√ |

|

10. |

SDGs under Management Accounting |

√ |

|

|

|

|

11. |

SRI, SROI, and SBS |

√ |

|

|

√ |

|

12. |

Sustainable Management Accounting in SA |

√ |

|

|

4.4 Empirical results

The current study employed a simple regression analysis to assess the integration of SDGs, such as SDG 4 (quality education) and SDG 8 (economic growth and productive employment), into the accounting program's curriculum. Two models were estimated alternatively: Quality Education (SDG 4) and Economic Growth and Productive Employment (SDG 8) were dependent variables, and student willingness and perception were independent variables. Table 5 reports the results of the simple regression.

Table 5. Results of simple regression

|

Model 1: Quality Education (DV) |

|||||

|

|

α |

β |

t-value |

p-value |

VIF |

|

Constant |

0.332 |

|

|

|

|

|

Wlg |

|

0.193 |

2.162 |

0.033 |

1.521 |

|

Perc |

|

0.570 |

3.679 |

0.000 |

1.521 |

|

Adjusted R2 |

0.312 |

|

|

|

|

|

F-statistic |

20.92 (0.000) |

|

|

|

|

|

Model 2: Economic Growth and Productive Employment (DV) |

|||||

|

Constant |

0.631 |

|

|

|

|

|

Wlg |

|

0.404 |

3.033 |

0.003 |

1.521 |

|

Perc |

|

0.635 |

2.749 |

0.007 |

1.521 |

|

Adjusted R2 |

0.32 |

|

|

|

|

|

F-statistic |

20.16 (0.000) |

|

|

|

|

The Model 1 results of simple regression show that the independent variable Wlg (student willingness), with a coefficient of 0.193, is positive and significant with a p-value of 0.03, which is less than a 5 percent level of significance. This indicates that the students are demonstrating a willingness to integrate sustainability concepts into the accounting curriculum. Further, the variable Perc (student perception) with a coefficient of 0.570 is positive and significant with a p-value of 0.000 which is less than 1 percent level of significance. The positive effect of student perception implies that the students perceive the incorporation of SDGs into the accounting curriculum positively, which might lead to their enhanced engagement with SDGs and better academic performance. The Variance Inflation Factor (VIF) of 1.521 shows no multicollinearity between the variables. The fitness of Model 1 is good, with an adjusted R2 of 31.2 percent and having an F-statistic significance at less than a 1 percent significance level.

Similarly, the Model 2 results of simple regression show that the independent variable Wlg (student willingness), with a coefficient of 0.404, is positive and significant with a p-value of 0.003, which is less than 1 percent significance. Further, the variable Perc (student perception) with a coefficient of 0.635 is positive and significant with a p-value of 0.007, which is less than a 1 percent level of significance. The Variance Inflation Factor (VIF) of 1.521 shows no multicollinearity between the variables. The fitness of Model 1 is good, with an adjusted R2 of 32 percent and having an F-statistic significance at less than a 1 percent significance level.

The results of models 1 and 2 indicate that as student willingness increases, the quality of education is also likely to improve. As the student perception becomes more favorable, the perceived quality of education tends to increase significantly.

The current study, which examines the integration of sustainability concepts into the curriculum of accounting departments in Saudi Arabian universities, particularly at Prince Sattam bin Abdulaziz University, yielded interesting results. The results are presented using qualitative methods, such as demographic results, student perception measurement through ranking of courses, accounting courses alignment with sustainability concepts, and quantitative methods, such as the results from estimating a simple regression. Initially, the qualitative results show that 95.6 percent of students were studying in levels 5 and 6 (third year) and 7 and 8 (fourth year), where the core accounting courses were taught. Furthermore, the results of students' perception of including sustainability concepts in the accounting courses, based on ranking, show that sustainability concepts should be included in all the accounting courses selected by the study (46.2 percent). Besides, the students assume managerial accounting courses (20.9 percent) are significant in including sustainability concepts, followed by Intermediate Accounting (16.5 percent), advanced accounting (8.8 percent), and Auditing (7.7 percent). The significance of managerial accounting for sustainability can be attributed to the importance of sustainability concepts within this field, including Environmental Management Accounting (EMA), Socially Responsible Investing (SRI), Social Return on Investment (SROI), Sustainability Balanced Scorecard (SBS), and the SDGs, all of which fall under management accounting. The alignment of sustainability concepts with accounting courses demonstrates that courses such as Intermediate Accounting and Advanced Accounting necessitate the integration of sustainable development & reporting principles, adhering to IASB and SASB guidelines, ESG reporting, the SDGs in financial reporting, and the application of the Integrated Reporting Framework, including the reporting of non-financial practices. The current syllabus of these two courses consists of topics related to financial reporting with only IASB guidelines.

