Kiran Sood![]() | Ercan Özen*

| Ercan Özen*![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This paper aims to find out the benefits of ESG in the insurance sector for achieving sustainability. The authors conduct a systematic literature review (SLR) to find and evaluate the ESG in the insurance industry using the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) method. Integrating ESG and sustainable insurance is a potential new revenue stream for the insurance sector. All business operations of insurers and pension funds will be impacted by ESG factors and sustainable insurance, with investment activity, risk management, product management, and the valuation of assets and liabilities having the most effects. It has been noted from the body of literature that very few researches using the PRISMA and SLR approaches have been carried out in this area. The authors also conducted a comprehensive study that focuses on three separate topics: ESG and sustainability, ESG impact in the insurance industry, and ESG and insurance.

ESG, insurance, sustainability, PRISMA, systematic literature review

The insurance industry is a cornerstone of modern economies, providing individuals and businesses with financial protection against various risks. Over the years, this sector has undergone significant transformations, adapting to changing market dynamics, regulatory environments, and consumer preferences. One of the most notable developments in recent years has been integrating Environmental, Social, and Governance (ESG) principles into the insurance industry [1, 2]. It includes many elements beyond financial measures, such as social responsibility, corporate governance, and environmental sustainability. Across industries, this all-encompassing method of assessing company practices has gained traction as insurance firms increasingly acknowledge its importance [3]. Sustainability, social responsibility, and governance (ESG) issues are a major factor driving transformation in the insurance sector. Insurers are now aware of the critical role they can play in advancing sustainability and social responsibility, and they are no longer satisfied with merely managing risk. The realisation that traditional risk assessment is inadequate in a world dealing with social injustice, climate change, and changing governance practices is at the core of this shift. Incorporating ESG criteria provides insurers with a more comprehensive understanding of potential risks. Consider an insurance policy that offers a cheaper price to a plant that does not pollute the environment, or that offers better terms to a business that has strong cybersecurity procedures. This makes it possible to price risks more precisely while simultaneously encouraging sustainable activities. Incorporating ESG also helps insurers meet the increasing demand for ethical investing. Investors of today are becoming pickier, directing their money towards businesses that uphold ESG standards. Insurers become more appealing to these investors by showcasing a dedication to sustainability in their investing methods, guaranteeing a secure financial future. The advantages go beyond only financial gains. Policyholders are looking for insurance policies that align with their values as they become more socially and environmentally conscious. Insurers can meet this need by creating cutting-edge products, such as providing coverage for risks associated with climate change that homes confront or cyberattacks that target companies with inadequate data protection.

Sustainable finance and ESG concepts are familiar; they have been discussed for over 20 years [4, 5]. What makes today's discussion unique is that it has progressed to the point where a fundamental regulatory framework will be created, based on which the Paris Agreement on Climate Change and the climate change targets of the United Nations Sustainable Development Programme will be pursued in the years leading up to 2030. Over the past four years (2015-2019), specific initiatives have been taken in the EU to create rules that will serve as the foundation for incorporating ESG principles into the operations of financial institutions [6]. ESG (environmental, social, and governance) factors have grown significantly within the insurance sector in recent years. ESG refers to a collection of standards businesses and investors use to assess a company's overall governance practices and impact on the environment and society [7]. These standards are also used in the insurance industry and will significantly impact how the sector develops in the future [8].

There are three components of ESG [9]: 1. Environmental (E): This component focuses on the environmental impact of a corporation. It entails evaluating a company's initiatives to lessen its carbon footprint, sustainably manage natural resources, and eliminate environmental risks. Calls for assessing the climate-related risks to which insurance products and portfolios are subject [10], 2. Social (S): The social component of ESG considers a company's ties to its workers, clients, communities, and the larger society. Consumers increasingly expect insurance companies to promote ethical behavior, exhibit diversity and inclusion in their workforces, and give back to the communities where they do business. 3. Governance (G): A firm's management and governance are controlled by governance principles. It entails assessing the organization's board composition, executive compensation, openness, and general corporate governance practices. Strong governance in the insurance sector guarantees that policyholders are treated fairly, and risks are effectively managed [11]. The Environmental, Social, and Governance (ESG) factors are becoming more and more critical for the success and dependability of many firms, to the point where ESG analysis is now seen as an ad-hoc non-financial assessment with its own unique and growing relevance to have the scanning and valuation of corporate assets, and to check the extent to which the company complies with the peculiar normative and reputational needs.

As a result, the economy may be significantly impacted by the insurance industry's approach to sustainability [12]. The insurance industry, which oversees substantial investment amounts, has the potential to play a vital role in pushing the entire financial sector in the direction of a far more sustainable imprint.

Environmental, social, and governance (ESG) considerations are being incorporated into insurance company operations. This is taking into account variables such as an organization's social responsibility or environmental policies when evaluating risk. The integration of ESG data into current systems and maintaining uniform data collection practices between businesses present challenges. By overcoming these obstacles, a more thorough risk assessment is possible, and clients who care about the environment and society are drawn in. Important aspects to take into account for insurers aiming to effectively operationalize ESG include regulation and the long-term effects of things like climate change. Top insurance players are strategically positioned through several ESG-related initiatives, including medium-term goals, institutional communication, and management training. Italy's companies are increasingly committed to creating plans to incorporate ESG themes into their core businesses, to unusual sustainability-related initiatives and particular business management and market offer (insurance products and protection tools more generally) actions [13].

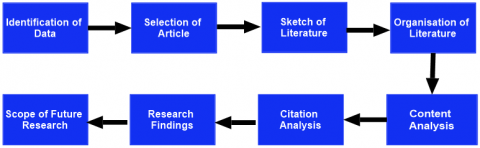

The research articles on the impact of the ESG directive on the insurance sector were reviewed as part of this study's systematic literature review method. The systematic approach, used to examine the literature on specific topics, can cover the entire body of literature pertinent to the field of study and explain how it works [14]. This study has included the "Systematic Literature Review" methodology. The best method to use when assessing the body of literature on a particular topic is a systematic literature review (SLR) [15-17]. The systematic review method can be divided into eight (08) steps [18], as described in the literature and shown in Figure 1.

2.1 Sample selection

Numerous searches in electronic databases were carried out to find the earlier studies that had been done in the insurance field. All studies conducted in the domain of ESG in the insurance industry make up the population. As a result, the following reputable electronic databases were searched for the analyses: Scopus, Web of Science, EBSCO, Emerald Insight, Oxford University Press, Taylor & Francis Group, JSTOR, Science Direct, Google Scholar, and conference papers and including grey literature (Appendix Table 2) and other unpublished literature in systematic reviews. These databases were chosen for the two main reasons mentioned below.

These are the top fifteen (15) journal publishers worldwide, which is the initial reason for this. The second reason is that replicate research studies are not published in these data banks, which only contain high-quality research publications. The searches in the above electronic databases used the term “ESG and Insurance sector." Further, only the peer-reviewed "Journal Articles" published in ESG directives in the insurance sector were considered for the sample selection.

