Jugal Kishor Kushwaha![]() | Abhijit Ghosh

| Abhijit Ghosh![]() | Anjay Kumar Mishra

| Anjay Kumar Mishra![]() | Om Prakash Giri*

| Om Prakash Giri*![]()

© 2025 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Sustainability in banks is now widely recognized as a relationship that grows from a dialogue between banks and customers, especially in developing countries. This paper offers a construct in framing toward mutual accountability in sustainability and managing ESG risks. Backed by stakeholder theory, systems thinking, and corporate social responsibility, the framework presents a six-level ESG co-creation model based on prosocial values of trust, transparency, and mutual goals. Scoping review methodology was used for this framework and guided by the framework of Arksey and O’Malley, extended by Levac et al., and presented in compliance with the PRISMA-ScR guidelines. We conducted an online search within Scopus, Web of Science, Google Scholar, and JSTOR for articles between 2010 and 2025 on bank–customer sustainability interactions. Fifty studies that met the inclusion/exclusion criteria were reviewed using a structured data extraction. Inductive thematic analysis was performed with validated inter-coder reliability. The study reveals internal and external drivers of sustainability for banks and customers with digital innovation and co-creation as the main enablers. This framework provides actionable recommendations for banks, policymakers, and sustainability champions to create ethical, resilient, and inclusive financial ecosystems.

bank and customers, CSR systems thinking, digital transformation, ESG, sustainable business viability, synergistic sustainability

Sustainability is a very big deal in the global corporate landscape, and companies across all industries are seeking how to balance economic, environmental, and social bottom lines. The banking sector is a significant part of this ecosystem cycle because sustainability within it affects more than just the bottom line and, in turn, trickles down to its customers, communities, and even the economy. With customer expectations in the past few years changing to wanting more sustainable practices, as proven by recent ESG ratings on banks and companies around the globe, it has become clear that sustainability cannot be achieved without collaboration. This transformation is pushing for an alternative commercial resilience, one that meets sustainable demands and at the same time drives local financial institutions to enable this transition within their scope of responsibility.

Banks have a pivotal role to play in driving the broader economy forward while simultaneously acting as financial intermediaries, functioning as an engine for sustainable growth [1]. As providers of money, capital, and ideas, banks are essential for sectors and people to step into ecologically sustainable and socially just behaviors. Consumers are shopping around for banking options that resonate more closely with their values, preferring organizations that demonstrate an environmental conscience. Banks and customers are part of a reciprocal relationship from which they emerge, therefore, an enabling structure that allows both to influence one another concerning sustainable outcomes. Recent studies suggest that companies with strong sustainability policies are expected to maintain their competitive advantage and business continuity in a continuously changing market atmosphere [2].

The concept of synergistic sustainability suggests that the activities that banks and their corporate clients engage in are interrelated, reinforcing rather than separate from each other. This community-owned model will enable a scalable, sustainable, and profitable business. Much work has been done on various aspects of corporate sustainability in banking, such as green finance and ethical banking [3], but scant scholarly attention has been paid to understanding the mutual influences between banks and their consumers for promoting sustainability [4]. Understanding this link is key to developing a holistic business case for the financial viability of sustainability that can support both financial institutions and their clients as they seek to implement sustainable strategies.

This study aims to curb this gap by developing a conceptual model that shows the symbiotic relationship between banks and customers in achieving sustainable benefits. It explores how the relationship between them can underpin a virtuous circle of sustainable behaviors that deliver long-term benefits from an economic, environmental, and social perspective. The proposed framework will explain how banks can produce services and products that better meet the values of their customers, as well as be sustainable in what types of goods & solutions may appeal to the core perspective from a bank customer side, while on another end it outlines an option to respond supporting sustainability through promoting those who grew sustainably.

The framework will be generated by building established sustainability theories and models, as well as contemporary empirical research. The lens of stakeholder theory, which emphasizes the importance of appropriately considering all stakeholders in corporate decision-making, and institutional theory for the legitimacy of external pressures [5] will guide this framework. Based on these theoretical foundations, we will be able to explore the interaction of lower needs when banks are interacting with customers and how this can assist academic research models as well as practice-related tactics for sustainable banking.

This research contributes to prior literature on sustainability in the financial sector by suggesting a new model that highlights collaborative work between banks and their clients. Strengthening these links can improve the lasting viability of financial institutions and their customers, as demonstrated by a recent report on mutual impacts. The findings have significant implications for banks seeking to align with global sustainability goals such as the UN Sustainable Development Goals (SDGs), and clients wanting access to ethical banking products. These findings provide a basis for future work on sustainability in the banking industry, particularly on how client engagements may encourage good and sustainable practices of banks.

The emergent literature on sustainable business practices increasingly underlines the importance of financial institutions as they shape both societal and economic sustainability outcomes [3]. The banking sector, as a principal intermediary between companies and individuals on the one hand and capital markets where risk-based returns are assessed, has an important role in steering those stakeholders toward more environmentally & socially responsible behaviors. This part explores some key concepts and the literature that deals with how such collaboration between banks and consumers can bring one-stone-two-bird level sustainability, as well as providing empirical evidence.

2.1 Corporate sustainability in the banking sector

Corporate sustainability in banking refers to strategies financial institutions undertake that deal with their social, environmental as well as economic impacts and yet deliver sustained returns [6]. Scholars, in this space, have focused on how financial institutions operationalize sustainability through green finance, ethical investment, and corporate social responsibility (CSR) of the bank [2]. Banks increasingly include sustainability in their core strategy due to regulatory requests, but also investor and stakeholder demands (such as customers or society itself) [1]. Increasing demand for sustainable financial instruments such as green bonds and sustainability-linked loans in turn suggests that the importance of sustainability in banking practices is rising.

