Thi Thuy Viet Nguyen![]() | Anh Tuan Nguyen*

| Anh Tuan Nguyen*![]() | Thi My Nguyet Le

| Thi My Nguyet Le![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This research seeks to assess the influence of green intellectual capital—comprising green human capital (GHC), green structural capital (GSC), and green relational capital (GRC)—on corporate environmental performance (CEP) within manufacturing firms in Vietnam. It also examines the mediating effects of environmental management accounting (EMA) and corporate sustainability culture (CSC), while considering digital transformation (DT) as a moderating variable that impacts the relationships between EMA and CEP, as well as CSC and CEP. According to the RBV-KBV model and data gathered from 260 survey responses from manufacturing firms in Vietnam, the analysis reveals that both EMA and CSC have a positive impact on CEP. The EMA exerts a more significant influence (β = 0.631), and the R² index of CEP attains 0.687, surpassing 0.5, which signifies robust explanatory power of the model. The research clarifies the mechanism by which green intellectual capital influences environmental performance via mediating and moderating variables. The research findings substantiate the RBV-KBV model and propose practical implications to assist manufacturing enterprises in Vietnam in improving environmental performance via the management of green intellectual capital, EMA, sustainable culture, and coordinated digital transformation.

green intellectual capital, environmental performance, environmental management accounting, sustainable culture, digital transformation

In the context of the growing global focus on sustainable development, businesses are under increasing pressure to enhance economic efficiency [1] while also ensuring their environmental and social responsibility [2]. Since 2020, Vietnam's [3] digital transformation has led to substantial alterations in management practices, compelling companies to reorganize their resources, especially knowledge, culture, and accounting systems, to achieve sustainable development [4].

Green intellectual capital (GIC) refers to the administration of knowledge, skills, and experience related to the environment, incorporating ecological information into human, structural, and relational capital, thereby transforming it into an organizational asset that facilitates green management accounting and sustainable reporting [5]. The association between GIC and CEP is garnering heightened interest, especially regarding the mediating function of environmental management accounting [6, 7] and the regulatory influence of corporate sustainability culture [8].

Many studies globally have investigated the relationship among GIC, EMA, and CEP across different contexts in the digital era. Many studies in Pakistan have evaluated the influence of GIC on CEP, alongside an analysis of the mediating effect of EMA and the regulatory impact of stakeholder pressure [7, 9, 10]. In Egypt, the study by Alnaim and Metwally [6] focused on listed manufacturing companies, clarifying the moderating role of EMA in the relationship between GIC and CEP. In Japan, studies primarily approach the subject from the perspective of EMA and environmental cost measurement but fail to incorporate GIC, EMA, and CSC into the assessment of CEP [11, 12]. Martínez-Falcó et al. [13] conducted a survey of 211 manufacturing enterprises in China, demonstrating that GIC influences environmental performance via green innovation, while another study on 100 environmental enterprises, also in China, analyzed the impact of GIC on financial performance under the moderating influence of digital transformation. In Iran, the research conducted by Asiaei et al. [14] and Rizavi et al. [15] evaluates the impact of GIC and EMA on CEP within industrial and manufacturing sectors. Research conducted by Solovida and Latan [16] on 68 manufacturing businesses in Malaysia indicates that EMA serves as an intermediate in the interaction between environmental strategy and CEP. GIC fosters a sustainable competitive advantage for wineries in Spain by employing EMA and adhering to green business trends [7, 13]. According to Amir et al. [17], a study was conducted in Mexico on 234 small and medium enterprises (SMEs) in various industries to assess the impact of EMA and GIC on CEP. In Brazil, research by Tonial et al. [18] focused on GIC and sustainability activities, and Vale et al. [19] studied the link between sustainable intellectual capital and sustainability performance.

Recent research in Vietnam, published in international publications, such as Thanh Thuy Ngoc [20] and Oanh et al. [21], has preliminarily examined the interaction between GIC, EMA, and CEP within the framework of digital transformation. Nevertheless, existing research predominantly examines each factor in isolation, such as GIC [22] or EMA [23, 24], lacking a holistic investigation that integrates the elements of GIC, EMA, and CSC within the digital context pertinent to CEP. In light of Vietnam's significant transition to a green economy and the challenges posed by climate change, this topic aims to establish a robust research model that can be substantiated with empirical data in Vietnam.

While numerous prior research studies have investigated the relationship between GIC and CEP, the majority have concentrated solely on individual aspects of GIC, neglecting to elucidate the mediating influence of internal company factors such as EMA and CSC. Given the importance of the ongoing digital revolution, few studies examine how this factor regulates the relationship between GIC and CEP. In developing nations like Vietnam, researchers observe that actual data about the integrated model of GIC-EMA-CSC-CEP remains scarce. Therefore, this study fills the gap by:

(1) Developing a comprehensive research framework to concurrently evaluate the influence of the three components of green intellectual capital (GHC, GSC, and GRC) on environmental performance.

(2) Elucidating the mediation processes of EMA and CSC—critical elements that signify the internal governance competencies of organizations.

(3) Analyzing the regulatory function of digital transformation—an original and significantly pertinent element within the framework of the 4.0 technological revolution.

(4) Conducting an empirical study in Vietnam, where integrated studies on GIC and environmental performance remain limited.

2.1 Green intellectual capital

In this study, the author uses the Resource-Based View (RBV) of Wernerfelt [25] and Barney [26] and the Knowledge-Based View (KBV) of Grant [27] and Spender and Grant [28] as the model chosen as the theoretical framework. Because RBV/KBV provides a clear explanation of how GIC acts as a strategic resource, contributing to enhancing CEP. According to RBV, internal resources that are rare, difficult to substitute, and have strategic value, such as GHC, GSC, and GRC, form the foundation for sustainable competitive advantage. KBV extends this perspective by emphasizing the role of knowledge and creativity in transforming GIC into specific management actions, helping businesses optimize costs, reduce emissions, and improve environmental processes. Several recent studies have demonstrated that applying RBV/KBV in the context of GIC helps to identify clear boundary conditions: for example, the level of human resource skills development, knowledge sharing capabilities, and digital technology adoption determine the effectiveness of transforming GIC into CEP [29-31]. At the same time, this model also allows us to clarify potential theoretical contradictions; for example, when GIC is invested but lacks a green knowledge management mechanism or lacks a supporting technology platform, the positive impact on CEP may be reduced. Therefore, RBV/KBV not only explains the mechanism by which GIC affects CEP but also provides a foundation for building research hypotheses and identifying moderating and mediating variables in this research model.

GIC extends the concept of intellectual capital encompassing GHC, GSC, and green GRC. GIC represents an intangible asset associated with environmental considerations and sustainable development within accounting and management practices [32]. GIC fosters innovation and strengthens the green competitive advantage of businesses [30], contributing to improved environmental and financial efficiency [33]. GIC identifies human capital, structure, relationships, and innovation capital as essential factors for the implementation of environmental accounting [32]. Buhaya and Metwally [31] examine the relationship between GIC and green supply chain performance, emphasizing external pressures in relation to management accounting and internal reporting. The study by Martínez-Falcó et al. [7] demonstrates that GIC improves corporate culture within the framework of sustainable development.

2.1.1 Green human capital (GHC), environmental management accounting (EMA), and corporate sustainability culture (CSC) impact corporate environmental performance (CEP)

GHC significantly contributes to encouraging enterprises to implement and advance EMA [33]. It promotes the establishment of internal environmental reporting systems inside enterprises to facilitate the management of costs, risks, and CEP. It facilitates strategic decision-making pertaining to sustainable development, particularly within the manufacturing sector and industries with significant environmental effects [34]. It improves the ability to amalgamate financial and non-financial information, consequently augmenting sustainable value and competitiveness [7]. Research conducted by Hooi et al. [35] and Tran [36] highlights the importance of GHC in maintaining the CSC framework to improve CEP, as indicated by Muisyo and Qin [37].

Hypothesis (H1): GHC has a positive impact on EMA.

Hypothesis (H2): GHC has a positive impact on CSC.

2.1.2 Green structural capital (GSC), environmental management accounting (EMA), and corporate sustainability culture (CSC) impact corporate environmental performance (CEP)

GSC [38] is regarded as a crucial component of green intellectual capital. It includes systems, processes, databases, technologies, policies, and organizational frameworks designed to support environmental protection and sustainable development initiatives within enterprises [6]. Green structural capital functions as the organizational basis that facilitates the maintenance, storage, and dissemination of environmental knowledge across the entire internal governance framework.

EMA plays a vital intermediary function between green intellectual capital factors, such as GSC, and the sustainable performance of enterprises [34]. Information systems, internal assessment procedures, and sustainable operating standards are efficient instruments for the collection, processing, and broadcasting of environmental data [6]. When enterprises possess a flexible and sustainable organizational framework, the application of EMA methods, including environmental cost analysis, environmental reporting, and green cost control, is rendered more effective and pragmatic. Furthermore, GSC serves as a tool for decision-making, providing managers with crucial data to integrate environmental factors into their production and business strategies.

