Lindawati Kartika*![]() | Mohamad Syamsul Maarif

| Mohamad Syamsul Maarif![]() | Anggraini Sukmawati

| Anggraini Sukmawati![]() | Harri Koeswanda

| Harri Koeswanda

© 2026 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Environmental, Social, and Governance (ESG) principles have emerged as critical frameworks for sustainable business operations. While ESG adoption among large corporations has gained momentum, micro, small, and medium enterprises (MSMEs), particularly in the food and beverage sector, continue to face challenges in aligning their human resource management (HRM) strategies with ESG goals. Despite a growing body of research on ESG and HRM independently, there is a notable lack of integrative models that support ESG implementation through HRM in the MSME context. This study conducts a systematic literature review (SLR) guided by the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) framework. Relevant peer-reviewed articles from Scopus and Web of Science, Q1 until Q4 published between 2016 and 2025 were collected using specific search strings combining keywords related to ESG, HRM, MSMEs, and the food and beverage industry. A total of 40 articles met the inclusion criteria after screening, deduplication, eligibility checks, and quality appraisal using the Mixed Methods Appraisal Tool (MMAT 2018), with substantial inter-rater reliability (Cohen’s kappa = 0.81). Three dominant themes emerged: (1) ESG awareness and organizational culture, (2) HRM practices fostering sustainability (e.g., green recruitment, employee training, and ethical leadership), and (3) challenges in ESG-HRM integration such as resource constraints and knowledge gaps. However, very few studies propose comprehensive HRM models tailored for ESG implementation in MSMEs. Most literature emphasizes large enterprise frameworks, indicating a contextual mismatch for MSMEs. The findings highlight a critical research and practice gap in developing context-specific HRM models that operationalize ESG in food and beverage MSMEs. This review proposes a conceptual foundation for future HRM-ESG integration models that prioritize simplicity, scalability, and local cultural alignment. These insights contribute to bridging theory and practice, helping MSMEs build resilience and competitive advantage through sustainable human capital strategies.

Environmental, Social, and Governance, food and beverage industry, human resource management, micro, small, and medium enterprises, sustainability

The global emphasis on sustainability has brought Environmental, Social, and Governance (ESG) frameworks to the forefront of business practices. While large corporations have been the primary focus of ESG research and implementation, the role of micro, small, and medium enterprises (MSMEs) in advancing sustainable development is gaining attention due to their significant contribution to economic growth, employment, and innovation [1, 2]. Specifically, the food and beverage sector dominated by MSMEs in both developed and developing countries plays a crucial role in ensuring food security and driving local economies [3, 4]. However, ESG adoption in MSMEs is often challenged by resource limitations, lack of standardized practices, and low regulatory pressure [5, 6].

Meanwhile, human resource management (HRM) is recognized as a vital enabler of organizational change and sustainability [7, 8]. Strategic HRM practices such as employee training, ethical labor management, and value-driven leadership are crucial for ESG alignment, yet there is limited understanding of how these practices can be effectively tailored to MSMEs in the food and beverage industry [9-11]. This lack of contextual models highlights the need for more integrative and MSME-relevant frameworks that can support ESG implementation through HR-driven mechanisms.

The integration of sustainability into various sectors, including the business and labor domains, has led to increased scholarly focus on sustainable human resource management (S-HRM) [12-14]. This growing interest also extends to how S-HRM practices are applied within small and medium-sized enterprises (SMEs) for several key reasons. SMEs serve as crucial employment generator especially in Europe accounting for nearly two-thirds of the workforce in the non-financial business sector [15]. Due to their relatively smaller size, SMEs are often more vulnerable to external pressures, making them more responsive to the expectations of diverse stakeholders [16, 17]. Despite their size, SMEs collectively exert a substantial environmental footprint, being responsible for approximately 60–70% of total pollution [18]. Their distinct characteristics summarized in the RECIPE acronym (Resource limitations, Environmental sensitivity, Centralized ownership, Informality, Close interpersonal relationships, and Employee-centric experience) influence the way they implement HRM practices [19]. These attributes often lead SMEs to approach sustainable development (SD) issues differently compared to larger firms [18, 20, 21]. Moreover, scholars argue that the understanding and enactment of sustainability in SMEs are significantly shaped by institutional factors, including prevailing regulations and contextual barriers that may hinder effective implementation [21, 22].

Despite the growing body of literature on ESG and HRM individually, there remains a notable absence of integrated frameworks that combine these two critical areas, particularly within the context of MSMEs [10, 23]. Most existing studies focus either on ESG adoption in large corporations or on HRM strategies without linking them directly to sustainability outcomes [7, 8]. Furthermore, HRM models often assume formal organizational structures and resource capacities that MSMEs typically lack [4, 9]. This presents a clear research gap: the need for practical and adaptable HRM models that facilitate ESG implementation within the structural realities of MSMEs, especially those operating in the food and beverage sector [2, 11]. MSMEs refer to business entities that operate on a smaller scale compared to large corporations. These enterprises are commonly defined based on various criteria such as employee count, asset size, and annual income, although these benchmarks may differ depending on a country’s economic landscape and regulatory framework [24, 25]. MSMEs is an entity that independently owned and managed businesses that generally focus on the production, distribution, and marketing of goods and services, yet function at a reduced scale [26]. These businesses typically operate with fewer employees, generate lower revenue, and possess limited assets. Furthermore, MSMEs often concentrate on serving local markets rather than competing in international ones [27]. Consistently, institutions like the World Bank also emphasize that MSMEs differ from larger firms in terms of their smaller workforce, limited income, and asset base. The various definitions reflect a broad understanding of MSMEs' operational scale, their structural features, and their contributions to both the economy and society.

Addressing this gap is essential not only to enhance the sustainability performance of these businesses but also to support broader environmental and social goals at the community level [5, 6]. The intersection between HRM and ESG is critical in small enterprises where workforce engagement, ethical governance, and environmental accountability can drive meaningful impact yet these dimensions are rarely operationalized in existing MSME-oriented studies. As such, there is a pressing need to synthesize emerging insights and propose integrative models that are both contextually relevant and practically feasible for small businesses in the food and beverage sector. This systematic literature review (SLR) aims to bridge that gap by synthesizing current research on HRM models and ESG integration in food and beverage MSMEs. This SLR aims to bridge that gap by synthesizing current research on HRM models and ESG integration in food and beverage MSMEs. This SLR aims to bridge that gap by synthesizing current research on HRM models and ESG integration in food and beverage MSMEs. The study is guided by the following research questions: (1) What HRM practices have been identified in the literature to support ESG implementation in MSMEs? (2) How do existing HRM-ESG models apply to MSMEs in the food and beverage sector? (3) What are the barriers and enablers for adopting integrated HRM-ESG strategies in these businesses? and (4) What future research directions are suggested by the current literature? These questions are designed to explore both theoretical developments and practical implications for small business sustainability [2, 10, 23].