However, most work on corporate sustainability in banks focuses on processes within the system and applies a top-down approach [3]. The mainstream of the extant research works on the issue of corporate sustainability in the banking industry has long tended to be of a top-down nature. Such a model makes decisions predominantly at upper-level groups (i.e., board of directors, C-levels), which cascade them through the organization for execution [7]. This approach is generally effective in terms of legal and ESG (Environmental, Social, and Governance) compliance, but it often doesn’t engage deeply with frontline workers, customers, and communities. And increasingly, many of these stakeholders, such as investors, customers, and regulators, are asking for more than financial returns. They anticipate banks to concentrate on long-term value creation and to manage material ESG issues, which relate to both the business and the broader society. These interested parties believe businesses need to be more focused on sustainable practices for the greater good, and that corporate management should balance short-term gains against long-term commitments.

A recent case analysis by Balarezo and Corcuera [8] found a gap between policy and practice among Nordic banks, where all decisions relating to sustainability, such as ESG information and investment screening, were made by the top management or executive board and not the branch-level customers, and the managers can contribute. The "culture of compliance" method often results in disengaged employees and a lack of customer confidence. The investigation advocates a bottom-up or co-creative approach, involving employees, customers, and other stakeholders in the design of sustainability projects. The model fosters forms of cooperative governance, co-designed products, participatory pathways for feedback, and transparent modes of communication that do not so much sustainability as a regulatory compliance issue or a public relations opportunity but rather already work with the real experiences and expectations of its employees and stakeholders. For example, organizations such as Triodos Bank and the Cooperative Bank (UK) demonstrate models in which stakeholders, such as customers voting on sustainability priorities or employees co-creating green financial products, can better align with sustainability goals and increase trust [9].

This approach is particularly beneficial in developing countries such as Nepal, where customer awareness and the features of the local markets are important. Through incorporating mutual feedback loops, a key feature of our framework, the paper enables systemic interactions between the institution’s strategies and customer behavior, fostering sustainability, responsibility, and corporate survival in the long run. The value of the co-creative approach is its inclusiveness and flexibility. Unlike top-down strategies, it leverages decentralized information, shared values, and mutual trust, triggering innovation and adaptive capacity. It is also in line with the increasing scholarly attention to relational governance and stakeholder collaboration as key to achieving meaningful sustainability outcomes [10, 11].

One of the most important trends in green and sustainable banking is represented by "green finance," which simply emphasizes what banks do as a business [12]. This is important, but no study has explored the influence of banks' sustainability practices on consumer behavior and preferences in contrast. Together, these works demonstrate the need to develop a more complete understanding of how sustainability can be enhanced through joint actions taken by banks and customers from both banking researchers and practitioners.

2.2 Customer impact on sustainable banking

Customers are what drive sustainability in banking by defining the market demand for sustainable products and services. Studies suggest that consumer preferences for ethical and sustainable banking are increasingly influencing the strategic decisions of financial companies [4]. This behavior is driven by changing societal values, with customers using the consumption of companies and products as a proxy for their environmental or ethical [13]. According to research on consumer behavior, we also know that customers are more likely to stay faithful to banks that take an active role in the realm of sustainability [14], which provides banks with incentives for introducing sustainable business models.

One of the biggest weaknesses in this research is understanding how relationships between banks and clients are interconnected. While much attention has been directed to the influence of customer demand on sustainable banking, less is known about how banks can steer their customers towards sustainability by using the products and services they provide. Financial instruments often incentivize customers to invest financing in ecologically sustainable projects, such as green mortgages or carbon offset schemes [15]. This mutual reinforcement cycle– where the customers advance banks towards sustainable innovation, which in return shapes customer preferences remains an unexplored subject within the literature.

2.3 Theoretical frameworks on synergistic sustainability

Using stakeholder, institutional, and other new theories, the interactions between banks with customers in promoting sustainability could be examined. Stakeholder theory was introduced by Freeman [16] to remind organizations of the fact that business decisions should be taken considering all stakeholders, like customers, employees, shareholders, and society itself. Within this framework, the consumers are seen as one of the key stakeholders, and they need to meet a bank’s sustainability requirements [17]. Recent research suggests that banks can boost customer loyalty and financial performance by actively engaging their customers in sustainability activities [2].

Furthermore, the institutionally based aspects of sustainable banking are detailed through theory development on how organizations/institutions such as banks proactively respond to external pressure with their sustainability policies; according to institutional theory, for example, orchestrated by DiMaggio and Powell [5], due to consumer expectations. The concept suggests that banks are coming under more pressure both from customers and society at large to enact sustainable frameworks that promote the long-term well-being of the environment and community. Banks shape these norms through financial solutions that promote sustainable behavior among clients [13].

Recently, some empirical studies have explored the relevance of co-created sustainability in banking. More efficient sustainability effects can be achieved if customers participate with banks in the formation of sustainable financial solutions. Indeed, with co-creation defined as collaborative creation between banks and customers to further innovation processes, it places focus on the argument that sustainability is a two-way path facilitated through sustainable banking practice.

2.4 New theoretical concept of sustainability

The evolving field of sustainable finance has led to the introduction of new theoretical concepts that analyze how banks and clients interact in promoting economic, environmental, and social sustainability. According to the Sustainable Value Creation Theory, companies can create value for their clients by incorporating sustainability into the company's core business model, with banks being the primary example. Increasingly, the objectives of banks are being aligned with broader stakeholder expectations related to consumers, society, and the environment rather than focusing solely on financial returns. As such, this alignment has allowed for a new range of sustainable financial products such as green loans and ESG (Environmental, Social, Governance) investment funds suitable to customers who advocate sustainability through financing choices they made in accounts with banks providing these opportunities as well (McKinsey & Company 2023; International Banker 2023). Supporting sustainability campaigns; for instance, renewable energy projects generate a mutual gain for banks and their customers, which boosts the overall business viability.

