Galad Mohamed Barre![]()

© 2024 The author. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The main objective of this study is to understand the level of awareness and green banking practices in Somali banks. This study focuses on the level of awareness of green banking practices, daily operations, investments, and banking policies related to green banking in Somalia. This study adopted a quantitative research method by using descriptive analysis. An adopted and self-administered questionnaire was distributed to 226 Somali bank employees. Convenience sampling was used to select the respondents and data was analyzed by employing Statistical Package for the Social Sciences (SPSS) 23. It was found that Somali bank employees have a poor level of awareness about green banking practices. Daily operations in green banking, investments in green banking, and banking policies related to green banking all showed low levels of green banking practices. As long as the majority of respondents claimed their banks don't offer any green products, it was also discovered that Somali banks only offer a small number of green products. The results of this study will help government officials and bank executives in Somalia in reducing climate change risk and eventually promoting environmental sustainability and sustainable banking practices. By raising awareness of green banking practices in Somalia, the survey adds to the literature.

green banking awareness, daily bank operations, investment in green loans, banking policies, Somalia

Development and acceptance of a more sustainable strategy for human everyday activities are required in light of the deterioration of climate change, which is linked to unsustainable behaviors [1]. Due to the fact that climate change has been one of the most pressing concerns in the globe for the past few decades, numerous efforts have been undertaken to reduce the risk of climate change and make the planet habitable. We are always taken care of by nature since we are born, raised, and created by it [2]. However, in reaction to these natural bounties, humans are damaging the environment in many ways, including by chopping down trees, polluting the air and water, and testing nuclear energy as a representation of scientific growth and the Industrial Revolution. Thus, nature exacts vengeful retaliation through a variety of catastrophes like storms, floods, droughts, earthquakes, extreme heat, and melting ice. When faced with such horrific natural retribution, many individuals throughout the world work to raise public awareness and inspire us to seriously consider global warming, its effects, and possible solutions in order to make the planet habitable and embrace eco-friendly policies. It emphasizes the importance of ecological sustainability and the need to adopt eco-friendly policies to avoid the adverse effects of global warming and other natural calamities [2].

Green finance refers to financial products and services that support sustainable growth while reducing the impact of economic activities on the environment. It includes investment in renewable energy, energy efficiency, sustainable agriculture, forestry, and other environmentally friendly projects. Green banking refers to the adoption and implementation of green finance principles and practices by banks [3]. Another paper indicates that the green banking adoption in Pakistan is initial stages and the banks proactively engage in green banking adoption which will benefit competitive pre-emption [3]. The Somali people mainly participate in climate change via degrading forest deforestation [4]. Therefore, there is substantial influence over multiple stakeholder groups, which can help make the world’s future truly green.

The Bank, which is regarded as the foundation of an economy, affects environmental sustainability both directly and indirectly [2]. Although the banking sector has historically been seen as environmentally benign, banks' carbon footprint has significantly expanded in recent years due to their extensive energy usage (lighting, air conditioning, computers), limited space, haphazard construction, and disregard for in-house sustainability. Consequently, banks are encouraged to employ eco-friendly technology, environmentally friendly products, novel procedures, and strategies to reduce carbon footprints and ensure a sustainable environment. Due to the importance of banks to the economy, businesses must adopt a more sustainable strategy [1]. The process of using financial services and products to foster a successful environment is known as sustainable banking [5]. There are a small number of banks that are using this strategy [6, 7]. Despite consumers' desire for more sustainable business models [8].

Green banking focuses on two aspects: the greening of internal operations through the use of renewable energy, digitization, and other strategies that can cut down on carbon emissions from banking activities, and the use of environmentally friendly financing such as sustainable banking, ethical banking, green mortgages, green loans, green credit cards, mobile banking, online banking, etc [9]. Additionally, banks throughout the world utilize energy-efficient Green Machines that get their power from emission-free sources like wind power and make significant investments in local environmental and wildlife programs in their neighborhood [10]. Even by the norms of sub-Saharan Africa (SSA), according to assessments from both international and national organizations, Somalia receives relatively little funding for climate change [11]. According to line ministries like the Ministry for Disaster Management and the National University of Somalia, climate financing is the most crucial input for addressing climate change, yet it is mostly absent or at extremely low levels in Somalia [11]. To adjust Somalia's sensitivity to climate change and its financial institutions' practices, a thorough grasp of green finance is essential. Given that relatively little funding has been committed to assisting adaptation initiatives, Africa's susceptibility to climate change raises a demand for national and local governments to support adaptation measures [12].

In the Somali context, the Somali government has severe budgetary constraints when it comes to efforts to adapt and mitigate the changing environment as they have other big priorities such as securities and other sectors. Thus, financial institutions are therefore crucial for funding climate change and helping directly and indirectly to mitigate climate challenges. Although Somalia is experiencing significant climate change, the banking sector is not ready to adapt to and mitigate environmental hazards concerns. There are still no policies in place to reduce the negative impact of climate change on the country's banking industry [13]. This might be because of weak governance institutions[14]. According to Barre et al. [4], even though over 75% of Somali bank employees are aware of and prefer green finance, the banks do not provide their customers with any green finance investment and the majority of employees see green finance as essential for their lives. In addition, they suggested that Somali commercial banks offer green funding to attract more new clients and retain existing ones.

Although a lot of research has already been conducted in developed and even developing countries, there is still a long way to go in Sub-Saharan Africa, particularly Somalia, to achieve the greatest success regarding green baking and environmental sustainability issues because the majority of the population in the country is not that aware of it. There is only one study that has studied the awareness and preference of green finance in commercial banks in Somalia [4]. However, this study examines both the direct use of renewable energy, digitization, and other strategies that can cut down on carbon emissions from banking activities and the indirect effects of the use of environmentally friendly financing such as sustainable banking, ethical banking, green mortgages, green loans, green credit cards, mobile banking, online banking. In addition, the study has a substantial justification from both regulators and bank management. To the best of my knowledge, this study is the first to examine the direct and indirect effects of Somali banks on the environment. There seems to be no visible study that explores the awareness of green banking, daily operations, investments, and banking policies related to the green banking and environmental sustainability of Somali banks. In general, this study aims to understand the level of awareness and green banking practices in Somali banks. The study specifically aims to achieve the following objectives:

To identify the policies of banks towards green financing such as setting up green branches, promoting an environmentally friendly policy at the corporate level, and environmental-related agreements with relevant parties.