The food and beverage (F&B) sector, which is heavily supported by the activities of MSMEs, plays a pivotal role in global economic and social development. The sector is recognized as one of the most dynamic drivers of economic activity, contributing substantially to employment creation, value-added production, and local supply-chain stability in both developed and developing economies. MSMEs dominate the landscape of food production, processing, and distribution, making them essential actors in shaping sustainable practices across the industry. As sustainability expectations continue to rise worldwide, the F&B sector faces increasing pressure to adopt more responsible ESG practices, with MSMEs positioned at the center of this transition due to their scale, flexibility, and close engagement with local communities. However, rising environmental pressures, social accountability expectations, and demands for ethical governance have compelled F&B enterprises regardless of size to adopt more sustainable practices aligned with ESG principles. MSMEs face unique challenges in this transition, including limited access to finance, formal training systems, and institutional support. To answer the research questions, this study follows the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) protocol, ensuring transparency and rigor in article selection and synthesis [28]. The literature was gathered from two leading academic databases Scopus and Web of Science (WoS) focusing exclusively on Q1 until Q4 journals published between 2016 and 2025. A total of 1.250 records were initially identified. After removing duplicates, non-relevant domains, and articles outside the designated time frame, 40 peer-reviewed studies were included in the final qualitative synthesis. These articles provide insights into emerging HRM practices, contextual ESG challenges in MSMEs, and sector-specific models that contribute to sustainable organizational transformation.

A SLR is a well-established and rigorous research methodology that is highly regarded in academic discourse for its ability to offer a transparent, replicable, and comprehensive synthesis of existing knowledge [29]. Unlike traditional or narrative reviews, which may be prone to subjectivity and selection bias, the SLR approach employs a structured and methodical process for identifying, selecting, evaluating, and synthesizing the available literature. This process typically involves the application of clearly defined inclusion and exclusion criteria, protocol registration, and documentation of every stage of the review process, thereby ensuring objectivity, traceability, and validity of findings [30].

Given these strengths, the SLR method is particularly suitable for analyzing the intersection between sustainability and HRM within micro, small, and medium-sized enterprises (MSMEs) especially in the food and beverage sector, where ESG practices are increasingly relevant. The SLR enables a holistic examination of emerging frameworks, practical strategies, and empirical evidence on how HRM supports or constrains the implementation of ESG principles in such enterprises.

To guide this review, the following research questions were formulated:

(1) What HRM practices have been identified in the literature to support ESG implementation in MSMEs?

(2) How do existing HRM-ESG models apply to MSMEs in the food and beverage sector?

(3) What are the barriers and enablers for adopting integrated HRM-ESG strategies in these businesses?

(4) What future research directions are suggested by the current literature?

By systematically addressing these questions, this study aims to bridge the gap in the literature concerning the strategic alignment of HRM and ESG within the operations of food and beverage MSMEs. The findings are expected to provide both theoretical contributions and practical implications for scholars, policymakers, and MSME practitioners engaged in sustainable enterprise development.

To ensure methodological transparency and rigor, this SLR adhered to the PRISMA framework. The literature search was conducted using two reputable academic databases Scopus and Web of Science (WoS) employing a set of predefined keywords related to ESG, HRM, sustainability, micro, small, and medium-sized enterprises (MSMEs), and the food and beverage industry. ("ESG" OR "Environmental Social Governance") AND ("Human Resource Management" OR "HRM") AND ("MSMEs" OR "Micro Small Medium Enterprises" OR "SMEs") AND ("Food and Beverage Industry") AND ("Competitiveness" OR "Business Performance" OR "Competitive Advantage").

Table 1. Inclusion and exclusion criteria

|

Category |

Inclusion Criteria |

Exclusion Criteria |

|

Type of Publication |

Peer-reviewed journal articles |

Conference papers, book chapters, dissertations, editorials, reports, non–peer-reviewed sources |

|

Indexing |

Q1 – Q4 |

Journals not indexed in Scopus/WoS |

|

Study Focus |

Studies examining ESG, HRM, sustainability, or their integration within MSMEs/SMEs |

Studies focusing only on large corporations, public sector, NGOs, or unrelated industries |

|

Language |

English |

Non-English publications |

|

Time Frame |

Published between 2016–2025 |

Published before 2016 |

The initial search yielded a total of 1,250 records across both databases (Figure 1). During the identification stage, several exclusion criteria (Table 1) were applied. First, duplicate records were removed. Following this filtering process, 762 unique records proceeded to the screening phase. Based on a review of titles and abstracts, 657 articles were excluded due to a lack of relevance to the research topic. The remaining 105 full-text articles were successfully retrieved for further evaluation. Quality appraisal of all full-text articles was conducted using the Mixed Methods Appraisal Tool (MMAT 2018) to ensure methodological rigor. Two independent reviewers assessed each study, and only articles scoring ≥60% were retained for synthesis. Any discrepancies were resolved through discussion, resulting in a substantial inter-rater reliability (Cohen’s kappa = 0.81). Following this appraisal process, 40 high-quality studies were included in the final review. No supplementary records were identified through other sources during the process.

Figure 1. PRISMA diagram flow

3.1 Descriptive analysis of journals publishing ESG and HRM studies in F&B MSMEs (2016–2024)

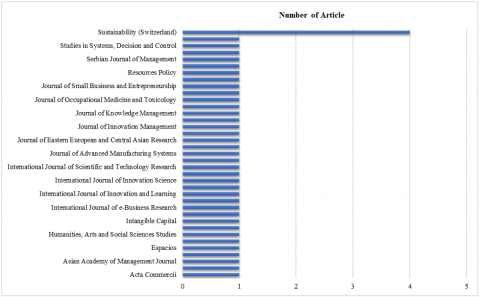

Figure 2 highlights the most frequent source journals (Q1 until Q4) contributing to the literature on ESG and HRM integration in food and beverage MSMEs. Based on the SLR conducted from Scopus and Web of Science databases, articles were published most frequently in Sustainability. These journals are reputable outlets in the sustainability and management fields, and indexed in the top quartiles (Q1) of Scopus.

