Herlina Lusmeida![]() | Magda Siahaan*

| Magda Siahaan*![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

To achieve the Sustainable Development Goals (SDGs), innovation is needed in the financial sector. Sustainable financial concepts that can overcome investment risks and pay attention to environmental, social, and economic dimensions are needed because conventional financing is inadequate. The overarching goal of this study is to examine how enterprise risk management, green intellectual capital (GIC), and shareholder rights (SHR) contribute to sustainable finance. This study uses 260 secondary data points from 65 financial services companies on the Indonesia Stock Exchange from 2018 to 2021. The ordinary least squares approach is employed in this research's multiple regression analysis, with sensitivity analysis conducted using prior sustainable finance metrics from the Indonesian Financial Services Authority Regulation. This study's findings demonstrate how sustainable finance affects enterprise risk management, GIC, SHR, and other critical areas, all of which add to the knowledge in management accounting. Enterprise risk management (ERM) and GIC positively impact sustainable finance, but SHR do not. This study contributes to sustainable finance literature by expanding the sustainable finance index measurement to include IT and stakeholders. The novelty of this research is measuring sustainable finance by modifying Regulation of Financial Services Authority No. 51 for the year 2017, namely by first creating an index based on the Regulation of Financial Services Authority, then adding the information technology dimension and stakeholder support dimension along with indicators, which are not yet contained in the regulation, so that by adding new dimensions and indicators it can make measurements better and more complete when compared to the previous one.

enterprise risk management (ERM), green intellectual capital (GIC), shareholder rights (SHR), sustainable finance

A considerable increase in development costs is needed to achieve the Sustainable Development Goals (SDGs), which require the construction of various innovations in the financial sector. The role of the financial sector is very important in increasing SDG funding and bridging the amount and risks arising from investments made to attract institutional investors [1]. Due to its failure to take into account the SDGs' three-dimensional viewpoint, conventional development financing is ill-suited to fund them. Unresolved social and environmental issues stemming from development are affected by a disregard for these three aspects. There are three reasons why sustainable finance is better suited to be used in the context of SDG achievement [2-4]: (1) integrating non-financial ESG factors into financial institutions' risk assessments [5]; (2) creating a roadmap for sustainable finance and improving regional cooperation; and (3) creating a typology for sustainable assets and financing. Financial decision-making that takes ESG (environmental, social, and governance) considerations into account is known as sustainability finance [6, 7]. The goal of sustainable finance is to incorporate long-term economic, social, and environmental risk concerns into credit management, financing, and investment. This approach applies across the board in the financial services business. The relevant financial services industry now includes the policy in its portfolio. There have been mandates in the financial sector to address sustainable finance [8].

Some nations' central banks have sustainable finance policies, including those of Brazil, Bangladesh, China, and India. Meanwhile, in Japan, the Netherlands, and Germany, it has been deliberately implemented with the help of the local government through a variety of policy tools, including investment, credit/financing, and fiscal policy support. Sustainable finance policy methods in various nations have diverse foundations; the presence of such legislation will level the playing field in the financial services industry's business practices [9]. PT. Bank OCBC is one of the banks in Indonesia. The presidential director revealed that Indonesia is in dire need of Sustainable Financing because most of the people of Indonesia depend on nature for their livelihoods, such as agriculture, fisheries, tourism, and livestock. On the other hand, the threat of disasters and natural damage continues to haunt us, so there must be efforts to preserve and maintain the environment. For this reason, Bank OCBC focuses on sustainable finance. Since 2018, Bank OCBC has done much green financing. As of December 2021, Bank OCBC NISP has disbursed sustainable financing of Rp. 30.89 trillion, and of this amount, 40% is used for green financing and is expected to continue to increase, and the rest is for inclusive financing. Indonesia is a developing country, so besides environmental factors, there are important social factors.

One of the main challenges to developing sustainable finance in Indonesia is overcoming short-term credit in Indonesia's financial market. The practice of banks in Indonesia to extend most short-term loans, which are usually extended with renegotiated interest rates, makes it difficult to finance any sustainable long-term investment. A longer investment horizon will likely increase awareness of ESG Environmental, Social, and Governance risk factors [10]. In its role as Indonesia's financial sector regulator, the Financial Services Authority (OJK) consistently backs low-carbon initiatives through sustainable finance. That is why sustainable finance plans have been made mandatory for banks to expand their loan portfolio. The Sustainable Finance Action Plans regulation is detailed in Financial Services Authority Regulation No. 51 for the year 2017. Financial services companies, as a subset of the financial industry, have considerable potential for impact. By rethinking its business model and product offerings and working with clients to achieve sustainable transitions, the financial sector may make a positive impact on sustainable development. Banks generate profits and benefits for their owners by supporting sustainable development [11].

The latest in this study is the modification of sustainable finance measurements. The measurement of sustainable finance before modification does not include the dimension of information technology and the dimension of stakeholders, so the measurement of sustainable finance before modification only consists of five dimensions, namely the economic dimension, the social dimension, the environmental dimension, the product and service dimension, and the dimension of the sustainability code of ethics. Only using these five dimensions to measure sustainable finance does not meet the needs of the era of technology competition 4.0. Following what was conveyed by Bankeler [12] and Williamson [13], technology expands space for society, facilitates transactions, and makes transactions efficient. Stakeholder theory proposes that collaborative efforts in relationships ideally benefit the focus of the business and all its stakeholders [14]. It fits the idea of a multi-directional value stream and supports an in-depth analysis of stakeholder relationships, creating what, with whom, and for whom. The view that different stakeholders are particularly prevalent in the sustainability-oriented business model literature [15-17].

There has been much interest in enterprise risk management (ERM) recently, both domestically and outside [18]. The increasing scrutiny of businesses has brought with it a host of problems related to risk management, such as international financial crises and corporate fraud [19]. Businesses cannot be adequately risk-prepared without integrated risk management. The identification, measurement, and management of risks—including sustainability-related risks—is an essential part of ERM's contribution to the company's sustainable development. According to Hanggraeni [20], this not only boosts efficiency and economic growth but also raises investor trust, which in turn ensures business sustainability. Effective risk management can be a competitive strategy to survive the instability that normally defines the banking sector, according to research conducted by Oyewo [21], which argues that ERM increases long-term performance. At the same time, studies done by Narumon [22] showed that ERM does not handle sustainability issues. Hence, he proposed creating an ERM framework specifically for those risks. From worldwide financial crises to corporate fraud [23, 24], there have been various obstacles linked to the increasing focus on risk management practices by corporations.

Currently, the business world focuses more on intangible assets than tangible assets to obtain better performance, and with the belief that intangible assets can support the company's survival, encourage value creation, and increase competitive advantage. These intangible assets refer to intellectual Capital, often called Intellectual Capital. Intellectual Capital positively impacts the company's financial performance and sustainable growth. Based on this, as we know, company performance and sustainable growth are positively related to physical Capital, Human Capital (HC), and relational Capital (RC). Intangible assets refer to intellectual Capital, often called Intellectual Capital. A company with higher intellectual Capital will benefit more when compared to a company that has less intellectual Capital. When it comes to environmental consciousness and responsibility, businesses need to be able to help solve issues that stem from poor management of intellectual Capital. Now that many businesses understand the need to be environmentally conscious in all aspects of their operations, a new green concept has evolved that can be used to improve intellectual capital management and help businesses incorporate green intellectual capital (GIC) into their strategies [25]. Furthermore, according to studies done by Yusoff et al. [26], a company's sustainability is positively correlated with both structural and relational capital, which make up GIC. This new knowledge reveals that GIC management and development give a competitive advantage, which improves the success of businesses, including sustainability-focused businesses. The balanced combination of GIC components hints at the future of performance and the possibility of creating high value. Therefore, GIC enhances organizational performance and sustainability by utilizing its unique resources and competencies, all within the context of RBV.

