A. Nurul Khaeria![]() | Majidah Majidah*

| Majidah Majidah*![]() | Hosam Alden Riyadh

| Hosam Alden Riyadh![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study aims to analyze the factors that influence the Environmental, Social, and Governance (ESG) in non-financial companies in Indonesia and Malaysia. These factors consist of profitability, leverage, human resource slack (HRS), cost leadership, audit committee, and firm size. Using sampling criteria, a sample of 95 non-financial companies listed on the Indonesia Stock Exchange and the Malaysia Stock Exchange during the period 2021-2023 was obtained, with a total of 285 observations. STATA 18 software was used for analysis. The combined results of the two countries indicated that cost leadership and firm size were positive determinants of ESG, while human resource slack is a negative determinant of ESG. The results of the Indonesian study indicate that leverage is a negative determinant, while human resource slack and firm size are positive determinants. The results of the Malaysian study indicate that human resource slack and audit committee are negative determinants. Meanwhile, it indicates that cost leadership and firm size are positive determinants. The results of this study provide insights for non-financial companies in Indonesia and Malaysia that can inform investors' decisions when considering investments in these companies across both countries.

ESG, profitability, leverage, human resource slack (HRS), cost leadership, audit committee

Corporate environmental, social and governance (ESG) practices and actions highlight the sustainability perspective. ESG supports organizations in protecting and optimizing their ability to create value that persists over the years [1]. Engaging in ESG initiatives enhances a company’s financial outcomes, potentially attracting investor interest [2]. ESG performance has been recognized as a crucial performance filed by various companies. These documents outline the ESG-related initiatives undertaken by the firms. Empirical and theoretical research examines the possible connection between ESG performance and business characteristics [3].

Farah et al. [4] explained that as pressure on social and environmental duties increases, companies are becoming more interested in ESG information. As a result, companies must manage their corporate governance systems to meet social and environmental criteria while still achieving long-term growth [5]. The environmental aspect covers awareness and preservation of the environment; the social aspect emphasizes human rights, workforce development, stakeholder concerns, and broader social matters; while the governance aspect pertains to the connection between company management and stakeholders [6]. However, there is a framework of regulations that outlines how shareholders, creditors, executives, employees, government authorities, and other stakeholders, both external and internal, interact in terms of their rights and responsibilities, essentially functioning as a mechanism that governs and oversees the company's operations [7]. In the stakeholder concept, an increasing number of companies globally are starting to produce sustainability reports as stakeholders demand increased openness on ESG matters. Adopting ESG best practices gives economic and non-financial corporations a long-term competitive advantage [8]. The economic development of Indonesia and Malaysia is strategically supported by non-financial companies. ESG performance is a key focus as it contributes to improving transparency and sustainability of company operations from regulators and investors. Financial Services Authority Regulation Number 51/POJK.03/2017 about the deployment of sustainable financial strategies, including public companies, requires all firms listed on the IDX to submit sustainability reports since 2021. Bursa Malaysia has required sustainability reporting for listed companies since 2015, with full implementation in 2016 [9].

However, one of the biggest challenges is the increasing risk of ESG washing or greenwashing, which is the presentation of sustainability information that does not match reality [10]. Without strict supervision, ESG reporting risks becoming a mere formality, without real substance in corporate practice [11]. Similarly, Nugraha [12] stated that more than 600 issuers have published ESG reports, but the quality and accuracy of these reports are still in doubt due to the absence of a strong verification mechanism.

The Environmental, Social, and Governance (ESG) phenomenon in Indonesia shows complex dynamics, reflecting the challenges in integrating sustainability principles into business practices. Since 2021, the Financial Services Authority has required issuers and public companies to submit sustainability reports, as specified in POJK No. 51/POJK.03/2017 on the application of sustainable financial strategies including public companies. However, this obligation has been enacted, its implementation still faces various challenges [10]. ESG is now considered an important parameter by investors in measuring a company's long-term performance and its exposure to non-financial risks, especially environmental and social risks [13]. Global interest in ESG investments is increasing rapidly, with funds raised reaching US$649 billion by the end of 2021, up significantly from previous years [14]. However, despite the rapid growth of ESG investments, the application of ESG strategies in companies in Indonesia and Malaysia still lags. A 2022 survey by PwC Singapore and the Center for Governance and Sustainability (CGS) revealed that less than 10% of companies in these two countries have comprehensively adopted ESG principles. This figure is far below other Asia Pacific countries such as Australia (50%), Taiwan (30%), Thailand (25%), Singapore (20%) and Japan (20%). In fact, Indonesia and Malaysia's position in ESG adoption is on par with the Philippines and India which also have low implementation rates with a percentage of less than 10%. This phenomenon is even more alarming because according to the Center for Risk Management & Sustainability (CRMS) Indonesia, the majority of large companies in the region - including Indonesia - still do not have sufficient awareness and capacity to manage ESG issues thoroughly. Current practices tend to be superficial, with many companies only reporting on ESG aspects superficially to meet compliance demands, not as a key aspect of a sustainable business strategy [15]. This creates a paradox between the high interest in ESG investments and the low level of implementation at the corporate level, pointing to the need for a more holistic approach and real commitment from businesses.

The level of ESG adoption in Malaysia is relatively low compared to Indonesia at less than 10% of companies, but Malaysia's ESG development shows a more mature regulatory framework than Indonesia. Bursa Malaysia has made sustainability reporting mandatory for listed companies since 2015, with full implementation in 2016, and further strengthened until 2023 by adopting the Task Force on Climate-related Financial Disclosures (TFCD) suggestions [9]. In contrast, Indonesia has only implemented a “comply-or-explain” rule for ESG reporting for issuers through POJK 51/2017 of the Financial Services Authority (OJK) on the Application of sustainable financial strategies including public companies, with implementation remaining voluntary until 2023. CRMS [15] found that the majority of companies in Indonesia still conduct ESG reporting as a compliance formality, not as a business strategy. The relatively low implementation of ESG in both countries and different regulatory support motivated this research to investigate the factors that impact ESG in Indonesia and Malaysia.

This study aims to analyze the factors that influence the ESG performance of non-financial companies in Indonesia and Malaysia during the 2021-2023 period. Specifically, this study evaluates five independent variables namely profitability, leverage, human resource slack (HRS), cost leadership, and audit committee on the company's ESG score obtained from LSEG. By comparing companies from two countries that have different levels of ESG adoption and regulation, this study is expected to provide a deeper understanding of the key determinants of ESG and the differences in its implementation, which can be used as a basis for decision-making by regulators and investors in promoting corporate sustainability.

The structure of this study consists of five main sections. The introduction outlines the background and urgency of ESG research in Indonesia and Malaysia. The literature review discusses theories and previous research related to factors that influence ESG performance. Methodology explains the use of panel data from 95 non-financial companies during 2021-2023 and regression analysis with the Random Effect model. Results and discussion present the empirical findings as well as the comparison between the two countries. Finally, the conclusion summarizes the main findings and provides implications and recommendations for improving ESG performance.

ESG performance has increased significantly for companies around the world in recent years [16]. One of the main forces behind ESG performance found is stakeholder demand which is in line with stakeholder theory [17]. Stakeholder theory, which states that stakeholders influence an organization's operations and vice versa, is at the core of non-financial performance issues [18]. Companies provide ESG information to all stakeholders because they pay attention to ESG issues and companies need to enhance transparency in ESG reporting performance to satisfy stakeholder demand, reduce knowledge asymmetry, and reduce stakeholder conflicts [19]. More ESG performance from companies has become a requirement from shareholders, especially corporate investors [20]. Greater emphasis on ESG performance as a strategy to appeal to and keep investors has resulted from this pressure [21].

Empirical research on factors affecting ESG performance is generally categorized into three levels [16, 22-26]. Political and labor systems, laws and regulations, economic growth, and cultural principles have all been identified as key factors influencing ESG performance at the national level [16, 24, 27]. Many factors, such as profitability, leverage, HRS, cost leadership and audit committee are known to have an impact on the level of corporate ESG performance [18, 28-30]. Using the ESG score as a proxy which is the overall company score in a certain period guided by on its reported activities by the company in the ESG categories [31].

2.1 Profitability

ESG performance has evolved into an effective means for firms to enhance their financial capabilities, stakeholder engagement, and public image. Thus, a growing number of analyses have examined the connection between a firm's financial performance and its ESG [32-34], showing how companies with strong financial results usually have high ESG scores as they have more resources available to them to continuously adopt sustainable practices. This illustrates how sustainability can deliver long-term value through improved risk management, increased investor loyalty and operational efficiency, rather than simply being a financial burden. Companies will benefit from increased demand and growth generated by sustainable operations, as well as reduced business risks.

H1: Profitability has a positive effect on ESG performance.

