Elena Potekhina*![]() | Galina Tretyakova

| Galina Tretyakova![]() | Olga Lebedeva

| Olga Lebedeva![]() | Elena Dudina

| Elena Dudina![]() | Aleksandr Shelygov

| Aleksandr Shelygov![]() | Kostyantyn Lebedev

| Kostyantyn Lebedev![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The paper examines the management of the government debt portfolio in the Russian Federation, focusing on the significant macroeconomic challenges and structural imbalances within the debt portfolio. Specifically, it addresses issues such as increasing debt levels, the growing burden of debt payments, and the imbalance in the composition of debt obligations. The study emphasizes the necessity of adopting new management approaches to mitigate significant economic and financial risks. It proposes a comprehensive method for targeted risk management, which includes optimizing the debt portfolio structure, coordinating state-level cash flows, and employing an improved system of debt load indicators. To minimize currency risk, the study introduces an approach to determine the optimal debt portfolio structure by balancing the impact of various borrowing currencies on debt payments. The results suggest substantial changes in public borrowing policy, advocating for a significant reduction in US dollar-denominated debt, diversification of the currency structure by increasing borrowings in other currencies, and enhancing the share of debt obligations in rubles and euros. These recommendations aim to create a more stable and balanced government debt portfolio, reducing vulnerability to external economic shocks.

debt portfolio structure, debt load indicators, risks, state, borrowing, currency risk, budget gaps

The increased impact of risks on financial and economic processes, particularly state debt borrowing, is a prominent feature of contemporary economic life. Consequently, state debt management has undergone significant adjustments. This study focuses on a comprehensive, scientifically-grounded risk analysis and strategic management of government debt portfolios, emphasizing the necessity for targeted risk management.

The impetus for developing debt risk management significantly increased after several sovereign defaults. The neglect of risk assessment issues and the balanced formation of government debt obligations were significant factors in the growing debt burden on global economies and their increased vulnerability to crises. Traditional cost-risk analysis, widely used before these crises to determine the optimal structure of public debt, has become inadequate when considering the full set of risk factors. Most models of such analysis abstract from the influence of macroeconomic factors on the level and structure of debt and consider interest rates and exchange rates as independent variables.

Several macroeconomic factors create zones of vulnerability, such as fluctuations in global capital flows, interest rate changes, and exchange rate volatility. These vulnerabilities, or weak points, significantly impact the structure and management of government debt. Additionally, non-obvious conditional obligations of the government, such as guarantees or contingent liabilities not immediately apparent in financial statements, further complicate debt management. These obligations can unexpectedly strain government finances, necessitating robust risk management strategies.

Using cost-risk analysis models often overlooks important relationships between these macroeconomic vulnerabilities and the structure of public debt. Moreover, models based on historical data cannot predict extreme future events. Therefore, new models and methods must consider all potential sources of risk, including shocks from capital flow reversals and financial shocks from transferring non-obvious conditional obligations to the state budget.

The purpose of this paper is to scientifically substantiate the applied aspects of state debt risk management and to generalize and adapt international experiences to the Russian context. The study will explore contemporary financial technologies and debt risk management tools, such as advanced statistical modeling, stress testing, and strategic portfolio standards, to improve the effectiveness of debt management in the Russian Federation. By incorporating international best practices, the paper aims to provide a tailored approach to managing government debt portfolios in the presence of risk.

The scientific novelty of the results lies in substantiating a holistic conceptual framework for risk management of the government debt portfolio and optimizing its structure. Additionally, the paper develops recommendations for forming a comprehensive system of state debt risk management.

The literature review acknowledges a broad spectrum of research on risk management and debt management. For example, Kosov [1] examines public debt management practices based on the Debt Sustainability Analysis (DSA) standard, highlighting the importance of sustainable borrowing practices. Lyasnikov and Ivashchenko [2] discuss the regulation of government securities markets, emphasizing the need for robust market infrastructure. Maruseva [3] evaluates the effectiveness of state debt portfolios, providing insights into performance metrics.