Shareholders have rights in the company. Shareholder rights (SHR) play an important role in sustainable finance and directly impact the company's decision-making process and the achievement of the company's sustainability goals [27]. Some important points that highlight the impact of SHR on sustainable finance include proxy voting. Namely, shareholders have the right to vote on various issues of the company [28]. Shareholder activism, namely shareholders, can engage in activism by advocating sustainable practices in the company. Through shareholder activism, investors can encourage companies to implement sustainable strategies, disclose environmental and social risks, and improve their overall sustainability performance [29, 30]. Additionally, shareholders have the right to disclosure and reporting, i.e., the right to access company information and financial statements. In recent years, there has been a growing demand for increased transparency and disclosure of sustainability-related information. Shareholders can use this information to assess the company's environmental and social impacts, evaluate risks and opportunities, and make informed investment decisions. Strong SHR encourage the availability of reliable sustainability data, allowing investors to assess a company's sustainability performance effectively [29].

SHR include the creation of long-term value by exercising their rights, shareholders can encourage companies to adopt sustainable business models, set meaningful environmental and social targets, and align their strategies with sustainable finance principles [27]. ESG integration, i.e., the rights of shareholders, facilitates integrating ESG factors into investment decisions. The last is the composition of the board and accountability, i.e., SHR, which includes the election of board members, which plays an important role in setting the company's strategic direction. Shareholders can influence the board's composition by selecting candidates with relevant sustainability expertise and advocating for a diverse and inclusive board. Boards that reflect shareholder interests and values, including sustainability considerations, are more likely to prioritize and encourage sustainable finance initiatives [31]. Due to the strong SHR, investors are empowered to shape corporate behavior, promote sustainable practices, and encourage the integration of environmental, social, and governance factors into investment decisions. Shareholders can encourage companies to adopt sustainable strategies, increase transparency, and contribute to broader sustainable finance goals if shareholders exercise their rights [27, 30].

This study intends to examine the impact of risk management, GIC, and SHR on sustainable finance in Indonesian financial services organizations. It does so in light of the necessity of adopting sustainable finance and the fact that prior research has shown mixed outcomes. This research tests the significance of sustainable finance measurements with the availability of two dimensions for modified sustainable finance.

2.1 Theoretical framework

In their 1975 publication, Dowling and Pfeffer lay forth the theory of legitimacy. An origin of the English word "legitimacy" in Latin, "legitimus" signifies "according to the law” [32]. The relevant legislation emphasizes social rules that govern moral and ethical conduct rather than merely laws to be enforced by a legal system. Legitimacy is the bedrock principle that establishes control and dominion over other entities. It stands for the Financial Services Authority (OJK), which is responsible for overseeing Indonesian financial institutions and issuing regulations such as the Financial Services Authority Regulations. The middle theory for independent variable in this research is the stakeholder theory [14], which is the middle theory of ERM and SHR. According to this theory, financial services companies have a responsibility to their stakeholders to ensure the company's survival through sustainable corporate finance practices, which include reducing and mitigating risks and keeping stakeholders informed about these risks. A business can compete because it is a combination of resources and skills. That is explained by the Resource Based View theory, which was put forth by Penrose and Pitelis [33] and Warnerfelt [34], and is sometimes referred to as RBV [14].

2.1.1 Sustainable finance

According to OJK [35], sustainable Finance in Indonesia is comprehensive support from industry for sustainable growth resulting from harmony between economic, social, and environmental interests. In order to support the achievement of the Long Term Development Plan and Medium Term Development Plan (RPJMn), the Financial Services Authority on 5 December 2014 published the 2015-2019 Sustainable Finance Roadmap. The roadmap contains an explanation of the sustainable finance program work plan for the financial services industry under the authority of the Financial Services Authority, namely banking, capital markets, and the non-bank financial industry (IKNB). The term "sustainable finance" refers to a way of doing business in the financial services industry that prioritizes long-term growth while also taking environmental, social, and ethical considerations into account [36]. By combining ESG (environmental, social, and governance) factors, Sustainable Finance provides a robust financial framework to back the worldwide SDG. Rising worries about climate change and human-caused damage, which, if left unchecked, might cause significant harm to the environment, have led to the rise of sustainable finance as a viable option. Then, realizing that natural capital is the primary engine of economic development, business actors—particularly investors—became conscious of the importance of environmental protection to the sustainability of their companies.

However, many investors tend only to seek profit while ignoring the condition and sustainability of the environment, which they use as a medium to keep their business on track. To overcome the problem, international institutions such as the United Nations and the IFC (International Finance Corporation) encourage many countries to introduce and better implement the concept of sustainable finance in their respective countries [37].

According to COSO, the ERM framework is defined as integrated risk management, integrated with aggregate and holistic strategy and performance, taking a portfolio or coordinated approach to risk and recognizing that many risks are correlated. Banks and financial institutions are at the forefront of managing risk aggregately. It is useful to consider the advancement of ERM frameworks [38]. ERM requires a continuous process to identify, analyze, evaluate, and address loss exposures, as well as monitor risk controls and financial resources to mitigate the adverse impact of financial operational losses. ERM is established to meet the needs of stakeholders who want to understand the broad spectrum of risks facing complex organizations to ensure they are robustly managed. By proactively addressing and identifying risks and opportunities, financial institutions project and create stakeholder value, while not neglecting customers, employees, owners, and society as a whole [39].

GIC is an intangible asset that incorporates environmental concepts into intellectual capital to compensate for previous deficiencies in addressing environmental issues, thereby creating a sustainable competitive advantage for an organization through its pool of resources [40, 41]. Furthermore, Yusliza et al. [42] revealed that GIC has a positive relationship with environmental, economic, and social performance. Three primary sources often used as proxies to measure GIC are green human capital, green structural capital, and green relational capital [25, 26 42, 43].

Good corporate governance is the fundamental foundation for a company to achieve its goals.

Sari et al. [44] stated that corporate governance is a set of relationships or systems between parties with an interest in a company or organization, with the aim of providing control and direction to the company or organization to achieve its goals. The corporate governance structure aims to distribute the rights and responsibilities of each role within the company, such as shareholders, board members, managers, employees, and other stakeholders. Rezaee [45] defined corporate governance as the process of aligning the interests of management and shareholders. According to the 2021 PUGKI (Indonesian Corporate Governance Standards), companies protect shareholders, both majority and minority shareholders. SHR are protected not only by financial rights but also by non-financial rights, such as fair treatment, transparency in accessing information, and accountability.

In the disclosure of Good Corporate Governance (GCG), Adu [28] also stated that SHR are measured through twenty-two indices containing requirements or indicators. The aim is to look more deeply and comprehensively at the SHR aspects within a company that have met the standards that have been set based on regulations and theories from previous founders, presenting the aspects that companies need to have today.

2.2 Hypothesis development

2.2.1 The effect of enterprise risk management on sustainable finance

Companies aim for optimal risk management because, according to stakeholder theory, they need to satisfy the demands of stakeholders in order to gain their support. According to Pergler [46], ERM is all about a company's capacity to spot, comprehend, quantify, and lessen the impact of potential dangers. Having solid risk management in place helps businesses weather storms and stay in business for the long haul. Risk management must be an ongoing process that assists businesses in carrying out strategies that contribute to their goal attainment to be effective [39, 47]. Organizational effectiveness, risk reporting, and company performance can all be improved by ERM [48]. The goal of the company's risk management strategy is to find potential threats and lessen their impact. The goal is for the company to be able to continue operating sustainably. The corporation must still think about potential dangers while giving value to its stakeholders. In order to sustainably maintain its finances, the organization must consider how to limit the risk in the event that it occurs in the future.

A strong correlation between risk management has been found in the company's research [47, 49, 50]. Environmental friendliness. This hypothesis's development is a reference to sustainability, which includes sustainable finance. Sustainable financing benefits from ERM. In other words, a company's ability to adopt sustainable finance is directly correlated to the quality of its enterprise risk management. This explanation, together with other studies, leads one to believe that risk management helps sustainable financing.

