Iwan Purwanto*![]() | Rizal Isnanto

| Rizal Isnanto![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study presents the development of a fuzzy rule-based system leveraging California Psychological Inventory (CPI) values as input variables to provide loan percentage recommendations. By analyzing data to determine the weights of relevant input variables, the findings reveal that significant weights were assigned to Control (0.498), Ego Strength (0.315), Social Presence (0.288), Warmth (0.187), Self-Acceptance (0.278), Empathy (0.572), Achievement via Conformance (0.524), Responsibility (0.374), Flexibility (0.085), and Realistic (0.072). The implementation of these weights allowed for the creation of 1,024 fuzzy rule bases using the IF-Then function. The analysis illustrates that applying CPI in loan amount recommendations can reduce losses from bad loans by up to 20%. The research emphasizes the importance of integrating psychometric assessments into credit evaluations, leading to improved decision-making for potential debtors and enhanced financial stability within the online lending sector. Furthermore, the findings provide a structured framework for future research, which should include additional variables to refine the assessment of loan suitability for borrowers.

fuzzy rule-based system, California Psychological Inventory (CPI), loan percentage recommendations, psychometric assessments, online lending sector

Online lending is a technology-based financial service in Indonesia that connects lenders and borrowers through online platforms. Despite its growth, regulations governing online lending remain limited. The credit agreement mechanisms adhere to the Financial Services Authority (OJK) Regulation No. 77/POJK.01/2016 [1]. Lenders on these platforms often face challenges in securing optimal loans due to a tendency to prioritize loan quantity over quality [2]. Furthermore, online lending has been shown to positively influence bank credit for non-MSMEs in regions with loose bank liquidity [2, 3].

The amount of loans, loan periods, and borrowers' loan history significantly impact financing decisions within online lending systems [4]. This sector can either replace or complement traditional bank lending in rural areas based on partnerships between rural banking associations and FinTech companies [3]. Access to financial institutions and ownership of savings accounts are crucial for promoting formal credit while reducing reliance on informal lending practices in Indonesia [5, 6].

However, the industry faces significant challenges related to high levels of non-performing loans (NPLs), which threaten stability among online lending players. In February 2024, the OJK reported an increase in unpaid loans across online lending platforms; NPLs rose to 3.36% as measured by the Total Write Off Percentage (TWP) [7, 8], with aggregate risk levels increasing by 28.11%, equivalent to IDR 51.46 trillion compared to January data [6].

A comprehensive user profile model for online lending can be developed by integrating data from various sources including basic attributes, abilities, social factors, and psychological characteristics of borrowers [9, 10]. Success criteria for these platforms are influenced by offer records that help reduce information asymmetry and improve loan approval rates [10, 11]. Additionally, user interface design plays a critical role in attracting users while influencing lender trust and borrowing intentions within online applications [12].

Alternative credit scoring models can be implemented using personality types inferred from borrowers' job categories through methods like the Myers-Briggs Type Indicator (MBTI) [13]. The application of fuzzy logic alongside multi-criteria decision-making methods significantly aids in assessing personal default risks on online lending platforms while considering lenders' psychological traits as well as borrower characteristics [14].

Defaults often arise from both internal factors-such as overly broad credit policies or ineffective assessment systems-and external factors like borrowers failing to meet agreed-upon arrangements due either to specific intentions or uncontrollable circumstances [7]. For instance, February 2023 saw defaults among legal online lending services resulting in totally losses IDR 975 million without corrective measures leading potentially further losses due to unreturned funds.

To mitigate these issues-particularly defaults-the California Psychological Inventory (CPI) presents a promising solution through psychometric evaluations aimed at reducing payment failure risks among borrowers [14]. Utilizing CPI allows for predictive identification of potential payment failures based on personality assessments which enhances borrower selection processes focused on reliability.

In terms of operational procedures within online lending applications: prospective borrowers register and undergo verification before their creditworthiness is assessed determining applicable interest rates [15]; upon approval they receive funds under agreed repayment schedules.

Indonesia has initiated strategic measures addressing persistent NPL issues including stricter regulations enforced by OJK aimed at fostering responsible lending practices alongside restructuring programs assisting debtors facing economic hardships while enhancing credit information systems [16].

Research indicates that CPI effectively assesses individual characteristics relevant not only for personal development but also within financial management contexts, thus this study aims at applying CPI during borrower assessments providing lenders with valuable insights into potential repayment behaviours thereby optimizing risk management strategies across Indonesian online lending frameworks.

2.1 The proposed system

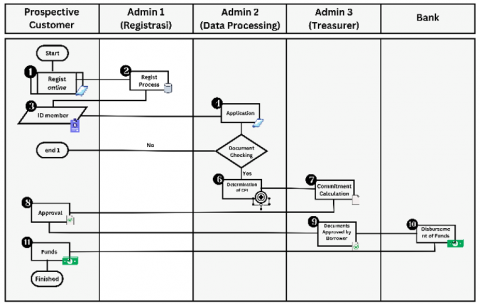

Based on Figure 1, the activities involved in the borrowing process are outlined. The first stage involves the borrower submitting a loan application to the online lending system along with the necessary supporting documents. The documents will then be screened, and after the selection process, the system will make a Stage 1 decision on whether to approve or reject the documents. If the documents are rejected, the process will end; however, if the application is approved, the borrower will receive a link to complete the CPI questions. After completing the test, the results will be processed using a fuzzy system, which will generate a loan amount recommendation based on the calculations. The recommended loan amount will be confirmed to the borrower, and if they agree, the process will proceed with approval and the disbursement of funds to the designated account or third party, in accordance with the initial agreement.