In terms of optimizing the structure of debt obligations, several works are noteworthy. Burkova [4], Mamedov [5], Nekhorosheva [6], Oladko [7], Rakhmetova [8], Solntsev et al. [9], Titova and Yuzhakova [10], and Yarasheva et al. [11] have all contributed valuable perspectives.

The increasing influence of debt borrowings on public finances and the associated search for effective debt management mechanisms, particularly in the context of financial security, have led to significant contributions from researchers such as Titarenko [12], Mian et al. [13], Bobryshev et al. [14], Karpov et al. [15], Lukiyanchuk et al. [16], Manakhova et al. [17], Markova et al. [18], Lebedev et al. [19], Schiller and Prpich [20], and Zavalko et al. [21].

Significant contributions to the development of risk theory and economic process modeling have been made by Bobrova [22], Engalychev [23], Kashinova [24], Mayer [25], Petukhova [26], Polyakova [27], Rodionov [28], Ukraintseva [29], Alhassan et al. [30], Nemirova and Savelyeva [31], Syrova [32], and Vovchenko et al. [33].

Despite extensive research on these individual topics, integrating risk management into debt management remains underdeveloped. This gap is crucial because a holistic approach that combines these areas is necessary for effective public debt management. The lack of comprehensive studies addressing this intersection creates a significant research void that this paper aims to fill. Understanding why this gap exists involves recognizing the complexities and dynamic nature of both risk and debt management, which require interdisciplinary approaches and advanced analytical tools.

Currently, the debt portfolio of the Russian Federation is formed irrationally. Its volume continues to increase, while annual debt payments, compounded by an undeveloped domestic capital market and high external risks, act as factors of instability for the fiscal sphere and increase the economy's dependence on external and internal factors.

Improving the effectiveness of the state debt policy will largely depend on the success and activity of efforts to develop this system. The state debt risk management in the Russian Federation is still forming from both theoretical and practical perspectives.

In conclusion, this study aims to enhance the theoretical and practical understanding of government debt risk management. By defining key terms, clearly stating the paper's purpose, and synthesizing relevant literature, this introduction sets the stage for a detailed exploration of innovative debt management strategies tailored to the needs of the Russian Federation.

This study employed a variety of scientific methods and techniques to comprehensively identify and solve theoretical and practical research objectives related to government debt risk management. Dialectics was utilized to understand and reveal the essence of government debt portfolio management by examining the dynamic and contradictory processes within debt management. Analysis and synthesis were applied to break down complex debt management processes into simpler components and then combine these components to form a coherent understanding. Classification and typology helped in identifying and categorizing risk factors, determining the nature of their impact on the debt portfolio. Factor and correlation analysis were employed to examine the relationships and dependencies between different risk factors and the government debt portfolio. Additionally, economic and mathematical modeling, including statistical modeling and comparative analysis, was used to simulate various scenarios and analyze the impact of risk factors on the debt portfolio of the Government of the Russian Federation (GRF).

2.1 Data sources

Federal State Statistics Service (Rosstat): Provided macroeconomic data, including GDP growth rates, inflation rates, and other economic indicators crucial for understanding the broader economic context in which the debt portfolio operates.

Ministry of Finance of the Russian Federation: Supplied detailed information on the composition, structure, and historical data of the government debt portfolio, including types of debt instruments, maturity profiles, and debt servicing costs.

Central Bank of the Russian Federation: Offered data on interest rates, exchange rates, and financial market conditions, which are essential for assessing the external and internal risks affecting the debt portfolio.

The works of leading scientists, legislative and regulatory acts, recommendations of international experts on government debt and risk management, analytical publications of international institutions and organizations (IMF, World Bank, Organization for Economic Cooperation and Development), publications and analytical studies of leading debt offices of foreign countries (Sweden, the Netherlands, New Zealand, Ireland, etc.).

These data sources were used to analyze the impact of various risk factors on the GRF's debt portfolio by providing a comprehensive set of quantitative and qualitative information.