One of the flagship concepts is Circular Economy Finance Theory, which refers to any system that seeks to mitigate unnecessary waste by continually reusing resources for as long as possible while recovering and regenerating products at the end of each service life. Banks are also indispensable when it comes to funding enterprises working in such paradigms by providing credits or investments designed for sustainable resource usage. As it pertains to environmentally friendly customers, a financial institution associating itself with circular economic activities can make the change from a linear (take-dispose) economic process into a more effective one and receive points for that additionally (Home of Sustainability News 2023). As a result, banks have started developing financial instruments tailored for sustainability-focused businesses, hence increasing their role in promoting sustainable consumption and production.

Emerging as a key driver for sustainability in the finance industry, Green FinTech Theory has become more pervasive during this era of digital transformation. This hypothesis focuses on how new technologies, such as AI-powered carbon tracking apps and blockchain for ESG reporting, can contribute to sustainability (McKinsey & Company, 2023). Digital banking devices are increasingly used to reduce the environmental impact of financial actions and offer consumers a strategy for tracking their carbon footprint, putting money into renewable possibilities, along with greater comparison. The seamless union of technology and sustainability has given rise to ways for banks to be more inclusive in their sustainable banking practices so that it is not just the bank working towards green goals but also its clients; in a sense, using tech as leverage to promote responsible behavior.

Behavioral Sustainability Finance Theory is a strand of behavioral economics that applies heuristics (common decision-making shortcuts) and nudge theory to finance. This includes banks setting up default options (like green savings accounts) and using nudges to drive environmentally friendly financial behaviors in the customers, which would make it easier for customers to make an eco-friendly choice (McKinsey & Company, 2023). This hypothesis illustrates how small changes in behavior like making sustainable options the default option, could lead to significant increases in sustainability results within the banking industry.

In response to growing client calls for transparency, Impact Investing Theory 2.0 places measurable ecosystem and social returns on an equal footing with financial return prospects. It brings greater focus on how investment portfolios are aligned with the goals of SDGs while balancing this desired alignment with financial performance. This second generation of Impact Investing 2.0 underscores the increasing importance and focus on transparency, with banks offering features for clients to track their investments in real-time; thereby setting in place levels of accountability that lead towards credibility (Home of Sustainability News, 2023. International Banker, 2023). This transition is made easy with robust measurement tools and reporting frameworks, enabling banks to meet client requests for verifiable sustainability claims.

Green Consumerism Theory has emerged as a reflection of the increasing demand from consumers for financial services provided ethically. Modern consumers are more and more demanding in terms of the provenance of what they buy, as well as environmentally friendly aspects of the fintech at their disposal. This prediction focuses on the rise of conscious consumption in financial products, with customers selecting banks that demonstrate substantial ESG commitments and clear sustainability initiatives (Associated Bank, 2023; McKinsey & Company, 2023). Consumers are now valuing financial institutions and companies (high street stores) that can prove they have reduced their environmental impact, following the idea that money makes this kind of ethical consumption.

So, it concludes that this suggests developing interaction between different banks and with clients in the context of sustainability. Digital innovation, new regulatory regimes, and evolving consumer behavior are pushing both into the same sphere of influence; a mutually beneficial ecosystem where it serves their common environmental practices for banks as well as customers in terms of financial operations.

2.5 Empirical research on collaborative sustainability

The empirical literature on how customers and financial institutions are jointly involved in sustainability projects is growing. Połeć and Murawska [18] showed that banks actively involving their consumers in sustainability initiatives, whether by designing special incentives to encourage the purchase of environmentally friendly products or promoting carbon-neutral financial solutions, lead to higher consumer engagement and satisfaction with the bank. Research by Khan et al. [4] proposed that banks are more likely to get customer recommendations and referrals where sustainability is emphasized, providing evidence of a mutually beneficial relationship between the two parties concerning sustainable activities.

Research suggests that digital banking will be central to collaborative sustainability efforts. Digitalization, such as mobile banking applications, also facilitates banks in terms of providing simpler and easier-to-access information about the sustainability aspects of their products or services [12]. Retail banking is meeting the trend by encouraging clients to participate directly in sustainability initiatives, from carbon tracking tools and customized advice on reducing their ecological impact, facilitated through digital platforms.

2.6 Deficiencies in literature

The current research provides some valuable evidence about corporate sustainability in the banking sector and consumer influence, and important gaps remain. Firstly, there is a lack of research on the bank-customer relationship sustainability and reciprocal dynamics. Considerable research has been focused on the possible influence of client demand when it comes to banking practices, but not much work is available that studies how a bank could preemptively affect consumer behavior concerning sustainability. However, another issue is the lack of holistic frameworks that would investigate synergizing sustainability achieved by aligning banks with their customers. This gap in our knowledge requires further research to build integrated models that take both of these systems into account and recognize their collaborative, reinforcing processes.

The banking sustainability literature has largely focused on either the internal affairs of banks or their external stakeholders (especially consumers) regarding bank sustainability ambitions. We have all become aware by now that sustainability is an equation, and a term of partnership with clients who, in return, impact it. The existence of customer preferences that banks must cater to leads them to adopt sustainable practices, whilst the products and services offered by a bank influence customer behavior in turn. This synergy of the interactions is a main track for further research, in particular, to develop more integrative conceptual lenses capturing the highly dynamic and co-creative character of financial services sustainability.