Figure 2. Journal name (Source Title)

Table 2. Journal name (Source Title) 2016-2025 years

|

No. |

Journal / Source Title |

Number of Articles |

Year |

|

1 |

Sustainability |

4 |

2019, 2020, 2022 |

|

2 |

Acta Commercii |

1 |

2020 |

|

3 |

African Journal of Science, Technology, Innovation and Development |

1 |

2024 |

|

4 |

Asian Academy of Management Journal |

1 |

2023 |

|

5 |

Asian Economic and Financial Review |

1 |

2019 |

|

6 |

Espacios |

1 |

2017 |

|

7 |

Finance Research Letters |

1 |

2025 |

|

8 |

Humanities, Arts and Social Sciences Studies |

1 |

2021 |

|

9 |

IBIMA Business Review |

1 |

2020 |

|

10 |

Intangible Capital |

1 |

2024 |

|

11 |

International Journal of Applied Business and Economic Research |

1 |

2017 |

|

12 |

International Journal of e-Business Research |

1 |

2021 |

|

13 |

International Journal of Information Systems and Project Management |

1 |

2017 |

|

14 |

International Journal of Innovation and Learning |

1 |

2016 |

|

15 |

International Journal of Innovation and Technology Management |

1 |

2020 |

|

16 |

International Journal of Innovation Science |

1 |

2020 |

|

17 |

International Journal of Production Economics |

1 |

2022 |

|

18 |

International Journal of Scientific and Technology Research |

1 |

2019 |

|

19 |

International Journal of Sustainable Development and Planning |

1 |

2024 |

|

20 |

Journal of Advanced Manufacturing Systems |

1 |

2021 |

|

21 |

Journal of Asian Finance, Economics and Business |

1 |

2021 |

|

22 |

Journal of Eastern European and Central Asian Research |

1 |

2023 |

|

23 |

Journal of Environmental Management |

1 |

2024 |

|

24 |

Journal of Innovation Management |

1 |

2020 |

|

25 |

Journal of Islamic Economics, Banking and Finance |

1 |

2018 |

|

26 |

Journal of Knowledge Management |

1 |

2018 |

|

27 |

Journal of Lifestyle and SDGs Review |

1 |

2025 |

|

28 |

Journal of Occupational Medicine and Toxicology |

1 |

2023 |

|

29 |

Journal of Risk and Financial Management |

1 |

2022 |

|

30 |

Journal of Small Business and Entrepreneurship |

1 |

2020 |

|

31 |

Quality - Access to Success |

1 |

2023 |

|

32 |

Resources Policy |

1 |

2024 |

|

33 |

Science Progress |

1 |

2024 |

|

34 |

Serbian Journal of Management |

1 |

2022 |

|

35 |

Strategic Management Journal |

1 |

2017 |

|

36 |

Studies in Systems, Decision and Control |

1 |

2025 |

|

37 |

Technology Analysis and Strategic Management |

1 |

2023 |

In order to provide a comprehensive overview of the literature supporting this study, Table 2 outlines the key journals and sources from which references were drawn. Each entry includes the number of articles utilized and the corresponding year of publication. This compilation not only reflects the multidisciplinary nature of the ESG and HRM discourse but also demonstrates the currency and relevance of the selected materials. A significant portion of the references come from highly reputable journals published between 2020 and 2024, indicating a strong emphasis on recent advancements and contemporary debates in the field. The dominance of sources such as the Sustainability suggests that sustainability issues remain central to academic inquiry, particularly in the context of integrating ESG frameworks into human resource strategies within MSMEs. Table 2 serves as a valuable resource for mapping the scholarly terrain and identifying key contributors to the ongoing conversation around sustainable enterprise management.

These journals were chosen for their consistent focus on topics such as green human resource practices, environmental performance, responsible governance, and SME sustainability transitions [4, 8, 10]. The prominence Sustainability indicates the interdisciplinary nature of this research domain and the growing demand for integrating HRM and ESG perspectives within small enterprise contexts.

Table 3. Top 10 keyword frequency

|

Keyword |

Frequency |

|

ESG |

12 |

|

HRM |

10 |

|

MSMEs |

9 |

|

Sustainability |

8 |

|

Food Industry |

6 |

|

Governance |

5 |

|

Green HRM |

5 |

|

Leadership |

4 |

|

Environmental |

4 |

|

Small Enterprises |

3 |

The publication trend, which spans from 2020 to 2024, reflects a growing academic interest in the intersection of ESG performance and human resource capabilities (Table 3) especially within resource-constrained and highly competitive sectors such as food and beverage.

An analysis of the 40 selected articles revealed a concentration of publications across a relatively small group of well-established academic publishers. As shown in the publisher distribution Table 4, MDPI emerged as the most dominant publisher, contributing 5 articles of the total, primarily through its high-impact journals such as the Sustainability and Journal of Risk and Financial Management. MDPI’s contribution underscores its focus on interdisciplinary research that integrates sustainability, environmental governance, and strategic management [11]. Following closely, Elsevier published 3 articles, mostly in the journal Resources Policy, which has become a widely used platform for open-access research on ESG issues, particularly within MSMEs and emerging markets [4]. World Scientific, Routledge, and Emerald, each of them contributed 2 articles, with key journals like Journal of Knowledge Management and International Journal of Innovation and Technology Management, both of which emphasize the strategic alignment of HR practices with organizational sustainability goals [8]. Meanwhile, publishers such as Springer Nature, Academic Press, and SAGE also have notable presence, which articles focused on innovation, corporate social responsibility, and SME performance in sustainable contexts.

Table 4. List of publishers

|

No. |

Publisher |

Number of Articles |

|

1 |

MDPI |

5 |

|

2 |

Elsevier |

3 |

|

3 |

World Scientific |

2 |

|

4 |

Routledge |

2 |

|

5 |

Emerald |

2 |

|

6 |

Others |

26 |

|

Total |

40 |

|

This distribution confirms that high-quality research on ESG and HRM in MSMEs particularly within the food and beverage sector is largely disseminated through Q1 until Q4 journals associated with reputable publishers. The presence of open-access platforms (e.g., MDPI) alongside traditional publishers reflects a shift in scholarly communication, providing broader visibility and accessibility for sustainability research across disciplines and regions [10].