Figure 1. Proposed system using CPI with Mamdani fuzzy logic

2.2 Personality assessment using the CPI

The selection of ten traits from the CPI for recommending loan amounts in online lending is justified by their relevance to financial behavior, comprehensive nature, high psychometric validity, and flexibility in data integration. These traits enhance objective decision-making and capture the complexity of individual financial management skills, ultimately improving predictive accuracy in lending assessments [17, 18].

The questionnaire utilized in this study was developed based on the CPI methodology, which is a recognized tool for assessing personality traits [17, 19]. It consists of 10 distinct components, each of which is represented by three specific questions designed to gauge the respective trait accurately. The 10 components included in the questionnaire are Control, which measures an individual's ability to manage impulses; Ego Strength, assessing resilience; Warmth, reflecting interpersonal engagement; Social Presence, evaluating charisma; Self-Acceptance, focusing on self-esteem; Empathy, measuring sensitivity to others; Achievement via Conformance, relating to adherence to social norms; Responsibility, assessing reliability; Flexibility, evaluating adaptability; and Realistic, which measures practicality in decision-making [3, 18].

Table 1 presents a list of CPI questions designed to assess various psychological aspects such as ego strength, warmth, social presence, self-acceptance, empathy, responsibility, flexibility, and realism. Each question offers response options on a scale ranging from 20 (Never) to 100 (Always).

Table 1. CPI questions

|

No. |

Question |

Option |

|

Control |

||

|

1 |

Do you often make to-do lists or daily schedules for yourself? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

2 |

Do you respond if there are sudden changes in your plans or schedule? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

3 |

Do you find it difficult to stay focused on one task at a time? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Ego Strength |

||

|

4 |

Do you usually respond when facing stressful or pressured situations? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

5 |

Do you find it easy to remain calm and composed in challenging situations? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

6 |

Do you assess your level of resilience and self-confidence? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Warmth |

||

|

7 |

Do you tend to respond to people you have just met? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

8 |

Do you feel comfortable sharing your feelings and emotions with others? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

9 |

Do you often show kindness or empathy towards others? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Social Presence |

||

|

10 |

Do you behave in crowded and attention-seeking social situations? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

11 |

Do you find it easy to speak in public or take on a leadership role in a group? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

12 |

Do you often feel the need to control situations or lead discussions? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Self-Acceptance |

||

|

13 |

How do you generally feel about yourself? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

14 |

Do you criticize or punish yourself for mistakes or failures? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

15 |

Are you satisfied with your personal achievements and characteristics? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Empathy |

||

|

16 |

Do you often try to understand other people's perspectives or feelings? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

17 |

Do you respond when others express their feelings or problems to you? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

18 |

Do you often feel disturbed by other people's problems or their difficult situations? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Achievement via Conformance |

||

|

19 |

Do you respond to social rules or norms in certain situations? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

20 |

Do you care about adhering to the rules or expectations of others? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

21 |

Do you feel burdened or pressured if you do not meet certain expectations or social norms? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Responsibility |

||

|

22 |

Do you respond to the responsibilities or obligations assigned to you? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

23 |

Do you often feel responsible for completing certain tasks or projects? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

24 |

Do you handle situations where you are unable to fulfill your obligations effectively? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Flexibility |

||

|

25 |

Are you easy to adapt to changes that occur in your life? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

26 |

Do you respond when plans or situations change suddenly? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

27 |

Do you tend to get stuck in the same routines or behavioral patterns? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

Realistic |

||

|

28 |

Do you evaluate the level of realism or wisdom in making decisions? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

29 |

Do you often consider the consequences of your previous actions or decisions? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

|

30 |

Do you tend to view situations objectively and consider the facts rationally before taking action? |

(100) Always (80) Rarely (60) Sometimes (40) Almost Never (20) Never |

2.3 Input variables

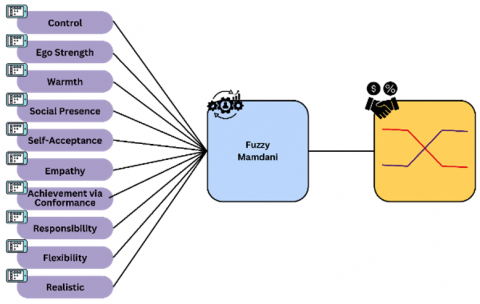

As input for the processing, data is obtained from borrowers who have been approved in Stage 1 selection, which involves documentation, to facilitate the completion of questions using the CPI. The recorded data from the 10 question components will be processed using a fuzzy system to produce output in the form of loan recommendations expressed as a percentage of the base loan amount on the platform [20, 21]. The input and output variables are presented in Figure 2.

Figure 2. Proposed input and output flow

2.3.1 Fuzzification function

Control measures an individual's ability to manage impulses and act in an orderly and disciplined manner. Individuals with high scores tend to effectively regulate their emotions and behaviours, often maintaining calm under pressure [22]. They are organized, reliable, and consistent in their actions. Conversely, individuals with low scores may be more impulsive, less organized, and more easily influenced by their immediate emotions [23].

Ego Strength measures how strongly an individual tends to influence or control social situations. Individuals with high scores on this scale are usually very assertive, willing to take initiative, and capable of leading others. They are often regarded as natural leaders by their peers. Conversely, a low score may indicate someone who prefers to follow or avoid conflict [24].

Warmth measures an individual’s preference for social interaction and tendency to seek the company of others. Individuals with high scores on this scale are typically friendly, open, and enjoy being part of social groups. They often blend in easily and build relationships quickly. Conversely, individuals with low scores may be more introverted, enjoy spending time alone, and have smaller social circles.

Social Presence assesses an individual's ability to attract attention and make a good impression in social situations. Individuals with high scores typically possess charisma, confidence in self-expression, and are skilled in non-verbal communication. They often make others feel comfortable and engaged with what they say. A low score may indicate someone who is quieter or less comfortable in public attention.