2.1 The need for green banking worldwide

The green banking idea has been described as a strategy to advance environmentally friendly banking practices, which attempts to minimize carbon footprint and to attract clients based on these distinctive practices [15]. However, the green banking idea is a stakeholder effort for a healthy environment and is not simply a concern of one party [16]. In terms of green banking applications, the philanthropic approach dominates the prior literature, although there is still no agreement on a single, comprehensive definition. Numerous academics agree that the advantages of green banking are for the greater good of society and are the driving force behind the expanding environmental effect [17]. The study argued that the concept of "green banking" not only promotes social responsibility but also considers responsibility by assessing a project's potential effects on the environment before funding [18]. Multiple studies have also backed green banking's social and environmental implications [19, 20].

According to another study, green banking is an ethical banking concept that emphasizes environmental conservation and encourages social and environmental responsibility by offering environmentally friendly financial services [18]. However, developed, developing, and underdeveloped countries typically take various approaches to green banking legislation [16]. To codify environmental policy under the control of central banks and regulators, several developing countries have established mandatory rules. For financing industries with sensitive climatic needs, India, for instance, imposed particular limitations. However, developed countries have adopted a voluntary approach to an industry-driven strategy to handle the financial risk associated with the environment as a component of maintaining a quality environment.

The devastating effects of human innovations on earth ecology began to become clear and widely recognized in the early 1980s [3]. Many academics, thought leaders, and decision-makers began establishing the foundation for the current green movement [21]. The worldwide banking industry has begun a corrective and control plan known as "Green Banking" as a result of realizing its obligation and accountability towards resource depletion and the environment [22]. Green banking is becoming more and more popular around the world, both as a component of the traditional banking system and as a stand-alone financial organization in the form of wholly green banks like the Connecticut Green Bank and the New York Green Bank [3]. However, similar to the bulk of green management initiatives, there is a considerable difference between the acceptance of green banking in both developed and developing countries. According to a study, 93 banks spent €232 billion on coal finance between 2005 and 2010 [23]. Therefore, banks have a negative direct and indirect influence on the environment.

The positive impact of Green banking practices is seen by businesses as a crucial strategy for establishing a favorable reputation and aiding in staff retention [24]. Similarly, Riffat et al. [25], argued that green banking improves relationships between businesses, clients, and the government. Another study found that green banking has a big impact on stakeholders' investment choices [26]. Similarly, this study demonstrates how green banking is concerned with the welfare of the community in which it works [2]. The adoption of energy-efficient practices in everyday banking operations and the promotion of E-banking practices to cut the cost of operations in solid forms, such as paper, are recognized as green banking in the daily operations of banks [27].

Green banking requires corporate strategies that put a higher emphasis on social and economic growth in a clean environment [28]. According to the findings of the following studies, the bank now holds everyday operations accountable for the environment, which reduces carbon footprints [29, 30]. Green banking practices are praised by researchers for their various advantages, including their contribution to reducing internal and external risk as well as their improvement of bank image and source of competitive advantage [31]. The research uses data from 713 institutions across 75 countries from 2013 to 2015 to assess the impact of environmental financing and access to finance on the financial performance of the industry internationally [32]. Their findings point to the positive effects of financial access on banks' financial performance as measured by managerial quality and loan expansion. Nevertheless, despite all the advantages, the adoption of green finance is still in its infancy stage in developing economies. These have the effect of decreasing the amount of interest in clean energy projects and the cost-effectiveness of adopting green banking practices [33]. Additionally, a different study carried out in 50 European bank samples indicated that only management topics had a positive correlation with environmental and sustainability performance, but not risk management techniques [34]. This confirms research findings that suggested a positive impact on financial growth through loan growth and management quality [32].

However, other studies indicated that green banking aims to lessen banks' negative direct and indirect environmental impacts by promoting effective strategies to change everyday internal operations and promote green investment initiatives [16]. Using data from the years 2008 to 2017, a study examined the sustainability of the Islamic banking paradigm [35]. Their findings demonstrated a strong correlation between sustainability practices and the financial success indicators of Islamic banks as well as shareholders' viewpoints. However, they discovered a negligible financial performance from a market standpoint. This study argued that green practices in the banking industry have been sparked by their potential negative role in the degradation of the global environment and the depletion of natural resources [3]. They added that many banking operations in the natural environment are potentially harmful, posing negative effects both indirectly and directly. Their study tracks Pakistan's banking sector's transition to green banking. They stressed how important it is for emerging economies to implement green banking. Due to the traditional banking ideology's direct and indirect negative effects on the environment, green banking has emerged [36]. However, with the International Finance Corporation (IFC)'s effort and the creation of the Sustainable Banking Network (SBN) to support green banking in poor countries, the adoption of green banking practices in particular gained considerable importance in 2012 [3]. Therefore, 15 of the 35 countries, have effectively started national guidelines, principles, and policies concerning green banking practices. Due to its direct and indirect negative effects on the environment, the banking sector is one of the most significant stakeholders and areas of interest for those involved in the green banking concept [16]. In contrast to direct consequences, however, banks' indirect effects are a big concern [37]. Banks are regarded as the primary source of financing for the sector in developing countries. According to data, foreign banks funded the coal industry with more than 220 million pounds between 2005 and 2010 [16]. However, Ikram et al. [38] recommended that adopting Quality Environment and Social (QES) standards had a noticeably favorable impact on exports of products and services, particularly in developing countries. This study also suggested that to promote the use of mobile banking, banks should put more effort into improving the convenience of online transactions [39].