The methodological approaches adopted in the reviewed studies demonstrate the diverse strategies scholars have used to investigate ESG and HRM integration in food and beverage MSMEs.

Table 5. Research methods used in reviewed articles

|

No. |

Method Used |

Number of Articles |

|

1 |

Qualitative Case Study |

11 |

|

2 |

Quantitative Survey |

9 |

|

3 |

Mixed Methods |

6 |

|

4 |

Systematic Literature Review |

10 |

|

5 |

Content Analysis |

4 |

|

Total |

40 |

|

As shown in Table 5, qualitative case studies were the most common approach (n = 11), reflecting the exploratory nature of ESG-HRM practices in diverse organizational contexts. These studies often employed interviews or participatory observations to understand sustainable human resource interventions [10]. Quantitative surveys were used in 9 studies, focusing on measurable variables such as employee behavior, ESG performance, or stakeholder perceptions using Likert-scale instruments and statistical regression techniques [4].

Mixed-methods designs accounted for 6 articles, integrating both qualitative insights and statistical validation to strengthen findings and bridge theoretical-practical gaps. Meanwhile, SLR were prominent (n = 10), indicating strong academic interest in consolidating theoretical frameworks and identifying emerging themes [8]. Lastly, content analysis was used in 4 studies to evaluate company reports, policies, or media content relating to ESG disclosures and HRM policy alignment. This diversity in methodology indicates the multidisciplinary and evolving nature of ESG-HRM research in MSMEs. While qualitative insights offer contextual richness, the increasing adoption of quantitative and mixed methods signals a shift toward empirical generalizability and policy relevance in this field.

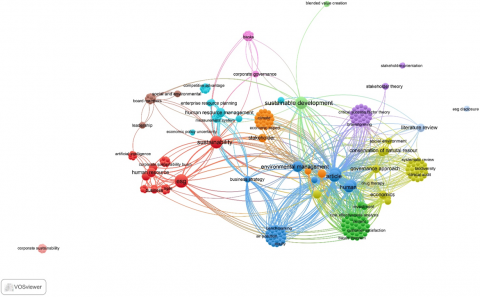

The keyword co-occurrence network visualization generated using VOS viewer provides a comprehensive overview of the thematic structure in the literature on ESG implementation and HRM in food and beverage MSMEs. This bibliometric map identifies several clusters of related keywords, reflecting distinct yet interconnected research themes. The red cluster, prominently featuring terms such as ESG, human resource, sustainability, and leadership, signifies a growing academic focus on the integration of sustainable governance principles into HRM practices. The blue cluster highlights methodological and review-focused contributions, with keywords like article, literature review, governance approach, and systematic review, suggesting a foundational base of conceptual and framework-building studies. The green cluster, centered on sustainable development, corporate governance, and stakeholder, indicates a strong emphasis on external accountability and stakeholder theory as key lenses for ESG-HRM discourse. Meanwhile, the yellow cluster, including economics, investment, and conservation of natural resources, reflects the environmental and financial implications of sustainable business practices. The purple and brown clusters reveal emerging interests in theoretical underpinnings (e.g., stakeholder theory, critical success factors) and competitive advantages related to social and environmental strategies.

Larger nodes such as sustainability, ESG, and HRM signify high-frequency keywords, while the proximity and link strength among nodes demonstrate their semantic interrelation across the literature. This visualization underscores the multidisciplinary nature of ESG-HRM integration and highlights the central role of stakeholder-driven governance and sustainability leadership in shaping MSME strategies. These insights align with recent studies emphasizing the strategic value of green HRM and ESG alignment in driving competitive and ethical performance in small enterprises.

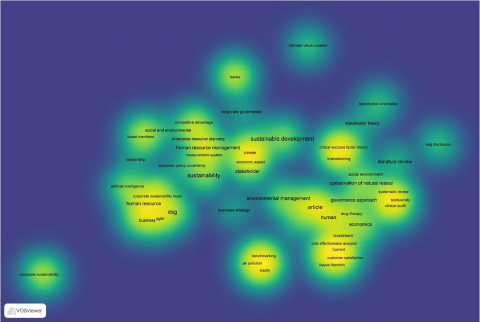

The heatmap visualization generated using VOS viewer (Figure 3) illustrates the density and intensity of author keyword co-occurrences within the reviewed literature on ESG, HRM, and sustainability practices in MSMEs, particularly in the food and beverage sector. In this map, areas with yellow and bright green clusters represent high-frequency keywords, indicating dominant research themes, while blue or purple areas reflect less frequent or emerging topics. The most prominent terms in this map include ESG, HRM, sustainability, sustainable development, and stakeholder, all of which appear in the brightest zones, suggesting their centrality in the discourse. The concentration around governance approach, literature review, and human also implies a significant emphasis on theoretical and methodological contributions to the field (Figure 4).

Moreover, the heatmap shows that ESG research in the MSME context is closely linked to broader themes such as corporate governance, economic aspect, and conservation of natural resources. The clustering of keywords like investment, customer satisfaction, equity, and air pollution near the economic and governance themes indicates an interdisciplinary integration of environmental and economic performance indicators. Meanwhile, the presence of artificial intelligence and high performance sustainable work systems in the outer, less dense areas suggests these are emerging concepts with growing scholarly interest. This visualization complements the co-occurrence network by emphasizing the hotspots of academic focus, reaffirming the growing integration of HRM strategies within ESG frameworks for MSMEs. As such, this heatmap aids in identifying both the core knowledge areas and underexplored themes within the field, offering valuable direction for future research on sustainable enterprise transformation.

Figure 3. The visualization of keyword using the VOS viewer

Figure 4. Density and intensity of author keyword co-occurrences

3.2 Thematic analysis

The final synthesis of 40 selected studies reveals several important findings regarding HRM practices that support ESG implementation in food and beverage MSMEs:

(1) What HRM practices have been identified in the literature to support ESG implementation in MSMEs?