Self-Acceptance measures how satisfied an individual feels with themselves and their acceptance of their strengths and weaknesses. Individuals with high scores tend to have high self-esteem and are rarely plagued by self-doubt. They accept themselves as they are and feel comfortable with their personality. Low scores may indicate self-dissatisfaction and struggles with self-acceptance [25, 26].

Empathy measures an individual's ability to understand and share the feelings of others. Individuals with high scores tend to be sensitive to the needs and emotions of others, making them effective in providing support and care [27, 28]. They can view situations from others' perspectives and are often regarded as understanding friends. Low scores may indicate difficulty in recognizing or responding to others' feelings.

Achievement via Conformance evaluates an individual's tendency to think and act independently rather than conforming to the group. People with high scores on this scale tend to make decisions based on their own beliefs and are often innovative in their approaches. They value autonomy and are frequently unaffected by peer pressure. Individuals with low scores may prioritize group consensus and seek guidance from others in decision-making.

Table 2 presents the magnitude of the limits for the calculation conditions. These calculation conditions serve as the basis for determining the recommendation computations.

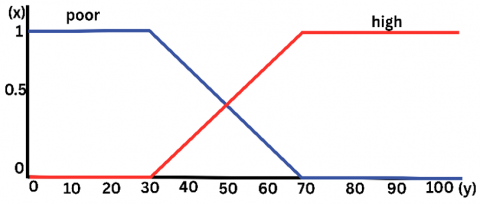

Based on Figure 3, it explains the gradual transition between the "poor" and "high" membership values in the fuzzy logic system. This figure illustrates fuzzy logic membership functions with two categories: "poor" and "high." The blue line represents the "poor" category, which holds a value of 1 from 0 to 30, then decreases to 0 at 70. The red line represents the "high" category, which remains at 0 until 30, then increases to 1 at 70, intersecting around the value of 50 on the x-axis.

Table 2. Fuzzification function of the variable “control, warmth, social presence, social presence, self-acceptance, empathy, achievement via conformance, responsibility, flexibility”

|

Input Variables |

Scope |

Fuzzification |

|

Control |

0-0.70 |

Poor |

|

0.50-1 |

High |

Figure 3. Membership function of the “control, warmth, social presence, social presence, self-acceptance, empathy, achievement via conformance, responsibility, flexibility” component

Responsibility assesses the extent to which individuals feel bound by ethical norms and social commitments. Individuals with high scores on this scale take their responsibilities toward others and society seriously. They are reliable and often seen as pillars of strength within their groups or families. Low scores may indicate a more relaxed attitude toward obligations and a lack of consistency in fulfilling commitments.

Flexibility assesses how open and accepting an individual is towards opinions, behaviors, and backgrounds that differ from their own. Individuals with high scores tend to be open to new and diverse ideas, demonstrating the ability to adapt to various social and cultural situations. They are not quick to judge and appreciate diversity. Conversely, individuals with low scores may be more resistant to change and less comfortable with differences.

2.3.2 Realistic

Realistic evaluates the extent of a person's desire and ability to gain recognition, social status, or professional standing. Individuals with high scores often have strong ambitions and work hard to achieve respected positions in society or their jobs. They are also likely to be very aware of their image and how they are perceived by others. Low scores may indicate a lack of concern for social status or satisfaction with simpler roles. Realistic is divided into two components, namely 'poor' and 'high', as described in detail in Table 3.

$\mu$ Poor $[x]=\left\{\begin{array}{cc}1 ; & x \leq 30 \\ \frac{70-x}{70-30} & 30 \leq x \leq 70 \\ 0 ; & x \geq 70\end{array}\right.$ (1)

$\mu$ High $[x]=\left\{\begin{array}{cc}0 ; & x \leq 30 \\ \frac{x-30}{70-30} & 30 \leq x \leq 70 \\ 1 ; & x \geq 70\end{array}\right.$ (2)

Table 3 presents the magnitude of the limits for the calculation conditions of the "high" and "poor" boundaries. These calculation conditions serve as the basis for determining the recommendation computations, which have values inverse to those in Table 2.

Table 3. Fuzzification function of the “realistic” variable

|

Input Variables |

Scope |

Fuzzification |

|

Realistic |

0-0.70 |

High |

|

0.50-1 |

Poor |

Figure 4 illustrates fuzzy logic membership functions with two categories: "high" and "poor." The blue line represents the "high" category, which holds a value of 1 from 0 to 30, then decreases to 0 at 70. The red line represents the "poor" category, which remains at 0 until 30, then increases to 1 from 70 to 100. Both lines intersect around the value of 50 on the x-axis.

Figure 4. Membership function of the “realistic” component

$\mu$High$[x]=\left\{\begin{array}{cc}1 ; & x \leq 30 \\ \frac{70-x}{70-30} & 30 \leq x \leq 70 \\ 0 ; & x \geq 70\end{array}\right.$ (3)

$\mu \operatorname{Poor}[x]=\left\{\begin{array}{cc}0 ; & x \leq 30 \\ \frac{x-30}{70-30} & 30 \leq x \leq 70 \\ 1 ; & x \geq 70\end{array}\right.$ (4)

2.4 Output variable

2.4.1 Loan recommendation (%)

The output of the CPI is in the form of loan amount recommendations expressed as a percentage, derived from the recommended value multiplied by the base loan platform.

Numeric values play a crucial role in determining the suggested loan limits, including minimum and maximum thresholds based on factors such as experience, caution, extroversion, compatibility, and the level of neuroticism of the loan applicants, all of which serve as inputs for the Fuzzy Evaluation System (FES). When the loan value does not exceed 35, there is a high likelihood that the applicant will receive a loan amount within the minimum range. Conversely, a value reaching or exceeding 65 indicates that the applicant is likely to obtain the maximum loan allocation. The output of this loan is categorized into two fuzzy categories, namely "minimum" and "maximum," employing trapezoidal curves to determine the output membership functions. Table 4 and Figure 5 provide illustrations of the fuzzy sets and membership functions related to the loan output.

