Alla Abramova* | Anton Chub | Dmytro Kotelevets | Oleksandr Lozychenko | Kateryna Zaichenko | Oleksandr Popov

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The scientific research is devoted to the development of methodological proposals for assessing the effectiveness of tax revenues of the countries of Eastern Europe through the system of economic indicators, the presentation of measures of the regulatory impact of increasing tax revenues in the future and strengthening the economic security of the countries. The methodological basis of the study is a comprehensive approach, thanks to which the tasks and tools of the regulatory policy are established through the prism of the components of tax security of Eastern European countries. The methodological toolkit for assessing the effectiveness of tax revenues in the system of regulatory policy in the direction of guaranteeing the economic security of the state provided for the following stages: collection of economic data, selection of analysis indicators, assessment methods and determination of the system of stimulating and destructive factors influencing the volume of tax payments. Having carried out the analysis, the author's vision of priority tasks and tools of regulatory influence on tax revenues with the aim of increasing the level of economic security of Eastern European countries is presented.

economic security, tax security, tax revenues, tax risks, regulatory policy, regulatory tools

The priority of each country today is economic security, which is based on sustainable economic growth, stable growth of national income, strong investment and innovative production potential, effective social and migration policy focused on a high standard of living and meeting development needs. Regulatory policy, determined by individual geopolitical, socio-economic and cultural features, acts as a means of ensuring economic security in the field of tax relations. The complexity of the declared relations and the mechanism of making tax payments is naturally influenced by endo- and exogenous factors, causing threats and risks of tax evasion, concealment of the tax base and other types of fiscal offenses that lead to permanent budget losses.

Such circumstances determine the need to review the mechanism of regulation of the field of tax relations through a system of tasks and goals, methods, principles and tools of regulation, threat and risk factors, as well as elements of tax security. Special attention needs to be paid to the issues of effective fulfillment of tax obligations, effective manipulation of tax system stability factors, as well as improvement of the system of tax administration, fees and improvement of tax culture.

Despite the extensive scientific and practical development of the analyzed issue, the continuous development of absolutely all financial and economic processes necessitates the further deepening of the research, as well as the transformation, specification and detailing of the policy of regulatory influence as an object of research, which determines the purpose of the work.

Many scientific works are devoted to the study of modern problems of the formation of regulatory policy based on ensuring the effectiveness of tax revenues as a dominant factor in the economic security of the state.

Rudnichenko et al. [1] propose to among important indicators of country’s independence is national security and in particular, economic security as its structural component, which is determined by the ability to take preventive measures and resist the impact of financial threats and risks. Globalizing political and economic disparities in recent years in world practice determine the need to deploy the practice of regulatory influence policy, in particular countries’ economic sphere.

Public administration practice has established that economic security is a qualitative parameter of the economic system, which is manifested in the ability to ensure an adequate standard of living based on the adequacy of the resource base for the reproductive processes development and the state’s functions. Economic security of the state is the basis of its financial security, including tax [2-6].

The researchers Lagovska et al. [7] aimed: tax policy effectiveness and targets’ implementation for filling budgets of countries at all levels requires special attention and the need for an integrated approach to the targeted use of numerous tools and levers of regulatory tax policy based on effective tax administration principles. Ensuring the stability of tax revenues in modern economic conditions should be implemented in a set of market and regulatory rules and influences.

As tax revenues accumulate significant financial resources in the country, problem of ensuring the effectiveness of their receipt is particularly important and has led to the existence of a wide research base and theoretical approaches. Their systematization and generalization create an opportunity to generate new approaches and practical recommendations for the implementation of regulatory policy to increase the efficiency of tax revenues dominated by the state economic security.

Many scientific papers Costello et al. [8], Waller [9], Popelo et al. [10], Shmygol et al. [11] and Marhasova et al. [12] interpret economic security as a system whose priority is an effective financial system, in particular, tax system, which determines the level of state economic security. Current economic situation necessitates the creation of conditions for the effective tax system functioning through the prism of tax revenues growth, as the constantly emerging financial and economic risks lead to an increase in government spending. In fact, we can say about tax security determining role as a basis and protection guarantees against a number of financial and economic risks and ensuring national interests in general.

Particular attention Zhavoronok et al. [13], Fedyshyn et al. [14] and Dubyna et al. [15] have paid to the risks of tax security as a set of events that provoke financial resources and their needs asymmetry, reduce the level of state financial independence, as well as systematization of fundamental threats to the tax revenues effectiveness in economic security. In their list primarily Kryvda et al. [16], Shaposhnykov et al. [17] and Shkarlet et al. [18] have included: reducing tax base and the number of taxpayers, reducing the profitability of taxes and fees as a result of increasing the shadow sector size, tax evasion and transfer, moratorium on tax control, reducing the level of tax administration, etc.

In terms of ensuring the effectiveness of the state tax system and combating tax risks, a number of scientists Danylyshyn et al. [19], Tymchenko et al. [20], Lee and Borcherding [21], Zhavoronok et al. [22], Tulchynska et al. [23] and Zybareva et al. [24] have generalized the research methodology and system of analysis methods of tax revenues effective and qualitative indicators with an emphasis on mathematical modeling methods.