Figure 1. Systematic review process

Source: [18]

Figure 2. Sample selection process

Source: Author Compilation

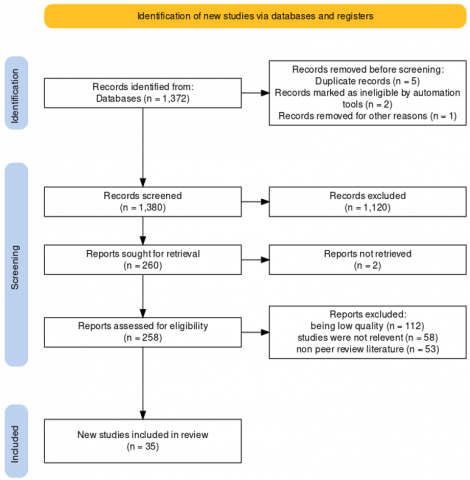

Five steps were used in the sample selection process (Figure 2). The search term "ESG in the Insurance sector" was used for the initial investigation. Based on the period, the following screening was performed. This analysis took into account the years 2013 through 2023. This time frame was chosen to examine the recent publications in this field. The search using the "field" was conducted after this. Under advanced search options, this search option is accessible. The screening results from steps one and two included numerous studies that needed to be more pertinent to the study under consideration. The screening for the abstract, title, or whole texts that contained these relevant studies was done in step three of the procedure. Step four only considered the research articles to which the authors had access. The studies that neared step four were then further examined to determine their applicability to the current investigation. The scope of the study did not include any trials that approached step 4. As a result, those studies were taken out of the sample. The sample selected through the above steps is thirty-five (35) research articles. The number of studies that were generated as a result of filtering via each of those above first four processes and the final sample that was chosen for each electronic data source are summarized in Table 1.

Table 1. Sample composition

|

Description |

No of Researches |

|

ESG and Insurance |

15 |

|

ESG impact on the Insurance sector |

12 |

|

ESG and Sustainability |

8 |

Source: Author Compilation

2.2 Prisma model

This study demonstrates how the minimum collection of topics to be studied in this systematic review was chosen using the PRISMA methodology. The graph below (Figure 3) shows the PRISMA Flow diagram created for this inquiry.

Figure 3. Sample characteristic (year of publication)

Source: Author Compilation

This section analyses the studies that met the eligibility requirements. To achieve the current study's goal, a thorough analysis of the findings from each study in the sample has been carried out under this section.

3.1 Sample composition

The chosen studies were divided into three (03) core categories for precise analysis.

ESG and Insurance

ESG impact on the Insurance sector

ESG and Sustainability

35 articles from each of the three categories of ESG and insurance. Fifteen (15) articles are accessible on ESG and Insurance, twelve (12) articles on ESG impact in the Insurance industry, and eight (8) articles on ESG and Sustainability.

3.2 Sample characteristics

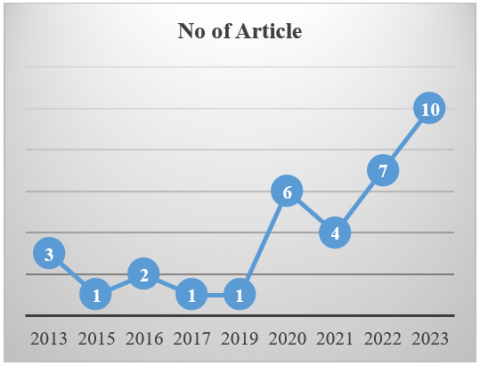

There are 35 participants in the study's sample (Appendix Table 3). The features of the sample were analyzed about three variables: Region, Year of publication, and Data collection method. Studies from the eleven period beginning in 2013 and ending in 2023 were used for this study. The year 2023 has seen the most publication activity out of the sample's 35 studies, with ten (10) studies published there. The years 2015, 2017, and 2019 have the lowest number of publications, which is one (01). The number of journals published during each year of the study's consideration period is shown in Figure 3.

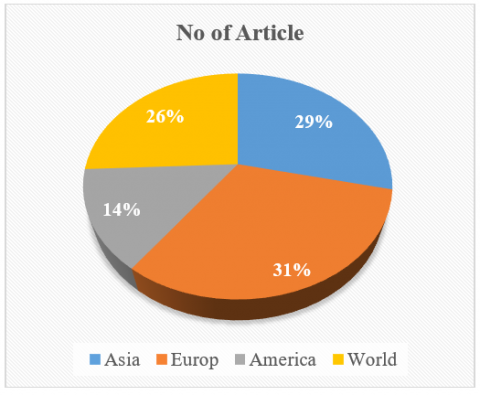

Figure 4. Sample characteristics (region wise)

Source: Author Compilation

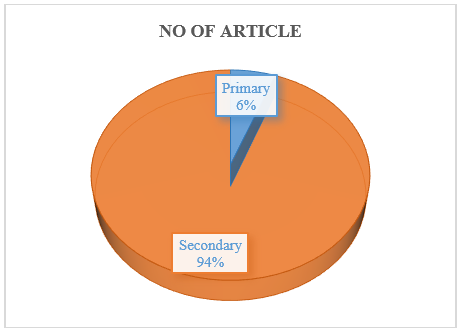

Figure 5. Sample characteristics (data collection method)

Source: Author Compilation

The sample comprises research from the entire world and studies from Asia, Europe, and America. The majority of the sampled studies are based in the continent of Europe. It represents 31% of the total. Figure 4 shows the distribution of the research by geographic region.

The data-collecting method is the third attribute examined in the sample analysis. In light of this, the sample was split into two groups: studies that used primary data gathering methods and studies that used secondary data collection methods. Of the sample's thirty-five (35) studies, 2 (two) were based on primary data collection methods. The secondary data gathering method was used in 33 (Thirty-two) studies shown in Figure 5. In contrast, surveys and interviews were used as the primary data collection methods in studies that have used it. Surveys and interviews have been combined as the main data-gathering methods in studies that use them.

3.3 Prisma model (Figure 6)

Figure 6. Prisma model

Source: Author Compilation

3.4 ESG and insurance

One of the main focuses of the research under ESG in the insurance industry is "ESG and insurance industry." Fifteen (15) studies were focused on ESG and the insurance industry. As the second-largest asset owner behind pension funds, insurance companies are anticipated to be a key player in the shift to a greener economy [19]. They can influence change through ethical operations and asset management. Still, they can encourage other companies and people by considering environmental, social, and governmental (ESG) aspects when underwriting. Insurance clients are at diverse stages of ESG maturity due to regulatory forces in various jurisdictions [20].

Environmental, social, and governance (ESG) factors demand more than just completing the minimum disclosure standards, according to a study [21] that focuses on the importance of ESG in the insurance business. Forward-thinking insurers are developing ESG strategies to include in every aspect of their business. The increasing demand for a clear position on how significant action will be taken, measured, and reported from insurance consumers, investors, boards, staff, and other ecosystem stakeholders adds to the pressure. Integrating an organization's mission, ESG initiatives, and business strategy results in successful value creation [22].

The ESG profile is created by combining the firm's level of ESG awareness, the method(s) by which the firm is integrating the ESG, and the firm's philosophy on ESG integration. The knowledge, preparedness, and potential of insurance firms in producing sustainable insurance are explored and examined in this study as indicators of sustainable insurance development in Indonesia [23].