Hypothesis (H3): GSC has a positive impact on EMA.

GSC also significantly impacts CSC to enhance environmental efficiency [39, 40]. The organizational structure reflects the alignment of ideals, regulations, and internal operational standards. GSC encourages the sharing of ecological knowledge and actively engages employees in environmental conservation initiatives, which contributes to establishing a corporate culture focused on sustainable development [41].

Many experimental studies indicate that GSC significantly influences both EMA and CSC. The studies conducted by Yusliza et al. [42], Long and Liao [43], Azizan et al. [44], and Alnaim and Metwally [6] collectively affirm that factors such as green knowledge management systems, environmental databases, and sustainable integrated operational processes significantly enhance the quality of environmental governance and establish a foundation for creating a green culture within organizations.

Hypothesis (H4): GSC has a positive impact on CSC.

2.1.3 Green relational capital (GRC), environmental management accounting (EMA), and corporate sustainability culture (CSC) impact corporate environmental performance (CEP)

GRC is a strategic intangible asset that reflects the quality of relationships with external stakeholders [45], established based on environmental collaboration, mutual trust, and sustainable development objectives, thereby enhancing environmental efficiency through the sharing of knowledge and resources.

GRC and EMA impact CEP: GRC assists and encourages the implementation of EMA through information dissemination [14], stakeholder pressure, and the assimilation of external environmental practices [34]. Strong GRC within a corporation enhances the efficacy of EMA, therefore improving environmental performance. Both GRC and EMA are favorably impactful and mutually supportive factors in enhancing environmental performance [34, 46]. GRC facilitates the expansion of connections and the acquisition of knowledge, whereas EMA converts that knowledge into actionable practices and environmental results [6, 14].

Hypothesis (H5): GRC positively impacts EMA.

GRC and CSC impact environmental performance: GRC collaborates to promote CSC's environmental practices by integrating external information with internal culture, therefore improving environmental performance [47]. GRC offers external environmental expertise and resources, whereas CSC fosters sustainable behaviors and values internally [48]. The interplay of these two factors establishes an effective basis, helping organizations to attain excellent environmental performance [49, 50].

Hypothesis (H6): GRC has a positive impact on CSC.

2.2 Environmental management accounting (EMA) and corporate sustainability culture (CSC)

2.2.1 Environmental management accounting (EMA)

The Association of Chartered Certified Accountants defines EMA as the management of financial and non-financial information related to environmental costs [51], supporting internal environmental decision-making [52] and fostering sustainable development in enterprises [53]. The EMA evaluates material flows, both physical and financial, to ascertain the expenses associated with raw materials, energy, waste, and emissions [54]. This information encompasses environmental performance indicators, equipment investment costs [55], treatment expenses, prevention measures, research and development, and potential business savings [56], thereby assisting managers in making strategic decisions, optimizing resources, and supporting green innovation. The EMA serves as both a compliance instrument and a strategy framework that facilitates long-term decision-making for sustainable development [57]. EMA combined with an environmental strategy enhances environmental performance (CEP) and financial results [58].

Environmental management accounting impacts corporate sustainability culture: The studies performed by Pratiwi et al. [59] and Fatmasari et al. [60] analyze the impact of EMA on CSC, facilitating the advancement of behavior, values, and internal governance frameworks focused on sustainability [61], establishing a culture and internal discipline system, and encouraging environmentally friendly behaviors [62].

Hypothesis (H7): EMA has a positive impact on CSC.

EMA impacts CEP: EMA has an effective and significant influence on the environmental performance of manufacturing companies in Malaysia [63]. EMA is an effective instrument that assists enterprises in identifying, quantifying, and managing environmental costs, hence substantially improving the organization's CEP [64, 65]. EMA not only enhances CEP but also fosters financial profitability [66]. The referenced research concurs that EMA is strategically significant for manufacturing companies in safeguarding the environment and enhancing financial performance [20].

Hypothesis (H8): EMA has a positive impact on CEP.

2.2.2 Corporate sustainability culture (CSC)

The sustainable culture of a business is a leadership competency containing social responsibility [67] and involves creating transparent internal communication channels while pursuing sustainable development across economic, social, and environmental dimensions [68]. CSC asserts that internal attitudes and norms foster the utilization of accounting information aimed at the sustainable development of an environmentally conscious business culture [69]. Zyznarska-Dworczak [70] asserts that a sustainable culture is vital to building trust and openness in sustainability reporting.

CSC impacts CEP: CSC promotes adaptive skills, thereby enhancing CEP [71] throughout the organization, enabling the execution of green management techniques and the optimal utilization of resources [72]. Recent studies indicate that CSC not only directly influences CEP but also acts as a mediating or moderating factor through elements such as green human resource management, green innovation, and environmental strategy [73] within the manufacturing sector, aiding businesses in enhancing environmental compliance, reducing emissions, and enhancing sustainable operational efficiency [74] in the healthcare sector.

Hypothesis (H9): CSC has a positive impact on CEP.

2.3 Digital transformation (DT) in the field of accounting

DT in accounting [75] is the integration of digital technology into accounting practices to enhance managerial efficiency [21], precision, analytical capacities, and financial decision-making [76]. The focus extends beyond data digitalization to encompass the reorganization of accounting procedures, work automation, and the formulation of intelligent financial strategies via real-time data analysis [77].

2.3.1 DT acts as a regulatory variable in the relationship between EMA and CEP

The study [78] indicates that DT significantly improves the quality of EMA data regarding accuracy, timeliness, and predictability, therefore serving as a regulatory variable that amplifies the effect of EMA on CEP [79]. DT serves a regulatory function in diminishing carbon emissions, an effect further enhanced by elements such as tax policies or environmental subsidies [80]. DT assists businesses in making timely and appropriate environmental management decisions to enhance their CEP [81]. The research of Abdelhalim et al. [78] indicates that organizations with inadequate degrees of digital transformation frequently encounter challenges in data integration, information dissemination, and the deployment of EMA measurement instruments, hence constraining the beneficial effects of EMA on CEP.

DT not only supports EMA in terms of data collection and processing but also plays the role of an “amplifier” in turning EMA data into a strategic tool to improve the enterprise's CEP [82]. Specifically, digital technologies such as artificial intelligence, big data analytics, and cloud computing allow businesses to exploit EMA data in real time, thereby improving the ability to forecast emission trends and promptly provide solutions to minimize environmental risks [83]. As a result, EMA goes beyond merely recording environmental costs; it also serves as a strategic decision-making platform that significantly enhances CEP [84]. In contrast, in the context of a lack of digital transformation applications, EMA is often limited to reporting, which reduces the positive impact on CEP. This indicates that DT plays an important regulatory role, ensuring that EMA information is transformed into practical environmental management actions [85, 86].

Hypothesis (H10a): DT as a moderating variable enhances the positive impact of EMA on CEP.

2.3.2 DT acts as a regulating variable in the relationship between CSC and CEP

DT is considered an important factor that assists companies in enhancing the function of supply chain collaboration in sustainable development goals [87]. The integration of DT and supply chain collaboration enhances innovative capacities and advances full circular economy frameworks, encompassing environmental considerations [88, 89]. Digital transformation regulates and amplifies the influence of supply chain collaboration on green innovation and circular economy frameworks [90].

CSC plays a guiding role for all environmental management and strategy activities; however, the level of impact on CEP depends largely on the ability to implement and control. In the context of DT's role as an important regulator, it helps to amplify the positive impact of CSC on CEP [91, 92]. Recent studies show that DT enables businesses to integrate sustainable values into their operational processes through digital technology, thereby turning sustainable development thinking into concrete actions [93]. Through technologies such as artificial intelligence, big data analytics platforms, and digital governance systems, DT helps businesses track emissions reduction targets, manage product life cycles, and optimize resource usage in real time. This makes CSC not only a philosophical orientation but also a governance driving force capable of significantly improving CEP [94]. Furthermore, DT also plays a regulatory role by providing a digital platform to amplify the influence of CSC on CEP, thereby enhancing the ability to implement green strategies [93].

Hypothesis (H10b): DT as a moderating variable enhances the positive impact of CSC on CEP

Table 1 presents the key aspects of the digital transformation of accounting.

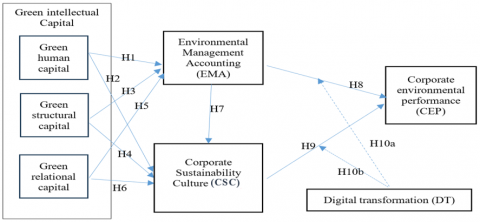

This study synthesizes GIC, EMA, CSC, and DT into a cohesive research framework, grounded in theoretical underpinnings and practical evidence. Figure 1 depicts the proposed model and the research hypotheses.