2.2 Leverage

Leverage is corporate debt used to improve the financial position of a business [35]. Overreliance on debt may elevate a company's financial risk exposure, including liquidity problems due to high interest expenses [36], decreased investment capacity [37] and increased risk of default during the economic crisis [38]. Leverage assessed applying the Debt to Asset Ratio (DTA) was shown to exhibit a negative effect on ESG performance [18, 39]. Firms with high leverage currently emphasize their financial achievements in order to be able to complete their financial obligations, so that ESG is not a company priority.

H2: Leverage has a negative effect on ESG Performance.

2.3 Human resource slack

Companies that prioritize sustainability can gain a competitive advantage by developing the potential and uniqueness of their assets [40]. HRS includes competencies in possibility knowledge sectors that are required when organizations are under pressure from strong rivalry [41-43]. Recent research suggests that HRS plays a distinctive role in supporting corporate ESG implementation. According to Tang and Tang [44], excess HR capacity allows firms to establish specialized teams that focus on ESG initiatives without compromising core operational productivity. The findings of Chen et al. [45] further reveal that HRS is an important catalyst for green innovation, as companies with sufficient HR reserves tend to experiment more actively with sustainable solutions. A quantitative study by Waddock and Graves [46] on 1.250 global companies reinforces these findings, showing a significant correlation between HRS and improved ESG scores, particularly in the social and governance dimensions. The main mechanism is the flexibility of HR allocation for ESG training and sustainability program development, which is hard for rivals to replicate [47].

H3: HRS has a positive effect on ESG performance.

2.4 Cost leadership

Cost leadership firms execute improve in terms of ESG and have a lower chance of going bankrupt. Related to this, companies that use cost leadership produce goods at reduced expenses and pricing compared to rivals to gain an edge in the market [28]. To guide corporate strategy, influence overall productivity, and improve performance, corporate strategy is essential. In the same framework, related studies argue that managers make strategic choices about strategic approaches, including those related to cost leadership, which can impact ESG performance [48, 49]. Similarly, related research argues that effective ESG practices and strong business strategies are critical to the development of the firm. The best source of improving performance and gaining competitive advantage, from a resource-based perception, is the internal competencies and assets of the firm [50]. Research results show that companies with Cost leadership are associated with enhanced ESG results among firms [28].

H4: Cost leadership has a positive effect on ESG performance.

2.5 Audit committee

To improve the level and effectiveness of ESG initiatives without undermining objectivity or shareholder interests, an autonomous and a functioning internal control system is essential [51]. Due to their role in implementing sustainable business practices and providing more open information, audit committees have attracted more attention from stakeholders in recent years [52]. A growing body of studies shows that a firm's ESG disclosure is impacted by its audit committee membership [53]. The audit committee is specifically tasked with monitoring and regulating management choices and corporate activities relating to community and societal engagement for the benefit of stakeholders [54]. According to Appuhami and Tashakor [55], an independent audit committee (AC) can offer the effective monitoring necessary to achieve a balance between stakeholder and managerial objectives in the context of ESG disclosure. The implementation of voluntary disclosure has been significantly aided by audit committees [56]. The reason is that audit committees have the authority to influence and control top management to engage in voluntary reporting, particularly in ESG performance. Furthermore, audit committees can act as a buffer to decrease information asymmetry and tension of enthusiasm amidst senior management and shareholders [57]. A key foundation of a sound framework for corporate governance, based on Buallay and Al-Ajmi [58], is the audit committee (AC). These committees aim to strengthen financial reporting, auditor performance, independence, objectivity, and the effectiveness of risk and financial decisions [59]. From an ESG perception, the duties of audit committees become more important as they are responsible for verifying that the sustainability information provided is correct, verifiable, and not merely symbolic. One indicator of audit committee diligence is the number of annual meetings [60]. Frequent meetings compel managers to offer greater detail in their reports [61].

H5: Audit committee has a positive effect on ESG performance.

2.6 Firm size

Firm size is a crucial factor in generating profits, as investors tend to place more trust in large-scale companies with significant assets. This is due to the assumption that large companies can consistently improve performance and continually strive to improve the quality of their profits [62]. Firm size has more adequate resources and infrastructure capacity to implement ESG initiatives [63]. Several studies have revealed that firm size, as measured by total assets, has a positive effect on ESG performance [64, 65].

H6: Firm size has a positive effect on ESG performance.

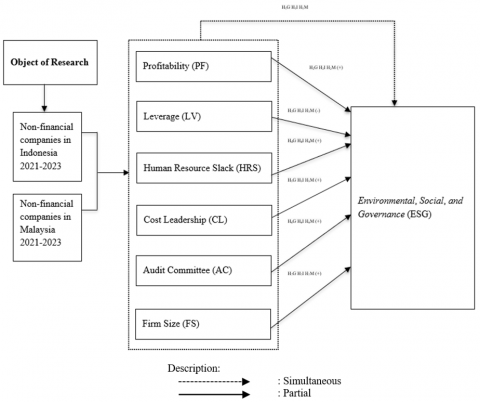

Based on the research model, the research hypothesis is formulated as follows (Figure 1):

Figure 1. Research model

H1G: Profitability, leverage, HRS, cost leadership, audit committee and firm size have an effect ESG in the non-financial sector in Indonesia and Malaysia for the period 2021-2023.

H1I : Profitability, leverage, HRS, cost leadership, audit committee and firm size have an effect ESG in the non-financial sector in Indonesia for the period 2021-2023.

H1M: Profitability, leverage, HRS, cost leadership, audit committee and firm size have an effect ESG in the non-financial sector in Malaysia for the period 2021-2023.

H2G: Profitability has positive effect ESG in the non-financial sector in Indonesia and Malaysia for the period 2021-2023.

H2I: Profitability has positive effect ESG in the non-financial sector in Indonesia for the period 2021-2023.

H2M: Profitability has positive effect ESG in the non-financial sector in Malaysia for the period 2021-2023.

H3G: Leverage has negative effect ESG in the non-financial sector in Indonesia and Malaysia for the period 2021-2023.

H3I: Leverage has negative effect ESG in the non-financial sector in Indonesia for the period 2021-2023.

H3M: Leverage has negative effect ESG in the non-financial sector in Malaysia for the period 2021-2023.

H4G: HRS has positive effect ESG in the non-financial sector in Indonesia and Malaysia for the period 2021-2023.

H4I: HRS has positive effect ESG in the non-financial sector in Indonesia for the period 2021-2023.

H4M: HRS has positive effect ESG in the non-financial sector in Malaysia for the period 2021-2023.

H5G: Cost leadership has positive effect ESG in the non-financial sector in Indonesia and Malaysia for the period 2021-2023.

H5I: Cost leadership has positive effect ESG in the non-financial sector in Indonesia for the period 2021-2023.

H5M: Cost leadership has positive effect ESG in the non-financial sector in Malaysia for the period 2021-2023.

H6G: Audit committee has positive effect ESG in the non-financial sector in Indonesia and Malaysia for the period 2021-2023.

H6I: Audit committee has positive effect ESG in the non-financial sector in Indonesia for the period 2021-2023.

H6M: Audit committee has positive effect ESG in the non-financial sector in Malaysia for the period 2021-2023.

H7G: Firm size has positive effect ESG in the non-financial sector in Indonesia and Malaysia for the period 2021-2023.

H7I: Firm size has positive effect ESG in the non-financial sector in Indonesia for the period 2021-2023.

H7M: Firm size has positive effect ESG in the non-financial sector in Malaysia for the period 2021-2023.

This research utilizes a purposive sampling method of non-financial companies recorded on the Malaysia Stock Exchange (BEM) and Indonesia Stock Exchange (IDX) for the period 2021-2023. The selection criteria include: (1) completeness of annual and financial reports, (2) availability of ESG scores from LSEG, and (3) completeness of research data. Using these criteria as a basis, out of 95 companies obtained, 28 were based in Indonesia and 67 were Malaysian companies, with a total observation of 285 data (collected over three years). The difference in the number of samples between the two countries is mainly due to variations in the number of non-financial companies recorded on each stock exchange, where Bursa Malaysia does have a larger base of non-financial issuers. In its analysis, this study focuses on six key variables: ESG score as a sustainability performance indicator, Debt to Assets Ratio (DTA), also Return on Assets (ROA) as financial performance measures, HRS and Asset Turnover Ratio (ATO) as Cost Leadership, and prevalence of audit committee meetings as a governance indicator. And Size as to Firm Size. The operationalization of all variables is shown in detail in Table 1.