Another author's empirical findings indicate the safest businesses supporting investment diversification and distinct relationships typical of tail contagion providers and receivers. The role of ESG Scores is then considered through (non-ESG related) assets, offering institutional investors and other financial market participants additional insights to develop better data-driven, actionable investment decisions and regulatory regulations [24].

In addition to those mentioned above, the research authors also present a paradigm for integrating ESG into benchmarks at different strategic levels, from the highest-level policy benchmark to the performance benchmark of individual allocations. They also emphasize the range of investing goals asset owners can pursue when integrating ESG and how they might reflect those goals using ESG benchmarks. Since benchmarks are used to define the underlying investable universe and serve as a performance yardstick across all asset management disciplines, including index-based, factor-based, and active management, as well as at various strategic levels, they find that incorporating ESG into benchmarks makes sense as a framework to achieve consistency [25].

A study by Apicella et al. [26] used a rigorous theoretical valuation framework for ESG reputation, which we define as the reputation or the increase in confidence brought about by having a good reputation as opposed to not having one when the ESG criteria are taken into account in the business analysis. The author uses explicitly behavioral finance models to model ESG reputational risk. The definition of the ESG reputational risk is based on subjective probabilities that are presented in a probability function based on the preferences of the possible trustees, such as actors or things that people might want to put their faith in. Calculating the sustainability premium or discount assesses the financial impact of an ESG investment's favorable or unfavorable reputation [26].

In Conclusion, the papers suggest that ESG factors influence the insurance sector in various ways, from risk analysis and underwriting to investment plans and client interactions. Insurance businesses are better equipped to negotiate the shifting environment of risks and possibilities in a changing world if they include ESG concepts in their business practices. The study highlights the crucial role of the insurance industries in accepting and transmitting changes related to sustainable development, including climate risk, and the need for the insurance industry to integrate ESG factors into underwriting activities and manage sustainability issues effectively.

3.5 ESG impact in the insurance sector

The environment for the insurance sector is evolving as environmental, social, and governance (ESG) considerations assume more significance. Stakeholders are pressuring insurers to address ESG risks as they grow in number and severity. ESG factors have a variety of effects on the insurance sector. For instance, climate change is making natural disasters more frequent and severe, which could result in more significant claims expenses. Social hazards like inequality and demographic change can also impact the demand for insurance goods and services.

Additionally, governance risks like fraud and corruption can jeopardize the financial viability of insurance. Insurers are progressively incorporating ESG into their operational procedures to address these issues. ESG-friendly products and services must be created, ESG risks must be evaluated and managed, and sustainable asset investments must be made. To improve their underwriting decisions, insurers are increasingly using ESG data. For instance, insurers might be more inclined to approve business plans for enterprises making efforts to lessen their environmental impact. Although the adoption of ESG in the insurance sector is still in its infancy, it has a significant influence. The shift to a more sustainable economy will benefit insurers on the cutting edge of ESG. Insurance businesses have been impacted by it because it offers risk reduction, cost reduction, etc. It is advised that the insurance industry in developing nations adopt ESG practices to be used globally, and small and midcap enterprises can also profit from them [27, 28].

ESG factors are increasingly impacting the insurance industry, affecting all aspects of the business. Insurers are integrating ESG into their underwriting, investment, customer engagement, and regulatory strategies.

Underwriting decisions are being made based on ESG performance, ESG data is being used to assess risks, and unsustainable assets are being diverted. ESG-themed products and services are being offered, and customers are being educated about ESG risks. Regulators also require insurers to disclose their ESG performance and encourage them to invest in sustainable assets and develop ESG-friendly products and services.

The overall implications of ESG for the insurance industry are significant. Insurers who fail to integrate ESG into their business practices face higher costs, more significant risks, and losing customers. Insurers ahead of the curve on ESG are well-positioned to benefit from the transition to a more sustainable economy.

3.6 ESG and sustainability

ESG and sustainability are closely related concepts [29]. ESG stands for environmental, social, and governance. At the same time, sustainability refers to the ability to meet the needs of the present without compromising the ability of future generations to meet their own needs [30].

ESG factors can have a significant impact on sustainability. For example, climate change is an essential environmental risk, and social inequality can lead to social unrest [10]. Good governance is critical for ensuring that resources are used sustainably.

ESG integration can help businesses to become more sustainable. For example, by investing in renewable energy and reducing their environmental impact, companies can reduce their carbon footprint and mitigate climate change risks. Businesses can create a more equitable and sustainable workforce by promoting diversity and inclusion. By implementing good governance practices, companies can ensure they use resources responsibly and ethically. There is a growing demand for sustainable products [31] and services from consumers and investors [32]. Businesses demonstrating their ESG performance are well-positioned to meet this demand and achieve long-term success.

Businesses committed to ESG and sustainability are better positioned to succeed long-term. By addressing ESG risks and investing in sustainable practices, companies can reduce costs, improve their reputation, and attract and retain top talent.

AlQubaisi and Nobanee [33] show that the link between the three sustainability scores (environmental, social, and governance) and insurance business stability was used to quantify the impact of sustainability. The effect of sustainability was evaluated by looking at the relationship between the strength of the insurance industry and the three sustainability scores (environmental, social, and governance).

The author discusses the problems of figuring out how insurance companies might manage their sustainable development using an ESG-driven approach. The Company ESG Risk Ratings (Sustainalytics) is the most appropriate rating for determining whether insurance companies can apply an ESG-driven approach to managing their sustainable development, according to the results of a comparison analysis of six ESG Ratings according to four main criteria (dependent variables, independent variables, scale type, sample) [34].

Scordis et al. [35] found that the recently adopted Principles for Sustainable Insurance (PSI) are being aggressively pursued by some of the biggest insurers in the world. Although a governance structure that prioritizes stakeholder value is frequently related to the concept of sustainability, the PSI does not seem to be an appeal for insurers who prioritize stakeholder interests. The PSI is about internalizing covert claims in insurers' business practices. According to conceptual and empirical research on maximizing shareholder value, the value to shareholders improves when an insurer honors its implicit claims. According to tradition and practice, the earnest pursuit of the PSI will broaden the scope of corporate risk management, which is a fundamental insight.

Determine whether ESG scores indicate an insurer's financial strength and market success because the expanding ESG issues across all economic sectors represent significant problems for insurance companies. Overall, the relevance of sustainable insurers for converting the entire economy to ESG should always be considered when making changes to the taxes of insurance businesses.

Sustainability indeed refers to constant welfare, ideally increasing, as well as the possibility of leaving behind a standard of living that is at least comparable to what it appears to be now. The level of occupancy of individuals is taken into account from three essential perspectives: governance, social issues, and the environment. Sustainability is thus no longer just an ethical issue; it has also emerged as a crucial economic aspect, making it a goal for all businesses, regardless of size. It has also emerged as a factor that helps companies to become more competitive and stand out in the market. Consumers, investors, and operators, among others, drive the market's demand that companies adopt sustainability practices. Sustainability is a differentiator in consumer purchasing decisions, investment, and financing.