2.2 Study stages

Stage 1:

Document Selection and Grouping: Documents were selected based on the key features of state debt risk management, such as relevance to debt optimization, risk assessment techniques, and international best practices. These documents were then grouped into two categories: statistical information and scientific research.

Stage 2:

Analysis of Direct Obligations: The currency structure of the obligations of the debt portfolio of the GRF was determined by analyzing the composition of debt instruments denominated in different currencies. This involved calculating the share of each currency in the total debt portfolio and forecasting future debt payments.

Stage 3:

Optimization and Simulation: A simulation model was developed to optimize the structure of the debt portfolio. This model considered various public borrowing strategies and aimed to balance the influence of different borrowing currencies on the volume of debt payments. The model's results were compared to the planned debt payment schedule to identify the most effective optimization strategies.

By following these methodological steps, the study provides a detailed analysis and practical recommendations for improving government debt risk management in the Russian Federation.

In considering the government debt portfolio, it is essential to interpret it both broadly and narrowly. The practical value of the latter approach is evident, as it views the government debt portfolio as a collection of appropriately designed debt obligations in monetary form, which are accepted by the government due to state borrowing and the provision of state guarantees. This perspective allows for a more comprehensive and adequate analysis than considering the category of government debt as a singular, undifferentiated entity [34, 35].

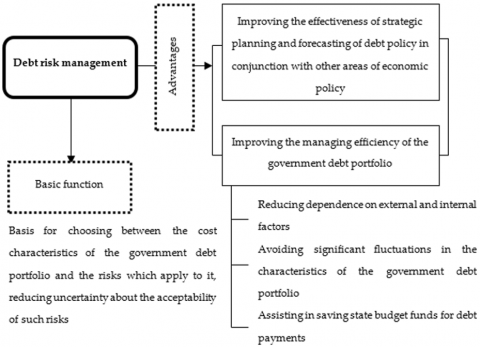

From a debt management standpoint in the Russian Federation, effective management of government debt obligations requires a focus on managing risks both in strategic planning and during the execution of transactions. The advantages of using debt risk management at the state level include improved financial stability and reduced vulnerability to economic shocks. These advantages are illustrated in Figure 1.

Generalizing contemporary practices of countries with high-quality debt management systems reveals that effective debt risk management involves more than just macroeconomic considerations. It requires attention to the internal structure of the debt portfolio, particularly the currency and interest structures of obligations and their maturity. Effective debt risk management also necessitates high levels of information, analytical, technical, and software support, as well as professional training for debt managers.

The integration of risk management theory with debt management practice allows for a comprehensive characterization of the debt risk management process. This process involves several stages, as depicted in Figure 2. One of the most challenging stages is quantitative risk assessment. Analyzing global practices shows the use of various risk measurements, including risk value indicators, budget risk, and risk expenditures, to assess the risk of increased debt payments. The practical value of using budget risk and risk expenditure methods lies in their ability to evaluate the risk of an increase in debt payment costs, contrasting with the more general risk value method [36-39].

Figure 1. Advantages of using government debt risk management

Figure 2. Risk management process components of the government debt portfolio

Stress testing, widely used alongside traditional probabilistic approaches to market risk assessment, is crucial for emergency planning. It helps mitigate the negative impacts of crises on the government debt portfolio. Additionally, risk management of the government debt portfolio employs a set of criteria indicators, including commonly used debt security indicators and specific portfolio structure indicators, such as strategic portfolio standards. These standards help avoid excessive risk and serve as the basis for practical measures to optimize the debt portfolio structure and assess the effectiveness of debt managers' actions.

The results of the study allow us to conclude that there is a need to develop a universal methodology for risk assessment. This should be one of the initial stages of forming a debt risk management system in the Russian Federation. Adapting global risk management practices to Russian realities is necessary, especially in balancing state-level cash flows within the budget accounting framework. Establishing a strategic portfolio standard for the medium term, known as the benchmark portfolio, and reviewing current debt security criteria to identify potential problems are also recommended.