2.2 The need for green banking in Sub-Sahara Africa

Sub-Saharan Africa (SSA)is in a unique position to reap the socio-economic and environmental benefits of renewable resources, and the energy efficiency practices as the demand for energy in the continent grows [40]. According to Doku et al. [41] the SSA countries are not developed enough and neither receive sufficient climate funding to address the challenges arising from climate change. Given the severe poverty and lack of development, the region heavily relies on agriculture but above 600 million people in Africa lack the necessities such as water and electricity [42]. In the Horn of Africa, the livestock and agricultural subsectors have suffered greatly in recent decades due to severe environmental degradation of the region's forest regions and climate change [14]. As mentioned above the Somali people mainly participate in climate change via degrading forest deforestation [4]. By the late 1980s, nearly all of Somalia's floodplain woods had been eradicated to make way for irrigated farmland. In 2014, just 10% of the country's surface area was covered by forests, down from 62% in 1980 [43]. The study also found, that since 1990, The woods of Somalia have lost an average of 1% of their area annually. The primary reason for widespread the unsustainable plucking of acacia trees for the manufacturing of charcoal has contributed to deforestation. Where their yearly shipments of charcoal reached their pinnacle in 2011 at $56 million in Somalia [43]. Additionally, the cumulative impacts of several poor rainy seasons have decreased grain output, which has resulted in a dire humanitarian crisis that became a famine in many areas of Somalia in 2011, 2017, and 2022 [44]. Figure 1 illustrates how environmental deterioration, as measured by deforestation, was steady in Somalia between 1990 and 2001. It began to rise in 2001 and peaked in 2005 mostly as a result of Somalia's expanding charcoal export business, which was primarily fueled by massive deforestation. From 2006 through 2013, it fluctuated, but starting in 2014, it stayed the same. The earth's surface temperature rises as a result of agricultural CH4 emissions, which include those from burning agricultural waste and those from the production of rice and animal manure. Figure 1 illustrates a rising trend in Somalia from 1991 to 2005. It subsequently started to decline until 2008 before starting to increase once more in 2009. In conclusion, environmental deterioration and pollution in Somalia are very dynamic and may hurt the country's agricultural output.

Somalia faces significant deforestation [43]. It involves a lack of current understanding, a dearth of global measuring tools, and a focus on the context and use of technology in a specific country. Thus, the majority of Somali banks are not even aware they could have an indirect negative impact on the environment by financing companies that are working in the charcoal industry. A lot of people turned to charcoal as gas prices rose in Somalia as an affordable energy source.

Figure 1. Environmental pollution and degradation in Somalia

Data source: World Bank, (2022).

2.3 Theoretical perspective

According to a theoretical standpoint, this serves as a starting point. Any investment approach that aims to include both financial return and social/environmental benefit to bring about social change is known as socially responsible investing (SRI). According to Chatzitheodorou et al. [45], it has been asserted that several terms, including ethical, social, sustainability, and investments, have been interlaced into the reasoning behind SRI theory. It has been said that SRI theory emphasizes individual values and societal well-being as crucial factors to take into account when evaluating investment options [46]. According to Newell and Lin Lee [47], SRI theory was perceived as advocating the use of both financial and well-being goals, particularly among microfinance institutions and socially motivated businesses, to combat the growing environmental challenges, create employment, and advance rural and urban development. According to another study, SRI theory employs finance with a social orientation to concurrently advance financial and social objectives and goals [47, 48]. However, according to Browner et al. [49], it has been suggested that owing to obstacles including a lack of paperwork and the usage of green energy, banks have limited information accessible to them in their investments in green initiatives. This can deter banks from making investments. But today's customers have higher expectations since they can identify additional uses for the money they put in and want to see more social good. As banks close, they dramatically affect the environment in both direct and indirect ways [50]. Banks, however, do not have access to enough information and data to support the implementation of green banking. Thus, this study aims to examine the direct and indirect effects of Somali banks on the environment in terms of awareness, daily operations, investments, and strategic policies in the bank system of Somalia, to fill out the empirical gap in the existing body of the literature.

In the current study, quantitative research and a survey methodology were applied. The information was gathered from the employees of 13 licensed Somali banks. A questionnaire was used to acquire the data for this study. The survey was delivered via a Google document form, and shared via social media sites including Facebook, WhatsApp, and email addresses of respondents. Each respondent was only given one opportunity to complete the survey. The respondents had to work for a Somali bank and, at the very least, be literate in reading, writing, and understanding English when the respondents were picked by the researchers. When distributing the survey questionnaire, the English language is utilized as the primary language. The study's sample size was 300, however, after removing all incomplete replies, 226 responses were still valid. This suggests that the study's response rate was 75.33 percent. The data was collected from April to June 2023. In this study, a convenient random sample is used to collect data. This sampling technique is widely used for primary data sets and is a cost-effective method for collecting the data. Additionally, convenience sampling is regularly used in previous research [51-54]. According to Shaikh et al. [54], convenience sampling is more prevalent in financial study. This sampling approach is popularly utilized for primary data sets and is an economical way to gather the data [51]. As a consequence, the authors used this sample strategy. The questionnaire uses a five-point Likert scale (1 being strongly agree, and 5 being strongly disagree) to evaluate the replies to the items. The reliability and validity of the data have been tested to check the quality of constructs, and all constructs have passed the necessary threshold of 0.70 [55]. Therefore, the result of this study is reliable. This study has used descriptive statistics as a method for data analysis the main reason is that is the most appropriate method as long as this study wants to find out number of people who aware the green banking practices, the Daily Operations, the Green Project Investments, and the Bank Policy in Somalia and other study uses same data analysis method as follows [56].

In this study, all the variables are adopted from previous studies related to green banking that had already been tested and verified. All of the Daily Operations, Green Project Investments, and Bank Policy Related Practices variables have been adopted by Rehman et al. [16], whereas the green banking awareness variables are self-created questions.

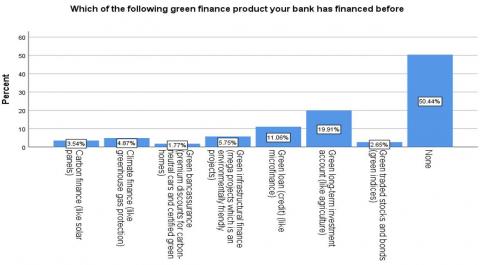

Table 1 provides a summary of the demographic part of the study. The data indicates that 67.7% of the respondents are men and 32.3% are women. Only 5.8% of respondents are beyond the age of 35, with 46.9% of respondents being between 20 and 25 and 47.3% between 25 and 35 years old. According to their degree of education, graduates make up the majority of respondents (71.9%). In terms of their marital status, 63.3 percent were single and 48.6 percent were married. Just 26.5 respondents had more than five years of experience, compared to 38.9% who have between three and five years, 34.5 percent with less than a year, and 34.5 percent with more than five years. Figure 2 shows that the majority of respondents just over 50 percent of the respondents said their bank does not provide any of the green finance products as laid out in Figure 2. Green long-term investment accounts (like agriculture) product that respondents think their bank finances, with 19.91 percent. The second product, which accounts for 11.06 percent, is a green loan (credit). As you can see in Figure 2, the other green financing products that Somali bank employees believe are available in their banks are less than double digits. Thus, this indicates that Somali banks mainly do not offer green financing products to their employees, or they offer negligible investments such as agricultural financing.