The importance of insurance companies as crucial medium- to long-term institutional investors and as physiological and structural "wealth and protection providers" is on the rise. Therefore, the insurance industry already plays a significant role in sustainable financing [36]. Customer preferences do include ESG policies. Banks, insurers, pension funds, and investment companies will increasingly integrate sustainable financing into operational procedures. ESG and sustainable insurance integration are seen as a potential new source of income for the insurance industry [6]. ESG considerations and sustainable insurance will impact all business operations of insurers and pension funds, with investment activity, risk management, product management, and the valuation of assets and liabilities having the most impact. In Conclusion, insurers and pension funds must incorporate ESG concepts into their operational procedures.

Environmental, social, and governance (ESG) considerations are leading the way in the insurance industry's transformation. But how can insurers make their way through this new environment and incorporate ESG into their operations? This essay provides practitioners with practical steps to adopt sustainability and realise the full potential of ESG.

Recognising the value of ESG in risk assessment is the first step. Conventional approaches may ignore important details. An example of a factory with inadequate environmental procedures is one that is more vulnerable to climate-related disasters, which increases insurance risk. Insurers may provide a more accurate price and a more comprehensive picture of potential risks by adding ESG data. This helps the financial line of the organisation and encourages others to use sustainable business methods.

Secondly, integrating ESG aligns your investment strategy with the growing demand for responsible investing. Investors are increasingly selective, channelling funds towards companies committed to ESG principles. By demonstrating your commitment to sustainability through your investment choices, you become more attractive to these investors, ensuring a stable financial future for your company.

Meeting the increasing demand for ESG-aware products is the next stage. Customers are looking for insurance that aligns with their values as they become more socially and environmentally concerned. Create cutting-edge solutions such as cyber insurance for companies with strong cybersecurity or risk coverage connected to climate change for homes. These goods encourage companies to give environmental sustainability a higher priority by drawing in eco-aware consumers.

ESG integration is not without its difficulties, though. Data may be inconsistent and dispersed. Establish standardised procedures for gathering and reporting ESG data by working with data providers and prominent members of the industry. By doing this, the accuracy of the data needed to evaluate risk and make investment decisions is guaranteed.

Lastly, dedicate yourself to continuous education. New approaches are continually emerging as the field of ESG analysis continues to evolve. Invest in educating your employees about risk assessment and ESG factors. This gives your team the ability to decide using the most recent facts and techniques.

Insurance professionals can lead towards a more sustainable future by taking these steps. Including ESG means more than just being environmentally conscious—it means building a more prosperous and secure future for the insurance sector as a whole. Accept the shift, and establish yourself as a sustainability leader, and help your insurance business achieve the full benefits of ESG.

In the study "ESG in the Insurance Industry: Navigating the Path to Sustainability," the expanding significance of environmental, social, and governance (ESG) considerations in the insurance sector is examined.

6.1 Theoretical implication

Extending Risk Assessment Frameworks: The study advances the theory of sustainable insurance practices by highlighting the limitations of approaches used to analyse ESG data in the context of insurance risk assessment. This closes a critical gap in current ESG research and expands the scope of risk analysis beyond traditional financial considerations to a more holistic approach.

Sustainable Insurance Practices: The study shows the potential of ESG for risk management and investment strategies, suggesting that integrating ESG can benefit both insurers and society at large.

Methodological Challenges in ESG Data Analysis: The paper identifies a critical gap in current ESG research by highlighting the limitations of methodologies used to analyze ESG data in the context of insurance risk assessment. This opens new avenues for research on developing robust methodologies for effective ESG analysis.

6.2 Practical implication

Improved Risk Management: For insurance companies, the paper offers practical guidance on incorporating ESG factors into risk assessment processes. This can lead to more accurate risk pricing, improved underwriting decisions, and ultimately, better financial performance.

Development of ESG-based Insurance Products: By identifying the growing demand for ESG-conscious products, the paper encourages insurers to develop innovative products that cater to this demand. Examples include climate-related risk coverage or cyber insurance for businesses with strong data security practices.

Collaboration for Data Standardization: The paper emphasizes the need for collaboration between insurers, data providers, and regulators. This collaboration can lead to standardized ESG data collection and reporting practices, improving the reliability and consistency of ESG data used by insurers.

Investment Strategies Aligned with Sustainability: The paper highlights the alignment between ESG integration and responsible investment strategies. This can guide insurers in making investment decisions that promote sustainability while ensuring a healthy financial future.

There are many difficulties in operationalizing ESG in the insurance industry, especially when it comes to data limits. ESG data may not be standardised across sources and may be unreliable and fragmented. Conclusions that may affect the result of this discrepancy's erroneous risk estimates.

Data Quality and Availability: The range of analysis may be limited by the scarcity of high-quality ESG data. Businesses might not provide ESG measures on a regular basis, or the data they report could be inaccurate. This can impede efficient risk management and result in biased findings.

Inconsistent Metrics and Definitions: It is challenging to make comparisons between industries because ESG metrics are not standardised. For instance, depending on the industry, "environmental sustainability" may mean different things. This discrepancy may cause evaluations of a company's actual ESG performance to be erroneous.

Limitations in Data Analysis Methodologies: As of right now, there isn't a single, widely recognised technique for evaluating ESG data in relation to insurance risk assessment. The methods selected can have a big impact on the findings and recommendations made.

Kiran Sood: Postdoc Researcher, University of Uşak, Faculty of Applied Sciences, Department of Finance and Banking, 64200 Uşak, Turkiye.

Ercan Özen: Supervisor, University of Uşak, Faculty of Applied Sciences, Department of Finance and Banking, 64200 Uşak, Turkiye.

This paper is derived from Postdoc research under supervision of Prof. Dr. Ercan Özen, who is member of Usak University, Faculty of Applied Sciences, Department of Finance and Banking, Uşak, Turkiye.

Appendix Table 2. Grey literature detail

|

Sr. No. |

Who |

When |

What |

Publisher Information |

DOI or URL |

|

1 |

Sood & Bak |

May, 2023 |

The insurance industry’s path to ESG impact |

Deoitte, Canada |

“https://www2.deloitte.com/content/dam/Deloitte/ca/Documents/financial-services/EN_FSI_Insurance_ESG_POV_V6_AODA.pdf” |

|

2 |

Hannah Tichansky |

July 7, 2021 |

Unpacking The Sec’s Speech on Environmental, Social, Governance (Esg) Initiatives |

Aravo Solution, San Francisco, Usa |

https://aravo.com/blog/sec-speech-on-environment-social-governance-esg-initiatives/ |

|

3 |

Jeannette Mitchell, Xavier Crepon, Marie Carr |

2022 |

ESG: A Growing Sense of Urgency |

Pwc, USA |

“https://www.pwc.com/us/en/industries/financial-services/library/next-in-insurance-top-issues/esg-insurance-industry.html” |

|

4. |

Petra Hielkema |

August 29, 2023 |

Insured Risks in Uncertain Times |

European Insurance and Occupational Pensions Authority (Eiopa), Germany |

https://www.eiopa.europa.eu/keynote-speech-croatian-financial-services-supervisory-authority-hanfa-conference-insured-risks-2023-08-29_en |

|

5 |

Daniel Wang |

November 15, 2023 |

Crisis To Collaboration: Insurance Supervisory Developments on Climate Change |

Monetary Authority of Singapore, Singapore |

https://www.mas.gov.sg/news/speeches/2023/crisis-to-collaboration---insurance-supervisory-developments-on-climate-change |

|

6 |

Tom Karol |

June 2019 |

Environmental, Social, And Governance Considerations for Property/Casualty Insurance |