The analysis highlights several factors that increase the potential negative impact of risks on the government debt portfolio, including the traditional imbalance of the state budget, an underdeveloped domestic capital market, and a disproportionate debt portfolio structure. Despite these challenges, the study found that the level of interest rate risk and the maturity of the GRF's external and internal debt components are acceptable. However, the significant share of foreign currency-denominated debt obligations exposes the government debt portfolio to foreign exchange policy and market fluctuations, which can increase negative consequences if access to foreign capital markets becomes restricted or borrowing costs rise.

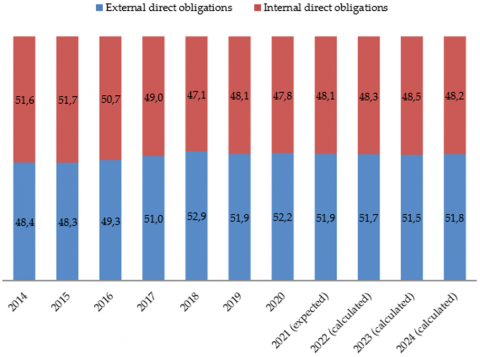

Figures 3 and 4 illustrate the current currency structure of the GRF's debt portfolio and the planned debt payments until 2024. The assessment of currency risk, based on assumptions about borrowing exchange rates and correlations between risk factors, indicates a wide range of possible debt payments. The analysis reveals a significant dependency of debt payments on fluctuations in the ruble/US dollar and euro/US dollar exchange rates. This sensitivity formed the basis for optimizing the government debt portfolio structure, aiming for a relatively equal impact of each borrowing currency on debt payments.

Figure 3. Direct obligations of the debt portfolio of the GRF by formation sources, %

Figure 4. The currency structure of the liabilities of the debt portfolio of the GRF as of 31.12.20 (data of the Ministry of Finance of the Russian Federation)

Another potential factor for the growth of liquidity risk in the GRF's debt portfolio, the deterioration of its structure, and the increase in the debt burden in the future is the determination of revenues from the sale of state property in the current year and the medium term. Additionally, the results of the conducted analysis demonstrate the need for qualitative improvement of government debt policy, in interaction with other areas of economic policy, within the context of risk management.

The system of debt risk management in the Russian Federation is still in formation. Currently, only a fragmentary assessment of the main risks and threats is conducted, and the results of these assessments rarely influence decision-making in government debt borrowing. The structure of the debt portfolio of the GRF is formed without a thorough assessment of the future economic burden and without a proper evaluation of alternative borrowing costs or the sensitivity of debt payments to changes in key risk factors.

Given the significant impact of currency risk on the cost of debt payments, the study examines the possibility of minimizing this risk by optimizing the current structure of the GRF's debt portfolio. This involves eliminating significant imbalances in the structure of debt payments over the medium term, as illustrated in Figures 4 and 5.

Figure 5. Currency structure of planned debt payments until 2024 (data from the Ministry of Finance of the Russian Federation)

The conducted assessment of the currency risk of the debt portfolio of the GRF using the accepted assumptions about the behavior of borrowing exchange rates, calculations of correlations between risk factors, and other statistical data allowed determining that the amount of payments on the obligations of the debt portfolio of the Government of Ukraine, which was formed at the beginning of 2021, in the medium term (until 2024) will be in a fairly wide range with a probability of 95%.

Conducting additional calculations allowed revealing the rate of dependency of debt payments on fluctuations in borrowing currencies was estimated, and the excessive potential influence of the behavior of the ruble/US dollar and euro/US dollar exchange rates on the change in the volume of payments on the debt portfolio of the GRF. The analysis of the sensitivity of debt payments to fluctuations in borrowing currencies became the initial basis for further calculations within the framework of optimizing the structure of the government debt portfolio. The proposed approach was based on the need to determine the structure of government debt obligations with a relatively equal impact of fluctuations in each of the borrowing currencies on the volume of debt payments.