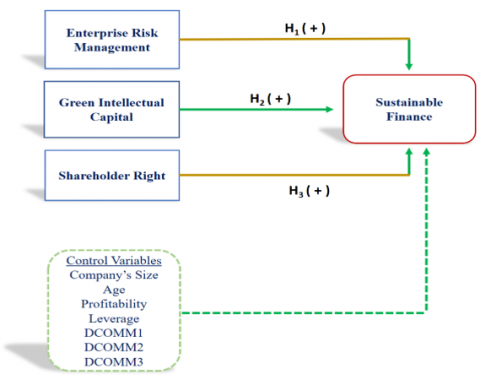

H1: ERM has a significant positive effect on sustainable finance.

2.2.2 The effect of green intellectual capital on sustainable finance

In order to stay ahead of the competition, businesses must make the most of their resources, especially their intellectual capital. The RBV theory reveals this. The concept is in line with intellectual capital, as shown by Alvino et al. [51]. The sustainable development agenda of 2030 has implications for the possibility of developing intellectual capital. The term "green intellectual capital" refers to the creation of environmentally friendly ideas that are a part of managing intellectual capital. Concern for people and the planet will motivate the business to engage in sustainable practices. The organization has considered all aspects pertaining to sustainability. GIC is the intellectual capital owned by companies to excel in competition while still paying attention to the concept of the environment and society. The GIC owned by the company allows the company to continue because it has an advantage in overcoming existing competitors. So, with its advantages, the company can provide products/services that suit customer needs while maintaining a green concept. Sustainable finance is a company concept that financial institutions use to generate profits while paying attention to the environment and society. Developing existing intellectual capital while still paying attention to the green concept, the company, which is the center of various resources, strives to have advantages that can answer customer needs because it can provide added value. The intellectual capital owned by financial services companies is expected to support sustainable finance.

Previous studies have shown that GIC significantly and positively affects the sustainability of businesses [25, 52, 53]. A company's long-term viability is enhanced by GIC. It is believed that GIC contributes to sustainable finance, according to the description given and other research. Thus, the following is the working theory of the two investigations:

H2: GIC has a significant positive effect on sustainable finance.

2.2.3 The effect of shareholders' rights on sustainable finance

Stakeholder theory supports the emergence of accountability and transparency of shareholders, which is expected to increase the role and support of shareholders in the implementation of sustainable finance to minimize various problems that can hinder transparency and reduce information asymmetry [54]. Agency problems often arise in companies due to information asymmetry, encouraging principals to find solutions to reduce company tension by building corporate governance with sustainable development to maintain sustainable finance [37]. Governance mechanisms positively impact sustainable decisions, such as those captured by environmental disclosures and sustainable banking initiatives. Performance sensitivity for sustainability depends on the quality of corporate governance [28]. SHR plays an important role in sustainable finance and directly impacts the company's decision-making process and its achievement of sustainability goals.

Shareholders use corporate social responsibility reports to monitor the company's level of accountability [31]. Research conducted by Michelon and Rodrigue [29] reveals that shareholders need disclosure regarding sustainability because it requires the necessary company transparency for decision-making and for providing value for shareholders. Gómez-Bezares et al. [27] stated that sustainability issues are necessary for business activities because it will be better to utilize the company's resources for better financial performance, so that it can provide value to shareholders.

H3: SHR have a significant positive effect on sustainable finance.

According to previous theories and research, this study can be analyzed from the existing weaknesses as a basis for developing this research so that the results of this study provide useful implications. Some weaknesses of previous research that will be examined in this study are as follows:

(1) There are not many previous studies that empirically test the effect of ERM on Sustainable Finance. Even though there is, the research tends to look at the effect of ERM on sustainability or financial performance. This study will specifically test the effect of ERM on sustainable finance using a modified index measurement.

(2) Most of the research related to GIC is related to financial performance or sustainability, which means that there is still very little research that analyzes the relationship between GIC and sustainable finance. The research conducted by Lusmeida and Augustine [47] uses intellectual capital only as a moderator; considering that GIC is one of the important factors expected to support the success of implementing sustainable finance, this study considers it necessary to prove the effect of GIC on sustainable finance empirically.

(3) Research related to SHR is usually associated with the company's financial performance or sustainability; in fact, there is very little research that analyzes the influence of SHR on sustainable finance. This study considers it necessary to analyze the role of SHR in the implementation of sustainable finance to overcome this deficiency. Moreover, considering that regulations indeed require financial institutions, banks, and non-bank companies, this study considers SHR as something that must be seen in terms of their influence, whether they have a significant influence or otherwise, on the implementation of sustainable finance.

To implement sustainable finance, as stipulated in Financial Services Authority Regulation No. 51/POJK.03/2017 issued by the Financial Services Authority of Indonesia (OJK), financial services companies require stakeholder support, and this support must be sought [14]. Stakeholder support will emerge if company management prioritizes the company's continuity and sustainability. Enterprise risk management is a corporate responsibility; attention to risk management will support the company's sustainability. Therefore, risk management will positively impact a company's sustainable finance. To survive, companies must be competitive. To achieve this, companies must possess a competitive advantage, one of which is GIC. GIC consists of three elements: green human capital, green relational capital, and green structural capital. Based on previous research, intellectual capital is distinguished from the intangible assets of an organization that will support a company's pursuit of sustainable finance. GIC has a positive impact on sustainable finance. One of the purposes of establishing a company is to meet the needs of its stakeholders. Therefore, to meet these needs, a company must be able to manage its business effectively. By implementing good management, the company increases oversight of the board and management to avoid information asymmetry. Shareholders, as stakeholders, have an interest in knowing information about the company. The information they receive should be consistent with the information received by management, so that shareholders feel comfortable knowing their needs for company information are met. This explanation clarifies that SHR have a positive impact on sustainable finance.

Table A1 shows the differences between this research and the results of previous research, which constitute gap research.

Based on theories, previous studies, and concept description, a conceptual framework has been formed for this research, as shown in Figure 1.

Figure 1. Conceptual model of the study

2.2.4 Financial service authority and its regulation

OJK is one of the regulatory institutions that has the authority to supervise financial institutions in Indonesia. With sustainable finance, OJK, as a regulator of financial institutions in Indonesia, always supports the low-carbon spirit. That is why regulations have been issued so that financial institutions can increase their credit portfolios through sustainable finance schemes. The Sustainable Finance Action Plan and the Issuance and Requirements of Environmentally Friendly Debt Securities are detailed in OJK Regulation (POJK) number 51 of 2017 and POJK number 60 of 2017 respectively. They are part of the sustainable finance rules. To launch a loan distribution project based on sustainable finance principles, OJK chose eight banks in early 2019. These banks have worked on a number of sustainable finance projects such as renewable energy, efficient energy, sustainable agriculture, green building and infrastructure, the recycling industry, and eco-tourism.

With the issuance of POJK No. 51/POJK.03/2017, a new era for the implementation of sustainable finance has begun. This regulation provides guidelines for financial services institutions, issuers, and public companies. This guideline is designed to provide technical explanations on the practical meaning of sustainable finance principles, sustainable finance program priorities, strategic steps in implementing sustainable finance programs, outline and content of the Sustainable Finance Action Plan (RAKB), outline and content of the Sustainability Report (SR); criteria and categories of sustainable business activities; allocation and use of Social and Environmental Responsibility (TJSL) funds to support Sustainable Finance implementation activities.

This research is quantitative, using secondary data documented by the Indonesia Stock Exchange (IDX) with a research period from 2018-2021. Table 1 describes the sampling method as purposive sampling, and 65 companies were obtained with a total of 260 observations. Using IDX organizations that fall within the financial sector group, those that provide all relevant data in response to research requests, those that became public after 2018, and those with a good DER score were the determinants of inclusion in the sample. 260 observations were derived from 65 firms using those criteria.