National Association of Mutual Insurance Companies, USA |

https://www.namic.org/pdf/19memberadvisory/190617_ESGTK_v2FINAL.pdf |

|

7 |

|

|

How insurance boards are elevating sustainable finance and ESG |

Ernst & Young Global Limited, UK |

file:///C:/Users/Divya/Downloads/ey-how-insurance-boards-are-elevating-sustainable-finance-and-esg.pdf |

|

8 |

Shantanu Srivastava |

February 11, 2022 |

IEEFA: Life Insurance Corporation of India’s ESG push |

Institute for Energy Economics and Financial Analysis, India |

https://ieefa.org/resources/ieefa-life-insurance-corporation-indias-esg-push |

|

9 |

Patrick McGeever, Elizabeth Henderson, Dan Byrnes, Marco Bravo, Peter Wirtala, CFA |

September 8, 2021 |

What is ESG? Why It’s Important for Insurance Companies and the Solutions Aam Provides |

AAM, USA |

https://www.aamcompany.com/podcasts/what-is-esg-why-its-important-for-insurance-companies-and-the-solutions-aam-provides/ |

|

10 |

Charlotte Gerken |

March 2, 2022 |

PRA’s supervisory priorities for the insurance in 2022 |

Bank of England, England |

“https://www.bankofengland.co.uk/speech/2022/march/charlotte-gerken-speech-at-norton-rose-fulbright-llp-pra-priorities-for-the-insurance-sector” |

|

11 |

Sheldon Mills |

May 13, 2022 |

“Insurance Brokers: Serving Consumers and Businesses in Times of Uncertainty and Change” |

Financial Conduct authority, England |

https://www.fca.org.uk/news/speeches/insurance-brokers-serving-consumers-and-businesses-times-uncertainty-and-change |

|

12 |

Brand Connect Initiative, Gautam Boda Read more |

Oct 10, 2023 |

The Volte-Face of Insurance Industry with Sustainability & ESG |

Economic Times, India |

https://bfsi.economictimes.indiatimes.com/blog/the-volte-face-of-insurance-industry-with-sustainability-esg/104312662#:~:text=The%20integration%20of%20ESG%20criteria,more%20stable%20and%20profitable%20business. |

|

13 |

ESG Matters Asia |

October 4, 2023 |

Navigating The Future of Insurance: ESG, Digitalisation, and Lessons from Aviva |

LinkedIn, USA |

https://www.linkedin.com/pulse/navigating-future-insurance-esg-digitalisation-lessons-from/?trk=article-ssr-frontend-pulse_more-articles_related-content-card |

|

14 |

Nina Jais, Ravi Malhotra |

Nov 3, 2021 |

Sustainability & ESG: A Strategic Resilience Guide for Insurance |

Accenture, Ireland |

https://insuranceblog.accenture.com/sustainability-esg-strategic-guide-for-insurers |

|

15 |

JAY D'APRILE |

November 2023 |

Embracing Sustainability: Why the Future of Insurance is Green |

Slaytan Search partners, USA |

https://www.slaytonsearch.com/2023/11/why-is-sustainability-in-insurance-so-important/ |

Appendix Table 2. Literature review

|

Sr. No. |

Author/s and Year of Publication |

Finding |

Title |

Journal/Book Series/Book/Chapter |

Sample From |

Total Citation |

|

1 |

Das (2013) [37] |

According to the study, compared to life insurance businesses, non-life insurance companies disclosed much less social information. Additionally, compared to other corporations, public life insurers announced noticeably more social news, according to the study. |

“Corporate social reporting and human resource disclosures: experiences from insurance companies in India” |

Social Responsibility Journal |

India |

38 |

|

2 |

Najjar & Salman (2013) [38] |

This finding demonstrates the long-term value of sound governance practices for both the company and the economy as a whole. |

“The Impact of Corporate Governance on the Insurance Firm’s Performance in Bahrain” |

International Journal of Learning & Development |

Bahrain |

108 |

|

3 |

Pasquini-Descomps & Sahut (2013) [39] |

To conclude, it is beneficial for firms to improve their ESG ratings as this could increase their return on assets. |

“ESG Impact on a Firm’s Performance in Switzerland” |

Working Paper |

Switzerland |

10 |

|

4 |

Raggi & Paglicci (2015) [17] |

After analyzing how ESG indicators affect the healthcare industry and the related insurance and reinsurance companies, the next step would be to apply the ESG performance scorecard to all the companies and analyze the connected trend to give specific and exemplary judgments to companies and their CEOs to be sustainable. |

“Healthcare and insurance companies: how ESG scorecards can be a sustainable solution for both” |

SSRN |

World |

1 |

|

5 |

Ashwin Kumar et al. (2016) [40] |

The author comes to the conclusion that ESG elements have varying effects on different industries and that ESG businesses have higher profits. |

ESG factors and risk-adjusted performance: a new quantitative model |

Journal of Sustainable Finance & Investment |

World |

246 |

|

6 |

Maftuchah (2018) [23] |

Insurance companies might more precisely assess the ESG risk if they had a deeper comprehension of sustainable finance concepts. |

Corporate ESG Profile on Performance: Evidence from the Indonesian Insurance Industry |

Indonesia Financial Service Authority |

Indonesia |

1 |

|

7 |

UNEP (2012) [41] |

Underwriters of insurance and reinsurance can evaluate ESG practices in delicate industries and business segments with the use of SCOR's rating grid. |

Principles for Sustainable Insurance |

UNEP |

|

18 |

|

8 |

Chen et al. (2019) [42] |

Maintaining the bottom line of system financial hazards requires early prevention and control, particularly with regard to the high leverage ratio of green projects, capital idle, and "washing green," among other issues. |

Research On Institutional Innovation Of China’s Green Insurance Investment |

Journal of Industrial Integration and Management |

China |

19 |

|

9 |

Gatzert et al. (2020) [43] |

Though the author does not find evidence to support the idea that one ESG dimension is dominating, there is a positive association between ESG and multiple corporate financial performance indicators. |

Sustainability risks & opportunities in the insurance industry |

Zeitschrift für die gesamte Versicherungswissenschaft |

Europe |

26 |

|

10 |

Khovrak (2020) [34] |

The study organises insurance companies' best practices for managing their sustainable development through the application of an ESG-driven methodology. It emphasises how insurance companies must enhance their disclosure and reporting procedures in order to advance the ESG-driven approach. |

ESG-driven approach to managing insurance companies’ sustainable development |

Insurance Markets and Companies |

World |

14 |

|

11 |

Pfeifer (2021) [44] |

The researcher talked about metrics that investors use to assess the risk and sustainability of their investments. |

The European way to sustainable insurance - the ESG Challenge |

ASTIN Online Colloquium |

Europe |

2 |

|

12 |

Santamaria et al. (2021) [13] |

The findings indicate that integrated reporting was a highly significant factor in generating a high ESG score and that three path types were driving the ESG score. |