Table 1. Key tools in the accounting digital transformation process

|

Tool Group |

Typical Tools |

Main Function |

Author |

|

Digital accounting software |

MISA, FAST, SAP, Oracle NetSuite, Xero, QuickBooks, Zoho Books, Oracle Financials |

Automating bookkeeping, generating reports, managing documents, connecting with banks. |

Bhimani [95], Silva and Perera [96] |

|

Cloud accounting platform |

SAP Cloud, Microsoft Dynamics 365, Wave Accounting |

Remote access, real-time data synchronization, reduced storage costs. |

Peretz-Andersson et al. [97], Bhatia [98] |

|

AI & Machine Learning |

MindBridge AI, DataSnipper |

Anomalous analysis, detection of accounting fraud, audit optimization. |

Bahodirovich [99], Hasan [100] |

|

Business Intelligence (BI) |

Power BI, Tableau, QlikView |

Data visualization for financial information, supporting budget analysis and forecasting. |

Ao et al. [101] |

|

Blockchain in accounting |

Hyperledger, Ethereum-based smart contracts |

Record transactions that are transparent, immutable, and support quick and accurate audits. |

Viet and Dan [102], Guo et al. [103] |

|

Robotic Process Automation (RPA) |

UiPath, Blue Prism, Automation Anywhere |

Automate repetitive tasks such as data entry, reconciliation, and verification. |

Van der Aalst et al. [104] |

|

OCR & Digital Document Management |

ABBYY, Kofax, DocuWare |

Scan and process invoices and accounting documents, store and quickly search for documents. |

Van der Aalst et al. [104] |

Figure 1. Proposed research framework

3.1 Qualitative research

Primary and secondary data were also collected. Primary data were collected through a predesigned questionnaire sent to the survey participants. The survey subjects were the Board of Directors, accounting department heads, and accounting staff of 60 manufacturing enterprises in Vietnam. The 60 surveyed enterprises included 45 manufacturing enterprises listed on the Ho Chi Minh City Stock Exchange (HOSE) and 15 manufacturing enterprises not listed on the exchange. Secondary data were collected from the financial statements of the export enterprises. A total of 300 survey questionnaires were distributed, of which 260 (86.67%) were valid. The data have a nested structure, with multiple respondents belonging to the same company. If this characteristic is ignored and all 260 questionnaires are treated as independent, the standard errors may be biased. The authors estimated the design effect (DE) coefficients for all seven factors using the formula DE = 1 + (m – 1) × ICC [105-107] and obtained the results as in Table 2.

With an average of 4.33 respondents per firm and the intraclass correlation (ICC) values assumed to range between 0.05 and 0.10 [108, 109], the DE values of the seven factors (GHC, GSC, GRC, EMA, CSC, CEP, and DT) vary from 1.17 to 1.33. Since all are below the threshold of 2, the clustering effect is negligible. Therefore, the use of a single-level PLS-SEM model remains appropriate under the current research conditions.

Table 2. Design effect

|

Construct |

Avg. Respondents per Firm (m = 4.33) |

Assumed ICC |

DE = 1 + (m − 1) × ICC |

|

GHC |

4.33 |

0.05 |

1.17 |

|

GSC |

4.33 |

0.06 |

1.20 |

|

GRC |

4.33 |

0.07 |

1.23 |

|

EMA |

4.33 |

0.08 |

1.26 |

|

CSC |

4.33 |

0.10 |

1.33 |

|

CEP |

4.33 |

0.05 |

1.17 |

|

DT |

4.33 |

0.05 |

1.17 |

3.2 Quantitative research

Propose a practical model/framework. The author applies tools such as SPSS and SmartPLS to analyze the data. The collected data were processed using SMART PLS 4.1.0.0 and SPSS 22 software.

4.1 Descriptive statistics

Enterprises with a large capital scale have 25 companies, accounting for 41.67%, and the remaining 35 are small and medium-sized enterprises, accounting for 58.33%. Data collected from accounting staff accounts for 63.85%. The leadership team accounts for 36.15%, of which the Board of Directors is 15.38% and the Chief Accountant is 20.77%. The educational level shows that university graduates make up the highest percentage at 61.54%, while employees with a doctorate degree represent a low percentage of only 3.85%. Master’s degrees accounted for another high rate of 13.46%. The characteristics of the research sample are presented in Table 3.

Table 3. Sample characteristics

|

Charateristic |

Contents |

Sample |

Rate % |

|

Capital size |

< 20 billion VND |

7 |

11.67 |

|

20-50 billion VND |

23 |

38.33 |

|

|

50-100 billion VND |

5 |

8.33 |

|

|

> 100 billion VND |

25 |

41.67 |

|

|

Work experience |

Less than 10 years |

62 |

23.85 |

|

10 years-15 years |

85 |

32.69 |

|

|

15 years-20 years |

80 |

30.77 |

|

|

More than 20 years |

33 |

12.69 |

|

|

Survey subjects |

Director |

40 |

15.38 |

|

Chief accountant |

54 |

20.77 |

|

|

Accounting staff |

166 |

63.85 |

|

|

Education |

College Bachelor's |

55 |

21.15 |

|

Bachelor's |

160 |

61.54 |

|

|

Master's |

35 |

13.46 |

|

|

PhD |

10 |

3.85 |

4.2 Assessing the reliability of the scale

The evaluation results indicate that the Cronbach's Alpha of each factor ranges from 0.751 to 0.927, meeting the reliability requirements of the scale. The Cronbach's Alpha indexes of each observed variable are all greater than 0.7 [110], in which some observed variables—“The environmental strategy of the business EMA1 = 0.676”; “Sustainable Business Policies and Strategies CSC4 = 0.694”; “The digital competency of accountants DT3 = 0.684”; “Resource utilization efficiency CEP1 = 0.208”; and “Compliance with environmental regulations CEP5 = 0.694”—have loading factors less than 0.700, so they are eliminated from the model.

The results of the reliability analysis show that the scales in the model all meet the requirements. Specifically, the rho_a values of the factors are all greater than 0.7—the acceptable threshold according to the recommendation in PLS-SEM [110], demonstrating that the observed variables have internal consistency. For GHC, rho_a is 0.757; GSC is 0.826; and GRC is 0.933, indicating a very high level of reliability. The remaining factors also remained at a reliable level: DT = 0.871; EMA = 0.911; CSC = 0.894; and CEP = 0.829. Thus, all scales ensured composite reliability, strengthening the basis for use in the next analysis steps.

The average variance extracted (AVE) value ranges from 0.572 to 0.776, so the scales of each variable in the model all achieve a convergent value. The results of the reliability assessment of the scale are shown in Table 4.

Table 4. Reliability and convergence analysis of factors

|

Factors |

Observation Variable |

Factor Loading |

CA |

CR |

AVE |

|

Green human capital |

GHC1-Training and developing a green workforce |

0.753 |

0.751 |

0.757 |

0.572 |

|

GHC2-Green human resources policy |

0.714 |

||||

|

GHC3-The level of awareness and personal attitude towards the environment |

0.744 |

||||

|

GHC4-Knowledge, skills, and attitudes towards the environment |

0.811 |

||||

|

Green structural capital |

GSC1-The sustainable development strategy of the enterprise |

0.764 |

0.813 |

0.826 |

0.641 |

|

GSC2-Green technology and technical infrastructure |

0.875 |

||||

|

GSC3-Environmental policies and legal regulations |

0.744 |

||||

|

GSC4-Green leadership and commitment from management level |

0.815 |

||||

|

Green relational capital |

GRC1-Green communication and transparency in environmental information |

0.894 |

0.927 |

0.933 |

0.776 |

|

GRC2-Customer and supplier satisfaction with environmental policies |

0.892 |

||||

|

GRC3-Information technology and digital platforms support green connectivity |

0.894 |

||||

|

GRC4-Green leadership and an outward-oriented culture |

0.912 |

||||

|

GRC5-Pressure from customers, suppliers, investors, the community, and the government |

0.808 |

||||

|

Digital transformation |

DT1-Pressure from competitors |

0.886 |

0.843 |

0.853 |

0.759 |

|

DT2-Information technology infrastructure |

0.855 |

||||

|

DT4-Digital transformation strategy |

0.817 |

||||

|

DT5-State policies and legal regulations |

0.807 |

||||

|

Environmental management accounting |

EMA2-Financial and human resources |

0.884 |

0.904 |

0.911 |

0.680 |

|

EMA3-Leadership commitment |

0.756 |

||||

|

EMA4-Automation and digitization of environmental data |

0.804 |

||||

|

EMA5-The level of technology and accounting information systems |

0.905 |

||||

|

EMA6-Legal compliance requirements |

0.734 |

||||

|

EMA7-Pressure from stakeholders |

0.851 |

||||

|

Corporate sustainability culture |

CSC1-Sustainable leadership style |

0.895 |

0.893 |

0.894 |

0.758 |

|

CSC2-Training and raising internal awareness |

0.834 |

||||

|

CSC3-Employee participation |

0.864 |

||||

|

CSC5-Industry standards and international models |

0.888 |

||||

|

Corporate environmental performance |

CEP2-The effectiveness of green innovation. |

0.845 |

0.823 |

0.829 |

0.656 |

|

CEP3-The level of customer and investor satisfaction regarding environmental responsibility |

0.891 |

||||

|

CEP4-Minimize waste and emissions |

0.767 |

||||

|

CEP6-ESG rankings from independent organizations |

0.727 |

4.3 Collinearity of observed variables

After eliminating some inappropriate observed variables, the results showed that the remaining observed variables of the model did not have multicollinearity because all of VIF < 5. The results of the multicollinearity test of the observed variables are shown in Table 5.