Table 1. Sample criteria

|

No. |

Sample Criteria |

Amount |

|

1 |

Companies (emiten) in the Indonesian Stock Exchange (IDX) that are included in the Financial Sector group |

99 |

|

2 |

Companies that IPO after 2018 |

-4 |

|

3. |

The company was not listed in the 2018-2021 period |

-1 |

|

4 |

Companies that do not provide complete information according to research needs |

-26 |

|

5 |

Companies that have DER (-) |

-3 |

|

6 |

Number of company samples |

65 |

|

7 |

Research period from 2018-2021 |

4 |

|

Total Sample: |

260 |

|

3.1 Variable measurements

This research uses dependent, independent, and control variables. The following explains the measurement of each variable used in this research, and the appendix provides a summary of the variables used in this research.

Sustainable finance is the focus of this study's dependent variable. Sustainable finance refers to the financial services industry's all-encompassing backing of long-term development that is environmentally, socially, and economically sound. To measure sustainable Finance using an index based on the Modified Measurement of Sustainable Finance, which is sourced from Financial Services Authority Regulation No. 51 for the year 2017, which has been modified so that there are a total of 38 indicators. This modification was made because it is in accordance with what has been explained in the previous chapter, namely, with the novelty. If based on Financial Services Authority Regulation No. 51 for the year 2017 to measure sustainable Finance before being modified using five dimensions and 28 indicators, then after being modified with the novelty, it becomes seven dimensions and 37 indicators. The sustainable finance index was calculated using the disclosure checklist measurement used by Boateng et al. [55], namely by using a dummy (1 or 0). The checklist used is derived very carefully from the official regulatory regulations in Indonesia, namely Financial Services Authority Regulation No. 51 of 2017. If the company discloses the indicator in question, it is given the number 1; otherwise, if it does not disclose it, it is given the number 0.

The Sustainable Finance (SF) index is calculated using the following formula:

SFij = ƩXij / nj

where,

Sfij = Sustainable Finance index for company j in year i

nj = Number of items for company j, nj ≤ .......

ƩXij = Number of items disclosed by company j for year i

Table A2 shows the variable operational definition. Furthermore, the unmodified Sustainable Finance index consists of 5 dimensions with 28 indicators. In comparison, the modified Sustainable Finance index consists of 7 dimensions (with the addition of information technology and stakeholder dimensions) with 37 indicators. Table A3 explains a list of unmodified and modified sustainable finance.

3.1.1 Enterprise Risk Management (ERM)

Using a portfolio or coordination approach to risk and acknowledging the correlation between several hazards, ERM integrates risk management with aggregate and holistic strategy and performance [38]. Using a model for ERM that was created in 2017, this research calculates ERM. This year, COSO released a more intricate ERM framework due to its integration with strategy and performance. The 2017 ERM framework primarily adds governance, culture, and strategy formulation as its key contributions [38]. In order to assess the efficacy of current business applications, this architecture may be used to build a company index. There are many foundations that support this framework's five main parts: culture and governance; strategy and goal formulation; performance; review and revision; and information, communication, and reporting. By utilizing the disclosure checklist measurement in every company, we can determine if they are following the 2017 framework or not. If they are, we assign a value of 1; otherwise, we assign a value of 0; and finally, we add up all the values and divide by 20, which is based on the total number of bases in this assessment.

3.1.2 Green Intellectual Capital (GIC)

An organization's GIC may help make up for its past mistakes in environmental matters by combining environmental principles into intellectual capital. This gives the organization a leg up in the market thanks to its resource pool [53]. To measure GIC, using the model developed by Chen [53], then Dewi et al. [56] also used the model in their research, so in this study using secondary data, the index number (GIC index) is used to calculate GIC disclosure. Initially [56] used the GIC element using a questionnaire filled out by respondents. However, this study tried to use the element using the disclosure checklist measurement method because they wanted to know whether the results obtained would be the same or different if applied using secondary data and disclosure checklist measurement. The GIC index is an index used to measure the application of GIC in companies that are sampled in this study. The index is then measured using a disclosure checklist, giving an index of 1 (one) for companies that disclose GIC indicators and a value of 0 (zero) if not. The items used to measure the index uses three GIC elements: human capital, structural capital, and relational capital.

3.1.3 Shareholder Right

SHR are rights held by shareholders. Rezaee [45] define corporate governance as the process of aligning the interests of management and shareholders. In searching for SHR, it was also formulated by Adu [28]. SHR is formulated into twenty-two indices containing the requirements or indicators of good corporate governance. The formulation aims to look more deeply and comprehensively at the SHR aspects that already exist in a company that has met the standards that have been set based on regulations and theories from previous initiators, presenting aspects that need to be owned by companies today. The SHR measurement adopted from Adu [28], only applies to shareholders because he wants to focus on finding out the extent of shareholders' influence on the implementation of sustainable finance in financial services companies during the research period.

3.1.4 Control variable

Control variables are variables that are controlled or maintained constant so that external factors do not influence the influence of independent variables on dependent variables. In this study, the control variables used are company size (in total assets), profitability (ROA), company age (Age), leverage (DER), and dummy control variable.

Company size

Company Size is calculated by the logarithm derived from the company's total assets, which is the assumption that the company's total assets tend to be more stable than the amount of sales.

Profitability

To measure the profitability ratio in this study, ROA is used, while to calculate ROA the formula used comes from Weygandt et al. [57].

Company age

The age of the company in the study measure with calculated based on the company's listing on the IDX until the period of this study [58].

Leverage

Leverage is calculated by dividing the company's liabilities (company debt) by the equity it owns.

Dummy

To be able to group the financial services company sub-sectors, a dummy is used as a control variable. This dummy is to facilitate grouping the existing financial services sub-sectors. The use of this dummy is in accordance with what was conveyed by Brown [59] namely regarding the significance of dummy variables in multiple regression related to economic and financial data.

3.2 Data analysis method

The data analysis method in this study uses multiple regression. The study uses sustainable finance as an independent variable, and then uses enterprise risk management, GIC, and SHR as independent variables. Control variables consisting of company size, company age, profitability, leverage and dummy industry based on sub-sectors in financial services companies to complete the model used in this study. So, the data processing is carried out for the model using the equation in empirical testing.

The research model for this study can be seen in Eq. (1). It is as follows:

SFit = α + β1ERM + β2GIC + β3SHR + β4SIZE+β5AGE+β6PROF+β7LEV+ β8DCOMM1 + β9DCOMM2 +β10DCOMM3 + ε (1)

where,

SF = Sustainable Finance

α = Constant

β1-β10 = Regression Coefficient

ERM = Enterprise Risk Management

GIC = Green Intellectual Capital

SHR = Shareholder Right

SIZE = Size of the Company

AGE = Company’s Age

PROF = Return on Assets

LEV = Leverage

DCOMM1 = Dummy Variable Control for Financing Institution Sub-Sector

DCOMM2 = Dummy Variable Control for Insurance Sub-Sector

DCOMM3 = Dummy Variable Control for Banking Sub-Sector.

The research results begin by explaining statistical descriptive results; assumption classics test results, hypothesis test results, and robustness test results.

Table 2 shows descriptive statistics for sustainable finance, with an average value of 22.20% or 0.222. The standard deviation value of 0.1140 (11.40%) indicates a considerable variation in the value of sustainable finance between one company and another in the financial industry. Verena Multi Finance Tbk owned the maximum value of 56.76% in 2020, while AHAP, BPII, CASA, GSMF, LPPS, and SMMA owned the lowest value of 0.27%. For details of the list of sustainable finance items, see Table A2.