The study of peculiarities of the country’s tax system functioning and indicators of its effectiveness in the context of tax revenues adequacy, stability and continuity is devoted to scientific works of Popelo et al. [25], Marhasova et al. [26], Grosu et al. [27] and Tulchynska et al. [28]. Along with them, Pîrvu et al. [29] and Grigoraș-Ichim et al. [30] argue the urgent need to implement an effective tax policy in combination with ensuring the profitability of budgets at all levels and an effective support of taxpayers’ interests to achieve raise in national income growth as a result of tax burden continuous improvement.

Ensuring completeness of tax revenues requires the search for effective tools, in connection with which a new research field has been identified, in particular, the introduction and use of new digital systems for processing, transmitting and evaluating data through the prism of digitalization in effective tax collection [31]. In vast majority of substantiated arguments, special attention is paid to the construction of a high functional digital infrastructure.

The relevance of stimulating and implementing tax policy as a structural component of the regulatory policy has determined in Belyaeva and Kobylatova [32] and Viknianska et al. [33] works, it indicates the unquestionable provision of tax revenues sustainability as a key task of modern tax policy and tax regulation in particular. Gechert et al. [34], Djakona et al. [35] and Alexander [36] once again proved that tax regulation as a component of state regulatory policy has an indirect impact on the activities of economic entities, determining their tax behavior by combining and synergy of classic or new instruments (introduction or abolition of tax payments, application of tax rates differentiation, tax bases or objects of taxation) on the way of relations harmonization between the state and economic agents in order to achieve public and national interests.

Results of scientific research [37-45] and summarize statements about the possibility of minimizing and avoiding significant tax losses in the fiscal relations system through the prism of coherence and stability of regulatory policy instruments and mechanisms, implemented on the basis of legal and economic mechanisms of domestic and foreign economic activity in order to achieve expected results.

Systematizing presented approaches and judgments, it is noted that scientific and practical excursion of the studied problem is due to the processes of economic relations’ globalization, determines the revision of theoretical and practical approaches to regulatory impact on the tax system and the results of its functioning on the way to guaranteeing the economic security of the state.

In this regard, the relevance of regulatory influence in the direction of creating conditions for tax revenues effectiveness in terms of state economic security is crucial. The study is relevant given the importance of regulatory impact on tax revenues to ensure state economic security.

Today, economic security of the state requires a holistic approach to the management of financial resources, including tax incomes as the predominant share of all revenues. Special place in the system of financial management is occupied by the study of taxes and fees amounts status and the identification of their volume trends in complex of ensuring their effectiveness. Value of this analysis is undeniable, as the ability to prevent critical risks, the effectiveness of regulatory policy and the effectiveness of subsequent management decisions will depend on the identification of influence factors and tax capacity expansion.

In this regard, the purpose of study is to establish the level of tax revenues effectiveness in the regulatory policy system in the direction of ensuring state economic security. In accordance with this goal, main tasks are to identify trends in tax revenues of the studied countries, to establish factors of influence that determine the amount of relevant revenues, as well as to calculate the actual efficiency level of taxes and fees mobilization.

Implementation of the stated tasks is based on the use of statistical analysis, synthesis, generalization, factor analysis and economic-metric modeling system of methods. Thanks to the chosen methods, it seems possible to propose regulatory measures due to the increase in tax revenues of the studied countries. Convinced, that selected research and analytical methods will ensure the effectiveness of regulatory actions.

Digital data source of the study were official statistics of the European Statistical Commission, the World Bank, the OECD, etc. on the performance of selected countries for 2011-2020. The time period chosen for the study successfully characterizes the nature and results of tax relations in the conditions of stable development and economic fluctuations, which are also caused by pandemic conditions in society, and reveals reserves and hidden opportunities for increasing the tax potential. Eastern European countries were selected as the studied countries: Bulgaria, Poland, Romania, Slovakia, Hungary and the Czech Republic. We believe that among European countries with high growth rates and a level of tax efficiency, the specified states are of interest from the point of view of the possibility of improving the regulatory policy of tax relations.

It should be noted that due to the lack of a single methodology for assessing the effectiveness of tax revenues, unavailability of full analytical information due to the secrecy or lack of separate economic data, but in order to ensure the most reliable and high-quality monitoring, has been presented an own view on the system of priority indicators for determining tax payments’ effectiveness in the context of state economic security.

І phase – statistical analysis of tax revenues dynamics based on classical methodology.

ІІ phase – determinants assessment of tax revenues effectiveness:

1. The level of tax burden (Ltb), %:

$L_{t b}=\sum T R / G N P * 100$, (1)

where, $\sum T R$–actual tax revenues;

GNP-Gross Domestic Product;

Normative value≤30.

2. The level of tax payment efficiency ($L_{e f} T R$):

$L_{e f} T R=\sum T R_f / \sum T R_p$ (2)

where, $\sum T R_f$-actual tax revenues;

$\sum T R_p$-planned tax revenues;

Normative value≥1.

3. Coefficient of elasticity (Е):

$\mathrm{E}=\Delta \mathrm{TR} / \Delta \mathrm{GDP}$ (3)

where, ∆TR–tax revenue growth rate, %;

∆GDP – GDP growth rate, %.