When reporting the VIF index to check for multicollinearity, according to Hair [111], assume that all values below 5 meet the standard. The more stringent threshold should be 3.3, not 5, so the authors eliminated 2 observed variables (VIP_DT5 = 4.273; VIP_EMA5 = 4.008) out of the research model [112]. After removing the observed variables, each factor in the model still has 3 observed variables, ensuring reliability and validity in analysis using the SMART PLS tool.

Table 5. Summary of VID magnification factors

|

Observation Variable |

VIF |

|

CEP2 |

2.477 |

|

CEP3 |

2.923 |

|

CEP4 |

1.594 |

|

CEP6 |

1.395 |

|

CSC1 |

2.904 |

|

CSC2 |

2.166 |

|

CSC3 |

2.518 |

|

CSC5 |

2.949 |

|

DT1 |

2.799 |

|

DT2 |

2.528 |

|

DT4 |

1.712 |

|

EMA2 |

3.506 |

|

EMA3 |

2.319 |

|

EMA4 |

2.637 |

|

EMA6 |

1.993 |

|

EMA7 |

2.969 |

|

GHC1 |

1.918 |

|

GHC2 |

1.863 |

|

GHC3 |

1.876 |

|

GHC4 |

1.959 |

|

GRC1 |

3.169 |

|

GRC2 |

3.282 |

|

GRC3 |

3.246 |

|

GRC4 |

3.279 |

|

GRC5 |

2.416 |

|

GSC1 |

1.680 |

|

GSC2 |

2.394 |

|

GSC3 |

1.810 |

|

GSC4 |

1.665 |

|

DT × CSC |

1.000 |

|

DT × EMA |

1.000 |

4.4 Difference value test

The results in Table 6 show that all HTMT values are below the threshold of 0.90, with many pairs of variables having coefficients lower than 0.80. This confirms that the research constructs achieve discriminant validity according to the standards of Henseler et al. [113]. In particular, the interaction variables (DT × CSC and DT × EMA) have significantly lower HTMT coefficients compared to the main variables, reflecting that they truly measure the moderating concept rather than overlapping with the original variables.

Based on Table 7, the Fornell-Larcker criterion, it can be seen that the square root values of AVE (diagonal) range from 0.768 to 0.854, which are larger than the off-diagonal correlation coefficients, thereby confirming the discriminant validity between factors [114]. Specifically, CEP has a square root of AVE of 0.824, which is larger than the correlation coefficients with CSC (0.781), DT (0.310), EMA (0.742), GHC (0.701), GRC (0.692), and GSC (0.774). Similarly, CSC reaches 0.849, surpassing all the correlation coefficients with the remaining factors, of which the highest is EMA (0.795). For DT, the value of 0.768 is also higher than that of EMA (0.287), GHC (0.402), and other variables. For EMA, the square root of AVE is 0.837, surpassing the highest correlation with CSC (0.795). For GHC, the value stands at 0.831, which is larger than the highest correlation coefficient with EMA (0.725). Meanwhile, GRC scored 0.843, surpassing the largest correlation with EMA (0.765). Finally, GSC had a square root AVE of 0.854, which was greater than all correlation coefficients, including the highest with EMA (0.823). Thus, all research constructs ensured discriminant validity, indicating that the scales reflected distinct and non-overlapping concepts.

Table 6. Heterotrait-monotrait ratio (HTMT)-matrix

|

|

CEP |

CSC |

DT |

EMA |

GHC |

GRC |

GSC |

DT × CSC |

DT × EMA |

|

CEP |

|

|

|

|

|

|

|

|

|

|

CSC |

0.878 |

|

|

|

|

|

|

|

|

|

DT |

0.350 |

0.392 |

|

|

|

|

|

|

|

|

EMA |

0.819 |

0.869 |

0.320 |

|

|

|

|

|

|

|

GHC |

0.803 |

0.771 |

0.48 |

0.817 |

|

|

|

|

|

|

GRC |

0.802 |

0.795 |

0.329 |

0.847 |

0.833 |

|

|

|

|

|

GSC |

0.863 |

0.854 |

0.332 |

0.887 |

0.818 |

0.866 |

|

|

|

|

DT × CSC |

0.177 |

0.196 |

0.072 |

0.182 |

0.116 |

0.191 |

0.097 |

|

|

|

DT × EMA |

0.091 |

0.180 |

0.067 |

0.162 |

0.099 |

0.133 |

0.021 |

0.806 |

|

Table 7. Fornell-Larcker criterion

|

|

CEP |

CSC |

DT |

EMA |

GHC |

GRC |

GSC |

|

CEP |

0.824 |

|

|

|

|

|

|

|

CSC |

0.781 |

0.849 |

|

|

|

|

|

|

DT |

0.310 |

0.335 |

0.768 |

|

|

|

|

|

EMA |

0.742 |

0.795 |

0.287 |

0.837 |

|

|

|

|

GHC |

0.701 |

0.689 |

0.402 |

0.725 |

0.831 |

|

|

|

GRC |

0.692 |

0.711 |

0.318 |

0.765 |

0.755 |

0.843 |

|

|

GSC |

0.774 |

0.761 |

0.329 |

0.823 |

0.781 |

0.812 |

0.854 |

4.5 R2 and adjusted R2

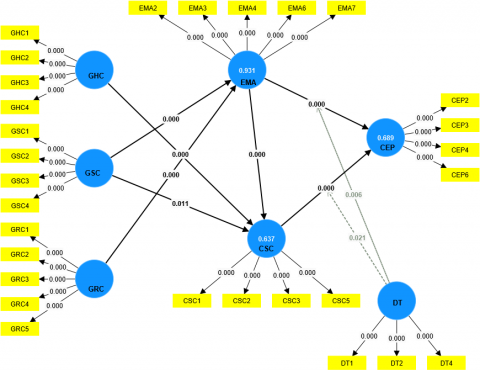

The analysis results in Table 8 show that the R² values of the dependent variables are all greater than 0.5, indicating that the research model is statistically significant and has excellent explanatory power. Specifically, the R² for CEP is 0.689 (Adjusted R² = 0.682), suggesting that the model can explain 68.9% of the variation in CEP; the small difference between R² and Adjusted R² confirms that the model is stable and not overfitted. For CSC, R² = 0.637 (Adjusted R² = 0.633), meaning that 63.7% of the variation in CSC is explained by the variables in the model, further reinforcing the model's adequacy. Notably, EMA has an R² of 0.931 (Adjusted R² = 0.930), indicating that the model explains 93.1% of the variation in EMA. This result reflects that EMA is strongly influenced by the explanatory factors while also reminding us to consider the risk of overfitting during the analysis process. Overall, the results confirm that the research model has high reliability, and the independent variables in the model have significant explanatory power regarding the dependent variables. This provides a solid empirical basis for testing the research hypotheses and discussing both theoretical and practical implications.

Table 8. R2 and adjusted R2

|

|

R-Square |

R-Square Adjusted |

|

CEP |

0.689 |

0.682 |

|

CSC |

0.637 |

0.633 |

|

EMA |

0.931 |

0.930 |

4.6 Official model

The impact of mediating variables is assessed according to the analysis in Table 9. EMA→CSC→CEP (0.158, p = 0.000): EMA indirectly affects CEP through CSC. This impact is positive and statistically significant (t = 3.879). GRC→EMA→CEP (0.307, p = 0.000): GRC indirectly affects CEP through EMA, with a strong and significant impact (t = 6.956). GHC→CSC→CEP (0.089, p = 0.001): GHC indirectly affects CEP through CSC, with a small but significant coefficient (t = 3.231). GRC→EMA→CSC (0.198, p = 0.000): GRC has a strong influence on CSC through EMA (t = 6.080). This is an important indirect path. GSC→EMA→CEP (0.079, p = 0.033): GSC indirectly affects CEP through EMA, which is significant (t = 2.138). GSC→EMA→CSC (0.167, p = 0.000): GSC affects CSC through EMA, with a fairly large and significant coefficient (t = 4.482). GSC→EMA→CSC→CEP (0.062, p = 0.000): GSC indirectly affects CEP through the mediating chain EMA→CSC, which is significant (t = 3.839). GRC→EMA→CSC→CEP (0.096, p = 0.000): GRC indirectly affects CEP through the chain EMA→CSC, which is significant (t = 3.666).