The review uncovers practices such as green recruitment, employee environmental training, sustainability-focused performance evaluations, ethical labor standards, and employee engagement in ESG goals [4, 8]. In the MSME context, where formal structures may be limited, these HRM practices are often adapted to fit flexible and resource constrained environments. By mapping these practices, the study highlights how human capital can act as a strategic lever for advancing sustainability in small enterprises. The study highlights the strategic role of human capital in advancing sustainability within small enterprises, particularly MSMEs. Human capital which encompasses employees' skills, knowledge, values, and competencies is identified as a critical enabler for embedding ESG principles into daily business operations [20, 31]. Unlike larger corporations with dedicated sustainability departments, small enterprises often rely heavily on individual and collective capabilities to implement sustainable practices. The study emphasizes that investing in training, leadership development, and fostering an ESG-oriented organizational culture equips employees at all levels with the tools necessary to make environmentally and socially responsible decisions [32, 33]. This makes human capital not merely a workforce asset but a strategic lever for transforming business models toward more sustainable trajectories. Moreover, the study demonstrates that human capital drives innovation, enhances stakeholder trust, and improves organizational resilience all of which are vital for long term sustainability [34]. Particularly in resource-constrained settings, human capital becomes the bridge between sustainability goals and operational execution, ensuring that sustainable development is not just a policy statement, but a lived practice. The research underscores that empowering human capital within small enterprises is not a passive support function; rather, it is a proactive strategic driver that amplifies the impact of sustainability initiatives, aligns business practices with ESG objectives, and strengthens the enterprise’s competitive edge in an increasingly sustainability driven economy [35]. The findings of the analysis reveal that the level of Green Financing literacy among MSMEs remains considerably low. A significant proportion of MSME actors lack a comprehensive understanding of the benefits, objectives, and operational mechanisms of green financing instruments. This limited awareness constrains their ability to adopt sustainable financial solutions that are essential for transitioning toward environmentally responsible business models.

Moreover, the study identifies structural and procedural barriers that hinder MSMEs from accessing Green Financing schemes. These include complex loan application procedures, insufficient dissemination of relevant information by financial institutions, and the limited capacity of MSMEs to implement eco-friendly practices due to resource constraints and inadequate technical knowledge. These insights underscore the urgent need for targeted interventions aimed at enhancing MSMEs’ financial literacy in the context of environmental sustainability. Systematic and widespread outreach initiatives including training sessions, policy briefings, and accessible information platforms are necessary to bridge the knowledge gap. Furthermore, financial institutions must streamline their processes and offer tailored advisory support to facilitate MSMEs’ engagement with green finance opportunities. By improving both literacy and access, this approach seeks to empower MSMEs to embrace sustainable business practices, strengthen their long-term competitiveness, and contribute meaningfully to addressing environmental challenges.

(2) How do existing HRM-ESG models apply to MSMEs in the food and beverage sector?

The literature suggests that many existing models are developed for large corporations with standardized HR departments, which may not be suitable for MSMEs characterized by informal structures, limited resources, and direct owner involvement [11]. The implementation of ESG principles within MSMEs is crucial not only from an environmental standpoint but also from social and governance perspectives. As entities embedded within communities, MSMEs bear a responsibility to operate beyond mere profit generation by contributing positively to both societal well-being and environmental sustainability. This encompasses a wide range of practices, including environmentally responsible production methods and the cultivation of constructive relationships with key stakeholders, such as customers and employees. In a country like Indonesia where MSMEs constitute a substantial portion of the economy the adoption of ESG presents both significant challenges and transformative opportunities. The Indonesian government has taken several steps to support MSMEs through sustainable development initiatives; however, substantial efforts are still required to ensure that MSMEs can meaningfully contribute to the achievement of the Sustainable Development Goals (SDGs). One of the key strategies to support MSMEs in adopting ESG principles is through collaboration with financial institutions, particularly banks. Both conventional and Islamic banks in Indonesia are expected to play a pivotal role in facilitating sustainable financing for MSMEs. Green financing emerges as a critical instrument that can enable MSMEs to transition toward more environmentally responsible business practices. In addition to financial support, regulatory backing from the government and financial authorities is essential to ensure that MSMEs have easier access to sustainable financing mechanisms.

The review identifies a need for adaptable and scalable frameworks that allow small businesses to incorporate ESG through HR without incurring prohibitive costs. ESG frameworks serve as standardized tools to evaluate a company's sustainability performance and the potential value derived from implementing ESG initiatives. ESG metrics help stakeholders including investors, regulators, and policymakers consistently assess corporate sustainability outcomes. A recent meta-analysis investigates the influence of ESG disclosures on firm performance by examining both the aggregated impact of ESG reporting and the individual effects of ESG disclosures. This study includes a sub-group analysis that evaluates firm performance using three key indicators: (1) cost of capital (including weighted average cost of capital, equity cost, and debt cost), (2) accounting-based performance measures (such as return on assets, return on equity, and earnings per share), and (3) market-based metrics (notably Tobin’s Q). To account for heterogeneity in outcomes, the analysis integrates moderator variables like firm size and visibility, along with control factors such as ownership structure, R&D intensity, capital expenditure, sales growth, firm age, risk profile, data source, and publication quality. There is a strong positive relationship between ESG disclosure and firm performance, especially regarding the environmental and social dimensions. Notably, all ESG components are linked to a reduction in capital costs and an enhancement in performance outcomes. The study recommends that companies adopt robust environmental protections, decentralize ESG reporting practices, implement mandatory transparency regulations, develop risk management strategies, and build ESG-focused data repositories to strengthen long-term sustainability practices.

(3) What are the barriers and enablers for adopting integrated HRM-ESG strategies in these businesses?

The literature identifies multiple barriers, such as limited ESG awareness, lack of regulatory incentives, insufficient HR capacity, and resistance to change. On the other hand, enablers include leadership commitment, stakeholder pressure (e.g., from buyers or investors), external support (e.g., government programs or NGOs), and alignment of sustainability with business performance [10]. Understanding these factors is crucial for designing interventions that can increase ESG adoption at the micro enterprise level. Despite increasing global attention to sustainability, the implementation of Environmental Management Systems (EMS) within MSMEs particularly in the food and beverage sector remains limited, especially in developing countries such as Indonesia. Studies on EMS adoption in UK-based SMEs show that internal barriers often outweigh external ones, a pattern that appears relevant in the Indonesian context as well. Resource-related challenges are among the most frequently cited limitations, including insufficient technical expertise (e.g., absence of environmental specialists), constrained managerial time, and unexpected capital expenditures [36]. These issues are especially acute among Indonesian MSMEs in the food and beverage industry, which typically operate with minimal staffing, limited access to technology, and tight operational budgets.