2.7 Conceptual framework of the study

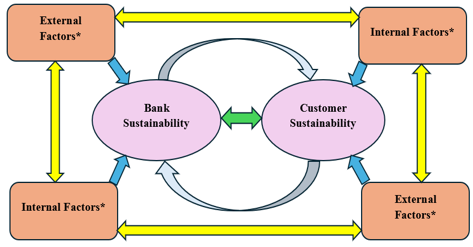

As illustrated in Figure 1, the relationship between bank sustainability and consumer sustainability is mutually constructive and dynamic. This approach focuses on both banks and customers, whose sustainable practices are mutually reinforcing. Banks affect consumer behavior thanks to sustainable finance products, an ethical approach, and ESG-oriented communications; consumers influence banks with changing preferences, values, and behavior expectations. As shown in the bidirectional arrows that connect all internal and external dimensions, sustainability is participatory and co-evolutionary. Inner values are influenced by external pressures, and external constraints tend, as a rule, to reflect inner behavior or the institutional culture. This systemic view recognizes sustainability as a co-creating, dynamic effort upheld by both organizational and human agents.

The sustainability of both entities is driven by internal and external factors. This being the case, for banks, the question of governance, growth, education of employees, and how they operate their business is more important than competitive market trends and technological changes. Personal belief, Eco-envy, financial planning, and behavior interface with political will, business savvy, and cultural cues on the consumer side. This line of thought puts it across that sustainability in a mutually beneficial manner-in terms of transparency, feedback, and participation, fosters sustainability banking (SB) in the long run, especially in detailed socio-economic environments like developing economies.

Figure 1. Bank and customer sustainability

Source: Author

2.8 Thematic organization of sustainability factors

Factors of Bank and Customer Sustainability (Table 1) were derived from a comprehensive scoping review of interdisciplinary academic literature, industry publications, and policy documents about corporate sustainability in the banking sector. Searches were conducted in Scopus, Web of Science, and ScienceDirect for the terms “bank sustainability drivers,” “customer sustainability behavior,” and “financial ESG factors.” Peer-reviewed studies published from 2010 to 2025, addressing sustainability from both institutional and consumer viewpoints in established and emerging economies, were incorporated [7, 8, 19].

Table 1. The thematic grouping of bank and customer sustainability factors

|

Bank Sustainability Factors |

||

|

Internal Factors |

Theme |

External Factors |

|

Corporate governance and leadership |

Governance and Leadership |

Regulatory and legal requirements |

|

Sustainability culture and values |

Strategy and Culture |

Stakeholder expectations |

|

Risk management and compliance |

Risk and Compliance |

Market and competitive pressure |

|

Technological innovation |

Technology and Innovation |

Technological advancements |

|

Employee training and development Operational efficiency |

Human Capital and Behavior |

Global environmental and social trends Partnerships and collaborations |

|

Sustainable financial products Internal sustainability reporting |

Financial Products and Services |

Customer demand for sustainable products Economic and financial stability |

|

Customer Sustainability Factors |

||

|

Internal Factors |

Theme |

External Factors |

|

Personal values and beliefs |

Values and Motivation |

Cultural and regional norms |

|

Environmental awareness |

Knowledge and Awareness |

Government policies and incentives |

|

Financial capability Long-term financial planning |

Financial Capability and Planning |

Economic conditions |

|

Lifestyle choices Behavioral habits |

Behavior and Lifestyle |

Market trends and consumer education |

|

Sustainability preferences Perceived benefits |

Engagement and Preferences |

Availability of sustainable products and services Corporate sustainability initiatives |

|

Technological Infrastructure |

Technology Orientation |

Technological advancements |

|

Theme Mapping Matrix |

||

|

Factor Theme |

Justification |

Supporting References |

|

Governance and Leadership |

Focuses on leadership architecture, stakeholder management, and upper-echelon sustainable banking frameworks. |

[7, 19, 20] |

|

Strategy and Culture |

Connects values of organization and culture of sustainability to long-range strategic planning. |

[7, 10, 21] |

|

Risk and Compliance |

Emphasizes the compliance systems, risk management, and ESG regulations. |

[19, 22] |

|

Technology and Innovation |

Explores how innovation and digital transformation support sustainable banking models. |

[10, 22] |

|

Human Capital and Behavior |

Regarding employee engagement, training and operational practices, and customer behavior. |

[8, 9] |

|

Financial Products and Services |

Links production of green financial products and reporting to co-creative focus on the customer. |

[9, 22] |

|

Customer Motivation and Values |

Built on CSR and stakeholder concepts related to internal value for external sustainability activity. |

[20, 21] |

|

Customer Knowledge and Awareness |

Demonstrates how learning, consciousness, and peer influence inform eco-friendly demeanor. |

[8, 9] |

|

Customer Preferences and Tech Orientation |

Describes market trends, technology accessibility, and customer co-design in sustainability. |

[9, 10] |

Alongside the literature synthesis, semi-structured interviews with experts from the Central Bank and other licensed banks and financial institutions in Nepal corroborated the criteria. Practicality and context were guaranteed. This conceptual framework employs stakeholder theory [20], corporate social responsibility (CSR) models [21], and systems thinking to highlight the interconnectedness and dynamic characteristics of the sustainable interaction between banks and customers.

The components have been systematically categorized into governance, strategy, operations, technology, and behavior to enhance clarity and interpretability, as per contemporary sustainability literature and frameworks [10, 22].

The factors of Bank and Customer Sustainability were compiled from a scoping review of the interdisciplinary academic literature, industry publications, and policy documents on sustainability for the banking industry. A search strategy in Scopus, Web of Science, and ScienceDirect was conducted using the keywords “bank sustainability drivers,” “customer sustainability behavior,” and “financial ESG factors.” Peer-reviewed papers during the period 2010 to 2025 addressing sustainability from an institutional and consumer perspective in developed and LSO economies were included [7, 8, 19]. In addition, the Semi semi-structured interviews conducted with the domain experts of the Central Bank and other licensed banks and financial institutions of Nepal validated the criteria. They ensured there would be utility and context. This mental frame integrates stakeholder theory [20], CSR models [21], and systems thinking to underscore the complex and dynamic nature of a sustainable bank-customer relationship. These factors have been collected systematically into governance, strategy, operations, technology, and behavior, to increase clarity and interpretability, in line with modern sustainability literature and frameworks [10, 22].