Table 1. The combination of debt payments according to the proposed optimization compared to the planned payment schedule until 2024

|

Payment Currency |

The Amount of Planned Debt Payments |

The Amount of Debt Payments According to the Proposed Optimization |

||

|

Thousand units |

Thousand US dollars |

Thousand units |

Thousand US dollars |

|

|

Russian Ruble |

8,263,745.4 |

1,238,625.4 |

11,800,000.3 |

1,828,617.6 |

|

US Dollar |

5,409,730.5 |

5,409,730.2 |

2,118,000.2 |

2,118,000.1 |

|

Euro |

788,130.8 |

1,150,298.3 |

1,337,053.4 |

1,951,465.3 |

|

Japanese Yen |

9,992,754.3 |

85,774.6 |

9,992,754.3 |

85,774.6 |

|

Swiss Franc |

52,729.4 |

43,577.7 |

2,424,965.4 |

1,944,148.7 |

|

Other currencies |

575,273.5 |

878,280.4 |

575,273.5 |

878,280.4 |

Constructing a simulation model for optimizing the structure of the debt portfolio of the GRF allowed determining several options for the optimal combination of obligations based on various public borrowing strategies. According to the authors, the most acceptable and sufficiently achievable model in terms of certain combinations of obligations in the government debt portfolio in the medium term is the model presented in Table 1.

According to calculations, the optimal debt portfolio of the GRF in terms of its currency component should be formed based on the conditions for achieving by the end of 2025 debt payments distribution, shown in Figure 6.

Figure 6. Distribution of debt payments until 2024 according to the proposed model for optimizing the debt portfolio of the GRF

Therefore, one can determine the following actions necessary to practically implement the proposed optimization of the currency structure of the debt obligations portfolio of the GRF:

-Diversifying the Currency Structure and Searching for New Borrowing Currencies: Diversification reduces dependency on any single currency, thereby mitigating the risk associated with currency fluctuations. By spreading debt across multiple currencies, the GRF can better manage exchange rate risks and avoid the adverse effects of volatility in specific currency markets.

-Reducing the Existing Volume of Liabilities in US Dollars by Almost Half: The US dollar currently constitutes a significant portion of the GRF's debt, making it vulnerable to changes in US monetary policy and exchange rate fluctuations. Reducing dollar-denominated liabilities decreases this exposure and helps stabilize debt service costs in the face of currency depreciation.

-Implementing Borrowing to Support Relatively Equal Levels of Future Payments in Rubles, US Dollars, Euros, and Swiss Francs (or Other Currencies with Similar Stability): Balancing debt obligations among multiple stable currencies reduces the risk of over-reliance on any one currency. This balanced approach helps ensure that no single currency fluctuation disproportionately impacts overall debt payments, providing a more predictable and stable financial outlook.

-Partial Revision of Existing Government Debt Agreements to Allow for Currency Swaps: Currency swaps can help realign the debt portfolio with the desired currency composition without issuing new debt. This action provides flexibility in managing currency risk and can be cost-effective compared to issuing new debt in different currencies.

-Developing the Internal Capital Market to Provide Financing of Economic Needs Domestically: Strengthening the domestic capital market reduces dependency on external borrowing and shields the GRF from global financial market volatility. A robust internal market can offer more stable and predictable funding sources, aligning with national economic conditions.

Implementing these actions should become a key element of a broader strategy to optimize the GRF's debt portfolio by minimizing currency risk. Establishing strategic portfolio standards will be crucial for this optimization.

At the same time, considering the exceptional role of high-quality risk management in the implementation of the tasks set, one can determine the main lines of actions for creating such a system in the Russian Federation. Among them, we can highlight developing institutional, legislative, methodological foundations, increasing the coordination of debt, fiscal, monetary policies, and using the latest approaches of debt management.