Table 1. Respondents profile

|

Variable |

Frequency |

Percent (%) |

|

Gender |

|

|

|

Male |

153 |

67.7 |

|

Female |

73 |

32.3 |

|

Age |

|

|

|

20 - 25 years |

106 |

46.9 |

|

25 - 35 years |

107 |

47.3 |

|

Above 35 |

13 |

5.8 |

|

Education Level |

|

|

|

Graduate |

176 |

77.9 |

|

Undergraduate |

40 |

17.7 |

|

High school |

2 |

0.9 |

|

Other |

8 |

3.5 |

|

Marital status |

|

|

|

Single |

143 |

63.3 |

|

Married |

83 |

36.7 |

|

Working experience |

|

|

|

Less one year |

78 |

34.5 |

|

3-5 years |

88 |

38.9 |

|

Above 5 years |

60 |

26.5 |

Figure 2. Green finance products

Assessing Somali bank employee awareness of green finance is the first step in the study. Table 2 presents the results. More than 52.2 percent of respondents strongly disagreed or disagreed with the first statement "I have general knowledge about green finance," meaning that the majority of bank employees in Somalia do not have a general understanding of what green finance entails. The second statement, "Generally speaking, I have already acquired enough knowledge about green finance," the majority of respondents gave negative responses (56.2 percent), indicating that the employees lacked general knowledge of what green finance is all about. The third statement, "I have enough information about the advantages of providing green finance" 61 percent of employees either strongly disagree or disagree with the statement, which shows that staff do not receive enough knowledge on the benefits of offering green products to bank clients. fourth statement “I have learned about green finance from media sources." Among the responses, 50% strongly disagree or disagree with such assertion, while 31% strongly agree or agree with that statement. Therefore, the result of this study is in contrast with the study of Barre et al. [4] who found that more than 75% of Somali bank employees are familiar with green finance. Similarly, the result of this study also contradicts the following study conducted in Nigeria which indicates a higher level of awareness of green finance [57]. However, the study revealed that there is a low level of implementation of green finance practices in infrastructure development in Nigeria. Thus, a high level of awareness does not lead to a high level of implementation of green finance practices Nigeria. Last but not least, more than 51% of respondents strongly disagree or disagree with the statement that "I am concerned about green finance," indicating that they are not concerned about the risk of climate change and environmental challenges, whereas fewer than 20% claim they are. Hence, Somali people are less concerned about climate change which indicates the low level of awareness of the risk climate change could bring on them. Furthermore, Cronbach's alpha was used in reliability testing. The quality of construct dependability was tested, and the findings indicate a score of 0.752, which is higher than the necessary threshold of .70 [55]. Therefore, the result of this study is reliable.

Table 2. Level of awareness in green finance

|

No. |

Statement |

1 |

2 |

3 |

4 |

5 |

Cronbach's Alpha (α) |

Mean |

Std. Dev. |

|

1 |

I have general information about green finance |

12.4 |

8.0 |

27.4 |

36.7 |

15.5 |

0.752 |

3.35 |

1.20 |

|

2 |

Generally speaking, I have already acquired enough knowledge about green finance |

4.9 |

11.1 |

27.9 |

39.8 |

16.4 |

3.52 |

1.04 |

|

|

3 |

I have received enough information about benefits of offering green finance |

6.6 |

10.2 |

22.1 |

42.0 |

19.0 |

3.57 |

1.11 |

|

|

4 |

I have received information about the green finance from media sources |

7.1 |

23.9 |

19.0 |

38.5 |

11.5 |

3.23 |

1.14 |

|

|

5 |

I am concerned about climate change |

9.3 |

10.2 |

28.8 |

37.6 |

14.2 |

3.37 |

1.133 |

1= strongly agree (%), 5= strongly disagree (%)

The second section of the study studies how Somali banks conduct their daily operations in terms of green finance. Table 3 presents results. The first statement "My bank has initiatives to reduce paper usage and other wastage of materials" by more than half of respondents strongly disagreed or disagreed. Thus, the majority of Somali bank employees feel that their institutions do not limit paper consumption and other waste products that might harm the environment to lessen the danger of climate change, even though only approximately 30% of Somali bank employees agree or strongly agree with the statement. In the second statement, the majority of respondents (more than 53%) disagree or strongly disagree with the statement that "My bank has introduced energy-efficient equipment, system solutions, and practices," indicating that the staff do not feel their banks do so. Nevertheless, only roughly 21% of people strongly or somewhat agree with the statement. Third, the majority 46 percent of employees disagree or strongly disagree with the statement that "My bank uses e-waste management practices," meaning that they believe their banks do not use e-waste management to help reduce environmental issues. Only 31% of employees say their banks do use some form of e-waste management. forth, the statement argued that "My bank has environmentally friendly banking practices (e-mail, intranet, e-statements, online approval system, etc.)" Only 14 percent of respondents agreed or strongly agreed with this claim, with a majority of more than 67 percent, indicating that Somali bank employees do not feel their institutions follow environmentally friendly methods. The fifth statement says "My bank encourages customers to use environmentally friendly banking practices (e-statements, online transfer, etc.)" The majority of respondents roughly 70% strongly disagree or disagree with that statement, while just over 14% agree or strongly agree, showing that Somali bank employees do not believe their institutions encourage their clients to adopt environmentally friendly practices. Six statements, the majority of employees (over 55 percent) strongly disagree or agree with the statement that "My bank regularly arranges seminars workshops to promote environment-friendly practices in daily operations," while only slightly more than 23 percent agree or strongly agree with it. This indicates that Somali bank employees believe their banks do not provide seminars and workshops related to the importance of the environment to increase environmental awareness. Finally, the statement "My bank encourages employees to communicate through digital connectivity" received almost 70% of respondents who disagree or strongly disagree, indicating that Somalian banks do not take into account how their employees interact and whether to use an environmentally friendly method or not. Therefore, bank personnel may not use digital communication. Overall, the daily operations of green finance in Somalia show that the Somali banks do not daily practice green finance activities which is consistent with previous studies [16, 29]. In addition, Cronbach's alpha was used in reliability testing. The findings indicate a score of 0.713, which is higher than the necessary threshold of .70 [55]. Thus, the result of this study is reliable.