2.9 Research questions of investigation

a) How do banks and customers collectively influence sustainable practices adoption?

b) Which factors are most important for collaborative sustainability in banking?

c) How can banks use consumer behavior for sustainable business models?

2.10 Hypothesis of research

H1: Banks and customers influence each other's sustainability.

H2: Environmental, social, and governance (ESG) legislation, regulatory frameworks, consumer demand for sustainable products, and technological advances shape collaborative sustainability in banking.

H3: Behavioral nudges, digital technologies, and sustainability-linked products can help banks become more sustainable.

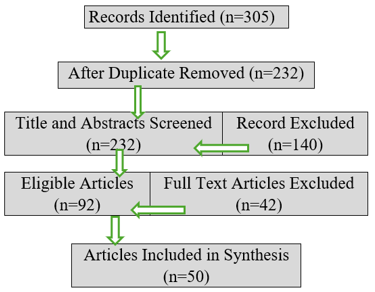

A scoping literature review approach is applied to explore this new developing context of collaborative and reciprocal sustainability practices between banks and their customers. Such a wide and multidisciplinary topic as eating, physical activity, and obesity can be mapped using a scoping review, which was selected as a methodology to map the key concepts and the gaps in available evidence and provide an overview of the findings from different types of evidence sources. The method is based on the core framework proposed by Arksey and O’Malley [23] and developed further by Levac et al. [24], and according to PRISMA-ScR guidelines for methodological transparency and methodological rigor (Figure 2).

Figure 2. PRISMA chart flow

Source: Author

The data collection and analysis were oriented towards three key research questions. The first question is: What are the internal and external sustainability drivers, both for banks themselves and for their customers? This inquiry examines governance systems, legislative contexts, market drivers, and behavioral motivations for engaging in sustainability. Second, what are the dynamics of banks and customers in making each other’s sustainability decisions and behaviors? This analyzes the reciprocal effect of policies, services, and expectations on sustainability. Thirdly, what theoretical or empirical insights can be gained on co-creation and co-dynamics in sustainable finance? This analysis aims to explore how collaboration structures and shared responsibilities contribute to wider ESG (Environmental, Social, and Governance) agendas.

To respond to these questions, the authors conducted searches using the structured literature search in Scopus, Web of Science, Google Scholar, and JSTOR, utilizing a Boolean search strategy that included (but were not limited to) terms such as ‘sustainable finance,’ ‘bank sustainability,’ ‘customer sustainability,’ ‘collaboration,’ ‘co-creation,’ and ‘reciprocal influence,’ as well as geographic tags such as ‘Nepal’ and ‘developing countries.’ The search was restricted to peer-reviewed articles, written in English, and was conducted between 2010 to 2025 and focused on sustainability in financial institutions and relationships with customers within the broader context of emerging and developing countries.

A standard data extraction form will collect information about authorship, research goals, methods, and main results for each article. According to strict inclusion and exclusion criteria, a total of 305 articles were found in our primary search. Following deduplication and title, abstract, as well as full-text review, 50 studies were included in the final synthesis. Variables of interest such as publication details, geographic focus, sustainability attributes, and collaboration systems were captured using a standardized data extraction form (Appendix A).

Thematic analysis was used to develop a narrative synthesis to reveal recurrent and patterned findings related to the collaborative & reciprocal benefits, sustainable practices, and banking economic viability [25]. Thematic analyses were performed by an inductive approach which included themes related to internal governance mechanisms, regulatory pressures, customer-driven sustainability, co-creation strategies, and mutual contributions. Dual independent coding and inter-coder reliability checks were used for consistency and reduction of bias. These results formed the basis for the integrative conceptualization presented in this paper.

This conceptual framework for synergistic sustainability invokes cooperation between the bank and its customers to determine what factors control company worth via a review of this synthesis literature. Ethics require correct citation and recognition of all sources considered to ensure proper credit for original authors' compliance. It is also built based on sustainable banking, being the foundation for research & practical relevance.

The scoping review suggests that joint sustainability efforts by banks and customers are crucial for long-term sustainability impact within the financial sector. This study does not present novel empirical evidence but collects evidence in the literature on common patterns and conceptual aspects. Several examined studies emphasize that sustainability is efficient with the active participation of both stakeholders, i.e., banks and their customers, in cooperation practices that are consistent with environmental, social, and governance (ESG) targets. Lin et al. [26] and Murè et al. [27] show how mutual stakeholder alignment increases trust, supports innovative green finance, and strengthens institutional resilience.

One topic that has been shown by a variety of studies is the impact of communication and feedback systems on the formation of sustainable behavior. Far from it being a reputational concern for the whole industry, these reports say that there is significant transformation available through active participation. Xu et al. [28] showed that the use of bidirectional digital communication channels between banks and customers significantly increased the uptake of green lending products. Fatmasari [29] argued that transparency in ESG reporting strengthens confidence and encourages customers to harmonize their financial decisions with the principles of sustainability.

Our study suggests that digitalization tends to influence continuously and extend the level of green banking. Going Digital, enables paperless transactions, mobile eco-friendly savings accounts, and even carbon footprint measurement, thereby minimizing the ecological footprint of banking. This pattern is supported by numerous studies. The usage of mobile banking in Developed Asia has led to a measurable decrease in physical banking requirements which is both the cause of improved efficiency of operations and environmentally friendly service provision [29]. Li et al. [30] argue that in particular in developing regions, banks at the forefront of the digital infrastructure are better placed to mainstream sustainability in core financial services.

The results suggest that the interdependence of sustainability goals through technical, behavioral, and policy alignment can help drive systemic change. The literature suggests that a relational paradigm based on feedback loops, co-creation, and shared aspirations should be seen, rather than treating banks and customers as separate entities, as vital for business continuity in a sustainable manner. Viewing sustainability as a two-way street, banks function not solely as marketers of green products, but also as active agents subject to consumer sentiments, market forces, and social norms.