Table 4. Fuzzification of the “loan” recommendation variable

|

Input Variables |

Scope |

Fuzzification |

|

Loan |

0-0.65 |

Minimum |

|

0.35-1.00 |

Maximum |

Figure 5. Output variable in the form of recommendations (%)

$\mu$ Minimum $[\mathrm{x}]=\left\{\begin{array}{cc}1 ; & \mathrm{x} \leq 35 \\ \frac{65-\mathrm{x}}{65-35} & 35 \leq \mathrm{x} \leq 65 \\ 0 ; & \mathrm{x} \geq 65\end{array}\right.$ (5)

$\mu$ Maximum $[x]=\left\{\begin{array}{cc}0 ; & x \leq 35 \\ \frac{x-35}{65-35} & 35 \leq x \leq 65 \\ 1 ; & x \geq 65\end{array}\right.$ (6)

2.4.2 Fuzzy rule base

In the system we developed, there are 10 input variables, each with 2 conditions, namely 'Poor' and 'High,' resulting in a calculation base of 2^10=1,024 possibilities. The rule base is constructed using the IF-Then formula to generate outputs in the form of percentages. We conducted an analysis to determine the weights for each output domain variable. We sought the weights for each variable that influence the output results. The highest weights are 0.467 for the Control variable, 0.214 for Ego Strength, 0.328 for Warmth, 0.247 for Social Presence, 0.451 for Self-Acceptance, 0.325 for Empathy, 0.472 for Achievement via Conformance, 0.325 for Responsibility, 0.712 for Flexibility, and 0.635 for Realistic. Based on the weight values, we established the conditional rules as follows:

|

[R092]: |

If Control=Medium, Ego Strength=High, Warmth=Poor, Social Presence=Medium, Social Presence=Poor, Self-Acceptance=Poor, Empathy=Poor, Achievement via Conformance=Poor, Responsibility=Poor, Flexibility=Poor, and Realistic=Poor, then Loan=Maximum (1). |

|

[R115]: |

If Control=Medium, Ego Strength=High, Warmth=Poor, Social Presence=High, Social Presence=Poor, Self-Acceptance=Poor, Empathy=Poor, Achievement via Conformance=Poor, Responsibility=Poor, Flexibility=Poor, and Realistic=Poor, then Loan=Maximum (1). |

|

[R172]: |

If Control=Medium, Ego Strength=High, Warmth=Medium, Social Presence=Medium, Social Presence=Poor, Self-Acceptance=Poor, Empathy=Poor, Achievement via Conformance=Poor, Responsibility=Poor, Flexibility=Poor, and Realistic=Poor, then Loan=Minimum (1). |

|

[R248]: |

If Control=Medium, Ego Strength=High, Warmth=Medium, Social Presence=High, Social Presence=Poor, Self-Acceptance=Poor, Empathy=Poor, Achievement via Conformance=Poor, Responsibility=Poor, Flexibility=Poor, and Realistic=Poor, then Loan=Maximum (1). |

|

[R320]: |

If Control=High, Ego Strength=High, Warmth=Poor, Social Presence=Medium, Self-Acceptance=Poor, Empathy=Poor, Achievement via Conformance=Poor, Responsibility=Poor, Flexibility=Poor, and Realistic=Poor, then Loan=Maximum (1). |

|

[R329]: |

If Control=High and Ego Strength=High and Warmth=Poor and Social Presence=High and Social Presence=Poor and Self-Acceptance=Poor and Empathy=Poor and Achievement via Conformance=Poor and Responsibility=Poor and Flexibility=Poor and Realistic=Poor, then Loan=Maximum (1). |

|

[R351]: |

If Control=High and Ego Strength=High and Warmth=Medium and Social Presence=Medium and Social Presence=Poor and Self-Acceptance=Poor and Empathy=Poor and Achievement via Conformance=Poor and Responsibility=Poor and Flexibility=Poor and Realistic=Poor, then Loan=Maximum (1). |

|

[R388]: |

If Control=High, Ego Strength=High, Warmth=Medium, Social Presence=High, Social Presence=Poor, Self-Acceptance=Poor, Empathy=Poor, Achievement via Conformance=Poor, Responsibility=Poor, Flexibility=Poor, and Realistic=Poor, then Loan=Maximum (1). |

2.4.3 Defuzzification and Mamdani inference

Defuzzification is executed to convert fuzzy values into crisp values that can be easily understood and applied in a non-fuzzy context. This process is used in fuzzy control systems, where decisions must be made based on fuzzy logic involving linguistic variables and fuzzy rules. After the fuzzy logic system evaluates the conditions and applies the relevant rules, the results obtained are in the form of fuzzy values. Defuzzification is necessary to transform these fuzzy values into real values or specific actions that can be implemented in physical systems or practical decisions. In FES, we utilize the centroid method to implement the defuzzification process (23).