In particular, a significant practical value of partial adaptation into the practice of the cash flow coordination method at the state level can be achieved through the following measures:

-Approaching the structure of the debt portfolio of the GRF in terms of the composition of currencies and their ratio to the structure of capital flows from abroad;

-Implementing a coordinated policy of the Ministry of Finance and the Central Bank of the Russian Federation regarding the compliance of the structure of international foreign exchange reserves and the currency basket of the government debt portfolio;

-Avoiding significant fluctuations in the exchange rate of the national currency during the period of receipt of foreign financing and implementing significant debt payments;

-Conducting effective distribution over time and in terms of debt payments to reduce the risk of refinancing, including harmonizing with state budget revenues and basic payments to avoid significant budget gaps.

In this context, implementing full-fledged debt risk management is possible while being aware of its importance and necessity in all parts of the government debt management process, using advanced global technologies and management tools, delineating clearly areas of responsibility, as well as continuity, information, logistics, financial and personnel support.

The study underscores the necessity of a systematic and integrated approach to managing risks associated with state debt borrowings. This approach should involve the use of advanced risk management strategies and tools that go beyond current practices. Specifically, the implementation of comprehensive risk assessment models, stress testing, and strategic portfolio standards are recommended. These tools can help in accurately predicting and mitigating potential risks by providing a more holistic view of the debt portfolio's vulnerabilities. Additionally, enhancing information, analytical, and technical support systems, along with professional training for debt managers, is crucial for effective risk management.

Macroeconomic issues, such as fluctuations in global capital flows, interest rate changes, and exchange rate volatility, often overshadow the problems of forming an optimal structure of the government debt portfolio. These issues create zones of vulnerability that significantly impact the management of government debt. For example, the dependency on foreign currency-denominated debt exposes the portfolio to exchange rate risks, while changes in global interest rates can affect borrowing costs. Addressing these macroeconomic challenges requires a balanced approach that considers both external and internal economic factors, enabling more effective and resilient debt management.

The study's limitations include the reliance on available data and the inherent assumptions in modeling and simulation. These constraints may have influenced the findings and the proposed optimization strategies. Future research should focus on developing more refined risk assessment methodologies and exploring the impact of emerging economic trends on government debt management. Additionally, further examination of the integration of fiscal and monetary policies in debt management, as well as the development of internal capital markets, would provide valuable insights for enhancing the effectiveness of debt management practices.

The implementation of a comprehensive debt risk management system is crucial for the effective management of government debt portfolios. By adopting advanced risk management tools, addressing macroeconomic challenges, and continuously improving methodologies, the Russian Federation can achieve a more stable and resilient debt portfolio. This study provides a foundation for future research and practical applications aimed at optimizing government debt management in the context of evolving economic dynamics.

[1] Kosov, M.E. (2020). Foreign practices of public debt management based on the DSA standard. Audit Statements, 1: 64-68. https://elibrary.ru/item.asp?id=42541924.

[2] Lyasnikov, N.V., Ivashchenko, N.P. (2014). Features of regulation of the government securities market: Problems and prospects of its development. Economy and Society: Contemporary Development Models, 8-2: 42-64. https://1economic.ru/lib/40274.

[3] Maruseva, K.A. (2017). Evaluation of the effectiveness of the state debt portfolio. Bulletin of the Belarusian State University of Economics, 3(122): 72-79. http://edoc.bseu.by:8080/handle/edoc/74513.

[4] Burkova, Y.A. (2014). Real estate investment trusts in the developed countries. MGIMO Review of International Relations, 4(37): 197-205. https://doi.org/10.24833/2071-8160-2014-4-37-197-205

[5] Mamedov, E.G.O., Lapteva, A.M. (2021). Risks of economic security and problems of the banking industry. International Science (Internauka), 3-2(179): 38-40. https://elibrary.ru/item.asp?id=44679545.

[6] Nekhorosheva, K.I. (2018). Review of strategies for managing currency risks. Eurasian Union of Scientists, 3-4(48): 45-46. https://elibrary.ru/item.asp?id=34914188.

[7] Oladko, V.S., Panchikhin, M.K., Rostovsky, D.E. (2019). Assessment of factors affecting the security of external remote banking services. Information Systems and Technologies, 2(112): 113-121. https://oreluniver.ru/public/file/archive/ISiT_2-19_kratkiy.pdf.