All indirect effects are statistically significant (p < 0.05). GRC and GSC have a strong indirect influence on CEP, particularly through EMA and CSC. EMA and CSC play an important mediating role in the model. The strongest path in the table is GRC→EMA→CSC (4.484).

The author uses PLS-SEM bootstrapping analysis. After the first test, the p-values of the hypotheses GHC→EMA = 0.460 and GRC→CSC = 0.585 have a significance level (p-value) > 0.05, proving that hypotheses H1 and H6 are not statistically significant and should be eliminated from the model. After eliminating hypotheses H1 and H6, the official research model was as shown in Figure 2. All relationships have a p-value < 0.05, meaning they are statistically significant at the 5% level. All research hypotheses are accepted.

The removal of H1 means that GHC no longer has a direct effect on EMA, suggesting that the effect of GHC may be mediated through CSC or that EMA is mainly influenced by other factors, such as GRC and GSC. Meanwhile, removing H6 shows that GRC does not directly affect CSC but still has a strong impact on EMA (coefficient 0.612). This confirms that in the Vietnamese context, GRC plays a central role in promoting EMA, rather than directly nurturing CSC. As a result, the model focuses more on the important relationships: GRC→EMA is the strongest, GHC and GSC have indirect effects through CSC, and CSC plays an important mediating role for CEP. Removing H1 and H6 does not weaken the model but rather cleans it up, keeping only statistically significant relationships, helping to explain more clearly how the components of green intellectual capital and EMA impact environmental performance. At the same time, it also highlights that GRC is the most important factor driving EMA, while GHC and GSC mainly influence CEP through CSC.

The results of testing the suitability of the official model are shown in Table 10. The research results indicate that all hypothesized relationships in the model are statistically significant with a p-value less than 0.05. The study confirms that green intellectual capital has a significant indirect impact on the environmental performance of enterprises through two mediating factors: EMA and CSC. The three components of green intellectual capital—GHC, GRC, and GSC—positively and statistically significantly influence sustainable culture and environmental management accounting. Among these, GRC has the strongest impact on EMA, with a coefficient of 0.612. This result reinforces the theory that external relationships can be a source of knowledge, pressure, and support to promote internal environmental management. Enterprises that want to improve their EMA system should not only rely on internal resources (human resources or processes) but also pay special attention to building and maintaining a green relationship network.

Explain the role of GRC for EMA in Vietnam: GRC, or green relational capital, reflects the quality and network of relationships a business has with stakeholders such as suppliers, customers, regulators, strategic partners, and the community. When businesses maintain effective green relationship networks, they not only receive information and resource support but also face pressure from stakeholders to comply with environmental standards.

In Vietnam, the context of “institutional gaps” and pressure from the supply chain makes GRC an important deciding factor in the implementation of EMA:

Institutional gaps: The environmental law system in Vietnam is not really complete, and enforcement is not synchronous. Therefore, businesses often rely on relationships with management agencies, reputable partners, and certification organizations to ensure effective implementation of EMA.

Pressure from the supply chain: Vietnamese enterprises participating in the global supply chain often have to meet the environmental standards of foreign customers and partners. Green relationship networks help enterprises receive the information, guidance, and resources necessary for EMA to operate properly, thereby improving the effectiveness of environmental management.

Table 9. Specific indirect effects

|

|

Original Sample (O) |

Sample Mean (M) |

Standard Deviation (STDEV) |

T Statistics (|O/STDEV|) |

P Values |

|

EMA→CSC→CEP |

0.158 |

0.156 |

0.041 |

3.879 |

0.000 |

|

GRC→EMA→CEP |

0.307 |

0.308 |

0.044 |

6.956 |

0.000 |

|

GHC→CSC→CEP |

0.089 |

0.091 |

0.028 |

3.231 |

0.001 |

|

GRC→EMA→CSC |

0.259 |

0.258 |

0.058 |

4.484 |

0.000 |

|

GSC→EMA→CEP |

0.198 |

0.199 |

0.033 |

6.080 |

0.000 |

|

GSC→EMA→CSC |

0.167 |

0.166 |

0.037 |

4.482 |

0.000 |

|

GSC→CSC→CEP |

0.079 |

0.080 |

0.037 |

2.138 |

0.033 |

|

GSC→EMA→CSC→CEP |

0.062 |

0.061 |

0.016 |

3.839 |

0.000 |

|

GRC→EMA→CSC→CEP |

0.096 |

0.096 |

0.026 |

3.666 |

0.000 |

Table 10. Results of coefficient testing

|

|

Original Sample (O) |

Sample Mean (M) |

Standard Deviation (STDEV) |

T statistics (|O/STDEV|) |

P Values |

|

CSC→CEP |

0.373 |

0.373 |

0.070 |

5.325 |

0.000 |

|

EMA→CEP |

0.502 |

0.503 |

0.066 |

7.641 |

0.000 |

|

EMA→CSC |

0.423 |

0.421 |

0.089 |

4.772 |

0.000 |

|

GHC→CSC |

0.238 |

0.243 |

0.049 |

4.897 |

0.000 |

|

GRC→EMA |

0.612 |

0.612 |

0.037 |

16.708 |

0.000 |

|

GSC→CSC |

0.212 |

0.212 |

0.083 |

2.542 |

0.011 |

|

GSC→EMA |

0.395 |

0.395 |

0.036 |

10.931 |

0.000 |

|

DT→CEP |

0.260 |

0.261 |

0.031 |

8.396 |

0.000 |

|

DT × CSC→CEP |

0.153 |

0.153 |

0.066 |

2.317 |

0.021 |

|

DT × EMA→CEP |

-0.176 |

-0.178 |

0.064 |

2.769 |

0.006 |

Figure 2. Final research model

Support knowledge and technology sharing: Relationships with green partners help businesses access better technology, environmental data, and processes, reducing risks in digitalization and EMA integration. Notably, GSC also affects EMA with a coefficient of 0.395. This indicates that the factors related to green intellectual capital not only contribute to shaping a culture of sustainable development but also promote the adoption of EMA in enterprises. GSC→CSC (β = 0.212, p = 0.011) indicates that GSC also has a positive effect on CSC, but the magnitude is smaller. It is still statistically significant (p < 0.05). Green organizational knowledge helps to encourage CSC, but the effect is weaker than GHC→CSC. GHC positively correlates with CSC, with a coefficient of 0.238; GHC promotes CSC at the small-medium level. Human resource training and green professional capacity enhancement play a key role in the formation and development of CSC.

Additionally, CSC also significantly affects CEP, with a coefficient of 0.373 and a T value of 5.325. The research results show that CSC, as an important mediating variable in the model, has a direct and positive impact on corporate environmental performance (CEP).

EMA has a positive and statistically significant impact on CSC (β = 0.423, p = 0.000), suggesting that EMA not only acts as an accounting tool but also acts as a cultural driver, helping to embed sustainability into the organization's daily values and practices. This study result is consistent with the previous findings of Burritt et al. [53], Pratiwi [59], Elizabeth [61], and Huy and Phuc [54]. Therefore, Hypothesis H7, which states that EMA has a positive impact on CSC, is supported. This study further supports the findings that EMA has a strong impact on CEP (β = 0.502, p = 0.000), emphasizing the central role of EMA in integrating environmental factors into business strategy and delivering measurable sustainability outcomes. Therefore, Hypothesis H8, which states that EMA has a positive impact on CEP, is strongly supported.

The regulatory role of DT in the model: The research results indicate that DT plays a role as a strategic contextual factor, determining the strength or weakness of the relationship between corporate sustainability culture and environmental performance. Specifically, the interaction coefficient DT × CSC→CEP reached 0.153 with p = 0.021, showing that when the level of digital transformation is high, businesses can exploit core values from CSC more effectively thanks to the technology system that supports the spread and maintenance of sustainable culture. This demonstrates that DT acts as an amplification mechanism, allowing the potential effects of CSC to be more strongly exerted on CEP. This regulatory role affirms that digital technology is not simply an operational tool but also a factor that strengthens the link between cultural factors and environmental outcomes. Thus, DT becomes the key connecting sustainable management and environmental achievements, helping businesses achieve more comprehensive efficiency.