The above topics are significant in aligning sustainable development and reporting with these two courses. The reason is that corporate companies must provide disclosures related to sustainable reporting. Moreover, sustainable concepts such as Environmental Management Accounting (EMA), SRI, SROI, SBS, and SDGs in management accounting are more significant to be included in the managerial accounting syllabus. The social and environmental concerns are crucial in managerial decision-making, specifically regarding reporting climate change and energy. Therefore, it is essential to address the issues of affordable and clean energy (SDG 7) and climate action (SDG 13). Integrating sustainability concepts into managerial accounting brings efficiency in managing environmental effects and complying with environmental regulations, which in turn increases environmental performance [48].

Furthermore, integrating sustainability development with Auditing provides more insights because there is a strong association between accounting, audit professionals, and accounting standards regulatory boards. This association and the integration of sustainable development might establish the best financial standards for the corporate sector [49]. The empirical results show that accounting program students are interested in integrating the accounting courses and Sustainability, and they have a positive perception regarding incorporating SDGs into the accounting curriculum. The quantitative results are from past studies [4, 6, 8, 11, 12] where students pursuing undergraduate and graduate programs specifically in accounting assume that the incorporation of SDG components into the study curriculum will be beneficial. Further, incorporating SDG components will boost the knowledge and skills required for corporate accountability.

Two program learning outcomes of the accounting program at Prince Sattam bin Abdulaziz University contribute to SDGs indirectly, such as “Demonstrating competency in other accounting areas of accounting information systems, specialized firms, government accounting, forensic accounting, governance, and sustainability” and “Recognize ethical issues appropriate to finding constructive solutions to issues related to individuals, accounting professionals and society." There is a need to incorporate sustainability concepts into the accounting curriculum since these concepts strengthen the program's learning outcomes. Therefore, the following SDGs should be incorporated into the accounting curriculum at the earliest.

SDG 4 - Quality education:

Prince Sattam bin Abdulaziz University's accounting program aims to provide rational and quality education to all, while offering career-long job opportunities to students by incorporating sustainability concepts into the accounting curriculum. The current accounting program plans to achieve SDGs through Target 4.7, which explains that 'by 2030, all learners will acquire the knowledge and skills needed to promote sustainable development'. The courses (1-8) presented in Table 4 suit the above target. By incorporating sustainability concepts into the content of these courses, students can learn these concepts through various learning approaches. The incorporation of the SDG 4 target into the accounting curriculum was reported by Cooray et al. [50].

SDG 8 - Promote decent work and economic growth:

Prince Sattam bin Abdulaziz University's accounting program aims to equip students with the necessary accounting knowledge and skills to secure productive employment in the Saudi labor market. The current accounting program attempts to achieve Targets 8.3 and 8.5 under SDG 8, where Target 8.3 says to 'Promote development-oriented policies that support productive activities, decent job creation, entrepreneurship, creativity, and innovation, and encourage the formalization and growth of micro, small- and medium-sized enterprises, including through access to financial services' and Target 8.5 says that 'by 2030, achieve full and productive employment and decent work for all women and men, including for young people and persons with disabilities, and equal pay for work of equal value'. In the context of these two targets, the accounting program offers an eight-week internship program designed to train students in various accounting areas, thereby helping them secure professional employment. Moreover, the program plans to incorporate concepts of the above-mentioned targets of SDG 8 into the curriculum. The incorporation of SDG 8 target into the accounting curriculum was reported by Cooray et al. [50].

The incorporation of different SDGs based on their targets into the accounting curriculum was reported by past studies [9, 10, 40, 41]. Therefore, the current study assumes the incorporation of SDGs to be more significant in the accounting curriculum of Prince Sattam bin Abdulaziz University, supporting both the hypotheses (H1 and H2) where the perception and willingness of students to the integration of SDG 4 and SDG 8 into the accounting curriculum is positive.