The indicator shows changes in tax revenues to increase GDP by 1%.

Normative value≥1.

4. Tax debt level of taxpayers (Ltd), %:

$L_{t b}=\sum T_d / \sum T R * 100 \%$ (4)

where, $\sum T_d$–tax debt.

$\sum TR$– actual tax revenues.

Normative value≤5.

ІІІ phase–establishing a rating of tax revenues effectiveness of the studied countries on the aggregation algorithm basis–geometric mean:

$B S=\left(\prod_i R_i^{W_i}\right)^{1 / \Sigma W_i}$ (5)

where, R – aggregated numeric values;

W – geometric mean;

і – number of values.

IV phase – impact assessment of the factors system based on the regression-correlation method in order to determine closeness and trends of the relationship between factors and performance (Y) of the studied countries for 2010-2020, using official databases. The unity of approaches of scientists and practitioners made it possible to group influence factors into the following categories: economic, political and legal, demographic and socio-cultural. A basis for identifying factor effect on the tax revenues volume is a system of economic indicators: X1– final consumption (in billion euros); X2 – import volumes (in billion euros); X3 – export volumes (in billion euros); X4 – population (in millions); X5– industrial production (in billion euros); X6 – income (in billion euros). The initial result should be a matrix of paired correlation coefficients. In order to increase the accuracy of determining factor effect, regression analysis was performed and values of R, R2 and Fisher’s F-test were calculated. Assessment of Student’s t-test is designed to identify the significance of regression equation parameters (normative level of significance - 0.05, and the level of reliability 95%).

Practical reflection of the multiple regression equation will take the following form:

$Y=b_0+b_1 * x_1+\cdots+b_i * x_i$ (6)

where, Y – estimated value of the resultant feature;

xi– influencing factors;

i – the number of studied factors;

bi– multiple regression coefficients that determine the degree of factors’ influence;

b0– the function average.

Having made functional calculations of the presented phases, it will be possible to rank Eastern European countries according to the level of tax revenues efficiency and identify problem areas for which it is advisable to take regulatory action to increase tax revenues in the future.

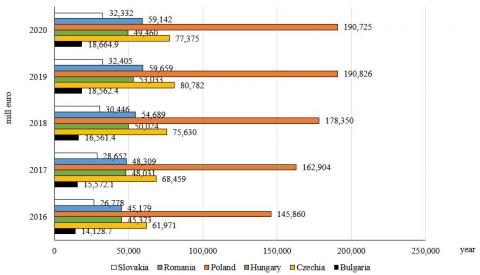

The sphere of tax relations’ regulation at national level directly depends on and is determined by the tasks of state economic development on the vector of its sustainable and secure development. The defining characteristic of this issue is an actual amount of tax revenues to the country’s budget. The study analyzed dynamics of tax revenues in Eastern Europe for 2016-2020 (Figure 1) [46].

Analyzing Fig. 1 data, there is a positive trend of increasing tax revenues for the selected countries during 2016-2019. In general, an average increase by country was 8.3%. The highest indicators were shown by: Romania (9.7%), Bulgaria (9.5%) and Poland (9.3%). Hungary showed the worst rate -5.3%. This situation is justified by the confident economic development of the studied countries. However, by the end of 2020, these indicators have changed – there was a decrease in taxes and fees payment in all countries - an average of 98.0%. The worst values of the studied indicator were observed in Czech Republic (-4.3%) and Hungary (-6.8%). Logical explanation for this situation is the quarantine conditions in connection with COVID-19 pandemic. Only Bulgaria in 2020 managed to achieve an increase of 100.5%.

The role of tax revenues in ensuring country’s economic security is determined by their share in the structure of gross national product. Evaluating official statistics for 2016-2020, it was found that their share for the studied countries is as follows (Table 1). According to estimated data during the study period, tax revenues’ share in the country’s income ranged from 25.7 to 39.0%, which indicates their significant revenue role.

Implementing the second stage of determining the effectiveness of tax revenues in ensuring country’s economic security, in particular examining tax burden level, which also provides ratio of tax revenues to GDP (Table 1), we note fairly high level of such burden on economic entities as its normative value is less than 30%. This fact leads to a decrease in their level of profitability after tax and may provoke various measures of tax evasion. At the same time, Hungary was the only Eastern European country in 2016-2020 to reduce the value of such an indicator.

The results analysis of tax revenues’ effectiveness is determined by establishing the ratio of actual and planned revenues to the budget for a year. After assessing official statistics of Eastern Europe, the following trends were identified (Figure 2) [46].

It is determined that during the study period only 2020 was the year of non-fulfillment of planned tax revenues, except for Bulgaria, Poland and Slovakia, where the level of implementation was 103.7%, 105.9% and 100.6%. Reasons for this situation are fully justified by the decline in business activity as a result of quarantine conditions, as a result of which a large proportion of small and medium-sized businesses have suspended or stopped doing business altogether. The size of taxation objects of big business entities has decreased. At the same time, the implementation pace of tax revenues’ planned values in 2016-2019 of the studied countries ranged from 0.1% to 9.7%. This situation indicates successful tax planning, as well as government actions aimed at stimulating economic activity of entrepreneurs.