In contrast, the coefficient DT × EMA→CEP is -0.176 with p = 0.006. This result reflects the reality in many Vietnamese manufacturing enterprises, where digital transformation and EMA implementation often take place asynchronously or in parallel without system integration. In many cases, environmental data is digitized but not directly connected to the environmental accounting process, and EMA still operates manually or semi-automatically, leading to data conflicts and delays in analysis. When DT stops at the level of data digitization without accompanying process standardization, improving analysis and decision-making capabilities, environmental data is prone to fragmentation, latency, or inconsistency, thereby reducing the expected positive impact of EMA on CEP. This view is reinforced by the study of Abdelhalim et al. [78], which shows that the effectiveness of digitally supported EMA depends largely on the level of system integration and organizational commitment.

Other factors also contribute to explaining this negative coefficient: Many businesses still face a gap in digital capabilities; although environmental data has been digitized, EMA teams lack the ability to exploit big data, AI, or IoT, making digital technology sometimes become an information “bottleneck,” slowing down the analysis process and reducing CEP efficiency. According to dynamic capability theory, technology only develops value when it is absorbed and operated based on organizational capabilities. At the same time, compliance costs and institutional pressures also weaken the impact of DT on EMA. In Vietnam, many enterprises implement EMA mainly to meet environmental reporting or ISO certification, while DT aims to increase productivity and profit, leading to formal EMA, which is less supportive of CEP and consistent with the institutional theory that governance tools will be less effective if only aimed at compliance.

In addition, the digital transformation process generates large volumes of data, but it is often stored scattered across many different systems (ERP, IoT, environmental sensors, operational reports, etc.), leading to data dispersion. It is difficult to synthesize into a synchronous information source for EMA. The lack of data standardization is also manifested in the lack of a unified format and unclear criteria for measuring and recording environmental costs. As a result, EMA cannot directly use these data to prepare accurate reports, reducing the reliability of the information, delaying analysis, and ultimately weakening EMA's impact on CEP.

Thus, in the context of digital transformation, the impact of organizational and governance factors such as CSC becomes more pronounced, while the role of EMA may be dispersed or altered. Overall, the model has confirmed the strong relationship between green intellectual capital, sustainable development culture, environmental accounting, and the environmental performance of enterprises, while also highlighting the complex influence of digital transformation on these relationships.

5.1 Conclusion

The research indicates that green intellectual capital has a positive and indirect influence on CEP via two mediating variables: EMA and CSC. Within the framework of DT, the functions of EMA and CSC are increasingly vital in translating environmental knowledge into targeted behaviors and initiatives that enhance environmental efficiency. Manufacturing enterprises in Vietnam are progressively embracing sustainable development; yet, the implementation of EMA and the cultivation of a sustainable culture remain inconsistent. Consequently, augmenting the capability of green intellectual capital alongside the digitization of environmental management systems will generate a substantial incentive to improve environmental performance.

5.2 Policy implications

For managers: It is important to perceive GIC not just as a soft resource but as a strategic asset that can be converted into actual environmental performance through astute governance and innovative strategies.

For internal policies: It is advisable to design integrated policies that align DT with sustainable development, particularly emphasizing the role of EMA in facilitating decision-making.

For the government and industry associations, they should support manufacturing companies in standardizing and promoting EMA while also providing best practice guidelines for fostering a sustainable culture in the digital era.

5.3 Limitations of the study

Although the research has confirmed a positive and statistically significant relationship between GIC, EMA, CSC, and CEP, some limitations need to be addressed in subsequent studies:

The research sample's limitations: the research predominantly examines manufacturing enterprises in Vietnam; therefore, the results might not accurately reflect other sectors or nations with differing levels of development and DT.

The absence of synchronization between EMA and DT: Analysis reveals that in many enterprises, the execution of environmental management accounting and digital transformation is not aligned, frequently functioning concurrently without systemic integration. This reduces the effectiveness of EMA and may incorporate extraneous variables into the research model.

Excluding additional mediating or moderating variables: The existing model concentrates solely on two mediating factors (EMA and CSC) and one moderating variable (DT). Additionally, factors such as environmental strategy, technical proficiency, leadership support, and legislative regulations may significantly influence the moderation or mediation of these relationships.

The survey data consists of 260 responses from 60 companies (an average of ~4.3 responses/company). This means that the data is hierarchically structured, i.e., individuals are nested within companies. However, conventional PLS analysis assumes observations are independent, while nested data can distort standard errors. Due to the limited company-level sample size (n = 60), the study could not be applied for analysis on SMART PLS. The study selected analysis at the individual level, and in the future, it can be extended by applying multilevel modeling (multilevel SEM/PLS) when larger data are available.

5.4 Future research

Broaden the research scope to include service industries or small and medium-sized enterprises (SMEs) to evaluate the model's generalizability. Conduct a comparative investigation among various countries to examine the disparities in the influence of green intellectual capital on environmental performance under various digital transformation conditions. Utilize qualitative research approaches, including in-depth interviews, to enhance comprehension of the obstacles to merging DT and EMA. Propose a comprehensive model that evaluates the influence of factors such as green leadership capability, green technological innovation, and environmental reward and punishment mechanisms on the relationship between GIC and CEP.

[1] Nishitani, K., Nguyen, T.B.H., Kokubu, K. (2025). Does the economic motivation of firms to address the United Nations’ sustainable development goals (SDGs) promote the SDGs or merely SDG-washing? Critical empirical evidence from Japan and Vietnam. Review of Managerial Science, 19(2): 415-465. https://doi.org/10.1007/s11846-024-00755-z

[2] Liu, L. (2024). Environmental performance factors: Insights from CSR-linked compensation, committees, disclosure, targets, and board composition. Journal of Sustainable Finance & Investment, 1-36. https://doi.org/10.1080/20430795.2024.2313497

[3] Nguyen, T., Le-Anh, T., Nguyen Thi Hong, N., Huong Nguyen, L.T., Nguyen Xuan, T. (2024). Digital transformation in accounting of Vietnamese small and medium enterprises. Journal of Financial Reporting and Accounting, 23(2): 769-787. https://doi.org/10.1108/JFRA-12-2023-0761

[4] Pargmann, J., Berding, F. (2024). Integrating sustainability in controlling and accounting practices: A critical review and implications for competences in German vocational business education. arXiv Preprint arXiv: 2406.02314. https://doi.org/10.48550/arXiv.2406.02314

[5] Bin-Nashwan, S.A., Li, J.Z. (2025). AI-infused knowledge and green intellectual capital: Pathways to spur accounting performance drawn from RBV-KBV model and sustainability culture. Technology in Society, 102913. https://doi.org/10.1016/j.techsoc.2025.102913

[6] Alnaim, M., Metwally, A.B.M. (2024). Green intellectual capital and corporate environmental performance: Does environmental management accounting matter? Administrative Sciences, 14(12): 311. https://doi.org/10.3390/admsci14120311

[7] Martínez-Falcó, J., Sánchez-García, E., Marco-Lajara, B., Zaragoza-Sáez, P. (2025). Green intellectual capital and sustainable competitive advantage: Unraveling role of environmental management accounting and green entrepreneurship orientation. Journal of Intellectual Capital, 26(1): 104-129. https://doi.org/10.1108/JIC-07-2024-0204

[8] Jiao, X., Zhang, P., He, L., Li, Z. (2023). Business sustainability for competitive advantage: Identifying the role of green intellectual capital, environmental management accounting and energy efficiency. Economic Research-Ekonomska Istraživanja, 36(2): 2125035. https://doi.org/10.1080/1331677X.2022.2125035

[9] Shehzad, M.U., Zhang, J., Dost, M., Ahmad, M.S., Alam, S. (2023). Linking green intellectual capital, ambidextrous green innovation and firms green performance: Evidence from Pakistani manufacturing firms. Journal of Intellectual Capital, 24(4): 974-1001. https://doi.org/10.1108/JIC-02-2022-0032

[10] Shahbaz, M.H., Ahmad, S., Malik, S.A. (2025). Green intellectual capital heading towards green innovation and environmental performance: Assessing the moderating effect of green creativity in SMEs of Pakistan. International Journal of Innovation Science, 17(3): 683-704. https://doi.org/10.1108/IJIS-08-2023-0169

[11] Kokubu, K., Nashioka, E. (2005). Environmental management accounting practices in Japan. In Implementing Environmental Management Accounting: Status and Challenges. Dordrecht: Springer Netherlands, 321-342. https://doi.org/10.1007/1-4020-3373-7

[12] Schaltegger, S., Burritt, R. (2017). Contemporary Environmental Accounting: Issues, Concepts and Practice. Routledge. https://doi.org/10.4324/9781351282529

[13] Martínez-Falcó, J., Sánchez-García, E., Marco-Lajara, B., Lee, K. (2024). Green intellectual capital and environmental performance: Identifying the pivotal role of green ambidexterity innovation and top management environmental awareness. Journal of Intellectual Capital, 25(2/3): 380-401. https://doi.org/10.1108/JIC-08-2023-0193

[14] Asiaei, K., Bontis, N., Alizadeh, R., Yaghoubi, M. (2022). Green intellectual capital and environmental management accounting: Natural resource orchestration in favor of environmental performance. Business Strategy and the Environment, 31(1): 76-93. https://doi.org/10.1002/bse.2875

[15] Rizavi, S.S., Amir, M., Siddique, M., Ali, K., Banin, S.U. (2025). Greening the path to firms’ success: Unveiling “Going Green” strategies through natural resource orchestration for sustainable development. Asia-Pacific Journal of Business Administration. https://doi.org/10.1108/APJBA-02-2024-0073

[16] Solovida, G.T., Latan, H. (2017). Linking environmental strategy to environmental performance: Mediation role of environmental management accounting. Sustainability Accounting, Management and Policy Journal, 8(5): 595-619. https://doi.org/10.1108/SAMPJ-08-2016-0046

[17] Amir, M., Uddin, M., Shaukat, H.S., Khan, S., Arshad, S., Ansari, M., Arshad, A. (2025). Green pathways: From environmental strategies and green intellectual capital to environmental performance, with the mediating role of environmental management accounting. Journal of Environmental Accounting and Management, 13(2): 107-124. https://www.lhscientificpublishing.com/Journals/articles/DOI-10.5890-JEAM.2025.06.001.aspx.