Sustainable development has attracted significant attention from various crucial factors, and education is among the most important. The UNECE on Education for Sustainable Development strategy presents education as an essential tool for attaining sustainable development. Therefore, HEIs, including universities, should recommend the SDGs by utilizing diverse teaching and learning methods and integrating them into the curriculum, providing quality education, and helping promote employment and growth. To achieve this, the current study examined the incorporation of sustainability development concepts into Saudi Arabian Universities' accounting curriculum, particularly emphasizing the accounting program at Prince Sattam bin Abdulaziz University. The study population was Saudi Arabian universities, and the sample consisted of students at different levels of accounting programs at Prince Sattam bin Abdulaziz University. The study used quantitative research for analysis. A structured questionnaire was designed in Google Forms, which consisted of questions on demography, ensuring quality education (SDG 4), and promoting economic growth and development (SDG 8). The final study sample consisted of 91 responses. Reliability was measured using Cronbach's Alpha and Mean Inter-item Correlation (for the variables of Cronbach's Alpha less than 0.60). Further, the study estimated two models using simple regression where SDG 4 (quality education) and SDG 8 (productive employment) were employed as dependent variables alternatively.

In contrast, student willingness and student perception were employed as independent variables. The study's findings show that students support the integration of sustainability concepts across all accounting courses analyzed—namely, Intermediate Accounting, Managerial Accounting, Advanced Accounting, and Auditing—with a stronger emphasis on Managerial Accounting. Additionally, the empirical evidence highlights students’ interest in linking accounting education with Sustainability and their favorable perception of embedding the SDGs into the curriculum. Considering the quantitative results, the study recommends incorporating SDG 4 and SDG 8 into the accounting curriculum at Prince Sattam bin Abdulaziz University. The results reported by the current study highlight the growing importance of integrating Sustainability into accounting education. Moreover, students' positive perceptions and willingness suggest that incorporating SDG 4 (Quality Education) and SDG 8 (Decent Work and Economic Growth) can enhance curriculum efficiency and support national development goals such as Vision 2030.

6.1 Practical implications

The results of the current study are helpful for curriculum development, where sustainability concepts can be embedded across core accounting courses, making the curriculum more relevant and aligned with national and global development. Further, linking accounting education with sustainability might enhance student skills in terms of employability in the areas of sustainability reporting, ESG analysis, and sustainable business practices. Moreover, aligning accounting education with sustainability might strengthen the institution's role in achieving the national development priorities, such as Vision 2030. Further, these findings can guide universities in revising their accounting programs to align with global sustainability standards, promote interdisciplinary learning, and prepare students for responsible professional roles.

6.2 Scope for future research

This study opens several directions for future research. Expanding the current analysis to other universities across Saudi Arabia and the GCC can offer interesting results. Moreover, including faculty perspectives would provide a more comprehensive view of curriculum integration. Further, studies may also explore the long-term impact of sustainability education on students' career outcomes and professional practices. Furthermore, integrating other SDGs and developing innovative teaching methods can further enhance the effectiveness of Sustainability in accounting education.

This project is sponsored by Prince Sattam bin Abdulaziz University (PSAU) as part of funding for its SDG Roadmap Research Funding Program Project number PSAU/2023/SDG/58.

[1] Saliba, D.T. (2019). Achieving sustainable development goals: The role of the accountancy profession in Malta. MCAST Journal of Applied Research and Practice, 3(2): 90-116. https://doi.org/10.5604/01.3001.0014.4391

[2] Fleacă, E., Fleacă, B., Maiduc, S. (2018). Aligning strategy with sustainable development goals (SDGs): Process scoping diagram for entrepreneurial higher education institutions (HEIs). Sustainability, 10(4): 1032. https://doi.org/10.20944/preprints201801.0140.v1

[3] Crespo, B., Míguez-Álvarez, C., Arce, M.E., Cuevas, M., Míguez, J.L. (2017). The sustainable development goals: An experience on higher education. Sustainability, 9(8): 1353. https://doi.org/10.3390/su9081353

[4] Stukalo, N., Lytvyn, M. (2021). Towards sustainable development through higher education quality assurance. Education Sciences, 11(11): 664. https://doi.org/10.3390/educsci11110664

[5] Sachs, J., Schmidt-Traub, G., Kroll, C., Durand-Delacre, D., Teksoz, K. (2017). SDG index and dashboards report 2017. New York: Bertelsmann Stiftung and Sustainable Development Solutions Network (SDSN). https://sdgtransformationcenter.org/reports/sdg-index-2017.