This paper introduces a new concept, "co-creation of synergistic sustainability", arguing that the collaboration and reciprocity between banks and customers have not been addressed sufficiently, although co-creation has been discussed in existing literature [31].

5.1 New contributions of this paper

An integrated theoretical framework: This paper provides a new conceptual model that combines stakeholder theory, Institutional theory [5], and many other new theories, to explain the multilevel interactions between banks and customers. To the best of our knowledge, this is a new approach using customer expectations as a point to explain banks' sustainable practices and also explain how they can go back through customers showing them, whereas available literature focused more on what sustainability activities banks perform such as green financing or ethical banking [3]. This symbiotic relationship fosters the mutual reinforcement of sustainable behaviors.

The unidirectional focus of bi-directionality between the bank and customer: Recent research on corporate sustainability in banking treats banking as a one-way street focusing either on the responsibility for banks [2] or behaviors towards ethics where easiness has been granted by customers [13]. This paper fills this gap by focusing on the feedback loop between banks and customers where banks influence customer behavior concerning sustainable financial products (e.g., green loans, ethical investment options) while customers force their banks to pursue higher levels of sustainability with the demand for responsible banking services. The idea of this collaborative sustainability represents a major development beyond traditional corporate efforts for promotion.

The approach described in this article has practical consequences for designing a long-sustenance business model that benefits both the financial institution and its customers. The paper provides strategic direction for enabling banks to better integrate their product and service offerings with the growing environmentally oriented consumer base resulting in a spirit of symbiotic utility allowing retention-base loyalty while contributing towards both corporate sustainability goals as well, contextualized throughout [4]. Additionally, the study also explores how customers could exert their power and start supporting banks with a strong sustainability claim to enable large-scale systemic transformation in finance.

The framework aligns with the United Nations' Sustainable Development Goals (SDGs), in particular, SDG 8: Decent Work and Economic Growth and SDG 13: Climate Action. This work lays out an innovative approach through which the financial industry and customers can be partners toward global sustainability, with a specific focus on how to stimulate sustainable behaviors in one of their biggest industries. This perspective has been somewhat neglected in the current literature, with a focus on individual banks simply creating environmental or social impact rather than reflecting how their interaction also changes/uplifts clients [1].

This study contributes to sustainability in banking academic discourse by introducing a co-created concept of bank sustainability, where all outcomes on sustainable issues originate from continuous interactions between companies and different stakeholders [17]. The proposed framework also underscores how the bank-customer interface is interconnected to sustainability goals, which opens up new ways for research insights along with avenues that can foster sustainable finance in practice.

The novelty of this article is an integrated view that considers the client and bank as co-creating each other. We find that organizations in the bank stakeholder system influence each other through policies and decisions supporting sustainability, which gives a unique contribution to literature relating to sustainable banking as well as business viability more generally. This essay covers a crucial textual void in our literature and offers concrete support for the reframing of banking activity towards sustainable goals, leading to growth over time and ethical commercial behavior.

6.1 Conclusion

This research highlights the need to develop sustainable initiatives that can be considered a joint and reciprocal commitment between financial institutions and their customers. The scoping review shows that co-created activities can help to create a more resilient and inclusive financial system. Properly implemented, these strategies can create a living financial system that will support growth, respond to immediate environmental challenges, and address urgent social needs.

This apparatus includes a large number of financial products and business models to bring the financial result in line with the ESG (Environmental, Social, and Governance) target. Green bonds are increasingly an important financing vehicle for renewable energy and green infrastructure [32]. In the same vein, ESG-linked loans incentivize borrowers to meet predetermined sustainability targets [22]. Impact investing, increasingly an investment approach that aims to generate measurable social or environmental benefits alongside financial return, is resonating with institutional and individual investors alike [33]. Furthermore, community-based banking models such as credit unions or local cooperative banks are rooted in inclusive finance and promote local sustainable development [34].

Analysis of synergistic sustainability manifests the importance of symbiotic involvement in assuring sustainable economic perpetuity by examining interactive and mutual influences between banks and consumers. The relationship between banks and customers is now starting to be understood as stakeholders with mutual Our results benefit creating sustainability. The model shows that for a sustainable relationship between banks and their clients, both parties must engage with one another: Banks provide products/services promoting sustainability, and consumers reward them through responsible banking behavior. Matching banks' and customers’ interests also increases the capacity for corporate resilience, risk control, and long-term financial value, achieved at the same time as fostering broader societal goals (e.g., environmental protection or social equity). This virtuous circle is crucial for companies looking to be relevant in a future where only sustainability seems to dream.

6.2 Implications for management

Financial managers and policymakers need to learn that future banking strategies will have to be flexible, stakeholder-based, and oriented toward the creation of long-term value using achieving sustainability. Banks can strengthen trust and build positive customer relationships by embracing digital innovation, stakeholder engagement, and transparent ESG principles. Further research needs to explore the equality of these tools in different geographic contexts, particularly in developing countries like Nepal, where sustainability practices are usually determined by cultural and legal issues.

The findings of the study show that banks should rethink their traditional business model and transform towards a value-based strategy for sustainability. Managers should put the development of financial products that serve clients' needs and also drive sustainable ambitions at the top of their list. This includes measures such as green loans, ethical investment products, or incentives for end customers that are ecologically sensitive and compatible with the well-being of our planet. In addition to that, building a reliable communication and trust system between the banks and their clients will help foster loyalty as well as long-term engagement, given that clients are more likely to advocate for institutions that align with their values on sustainability.