ERM disclosure in companies included in the financial group resulted in high achievements and an average score of 83.28%. The standard deviation value of 0.104 shows that the overall ERM disclosure achievement between one company and another is not too heterogeneous or too varied. The maximum value of 100% was obtained by several companies, namely BBRI, BDMN, BMRI, BNII, BNLI, and BCIC, while LPS and BPII owned the lowest value of 40%. The achievement of GIC disclosure in financial companies is still low, as shown by an average score of 6.55%. A large standard deviation from the average of 10.38% indicates considerable variation in data between one company and another for GIC disclosure. The highest achievement of 33.3% was achieved by several companies, namely BBCA, ABDA, ADMF, and SMMA. At the same time, the lowest score of 0 was owned by many companies, which shows that the implementation of GIC is still relatively low in the financial industry.

Table 2. Statistic descriptive

|

Variable |

N |

Minimum |

Maximum |

Mean |

Standard Deviation |

|

SF |

260 |

0.0270 |

0.5676 |

0.2242 |

0.1143 |

|

ERM |

260 |

0.4000 |

10.000 |

0.8353 |

0.1038 |

|

GIC |

260 |

0.0000 |

0.3330 |

0.0655 |

0.1038 |

|

SHR |

260 |

0.0450 |

0.9090 |

0.5389 |

0.1940 |

|

AGE |

260 |

0.0000 |

38.000 |

16.737 |

93.814 |

|

SIZE |

260 |

96.190 |

17.278 |

13.662 |

14.617 |

|

LEV |

260 |

0.0070 |

16.195 |

41.521 |

32.623 |

|

PROF |

260 |

-0.7310 |

0.6810 |

0.0254 |

0.1157 |

The company size shows an average company size value of 13.662 years. The standard deviation value of 1.461 indicates a fairly heterogeneous company size variation between companies. Bank Central Asia owns the highest company size of 17.280 while the lowest company size is 9.619 Bank Maspion. Descriptive statistics for the ROA variable show an average value of 0.25%, which means that overall, during the 2019-2021 period, companies in the financial group experienced an average profit of 0.25%. A standard deviation value greater than the average of 0.115 indicates a heterogeneous ROA variation between companies. DEFI owns the highest ROA of 68.10%, and the lowest ROA value of -PT Magna Investama Mandiri Tbk is 73.10%. Descriptive statistical calculations for DER show an average DER value of 4.152. A standard deviation value of 3.263 indicates a small variation in DER data between one company and another in the financial industry group. BBTN owns the maximum DER value of 16.195, while ARTO owns the minimum DER value of 0.007.

Coefficient determination test

To find out how much an independent variable can explain a dependent variable in a model, one uses the coefficient of determination test. This involves looking at the adjusted R2 value. Table 3 displays the findings of the research's coefficient of determination tests.

Table 3. Test result of the coefficient determination R2

|

Indicators |

Probability |

|

Adjusted R2 |

0.417199 |

|

R2 |

0.441951 |

The adjusted R2 value of 0.417199, or 41.72%, obtained from the coefficient of determination test indicates that the independent variables (ERM disclosure, GIC, SHR), control variables (AGE, SIZE, profitability, leverage, and DCOMM1–DCOMM3), and the dependent variable (Sustainable Finance) can explain 41.72% of the variation in Sustainable Finance. The remaining 58.28% is attributable to the variation in other independent variables that impact Sustainable Finance but are not part of the model. These outcomes demonstrate that the research model produces a good model fit.

F-test

The F-test is carried out to determine whether at least one independent variable has a significant effect on the dependent variable. The processing results for the F-test are shown in Table 4.

Table 4. Test result of the F-test

|

Indicators |

Probability |

|

F-Statistic |

1.785506 |

|

Prob (F-statistic) |

0.000000 |

This suggests that for the sustainable finance model, at least one independent variable has a significant influence on the dependent variable, as the F-test results generated a statistical F value of 17.85506 with a p-value of 0.000 < 0.05. According to these findings, the model is either viable or fits the data.

T-test

Table 5 shows the results of the following equation:

SFit= -0.378138+ 0.233161ERM+0.255465GIC - 0.021151SHR + 0.019183SIZE-0.000232AGE+0.047773PROF--0.003100LEV+0.120832DCOMM1+0.055599 DCOMM2+0.086924DCOMM3+ε (2)

According to the T-test for hypothesis 1, which states that raising ERM would improve sustainable finance and decreasing ERM will reduce sustainable finance, the estimated coefficient value is 0.233161. The statistical t-value of 3.430905 yields a p-value of 0.00035 <0.05, proving that ERM positively impacts sustainable financing. Just as expected, the findings demonstrate that ERM has a positive impact on sustainable financing. An estimated coefficient value of 0.255465 was obtained using the T-test for hypothesis 2, which suggests that Sustainable Finance will grow with an increase in GIC and that Sustainable Finance will decrease with a decrease in GIC. With a p-value of 0.00025 < 0.001 and a statistical t-value of 3.548872, the hypothesis that GIC positively impacts sustainable finance is confirmed. An estimated coefficient value of -0.021151 was obtained from the T-test for hypothesis 3, which suggests that sustainable finance will decrease with an increase in SHR and increase with a decrease in SHR. We cannot conclude that SHR negatively impacts sustainable finance based on the statistical t-value of -0.405226, which yields a p-value of 0.34285 > 0.1.

Table 5. The test result of T-test and robustness test

|

Variable |

Predictions |

SF Models with Modifications |

SF Model without Modification |

||||

|

Coefficient |

T Statistics |

P-Value |

Coefficient |

T Statistics |

P-Value |

||

|

C |

-0.378138 |

-5.154.595 |

0.0000 |

-0.486922 |

-5.216.481 |

0.0000 |

|

|

ERM |

+ |

0.233161 |

3.430.905 |

0.00035*** |

0.328907 |

3.803.645 |

0.0001*** |

|

GIC |

+ |

0.255465 |

3.548.872 |

0.00025*** |

0.317264 |

3.463.806 |

0.0003*** |

|

SHR |

+ |

-0.021151 |

-0.405226 |

0.34285 |

-0.049994 |

-0.752769 |

0.22615 |

|

SIZE |

0.019183 |

4.882.797 |

0.0000*** |

0.023782 |

475.753 |

0.0000*** |

|

|

PROF |

0.047773 |

0.935588 |

0.1752 |

0.062525 |

0.962334 |

0.1684 |

|

|

AGE |

-0.000232 |

-0.379329 |

0.3524 |

-0.000369 |

-0.475442 |

0.31745 |

|

|

LEV |

-0.003100 |

-1.434.660 |

0.0763* |

-0.003933 |

-1.430.303 |

0.07695 |

|

4.1 Further analysis

The results of robustness test

The sensitivity test results can be seen for the sustainable finance model with better modifications when compared to the main sustainable finance model (without modification). The results of the sensitivity test of this study show that the new measurement for sustainable finance provides a better picture of the research because the adj-R2 value in the sustainable finance measurement of the Financial Services Authority Regulation model has been modified with an adj-R2 value of 0.417199 while the adj-R2 value before modification is only 0.397695. The measurement of sustainable finance with the addition of information technology and stakeholder dimensions is higher than the measurement of sustainable finance based on Regulation of Financial Services Authorities No. 51/POJK.03/2017 before it was modified. It can be seen from the value of the variable coefficient that it is larger with a smaller probability, which means that the influence of independent and control variables on the dependent variable is greater than the measurement before modification. Other results show that with the addition of information technology and stakeholder dimensions in sustainable finance, on average, it shows better measurement results when compared to the old measurement, which can be seen from a better coefficient value and a more significant significance value if using the new measurement.