Figure 1. Dynamics of planned state tax revenues fulfillment of Eastern European countries

Table 1. The share of tax revenues in the structure of Eastern Europe national incomes

|

Country |

Years, % |

Increase, % |

|||||||

|

2016 |

2017 |

2018 |

2019 |

2020 |

2017/ 2016 |

2018/ 2017 |

2019/ 2018 |

2020/ 2019 |

|

|

Bulgaria |

29.0 |

29.8 |

29.5 |

30.3 |

30.8 |

0.7 |

-0.2 |

0.8 |

0.5 |

|

Czechia |

34.9 |

35.3 |

35.9 |

35.8 |

35.9 |

0.3 |

0.6 |

0.0 |

0.1 |

|

Hungary |

39.0 |

37.8 |

36.8 |

36.3 |

36.2 |

-1.2 |

-1.0 |

-0.5 |

-0.1 |

|

Poland |

34.2 |

34.9 |

35.8 |

35.8 |

36.4 |

0.7 |

1.0 |

-0.1 |

0.7 |

|

Romania |

26.6 |

25.7 |

26.7 |

26.8 |

27.1 |

-0.8 |

1.0 |

0.0 |

0.4 |

|

Slovakia |

33.1 |

33.9 |

34.0 |

34.5 |

35.1 |

0.9 |

0.1 |

0.4 |

0.7 |

An important indicator of tax system flexibility and, accordingly, efficiency of tax revenues, we consider tax revenues elasticity by GDP (Table 2).

Table 2 data analysis found that the absolute elasticity of tax revenues is typical for Czech Republic, Poland, Romania and Slovakia, based on the results of which the studied coefficient is more than 1. Countries such as Bulgaria and Hungary need to review organization principles of the country tax system, the peculiarities of tax policy and administrative rules in order to regulate relevant value of the indicator.

An important indicator of tax revenues’ effectiveness is the status of tax arrears, in particular its size and dynamics of change due to effective measures to collect it. The Eastern Europe tax debt status is evidenced by the data in Table 3 [47].

Taking into account presented statistical data, different trends in the dynamics of tax debt changes of the studied countries were observed. In particular, during 2016-2019, countries such as Bulgaria (-225.2%), Poland (-135.3%), Romania (-125.8%) and Slovakia (-158.0%) significantly reduced the actual value of the study indicator. However, Czech Republic and Hungary, on the other hand, increased the debt amount: + 131.0% and + 109.5%, which does not positively characterize tax policy of these countries, as tax debt is an uncollected part of the country’s budget revenues and unfulfilled functions and obligations.

In order to logically complete the establishment of tax revenues effectiveness of the studied countries there was formed an Eastern European countries rating on the basis of preliminary estimated tabular data (Figure 3). Thus, the highest efficiency degree of tax revenues is observed in the practice of Slovakia and Bulgaria tax administration, the lower level of tax revenues and fees efficiency is inherent in Hungary and the Czech Republic.

Figure 2. Dynamics of the percentage indicator of the collection of planned tax revenues of Eastern European countries

Table 2. Indicators dynamics of tax revenues elasticity by GDP in Eastern Europe

|

Years |

Country |

|||||

|

Bulgaria |

Czechia |

Hungary |

Poland |

Romania |

Slovakia |

|

|

2016 |

0.95 |

1.01 |

0.97 |

1.002 |

0.97 |

1.03 |

|

2017 |

0.93 |

1.02 |

0.97 |

1.03 |

1.04 |

1.0 |

|

2018 |

0.92 |

1.0 |

0.99 |

1.0 |

1.0 |

1.01 |

|

2019 |

1.01 |

1.0 |

0.99 |

1.02 |

1.01 |

1.02 |

Table 3. Dynamics of the Eastern Europe tax debt status

|

Years |

Country |

|||||

|

Bulgaria |

Czechia |

Hungary |

Poland |

Romania |

Slovakia |

|

|

2016 |

6523.25 |

47.20 |

452.16 |

3374.0 |

2956.40 |

4866.95 |

|

2017 |

7459.26 |

44.49 |

452.17 |

3702.64 |

3164.20 |

5618.17 |

|

2018 |

2902.0 |

57.82 |

501.41 |

2386.65 |

2079.10 |

2993.24 |

|

2019 |

2896.68 |

61.85 |

495.34 |

2493.30 |

2349.58 |

3081.08 |

Given the analysis, it seems necessary to develop a system of recommendations for regulatory action aimed at improving the efficiency of tax revenues in order to ensure the state economic security. We believe that a step in this direction should be to identify areas of regulation by identifying the factor impact on the actual amount of tax revenues. These measures were implemented through the prism of regression analysis and functional dependencies methods, the results of which are shown in Table 4.