Moreover, many MSME owners in Indonesia exhibit a low level of awareness regarding the strategic benefits of EMS adoption. This includes limited understanding of their operational environmental impact, poor familiarity with sustainability reporting, and inadequate exposure to formalized EMS frameworks. These knowledge gaps often extend to the regulatory environment, as MSMEs may lack clarity on the legal obligations and incentives tied to sustainable practices. As in the UK case, Indonesian MSMEs also show uncertainty about how to sustain and improve their environmental performance over time. Compounding these issues are inconsistent leadership support, resistance to organizational change, and competitive disadvantages when compared to larger firms that are more proactive in environmental compliance. Given the growing significance of food safety, waste reduction, and resource efficiency in the food and beverage sector, these challenges underscore the urgent need for capacity-building initiatives tailored to Indonesian MSMEs. Interventions could include sector-specific training, regulatory simplification, incentive-based green financing, and greater collaboration between MSMEs, government bodies, and financial institutions.

Addressing internal constraints is critical to enabling broader EMS adoption and ensuring that MSMEs in Indonesia actively contribute to national and global sustainability goals. A systematic review of HRM-ESG implementation in UK based SMEs reveals that internal limitations are more frequently reported than external ones (see Table 6), suggesting that many of the barriers are rooted within the organizational structure and capacity of the enterprises themselves. Among the most commonly cited constraints are inadequate technical capabilities, including the lack of specialist staff, limited managerial time, and unforeseen capital expenditures. These resource constraints are often compounded by a lack of awareness of environmental impacts, limited understanding of environmental reporting, and unfamiliarity with formal EMS frameworks.

Table 6. Most frequently reported internal barriers to HRM-ESG implementation in SMEs (based on 40 reviewed studies)

|

Internal Limitation |

Number of Studies (n = 40) |

|

Lack of specialist staff |

12 |

|

Insufficient managerial time |

10 |

|

Unexpected capital expenditure |

9 |

|

Limited awareness of environmental impacts |

4 |

|

Poor understanding of environmental reporting |

2 |

|

Unfamiliarity with formal HRM-ESG systems |

1 |

|

Inconsistent management support |

1 |

|

Resistance to change |

1 |

(4) What future research directions are suggested by the current literature?

The literature calls for more empirical research in emerging economies, development of MSME-specific ESG-HRM models, and cross-sector comparative studies. Additionally, there is growing interest in exploring the role of digital tools, such as AI and HR analytics, in advancing ESG-HRM integration, as well as the long-term impact of such strategies on employee well-being, innovation, and resilience [4]. The current literature on ESG, HRM, and sustainability presents several potential avenues for future investigation. First, there is a growing need to explore the practical integration of ESG principles within HRM systems particularly how green HRM practices contribute to organizational sustainability and employee performance, especially within MSMEs in emerging economies [8, 32]. Despite the presence of research linking ESG to corporate strategy, governance and performance metrics, the HR dimension remains relatively underexamined. Second, stakeholder orientation and governance mechanisms require further analysis, particularly in terms of how different stakeholder engagement models impact ESG adoption and compliance. This is particularly relevant for institutions operating in hybrid systems, such as Islamic banks or cooperatives, which may hold alternative governance logics. Third, digital transformation and environmental management are emerging but underexplored themes in the ESG discourse. The role of enterprise resource planning (ERP), artificial intelligence (AI), and digital dashboards in tracking, reporting, and benchmarking ESG performance merits greater attention [37]. Fourth, standardization of ESG disclosure practices remains a critical challenge. More research is needed to develop and test sector-specific ESG reporting frameworks especially for small businesses and MSMEs operating in high-impact sectors such as food and beverage [38].

Fifth, environmental governance research could be expanded to better integrate conservation, biodiversity, and sustainable resource use into corporate ESG strategies. This intersection remains fragmented in current literature. Finally, given the limited ESG preparedness among MSMEs in developing nations, future studies should examine how green financing, government incentives, and policy instruments can enhance ESG readiness and adoption. A cross-disciplinary approach that incorporates environmental science, economics, and organizational behavior would be especially valuable in addressing these gaps.

3.3 The integration model of MSME-HRM-ESG

Synthesizing the findings from the 40 reviewed articles, this study proposes an MSME-oriented HRM–ESG Integration Model specifically tailored for food and beverage enterprises. The model links HRM levers to ESG outcomes through a set of organizational translation mechanisms, while also accounting for MSME-specific moderators. It responds directly to the gap identified in the literature, where most existing ESG and green HRM frameworks are designed for large, formally structured organizations and are therefore difficult to operationalize in resource-constrained MSMEs

At the input level, the model identifies four core HRM levers: (1) green recruitment and selection, emphasizing the hiring of employees who value sustainability and ethical conduct; (2) ESG-oriented training and development, which builds employees’ environmental and social competencies; (3) sustainability-linked performance management and rewards, where ESG criteria are integrated into appraisal and incentive systems; and (4) ethical and sustainability-oriented leadership, in which owners and managers act as role models for ESG practices.

These HRM levers operate through ESG translation mechanisms that embed sustainability into everyday routines. The review highlights three main mechanisms: (a) the development of an ESG-supportive organizational culture that normalizes pro-environmental and socially responsible behaviour; (b) employee engagement and participation in ESG initiatives, such as waste-reduction projects or community programmes; and (c) knowledge-sharing and green innovation, where employees jointly identify and experiment with ESG-related process improvements.

At the output level, the model distinguishes between three clusters of ESG outcomes. Environmental outcomes include resource efficiency, reduced waste and emissions, and adherence to environmental regulations. Social outcomes capture employee well-being, fair labour practices, and contributions to local communities. Governance outcomes relate to transparency, accountability, and compliance with ethical standards. In MSMEs, these ESG outcomes are closely tied to business performance outputs, such as cost savings, reputation, customer loyalty, and long-term resilience.

The model also incorporates mediators and moderators that shape how HRM levers translate into ESG outcomes. Empirical evidence suggests that ESG-oriented organizational culture and employee green behaviour often mediate the relationship between HRM practices and sustainability performance. At the same time, typical MSME characteristics, such as resource constraints, owner-manager values, regulatory and stakeholder pressures, and the degree of digitalization, act as moderators that can either strengthen or weaken HRM–ESG linkages. This model provides a conceptual roadmap for designing future empirical studies on HRM–ESG integration in MSMEs. It also offers a practical guide for owners, managers, and policymakers who seek to implement ESG principles through simple, scalable HRM practices adapted to the realities of food and beverage MSMEs in emerging economies.