[18] Tonial, G., Cassol, A., Selig, P.M., Giugliani, E. (2018). Intellectual capital management and sustainability activities in Brazilian organizations: A case study. In Intellectual Capital Management as a Driver of Sustainability: Perspectives for Organizations and Society. Cham: Springer International Publishing, pp. 119-138. https://doi.org/10.1007/978-3-319-79051-0_7

[19] Vale, J., Miranda, R., Azevedo, G., Tavares, M.C. (2022). The impact of sustainable intellectual capital on sustainable performance: A case study. Sustainability, 14(8): 4382. https://doi.org/10.3390/su14084382

[20] Thanh Thuy Ngoc, T. (2025). Unlocking environmental management accounting and environmental performance: A mediated moderation model through green technology innovation and environmental strategy. Meditari Accountancy Research, 33(2): 733-758. https://doi.org/10.1108/MEDAR-07-2024-2558

[21] Oanh, L.T.T., Ngoc, B.T., Dung, N.T., Trang, N.T., Anh, V.T.K. (2025). The impact of digital transformation in management accounting on governance efficiency: The intermediary role of accounting information quality. Journal of Governance and Regulation, 14(1): 295-306. https://doi.org/10.22495/jgrv14i1siart6

[22] Son, Đ.B., Tri, H.M., Trinh, H.N.C. (2023). Corporate social responsibility, intellectual capital, and innovation performance: Evidence from the information and communication technology (ICT) industry in Ho Chi Minh City. Journal of Finance and Marketing Research, 73-85. https://doi.org/10.52932/jfm.vi2.335

[23] Bui, T.K.H. (2022). Current status of environmental cost management accounting at animal domestic feed production enterprises in Vietnam. Vietnam Journal of Agricultural Science, 20(4): 528-538. https://vie.vjas.vn/index.php/vjasvn/article/view/981.

[24] Hung, P.H. (2025). The applicability of lean accounting in enterprises: The case of pulp and paper manufacturing enterprises in Vietnam. Multidisciplinary Reviews, 8(4): 2025121-2025121. https://10.31893/multirev.2025121

[25] Wernerfelt, B. (1984). A resource-based view of the firm. Strategic Management Journal, 5(2): 171-180. https://doi.org/10.1002/smj.4250050207

[26] Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1): 99-120. https://doi.org/10.1177/014920639101700108

[27] Grant, R.M. (1996). Toward a knowledge-based theory of the firm. Strategic Management Journal, 17(S2): 109-122. https://doi.org/10.1002/smj.4250171110

[28] Spender, J.C., Grant, R.M. (1996). Knowledge and the firm: Overview. Strategic Management Journal, 17(S2): 5-9. https://doi.org/10.1002/smj.4250171103

[29] Chen, Y.S. (2008). The positive effect of green intellectual capital on competitive advantages of firms. Journal of Business Ethics, 77(3): 271-286. https://doi.org/10.1007/s10551-006-9349-1

[30] Benevene, P., Buonomo, I., Kong, E., Pansini, M., Farnese, M.L. (2021). Management of green intellectual capital: Evidence-based literature review and future directions. Sustainability, 13(15): 8349. https://doi.org/10.3390/su13158349

[31] Buhaya, M.I., Metwally, A.B.M. (2024). Green intellectual capital and green supply chain performance: Do external pressures matter? Cogent Business & Management, 11(1): 2349276. https://doi.org/10.1080/23311975.2024.2349276

[32] Safitri, N., Ahmar, N., Zaky, M., Rahmani, M.A. (2022). Green intellectual capital and environmental management accounting: A literature review. Jurnal Proaksi, 9(3): 281-291. https://doi.org/10.32534/jpk.v9i3.3096

[33] Mansoor, A., Jahan, S., Riaz, M. (2021). Does green intellectual capital spur corporate environmental performance through green workforce? Journal of Intellectual Capital, 22(5): 823-839. https://doi.org/10.1108/JIC-06-2020-0181

[34] Noor, A., Bano, A. (2024). Impact of green intellectual capital and environmental management accounting on sustainable performance: The moderating role of stakeholder pressure. Sustainable Trends and Business Research, 2(1): 1-14. https://doi.org/10.70291/stbr.2.1.2024.15

[35] Hooi, L.W., Liu, M.S., Lin, J.J. (2022). Green human resource management and green organizational citizenship behavior: Do green culture and green values matter? International Journal of Manpower, 43(3): 763-785. https://doi.org/10.1108/IJM-05-2020-0247

[36] Tran, N.K.H. (2023). An empirical investigation on the impact of green human resources management and green leadership on green work engagement. Heliyon, 9(11): e21018. https://doi.org/10.1016/j.heliyon.2023.e21018

[37] Muisyo, P.K., Qin, S. (2021). Enhancing the FIRM’S green performance through green HRM: The moderating role of green innovation culture. Journal of Cleaner Production, 289: 125720. https://doi.org/10.1016/j.jclepro.2020.125720

[38] Khader, A.R., Nissar, P. (2025). Impact of green structural capital on green supply chain agility. In Green Supply Chain Management. Apple Academic Press, pp. 187-195.

[39] Bhatti, S.M., ul Haq, M.Z., Kanwal, S., Makhbul, Z.K.M. (2024). Impact of green intellectual capital, green organizational culture, and frugal innovation on sustainable business model innovation: Dataset of manufacturing firms in Pakistan. Data in Brief, 54: 110419. https://doi.org/10.1016/j.dib.2024.110419

[40] Al Doghan, M.A., Abdelwahed, N.A.A., Soomro, B.A., Ali Alayis, M.M.H. (2022). Organizational environmental culture, environmental sustainability and performance: The mediating role of green HRM and green innovation. Sustainability, 14(12): 7510. https://doi.org/10.3390/su14127510

[41] Aloqaily, A.N., Al-Zaqeba, M.A.A. (2024). The impact of green human resource management practices on engagement of employee and organizational creativity towards the green environment. In International Conference on Business and Technology. Cham: Springer Nature Switzerland, pp. 265-276. https://doi.org/10.1007/978-3-031-67444-0_26

[42] Yusliza, M.Y., Yong, J.Y., Tanveer, M.I., Ramayah, T., Faezah, J.N., Muhammad, Z. (2020). A structural model of the impact of green intellectual capital on sustainable performance. Journal of Cleaner Production, 249: 119334. https://doi.org/10.1016/j.jclepro.2019.119334

[43] Long, S., Liao, Z. (2023). Green relational capital, integration capabilities and environmental innovation adoption: The moderating role of normative pressures. Sustainable Development, 31(3): 1570-1580. https://doi.org/10.1002/sd.2467

[44] Azizan, O., Tajmir Riahi, M., Shahriari, M., Rasti-Barzoki, M. (2025). The effect of green culture and identity on organizational commitment. Journal of Environmental Planning and Management, 68(4): 843-865. https://doi.org/10.1080/09640568.2023.2273778

[45] Li, W., Bhutto, M.Y., Waris, I., Hu, T. (2023). The nexus between environmental corporate social responsibility, green intellectual capital and green innovation towards business sustainability: An empirical analysis of Chinese automobile manufacturing firms. International Journal of Environmental Research and Public Health, 20(3): 1851. https://doi.org/10.3390/ijerph20031851

[46] Az'mi, Y.U., Kristina, G.R. (2024). Green intellectual capital and environmental management accounting: How does it influence environmental performance? Indonesian Journal of Economics, Social, and Humanities, 6(3): 287-298. https://doi.org/10.31258/ijesh.6.3.287-298