[6] Leal Filho, W., Shiel, C., Paço, A., Mifsud, M., Ávila, L.V., et al. (2019). Sustainable development goals and sustainability teaching at universities: Falling behind or getting ahead of the pack? Journal of Cleaner Production, 232: 285-294. https://doi.org/10.1016/j.jclepro.2019.05.309

[7] Gunawan, J., Permatasari, P., Tilt, C. (2020). Sustainable development goal disclosures: Do they support responsible consumption and production? Journal of Cleaner Production, 246: 118989. https://doi.org/10.1016/j.jclepro.2019.118989

[8] Al-Hazaima, H., Low, M., Sharma, U. (2024). The integration of education for sustainable development into accounting education: Stakeholders’ salience perspectives. Journal of Public Budgeting, Accounting and Financial Management, 37(2): 296-328. https://doi.org/10.1108/jpbafm-06-2023-0105

[9] Pitt-Watson, D. (2021). Why accounting really matters for climate change, and what you need to know about it. Responsible Investor. https://www.responsible-investor.com/why-accounting-really-matters-for-climate-change-and-what-you-need-to-know-about-it/, accessed on Mar. 22, 2025.

[10] Pincus, K.V., Stout, D.E., Sorensen, J.E., Stocks, K.D., Lawson, R.A. (2017). Forces for change in higher education and implications for the accounting academy. Journal of Accounting Education, 40: 1-18. https://doi.org/10.1016/j.jaccedu.2017.06.001

[11] Cho, C., Mäkelä, H. (2019). Can accountants save the world? Incorporating sustainability in accounting courses and curricula. European Accounting Association’s (EAA) Accounting Research Center, Brussels, Belgium.

[12] Seva-Larrosa, P., Marco-Lajara, B., Úbeda-García, M., Zaragoza-Sáez, P., et al. (2023). Students' perception of sustainable development goals (SDGs) and the benefits for companies derived from their implementation. Economic Research-Ekonomska Istraživanja, 36(1): 2167100. https://doi.org/10.1080/1331677x.2023.2167100

[13] Albareda-Tiana, S., Vidal-Raméntol, S., Fernández-Morilla, M. (2018). Implementing the Sustainable Development Goals at university level. International Journal of Sustainability in Higher Education, 19(3): 473-497. https://doi.org/10.1108/ijshe-05-2017-006

[14] Franco, I., Saito, O., Vaughter, P., Whereat, J., Kanie, N., Takemoto, K. (2019). Higher education for sustainable development: Actioning the global goals in policy, curriculum and practice. Sustainability Science, 14(6): 1621-1642. https://doi.org/10.1007/s11625-018-0628-4

[15] Argento, D., Einarson, D., Mårtensson, L., Persson, C., Wendin, K., Westergren, A. (2020). Integrating sustainability in higher education: A Swedish case. International Journal of Sustainability in Higher Education, 21(6): 1131-1150. https://doi.org/10.1108/ijshe-10-2019-0292

[16] Miotto, G., Blanco-González, A., Díez-Martín, F. (2020). Top business schools legitimacy quest through the sustainable development goals. Heliyon, 6(11): e05395. https://doi.org/10.1016/j.heliyon.2020.e05395

[17] Kioupi, V., Voulvoulis, N. (2020). Sustainable development goals (SDGs): Assessing the contribution of higher education programmes. Sustainability, 12(17): 6701. https://doi.org/10.3390/su12176701

[18] Heleta, S., Bagus, T. (2021). Sustainable development goals and higher education: Leaving many behind. Higher Education, 81(1): 163-177. https://doi.org/10.1007/s10734-020-00573-8

[19] Filho, W.L., Frankenberger, F., Salvia, A.L., Azeiteiro, U., et al. (2021). A framework for the implementation of the Sustainable Development Goals in university programmes. Journal of Cleaner Production, 299: 126915. https://doi.org/10.1016/j.jclepro.2021.126915

[20] Chankseliani, M., McCowan, T. (2021). Higher education and the Sustainable Development Goals. Higher Education, 81(1): 1-8. https://doi.org/10.1007/s10734-020-00652-w