$z=\frac{\int \mu C(z) \cdot z d z}{\int \mu C(z) \cdot d z}$ (7)

In a data capture showing the aggregation results with the following conditions: Control=68, Ego Strength=72, Warmth=83, Social Presence=74, Self-Acceptance=60, Empathy=84, Achievement via Conformance=76, Responsibility=78, Flexibility=42, and Realistic=38. The next step will be to calculate the membership degrees for each variable. The truth degree (i) is a component of the Mamdani FIS rules by taking the minimum value from several displayed membership degrees. Subsequently, the largest value will be selected from the smallest values compared. After that, through calculations using the centroid method, the crisp value for the loan output is obtained. The steps below illustrate the input data as stated above:

(1) Control $=68, \mu(Poor)=0$, and $\mu$ High $=0.70$

(2) Ego Strength $=72, \mu(Poor)=0$, and $\mu$ High $=1$

(3) Warmth $=83, \mu(Poor)=0$, and $\mu$ High $=1$

(4) Social Presence $74, \mu(Poor)=0$, and $\mu$ High $=0.88$

(5) Self - Acceptance $=60, \mu(Poor)=0$, and $\mu$ High $=0.70$

(6) Empathy $=84, \mu (Poor) =0$, and $\mu$ High $=1$

(7) $\begin{aligned} & \text { Achievement via Conformance }=76, \mu \text { (Poor) } =0 \text {, and } \mu \text { High }=1\end{aligned}$

(8) Responsibility $=78, \mu(Poor) =0$, and $\mu$ High $=1$

(9) Flexibility $=42, \quad \mu(Poor)=0$, and $\mu$ High $=1$

(10) Realistic $=34, \quad \mu(Poor)=0$, and $\mu$ High $=1$

Based on the collected data, it can be conditioned using the above formulation through the 8 rule approaches that have been described, resulting in the outcomes displayed below:

(1) $\alpha_{092}=\min (0.21 ; 1 ; 0.14 ; 0.31 ; 1)=0.14$

(2) $\alpha_{115}=\min (0.22 ; 1 ; 0.16 ; 0.81 ; 1)=0.16$

(3) $\alpha_{172}=\min (0.18 ; 1 ; 0.19 ; 0.48 ; 1)=0.18$

(4) $\alpha_{248}=\min (0.17 ; 1 ; 0.16 ; 0.92 ; 1)=0.16$

(5) $\alpha_{320}=\min (0.98 ; 1 ; 0.42 ; 0.38 ; 1)=0.38$

(6) $\alpha_{329}=\min (0.72 ; 1 ; 0.63 ; 0.82 ; 1)=0.63$

(7) $\alpha_{351}=\min (0.98 ; 1 ; 0.62 ; 0.82 ; 1)=0.62$

(8) $\alpha_{388}=\min (0.78 ; 1 ; 0.61 ; 0.72 ; 1)=0.61$

Based on the calculations, the results will be as follows:

$\begin{gathered}\alpha= \max \left(\alpha_{092}, \alpha_{115}, \alpha_{172}, \alpha_{248}, \alpha_{320}, \alpha_{329}, \alpha_{351}, \alpha_{388}\right) \\ \alpha=\max (0.14,0.16,0.18,0.16,0.38,0.63,0.62,0.61) \\ \alpha=0.63\end{gathered}$ (8)

Using the centroid method, the recommendation given is 63%, which indicates that this recommendation is lower than the recommendation provided by the admin system, which is 70%. In this regard, we recommend that the suggested loan percentage be 36%, considering the psychological influence of borrowers that will impact the repayment process for the loan.

We distributed questionnaires filled out by prospective Debtors. This questionnaire is designed to assess the personality of Debtors based on five variables from the CPI, namely Control, Ego Strength, Warmth, Social Presence, Self-Acceptance, Empathy, Achievement via Conformance, Responsibility, Flexibility, and Realistic. The questionnaire was developed from borrowers applying for loans through the online lending platform. Data collection took place over a period of two months. The results from the tests filled out by 25 prospective debtors using the CPI are presented in Table 5.