5.1 Discussion

Stakeholders in complex organizations want to know what risks are out there and how to manage them, and ERM is going to help with that. Financial institutions generate value for their stakeholders—customers, staff, owners, and society at large—by anticipating and responding to risks and opportunities for the sake of long-term viability. Previous research [39, 47, 49, 50] are likewise consistent with the findings of this study. Eventually, sustainable finance will feel the good consequences of ERM. Theoretically, financial services providers have a responsibility to inform their stakeholders of potential risks to the company and work to reduce or eliminate them. That includes meeting their needs in terms of the company's ability to stay in business and maintain a healthy financial position. Essentially, when firm management prioritizes the survival and financial health of the organization, support from stakeholders will follow. The ERM disclosures from the sample companies indicate that sustainable finance is on the rise, which bodes well for the financial services industry's sustainable financing efforts. Due to the abundance of laws and regulations, both internal and issued by regulators, financial services organizations implemented fairly effective risk mitigation strategies. As a result, the sample companies' fairly good ERM disclosure findings can be attributed to this.

The introduction of sustainable finance to aid GICs in the financial services industry has apparently been given some thought during their deployment. Companies in the financial sector recognize that in order to stay ahead of the competition, they need green-concept-aligned competitive resources. Thus, they work to get their intellectual capital on board. Based on the work of Penrose and Pitelis [33] and Wernerfelt [60], this study's findings conform to the RBV hypothesis, which is sometimes referred to as RBV for the first time. According to this school of thought, a company's competitive edge stems from its unique combination of resources and competencies. Companies in the financial sector take customer preferences for environmental concerns into account when developing new products and services. The company's efforts to protect the environment have pleased its customers. That will provide a steady flow of cooperation between the company and its suppliers, partners in business, and other outside parties in the interest of environmental preservation. The various efforts made by financial services companies to create competitive finance by utilizing GIC are expected to support the implementation of sustainable finance.

This result is contrary to what is expected from this stakeholder theory. One of the goals of the establishment of the company is to be able to meet the needs of its stakeholders so that to be able to meet the needs of its stakeholders. The company must be able to manage the company well. By conducting good management, the company increases board supervision and company management supervision to avoid information asymmetry. Some people argue that SHR do not affect sustainable finance. Because SHR can encourage companies to focus on short-term rather than long-term profits, for example, companies may choose to make cost savings that can negatively impact the environment, or companies may choose not to invest in research and development that can help them become more sustainable [61]. The results of this research are contrary to what previous research conducted which revealed that SHR support sustainable finance [27, 29-31].

SHR are generally focused on increasing short-term value. Rights such as the right to elect directors and commissioners, the right to receive dividends, and the right to claim compensation can generally encourage companies to make decisions that benefit shareholders in the short term, even if those decisions may harm other stakeholders or the environment [61]. Sustainable finance focuses on increasing long-term value for all stakeholders. Sustainable finance recognizes that a company's long-term success depends not only on its financial performance but also on its social and environmental performance. Therefore, companies committed to sustainable finance need to make decisions that benefit all stakeholders, including shareholders. The following are some examples of how SHR can encourage companies to make unsustainable decisions:

Of course, SHR can also positively impact sustainable finance. For example, the right to elect directors and commissioners can encourage companies to elect boards committed to sustainability. Furthermore, the right to receive dividends can encourage companies to manage their finances prudently. However, in general, SHR do not directly encourage companies to make sustainable decisions. Therefore, companies committed to sustainable finance need to have other mechanisms to encourage sustainable decision-making, such as commitment from management and the board of commissioners, and the implementation of good governance [62].

5.2 Implications

5.2.1 For regulators

ERM helps regulators improve financial stability by identifying and managing risks in the financial system through collaborative prevention and mitigation, in accordance with FRS S1, which covers social, environmental, and corporate governance aspects, providing a better understanding of sustainability-related risk management. Regulators can also encourage financial institutions to develop GIC through relevant regulations, incentives, and reporting standards, aligned with FRS S2 regarding financial performance and sustainability. Collaboration with stakeholders across sectors can be achieved by holding forums and sharing best practices. Furthermore, regulators can encourage the adoption of business ethics and impose sanctions to make companies more accountable in support of sustainable finance, strengthening investor confidence, and aligning with FRS S1.

5.2.2 For companies

ERM provides benefits such as improved financial performance, reduced costs, and enhanced reputation. It also supports the identification and management of risks related to sustainable finance (FRS S1). Developing GIC through sustainable technologies and processes can reduce environmental costs and increase profits, supporting the integration of financial performance with sustainability (FRS S2). Companies can also encourage investors to prioritize long-term returns over short-term profits. The implementation of business ethics will reduce risk and support long-term financial goals and sustainable development (FRS S1). Financing and banking institutions can strengthen green finance through sustainable credit/loan products, which are in line with FRS S2.

5.2.3 For investors

ERM supports investor confidence that organizations are well-managed and sustainable (FRS S1), thereby increasing investment interest. Investors can achieve higher returns in companies committed to sustainability due to lower risks and higher growth potential (FRS S2). Investors should also focus on long-term profitability, supporting sustainable finance practices such as environmental costs, environmentally friendly products, and CSR.

5.2.4 For theory development

This research enriches management accounting knowledge through: (a) Legitimacy theory—regulators strive to regulate to meet stakeholder needs in implementing sustainable finance (POJK 51/POJK.03/2017); (b) Stakeholder theory—companies, consumers, and investors influence each other through company activities; (c) RBV theory—the advantages of GIC provide a competitive advantage in supporting sustainable finance. This research also enriches the sustainable finance literature, particularly in terms of measurement.

ERM positively affects sustainable finance, according to the hypothesis tested, and this is the premise upon which the research's discussion and analysis are founded. Sustainable finance benefits from GIC, but SHR have no such impact. According to the report, improving financial performance, lowering costs, and enhancing reputation are just a few ways in which ERM can help businesses. Additionally, ERM may aid in sustainable finance by assisting businesses in recognizing and mitigating risks related to sustainable finance, while GIC can assist organizations in lowering their environmental expenditures. Creating new, more efficient technologies and processes that make better use of sustainable resources is one way to lower environmental expenses. Businesses can save money on environmental expenses with the help of GIC.

The results of this research contribution to the development of management accounting science, first for legitimacy theory, which is the grand theory of this research, Financial Services Authority Regulation No. 51 for the year 2017, which Financial Services Authority regulates as a regulator, proves that the regulator is trying to make regulations in accordance with stakeholder needs to support the implementation of sustainable finance. Second, according to stakeholder theory, companies, consumers, management, and investors have different interests. Because of these interests, they influence each other through the activities carried out by the company. The theory for RBV theory, the theory is a middle theory from GIC; through this research, it can be proven that having the advantage of GIC causes companies to be able to compete, which can support the implementation of sustainable finance.

Particularly in regard to the development of its metrics, this study has the potential to enhance the literature on sustainable finance. Since disclosure was still optional for many organizations during the research period, this study's disclosure checklist method—which employs a dummy of 0 for no disclosure and 1 for disclosure—is a restriction. Only in 2021, according to a circular letter issued by the Financial Services Authority, or we call it SE. OJK/16/2021, will sustainable financing be required? The second drawback is that every researcher may have a unique viewpoint when it comes to scoring the ERM, GIC, SHR, and SF index indicators because it is subjective. There might be certain things that the corporation does not mention that they will probably expose later on.

Suggestions for the next research include using more complex weighting when calculating the index. Then, the companies that are the research samples can verify the next research. For further research, verification can be carried out on some of the companies that are part of the research sample.