[47] Awuah-Gyawu, M., Abdul Muntaka, S., Owusu-Bio, M.K., Otchere Fianko, A. (2024). Assessing the effects of sustainable supply chain management practices on operational performance: The role of business regulatory compliance and corporate sustainability culture. Benchmarking: An International Journal. https://doi.org/10.1108/BIJ-10-2023-0721

[48] Hameed, S., Khan, M.S., Siddiqui, D., Ali, S.M. (2024). Effect of employee religious and cultural values on sustainable behaviour of employee: Mediating effect of pro-environmental attitude. International Journal of Trends and Innovations in Business & Social Sciences, 2(2): 154-167. https://doi.org/10.48112/tibss.v2i2.795

[49] Aggarwal, P., Agarwala, T. (2023). Relationship of green human resource management with environmental performance: Mediating effect of green organizational culture. Benchmarking: An International Journal, 30(7): 2351-2376. https://doi.org/10.1108/BIJ-08-2021-0474

[50] Zahoor, N., Gerged, A.M. (2021). Relational capital, environmental knowledge integration, and environmental performance of small and medium enterprises in emerging markets. Business Strategy and the Environment, 30(8): 3789-3803. https://doi.org/10.1002/bse.2840

[51] Bennett, M., Rikhardsson, P., Schaltegger, S. (2003). Adopting environmental management accounting: EMA as a value-adding activity. In Environmental Management Accounting-Purpose and Progress. Dordrecht: Springer Netherlands. Springer, Dordrecht, pp. 1-14. https://doi.org/10.1007/978-94-010-0197-7_1

[52] Huynh, Q.L., Nguyen, V.K. (2024). The role of environmental management accounting in sustainability. Sustainability, 16(17): 7440. https://doi.org/10.3390/su16177440

[53] Burritt, R.L., Hahn, T., Schaltegger, S. (2002). Towards a comprehensive framework for environmental management accounting-Links between business actors and environmental management accounting tools. Australian Accounting Review, 12(27): 39-50. https://doi.org/10.1111/j.1835-2561.2002.tb00202.x

[54] Huy, P.Q., Phuc, V.K. (2024). Insight into how environmental management accounting practices and complexity of green innovation management pave the way toward strategic resilience. Journal of the Knowledge Economy, 16: 14146–14179. https://doi.org/10.1007/s13132-024-02461-3

[55] Jasch, C. (2003). The use of environmental management accounting (EMA) for identifying environmental costs. Journal of Cleaner Production, 11(6): 667-676. https://doi.org/10.1016/S0959-6526(02)00107-5

[56] Le, T.T., Nguyen, T.M.A., Phan, T.T.H. (2019). Environmental management accounting and performance efficiency in the Vietnamese construction material industry-A managerial implication for sustainable development. Sustainability, 11(19): 5152. https://doi.org/10.3390/su11195152

[57] Swalih, M.M., Ram, R., Tew, E. (2024). Environmental management accounting for strategic decision-making: A systematic literature review. Business Strategy and the Environment, 33(7): 6335-6367. https://doi.org/10.1002/bse.3828

[58] Appannan, J.S., Mohd Said, R., Ong, T.S., Senik, R. (2023). Promoting sustainable development through strategies, environmental management accounting and environmental performance. Business Strategy and the Environment, 32(4): 1914-1930. https://doi.org/10.1002/bse.3227

[59] Pratiwi, Y.N., Meutia, I., Syamsurijal, S. (2020). The effect of environmental management accounting on corporate sustainability. Binus Business Review, 11(1): 43-49. https://doi.org/10.21512/bbr.v11i1.6028

[60] Fatmasari, R.R., Hanuun, N.N.P., Yolistina, A. (2024). Exploring the role of environmental accounting in promoting corporate sustainability practices. Kriez Academy: Journal of Development and Community Service, 1(10): 57-76. https://kriezacademy.com/index.php/kriezacademy/article/view/45.

[61] Elizabeth, E. (2022). Exploring the influence of corporate culture on building environmental management value systems. Studies in Economics and Business Administration, 2(1): 12-17, https://mfacademia.org/index.php/seba/article/view/74.

[62] Huy, H.P. (2024). The role of sustainability accounting in improving environmental performance in Vietnam's manufacturing industry. Journal of Economics, Bussiness and Management Issues, 2(1): 1-12. https://doi.org/10.47134/jebmi.v2i1.490

[63] Mohamed, R., Jamil, C.Z.M. (2020). The influence of environmental management accounting practices on environmental performance in small-medium manufacturing in Malaysia. International Journal of Environment and Sustainable Development, 19(4): 378-392. https://doi.org/10.1504/IJESD.2020.110643

[64] Phan, T.N., Baird, K., Su, S. (2017). The use and effectiveness of environmental management accounting. Australasian Journal of Environmental Management, 24(4): 355-374. https://doi.org/10.1080/14486563.2017.1354235

[65] Asa'd, M., Ahmad, W.N.W., Ayoup, H. (2024). Environmental management accounting information and environmental performance, the mediating effect of environmental decision quality. International Journal of Energy Economics and Policy, 14(2): 562-573. https://doi.org/10.32479/ijeep.15487

[66] Deb, B.C., Rahman, M.M., Rahman, M.S. (2023). The impact of environmental management accounting on environmental and financial performance: Empirical evidence from Bangladesh. Journal of Accounting & Organizational Change, 19(3): 420-446. https://doi.org/10.1108/JAOC-11-2021-0157

[67] Sahu, S.K. (2025). Ethical agile: Integrating business ethics and corporate social responsibility into agile project management. In AI-Powered Leadership: Transforming Organizations in The Digital Age. IGI Global Scientific Publishing, pp. 163-194. https://doi.org/10.4018/979-8-3373-1687-1.ch006

[68] Garoui, N., Ibrahim, S. (2025). Identifying the enablers of corporate social responsibility adoption in construction firms. Discover Sustainability, 6(1): 503. https://doi.org/10.1007/s43621-025-01364-w

[69] Soares, E.C., Lima, N.C., Coelho, A.F.M. (2024). Towards sustainability engaged accounting: A behavioral approach. Revista Contabilidade & Finanças, 35(95): e2019. https://doi.org/10.1590/1808-057x20242019.en

[70] Zyznarska-Dworczak, B. (2020). Sustainability accounting-cognitive and conceptual approach. Sustainability, 12(23): 9936. https://doi.org/10.3390/su12239936

[71] Niazi, U.I., Nisar, Q.A., Nasir, N., Naz, S., Haider, S., Khan, W. (2023). Green HRM, green innovation and environmental performance: The role of green transformational leadership and green corporate social responsibility. Environmental Science and Pollution Research, 30(15): 45353-45368. https://doi.org/10.1007/s11356-023-25442-6

[72] Hu, W., Xu, Y., Yang, J. (2025). Green human resource practices and corporate sustainable performance-the role of corporate green culture and dynamic capabilities. Corporate Social Responsibility and Environmental Management, 32(1): 635-646. https://doi.org/10.1002/csr.2978

[73] Khaddage-Soboh, N., Yunis, M., Imran, M., Zeb, F. (2024). Sustainable practices in Malaysian manufacturing: The influence of CSR, transformational leadership, and green organizational culture on environmental performance. Economic Analysis and Policy, 82: 753-768. https://doi.org/10.1016/j.eap.2024.04.001

[74] Luo, J., Zaman, S.I., Jamil, S., Khan, S.A. (2025). The future of healthcare: Green transformational leadership and GHRM’s role in sustainable performance. Benchmarking: An International Journal, 32(3): 805-837. https://doi.org/10.1108/BIJ-08-2023-0523

[75] Hasan, M.S. (2023). The impact of digital transformation on the quality of financial reports a field study in a sample of banks listed in the Iraqi Stock exchange. American Journal of Business Management, Economics, and Banking, 8: 101-120.

[76] Wu, J.W., Chen, J.Q., Li, L., Li, Y.Z., GU, Z., Ooi, K.L. (2023). The impact of digital transformation on financial reporting and analysis in the accounting industry. International Journal of Accounting, 8(50): 290-309. https://doi.org/10.55573/IJAFB.085021

[77] Petcu, M.A., Sobolevschi-David, M.I., Curea, S.C. (2024). Integrating digital technologies in sustainability accounting and reporting: Perceptions of professional cloud computing users. Electronics, 13(14): 2684. https://doi.org/10.3390/electronics13142684

[78] Abdelhalim, A.M., Ibrahim, N., Alomair, M. (2023). The moderating role of digital environmental management accounting in the relationship between eco-efficiency and corporate sustainability. Sustainability, 15(9): 7052. https://doi.org/10.3390/su15097052

[79] Zhang, W., Zhao, J. (2023). Digital transformation, environmental disclosure, and environmental performance: An examination based on listed companies in heavy-pollution industries in China. International Review of Economics & Finance, 87: 505-518. https://doi.org/10.1016/j.iref.2023.06.001