Table 5. Survey results acquisition

|

Name |

Control |

Ego Strength |

Warmth |

Social Presence |

Self-Acceptance |

Empathy |

Achievement via Conformance |

Responsibility |

Flexibility |

Realistic |

|

Costumer 1 |

71 |

61 |

77 |

72 |

73 |

74 |

71 |

81 |

34 |

31 |

|

Costumer 2 |

75 |

55 |

52 |

66 |

81 |

65 |

68 |

68 |

32 |

28 |

|

Costumer 3 |

84 |

17 |

65 |

72 |

66 |

72 |

77 |

48 |

35 |

35 |

|

Costumer 4 |

74 |

80 |

75 |

71 |

61 |

72 |

50 |

67 |

26 |

31 |

|

Costumer 5 |

79 |

70 |

73 |

69 |

55 |

57 |

64 |

77 |

36 |

39 |

|

Costumer 6 |

48 |

74 |

81 |

76 |

71 |

57 |

64 |

77 |

33 |

36 |

|

Costumer 7 |

76 |

77 |

66 |

60 |

80 |

63 |

74 |

73 |

36 |

31 |

|

Costumer 8 |

63 |

60 |

62 |

70 |

72 |

62 |

82 |

72 |

38 |

28 |

|

Costumer 9 |

78 |

67 |

68 |

76 |

66 |

73 |

69 |

63 |

31 |

43 |

|

Costumer 10 |

70 |

56 |

60 |

84 |

58 |

76 |

74 |

67 |

33 |

33 |

|

Costumer 11 |

60 |

57 |

57 |

68 |

74 |

77 |

62 |

63 |

38 |

41 |

|

Costumer 12 |

80 |

75 |

75 |

80 |

72 |

75 |

68 |

68 |

36 |

35 |

|

Costumer 13 |

70 |

74 |

74 |

49 |

82 |

65 |

60 |

81 |

35 |

37 |

|

Costumer 14 |

76 |

83 |

83 |

74 |

69 |

80 |

75 |

61 |

35 |

33 |

|

Costumer 15 |

68 |

62 |

68 |

74 |

68 |

73 |

70 |

77 |

33 |

35 |

|

Costumer 16 |

83 |

73 |

74 |

69 |

60 |

79 |

79 |

81 |

33 |

30 |

|

Costumer 17 |

51 |

89 |

85 |

83 |

57 |

76 |

77 |

81 |

36 |

30 |

|

Costumer 18 |

58 |

59 |

64 |

61 |

70 |

55 |

63 |

69 |

41 |

41 |

|

Costumer 19 |

74 |

70 |

76 |

73 |

74 |

76 |

75 |

79 |

28 |

39 |

|

Costumer 20 |

72 |

57 |

73 |

56 |

77 |

81 |

69 |

78 |

33 |

33 |

|

Costumer 21 |

82 |

74 |

73 |

70 |

60 |

78 |

80 |

64 |

34 |

33 |

|

Costumer 22 |

81 |

74 |

67 |

85 |

67 |

85 |

78 |

65 |

30 |

32 |

|

Costumer 23 |

82 |

67 |

67 |

67 |

73 |

68 |

80 |

53 |

32 |

35 |

|

Costumer 24 |

71 |

68 |

68 |

82 |

81 |

70 |

68 |

71 |

44 |

31 |

|

Costumer 25 |

75 |

70 |

76 |

64 |

66 |

78 |

74 |

84 |

34 |

37 |

The assessment system developed to manage the interface evaluation is implemented using the Fuzzy Matlab graphical user interface (GUI). The input variables in the system consist of 10 components, namely Control, Ego Strength, Warmth, Social Presence, Self-Acceptance, Empathy, Achievement via Conformance, Responsibility, Flexibility, and Realistic. Based on 'Customer 1', the acquired values are Control=71, Ego Strength=61, Warmth=77, Social Presence=72, Self-Acceptance=73, Empathy=74, Achievement via Conformance=71, Responsibility=81, Flexibility=34, and Realistic=31, thus the recommended output is 66%.

The findings presented in the table in the appendix provide valuable insights into borrower characteristics and the loan recommendations generated from the analysis conducted. The table includes data from 25 borrowers from various cities and provinces in Indonesia, along with information regarding the loan amounts requested, the percentage of loan recommendations made by the admin, and the percentages based on the CPI. The average percentage of loan recommendations given by the admin is 79.4%, while the CPI-based recommendations average 65.1%. These figures indicate a discrepancy between the admin's assessments and the underlying psychological evaluations that inform loan recommendations.

Further analysis of this data reveals a tendency for the admin to recommend higher loan amounts. For instance, Customer 12 from Pasuruan received a CPI recommendation of 68% yet was still allocated a loan percentage of 80% by the admin. Conversely, Customer 18 from Magelang exhibited the lowest CPI recommendation at 59% for a loan of IDR 50,000,000, reflecting a mismatch between the psychological profile of the borrower and the proposed loan amount. This underscores the importance of aligning psychometric assessments with administrative decisions in the loan approval process.

Table 6. Comparison data of credit recommendations based on admin assessments and improvements to the CPI principles using fuzzy methods

|

Name |

City |

Province |

Loan (IDR) |

Loan (%) by Admin |

Loan (%) by CPI |

|

Costumer 1 |

Sleman |

Yogyakarta |

60.000.000 |

80 |

66 |

|

Costumer 2 |

Bandung |

West Java |

55.000.000 |

75 |

61 |

|

Costumer 3 |

Gresik |

East Java |

40.000.000 |

80 |

64 |

|

Costumer 4 |

Badung |

Bali |

80.000.000 |

70 |

63 |

|

Costumer 5 |

Cimahi |

West Java |

20.000.000 |

80 |

63 |

|

Costumer 6 |

Semarang |

Central Java |

50.000.000 |

100 |

63 |

|

Costumer 7 |

Sidoarjo |

East Java |

25.000.000 |

80 |

65 |

|

Costumer 8 |

Karawang |

West Java |

40.000.000 |

75 |

63 |

|

Costumer 9 |

Jember |

East Java |

40.000.000 |

80 |

64 |

|

Costumer 10 |

Buleleng |

Bali |

50.000.000 |

80 |

63 |

|

Costumer 11 |

Sampang |

East Java |

80.000.000 |

75 |

61 |

|

Costumer 12 |

Pasuruan |

East Java |

75.000.000 |

80 |

68 |

|

Costumer 13 |

Bantul |

Yogyakarta |

30.000.000 |

75 |

64 |

|

Costumer 14 |

Tulungagung |

East Java |

50.000.000 |

100 |

69 |

|

Costumer 15 |

Banyuwangi |

East Java |

60.000.000 |

80 |

65 |

|

Costumer 16 |

Cirebon |

West Java |

40.000.000 |

90 |

68 |

|

Costumer 17 |

Malang |

East Java |

40.000.000 |

80 |

69 |

|

Costumer 18 |

Magelang |

Central Java |

50.000.000 |

75 |

59 |

|

Costumer 19 |

Purwakarta |

West Java |

40.000.000 |

75 |

69 |

|

Costumer 20 |

Nganjuk |

East Java |

80.000.000 |

80 |

65 |

|

Costumer 21 |

Indramayu |

West Java |

20.000.000 |

70 |

67 |

|

Costumer 22 |

Pati |

Central Java |

50.000.000 |

75 |

69 |

|

Costumer 23 |

Klaten |

Central Java |

25.000.000 |

80 |

64 |

|

Costumer 24 |

Palembang |

South Sumatra |

40.000.000 |

80 |

67 |

|

Costumer 25 |

Sumba Barat |

East Nusa Tenggara |

40.000.000 |

70 |

68 |

|

Average |

79.4 |

65.1 |

|||

Figure 6. Comparison chart of recommendations based on admin assessments and CPI

The data also reveals that the variable weights within the fuzzy model play a crucial role in determining loan recommendations. The analysis indicates that the Empathy variable holds the highest weight at 0.572, followed closely by Achievement via Conformance at 0.524, while the Flexibility variable has the lowest weight at 0.085. By utilizing these weights, this study successfully established 1,024 fuzzy rule bases, which contribute to more accurate loan recommendations.