Table A1. Gap Researches

|

No. |

Gap Researches |

|

1 |

Research conducted by Islam et al. (2016) revealed that banks participating in global reporting initiatives disclose more sustainability than banks that do not, while research conducted by Gunawan et al. (2022) found that Indonesian banking tends to favor economic indicators over other indicators, such as social and environmental. |

|

2 |

Research conducted by Oko and Oko (2021); Uchechukwu et al. (2020) revealed a significant relationship between ERM and sustainable finance. Research conducted by Oyewo (2022) stated that ERM improves long-term performance, meaning that effective risk management can serve as a competitive strategy to survive the turbulence that typically characterizes the banking sector. Meanwhile, research conducted by Narumon (2013) revealed that the ERM framework fails to address sustainability risks, thus suggesting the development of an ERM framework to address sustainability-related risks. |

|

3 |

Research conducted by Yusoff et al. (2019) revealed that GIC has a positive relationship with business continuity, so the increasing IC inherent in a company will further support the company's sustainability. Research conducted by Chandra and Augustine (2019) revealed that GIC significantly influences a company's financial sustainability, then moderated by transparency, which can moderate the positive relationship between sustainability disclosure and sustainable finance. That provides new insights that show how the management and development of GIC offers greater competitiveness, thereby improving business performance, including business sustainability performance. The combination of GIC components parity means the potential for high value creation and future performance. |

|

4 |

Shareholders have rights in the company. Shareholder Rights play an important role in sustainable finance and directly impact the company's decision-making process and the achievement of the company's sustainability goals (Bezares et al. 2017). Research conducted by Michelon & Rodrigue (2015) revealed that shareholders need disclosure regarding sustainability because they need the necessary transparency from the company that is useful for decision-making and providing value for shareholders. |

Table A2. Variable operational definition

|

No. |

Variables |

Variables Concept |

Indicator |

Sources |

|

1 |

SF |

Corporate sustainable financial disclosure |

SF = Sustainable Finance Index = ƩXij / nj |

(POJK, 2017) |

|

Σ Xij: Total number of Sustainable Finance (SF) disclosures by the company |

||||

|

nj = number of items for SF in the company 28 indicators (before modification); 37 indicators (with modifications) |

||||

|

score 1 if the item is disclosed |

||||

|

score 2 if the item isn't disclosed |

||||

|

2 |

ERM |

Integrated risk management disclosure integrated with aggregate and holistic strategy and performance |

ERM=Enterprise Risk Management Index = ƩXij / nj |

(Prewett & Terry, 2018) |

|

Σ Xij: Total number of Enterprise Risk Management (ERM) disclosures by the company |

||||

|

nj = number of items for ERM in the company; 20 indicators |

||||

|

score 1 if the item is disclosed |

||||

|

score 2 if the item isn't disclosed |

||||

|

score 1 if the item is disclosed |

||||

|

score 2 if the item isn't disclosed |

||||

|

3 |

GIC |

Green intellectual capital consists of human, structural, and relational capital. |

GIC = Green Intellectual Index = ƩXij / nj |

(Yusoff et al., 2019) |

|

Σ Xij: Total number of Green Intellectual Capital (GIC) disclosures by the company |

||||

|

nj = number of items for GIC; 18 indicators |

||||

|

score 1 if the item is disclosed |

||||

|

score 2 if the item isn't disclosed |

||||

|

score 1 if the item is disclosed |

||||

|

score 2 if the item isn't disclosed |

||||

|

4 |

SHR |

Rights of Shareholders in Corporations |

SHR = Shareholder Right Index = ƩXij / nj |

(Adu, 2022) |

|

Σ Xij: Total number of SHR disclosures by the company |

||||

|

nj = number of items for SHR in the company; 22 indicators |

||||

|

score 1 if the item is disclosed |

||||

|

score 2 if the item isn't disclosed |

||||

|

5 |

Size |

Company size |

SIZE = ln Total Assets |

(Indriyani & Sudaryati, 2020) |

|

6 |

AGE |

The length of time the company was established |

Age = Research Year minus the first year listed on IDX |

(Orazalin & Mahmood, 2020) |

|

7 |

PROF |

The company's ability to generate profits |

ROA = Net profit divided by the average of total assets |

(Weygandt et al., 2019) |

|

8 |

LEV |

The amount of the company's obligations |

DER = Total Debt divided by total assets |

(Weygandt et al., 2019) |

|

9 |

DCOMM1 |

The company variable is used to make it easier to group existing subsectors. |

DCOMM1 = 1 for financing institutions; 0 for insurance, banks, and others. |

(Brown, 1968)Brown (1968) |

|

10 |

DCOMM2 |

The company variable is used to make it easier to group existing subsectors. |

DCOMM2 = 1 for insurance; 0 for financing institutions, banks, etc. |

(Brown, 1968) |

|

11 |

DCOMM3 |

The company variable is used to make it easier to group existing subsectors. |

DCOMM3 = 1 for banks; 0 for financing institutions, insurance, etc. |

(Brown, 1968) |

Table A3. Sustainable finance measurement table based on POJK51/POJK.03/2017

|

No. |

Old Measurement |

New Measurement |

|

1 |

Economic Dimension |

Economic Dimension |

|

1.Quantity of services sold and revenue or sales; |

1. Quantity of services sold and revenue or sales; |

|

|

2. Net profit; |

2. Net profit; |

|

|

3. Number of customers whose products are 50% environmentally friendly; and |

3. Number of customers whose products are 50% environmentally friendly; and |

|

|

4. Number of domestic investment customers exceeding 50%. |

4. Number of domestic investment customers exceeding 50%. |

|

|

2 |

Social Dimension |

Social Dimension |

|

1. The Company's commitment to providing equal service to all customers |

1. The Company's commitment to providing equal service to all customers; |

|

|

2. Statement of equal employment opportunity |

2. Statement of equal employment opportunity; |

|

|

3. Employment of workers in accordance with applicable laws and regulations |

3. Employment of workers in accordance with applicable laws and regulations; |

|

|

4. Percentage of remuneration >/= 80% of the regional minimum wage for permanent employees at the lowest level; |

4. Percentage of remuneration >/= 80% of the regional minimum wage for permanent employees at the lowest level; |

|

|

5. A decent and safe working environment; and |

5. A decent and safe working environment; |

|

|

6. Training and development of employee skills to support sustainable finance. |

6. Training and development of employee skills to support sustainable finance; |

|

|

7. Outreach to the surrounding community, including financial literacy and inclusion; |

7. Outreach to the surrounding community, including financial literacy and inclusion; |

|

|

8. A public complaints system and follow-up. |

8. A public complaints system and follow-up; and |

|

|

9. An ESG-based Customer Database Platform (CDP) program that supports the SDGs. |

9. An ESG-based Customer Database Platform (CDP) program that supports the SDGs. |

|

|

3 |

Environmental Dimensions |

Environmental Dimensions |

|

1. Environmental costs incurred |

1. Environmental costs incurred; |

|

|

2. Reduction of energy use (including electricity and water) and emissions generated by the company. |

2. Reduction of energy use (including electricity and water) and emissions generated by the company; and |

|

|

3. Biodiversity conservation. |

3. Biodiversity conservation. |

|

|

4 |

Product/Service Dimensions |

Product/Service Dimensions |

|

1. Innovation and development of Sustainable Financial Products and/or Services; |

1. Innovation and development of Sustainable Financial Products and/or Services; |

|

|

2. Positive impacts generated by Sustainable Financial Products and/or Services. |

2. Positive impacts generated by Sustainable Financial Products and/or Services; |

|

|

3. Negative impacts arising from Sustainable Financial Products and/or Services. |

3. Negative impacts arising from Sustainable Financial Products and/or Services; |

|

|

4. Risk mitigation measures taken to address negative impacts. |

4. Risk mitigation measures taken to address negative impacts; and |

|

|

5. Customer satisfaction surveys regarding Sustainable Financial Products and/or Services. |

5. Customer satisfaction surveys regarding Sustainable Financial Products and/or Services. |

|

|

5 |

Dimensions of Sustainability Code of Conduct, Sustainability Reporting, ESG Index |

Dimensions of Sustainability Code of Conduct, Sustainability Reporting, ESG Index |

|

1. Publishing a Sustainability Report |

1. Publishing a Sustainability Report; |

|

|

2. Business Highlights in the Annual Report |

2. Business Highlights in the Annual Report; |

|

|

3. Environmental Policy |

3. Environmental Policy; |

|

|

4. GRI Membership |

4. GRI Membership; |

|

|

5. UNEP Signatory |

5. UNEP Signatory; |

|

|

6. Green Category in PROPER |

6. Green Category in PROPER; and |

|

|

7. Member of the Indonesia Stock Exchange |

7. Member of the Indonesia Stock Exchange |

|

|

6 |

--- |

Dimensi Teknologi Informasi |

|

1. Cost Efficiency for Digital Technology Infrastructure; |

||

|

2. Shorter Transaction Times; |

||

|

3. Easier Customer Account Access; |

||

|

4. Providing a green lifestyle (email/paperless communication); and |

||

|

5. Ability to reach a wider customer base (green finance becomes inclusive). |

||

|

7 |

--- |

Stakeholder Dimensions |

|

1. Customers (Increasing the Number of Customers); |

||

|

2. Suppliers/Vendors (Responsive support from IT Vendors); |

||

|

3. Investors/Shareholders (The company is a reputable business group); and |

||

|

4. Regulators (Regulations that increase company revenue). |

[1] United Nations Global Compact. (2019). UN Global Compact Progress Report 2019. https://unglobalcompact.org/library/5716.