Table 4. Results of regression analysis of Eastern European countries tax revenues

|

Country |

Linear Function |

R2 |

|

Bulgaria |

Y=1206.3х+13079 |

0.9553 |

|

Czechia |

Y=413.1х+59904 |

0.8932 |

|

Hungary |

Y=1317.6х+45232 |

0.552 |

|

Poland |

Y=11765х+138437 |

0.925 |

|

Romania |

Y=3927.7х+41612 |

0.922 |

|

Slovakia |

Y=1486х+25665 |

0.938 |

After analyzing tax revenues on a linear trend, it was noted that over years the change in absolute increase in tax revenues is the smallest in Czech Republic (413.1 million euros), and the largest in Poland - 11765 million euros. These results indicate the existence of tax capacities differentiation of studied countries’ tax revenues, as determined by historical, geopolitical, socio-economic and other factors number.

Thus, in creating conditions for economic security in the regulation of tax revenues effectiveness is crucial to identify priority factors that determine the growth of budgets’ tax revenues. To determine conditions for the implementation of regulatory impact on tax revenues amount of the studied countries, it is necessary to clarify the content of factors whose impact determines the effectiveness of tax revenues in general. Taking into account the list of such factors, we will study the impact some of them on the tax revenues of the studied countries according to the multiple regression and criteria methodology that determine real impact on the value of performance indicator.

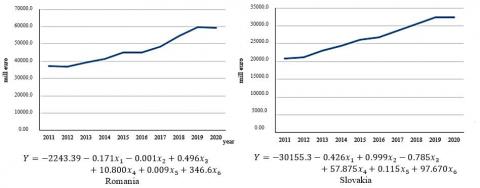

Assessing indicators of regression statistics, in particular, R2, it was found that constructed models of variables sufficiently determine the variable B at the significance level of 0.5 and reliability of 0.95. Fisher’s coefficient indicates a high degree of built models’ adequacy in terms of economic performance of the studied countries. Statistical data analysis results, which determined hidden characteristics, as well as econometric calculations of the factor impact on the tax revenues value of Eastern Europe are based on Figure 4. In general, established dependencies provide opportunities for forecasting tax revenues in future periods.

It is safe to say that such factor as consumption volumes (X1) has the greatest positive impact in Czech Republic (0.714) and Hungary (0.277), and its negative impact is in the economic activities of Romania (-0.171) and Slovakia (-0.426). The factor of products’ import (X2) provides the largest increase in Slovakia tax revenues (0.999), and in Bulgaria the smallest (-0.137). The growth of tax payments in Poland (0.522) against Slovakia (-0.785) has the strongest impact on the export operation (X3). Population growth (X4) has the largest impact on the increase in Czech Republic tax payments (87.248), and the least in Hungary. Only in Czech Republic the volume of production (X5) have the worst impact on tax revenues (-0.04). Regarding the income factor (X6) of economic entities, the best impact was observed in Bulgaria (406.116), while the worst but positive impact was observed in Hungary (4.912). At the same time, it is determined that a significant positive impact on the growth of tax revenues has the factor of economic entities income, which in future will determine the volume of consumption and savings, growth of production processes, etc.

Thus, in such conditions it is difficult to speak about the unity of a single factor positive influence in the studied countries. The process is due to the wide variety of location features, the level of country business activity, the availability of economic activity resources, the functioning of economy specific areas, national traditions and state policies as a whole. It is difficult to talk about the unity of recommendations and their universality in terms of implementing the regulatory impact on the volume and effectiveness of tax revenues to the budget.

Figure 3. Ranking of Eastern European countries in terms of tax revenues efficiency

Figure 4. Analysis results of the factors impact on the volume of Eastern Europe tax revenues

Such circumstances determine an increased interest in regulatory influence methods and tools through the prism of tax security structural components (Figure 5).

In our opinion, this should be organizational and legal scheme of economic security, which will function through the prism of tax security. Since tax security system is independent, its main components should be:

1. Goals and objectives related to increasing tax effectiveness through a system of factors influencing the level of budget tax revenues.

2. Measures to ensure economic security, carried out on the basis of effective state regulation and tax system management through a system of tax administration control and supervision institutions.

3. Impact factors identification, forecasts development and identification of possible risks.

4. Indicators of threshold values (standard of living, inflation, unemployment).

5. Methods and tools of influence, the application of which is determined by the results of situation assessment based on statistical and econometric modeling methods and subsequent forecasting.

The application of an effective planning and control system based on the latest IT systems seems to be effective here, which ensures maximum tax potential formation in the country. The presented elements should be leading in the governance and regulatory activities of each country.

We believe that goals and objectives of regulating tax revenues effectiveness should be the following areas: increasing the conditions of investment-attractive business environment; increasing the level of a fair competitive environment and minimizing shadow economy, as well as increasing the efficiency of public money resources;

Regulatory impact tools should include:

1) measures to create sustainable tax conditions and increase the number of real business entities – taxpayers;

2) terms reduction of VAT budgetary refund the on the basis of legislation and service modification of given processes by the newest information technologies;

3) change in the tax burden structure, including the way of revision in direction of tax rates differentiation as a result of not more than normative value of 30%;

4) optimization and increase of professional level of tax control and supervision bodies employees, methods of tax administration.

Thus, the obtained calculations results, modeling and their effective application through the prism of tasks, goals, instruments of regulatory influence in the future with sufficient probability can provide an increase in the state level of tax revenues efficiency.