By integrating psychometric analysis with financial data, this research provides evidence supporting the application of the CPI in credit assessments, potentially reducing the risk of problematic loans by up to 20%. Through this approach, financial institutions are expected to make more informed decisions regarding loan provisions, ultimately enhancing financial stability within the online lending sector in Indonesia. Furthermore, the findings highlight the need to further explore additional factors that may influence the evaluation of prospective borrowers, such as their financial conditions and loan history.

The potential reduction of problematic loan risk by up to 20% is achieved through the accumulation process of model performance metrics. Model performance metrics are essential tools for evaluating the effectiveness of models in prediction and classification, particularly in online lending. Key metrics include accuracy, precision, recall, and F1 score, which measure the reliability of detecting bad loans. Additionally, AUC-ROC assesses the ability to distinguish between positive and negative classes, while the confusion matrix provides detailed insights into classification errors. Mean Absolute Error (MAE) and Mean Squared Error (MSE) are utilized in regression to measure prediction errors. The use of these metrics aids in comprehensively understanding model performance and identifying areas for improvement.

This table presents a comparison of credit recommendation data based on administrative assessments and improvements using the California Psychological Inventory (CPI) principles with fuzzy methods. It includes customer details, loan amounts, and loan percentages by both admin and CPI, highlighting differences and averages across 25 customers. This is shown in Table 6.

The comparison of loan percentages by Admin and CPI over 25 periods reveals distinct patterns of fluctuation and stability. Loans managed by Admin (blue line) exhibit high variability, with significant peaks occurring in periods 7 and 14. In contrast, loans managed by CPI (orange line) remain relatively stable and consistent within the 60–70 percent range throughout the entire period. Although Admin’s loan percentages are generally higher, they are notably unstable, reflecting significant volatility. On the other hand, CPI demonstrates a lower but steady loan percentage, indicating greater consistency in loan management. This suggests that CPI tends to adopt a more conservative or structured approach compared to Admin, as illustrated in Figure 6.

We have developed a fuzzy rule-based system that utilizes CPI values as input variables and loan percentages as outputs. In this study, we analyze data to establish the rule base by calculating the weights of each input variable. The results indicate that the Control variable has a weight of 0.498, the Ego Strength variable is 0.315, the Social Presence variable is 0.288, the Warmth variable is 0.187, the Self-Acceptance variable is 0.278, the Empathy variable is 0.572, the Achievement via Conformance variable is 0.524, the Responsibility variable is 0.374, the Flexibility variable is 0.085, and the Realistic variable is 0.072. Using these weights, we created 1,024 fuzzy rule bases by applying the IF-Then function. The comparative analysis between the recommendations from the admin and the proposed system shows that the application of CPI in loan amount recommendations can reduce losses related to bad loans by up to 20%. The findings from this research will serve as considerations for a more accurate assessment of prospective debtors, which in turn can enhance company revenue. Additionally, this will benefit the community by boosting business activities and assist the government in supporting the economic activities of the populace. The proposed system can serve as a reference in assessing prospective debtors within the banking sector. This research still requires further development by including additional variables such as the financial condition of prospective debtors, psychological values, and loan history, as well as conducting more in-depth studies regarding recommendations for loan amounts related to bad credit.

Existing studies on online lending often focus on financial metrics and historical data, lacking the integration of psychometric evaluations. This gap highlights the need for incorporating tools like the CPI to assess borrower characteristics, which could enhance creditworthiness assessments and improve loan decision-making processes.

The author wishes to express gratitude to Universitas Trisakti for their support in providing funding for this research. Additionally, thanks are extended to the Online Loan Service for their assistance in supplying loan data for this study, as well as to all related parties who have contributed help and support throughout the completion of this research.

|

CPI |

California Psychological Inventory |

|

OJK |

Financial Services Authority |

|

TWP |

Total Write Off Percentage |

|

CRM |

Customer Relationship Management |

|

FES |

Fuzzy Evaluation System |

|

GUI |

Graphical User Interface |

|

TC |

Total Control |

|

TES |

Ego Strength |

|

TW |

Warmth |

|

TSP |

Social Presence |

|

TSC |

Self-Acceptance |

|

TE |

Empathy |

|

TAC |

Achievement via Conformance |

|

TR |

Responsibility |

|

TF |

Flexibility |

|

TRe |

Realistic |

|

Greek symbols |

|

|

$\mu$ |

Myu |

|

$\alpha$ |

Alpha |

|

> |

Greater than |

|

< |

Less than |

[1] Budiharto, B., Lestari, S.N., Hartanto, G. (2019). The legal protection of lenders in peer to peer lending system. Law Reform, 15(2): 275-289. https://doi.org/10.14710/lr.v15i2.26186

[2] Suryono, R.R., Budi, I., Purwandari, B. (2021). Detection of fintech P2P lending issues in Indonesia. Heliyon, 7(4): e06782, https://doi.org/10.1016/j.heliyon.2021.e06782

[3] Soto, C.J., John, O.P. (2009). Using the california psychological inventory to assess the big five personality domains: A hierarchical approach. Journal of Research in Personality, 43(1): 25-38. https://doi.org/10.1016/j.jrp.2008.10.005

[4] Kurniawan, F., Wijaya, C. (2020). The effect of loan granted factor on peer-to-peer lending (funded loan) in Indonesia. Investment Management & Financial Innovations, 17(4): 165-174, http://doi.org/10.21511/imfi.17(4).2020.16

[5] Maulana, R., Nuryakin, C. (2021). The effect of saving account ownership and access to financial institutions on household loans in Indonesia. Bulletin of Monetary Economics and Banking, 24(3): 465-486. https://doi.org/10.21098/bemp.v24i3.1428