Table 1. Operational variable

|

Variable |

Indicator |

Scale |

|

ESG |

ESG Score Range by Indicator:

|

Nominal |

|

Profitability |

$\mathrm{ROA}=\frac{\text { Net Income }}{\text { Average Total Asset }} \times 100 \%$ [67] |

Ratio |

|

Leverage |

DAR $=\frac{\text { Total Liabilities }}{\text { Total Asset }} \times 100 \%$ [68] |

Ratio |

|

HRS |

$\operatorname{HRS}=\left[\frac{\left(\frac{\text { firm sales it }}{\text { firm employees it }}\right)}{\left(\frac{\text { firm sales }_{\mathrm{it}-1}}{\text { firm sales }_{\mathrm{it}-1}}\right)}\right]-1$ If HR Slack >1: Increase. If HR Slack <1: Decrease [69] |

Ratio |

|

Cost Leadership |

ATO $=\frac{\text { Operating Sales }}{\text { Average Net Operating Assets }}$ [70] |

Ratio |

|

Audit Committee |

Number of meetings held by Audit Committee [30] |

Ratio |

|

Firm Size |

Size = Natural logarithm of total assets of enterprises [71] |

Ratio |

|

Country Code |

0 |

Nominal |

|

|

1 |

|

Descriptive statistical analysis was conducted as an initial stage to realize the basic aspects of the research data, including examination of data distribution and calculation of mean values of all variables. Comparative analysis between Indonesian and Malaysian companies was then applied to identify the basic patterns of differences in characteristics between the two sample groups. This study utilizes quantitative analysis techniques with a panel data approach, which was chosen because it covers a wide range of companies (cross-section) within three years (time-series). To obtain accurate results, panel data regression was carried out employing STATA 18 software. The estimation model employed in this study is formulated as follows:

$\begin{gathered}\mathrm{ESG}=\alpha+\beta_1 \mathrm{PF}+\beta_2 \mathrm{LV}+\beta_3 \mathrm{HRS}+\beta_4 \mathrm{CL} +\beta_5 \mathrm{AC}+\beta_6 \mathrm{FS}+\varepsilon\end{gathered}$

$\begin{gathered}\mathrm{ESG} 0=\alpha+\beta_1 \mathrm{PF} 0+\beta_2 \mathrm{LV} 0+\beta_3 \mathrm{HRS} 0+\beta_4 \mathrm{CL} 0 +\beta_5 \mathrm{AC} 0+\beta_6 \mathrm{FS} 0+\varepsilon\end{gathered}$

$\begin{gathered}\mathrm{ESG} 1=\alpha+\beta_1 \mathrm{PF} 1+\beta_2 \mathrm{LV} 1+\beta_3 \mathrm{HRS} 1+\beta_4 \mathrm{CL} 1 +\beta_5 \mathrm{AC} 17 \beta_6 \mathrm{FS} 1+\varepsilon\end{gathered}$

where,

ESG: Environmental, Social, and Governance

$\alpha$: Constant

$\beta$: Regression Coefficient

PF: Profitability

LV : Leverage

HRS: Human Resource Slack

CL: Cost Leadership

AC: Audit Committee

FS: Firm Size

0: Indonesia

1: Malaysia

$\varepsilon$: Error term

Three estimation techniques in panel data regression are fixed effect, common effect, random effect. To find out which model to use, it is needed to test the model selection of the three models, namely, Lagrange Multiplier, Chow, and Hausman Test.

The descriptive statistics findings analysis related to profitability, leverage, human resources slack, cost leadership, audit committee, and ESG for Indonesian and Malaysian companies are presented in Table 2 below.

Table 2 presents the findings from descriptive analysis of the two countries as follows:

Table 2. Descriptive statistics

|

Variable |

Obv |

Mean |

Std. Deviation |

Min |

Max |

|

Indonesia & Malaysia |

|||||

|

ESG |

285 |

49.97544 |

17.95405 |

7 |

89 |

|

Profitability |

285 |

.0657965 |

.1587481 |

-1.065 |

1.036 |

|

Leverage |

285 |

.4752667 |

.3386924 |

.004 |

3.162 |

|

Human Resources Slack |

285 |

.1678246 |

1.408888 |

-.99 |

22.235 |

|

Cost Leadership |

285 |

1.036726 |

2.174033 |

.001 |

16.598 |

|

Audit Committee |

285 |

7.161404 |

5.97606 |

2 |

43 |

|

Firm Size |

285 |

30.04688 |

1.638382 |

25.835 |

33.731 |

|

Indonesia |

|||||

|

ESG |

84 |

49.70238 |

18.40101 |

19 |

89 |

|

Profitability |

84 |

.0761786 |

.1383066 |

-.159 |

1.036 |

|

Leverage |

84 |

.4836548 |

.2404422 |

.081 |

1.39 |

|

Human Resources Slack |

84 |

.1104405 |

.2710014 |

-.36 |

1.055 |

|

Cost Leadership |

84 |

.6520952 |

.5230607 |

.115 |

2.445 |

|

Audit Committee |

84 |

10.30952 |

9.838425 |

3 |

43 |

|

Firm Size |

84 |

31.11877 |

1.278965 |

26.326 |

33.731 |

|

Malaysia |

|||||

|

ESG |

200 |

49.985 |

17.79206 |

7 |

84 |

|

Profitability |

200 |

.06155 |

.1670947 |

-1.065 |

.81 |

|

Leverage |

200 |

.473275 |

.3729512 |

.004 |

3.162 |

|

Human Resources Slack |

200 |

.192465 |

1.673357 |

-.99 |

22.235 |

|

Cost Leadership |

200 |

1.20256 |

2.556823 |

.001 |

16.598 |

|

Audit Committee |

200 |

5.84 |

2.158168 |

2 |

18 |

|

Firm Size |

200 |

29.59009 |

1.563704 |

25.835 |

33.278 |

Indonesia's average ESG score of 49.975 is more than the standard deviation of 17.954; the score indicates that ESG in Indonesia is relatively satisfactory. Meanswhile, the average ESG score of Malaysian firms is 49.985, more than the standard deviation of 17.79206. The ESG score of Malaysian companies although slightly higher than Indonesian companies, but both are at a relatively satisfactory level.

The average profitability of Indonesian companies is 0.0761786 less than 0.1383066; the profitability of Indonesian companies included in the ESG score varies. The average profitability proxied by ROA is 7.61786%, the percentage explains that the ability of Indonesian companies included in the ESG score to generate profits using the company's asset resources is 7.61786. The average profitability of Malaysian companies contained in the ESG score is .06155 less than the standard deviation of 0.1670947. The ability of Malaysian companies included in the ESG score to generate profits using their asset resources is 6.155%. This value is lower than Indonesian companies, with a higher variation in ROA than Indonesian companies.

The average leverage of companies in Indonesia, included in the ESG score of 0.4836548 with a standard deviation of 0.2404422, indicates that the financing structure of these companies is relatively high and fairly consistent between companies. Leverage is assessed based debt to asset ratio so that the percentage explains that almost half of the firms' debt is financed from the firms' total resources. Meanwhile, the average leverage of companies in Malaysia recorded in the ESG score of 0.473257 is slightly lower than Indonesia, with a larger standard deviation of 0.3729512. This result that debt financing financed by assets in Malaysia tends to be more diverse, although in general leverage is slightly lower than companies in Indonesia.

The average human resources slack of Indonesian companies included in the ESG score was recorded at 0.1104405 with a standard deviation of 2.710014, reflecting a considerable level of disparity in the utilization of spare human resources among companies that have an ESG score. This figure shows that some companies have considerable spare labor capacity, but not a few have a low level of labor efficiency. This value indicates that the ability of Indonesian companies to manage labor efficiency, proxied by the ratio of total sales per total employees among the previous and current year, is still uneven across sectors. On the other hand, companies in Malaysia show an average human resources slack also included in the ESG score of 0.192465 with a standard deviation of 1.673357. This suggests that higher efficiency and better consistency in labor management compared to Indonesia. Although Malaysia's average HRS is higher, the variation between companies tends to be smaller, reflecting that companies with ESG scores have more stable and controlled human resource management.

The cost leadership strategy of companies in Indonesia included in the ESG score has an average of 0.6520952 with a standard deviation of 0.5230607. This reflects that the implementation of cost efficiency strategies is applied at a moderate level, with a relatively low level of variation between companies. These findings that Indonesian firms in the ESG group tend to have a more consistent approach to cost efficiency. In contrast, companies in Malaysia show an average cost leadership of 1.20256 and a standard deviation of 2.556823. This value suggests that cost efficiency strategies in Malaysia vary significantly, with some companies showing more dominance in cost efficiency than others. Thus, on average, Malaysian firms exhibit a stronger focus on cost leadership with a much greater degree of non-uniformity than companies in Indonesia.