Customers, the findings suggest, are not passive users of financial services but participate vigorously in shaping sustainable banking spaces. Financial managers and advisors should leverage clients to these sustainable projects by informing them of the connotations of their financial decisions on environmental welfare and social wellbeing. Also, distinctive financial solutions that are in line with the sustainability values of clients play a role in augmenting connections, resulting in higher customer retention as well as giving further credibility for the bank.

Managers should stand back and try to develop a broader view, recognizing that sustainability is part of the landscape any business must navigate today if it wants to flourish in the future. In a competitive market, it will be the banks that establish collaborations with their customers to partner and construct sustainable solutions and embed sustainability into core banking strategies that profit.

6.3 Future research avenues

This research paves the way for understanding the joint sustainability impact of banks and clients; however, there is a lot more to be looked at in further areas. Based on an investigation of these issues [35], forthcoming research can deepen our insight into how collaborative relationships between banks and their customers support economic sustainability while enabling sophisticated strategies for both academic scholars and industry practitioners.

Customer Behavior Dynamics: Future research might explore more deeply the specific consumer behaviors and decision-making processes that impact sustainability outcomes. A deeper understanding of these behaviors can help banks create stronger products and strategies.

Technological integration: The effect of digital transformation on the progression of sustainable banking practices needs further examination. Finally, follow-up research might look at whether new fintech solutions in the form of AI-driven advisory services and blockchain-based transparency tools can help banks advance their sustainable development objectives without sacrificing deeper customer involvement.

Cross-cultural studies: Banking and consumer cultures vary across locations; accordingly, conducting cross-cultural research is vital to understanding differences in bank-customer sustainability relationships between different economic, social, and regulatory contexts.

Regulatory Influence: Exploring the role of regulatory policies in catalyzing or impeding collaborative sustainability efforts between bank-consumer alliances may then guide us on how sustainable banking ecosystems are likely to thrive better under different policy frameworks.

Longitudinal Studies: Long-term studies to assess the impact of sustainability initiatives on bank performance and consumer behavior could be helpful. This article could uncover direct evidence of how great or poor sustainability programs work to promote sustainable business in the long term.

Therefore, subsequent research should explore the lasting influence of cooperative sustainability ventures on consumer loyalty and firm performance. Meanwhile, longitudinal studies may offer valuable insights to practitioners and policymakers on this evolving relationship between banks and clients concerning the sustainability dimension.

It is our wish to extend sincere appreciation to every person who has been a part of this work. We are thankful to our academic mentors and colleagues at Lincoln University College who have provided their invaluable feedback and guided us through the course of this project. A big thank you to the banking professionals, customers, and experts involved in sharing their experiences and thoughts about sustainability in banking. The openness in contributing to their insights has enhanced our investigation and solidified the structure of what is presented in this paper. Finally, we thank our friends and family for their continuous support during this research journey.

Appendix A. Format of standardized data extraction

|

Field |

Description |

|

Author(s) |

Full names of the authors |

|

Year of Publication |

Year of publication of the article |

|

Country/Region |

Global and Geographical focus |

|

Study Type |

Empirical (quantitative/qualitative), Conceptual, review, or theoretical |

|

Methodology |

Methodology (e.g., survey, case study, content analysis, interviews) |

|

Conceptual Framework |

The model theory or framework used or recommended |

|

Bank Sustainability Drivers |

Banks Factors of the sustainability within banks inner Factors and outer Factors that affect the sustainability of banks |

|

Customer Sustainability Drivers |

Individual, group, action, and organization factors influence customers |

|

Stakeholder Engagement |

Co-creation, mutual impact, collaboration, Nature of engagement |

|

Major Findings |

Principal results or main contributions of the study |

|

Limitations |

The limitations as reported by the authors or noted during extraction |

[1] Dyllick, T., Muff, K. (2016). Clarifying the meaning of sustainable business: Introducing a typology from business-as-usual to true business sustainability. Organization & Environment, 29(2): 156-174. https://doi.org/10.1177/1086026615575176

[2] Alam, Z., Tariq, Y.B. (2020). Corporate sustainability performance evaluation and firm financial performance: Evidence from Pakistan. SAGE Open, 13(3): 1-19. https://doi.org/10.1177/21582440231184856

[3] Ashwin Kumar, N.C., Smith, C., Badis, L., Wang, N., Ambrosy, P., Tavares, R. (2016). ESG factors and risk-adjusted performance: A new quantitative model. Journal of Sustainable Finance & Investment, 6(4): 292-300. https://doi.org/10.1080/20430795.2016.1234909

[4] Khan, M., Serafeim, G., Yoon, A. (2023). Corporate sustainability: First evidence on materiality. The Accounting Review, 98(1): 235-263. https://doi.org/10.2139/ssrn.2575912

[5] DiMaggio, P.J., Powell, W.W. (1983). The iron cage revisited: Institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(2): 147-160. https://doi.org/10.2307/2095101

[6] Scholtens, B. (2009). Corporate social responsibility in the international banking industry. Journal of Business Ethics, 86(2): 159-175. https://doi.org/10.1007/s10551-008-9841-x

[7] Gallego-Álvarez, I., Rodríguez-Domínguez, L., García-Sánchez, I.M. (2011). Study of some explanatory factors in the opportunities arising from climate change. Journal of Cleaner Production, 19(9-10): 912-926. https://doi.org/10.1016/j.jclepro.2011.02.012

[8] Balarezo, R., Corcuera, P. (2023). Micro-foundations of corporate sustainability. Academy of Management Discoveries. In Knowledge Management for Corporate Social Responsibility. http://doi.org/10.4018/978-1-7998-4833-2.ch015

[9] de Jager, T., Maserumule, M.H. (2021). Innovative community projects to educate informal settlement inhabitants in the sustainment of the natural environment. Sustainability, 13(11): 6238. https://doi.org/10.3390/su13116238