Non-financial strategy disclosure and environmental, social, and governance score: Insight from a configurational approach |

Business Strategy and the Environment |

Italy |

52 |

|

13 |

Dimitrov (2020) [6] |

The study's findings are that adopting ESG principles in the business processes of insurers and pension funds is necessary. |

Integration of environmental, social, and governance principles in pension funds and insurance companies activities |

VUZF Review |

European Union |

3 |

|

14 |

Chiaramonte et al. (2020) [30] |

Researchers discovered a more robust correlation with life insurance. Endogeneity, enterprise heterogeneity, and any biases in sample selection do not affect our results. |

Sustainability Practices and Stability in the Insurance Industry |

Sustainability |

USA |

3 |

|

15 |

Dimson et al. (2020) [16] |

The authors believe that ESG ratings alone are not expected to have a significant impact on portfolio results. |

Divergent ESG Ratings |

The Journal of Portfolios Management |

world |

223 |

|

16 |

Hindkjaer & Slettan (2020) [45] |

The findings support the hypothesis that a firm's ESG performance has an insurance-like impact by demonstrating a strong correlation between the banks' overall ESG performance and fewer negative anomalous returns in the context of a corporate scandal. |

The insurance value of ESG performance: An Event Study of European Banking Scandals |

Copenhagen Business School |

Europe |

0 |

|

17 |

Park & Jang (2021) [46] |

The study's findings demonstrate that institutional investors give environmental and governance factors a higher priority than social factors. |

The impact of ESG management on investment decision: Institutional investors’ perceptions of country-specific ESG criteria |

International Journal of Financial Studies |

Korea |

87 |

|

18 |

Kaur et al. (2023) [47] |

The authors defined sustainability as an ethical question and an important economic variable. |

Sustainable solutions for insurance and risk management |

The Impact of Climate Change and Sustainability Standards on the Insurance Market |

European Union |

4 |

|

19 |

Xu & Zhao (2022) [48] |

The findings demonstrate that D&O insurance considerably raises the ESG performance of businesses. |

Can directors’ and officers’ liability insurance improve corporate ESG performance? |

Frontiers in Environmental Science |

China |

2 |

|

20 |

Huang & Lu (2022) [49] |

The author's findings suggest that providing voluntary ESG disclosure is only sometimes correlated with better ESG performance. We find that firms with better gender pay gaps are likelier to have worse Asset4 social scores, which rely heavily on voluntary disclosure. |

ESG Performance and Voluntary ESG Disclosure: Mind the (Gender Pay) Gap |

SSRN |

UK |

12 |

|

21 |

Gatzert & Reichel (2022) [50] |

According to observations made by researchers, insurers are becoming more sophisticated in their investment plans. In the future, it is probable that insurance companies would implement various systems rather than just excluding some sectors. |

Sustainable investing in the US and European insurance industry: a text mining analysis |

The Geneva Papers on Risk and Insurance - Issues and Practice |

USA & Europe |

4 |

|

22 |

Brogi et al. (2022) [51] |

The author discovers that the insurance companies with the highest level of ESG awareness are the larger, more profitable, and more solvent ones. |

Determinants of insurance companies' environmental, social, and governance awareness |

Corporate Social Responsibility and Environmental Management |

USA |

13 |

|

23 |

Özer et al. (2022) [52] |

The researcher discovers that monetary holdings that are higher, lower, or smaller are non-life and have no environmental, social, or governance (ESG) scores. If insurance companies are non-life, have more intangibles, cash flow, and profitability, and lack ESG rankings, they are more likely to be acquired. |

Determine Determinants of Becoming An M&A Acquirer or Target: Evidence from The US Insurance Industry. |

Journal of Capital Markets Studies |

USA |

0 |

|

24 |

Tong (2022) [53] |

Catastrophe insurance development adheres to the ESG development idea and incorporates the environment, society, and governance. In addition, it contributes to the growth of the green economy, green finance, and green insurance as a component of green insurance. |

China “Catastrophe Insurance: A Boost to Green Insurance Development Under ESG Concept” |

Academic Journal of Business & Management |

China |

0 |

|

25 |

Fianu (2021) [24] |

The empirical results of the study identify the safest companies that support investment diversification and demonstrate numerous links typical of givers and receivers of tail contagion. |

Understanding Environmental, Social and Governance (ESG) contributions in the downside systematic and systemic risk measurement of the insurance sector |

Social and Governance (ESG) Contributions in the Downside Systematic and Systemic Risk Measurement of the Insurance Sector |

World |

1 |

|

26 |

Eisenkopf et al. (2023) [54] |

The study's conclusions are consistent with the idea that ESG stocks reduce risk during major emergencies and offer some insurance. |

“Responsible Investment and Stock Market Shocks: Short-Term Insurance Without Persistence” |

British Journal of Management |

European Union |

1 |

|

27 |

Di Tommaso & Mazzuca (2023) [55] |

The study's findings indicate that ESG ratings are crucial to insurance companies' pricing strategies and that an upgrade raises stock prices while a downgrade lowers them. The Pre-Paris period shows that the market is especially sensitive to changes in ESG ratings, indicating that these changes can have a big impact on the efficiency and equilibrium of the stock market. |

“The stock price of European insurance companies: What is the role of ESG factors?” |

Finance Research Letters |

Europe |

1 |

|

28 |

Otavova et al. (2023) [56] |

The study found that non-financial reporting increased both in insurance companies required to report non-financial information and in insurance companies not required to do so following the Directive's introduction. |

Social Responsibility for Insurance Companies |

Montenegrin Journal of Economics |

Czech Republic |

1 |

|

29 |

Bressan (2023b) [15] |

High ESG insurers are less profitable than low ESG insurers and pay more taxes, according to the author. |

ESG, Taxes, and Profitability of Insurers |

Preprints |

Korea |

0 |

|

30 |

Bressan (2023) [57] |

The findings indicate a relationship between the metrics used to track financial strength and ESG rankings. According to the author, more sustainable insurance portfolios produce greater abnormal returns. This leads us to the conclusion that sustainable insurers add a significant amount of value for shareholders. |

Effects from ESG Scores on P&C Insurance Companies |

Sustainability |

World |

1 |

|

31 |

Tang et al. (2023) [58] |

A favourable correlation between ESG performance and D&O insurance. This study adds to the body of research on the financial advantages of D&O insurance by presenting preliminary data suggesting that the policy may strengthen corporate governance and boost ESG performance. |

Does Directors' and Officers' Liability Insurance Improve Corporate ESG Performance? Evidence From China |

International Journal of Finance & Economics. |

China |

0 |

|

32 |

Van Roosebeke & Defina (2023) [20] |

Over the next two years, ESG issues, according to 60% of deposit insurers, will become more significant for their core operations. |

ESG and Deposit Insurance: Taking Stock and Looking Ahead |

International Association of Deposit |

World |

3 |

|

33 |

Moalla & Dammak (2023) [59] |

The results imply that stock price volatility is lower for companies with strong ESG performance than for those with weak ESG performance. |

“Corporate ESG Performance as Good Insurance in Times of Crisis: Lessons from Us Stock Market During Covid-19 Pandemic” |