[2] Pisano, U., Martinuzzi, A., Bruckner, B. (2012). The financial sector and sustainable development: Logics, principles and actors. ESDN Quarterly Report N°27.

[3] Ziolo, M., Bak, I., Cheba, K. (2021). The role of sustainable finance in achieving Sustainable Development Goals: Does it work? Technological and Economic Development of Economy, 27(1): 45-70. https://doi.org/10.3846/tede.2020.13863

[4] Zorlu, P. (2018). Transforming the financial system for delivering sustainable development: A high-level overview. Institute for Global Environmental Strategies. http://www.jstor.org/stable/resrep21811.

[5] OECD. (2023). Achieving SDG results in development Co-operation. A comparative assessment. https://www.oecd.org/en/publications/achieving-sdg-results-in-development-co-operation_5b2b0ee8-en.html.

[6] Schoenmaker, D. (2018). A framework for sustainable finance. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3125351

[7] Lisnawati, L., Siahaan, M. (2025). Can green and blue thematic financing enhance sustainability value? Evidence from Southeast Asia. International Journal of Ethics and Systems. https://doi.org/10.1108/IJOES-11-2024-0374

[8] Aracil, E., Nájera-Sánchez, J.J., Forcadell, F.J. (2021). Sustainable banking: A literature review and integrative framework. Finance Research Letters, 42: 101932. https://doi.org/10.1016/j.frl.2021.101932

[9] Dong, S., Xu, L., McIver, R. (2021). China's financial sector sustainability and "green finance" disclosures. Sustainability Accounting, Management and Policy Journal, 12(2): 353-384. https://doi.org/10.1108/SAMPJ-10-2018-0273

[10] United Nations Environment Programme. (2019). Letter from the executive UNEP in 2019: 1-16. https://digitallibrary.un.org/record/4051788?v=pdf.

[11] Da Silva Inácio, L., Delai, I. (2021). Sustainable banking: A systematic review of concepts and measurements. Environment, Development and Sustainability, 24(1): 1-39. https://doi.org/10.1007/s10668-021-01371-7

[12] Bankeler, Y. (2006). The Wealth of Networks. https://www.jstor.org/stable/j.ctt1njknw.

[13] Williamson, O.E. (1979). Transaction-cost economics: The governance of contractual relations. The Journal of Law and Economics, 22(2): 233-261. https://doi.org/10.1086/466942

[14] Freeman, R.E. (2010). Strategic Management: A Stakeholder Approach. Cambridge University Press.

[15] Bocken, N., Short, S., Rana, P., Evans, S. (2013). A value mapping tool for sustainable business modelling. Corporate Governance, 13(5): 482-497. https://doi.org/10.1108/CG-06-2013-0078

[16] Freudenreich, B., Lüdeke-Freund, F., Schaltegger, S. (2020). A stakeholder theory perspective on business models: Value creation for sustainability. Journal of Business Ethics, 166(1): 3-18. https://doi.org/10.1007/s10551-019-04112-z

[17] Lüdeke-Freund, F., Dembek, K. (2017). Sustainable business model research and practice: Emerging field or passing fancy? Journal of Cleaner Production, 168: 1668-1678. https://doi.org/10.1016/j.jclepro.2017.08.093

[18] Arena, M., Arnaboldi, M., Azzone, G. (2010). The organizational dynamics of enterprise risk management. Accounting, Organizations and Society, 35(7): 659-675. https://doi.org/10.1016/j.aos.2010.07.003

[19] Siahaan, M., Suharman, H., Fitrijanti, T., Umar, H. (2023). Will the integrated GRC implementation be effective against corruption? Journal of Financial Crime, 30(1): 24-34. https://doi.org/10.1108/jfc-12-2021-0275

[20] Hanggraeni, D. (2023). The influence of enterprise risk management (ERM) on profitability, cost of debt, and company value: The role of moderation of environmental, social, governance (ESG) in Asean-5 countries period 2017-2021. International Journal of Economics Development Research, 4(2): 830-845. https://doi.org/10.37385/ijedr.v4i3.2823

[21] Oyewo, B. (2022). Enterprise risk management and sustainability of banks performance. Journal of Accounting in Emerging Economies, 12(2): 318-344. https://doi.org/10.1108/JAEE-10-2020-0278

[22] Narumon, S. (2013). Enterprise risk management under sustainability platform. Journal of Business and Economics, 4(1): 1-12.

[23] Siahaan, M., Suharman, H., Fitrijanti, T., Umar, H. (2023). When internal organizational factors improve detecting corruption in state-owned companies. Journal of Financial Crime, 31(2): 376-407. https://doi.org/10.1108/JFC-11-2022-0292

[24] Siahaan, M., Nauli, T.D., Siahaan, B.P. (2024). Can internal mechanisms control detect corruption through fraudulent behaviour? AFRE Accounting and Financial Review, 7(1): 1-8. https://doi.org/10.26905/afr.v7i1.11893

[25] Chandra, M., Augustine, Y. (2019). The effect of green intellectual capital index and sustainability disclosure on company financial and non-financial performance with transparency as a moderating variable. Jurnal Magister Akuntansi Trisakti, 6(1): 45-70. https://doi.org/10.25105/jmat.v6i1.5066

[26] Yusoff, Y.M., Omar, M.K., Kamarul Zaman, M.D., Samad, S. (2019). Do all elements of green intellectual capital contribute toward business sustainability? Evidence from the Malaysian context using the partial least squares method. Journal of Cleaner Production, 234: 626-637. https://doi.org/10.1016/j.jclepro.2019.06.153

[27] Gómez-Bezares, F., Przychodzen, W., Przychodzen, J. (2017). Bridging the gap: How sustainable development can help companies create shareholder value and improve financial performance. Business Ethics, the Environment & Responsibility, 26(1): 1-17. https://doi.org/10.1111/beer.12135

[28] Adu, D.A. (2022). Sustainable banking initiatives, environmental disclosure and financial performance: The moderating impact of corporate governance mechanisms. Business Strategy and the Environment, 31(5): 2365-2399. https://doi.org/10.1002/bse.3033

[29] Michelon, G., Rodrigue, M. (2015). Demand for CSR: Insights from shareholder proposals. Social and Environmental Accountability Journal, 35(3): 157-175. https://doi.org/10.1080/0969160X.2015.1094396

[30] Money, K., Schepers, H. (2007). Are CSR and CG converging. Journal of General Management, 33(2): 1-11. https://doi.org/10.1177/030630700703300

[31] Smith, V., Lau, J., Dumay, J. (2022). Shareholder use of CSR reports: An accountability perspective. Meditari Accountancy Research, 30(6): 1658-1679. https://doi.org/10.1108/MEDAR-02-2020-0769

[32] Siahaan, M. (2025). Use big theory clarifies financial performance: The role of internal mechanisms control. Journal of Accounting and Strategic Finance, 8(1): 94-109. https://doi.org/10.33005/jasf.v8i1.596