Figure 5. The mechanism of regulatory policy through tax security elements

Having carried out a study of the assessment of the level of efficiency of tax revenues, it was established that the highest degree of their efficiency among the countries of Eastern Europe is noted in the practice of tax administration of Slovakia and Bulgaria, the lower level of efficiency is characteristic of Hungary and the Czech Republic. Research using the method of factor regression analysis determined the areas of regulation of tax relations on the way to increase the level of efficiency of tax revenues to the budgets for each of the countries of Eastern Europe. The lack of unity of positive and negative effects of each separately investigated factor was revealed, which is argued by differences in geographical location, the level of business activity of economic entities in countries, the availability of a resource base, the degree of development of specific areas of the economy, national traditions, state policy, etc. In this regard, it is difficult to talk about the unity of recommendations, as well as the universality of methods and tools of regulatory influence on the dynamics of the efficiency indicators of tax revenues to the budget of the countries under study. Regulatory policy requires an individual approach.

The author's approach to the application of methodological tools for the assessment of economic tax revenues of the studied countries is presented, the components of which are recognized as the sequence of stages and methods of analysis and modeling, in particular, the determination of influencing factors. In the course of the study of the efficiency of tax revenues, it is proposed to use such criteria as: tax burden, level of efficiency of paying taxes and fees, coefficient of elasticity of tax revenues and level of tax arrears.

The conducted research made it possible to substantiate the system of methods, principles and tools of regulatory influence through the prism of the structural components of tax security: tax liability of taxpayers, factors of the stability of the tax system, improvement of the taxation mechanism, raising the level of tax culture and increasing the level of effectiveness of tax administration. The proposed toolkit has applied value for ensuring the economic security of the studied countries and is aimed at overcoming the instability of the economic situation, resource dependence, increasing the indicators of tax revenue mobilization in the conditions of crisis and quarantine phenomena, taking into account the need to reduce the level of the tax burden.

[1] Rudnichenko, Y., Melnyk, S., Havlovska, N., Illiashenko, O., Nakonechna, N. (2021). Strategic interaction of state institutions and enterprises with economic security positions in digital economy. WSEAS Transactions on Business and Economics, 18: 218-230. https://doi.org/10.37394/23207.2021.18.23

[2] Rekunenko, I., Zhuravka, F., Nebaba, N., Levkovych, O., Chorna, S. (2022). Assessment and forecasting of Ukraine’s financial security: Choice of alternatives. Problems and Perspectives in Management, 20(2): 117-134. https://doi.org/10.21511/ppm.20(2).2022.11

[3] Britchenko, I., Filyppova, S., Niekrasova, L., Chukurna, O., Vazov, R. (2022). The system of evaluation efficiency of the strategy of sustainable development of the enterprise in the decentralization conditions. Ikonomicheski Izsledvania, 31(1): 118-138. https://www.iki.bas.bg/Journals/EconomicStudies/2022/2022-1/07_Britchenko-3.pdf.

[4] Vdovenko N.M. (2015). Mechanisms of regulatory policy application in agriculture. Economic Annals-XXI, 5-6: 53-56. http://ea21journal.world/wp-content/uploads/2022/04/ea-V151-13.pdf.

[5] Vovk, O., Kravchenko, M., Popelo, O., Tulchynska, S., Derhaliuk, M. (2021). Modeling the choice of the innovation and investment strategy for the implementation of modernization potential. WSEAS Transactions on Systems and Control, 16: 430-438. https://doi.org/10.37394/23203.2021.16.38

[6] Filyppova, S., Kovtunenko, Y., Filippov, V., Voloshchuk, L., Malin, O. (2021). Sustainable development entrepreneurship formation: System-integrated management tools. E3S Web of Conferences, 255: 01049. https://doi.org/10.1051/e3sconf/202125501049

[7] Lagovska, O., Ilin, V., Kotsupatriy, M., Ishchenko, M., Verbivska, L. (2020). Priority directions of tax policy change in the information sphere. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, 3: 183-190. https://doi.org/10.33271/nvngu/2020-3/183

[8] Costello, C.B., Wight, V.R., Stone, A.J. (2016). Economic security. The American Woman, 2003-2004: Daughters of a Revolution: Young Women Today, 291-308. https://doi.org/10.1007/978-1-137-11600-0

[9] Waller, W.T. (2019). Economic security and the state. The Stratified State: Radical Institutionalist Theories of Participation and Duality: Radical Institutionalist Theories of Participation and Duality, 153-171. https://doi.org/10.4324/9781315487090-7

[10] Popelo, O., Tulchynska, S., Garafonova, O., Kovalska, L., Khanin, S. (2021). Methodical approach to assessing innovative development efficiency of regional economic systems in the conditions of the creative economy development. WSEAS Transactions on Environment and Development, 17: 685-695. https://doi.org/10.37394/232015.2021.17.66

[11] Shmygol, N., Galtsova, O., Shaposhnykov, K., Bazarbayeva, S. (2021). Environmental management policy: an assessment of ecological and energy indicators and effective regional management (on the example of Ukraine). Polityka Energetyczna, 24(4): 43-60. https://doi.org/10.33223/epj/143836