On average, Indonesian firms recorded 10.31 audit committee meetings, as reflected in the ESG scores with a standard deviation of 9.838425. This relatively high average value with large variations reflects the absence of uniform standards or guidelines in the prevalence of audit committee meetings, as elements within the internal control structure in Indonesian companies. Meanwhile, companies in Malaysia that are also comprised in the ESG score have an average frequency of audit committee members of 5.845771 with a standard deviation of 2.158168, indicating that the audit committee structure in Malaysia tends to be more consistent and uniform than in Indonesia. Thus, the implementation of governance through the frequency of audit committee meetings in Indonesia still varies, while Malaysia shows a more stable pattern.

The average size of companies in Indonesia that fall into the ESG-scored company category is 31.11877 with a standard deviation of 1.278965. This indicates that companies in Indonesia within the ESG category generally have relatively large sizes with low variation among companies. This finding reflects consistency in the operational scale of ESG companies in Indonesia. Meanwhile, companies in Malaysia have an average size of 29.59009 with a standard deviation of 1.563704. This value indicates that the size of ESG companies in Malaysia tends to be smaller than in Indonesia, but with higher variation. Therefore, on average, ESG companies in Indonesia have a larger and more uniform scale than ESG companies in Malaysia.

The panel data regression analysis was conducted in three stages, namely: (1) combined regression for Indonesian and Malaysian companies, (2) regression specifically for Indonesian companies, and (3) regression specifically for Malaysian companies. The selection of the estimation model is done through testing with the Lagrange Multiplier Test, Chow Test, and Hausman Test. From all these stages, the chosen model is the Random Effect Model. Before interpretation, the model is tested for classical assumptions, and if violations are found, such as autocorrelation or heteroscedasticity, transformation is carried out using the Generalized Least Squares (GLS) method to make the results more robust.

Table 3 shows that the data do not reject H0 and conclude that the data is normally distributed because prob.=0.2136>alpha (0.05), but in line with the Gaussian central limit theorem and the law of large numbers, if n>30, the data can be assumed to be approximately normally distributed.

Table 3. Data normality test for both Indonesia & Malaysia

|

Skewness and Kurtosis Tests for Normality |

|||||

|

Variable |

Obs |

Pr(Skewness) |

Pr(Kurtosis) |

Join Test |

|

|

Adj chi2(2) |

Prob>Chi2 |

||||

|

resid |

285 |

0.9583 |

0.0800 |

3.09 |

0.2136 |

Table 4 shows that the data are free of heteroscedasticity because prob. =0.4545>alpha (0.05), so the chosen REM model is robust to heteroscedasticity.

Table 4. Heteroscedasticity test of data for both countries, Indonesia & Malaysia

|

Breusch-Pagan/Cook-Weisberg Test for Heteroskedasticity |

|

|

Assumption |

: Normal Error Terms |

|

Variable |

: Fitted values for ESG |

|

HØ |

: Constant Variance |

|

chi2 (1) |

=0.56 |

|

Prob>Chi2 |

= 0.4545 |

Table 5 shows that the model is the model is free of autocorrelation because p-value =0.0036<alpha (0.05), so the REM model is transformed to be robust against autocorrelation.

Table 5. Autocorrelation test for data of both Indonesia & Malaysia

|

Woolridge Tests for Autocorrelation in Panel Data |

|

|

HØ |

: No First-Order autocorrelation |

|

F (1, 94) |

=8.906 |

|

Prob>F |

=0.0036 |

Table 6 presents that the model is free of multicollinearity assumptions because the VIF value is <10.

Table 6. Multicollinearity test data for both Indonesia & Malaysia

|

Variable |

VIF |

1/VIF |

|

Cost leadership |

1.35 |

0.738223 |

|

Profitability |

1.32 |

0.758951 |

|

Size |

1.24 |

0.805052 |

|

Leverage |

1.14 |

0.880399 |

|

Audit committee |

1.08 |

0.922380 |

|

Human resource slack |

1.08 |

0.860872 |

|

Mean VIF |

1.20 |

The results indicate that there is only a violation of the autocorrelation hypothesis so that the selected REM model will be transformed with PCSE as follows:

Table 7. Transformation with PCSE

|

Linear Regression, Correlated Panels Corrected Standard Errors (PCSEs) |

||||||

|

Group variable |

: firm |

number of obs |

=285 |

|||

|

Time Variable |

: year |

number of groups |

=95 |

|||

|

Panels |

: correlated (Balanced) |

obs per group: |

||||

|

Autocorrelation |

: common AR (1) |

min |

3 |

|||

|

avg |

3 |

|||||

|

max |

3 |

|||||

|

Estimated covariances |

=4560 |

R-squared |

0.5332 |

|||

|

Estimated autocorrelation |

=1 |

Wald chi2 (6) |

530.35 |

|||

|

Estimated coefficients |

=7 |

Prob>chi2 |

0.0000 |

|||

|

ESG |

Panel-corrected |

|||||

|

Coefficient |

std. error |

z |

P>| z | |

[95% conf. interval] |

||

|

Profitability |

1.261709 |

5.440019 |

0.23 |

0.817 |

-9.400533 |

11.92395 |

|

Leverage |

-.7709677 |

1.586401 |

-0.49 |

0.627 |

-3.880256 |

2.33832 |

|

Human resource slack |

-.4383523 |

. 2009345 |

-2.18 |

0.029 |

-.8321767 |

-.044528 |

|

Cost leadership |

1.731232 |

.3732335 |

4.64 |

0.000 |

.9997082 |

2.462757 |

|

Audit committee |

-.1278828 |

. 0810083 |

-1.58 |

0.114 |

-.2866561 |

. 0308906 |

|

Size |

5.279124 |

. 3689042 |

14.31 |

0.000 |

4.556085 |

6.002163 |

|

_Cons |

-109.2129 |

12.86624 |

-8.49 |

0.000 |

-134.4302 |

-83.99551 |

Table 7 shows that only violations of the hypothesis were found, indicating heteroscedasticity and correlation between cross-section units, which makes the OLS method inefficient and FGLS estimation potentially producing standard errors that are too small and unreliable. Therefore, the selected REM model will be modified using GLS white cross.

Table 8 shows that the data are normally distributed due to prob. =0.4335>alpha (0.05) and according to the large number theory and Gaussian central limit theory, if n>30, then the data can be considered to be close to normal distribution.

Table 8. Normality test of data for both Indonesian countries

|

Variable |

Obs |

Pr(Skewness) |

Pr(Kurtosis) |

Join Test |

|

|

Adj chi2(2) |

Prob>Chi2 |

||||

|

Resid |

84 |

0.6239 |

0.2394 |

1.67 |

0.4335 |

Table 9 shows that the conclusion data are free of heteroscedasticity because prob. =0.1029>alpha (0.05), so the selected REM model to be robust to heteroscedasticity.

Table 9. Heteroscedasticity test for the second data of Indonesia

|

Breusch-Pagan/Cook-Weisberg Test for Heteroskedasticity |

|

|

Assumption |

: Normal Error Terms |

|

Variable |

: Fitted values for ESG |

|

HØ |

: Constant Variance |

|

chi2 (1) |

=2.66 |

|

Prob > Chi2 |

=0.1029 |

Table 10 shows that the model is not free of autocorrelation because prob. =0.0014<alpha (0.05) so that the REM model to be robust to autocorrelation.

Table 10. Autocorrelation test of data for the two countries of Indonesia

|

Woolridge Tests for Autocorrelation in Panel Data |

|

|

HØ |

: No First-Order autocorrelation |

|

F (1, 27) |

=12.747 |

|

Prob > F |

=0.0014 |

Table 11 shows that the model is free of multicollinearity assumptions because the VIF value is <10.

Table 11. Multicollinearity test for Indonesian country data

|

Variable |

VIF |

1/VIF |

|

Size |

1.54 |

0.649425 |

|

Profitability |

1.43 |

0.699641 |

|

Cost leadership |

1.39 |

0.718421 |

|

Leverage |

1.21 |

0.829656 |

|

Audit committee |

1.18 |

0.844529 |

|

Human resource slack |

1.05 |

0.950512 |

|

Mean VIF |

1.30 |

Violations of autocorrelation and heteroscedasticity assumptions occur so that the selected REM model will be transformed with PCSE as follows (Table 12).

Table 13 shows that the data is normally distributed because prob. =0.7617<alpha (0.05) but is consistent with the large number and Gaussian central limit theory if n>30, then the data can be considered to be close to normally distributed.

Table 14 shows that the conclusion data is not free of heteroscedasticity because prob. =0.0359<alpha (0.05) so that the chosen REM model is robust to heteroscedasticity.