[10] Schaltegger, S., Hansen, E.G., Lüdeke-Freund, F. (2023). Business models for sustainability: Origins, present research, and future avenues. Organization & Environment, 29(1): 3-10. http://doi.org/10.1177/1086026615599806

[11] De los Reyes, G., Scholz, M., Smith, W.K. (2017). Beyond the "win-win": Creating shared value requires ethical frameworks. California Management Review, 59(2): 142-167. https://doi.org/10.1177/0008125617695286

[12] Jaiswal, D., Kaushal, V., Kant, R., Kumar Singh, P. (2021). Consumer adoption intention for electric vehicles: Insights and evidence from Indian sustainable transportation. Technological Forecasting and Social Change, 173: 121089. https://doi.org/10.1016/j.techfore.2021.121089

[13] Nuber, C., Velte, P. (2021). Board gender diversity and carbon emissions: European evidence on curvilinear relationships and critical mass. Business Strategy and the Environment, 30(4): 1958-1992. https://doi.org/10.1002/bse.2727

[14] Yafie, R.I.M.., Zuhroh, I., Anindyntha, F.A. (2020). The impact of green finance on banking performance in Indonesia. Jurnal Aplikasi Akuntansi, 9(1): 288-301. http://doi.org/10.29303/jaa.v9i1.464

[15] Połeć, W., Murawska, D. (2021). The social constraints on the preservation and sustainable development of traditional crafts in a developed society. Sustainability, 14(1): 120. https://doi.org/10.3390/su14010120

[16] Freeman, R.E. (2010). Strategic Management. Cambridge University Press. https://doi.org/10.1017/cbo9781139192675

[17] Freeman, R.E., Harrison, J.S., Wicks, A.C., Parmar, B.L., de Colle, S. (2010). Stakeholder Theory. Cambridge University Press. https://doi.org/10.1017/cbo9780511815768

[18] Połeć, W., Murawska, D. (2021). The social constraints on the preservation and sustainable development of traditional crafts in a developed society. Sustainability, 14(1):120. https://doi.org/10.3390/su14010120

[19] Nasrallah, N., El Khoury, R. (2021). Is corporate governance a good predictor of SMEs financial performance? Evidence from developing countries (the case of Lebanon). Journal of Sustainable Finance & Investment, 12(1): 13-43. https://doi.org/10.1080/20430795.2021.1874213

[20] Freeman, R.E. (2010). Strategic Management. Cambridge University Press. https://doi.org/10.1017/cbo9781139192675

[21] Carroll, A.B., Shabana, K.M. (2010). The business case for corporate social responsibility: A review of concepts, research and practice. International Journal of Management Reviews, 12(1): 85-105. https://doi.org/10.1111/j.1468-2370.2009.00275.x

[22] Schoenmaker, D., Schramade, W. (2019). Principles of Sustainable Finance. Oxford University Press.

[23] Arksey, H., O’Malley, L. (2005). Scoping studies: Towards a methodological framework. International Journal of Social Research Methodology, 8(1): 19-32. https://doi.org/10.1080/1364557032000119616

[24] Levac, D., Colquhoun, H., O’Brien, K.K. (2010). Scoping studies: Advancing the methodology. Implementation Science, 5: 69. https://doi.org/10.1186/1748-5908-5-69

[25] Braun, V., Clarke, V. (2006). Using thematic analysis in psychology. Qualitative Research in Psychology, 3(2): 77-101. https://doi.org/10.1191/1478088706qp063oa

[26] Lin, W.L., Mohamed, A.B., Sambasivan, M., Yip, N. (2019). Effect of green innovation strategy on firm-idiosyncratic risk: A competitive action perspective. Business Strategy and the Environment, 29(3): 886-901. https://doi.org/10.1002/bse.2405

[27] Murè, P., Spallone, M., Mango, F., Marzioni, S., Bittucci, L. (2020). ESG and reputation: The case of sanctioned Italian banks. Corporate Social Responsibility and Environmental Management, 28(1): 265-277. https://doi.org/10.1002/csr.2047

[28] Xu, B., Zhong, R., Hochman, G., Dong, K. (2019). The environmental consequences of fossil fuels in China: National and regional perspectives. Sustainable Development, 27(5): 826-837. https://doi.org/10.1002/sd.1943

[29] Fatmasari, D. (2018). Effectiveness and ease of use of BSI mobile as implementation green banking. Journal of Information Systems Engineering & Management, 10(49s): 308-316. http://doi.org/10.52783/jisem.v10i49s.9876

[30] Li, N., Jiang, Q., Wang, F., Cui, P., Xie, J., Li, J., Wu, S., Barbieri, D.M. (2021). Comparative Assessment of asphalt volatile organic compounds emission from field to laboratory. Journal of Cleaner Production, 278: 123479. https://doi.org/10.1016/j.jclepro.2020.123479

[31] Bowman, C., Ambrosini, V. (2010). How value is created, captured and destroyed. European Business Review, 22(5): 479-495. https://doi.org/10.1108/09555341011068903

[32] Denbee, E., Julliard, C., Li, Y., Yuan, K. (2021). Network risk and key players: A structural analysis of interbank liquidity. Journal of Financial Economics, 141(3): 831-859. https://doi.org/10.1016/j.jfineco.2021.05.010

[33] Samuel, A, Yeboah, S,A. (2023). Investing with purpose: Unveiling the potential of impact investing in developing nations.

[34] Hunt, K, Lamandini, M., Muñoz, D.R. (2019). Nudging inclusive banking and micro finance towards self-sustainability. In Research Handbook on Law and Ethics in Banking and Finance. http://doi.org/10.4337/9781784716547.00013

[35] Bui, B., Houqe, M.N., Zaman, M. (2021). Climate change mitigation: Carbon assurance and reporting integrity. Business Strategy and the Environment, 30(8): 3839-3853. https://doi.org/10.1002/bse.2843