[8] Rakhmetova, A.M. (2012). The role of the banking sector in the financing of the regional economy. Bulletin of the Financial University, 6(72): 34-44. http://www.fa.ru/org/div/edition/vestnik/journals/2012%20%E2%84%966.pdf.

[9] Solntsev, O., Pestova, A., Mamonov, M. (2010). Stress test: Will banks need new state support? Economic Issues, 4: 61-81. https://doi.org/10.32609/0042-8736-2010-4-61-81

[10] Titova, L.N., Yuzhakova, K.A. (2012). Financial management in public administration bodies: Risk management system. Bulletin of the AKSOR, 2(22): 30-37. https://elibrary.ru/item.asp?id=17832166.

[11] Yarasheva, A.V., Makar, S.V., Simagin Yu, A. (2020). Behavioral economics: Population on the credit services market. Human Population, 23(3): 48-58. https://doi.org/10.19181/population.2020.23.3.5

[12] Titarenko, B.P. (2006). Risk management within the framework of the system model of project-oriented management. Project and Program Management, 1: 76-89. https://grebennikon.ru/article-58vh.html.

[13] Mian, A., Straub, L., Sufi, A. (2021). Non-bank financial institutions and the functioning of government bond markets (BIS Working Papers No. 968). Bank for International Settlements. https://www.bis.org/publ/work968.pdf.

[14] Bobryshev, A.N., Chaykovskaya, L., Dudaev, G.H., Serebryakova, E.A. Karlov, D.I. (2020). The concept of management accounting in the conditions of uncertainty and risk. Journal of Organizational Behavior Research, 5(2): 68-81.

[15] Karpov, V.V., Kovalev, V.A., Korableva, A.A., Khairov, B.G., Lebedev, K.A. (2017). Methodical framework of forming territorial innovation clusters based on import substitution mechanism. Revista Espacios, 38(58): 11.

[16] Lukiyanchuk, I.N., Panasenko, S.V., Kazantseva, S.Y., Lebedev, K.A.E., Lebedeva, O.E. (2020). Development of online retailing logistics flows in a globalized digital economy. Revista Inclusiones, 7(S2-1): 407-416.

[17] Manakhova, I., Levchenko, E., Bekher, V., Bystrov, A. (2020). Quality of human resources and personnel security risk management in digital economy. Calitatea, 21(175): 74-79.

[18] Markova, O.V., Listopad, E.Y., Shelygov, A.V., Fedorov, A.G., Kiselevich, I.V. (2021). Economic and legal aspects of the innovative activity of enterprises in the context of the digital economy. Nexo Revista Científica, 34(2): 964-972. https://doi.org/10.5377/nexo.v34i02.11623

[19] Lebedev, K.A., Ogloblina, E.V., Seredina, M.I., Altunina, Y.O., Kodolov, V.A. (2020). Socio-economic consequences of digital development of the economy. Revista Inclusiones, 7(S3-5): 421-430.

[20] Schiller, F., Prpich, G. (2014). Learning to organise risk management in organisations: What future for enterprise risk management? Journal of Risk Research, 17(8): 999-1017. https://doi.org/10.1080/13669877.2013.841725

[21] Zavalko, N.A., Kozhina, V.O., Kovaleva, O.P., Kolupaev, R.V., Lebedeva, O.Y. (2018). System approach to diagnostics and early prevention of a financial crisis at an enterprise. Journal of Applied Economic Sciences, 13(1): 84-88.

[22] Bobrova, N.M. (2014). Risk management planning, as a key element of the risk management system. Economics and Entrepreneurship, 11-3(52): 808-811. https://elibrary.ru/item.asp?id=22814181.

[23] Engalychev, O.V. (2004). Risk management: An important component of the corporate governance system. Gas Industry, 9: 70-71. https://elibrary.ru/item.asp?id=9136648.