Table 12. Transformation with PCSE

|

Linear Regression, Correlated Panels Corrected Standard Errors (PCSEs) |

|||||

|

: firm |

number of obs |

=84 |

|||

|

: year |

number of groups |

=28 |

|||

|

: correlated (balanced) |

obs per group |

||||

|

common AR (1) |

min |

3 |

|||

|

avg |

3 |

||||

|

max |

3 |

||||

|

=406 |

R-squared |

0.5238 |

|||

|

=0 |

Wald chi2 (6) |

144.79 |

|||

|

=6 |

Prob > chi2 |

0.0000 |

|||

|

Panel-corrected |

|||||

|

Coefficient |

std. error |

z |

P > | z | |

[95% conf. interval] |

|

|

-3.040354 |

7.328446 |

-0.41 |

0.678 |

-17.40384 |

11.32314 |

|

-18.88864 |

7.040546 |

-2.68 |

0.007 |

-32.68786 |

-5.089427 |

|

3.553732 |

1.795036 |

1.98 |

0.048 |

.0355269 |

7.071937 |

|

-2.728638 |

2.319735 |

-1.18 |

0.239 |

-7.275234 |

1.817958 |

|

.1328247 |

. 085753 |

-1.55 |

0.121 |

. 0352482 |

. 3008976 |

|

4.900527 |

1.785342 |

2.74 |

0.006 |

1.401321 |

8.399734 |

|

-93.21977 |

59.67995 |

-1.56 |

0.118 |

-210.1903 |

23.75077 |

Table 13. Data normality test of both Malaysian countries

|

Variable |

Obs |

Pr(Skewness) |

Pr(Kurtosis) |

Join Test |

|

|

Adj chi2(2) |

Prob>Chi2 |

||||

|

Resid |

200 |

0.5186 |

0.7264 |

0.54 |

0.7617 |

Table 14. Heteroscedasticity test of data for both countries

|

Breusch-Pagan/Cook-Weisberg Test for Heteroskedasticity |

|

|

Assumption |

: Normal Error Terms |

|

Variable |

: Fitted values of ESG |

|

HØ |

: Constant Variance |

|

chi2 (1) |

=4.40 |

|

Prob>Chi2 |

=0.0359 |

Table 15 shows that the model is free of autocorrelation because prob. =0.0650>alpha (0.05) so that the REM model to be robust to autocorrelation.

Table 15. Autocorrelation test of data for both countries

|

Woolridge Tests for Autocorrelation in Panel Data |

|

|

HØ |

: No First-Order autocorrelation |

|

F (1, 65) |

=3.523 |

|

Prob>F |

=0.0650 |

Table 16 shows that the model is free of multicollinearity assumptions because the VIF value is <10.

The results indicate that there is only a violation of the autocorrelation assumption so the selected REM model will be transformed with PCSE as follows.

Table 16. Multicollinearity test of data for both countries

|

Variable |

VIF |

1/VIF |

|

Profitability |

1.40 |

0.714973 |

|

Cost leadership |

1.39 |

0.718153 |

|

Leverage |

1.15 |

0.871011 |

|

Size |

1.15 |

0.871585 |

|

Human resource slack |

1.10 |

0.913163 |

|

Audit committee |

1.05 |

0.948469 |

|

Mean VIF |

1.21 |

In Table 17, a simultaneous hypothesis test (F-test) is used to assess if all independent variables in the model significantly impact the dependent variable. Based on the findings of panel data regression F statistics and probability value =0.000 <0.05, it is suggested that simultaneously the independent variables of profitability, leverage, human resources slack, cost leadership, audit committee and firm size have a significant linear influence on the dependent variable ESG.

Table 17. Transformation with PCSE

|

Linear Regression, Correlated Panels Corrected Standard Errors (PCSEs) |

||||||

|

Group variable |

: firm |

number of obs |

=200 |

|||

|

Time Variable |

: year |

number of groups |

=67 |

|||

|

Panels |

: correlated (unbalanced) |

obs per group |

||||

|

Autocorrelation |

Common AR (1) |

min |

2 |

|||

|

avg |

2.9850746 |

|||||

|

max |

3 |

|||||

|

Estimated covariances |

=2278 |

R-squared |

0.5830 |

|||

|

Estimated autocorrelation |

=1 |

Wald chi2(6) |

715.16 |

|||

|

Estimated coefficients |

=7 |

Prob > chi2 |

0.0000 |

|||

|

ESG |

Panel-corrected |

|||||

|

Coefficient |

std. error |

z |

P>| z | |

[ 95% conf.interval] |

||

|

Profitability |

2.723091 |

4.020422 |

0.68 |

0.498 |

-5.156791 |

10.60297 |

|

Leverage |

. 8306371 |

.752074 |

1.10 |

0.269 |

- . 6434009 |

2.304675 |

|

Human resource slack |

-.5693148 |

. 1573125 |

-3.62 |

0.000 |

-.8776416 |

-.260988 |

|

Cost leadership |

1.777244 |

.4177371 |

4.25 |

0.000 |

.9584943 |

2.595994 |

|

Audit committee |

-.5871198 |

. 2208786 |

-2.66 |

0.008 |

-1.020034 |

-.1542056 |

|

Size |

6.277438 |

.5539977 |

11.33 |

0.000 |

5.191623 |

7.363254 |

|

_Cons |

-134.9996 |

17.19229 |

-7.85 |

0.000 |

-168.6965 |

-101.3034 |

Table 18 presents the panel data regression findings of the three research models. The results on the regression coefficient for HRS of Indonesia and Malaysia (β3G) is -.4383523 with a significance level of 0.029, which is smaller than α=0.05, indicating that HRS has a negative effect on ESG. Companies with excess human resources tend to have lower ESG scores due to potential inefficiencies in workforce management, which can impact ESG performance. On the other hand, the regression coefficient for cost leadership (β4G) is 1.731232 with a significance level of 0.000, which is smaller than α=0.05, indicating that the cost leadership has a positive effect on ESG. Companies that effectively implement cost efficiency strategies can allocate resources optimally, increase productivity, and support better sustainability practices, thereby achieving higher ESG. In addition, the firm size regression coefficient (β6G) of 5.279124 with a significance level of 0.000, which is smaller than α=0.05, also shows that firm size has a positive effect on ESG scores. Larger companies generally have more adequate resources to invest in ESG initiatives.

The regression results for Indonesian companies show that the leverage has a negative effect on ESG with coefficient (β2I) of -18.88864 with a significance level of 0.007, which is smaller than α=0.05. This suggests that the higher a company's debt proportion, the lower its ESG score. Companies with high leverage tend to prioritize financial stability and debt repayment, thereby reducing their focus on sustainability initiatives. Conversely, the HRS has a positive effect on ESG with a coefficient (β3I) of 3.553732 and a significance value of 0.048, which is less than α=0.05. This indicates that the availability of human resources that are not fully utilized can be leveraged to support sustainability activities, such as ESG reporting, internal training, and corporate social engagement. In addition, firm size has a positive effect on ESG scores, with a coefficient (β6I) of 4.900527 and a significance value of 0.006, which is below the α=0.05 threshold. This finding indicates that larger companies tend to have more adequate resources to implement ESG practices, both in terms of finance, management, and operational infrastructure.

Table 18. Panel data regression result

|

Variable |

Coeff |

T Stat |

P Value |

|

|

Indonesia & Malaysia |

|

|

|

Profitability |

1.261709 |

0.23 |

0.817 |

|

Leverage |

‐.7709677 |

‐0.49 |

0.627 |

|

Human Resources Slack |

‐.4383523 |

‐2.18 |

0.029 |

|

Cost Leadership |

1.731232 |

4.64 |

0.000 |

|

Audit Committee |

‐.1278828 |

‐1.58 |

0.114 |

|

Size |

5.279124 |

14.31 |

0.000 |

|

|

Indonesia |

|

|

|

Profitability |

‐3.040354 |

‐0.41 |

0.678 |

|

Leverage |

‐18.88864 |

‐2.68 |

0.007 |

|

Human Resources Slack |

3.553732 |

1.98 |

0.048 |

|

Cost Leadership |

‐2.728638 |

‐1.18 |

0.239 |

|

Audit Committee |

0.1328247 |

1.55 |

0.121 |

|

Size |

4.900527 |

2.74 |

0.006 |

|

|

Malaysia |

|

|

|

Profitability |

2.723091 |

0.68 |

0.498 |

|

Leverage |

0.8306371 |

1.10 |

0.269 |

|

Human Resources Slack |

‐.5693148 |

‐3.62 |

0.000 |

|

Cost Leadership |

1.777244 |

4.25 |

0.000 |

|

Audit Committee |

‐.5871198 |

‐2.66 |

0.008 |

|

Size |

6.277438 |

11.33 |

0.000 |

The results of panel data regression in Malaysia show that HRS and audit committees have a significant negative effect on ESG scores. HRS has a coefficient (β3M) of -0.5693148 with a significance level of 0.000, and the audit committee has a coefficient (β5M) of -0.5871198 with a significance level of 0.008, both below α=0.05. These results indicate that the presence of underutilized labor can create inefficiency or ineffectiveness in the implementation of ESG initiatives. Additionally, a weak or more formalistic audit committee role may not yet contribute meaningfully to oversight and promotion of the sustainability agenda. In contrast, cost leadership strategy and company size have a significant positive impact on ESG scores. The cost leadership strategy has a coefficient (β4M) of 1.777244 and a significance value of 0.000, while company size has a coefficient (β6M) of 6.277438 with a significance value of 0.000, both of which are below α=0.05. These findings suggest that companies that are efficient in cost management and have a larger scale of operations are more likely to be able to allocate resources to sustainability initiatives.