[6] Fitrianah, D., Ratnasari, A., Fuji, S.A.E., Lim, S.M. (2022). A data mining approach to determine prospective debtor of unsecured credit (Case Study: Bank XYZ in Indonesia). In International Conference on Emerging Technologies and Intelligent Systems, pp. 138-149. https://doi.org/10.1007/978-3-031-20429-6_14

[7] Liu, Z., Zhang, Z., Yang, H., Wang, G., Xu, Z. (2023). An innovative model fusion algorithm to improve the recall rate of peer-to-peer lending default customers. Intelligent Systems with Applications, 20: 200272. https://doi.org/10.1016/j.iswa.2023.200272

[8] Astutik, S., Soerodjo, I. (2023). The role of the financial services authority in setting the interest rate for financial technology loans as consumer protection of financial services. Yuridika, 38(2): 431-442. https://doi.org/10.20473/ydk.v38i2.40064

[9] Zhang, W., Chen, R.S., Chen, Y.C., Lu, S.Y., Xiong, N., Chen, C.M. (2019). An effective digital system for intelligent financial environments. IEEE Access, 7: 155965-155976. https://doi.org/10.1109/ACCESS.2019.2943907

[10] Johan, S. (2021). Peer-to-peer lending’s customer profile: Empirical research on Indonesia’s financial technology market. Southeast Asian Journal of Economics, 9(1): 103-120.

[11] Cai, C., Marrone, M., Linnenluecke, M. (2022). Trends in fintech research and practice: Examining the intersection with the information systems field. Communications of the Association for Information Systems, 50(1): 803-834. https://doi.org/10.17705/1CAIS.05036

[12] Setiawan, A.A., Silaen, Y.E., Andreas, T., Oktavia, T. (2022). Analysis of intention to use on pay later payment system during COVID-19 pandemic. International Journal of Emerging Technology and Advanced Engineering, 12(3): 119-129. https://doi.org/10.46338/IJETAE0322_14

[13] Woo, H., Sohn, S.Y. (2022). A credit scoring model based on the Myers-Briggs type indicator in online peer-to-peer lending. Financial Innovation, 8(1): 42. https://doi.org/10.1186/s40854-022-00347-4

[14] Rasipuram, S., Jayagopi, D.B. (2020). Automatic multimodal assessment of soft skills in social interactions: A review. Multimedia Tools and Applications, 79(19): 13037-13060. https://doi.org/10.1007/s11042-019-08561-6

[15] Bojanowska, A.B., Kulisz, M. (2023). Using fuzzy logic to make decisions based on the data from customer relationship management systems. Advances in Science and Technology. Research Journal, 17(5): 269-279. http://doi.org/10.12913/22998624/172374

[16] Abdurrahman, M.A., Anto, D., Lubis, M. (2022). Analysis of fintech use at early working age in Indonesia. In Proceedings of the 8th International Conference on Industrial and Business Engineering, pp. 400-405. https://doi.org/10.1145/3568834.3568867

[17] Detrick, P., Roberts, R.M. (2022). Police applicant response bias on the California Psychological Inventory. Psychological Services, 19(1): 176-182. https://doi.org/10.1037/ser0000524

[18] Whitman, M.R., Elias, L.S., Cappo, B.M., Ben-Porath, Y.S. (2021). Criterion validity of MMPI-3 scores in preemployment evaluations of public safety candidates. Psychological Assessment, 33(12): 1169-1180. https://doi.org/10.1037/pas0001042

[19] Baumgartner, L., Roller, L., LeVay, M., Trinh, J., Morris, A. (2022). Burnout among pharmacy preceptors in northern California. American Journal of Pharmaceutical Education, 86(8): ajpe8759. https://doi.org/10.5688/ajpe8759

[20] Bonsall IV, S.B., Koharki, K., Kraft, P., Muller III, K.A., Sikochi, A. (2023). Do rating agencies behave defensively for higher risk issuers? Management Science, 69(8): 4864-4887. https://doi.org/10.1287/mnsc.2022.4537

[21] Vyshnavi, M., Muthukumar, M. (2024). Optimizing hidden markov models with fuzzification techniques. Reliability: Theory & Applications, 19(4(80)): 599-610. https://doi.org/10.24412/1932-2321-2024-480-599-610

[22] Cheng, Y. (2024). Fuzzy logic-based quantitative development model for job satisfaction in college graduates. International Journal of Computational Intelligence Systems, 17(1): 226. https://doi.org/10.1007/s44196-024-00637-y

[23] Juhász, I. (2019). Personality testing of salespeople working in finance. Public Finance Quarterly=Pénzügyi Szemle, 64(2): 173-188.

[24] Ge, R., Gu, B., Feng, J. (2017). Borrower’s self-Disclosure of social media information in P2P lending. In Proceedings of the Annual Hawaii International Conference on System Sciences, pp. 5562-5571.

[25] Robinson, C.S., Fokas, K., Witkiewitz, K. (2018). Relationship between empathic processing and drinking behavior in project MATCH. Addictive Behaviors, 77: 180-186. https://doi.org/10.1016/j.addbeh.2017.10.001

[26] Lee, S.M., Kim, H.K. (2022). The effect of system and user characteristics on intention to use: An empirical study of face recognition payment. Journal of System and Management Sciences, 12(3): 318-344. https://doi.org/10.33168/JSMS.2022.0316

[27] Contreras, G., Bos, J.W., Kleimeier, S. (2019). Self-Regulation in sustainable finance: The adoption of the Equator Principles. World Development, 122: 306-324. https://doi.org/10.1016/j.worlddev.2019.05.030

[28] Pajević, F. (2021). The Tetris office: Flexwork, real estate and city planning in Silicon Valley North, Canada. Cities, 110: 103060. https://doi.org/10.1016/j.cities.2020.103060