[12] Marhasova, V., Garafonova, O., Popelo, O., Tulchynska, S., Pohrebniak, A., Tkachenko, T. (2022). Environmentalization of Production as a direction of ensuring the sustainability of production activities of enterprises and increasing their economic security. International Journal of Safety and Security Engineering, 12(2): 159-166. https://doi.org/10.18280/ijsse.120203

[13] Zhavoronok, A., Chub, A., Yakushko, I., Kotelevets, D., Lozychenko, O., Kupchyshynа, O. (2022). Regulatory policy: Bibliometric analysis using the VOSviewer program. International Journal of Computer Science and Network Security, 22(1): 39-48. https://doi.org/10.22937/IJCSNS.2022.22.1.7

[14] Fedyshyn, M., Dubyna, M., Popelo, O., Kholiavko, N., Zhavoronok, A., Yakushko, I. (2022). Mapping the literature on financial behavior: A bibliometric analysis using the VOSviewer program. WSEAS Transactions on Business and Economics, 19: 231-246. https://doi.org/10.37394/23207.2022.19.22

[15] Dubyna, M., Kholiavko, N., Zhavoronok, A., Safonov, Yu., Krylov, D., Tochylina, Yu. (2022). The ICT sector in economic development of the countries of Eastern Europe: A comparative analysis. WSEAS Transactions on Business and Economics, 19: 169-185. https://doi.org/10.37394/23207.2022.19.18

[16] Kryvda O., Tulchynska S., Smerichevskyi S., Lagodiienko N., Marych M., Naghiyeva A. (2022). Harmony of ecological development in the conditions of the circular economy formation. Environment and Ecology Research, 10(1): 11-20. https://doi.org/10.13189/eer.2022.1001

[17] Shaposhnykov, K., Kochubei, O., Grygor, O., Protsenko, N., Vyshnevska, O., Dzyubina, A. (2021). Organizational and economic mechanism of development and promotion of IT products in Ukraine. Estudios de Economía Aplicada, 39(6). https://doi.org/10.25115/eea.v39i6.5264

[18] Shkarlet, S., Kholiavko, N., Dubyna, M. (2015). Territorial reform in the system of strategic management of energy-economic and information spheres of the state. Economic Annals-XXI, 5-6: 103-107.

[19] Danylyshyn, B., Dubyna, M., Zabashtanskyi, M., Ostrovska, N., Blishchuk, K., Kozak, I. (2021). Innovative instruments of monetary and fiscal policy. Universal Journal of Accounting and Finance, 9(6): 1213-1221. https://doi.org/10.13189/ujaf.2021.090601

[20] Tymchenko, O., Sybirianska, Yu., Abramova, A. (2019). The approach to tax debtors segmentation. Ikonomicheski Izsledvania, 28(5): 103-119.

[21] Lee, D., Borcherding, T.E. (2006). Public choice of tax and regulatory instruments - The role of heterogeneity: Evidence from U.S. state environmental policy, 1980-1994. Public Finance Review, 34(6): 607-636. https://doi.org/10.1177/1091142106291501

[22] Abramova, A., Shaposhnykov, K., Zhavoronok, A., Liutikov, P., Skvirskyi, I., Lukashev, O. (2021). The Ecosystem of VAT administration in E-commerce: Case of the Eastern Europe Countries. Estudios de Economía Aplicada, 39(5). http://dx.doi.org/10.25115/eea.v39i5.4909

[23] Tulchynska, S., Popelo, O., Marhasova, V., Nusinova, O., Zhygalkevych, Z. (2021). Monitoring of the ecological condition of regional economic systems in the context of sustainable development. Journal of Environmental Management and Tourism, 12(5): 1220-1228. https://doi.org/10.14505//jemt.v12.5(53).06

[24] Zybareva, O., Kravchuk, I., Pushak, Y., Verbivska, L., Makeieva, O. (2021). Economic and legal aspects of the network readiness of the enterprises in Ukraine in the context of business improving. Estudios de Economia Aplicada, 39(5). https://doi.org/10.25115/eea.v39i5.4972

[25] Popelo, O., Tulchynska, S., Marhasova, V., Garafonova, O., Kharchenko, Y. (2021). Public management of regional development in the conditions of the inclusive economy formation. Journal of Management Information and Decision Sciences, 24(S2): 1-8. https://www.abacademies.org/articles/Public-management-of-regional-development-in-the-conditions-of-the-inclusive-economy-formation-1532-5806-24-7-307.pdf.

[26] Marhasova, V., Tulchynska, S., Popelo, O., Garafonova, O., Yaroshenko, I., Semykhulyna, I. (2022). Modeling the harmony of economic development of regions in the context of sustainable development. International Journal of Sustainable Development and Planning, 17(2): 441-448. https://doi.org/10.18280/ijsdp.170209

[27] Grosu, V., Kholiavko, N., Zhavoronok, A., Zlati, M.L., Cosmulese, C.G. (2021). Conceptualization of model of financial management in Romanian agriculture. Economic Annals-XXI, 191(7-8(1)): 54-66. https://doi.org/10.21003/ea.V191-05