This study underscores the increasing significance of integrating ESG principles into the operational and strategic management of MSMEs, with a particular focus on the food and beverage sector. As global attention to sustainability intensifies, ESG has emerged as a vital framework for promoting ethical governance, environmental stewardship, and social responsibility. For MSMEs, especially those operating in resource-sensitive sectors like food and beverage, adopting ESG practices is not only a matter of compliance but also a strategic imperative for long-term competitiveness and market resilience. However, the study reveals that the implementation of ESG within MSMEs remains relatively underdeveloped. A range of internal barriers such as limited awareness, insufficient technical expertise, and lack of financial and human capital continue to hinder widespread ESG adoption. These challenges are further compounded by managerial inertia and a lack of structured policy support tailored to the specific needs of small enterprises. Unlike larger corporations, MSMEs often lack dedicated sustainability units, making ESG integration more complex and fragmented. The role of HRM in facilitating ESG goals is another critical but often overlooked dimension. HRM functions such as green recruitment, environmental training, performance appraisal, and employee engagement can significantly support the internalization of ESG values across the organization. Nonetheless, current research tends to treat HRM and ESG as separate domains, leaving a gap in understanding their potential synergies, particularly within the MSME context. Furthermore, the study identifies the need for stronger collaboration between MSMEs and financial institutions to expand access to green financing instruments. Regulatory bodies and policymakers also play a crucial role in setting clear guidelines, offering incentives, and promoting ESG literacy. Addressing these institutional and capacity based gaps is essential for enabling MSMEs to become active agents of sustainable development.

To address these challenges, it is recommended that future research focus on developing context-specific ESG-HRM integration models tailored to MSMEs in emerging economies. Governments and financial authorities should intensify efforts to provide accessible green financing schemes and capacity-building programs. Additionally, companies should be encouraged to adopt digital tools and transparent reporting systems to improve ESG implementation. Interdisciplinary approaches that connect environmental science, finance, and organizational behavior will be essential in advancing sustainability efforts and ensuring that MSMEs contribute meaningfully to national and global sustainable development goals.

[1] Setyaningsih, S., Widjojo, R., Kelle, P. (2024). Challenges and opportunities in sustainability reporting: A focus on small and medium enterprises (SMEs). Cogent Business & Management, 11(1): 2298215. https://doi.org/10.1080/23311975.2023.2298215

[2] Verma, T.L., Nema, D.K. (2019). Role of micro, small and medium enterprises (MSMES) in achieving sustainable development goals. International Journal for Research in Engineering Application & Management, 4(12): 575-582. https://doi.org/10.18231/2454-9150.2019.0189

[3] Kamble, S., Gunasekaran, A., Dhone, N.C. (2020). Industry 4.0 and lean manufacturing practices for sustainable organisational performance in Indian manufacturing companies. International Journal of Production Research, 58(5): 1319-1337. https://doi.org/10.1080/00207543.2019.1630772

[4] Mabaya, E., Babadara, J.B., Jagne, J., Mubichi-Kut, F. (2025). ESG for a small enterprise in an emerging market: Airsmat’s innovative approach to sustainable agriculture in Nigeria. International Food and Agribusiness Management Review, 1: 1-14. https://doi.org/10.22434/ifamr.1256

[5] Zhang, Y. (2025). Small and medium-sized enterprises in the green transition: Survival and sustainability challenges in ESG practices. Journal of Frontier in Economic and Management Research, 1(1): 429-438. https://doi.org/10.63944/2q3JFEMR

[6] Fatima, M., Ata, G., Rizwan, A. (2023). Institutional pressures and sustainable business practices: A case of strategic environmental management. Global Economics Review, 8(1): 196-212. https://doi.org/10.31703/GER.2023(VIII-I).18

[7] Shahzad, M.A., Wang, X., Li, Z., Junaid, M. (2025). The nexus between green HRM, employee well-being, and citizenship behavior: Exploring the mediating role of employee sustainability and motivation. International Journal of Hospitality Management, 126: 104053. https://doi.org/10.1016/j.ijhm.2024.104053

[8] Sharma, D., Bhardwaj, B. (2025). Green human resource management practices and sustainable development in India: A systematic literature review and future research agenda. Social Sciences & Humanities Open, 11: 101420. https://doi.org/10.1016/j.ssaho.2025.101420

[9] Becker, K., Smidt, M. (2016). A risk perspective on human resource management: A review and directions for future research. Human Resource Management Review, 26(2): 149-165. https://doi.org/10.1016/j.hrmr.2015.12.001

[10] Arshad, M.Z., Liu, C. (2025). Promoting pro-green behavior towards sustainable excellence: Unveiling the path from strategic Green HRM practices and green innovation to sustainable performance. Acta Psychologica, 261: 105859. https://doi.org/10.1016/j.actpsy.2025.105859

[11] Setyadi, A., Pawirosumarto, S., Damaris, A., Syarif, D. (2025). Integrating green HRM and sustainable operations: The moderating role of digital transformation in the Indonesian energy sector. Discover Sustainability, 6(1): 924. https://doi.org/10.1007/s43621-025-01764-y

[12] Ahmad, S., Javed, U., Sharma, C., Siddiqui, M.S. (2025). Green human resource management: Analyzing sustainable practices and organizational impact through a Word2Vec approach. Green Technologies and Sustainability, 3(4): 100224. https://doi.org/10.1016/j.grets.2025.100224

[13] Ehnert, I., Parsa, S., Roper, I., Wagner, M., Muller-Camen, M. (2016). Reporting on sustainability and HRM: A comparative study of sustainability reporting practices by the world's largest companies. The International Journal of Human Resource Management, 27(1): 88-108. https://doi.org/10.1080/09585192.2015.1024157

[14] Bag, S., Dhamija, P., Pretorius, J.H.C., Chowdhury, A.H., Giannakis, M. (2022). Sustainable electronic human resource management systems and firm performance: An empirical study. International Journal of Manpower, 43(1): 32-51. https://doi.org/10.1108/IJM-02-2021-0099

[15] Eurostat. (2024). Micro & small businesses make up 99% of enterprises in the EU. https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20241025-1.