Journal of Global Responsibility |

USA |

5 |

|

34 |

Apicella et al. (2023) [26] |

In order to quantify the financial impact of a positive or negative reputation resulting from ESG investments, the author calculates the sustainability premium or discount. The impact of policyholder trust on the insurer's commitment to ESG investing is the first key result to be discussed. |

Policyholders’ subjective beliefs: approaching new drivers of insurance ESG reputational risk |

SSRN |

World |

0 |

|

35 |

Li & Zhu (2023) [60] |

High contribution rates have a substantial negative impact on ESG performance, and robustness tests confirm our findings. We see that the relationship between ESG and the pension insurance contribution rate is non-linear. |

Pension Insurance Contributions and ESG Performance: Evidence from China |

SSRN |

China |

0 |

[1] Shalender, K., Singla, B., Sharma, S. (2023). Adoption of ESG by the insurance industry: Conceptual framework and future recommendations. In the Impact of Climate Change and Sustainability Standards on the Insurance Market (1st ed). Wiley. https://doi.org/10.1002/9781394167944.ch22

[2] Saraçlı, S., Tunca, B., Gül, I., Arı, E., Villi, B., Berk, B.I., Berk, I., Boca, G.D. (2023). Modeling the influences on sustainable attitudes of students towards environmental challenges: A partial least squares-structural equation modelling approach. Opportunities and Challenges in Sustainability, 2(3): 161-171. https://doi.org/10.56578/ocs020305

[3] Celik, I.E. (2023). Impact of sustainability reporting on financial performance. Opportunities and Challenges in Sustainability, 2(1): 23-29. https://doi.org/10.56578/ocs020103

[4] Migliorelli, M. (2021). What do we mean by sustainable finance? Assessing existing frameworks and policy risks. Sustainability, 13(2): 975. https://doi.org/10.3390/su13020975

[5] Ziolo, M., Filipiak, B.Z., Bąk, I., Cheba, K. (2019). How to design more sustainable financial systems: The roles of environmental, social, and governance factors in the decision-making process. Sustainability, 11(20): 5604. https://doi.org/10.3390/su11205604

[6] Dimitrov, S. (2020). Integration of environmental, social and governance principles in pension funds and insurance companies activities. VUZF Review, 5(3): 31-39. https://doi.org/10.38188/2534-9228.20.3.04

[7] Tarmuji, I., Maelah, R., Tarmuji, N.H. (2016). The impact of environmental, social and governance practices (ESG) on economic performance: Evidence from ESG score. International Journal of Trade, Economics and Finance, 7(3): 67. https://doi.org/10.18178/ijtef.2016.7.3.501

[8] Arslan, M., Kekeç, H.M. (2023). Health financing in the pursuit of sustainable development goals: An examination of global averages and Turkey's position. Opportunities and Challenges in Sustainability, 2(3): 141-147. https://doi.org/10.56578/ocs020303

[9] Limkriangkrai, M., Koh, S., Durand, R.B. (2017). Environmental, social, and governance (ESG) profiles, stock returns, and financial policy: Australian evidence: ESG profiles, returns, and financial policy. International Review of Finance, 17(3): 461-471. https://doi.org/10.1111/irfi.12101

[10] Kumar, S., Raheja, K., Dhiraj, A. (2023). Environment education and insurance awareness - A boon to indian insurance sector. In the Impact of Climate Change and Sustainability Standards on the Insurance Market (1st ed). Wiley. https://doi.org/10.1002/9781394167944.ch20

[11] Najjar, N. (2013). The impact of corporate governance on the insurance firm’s Performance in Bahrain. International Journal of Learning and Development, 2(2): 1-17. https://doi.org/10.5296/ijld.v2i2.1412

[12] Almajali, A.Y., Alamro, S.A., Al-Soub, Y.Z. (2012). Factors affecting the financial performance of Jordanian insurance companies listed at Amman Stock Exchange. Journal of Management Research, 4(2): 266-289. https://doi.org/10.5296/jmr.v4i2.1482

[13] Santamaria, R., Paolone, F., Cucari, N., Dezi, L. (2021). Non-financial strategy disclosure and environmental, social and governance score: Insight from a configurational approach. Business Strategy and the Environment, 30(4): 1993-2007. http://doi.org/10.1002/bse.2728

[14] Fink, A. (2019). Conducting Research Literature Reviews: From the Internet to Paper. Sage Publications.

[15] Bressan, S. (2023b). ESG, Taxes, and Profitability of Insurers.

[16] Dimson, E., Marsh, P., Staunton, M. (2020). Divergent ESG ratings. The Journal of Portfolio Management, 47(1): 75-87. https://doi.org/10.17863/CAM.55949

[17] Raggi, E., Paglicci, E. (2015). Healthcare and Insurance Companies: How ESG Scorecards can be a Sustainable Solution for Both.

[18] Kayani, U.N., De Silva, T.A., Gan, C. (2019). A systematic literature review on working capital management-An identification of new avenues. Qualitative Research in Financial Markets, 11(3): 352-366. http://doi.org/10.1108/QRFM-05-2018-0062

[19] Mills, E. (2009). A global review of insurance industry responses to climate change. The Geneva Papers on Risk and Insurance-Issues and Practice, 34(3): 323-359. https://doi.org/10.1057/gpp.2009.14

[20] Van Roosebeke, B., Defina, R. (2023). ESG and Deposit Insurance: Taking Stock and Looking Ahead.

[21] Sridharan, V. (2018). Bridging the disclosure gap: Investor perspectives on environmental, social & governance (ESG) disclosures. Social & Governance (ESG) Disclosures. https://doi.org/10.2139/ssrn.3180412

[22] Sood, S., Bak, C. (2023). The insurance industry’s path to ESG impact. https://www2.deloitte.com/content/dam/Deloitte/ca/Documents/financial-services/EN_FSI_Insurance_ESG_POV_V6_AODA.pdf.

[23] Maftuchah, I. (2018). Corporate ESG profile on performance: Evidence from Indonesian insurance industry. http://repository.crmsindonesia.org/handle/123456789/216.

[24] Fianu, E.S. (2021). Understanding environmental, social and governance (ESG) Contributions in the downside systematic and systemic risk measurement of the insurance sector. Social and Governance (ESG) Contributions in the Downside Systematic and Systemic Risk Measurement of the Insurance Sector (November 30, 2021).

[25] Giese, G., Lee, L.E., Melas, D., Nagy, Z., Nishikawa, L. (2019). Consistent ESG through ESG Benchmarks. The Journal of Beta Investment Strategies. https://jii.pm-research.com/content/early/2019/07/27/jii.2019.1.072.full.

[26] Apicella, G., Carannante, M., D’Amato, V. (2023). Policyholders’ Subjective Beliefs: Approaching New Drivers of Insurance ESG Reputational Risk.