Table 3. Daily operations

|

No. |

Statement |

1 |

2 |

3 |

4 |

5 |

Cronbach's Alpha (α) |

Mean |

Std. Dev. |

|

1 |

My bank has initiatives to reduce paper usage and other wastage of materials. |

15.5 |

14.6 |

19.9 |

31.0 |

19.0 |

0.713 |

3.23 |

1.33 |

|

2 |

My bank has introduced energy-efficient equipment’s, system solutions and practices. |

7.1 |

14.6 |

25.2 |

34.5 |

18.6 |

3.43 |

1.15 |

|

|

3 |

My bank uses e-waste management practices. |

11.5 |

19.5 |

23.0 |

34.5 |

11.5 |

3.15 |

1.20 |

|

|

4 |

My bank has environmental friendly banking practices (e-mail, intranet, e-statements, online approval system, etc.). |

5.3 |

8.8 |

18.6 |

38.1 |

29.2 |

3.77 |

1.12 |

|

|

5 |

My bank encourages customers to use environmental friendly banking practices (e-statements, online transfer etc.). |

6.6 |

8.0 |

16.4 |

35.8 |

33.2 |

3.81 |

1.17 |

|

|

6 |

My bank regularly arranges seminars workshop to promote environment friendly practices in daily operations. |

10.2 |

13.7 |

20.8 |

35.4 |

19.9 |

|

3.41 |

1.23 |

|

7 |

My bank encourage employee to communicate through digital connectivity. |

4.4 |

8.4 |

21.2 |

41.6 |

24.3 |

3.73 |

1.05 |

1= strongly agree (%), 5= strongly disagree (%)

The third section of the study looks at the investments or loans that Somali banks provide in green initiatives. Table 4 presents the findings. The first statement, "My bank provides loans to environmental protection and energy-saving related projects," is strongly disagreed or disagreed with by the majority of respondents (approximately 54 percent). While just slightly more than 25% of Somali bank workers agree or strongly agree with the statement. Thus, this indicates that the majority of them think their local banks do not offer sufficient finances and loans to mitigate the community's risk from climate change. Second, a majority of respondents with more than 45 percent strongly disagree or disagree with the statement, which is that "My bank implements certain independent and unique green initiatives, projects, etc. (e.g., tree planting)" While around 26% of employees strongly agree or agree with the statement. Hence, they think their banks do not take green measures like planting trees to mitigate environmental concerns. Third, the majority of employees, approximately 60%, disagree or strongly disagree with the statement that "My bank promotes and facilitates environmentally oriented enterprises through special grants, loans, and guidance," thus, this indicates that the employees do not believe their banks offer special grants and loans to promote environmental friendly enterprises. However, just over 16% of employees agree or strongly agree with the statement. Fourth, the majority of respondents 54 percent disagree or strongly disagree with the statement that "My bank uses social and environmental management systems or any other mechanisms to evaluate all project proposals," while just over 22 percent agree or strongly agree with it. Therefore, this shows that Somali bank employees feel their banks do not use any mechanisms to evaluate the proposals by checking how they are environmentally friendly proposals. Fifth, the majority of respondents 53.6 percent disagree or strongly disagree with the statement "My bank promotes and facilitates environmental-oriented guidance to promote green projects," while just over 20 percent agree or strongly agree. Thus, this finding suggests that Somali bank employees do not believe their institutions support and facilitate environmentally friendly projects. Finally, the majority of employees over 50% strongly disagree or strongly disagree with the statement that "My bank promotes and facilitates credit line to green projects," whereas just over 22% agree or strongly agree with it. Therefore, this finding shows that Somali bank employees believe their institutions do not provide special credit lines to encourage green projects to address environmental challenges. Overall, the result of this section of investments and loans that Somali banks provide in green finance initiatives indicated that they less care to invest and loan money to promote green investment with is consistent with previous study [29]. likewise, Cronbach's alpha was used in reliability testing, and the findings revealed 0.751, which was higher than the necessary threshold of .70 [55]. Therefore, the result of this section is reliable.

Table 4. Investments in green projects

|

No. |

Statement |

1 |

2 |

3 |

4 |

5 |

Cronbach's Alpha (α) |

Mean |

Std. Dev. |

|

1 |

My bank provides loans to environmental protection and energy saving related projects. |

8.4 |

16.8 |

20.8 |

37.2 |

16.8 |

0.751 |

3.37 |

1.19 |

|

2 |

My bank implements certain independent and unique green initiatives, projects, and etc. (e.g. tree planting). |

8.8 |

18.1 |

27.9 |

34.1 |

11.1 |

3.20 |

1.13 |

|

|

3 |

My bank promotes and facilitates environmental oriented enterprises through special grants, loans, and guidance. |

3.5 |

12.8 |

25.7 |

42.5 |

15.5 |

3.54 |

1.01 |

|

|

4 |

My bank uses social and environmental management system or any other mechanisms to evaluate all project proposals. |

8.4 |

13.7 |

23.5 |

34.5 |

19.9 |

3.44 |

1.19 |

|

|

5 |

My bank promotes and facilitates environmental oriented guidance to promote green projects. |

8.0 |

12.4 |

26.1 |

38.1 |

15.5 |

|

3.41 |

1.13 |

|

6 |

My bank promotes and facilitates credit line to green projects. |

8.4 |

14.2 |

26.5 |

37.6 |

13.3 |

3.33 |

1.13 |

1= strongly agree (%), 5= strongly disagree (%)