[21] Caputo, F., Ligorio, L., Pizzi, S. (2021). The contribution of higher education institutions to the SDGs—An evaluation of sustainability reporting practices. Administrative Sciences, 11(3): 97. https://doi.org/10.3390/admsci11030097

[22] Elmassah, S., Biltagy, M., Gamal, D. (2022). Framing the role of higher education in sustainable development: A case study analysis. International Journal of Sustainability in Higher Education, 23(2): 320-355. https://doi.org/10.1108/ijshe-05-2020-0164

[23] Ferrer-Estévez, M., Chalmeta, R. (2021). Integrating sustainable development goals in educational institutions. The International Journal of Management Education, 19(2): 100494. https://doi.org/10.1016/j.ijme.2021.100494

[24] Abad-Segura, E., González-Zamar, M.D. (2021). Sustainable economic development in higher education institutions: A global analysis within the SDGs framework. Journal of Cleaner Production, 294: 126133. https://doi.org/10.1016/j.jclepro.2021.126133

[25] De Iorio, S., Zampone, G., Piccolo, A. (2022). Determinant factors of SDG disclosure in the university context. Administrative Sciences, 12(1): 21. https://doi.org/10.3390/admsci12010021

[26] Cottafava, D., Ascione, G.S., Corazza, L., Dhir, A. (2022). Sustainable development goals research in higher education institutions: An interdisciplinarity assessment through an entropy-based indicator. Journal of Business Research, 151: 138-155. https://doi.org/10.1016/j.jbusres.2022.06.050

[27] Serafini, P.G., de Moura, J.M., de Almeida, M.R., de Rezende, J.F.D. (2022). Sustainable development goals in higher education institutions: A systematic literature review. Journal of Cleaner Production, 370: 133473. https://doi.org/10.5296/jet.v10i1.20227

[28] Ashida, A. (2022). The role of higher education in achieving the Sustainable Development Goals. In Sustainable Development Disciplines for Humanity: Breaking Down the 5Ps—People, Planet, Prosperity, Peace, and Partnerships, pp. 71-84. https://doi.org/10.1007/978-981-19-4859-6_5

[29] Leal Filho, W., Salvia, A.L., Eustachio, J.H.P.P. (2023). An overview of the engagement of higher education institutions in the implementation of the UN Sustainable Development Goals. Journal of Cleaner Production, 386: 135694. https://doi.org/10.1016/j.jclepro.2022.135694

[30] Adams, T., Jameel, S.M., Goggins, J. (2023). Education for sustainable development: Mapping the SDGs to university curricula. Sustainability, 15(10): 8340. https://doi.org/10.3390/su15108340

[31] Ocaña-Zúñiga, C.L., Tineo, M., Fernandez-Zarate, F.H., Quiñones-Huatangari, L., Huaccha-Castillo, A.E., Morales-Rojas, E., Miguel-Miguel, H.W. (2023). Implementing the Sustainable Development Goals in university higher education: A systematic review. International Journal of Sustainable Development and Planning, 18(6): 1769-1776. https://doi.org/10.18280/ijsdp.180612

[32] Gehlot, V., Kaur, M., Kaushik, M.B., Rajharia, P., Chandrawat, P. (2024). Bibliometric analysis of sustainable development goals (SDGs) research in India: Trends, contribution, and impact. International Journal of Sustainable Development and Planning, 19(5): 1747-1754. https://doi.org/10.18280/ijsdp.190512

[33] De Villiers, C., Dimes, R., Molinari, M. (2024). Determinants, mechanisms and consequences of UN SDGs reporting by universities: Conceptual framework and avenues for future research. Journal of Public Budgeting, Accounting and Financial Management. https://doi.org/10.1108/jpbafm-07-2023-0125

[34] Handayani, E., Anggara, A.A., Hapsari, I. (2024). Developing an instrument and assessing SDGs implementation in Indonesian higher education. International Journal of Sustainable Development and Planning, 19(2): 577-590. https://doi.org/10.18280/ijsdp.190215

[35] Bebbington, J., Russell, S., Thomson, I. (2017). Accounting and sustainable development: Reflections and propositions. Critical Perspectives on Accounting, 48: 21-34. https://doi.org/10.1016/j.cpa.2017.06.002