[24] Kashinova, N.E. (2014). Identification and classification of risks as risk management tools in the anti-crisis management of a contemporary enterprise. Concept Scientific and Methodological Electronic Journal, 5: 101-105. http://e-koncept.ru/2014/14129.htm.

[25] Mayer, N.V. (2011). Risk management in the currency operations management system. Issues of Economy and Law, 33: 267-270. https://law-journal.ru/journal/5578.

[26] Petukhova, K.A. (2014). The practice of implementing risk management tools in public administration of foreign countries: Basic standards and local documents. Problems of Risk Analysis, 11(6): 6-21. https://elibrary.ru/item.asp?id=23052577.

[27] Polyakova, A.G. (2010). Non-financial risk management in the corporate governance system. Upravlenets. Ekonomika i Biznes, 5-6(9-10): 32-38. https://upravlenets.usue.ru/download/upravlenets_5_6_2010.pdf.

[28] Rodionov, A.S. (2020). Risk management, and risk of managing the creation of innovative products. Economy. Business. Banks, 10(48): 8-23. http://rimuniver.ru/?page_id=3631.

[29] Ukraintseva, I.V. (2015). Development of technology for categorizing foreign trade participants in the risk management system of the federal customs service of Russia. Bulletin of the Rostov State University of Economics (RINH), 2(50): 214-219. https://vestnik.rsue.ru/doc/vestnik/2(50)2015.pdf.

[30] Alhassan, A.M., Solovjeva, N.E., Bykanova, N.I. (2018). The analysis of the system of monitoring and forecasting of banking risks. Научный результат. Экономические исследования, 4(4): 66-73.

[31] Nemirova, G.I., Savelyeva, T.I. (2020). Significance assessment of the risk management system to improve the quality of customs service provision. Economic Consultant, 31(3): 42-52. https://doi.org/10.46224/ecoc.2020.3.3

[32] Syrova, T.N. (2020). Risk management of innovation activities in the conditions of the digital economy. In Digital Transformation of the Economy: Challenges, Trends and New Opportunities, pp. 306-311. https://doi.org/10.1007/978-3-030-11367-4_30

[33] Vovchenko, N.G., Andreeva, O.V., Orobinskiy, A.S., Sichev, R.A. (2019). Risk control in modeling financial management systems of large corporations in the digital economy. International Journal of Economics & Business Administration, 7(1): 3-15.

[34] Agamirova, E.V., Agamirova, E.V., Lebedeva, O.Y., Lebedev, K.A.E., Ilkevich, S.V. (2017). Methodology of estimation of quality of tourist product. Calitatea, 18(157): 82-84.

[35] Kozhevnikova, M.A., Kuznetsova, L.V., Shermazanova, S.V., Lopatinskaya, V.V., Shelygov, A.V. (2020). The improvement of approaches to service activities teaching. Journal of Environmental Management and Tourism, 11(6): 1508-1514. https://doi.org/10.14505/jemt.11.6(46).21

[36] Bykova, O.N., Repnikova, V.M., Starovoytov, V.G., Artamonova, K.A., Gavel, O.Y., Sharonin, P.N. (2021). Formation of the logistics services market for small and medium-sized businesses in the context of globalization. Academy of Strategic Management Journal, 20(1): 1-10.

[37] Fedulin, A.A., Chernaya, I.V., Orlova, E.Y., Avtsinova, G.I., Simonyan, T.V. (2020). Formation of approaches to environmental policy under conditions of digital economy. Journal of Environmental Management and Tourism, 11(3): 549-554. https://doi.org/10.14505//jemt.v11.3(43).06

[38] Markova, O.V., Zavalko, N.A., Kozhina, V.O., Panina, O.V., Lebedeva, O.Y. (2018). Enhancing the quality of risk management in a companyO. Revista Espacios, 39(48): 26.

[39] Tretyakova, G.V., Azarova, O.A., Levchenko, V.V., Meshcheryakova, O.V., Lebedeva, O.E. (2018). Economic prospects of balanced development of international relations. International Journal of Engineering and Technology (UAE), 7(4.38): 573-576.