The study's fourth section examines the banks' environmental practices about strategic policies. Table 5 presents the findings. About 51% of respondents strongly disagreed or disagreed with the first claim, which says "My bank participates in the establishment of green branches (energy-efficient buildings/green buildings)". Thus, the majority of the Somali bank employees suggest that their institutions are not opening green branches to contribute to the mitigation of climate change, which might result in environmental disaster, compared to just over 20% who agree or strongly agree with the statement. Second, the statement that "My bank has an environmental (green) policy" similarly by more than 52% of respondents strongly disagreed or disagreed and only 19% of employees agree or strongly agree with the statement. Thus, this indicates that they don't think their banks have environmental policies in place to reduce or adopt environmental hazards. Third statement claimed "My bank has environmental-related agreements with relevant parties/ stakeholders (suppliers, customers, etc.)" The majority of employees 58 percent strongly disagree or disagree with. Therefore, this means the employees think their banks do not have an agreement with their stakeholders, including suppliers, customers, and others, that relates to the environmental protection. Fourth, just over 54 percent of respondents disagree or strongly disagree with the statement that "In my bank, head office level or top management involves environmental protection-related planning and implementation," while just over 20 percent agree or strongly agree. Therefore, this shows that Somali bank employees feel that the top management of the banks are not planning to implement environmental protection plans. Fifth statement says "My bank promotes an environmental friendly policy at corporate level," the majority of respondents disagreed or strongly disagreed with it in a ratio of just over 62 percent. Hence, this indicates that Somali bank employees do not believe their institutions are encouraging or promoting environmental policies at the corporate level. Final statement says "My bank purchases its office supplies, technology, and other items from environmentally friendly companies (such as printers, computers, etc.)" Over 55% of employees strongly disagree or disagree with this statement, compared to just over 17% who agree or strongly agree. Therefore, this shows the Somali bank employees believe their institutions are not buying stationeries from environmentally friendly companies to promote environmental protection. Overall, the result of this study shows that the Somali banks do not have any strategic policies toward green finance which is consistent with the previous studies [29, 16]. Furthermore, Cronbach's alpha was used in reliability testing and the findings revealed 0.727, which was higher than the necessary threshold of .70 [55]. Therefore, the results of this section are reliable too.

Table 5. Banks policy related practices

|

No. |

Statement |

1 |

2 |

3 |

4 |

5 |

Cronbach's Alpha (α) |

Mean |

Std. Dev. |

|

1 |

My bank involves in setting up green branches (energy-efficient buildings/ green buildings). |

5.5 |

14.6 |

31.9 |

32.1 |

15.9 |

0.727 |

3.55 |

1.21 |

|

2 |

My bank has an environmental (green) policy. |

6.6 |

12.4 |

28.3 |

35.0 |

17.7 |

3.55 |

1.11 |

|

|

3 |

My bank has environmental-related agreements with relevant parties/ stakeholders (suppliers, customers, etc.). |

8.0 |

10.2 |

24.3 |

38.1 |

19.5 |

3.55 |

1.15 |

|

|

4 |

In my bank, head office level or top management involves environmental protection-related planning and implementation. |

8.8 |

11.9 |

23.0 |

33.2 |

23.0 |

3.55 |

1.21 |

|

|

5 |

My bank promotes an environmental friendly policy at corporate level. |

7.5 |

9.3 |

20.4 |

46.0 |

16.8 |

3.55 |

1.10 |

|

|

6 |

My bank purchases its stationeries, equipment’s and other items from environmentally friendly companies (e.g. printers, computers, etc.) |

7.1 |

10.6 |

26.5 |

33.6 |

22.1 |

|

3.53 |

1.15 |

1= strongly agree (%), 5= strongly disagree (%)

The study aimed to examine green banking practices in Somali banks. Data were analyzed by using descriptive statistics research design in order understand the awareness and level of green banking practices in Somali banks. the reliability of the data with employing by using Cronbach alpha and all constructs has passed the required threshold 0.70 [55]. The SPSS is used as tool to analysis data to find out the level of green banking practices by Somali banks of the variables of this research study including level of awareness, daily bank operations, Investments in green projects and the bank policies related environmental practices. Although different strategies have been initiated to promote environmentally friendly business practices, but in Somalia there is no clear strategies relates to environmental protection that have been implemented so far. Some developing countries have implemented green banking initiatives although it is on initial stages. For instance, online banking, paying online bill facilities, and other financia l transactions, encouraging online digital activities, are few of the banking technologies contributing to the green environment that have been implemented in Pakistan and other countries [16]. In Somalia, there is no clear strategies relates to environmental protection that have been implemented so far. However, online banking, paying online bill facilities, online digital activities and other financial transactions are their intial stages. In Somalia, like in most of Eastern Africa, major climate-related calamities are occurring [11]. Because the country depends on climate-sensitive industries like livestock and grain production, this has a significant impact on the people’s livelihood.

First, regarding the level of awareness in green banking activities, a recent study by Javelin Strategy and Research estimates that about 53% of customers want to belong to the banks that have the authority to instigate positive actions for the environment and society, so the banks must be certain about their responsibility toward the environment for the sustainable financial reward and success [58]. Although, the Somali bank employees have very low levels of understanding for green finance since the majority of respondents either knew nothing about it or knew very little about green finance as the result of the study indicates. Therefore, it is needed to increase the level of awareness of green finance and to explain the important of green banking to the Somalis to ultimately to contribute the environmental protection of the country.

Second, in terms of daily bank operations, the findings of this study indicates that Somali banks few relatively operate on a daily basis that are engaged in green banking activities, because most employees think their banks don't regularly engage in green banking activities. The results of this study is consistent with Rehman et al. [16], who found that traditional banks' day-to-day operations are unrelated to the environment, but their environmentally friendly practices would have a significant external influence on the environment as a whole. However, the banking industry, with its vast network of branches and automated teller machines (ATMs), is the biggest user of resources like paper and power. However, using in-house greenhouse projects and supporting digital banking technology can help to a larger extent in reducing the negative environmental effect. Thus, adopting green banking practices into daily operations is more important. Therefore, green finance techniques help preserve the environment by lowering CO2 emissions footprints, which motivate businesses to choose clean energy technology [18]. Similarly, the daily operations of bank direct daily operations to environmental accountability, which helps in the reduction of carbon footprints [30]. This study indicates that Somali banks rely heavily on paper usage and other wastage materials that could harm environment. Althogought, there is a little progress in terms of using online banking, paying online bills, and online digital activities. Therefore, Somali banks slightly adopted environmental friendly practices such as e-mail, intranet, e-statements, online approval system, and etc.

Third, Investments in green projects is very essential to reduce the indirect impact of banks on the environment. The results of this study indicates that Somali banks provide less meaningful funds and loans to green projects that could protect climate change and environmental deforestation which ultimately contribute green initiatives such as planting trees to reduce environmental risks. The result of this study is consistent with Nizam et al. [32], who finds in emerging nations, green banking is still extremely new and in its infancy. It faces several obstacles, including a lack of current information, a lack of global measuring tools, and its reliance on local context and technological uptake. Similar findings were made by another study, which revealed low levels of interest in clean energy projects and lower adoption costs for green banking practices [33]. Hence, it is also evident that Somali banks do not support and enable environmentally conscious businesses with specialized grants, loans, and advice to address the environmental issues that Somali people is experiencing.