This study focuses on analyzing factors that may impact the ESG scores of non-financial firms in Indonesia and Malaysia. The factors tested include profitability, leverage, human resources slack, cost leadership, audit committees and firm size. According to the data analysis in Table 3, further analysis can be conducted regarding the influence of the aforementioned factors on the ESG performance scores of non-financial firms in Indonesia and Malaysia.

Profitability was found to have no significant effect on ESG scores in the combined dataset of both countries, as well as in the individual datasets of Indonesia and Malaysia. This finding is inconsistent with the research hypothesis [18, 33, 72] which assumed profitability has a positive effect on ESG performance. This study indicates that corporate profitability has not yet become a primary driver of active implementation of sustainability or ESG practices. Although descriptive data shows that the average profitability of non-financial companies in Indonesia is higher than that of Malaysia, this does not directly correlate with an increase in ESG scores.

Leverage has a significant adverse effect on the datasets of Indonesia, in line with the research hypothesis, whereas it has no significant effect on the datasets of both countries and Malaysian, contrary to the hypothesis. Research by Doshi et al. [18] shows similar results for the datasets of Indonesia, namely, leverage has a negative effect on ESG. This outcome is that firms with high leverage are more likely to have lower ESG performance. In contrast, the Malaysian dataset shows that companies with both high and low leverage do not have an effect on the ESG performance of those firms. The findings of the data analysis show that leverage in non-financial companies in Indonesia has a negative effect on ESG performance scores, while in Malaysia, leverage does not affect ESG performance scores. The average leverage of non-financial firms in Indonesia, as seen from the descriptive statistical results, is higher than that of non-financial companies in Malaysia.

Sustainable innovation depends on recruiting personnel who are more competent than necessary. In theory, having additional human resources will help overcome unexpected environmental disasters that cannot be quickly recruited and trained [73]. Data analysis results indicate that human resources slack has a significant favorable outcome on the Indonesian dataset aligned with the study findings hypothesis, while it has a significant negative impact on dataset of other two countries and Malaysian dataset, thus rejecting the hypothesis. Heubeck and Ahrens [29] and Adomako and Nguyen [73] show similar results with the Indonesian dataset, which are significantly positive. This highlights the importance of human resources slack, previously overlooked, in driving sustainable innovation. Unutilized human resources are a key driver of sustainable innovation through integrating findings from the studies on sustainable innovation and the perspective of resource slack [73]. However, traditional literature on slack resources states that slack resources are not optimal for environmental efficiency [74, 75]. Nevertheless, this literature supports the data analysis results for the datasets of Indonesia and Malaysia, as well as Malaysia alone, indicating that human resources slack has a significant negative effect on ESG performance. The outcomes of analyzing human slack resources have a positive effect on ESG in Indonesia, while human slack resources in non-financial companies in Malaysia have a negative effect on ESG. Descriptive statistics present that the average human resources slack of non-financial firms in Malaysia is higher than that of non-financial firms in Indonesia.

In addition, the hypothesis regarding cost leadership in this study is aligned with prior research findings, which suggest that cost leadership has a positive effect on ESG performance [28, 76]. Company strategy has a significant impact on sustainability performance, according to Yuan et al. [76] who examined the correlation between corporate strategy and sustainability performance. This axis states that to gain a competitive advantage, companies that use cost leadership strategies produce goods at lower costs and prices than their competitors. The results of the dataset research for both countries and Malaysia show that cost leadership has a positive impact on ESG performance, while the dataset for Indonesia has no impact on ESG performance. Nevertheless, the findings of this study are supported by the study of Jermias and Mahmoudian [77], which concluded that managers in cost leadership organizations that prioritize efficiency and direct financial gains are less likely to fund ESG initiatives. This is consistent with the results of Zhao et al. [78] and Zhang et al. [43]. The research findings for both countries and Malaysia indicate that cost leadership has a positive influence on ESG performance scores, while in Indonesia, cost leadership has no influence on ESG performance scores. The average cost leadership in Malaysia is higher than the average cost leadership in Indonesia. Once again, effective monitoring can improve compliance with corporate governance regulations and reduce opportunistic behavior by company managers [79, 80].

The regularity of audit committee meetings is one of many qualities that enable its members to monitor business operations more closely and efficiently [81]. Therefore, the researchers propose the hypothesis that the audit committee has a beneficial effect on a firm's ESG performance score. These findings are funded by previous studies that revealed corresponding outcomes, suggesting that a number of audit committee meetings can enhance a firm’s ESG achievement [51, 82]. However, the results of data analysis show that audit committees do not have an effect on ESG performance in the combined data set of both countries and Indonesia, while the Malaysian data audit committees have a negative effect on ESG. This indicates that non-financial companies in Malaysia have a lower level of audit committee involvement than similar companies in Indonesia, which may explain the identified negative effect.

Firm size is an important characteristic that can enhance a company's ability to implement sustainable practices and improve ESG performance. Therefore, the hypothesis is that firm size has a positive effect on ESG. This assumption is supported by data analysis results, which show that company size has a positive effect on ESG scores in the data sets of both countries, as well as in each country, Indonesia and Malaysia. This finding aligns with research findings [64, 65].

The purpose of this research is to examine the factors that affect Environment, Social, and Governance (ESG) scores in Indonesian and Malaysian non-financial organizations. The combined regression findings from data from both countries reveal that only HRS has a negative effect on ESG performance. This conclusion shows that the existence of HRS, reflected in the high number of employees compared to sales levels, tends to be an obstacle for companies in integrating sustainability and good governance principles. Inefficiency in labor utilization can divert the company's focus and resources from ESG initiatives, thereby negatively impacting the company's ESG score.

In addition, the combined regression results from the data of both countries also show that cost leadership and company size have a positive effect on ESG. This conclusion indicates that a company's effectiveness in maximizing the use of assets to generate revenue as a reflection of its cost leadership strategy is an important factor that encourages companies to be more aware of the importance of implementing sustainable practices and good governance, which ultimately contributes positively to ESG. Furthermore, this indicates that the total assets held by a company are a primary factor driving the capacity and awareness to adopt sustainability principles and good governance, which in turn positively impact ESG.

In Indonesian data, leverage has a negative effect, but human slack resources and firm size have a positive effect. Conversely, in the Malaysian data, HRS and audit committee have a negative effect, but cost leadership and firm size have a positive effect. Overall, Malaysian companies have slightly higher ESG scores than Indonesian companies, likely due to Malaysia's stricter ESG laws. However, leverage in Indonesia may be a barrier to improving ESG performance, despite the fact that Indonesian companies are often more profitable. On the other hand, Malaysian companies can optimize cost leadership and firm size, while strengthening internal oversight mechanism to avoid negative effects on HRS and audit committee. These activities are important for improving a company's global reputation and attracting investors who value sustainability.

ESG literature, particularly in the context of developing countries in Southeast Asia, namely Indonesia and Malaysia. Using panel data from non-financial firms over the period 2021-2023, this study identifies firm-internal factors that influence ESG performance. The finding that HRS has a negative effect, while cost leadership and firm size have a positive effect, enriches the understanding of relevant ESG determinants in a region with a still-developing level of sustainability adoption. In addition, this cross-country comparison offers new insights into the different roles of institutions and governance on the effectiveness of ESG implementation.

The practical implications of this study point to the importance of companies and regulators to not only focus on ESG reporting obligations, but also on strengthening internal capacity, such as the effectiveness of audit committees and the management of financial structures. For investors, these findings can be used as a reference in evaluating ESG-based companies for more sustainable investment decision-making. Meanwhile, regulators in Indonesia and Malaysia can utilize the results of this study to design policies that emphasize quality, not just formal compliance in ESG reporting.

This study has several limitations, including a focus on non-financial companies listed on the stock exchange, which means the results do not yet reflect the entire industrial sector, especially the MSME sector and private companies. In addition, the ESG variables used are based on scores from one data provider (LSEG), which may have a different assessment approach from other institutions. This study also only covers a three-year period, so it has not been able to illustrate the long-term dynamics of ESG implementation in each country. For future development, further research involving qualitative analysis that explores how companies internalize ESG values in their business strategies is recommended. Longer cross-sectoral and cross-time studies are also needed to see the consistency of the influence of internal factors on ESG performance. In addition, including external indicators such as pressure from institutional investors, government regulations, and organizational culture can provide a more holistic picture of the determinants and impacts of ESG implementation in Southeast Asia.