[36] Bebbington, J., Unerman, J. (2018). Achieving the United Nations sustainable development goals: An enabling role for accounting research. Accounting, Auditing and Accountability Journal, 31(1): 2-24. https://doi.org/10.1108/aaaj-05-2017-2929

[37] Bebbington, J., Unerman, J. (2020). Advancing research into accounting and the UN Sustainable Development Goals. Accounting, Auditing and Accountability Journal, 33(7): 1657-1670. https://doi.org/10.1108/aaaj-05-2020-4556

[38] Frizon, J.A., Eugénio, T. (2022). Recent developments on research in sustainability in higher education management and accounting areas. The International Journal of Management Education, 20(3): 100709. https://doi.org/10.1016/j.ijme.2022.100709

[39] Mohammed, N.F., Mahmud, R., Islam, M.S., Mohamed, N. (2022). Towards achieving SDGs through integrated reporting in Malaysian public universities. International Journal of Sustainability in Higher Education, 24(5): 1002-1023. https://doi.org/10.1108/ijshe-08-2021-0344

[40] Alakkas, A.A., Shabir, S., Alhumoudi, H., Boukhris, M., Baig, A., Khan, I.A. (2023). The impact of sustainability accounting on environmental performance and productivity: A panel data analysis. International Journal of Sustainable Development and Planning, 18(8): 2431-2441. https://doi.org/10.18280/ijsdp.180814

[41] Falivena, C., Gulluscio, C. (2023). Integrating SDGs in accounting education: Evidence from Italian universities. The Elgar Companion to Corporate Social Responsibility and the Sustainable Development Goals, pp. 68-84. https://doi.org/10.4337/9781803927367.00013

[42] Cachero, C., Grao-Gil, O., Pérez-delHoyo, R., Ordóñez-García, M.C., Andújar-Montoya, M.D., Lillo-Ródenas, M.Á., Torres, R. (2023). Perception of the sustainable development goals among university students: A multidisciplinary perspective. Journal of Cleaner Production, 429: 139682 https://doi.org/10.1016/j.jclepro.2023.139682

[43] Abowardah, E.S., Labib, W., Aboelnagah, H., Nurunnabi, M. (2024). Students’ perception of sustainable development in higher education in Saudi Arabia. Sustainability, 16(4): 1483. https://doi.org/10.3390/su16041483

[44] Novieastari, E., Pujasari, H., Abdul Rahman, L.O., Ganefianty, A., Rerung, M.P. (2022). Knowledge, perception, and awareness about sustainable development goals (SDGs) among students of a public university in Indonesia. International Journal of Health Promotion and Education, 60(4): 195-203. https://doi.org/10.1080/14635240.2022.2066557

[45] Hinton, P.R. (2014). Statistics Explained (3rd ed.). Routledge. https://doi.org/10.4324/9781315797564

[46] Kuehl, C., Sparks, A.C., Hodges, H., Smith, E.R. (2023). Exploring sustainability literacy: Developing and assessing a bottom-up measure of what students know about sustainability. Frontiers in Sustainability, 4: 1167041. https://doi.org/10.3389/frsus.2023.1167041

[47] Clark, L.A., and Watson, D. (1995). Constructing validity: Basic issues in objective scale development. Sustainability, 7(3): 309-319. https://doi.org/10.1037//1040-3590.7.3.309

[48] Johri, A., Singh, R.K., Alhumoudi, H., Alakkas, A. (2024). Examining the influence of sustainable management accounting on sustainable corporate governance: Empirical evidence. Sustainability, 16(21): 9605. https://doi.org/10.3390/su16219605

[49] Petricică, A.E., Buboi, A. (2024). The Journey to a Sustainable Economy. Accounting and Auditing for Long-Term Performance. Annals of Dunarea de Jos University of Galati Fascicle I Economics and Applied Informatics, 30(1): 156-165. https://doi.org/10.35219/eai15840409402

[50] Cooray, T., Senaratne, S., Gunarathne, N. (2022). Engagement with sustainable development goals in accounting education: The case of a public university in Sri Lanka. In Engagement with Sustainable Development in Higher Education: Universities as Transformative Spaces for Sustainable Futures, pp. 19-37. https://doi.org/10.1007/978-3-031-07191-1_2