Lastly, the bank policies related environmental practices. However, with the International Finance Corporation's (IFC) effort and the creation of the Sustainable Banking Network (SBN) to support green banking in poor countries, the adoption of green banking practices in particular attracted considerable attention in 2012 [16]. IFC estimates that 15 of the world's 35 countries have effectively implemented national-level guidelines, principles, and regulations regarding green banking practices. the findings of this study indicates that there are no explicit environmental protection policies that Somali banks implemented so far. For example, installing green branches to decrease climate change, which might result in environmental catastrophe. This study also findings, Somali banks have less environmental agreements with key parties and stakeholders. The senior management of the banks lacks a clear strategy for how to implement environmental protection in their institutions. Therefore, the environment and the climate change receive less attention and concern in the rules and standards of Somali banks.

6.1 Theoretical implications of the study

According to Bose and Gupta [59] argued that the theoretical framework for the implementation of green banking is not well studied. In this context, further study is required to better understand the factors that influence the adoption of green banking, particularly in developing countries [60]. This study uses socially responsible investing (SRI) theory as a baseline theory which is suitable to this study. SRI theory was perceived as advocating the use of both financial and well-being goals, particularly among microfinance institutions and socially motivated businesses, to combat the growing environmental challenges, create employment, and advance rural and urban development. Thus, this SRI theory employs finance with a social orientation to concurrently advance financial and social objectives and goals [47, 48]. There are no any known studies available in the literature on the level of awareness and green banking practices in sub-Sahara countries. In Somalia particularly, there is a need to investigate and explore as long as Somalia is one of the most effected countries by climate change [43]. thus, this study investigates the green banking practices in all licensed banks in Somalia for the purpose of filling the empirical gap in the existing knowledge and to provide rich updated literature platform for the future research. Moreover, empirical research is not existing at all in bank system of Somalia, and there is a lack of evidence of the awareness and level of adoption in green banking system sustainability. This study suggests that banking sector in Somalia should focus on increasing the awareness and environmental performance equally with a view to address and minimize the harmful effect in broader environmental perspective.

6.2 Practical and managerial implications of the study

The study has implications for both bank management and regulators. By adopting an appropriate methodology and ensuring the reliability of the data, the study has a sound basis for both theoretical and managerial implications. Empirically, this study explores the level of awareness and the existing green banking practices adoption in Somalia. Based on this study, the top management of the banks and regulators will have a better understanding of the low level of employee awareness and the low level of Somali banks practicing sustainable green banking practices to increase the awareness and green bank adoption to their banks. This may be used in future valuation of the bank’s employee awareness and green practices adoption and financial performance in Somalia. This study also bears implications for regulatory and bank management in Somalia. As the general of objective of this study was to understand the level of awareness and green banking practices in Somali banks. Thus, the result shown low level of awareness and practices in green banking in Somalia. Thus, the top management of Somali financial institutions should endeavor to create an environment which should be conducive to the sustainability of green practices in the banking sector and to participate the enhancing the awareness of green banking practices to participate in the impact of climate change. The bank management should also allocate part of the funds to finance environmentally friendly projects. Moreover, the bank's management should create clear policies and plans to enhance green banking practices. Therefore, the top bank management should be clear about climate change adoption and mitigation. Second, the central bank of Somalia should make it compulsory for all licensed banks to train their employees to enhance the awareness of green banking and disclose its green banking strategies and policies in its final reports to disseminate exact awareness of such practices to the stakeholders as the result indicates the low level of awareness and practices in green banking in Somalia. In addition, the central bank of Somalia must also formulate a robust strategic framework for green practices to be implemented by commercial banks, which can contribute to the environmental performance and awareness in general. In addition, government should include as a clause on the banks to financing of enterprise that are friendly with environment. This will substantiate banks’ practices of green banking and will contribute to its environmental performance. likewise, the government of Somalia should encourage the use of e-mail, intranet, e-statements, online approval systems, etc. as alternatives to paper consumption and other material waste that might harm the environment.

There are some limitations related to this study that give direction to potential researchers in this field. Firstly, the researcher conducted this empirical study in Somalia. the future researchers should include all sub-sahara African countries to get more insightful results pertaining to awareness and practices of green banking. Therefore, it has geographical limitations. Secondly, the primary data source of this study is collected only from employees of Somali banks. Future research should be included both Somali bank staff and clients to see their awareness of green banking. Finally, a questionnaire instrument was used in this study to collect data. Future studies should be considered using other data collection tools, such as interviews.

[1] Igbudu, N., Garanti, Z., Popoola, T. (2018). Enhancing bank loyalty through sustainable banking practices: The mediating effect of corporate image. Sustainability, 10(11): 4050. https://doi.org/10.3390/su10114050

[2] Chen, Z.X., Hossen, M.M., Muzafary, S.S., Begum, M. (2018). Green banking for environmental sustainability-present status and future agenda: Experience from Bangladesh. Asian Economic and Financial Review, 8(5): 571-585. https://doi.org/10.18488/journal.aefr.2018.85.571.585

[3] Bukhari, S.A.A., Hashim, F., Amran, A. (2020). The journey of Pakistan’s banking industry towards green banking adoption. South Asian Journal of Business and Management Cases, 9(2): 208-218. https://doi.org/10.1177/2277977920905306

[4] Barre, G.M., AliWarsame, A., Hussein, H.A. (2024). Examining awareness and preferences for green finance among commercial banks in Somalia. International Journal of Sustainable Development & Planning, 19(1): 97-108. https://doi.org/10.18280/ijsdp.190108

[5] Korslund, D., Spengler, L. (2012). Strong, straightforward and sustainable banking. Global Alliance for Banking on Values, Mars. https://www.ess-europe.eu/en/publication/strong-straightforward-and-sustainable-banking-financial-capital-and-impact-metrics.