[16] Harney, B. (2021). Accommodating HRM in small and medium-sized enterprises (SMEs): A critical review. Economic and Business Review, 23(2): 72-85. https://doi.org/10.15458/2335-4216.1007

[17] Lundmark, E., Coad, A., Frankish, J.S., Storey, D.J. (2020). The liability of volatility and how it changes over time among new ventures. Entrepreneurship Theory and Practice, 44(5): 933-963. https://doi.org/10.1177/1042258719867564

[18] Yadav, G., Luthra, S., Jakhar, S.K., Mangla, S.K., Rai, D.P. (2020). A framework to overcome sustainable supply chain challenges through solution measures of Industry 4.0 and circular economy: An automotive case. Journal of Cleaner Production, 254: 120112. https://doi.org/10.1016/j.jclepro.2020.120112

[19] Nudurupati, S.S., Budhwar, P., Pappu, R.P., Chowdhury, S., Kondala, M., Chakraborty, A., Ghosh, S.K. (2022). Transforming sustainability of Indian small and medium-sized enterprises through circular economy adoption. Journal of Business Research, 149: 250-269. https://doi.org/10.1016/j.jbusres.2022.05.036

[20] Langwell, C., Heaton, D. (2016). Using human resource activities to implement sustainability in SMEs. Journal of Small Business and Enterprise Development, 23(3): 652-670. https://doi.org/10.1108/JSBED-07-2015-0096

[21] Yong, J.Y., Yusliza, M.Y., Ramayah, T., Fawehinmi, O. (2019). Nexus between green intellectual capital and green human resource management. Journal of Cleaner Production, 215: 364-374. https://doi.org/10.1016/j.jclepro.2018.12.306

[22] Álvarez Jaramillo, J., Zartha Sossa, J.W., Orozco Mendoza, G.L. (2019). Barriers to sustainability for small and medium enterprises in the framework of sustainable development—literature review. Business Strategy and the Environment, 28(4): 512-524. https://doi.org/10.1002/bse.2261

[23] Dauerer, A. (2025). A systematic literature review of performance measurement systems and the integration of ESG factors. Environmental and Sustainability Indicators, 27: 100746. https://doi.org/10.1016/j.indic.2025.100746

[24] Zaridis, A.D., Mousiolis, D.T. (2014). Entrepreneurship and SME's organizational structure. Elements of a successful business. Procedia-Social and Behavioral Sciences, 148: 463-467. https://doi.org/10.1016/j.sbspro.2014.07.066

[25] Samputra, P.L., Alfarizi, M. (2025). Can advanced society 5.0 technology create economic and social value for millennial and Generation Z MSMEs in Surabaya, Indonesia? An economic resilience perspective. Asia Pacific Management Review, 30(3): 100355. https://doi.org/10.1016/j.apmrv.2025.100355

[26] Knight, G.A., Liesch, P.W. (2016). Internationalization: From incremental to born global. Journal of World Business, 51(1): 93-102. https://doi.org/10.1016/j.jwb.2015.08.011

[27] Kolk, A. (2016). The social responsibility of international business: From ethics and the environment to CSR and sustainable development. Journal of World Business, 51(1): 23-34. https://doi.org/10.1016/j.jwb.2015.08.010

[28] Page, M.J., McKenzie, J.E., Bossuyt, P.M., Boutron, I., et al. (2022). The Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) statement. Revista Panamericana de Salud Pública, 46: 1-12. https://doi.org/10.26633/rpsp.2022.112

[29] Boon, C., Den Hartog, D.N., Lepak, D.P. (2019). A systematic review of human resource management systems and their measurement. Journal of Management, 45(6): 2498-2537. https://doi.org/10.1177/0149206318818718

[30] Hosen, M.S., Ahmad, S., Shamoon, S., Anwer, S., Hassan, S.M.S., Saeed, A. (2024). Navigating the global market focusing on AI: An analysis on strategic insights for entrepreneurs. Educational Administration: Theory and Practice, 30(5): 14337-14345. https://doi.org/10.53555/kuey.v30i5.6588

[31] Shari, W., Hassan, M.H.A., Ezanee, A.A.M., Wahab, N.M.A., Abd Wahab, N. (2024). Ways to promote sustainable practices among Malaysian SMEs from the viewpoints of experts. Journal of Asian Scientific Research, 14(4): 597-611. https://doi.org/10.55493/5003.v14i4.5179

[32] Nisar, Q.A., Haider, S., Ali, F., Jamshed, S., Ryu, K., Gill, S.S. (2021). Green human resource management practices and environmental performance in Malaysian green hotels: The role of green intellectual capital and pro-environmental behavior. Journal of Cleaner Production, 311: 127504. https://doi.org/10.1016/j.jclepro.2021.127504

[33] Awwad Al-Shammari, A.S., Alshammrei, S., Nawaz, N., Tayyab, M. (2022). Green human resource management and sustainable performance with the mediating role of green innovation: A perspective of new technological era. Frontiers in Environmental Science, 10: 901235. https://doi.org/10.3389/fenvs.2022.901235

[34] Khan, M.H., Muktar, S.N. (2024). Green employee empowerment: The missing linchpin between green HRM and sustainable organizational performance. Journal of Cleaner Production, 434: 139812. https://doi.org/10.1016/j.jclepro.2023.139812

[35] Maheshwari, M., Samal, A., Bhamoriya, V. (2020). Role of employee relations and HRM in driving commitment to sustainability in MSME firms. International Journal of Productivity and Performance Management, 69(8): 1743-1764. https://doi.org/10.1108/IJPPM-12-2019-0599

[36] Rizos, V., Behrens, A., Van der Gaast, W., Hofman, E., et al. (2016). Implementation of circular economy business models by small and medium-sized enterprises (SMEs): Barriers and enablers. Sustainability, 8(11): 1212. https://doi.org/10.3390/su8111212

[37] Dubey, R., Gunasekaran, A., Childe, S.J., Blome, C., Papadopoulos, T. (2019). Big data and predictive analytics and manufacturing performance: Integrating institutional theory, resource-based view and big data culture. British Journal of Management, 30(2): 341-361. https://doi.org/10.1111/1467-8551.12355

[38] Kotsantonis, S., Serafeim, G. (2019). Four things no one will tell you about ESG data. Journal of Applied Corporate Finance, 31(2): 50-58. https://doi.org/10.1111/jacf.12346