[27] Singh, A., Bathla, G. (2023). Environmental, social, and governance (ESG) measures and their impact on insurance industry: A Global Perspective. In the Impact of Climate Change and Sustainability Standards on the Insurance Market. Wiley. https://doi.org/10.1002/9781394167944.ch27

[28] Kaur, S., Kumar, R., Singh, K., Huang, Y.L. (2024). Leveraging artificial intelligence for enhanced sustainable energy management. Journal of Sustainability for Energy, 3(1): 1-20. https://doi.org/10.56578/jse030101

[29] Clément, A., Robinot, É., Trespeuch, L. (2022). Improving ESG scores with sustainability concepts. Sustainability, 14(20): 13154. https://doi.org/10.3390/su142013154

[30] Chiaramonte, L., Dreassi, A., Paltrinieri, A., Piserà, S. (2020). Sustainability practices and stability in the insurance industry. Sustainability, 12(14): 5530. https://doi.org/10.3390/su12145530

[31] Hoffman, A.J. (2018). The next phase of business sustainability. Stanford Social Innovation Review, 16(2): 34-39. https://doi.org/10.2139/ssrn.3191035

[32] Uzsoki, D. (2020). Sustainable investing. International Institute for Sustainable Development. IISD.

[33] AlQubaisi, K., Nobanee, H. (2021). The impact of sustainability on performance of insurance companies.

[34] Khovrak, I. (2020). ESG-driven approach to managing insurance companies’ sustainable development. Insurance Markets and Companies, 11: 42-52. http://doi.org/10.21511/ins.11(1).2020.05

[35] Scordis, N.A., Suzawa, Y., Zwick, A., Ruckner, L. (2014). Principles for sustainable insurance: Risk management and value. Risk Management and Insurance Review, 17(2): 265-276. https://doi.org/10.1111/rmir.12024

[36] Sachs, J.D., Woo, W.T., Yoshino, N., Taghizadeh-Hesary, F. (2019). Importance of green finance for achieving sustainable development goals and energy security. Handbook of Green Finance: Energy Security and Sustainable Development, 10: 1-10.

[37] Das, S.C. (2013). Corporate social reporting and human resource disclosures: Experiences from insurance companies in India. Social Responsibility Journal, 9(1): 19-32. https://doi.org/10.1108/17471111311307796

[38] Najjar, N.J., Salman, R.A.M. (2013). The impact of corporate governance on the insurance firm’s performance in Bahrain. International Journal of Learning and Development, 3(2): 56-69. http://doi.org/10.5296/ijld.v3i2.3511

[39] Pasquini-Descomps, H., Sahut, J.M. (2013). ESG impact on a firm’s performance in Switzerland.

[40] Ashwin Kumar, N.C., Smith, C., Badis, L., Wang, N., Ambrosy, P., Tavares, R. (2016). ESG factors and risk-adjusted performance: A new quantitative model. Journal of Sustainable Finance & Investment, 6(4): 292-300. https://doi.org/10.1080/20430795.2016.1234909

[41] UNEP, F. (2012). Principles for sustainable insurance. Geneva: UNEP FI. https://www.unepfi.org/wordpress/wp-content/uploads/2017/09/EXTRANET-10-15-Butch-UNEP-FI-NA-members-meeting-PSI-Sep-2017-final.pdf.

[42] Chen, H., Yao, M., Chong, D. (2019). Research on institutional innovation of China’s green insurance investment. Journal of Industrial Integration and Management, 4(1): 1950003. https://doi.org/10.1142/S2424862219500039

[43] Gatzert, N., Reichel, P., Zitzmann, A. (2020). Sustainability risks & opportunities in the insurance industry. Zeitschrift Für Die Gesamte Versicherungswissenschaft, 109: 311-331. http://doi.org/10.1007/s12297-020-00482-w

[44] Pfeifer, D. (2021). The European way to sustainable insurance-The ESG challenge. https://www.staff.uni-oldenburg.de/dietmar.pfeifer/KeyNote_Pfeifer_ASTIN_2021.pdf.

[45] Hindkjaer, N.B., Slettan, A.M.N. (2020). The Insurance value of ESG performance: An event study of European banking scandals. https://research.cbs.dk/en/studentProjects/the-insurance-value-of-esg-performance-an-event-study-of-european.

[46] Park, S.R., Jang, J.Y. (2021). The impact of ESG management on investment decision: Institutional investors’ perceptions of country-specific ESG criteria. International Journal of Financial Studies, 9(3): 48. https://doi.org/10.3390/ijfs9030048

[47] Kaur, H., Sood, K., Yadav, U.S., Grima, S. (2023). Sustainable solutions for insurance and risk management. In The Impact of Climate Change and Sustainability Standards on the Insurance Market, pp. 359-372. https://doi.org/10.1002/9781394167944.ch23

[48] Xu, H., Zhao, J. (2022). Can directors’ and officers’ liability insurance improve corporate ESG performance? Frontiers in Environmental Science, 10: 949982. https://doi.org/10.3389/fenvs.2022.949982

[49] Huang, J., Lu, S. (2022). ESG Performance and Voluntary ESG Disclosure: Mind the (Gender Pay) Gap.

[50] Gatzert, N., Reichel, P. (2022). Sustainable investing in the US and European insurance industry: A text mining analysis. In the Geneva Papers on Risk and Insurance-Issues and Practice, pp. 1-37.

[51] Brogi, M., Cappiello, A., Lagasio, V., Santoboni, F. (2022). Determinants of insurance companies’ environmental, social, and governance awareness. Corporate Social Responsibility and Environmental Management, 29(5): 1357-1369. https://doi.org/10.1002/csr.2274

[52] Özer, G., Okur, N., Çam, İ. (2022). Determinants of becoming an M&A acquirer or target: Evidence from the US insurance industry. Journal of Capital Markets Studies, 6(2): 203-218. http://doi.org/10.1108/JCMS-04-2022-0014

[53] Tong, L. (2022). China catastrophe insurance: A boost to green insurance development under ESG concept. Academic Journal of Business & Management, 4(17): 11-19. https://doi.org/10.25236/AJBM.2022.041703

[54] Eisenkopf, J., Juranek, S., Walz, U. (2023). Responsible investment and stock market shocks: Short-term insurance without persistence. British Journal of Management, 34(3): 1420-1439. https://doi.org/10.1111/1467-8551.12664

[55] Di Tommaso, C., Mazzuca, M. (2023). The stock price of European insurance companies: What is the role of ESG factors? Finance Research Letters, 56: 104071. https://doi.org/10.1016/j.frl.2023.104071

[56] Otavova, M., Glaserova, J., Kova, I.H. (2023). Social responsibility for insurance companies. Montenegrin Journal of Economics, 19(2): 129-140. https://doi.org/10.14254/1800-5845/2023.19-2.11

[57] Bressan, S. (2023). Effects from ESG Scores on P&C Insurance Companies. Sustainability, 15(16), 12644.

[58] Tang, S., He, L., Su, F., Zhou, X. (2023). Does directors’ and officers’ liability insurance improve corporate ESG performance? Evidence from China. International Journal of Finance & Economics. https://doi.org/10.1002/ijfe.2849

[59] Moalla, M., Dammak, S. (2023). Corporate ESG performance as good insurance in times of crisis: Lessons from US stock market during COVID-19 pandemic. Journal of Global Responsibility, 14(4): 381-402. https://doi.org/10.1108/JGR-07-2022-0061

[60] Li, R., Zhu, Z. (2023). Pension insurance contributions and ESG performance: Evidence from China. Finance Research Letters, 55: 103940.