[1] Chebbi, K., Ammer, M.A. (2022). Board composition and ESG disclosure in Saudi Arabia: The moderating role of corporate governance reforms. Sustainability, 14(19): 12173. https://doi.org/10.3390/su141912173

[2] Atan, R., Alam, M.M., Said, J., Zamri, M. (2018). The impacts of environmental, social, and governance factors on firm performance: Panel study of Malaysian companies. Management of Environmental Quality: An International Journal, 29(2): 182-194. https://doi.org/10.1108/MEQ-03-2017-0033

[3] Ellili, N.O.D. (2023). Impact of corporate governance on environmental, social, and governance disclosure: Any difference between financial and non‐financial companies? Corporate Social Responsibility and Environmental Management, 30(2): 858-873. https://doi.org/10.1002/csr.2393

[4] Farah, B., Elias, R., Aguilera, R., Abi Saad, E. (2021). Corporate governance in the Middle East and North Africa: A systematic review of current trends and opportunities for future research. Corporate Governance: An International Review, 29(6): 630-660. https://doi.org/10.1111/corg.12377

[5] Kamal, Y. (2021). Stakeholders expectations for CSR-related corporate governance disclosure: evidence from a developing country. Asian Review of Accounting, 29(2): 97-127. https://doi.org/10.1108/ARA-04-2020-0052

[6] MSCI, E. (2022). MSCI ESG ratings methodology. MSCI ESG Research LLC.

[7] Nazar, M.R., Muslih, M., Anggraeni, G. (2016). Earnings quality: Corporate governance perception index, intellectual capital and spiritual values. Advanced Science Letters, 22(12): 4338-4340. https://doi.org/10.1166/asl.2016.8145

[8] Gurol, B., Lagasio, V. (2023). Women board members’ impact on ESG disclosure with environment and social dimensions: evidence from the European banking sector. Social Responsibility Journal, 19(1): 211-228. https://doi.org/10.1108/SRJ-08-2020-0308

[9] Bursa Malaysia. Main market listing requirements. https://www.bursamalaysia.com/regulation/listing_requirements/main_market/listing_requirements.

[10] Rahmasari, D., Feranda, K.R. Verani, R.R. (2025). Memperkuat pengaturan ESG di Indonesia. https://www.hukumonline.com/berita/a/ancaman-esg-washing--memperkuat-pengaturan-esg-di-indonesia-lt6780e6076fa2e/.

[11] Chen, H.Y., Yang, S.S. (2020). Do investors exaggerate corporate ESG information? Evidence of the ESG momentum effect in the Taiwanese market. Pacific-Basin Finance Journal, 63: 101407. https://doi.org/10.1016/j.pacfin.2020.101407

[12] Nugraha, D.W. Waspadai praktik “Greenwashing” dalam Laporan ESG. Kompas.id.

[13] Mariana, H. (2022). Saatnya Investor melirik prospek investasi berbasis ESG. Kompas. https://amp.kompas.com/money/read/2022/03/25/200627426/saatnya-investor-melirik-prospek-investasi-berbasis-esg.

[14] Reuters. (2021). U.S. investors flee to money market funds in the week ended May 19-Lipper. https://www.reuters.com/business/finance/us-investors-flee-money-market-funds-week-ended-may-19-lipper-2021-05-21/.

[15] CRMS. Mayoritas perusahaan besar asia pasifik belum peka terhadap ESG. https://crmsindonesia.org/publications/mayoritas-perusahaan-besar-asia-pasifik-belum-peka-terhadap-esg/.

[16] Jian, M., Sheng, Q. (2024). Macroeconomic factors and ESG performance: A cross-country study. Journal of Financial Economics, 145(2): 245-267.

[17] Zhu, Y., Zhang, R. (2024). How local tournament incentives influence ESG disclosure: CEO’s genuinely altruistic or self-serving? Social Responsibility Journal, 20(2): 383-404. https://doi.org/10.1108/SRJ-03-2023-0180

[18] Doshi, M., Jain, R., Sharma, D., Mukherjee, D., Kumar, S. (2024). Does ownership influence ESG disclosure scores? Research in International Business and Finance, 67: 102122. https://doi.org/10.1016/j.ribaf.2023.102122

[19] Al Amosh, H., Khatib, S.F. (2023). ESG performance in the time of COVID-19 pandemic: Cross-country evidence. Environmental Science and Pollution Research, 30(14): 39978-39993. https://doi.org/10.1007/s11356-022-25050-w

[20] Dyck, A., Lins, K.V., Roth, L., Wagner, H.F. (2019). Do institutional investors drive corporate social responsibility? International evidence. Journal of Financial Economics, 131(3): 693-714. https://doi.org/10.1016/j.jfineco.2018.08.013

[21] Ioannou, I., Serafeim, G. (2012). What drives corporate social performance? The role of nation-level institutions. Journal of International Business Studies, 43(9): 834-864. https://doi.org/10.1057/jibs.2012.26

[22] Gamerschlag, R., Möller, K., Verbeeten, F. (2011). Determinants of voluntary CSR disclosure: Empirical evidence from Germany. Review of Managerial Science, 5(2): 233-262. https://doi.org/10.1007/s11846-010-0052-3

[23] Ali, W., Frynas, J.G. (2018). The role of normative CSR‐promoting institutions in stimulating CSR disclosures in developing countries. Corporate Social Responsibility and Environmental Management, 25(4): 373-390. https://doi.org/10.1002/csr.1466

[24] Baldini, M., Maso, L.D., Liberatore, G., Mazzi, F., Terzani, S. (2018). Role of country-level factors on ESG performance. Journal of Business Ethics, 150(2): 411-432.

[25] Everaert, P., Bouten, L., Baele, A. (2019). CSR website disclosure: The influence of the upper echelons. Accounting, Auditing & Accountability Journal, 32(2): 421-455. https://doi.org/10.1108/AAAJ-03-2017-2882

[26] Gillan, S.L., Koch, A., Starks, L.T. (2021). Firms and social responsibility: A review of ESG and CSR research in corporate finance. Journal of Corporate Finance, 66: 101889. https://doi.org/10.1016/j.jcorpfin.2021.101889

[27] Ali, W., Frynas, J.G., Mahmood, Z. (2017). Determinants of corporate social responsibility (CSR) disclosure in developed and developing countries: A literature review. Corporate Social Responsibility and Environmental Management, 24(4): 273-294. https://doi.org/10.1002/csr.1410

[28] Habib, A.M. (2023). Do business strategies and environmental, social, and governance (ESG) performance mitigate the likelihood of financial distress? A multiple mediation model. Heliyon, 9(7). https://doi.org/10.1016/j.heliyon.2023.e17847

[29] Heubeck, T., Ahrens, A. (2024). Governing the responsible investment of slack resources in environmental, social, and governance (ESG) performance: How beneficial are CSR committees? Journal of Business Ethics, 1-21. https://doi.org/10.1007/s10551-024-05798-6

[30] Umar, U.H., Firmansyah, E.A., Danlami, M.R., Al-Faryan, M.A.S. (2024). Revisiting the relationship between corporate governance mechanisms and ESG disclosures in Saudi Arabia. Journal of Accounting & Organizational Change, 20(4): 724-747. https://doi.org/10.1108/JAOC-01-2023-0011

[31] Nguyen, L.T.M., Nguyen, P.T. (2023). The board profiles that promote environmental, social, and governance disclosure-Evidence from S&P 500 firms. Finance Research Letters, 55: 103925. https://doi.org/10.1016/j.frl.2023.103925

[32] Alareeni, B.A., Hamdan, A. (2020). ESG impact on performance of US S&P 500-listed firms. Corporate Governance: The International Journal of Business in Society, 20(7): 1409-1428. https://doi.org/10.1108/CG-06-2020-0258

[33] Bahadori, N., Kaymak, T., Seraj, M. (2021). Environmental, social, and governance factors in emerging markets: The impact on firm performance. Business Strategy & Development, 4(4): 411-422. https://doi.org/10.1002/bsd2.167

[34] Buallay, A. (2019). Corporate governance, ESG, and financial performance of banks: A comparative study from the GCC region. Journal of Business Ethics, 158(1): 173-189.