[28] Tulchynska, S., Popelo, O., Vovk, O., Dergaliuk, B., Kreidych, I., Tkachenko, T. (2021). The resource supply of innovation and investment strategies of the microeconomic systems modernization in the conditions of digitalization. WSEAS Transactions on Environment and Development, 17: 819-828. https://doi.org/10.37394/232015.2021.17.77

[29] Pîrvu, D., Duţu, A., Mogoiu, C.M. (2021). Clustering tax administrations in European Union member states. Transylvanian Review of Administrative Sciences, 17(63): 110-127. https://doi.org/10.24193/tras.63E.6

[30] Grigoraș-Ichim, C.E., Cosmulese, C.G., Savchuk, D., Zhavoronok, A. (2018). Shaping the perception and vision of economic operators from the Romania – Ukraine – Moldova border area on interim financial reporting. Economic Annals-XXI, 173(9-10): 60-67. https://doi.org/10.21003/ea.V173-10

[31] Boiarynova, K., Popelo, O., Tulchynska, S., Gritsenko, S., Prikhno, I. (2022). Conceptual foundations of evaluation and forecasting of innovative development of regions. Periodica Polytechnica Social and Management Sciences, 30(2): 167-174. https://doi.org/10.3311/PPso.18530

[32] Belyaeva, S.V., Kobylatova, M.F. (2016). Priorities for formation of anti-crisis tax policy. Turkish Online Journal of Design Art and Communication, 6: 2546-2555. https://doi.org/10.7456/1060NVSE/059

[33] Viknianska, A., Kharynovych-Yavorska, D., Sahaidak, M., Zhavoronok, A., Filippov, V. (2021). Methodological approach to economic analysis and control of enterprises under conditions of economic systems transformation. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, 4: 150-157. https://doi.org/10.33271/nvngu/2021-4/150

[34] Gavkalova, N., Kolupaieva, I., Barka, Z.M. (2017). Analysis of the efficiency of levers in the context of implementation of the state regulatory policy. Economic Annals-XXI, 165(5-6): 41-46. https://doi.org/10.21003/ea.V165-09

[35] Djakona, A., Kholiavko, N., Dubyna, M., Zhavoronok, A., Fedyshyn, M. (2021). Educational dominant of the information economy development: A case of Latvia for Ukraine. Economic Annals-XXI, 192(7-8(2)): 108-124. https://doi.org/10.21003/ea.V192-09

[36] Alexander, K. (2010). International regulatory reform and financial taxes. Journal of International Economic Law, 13(3): 893-910. https://doi.org/10.1093/jiel/jgq036

[37] Shkarlet, S., Dubyna, M., Hrubliak, O., Zhavoronok, A. (2019). Тheoretical and applied provisions of the research of the state budget deficit in the countries of Central and Eastern Europe. Administratie si Management Public, 32: 120-138. https://doi.org/10.24818/amp/2019.32-09

[38] Kholiavko, N., Popova, L., Marych, M., Hanzhurenko, I., Koliadenko, S., Nitsenko, V. (2020). Comprehensive methodological approach to estimating the research component influence on the information economy development. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, 4: 192-199. https://doi.org/10.33271/nvngu/2020-4/192

[39] Balcerzak, A. (2016). Fiscal burden in the European Union member states. Economic Annals-ХХI, 16(9-10): 4-6. https://doi.org/10.21003/ea.V161-01

[40] Bulatova, O., Marena, T., Chentukov, Yu., Shabelnyk, T. (2020). The impact of global financial transformations on the economic security of Central and Eastern European countries. Public and Municipal Finance, 9(1): 1-13. https://doi.org/10.21511/pmf.09(1).2020.01

[41] Eatwell, J., Alexander, K. (2012). International regulatory reform and financial taxes. Research Handbook on International Financial Regulation, 397-413. https://doi.org/10.4337/9780857930453.00029

[42] Serikova, M., Sembiyeva, L., Mussina, A., Kuchukova N., Nurumov, A. (2018). The institutional model of tax administration and aspects of its development. Investment Management and Financial Innovations, 15(3): 283-293. https://doi.org/10.21511/imfi.15(3).2018.23

[43] Gechert, S., Horn, G., Paetz, C. (2018). Long term effects of fiscal stimulus and austerity in Europe. Oxford Bulletin of Economics and Statistics, 81(3): 647-666. https://doi.org/10.1111/obes.12287

[44] Popelo, O., Tulchynska, S., Lagodiienko, N., Radin, A. M., Moskalenko, A. (2021). Methodical approach to forecasting the intensification of innovative development of regions using the Mathcad program. International Journal of Circuits, Systems and Signal Processing, 15: 1591-1601. https://doi.org/10.46300/9106.2021.15.171

[45] Zybareva, O., Lagodiienko, V., Popelo, O., Samiilenko, H., Mykytyuk, Y., Alsawwafi, F.M.A.S. (2022). Peculiarities of the management of the foreign economic activity of enterprises in current conditions of sustainability. International Journal of Sustainable Development and Planning, 17(4): 1215-1223. https://doi.org/10.18280/ijsdp.170420

[46] EUROSTAT. European Commission. https://ec.europa.eu, accessed on Apr. 6, 2022.

[47] International Survey on Revenue Administration (ISIRA). https://data.rafit.org, accessed on Apr. 6, 2022.