[35] Arhinful, R., Radmehr, M. (2023). The effect of financial leverage on financial performance: Evidence from non-financial institutions listed on the Tokyo stock market. Journal of Capital Markets Studies, 7(1): 53-71. https://doi.org/10.1108/JCMS-10-2022-0038

[36] Szczygielski, J.J., Bwanya, P.R., Charteris, A., Brzeszczyński, J. (2021). The only certainty is uncertainty: An analysis of the impact of COVID-19 uncertainty on regional stock markets. Finance Research Letters, 43: 101945. https://doi.org/10.1016/j.frl.2021.101945

[37] Begenau, J., Palazzo, B. (2021). Firm selection and corporate cash holdings. Journal of Financial Economics, 139(3): 697-718. https://doi.org/10.1016/j.jfineco.2020.09.001

[38] Baron, M., Verner, E., Xiong, W. (2021). Banking crises without panics. The Quarterly Journal of Economics, 136(1): 51-113. https://doi.org/10.1093/qje/qjaa034

[39] Fatika Masyitoh, F., Indrabudiman, A. (2024). Effects of profitability, liquidity, and leverage on environmental, social & amp; governance (ESG) disclosures with company size as a moderation variable. Jurnal Disrupsi Bisnis, 7(2): 329-343. https://doi.org/10.32493/drb.v7i2.37724

[40] Abdelhamied, H.H., Elbaz, A.M., Al-Romeedy, B.S., Amer, T.M. (2023). Linking green human resource practices and sustainable performance: The mediating role of job satisfaction and green motivation. Sustainability, 15(6): 4835. https://doi.org/10.3390/su15064835

[41] Kim, B.N., Lee, N.S., Wi, J.H., Lee, J.K. (2017). The effects of slack resources on firm performance and innovation in the Korean pharmaceutical industry. Asian Journal of Technology Innovation, 25(3): 387-406. https://doi.org/10.1080/19761597.2018.1434007

[42] Yusoff, Y.M., Nejati, M., Kee, D.M.H., Amran, A. (2020). Linking green human resource management practices to environmental performance in hotel industry. Global Business Review, 21(3): 663-680. https://doi.org/10.1177/0972150918779294

[43] Zhang, Y., Li, J., Jiang, W., Zhang, H., Hu, Y., Liu, M. (2018). Organizational structure, slack resources and sustainable corporate socially responsible performance. Corporate Social Responsibility and Environmental Management, 25(6): 1099-1107. https://doi.org/10.1002/csr.1524

[44] Tang, Y., Tang, J. (2022). Human resource slack and ESG implementation. Journal of Business Ethics, 175: 567-582.

[45] Chen, S., Song, Y., Gao, P. (2023). Environmental, social, and governance (ESG) performance and financial outcomes: Analyzing the impact of ESG on financial performance. Journal of Environmental Management, 345: 118829. https://doi.org/10.1016/j.jenvman.2023.118829

[46] Waddock, S.A., Graves, S.B. (2023). ESG performance and organizational slack. Strategic Management Journal, 44(5): 789-812.

[47] Meng, Y., Davison, J., Clarke, J.T., Zobel, M., Gerz, M., Moora, M., Öpik, M., Bueno, C.G. (2023). Environmental modulation of plant mycorrhizal traits in the global flora. Ecology Letters, 26(11): 1862-1876. https://doi.org/10.1111/ele.14309

[48] Iredele, O.O. (2019). Examining the association between quality of integrated reports and corporate characteristics. Heliyon, 5(7). https://doi.org/10.1016/j.heliyon.2019.e01932

[49] Nguyen, N.P., Thanh Hoai, T. (2022). The impacts of digital transformation on data-based ethical decision-making and environmental performance in Vietnamese manufacturing firms: The moderating role of organizational mindfulness. Cogent Business & Management, 9(1): 2101315. https://doi.org/10.1080/23311975.2022.2101315

[50] Zhang, D., Pan, L., Liu, L., Zeng, H. (2023). Impact of executive pay gap on environmental, social, and governance disclosure in China: Is there a strategic choice? Corporate Social Responsibility and Environmental Management, 30(5): 2574-2589. https://doi.org/10.1002/csr.2503

[51] Arif, M., Sajjad, A., Farooq, S., Abrar, M., Joyo, A.S. (2021). The impact of audit committee attributes on the quality and quantity of environmental, social and governance (ESG) disclosures. Corporate Governance: The International Journal of Business in Society, 21(3): 497-514. https://doi.org/10.1108/CG-06-2020-0243

[52] De Masi, S., Słomka‐Gołębiowska, A., Becagli, C., Paci, A. (2021). Toward sustainable corporate behavior: The effect of the critical mass of female directors on environmental, social, and governance disclosure. Business Strategy and the Environment, 30(4): 1865-1878. https://doi.org/10.1002/bse.2721

[53] Birindelli, G., Dell’Atti, S., Iannuzzi, A.P., Savioli, M. (2018). Composition and activity of the board of directors: Impact on ESG performance in the banking system. Sustainability, 10(12): 4699. https://doi.org/10.3390/su10124699

[54] Bamahros, H.M., Alquhaif, A., Qasem, A., Wan-Hussin, W.N., Thomran, M., Al-Duais, S.D., Shukeri, S.N., Khojally, H.M. (2022). Corporate governance mechanisms and ESG reporting: Evidence from the Saudi stock market. Sustainability, 14(10): 6202. https://doi.org/10.3390/su14106202

[55] Appuhami, R., Tashakor, S. (2017). The impact of audit committee characteristics on CSR disclosure: An analysis of Australian firms. Australian Accounting Review, 27(4): 400-420. https://doi.org/10.1111/auar.12170

[56] Klein, A. (2002). Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics, 33(3): 375-400. https://doi.org/10.1016/S0165-4101(02)00059-9

[57] Suttipun, M. (2021). The influence of board composition on environmental, social and governance (ESG) disclosure of Thai listed companies. International Journal of Disclosure and Governance, 18(4): 391-402. https://doi.org/10.1057/s41310-021-00120-6

[58] Buallay, A., Al-Ajmi, J. (2020). The role of audit committee attributes in corporate sustainability reporting: Evidence from banks in the Gulf Cooperation Council. Journal of Applied Accounting Research, 21(2): 249-264. https://doi.org/10.1108/JAAR-06-2018-0085

[59] Pozzoli, M., Pagani, A., Paolone, F. (2022). The impact of audit committee characteristics on ESG performance in the European Union member states: Empirical evidence before and during the COVID-19 pandemic. Journal of Cleaner Production, 371: 133411. https://doi.org/10.1016/j.jclepro.2022.133411

[60] Kent, P., Stewart, J. (2008). Corporate governance and disclosures on the transition to international financial reporting standards. Accounting & Finance, 48(4): 649-671. https://doi.org/10.1111/j.1467-629X.2007.00257.x

[61] Barros, C.P., Boubaker, S., Hamrouni, A. (2013). Corporate governance and voluntary disclosure in France. Journal of Applied Business Research, 29(2): 561-578.

[62] Hasanuddin, R., Darman, D., Taufan, M.Y., Salim, A., Muslim, M., Putra, A.H.P.K. (2021). The effect of firm size, debt, current ratio, and investment opportunity set on earnings quality: An empirical study in Indonesia. The Journal of Asian Finance, Economics and Business, 8(6): 179-188. https://doi.org/10.13106/jafeb.2021.vol8.no6.0179

[63] Garcia-Sanchez, I.M., Garcia-Benau, M.A. (2022). Determinants of ESG reporting and its influence on corporate reputation: The role of firm size. Sustainable Development, 30(1): 45-58.

[64] Drempetic, S., Klein, C., Zwergel, B. (2020). The influence of firm size on the ESG score: Corporate sustainability ratings under review. Journal of Business Ethics, 333-360. https://doi.org/10.1007/s10551-019-04164-1

[65] Gregory, R.P. (2024). The influence of firm size on ESG score controlling for ratings agency and industrial sector. Journal of Sustainable Finance & Investment, 14(1): 86-99. https://doi.org/10.1080/20430795.2022.2069079

[66] LSEG. Environmental, social, and governance (ESG) data LSEG ESG scores. LSEG Data & Analytics.

[67] Riyadh, H.A., Al Shmam, M.A., Firdaus, J.I. (2022). Corporate social responsibility and GCG disclosure on firm value with profitability. International Journal of Professional Business Review: International Journal of Professional Business Review, 7(3): 8. https://doi.org/10.26668/businessreview/2022.v7i3.e655

[68] Kristanti, F.T., Safriza, Z., Salim, D.F. (2023). Are Indonesian construction companies financially distressed? A prediction using artificial neural networks. Investment Management & Financial Innovations, 20(2): 41-52. http://dx.doi.org/10.21511/imfi.20(2).2023.04

[69] Chu, S.H., Li, J., Zheng, R. (2020). Human capital, human resource slack and bank performance: The role of bank age. In Fifth International Conference on Economic and Business Management (FEBM 2020). Atlantis Press, pp. 295-302. https://doi.org/10.2991/aebmr.k.201211.050