[6] Batchelor, S. (2012). Changing the financial landscape of Africa: An unusual story of evidence-informed innovation, intentional policy influence and private sector engagement. IDS Bulletin, 43(5): 84-90. https://doi.org/10.1111/j.1759-5436.2012.00367.x

[7] Yunus, M., Moingeon, B., Lehmann-Ortega, L. (2010). Building social business models: Lessons from the Grameen experience. Long Range Planning, 43(2-3): 308-325. https://doi.org/10.1016/j.lrp.2009.12.005

[8] Climent, F. (2018). Ethical versus conventional banking: A case study. Sustainability, 10(7): 2152. https://doi.org/10.3390/su10072152

[9] Inderst, G., Kaminker, C., Stewart, F. (2012). Defining and measuring green investments: Implications for institutional investors asset allocations. OECD Working Papers on Finance, Insurance and Private Pensions. https://doi.org/10.1787/5k9312twnn44-en

[10] Hossain, M.Z., Ahmed, M., Nisha, N. (2015). Consumer attitudes and perception towards green banking in Bangladesh. In Green Banking in Bangladesh and Beyond. Zaman Printing & Packaging, Bangladesh, pp. 48-76. https://www.researchgate.net/publication/280570348.

[11] Bezabih, M. (2022). Climate change, adaptation and building human resilience in Somalia. National Economic Council of Somalia. https://nec.gov.so/wp-content/uploads/2023/06/Climate-change-adaptation-and-building-human-resilience-in-Somalia.pdf.

[12] Nakhooda, S., Caravani, A., Bird, N., Schalatek, L. (2011). Climate finance in Sub-Saharan Africa. Climate Finance Policy Brief. Overseas Development Institute and Heinrich Böll Stiftung North America. https://media.odi.org/documents/7480.pdf.

[13] Warsame, A.A., Sheik-Ali, I.A., Ali, A.O., Sarkodie, S.A. (2021). Climate change and crop production nexus in Somalia: An empirical evidence from ARDL technique. Environmental Science and Pollution Research, 28(16): 19838-19850. https://doi.org/10.1007/s11356-020-11739-3

[14] World Bank, FAO. (2018). Rebuilding Resilient and Sustainable Agriculture in Somalia? https://documents1.worldbank.org/curated/en/803231522165074948/pdf/124653-WP-P159009-PUBLIC-Somalia-CEM-Agriculture-Report-Overview-English-Mar-2018.pdf.

[15] Schultz, L., Lundholm, C. (2013). Learning for resilience? Exploring learning opportunities in biosphere reserves. In Resilience in Social-Ecological Systems. Routledge. https://www.taylorfrancis.com/chapters/edit/10.4324/9781315868387-12/learning-resilience-exploring-learning-opportunities-biosphere-reserves-lisen-schultz-cecilia-lundholm.

[16] Rehman, A., Ullah, I., Afridi, F.E.A., Ullah, Z., Zeeshan, M., Hussain, A., Rahman, H.U. (2021). Adoption of green banking practices and environmental performance in Pakistan: A demonstration of structural equation modelling. Environment, Development and Sustainability, 23: 13200-13220. https://doi.org/10.1007/s10668-020-01206-x

[17] Bai, Y. W. (2011). Financing a green future: An examination of China’s banking sector for green finance. IIIEE Master thesis, Lund University. https://lup.lub.lu.se/luur/download?func=downloadFile&recordOId=2203222&fileOId=2203226.

[18] Bihari, S.C., Pradhan, S. (2011). CSR and performance: The story of banks in India. Journal of Transnational Management, 16(1): 20-35. https://doi.org/10.1080/15475778.2011.549807

[19] Bhardwaj, B.R., Malhotra, A. (2013). Green banking strategies: Sustainability through corporate entrepreneurship. Greener Journal of Business and Management Studies, 3(4): 180-193.

[20] Mishra, D.K. (2013). Green strategies: Response of Indian banks to climate change. Development, III: 345-348. https://scholar.google.com/scholar?hl=en&as_sdt=0%2C5&q=Green+strategies%3A+Response+of+Indian+banks+to+climate+change.&btnG=.

[21] Gibbs, D. (1991). Greening the local economy. Local Economy, 6(3): 224-239. https://doi.org/10.1080/02690949108726105

[22] Kaufer, D. (2011). Banking as if society mattered: The case of Triodos Bank. https://www.socioeco.org/bdf_fiche-document-706_en.html, accessed on Sep. 31, 2017.

[23] Schücking, H., Kroll, L., Louvel, Y., Richter, R. (2010). Bankrolling climate change. Urgewald, groundWork, Earthlife Africa Johannesburg and BankTrack. https://www.banktrack.org/download/bankrolling_climate_change/climatekillerbanks_final_0.pdf.

[24] Borghesi, R., Houston, J.F., Naranjo, A. (2014). Corporate socially responsible investments: CEO altruism, reputation, and shareholder interests. Journal of Corporate Finance, 26: 164-181. https://doi.org/10.1016/j.jcorpfin.2014.03.008

[25] Riffat, S., Powell, R., Aydin, D. (2016). Future cities and environmental sustainability. Future Cities and Environment, 2(1): 1-23. https://doi.org/10.1186/s40984-016-0014-2

[26] Bauer, R., Eberhardt, I., Smeets, P. (2017). Financial incentives beat social norms: A field experiment on retirement information search. https://www.netspar.nl/wp-content/uploads/E20181901_Paper-Paul.pdf.

[27] Aggarwal, M., Dutta, M., Madaan, V., Pham, Long T., Lourens, M. (2017). Impacts of green human resource management and electronic-human resource management on green banking. E3S Web of Conferences, 399: 07005. https://doi.org/10.1051/e3sconf/202339907005

[28] Hart, S.L., Dowell, G. (2011). Invited editorial: A natural-resource-based view of the firm: Fifteen years after. Journal of Management, 37(5): 1464-1479. https://doi.org/10.1177/01492063103902

[29] Masud, M.A.K., Hossain, M.S., Kim, J.D. (2018). Is green regulation effective or a failure: Comparative analysis between Bangladesh Bank (BB) green guidelines and global reporting initiative guidelines. Sustainability, 10(4): 1267. https://doi.org/10.3390/su10041267

[30] Shaumya, K., Arulrajah, A. (2016). Measuring green banking practices: Evidence from Sri Lanka. In 13th International Conference on Business Management (ICBM), Colombo, Sri Lanka, pp. 999-1023. http://doi.org/10.2139/ssrn.2909735

[31] Nath, B., Chaudhuri, P., Birch, G. (2014). Assessment of biotic response to heavy metal contamination in Avicennia marina mangrove ecosystems in Sydney Estuary, Australia. Ecotoxicology and Environmental Safety, 107: 284-290. https://doi.org/10.1016/j.ecoenv.2014.06.019

[32] Nizam, E., Ng, A., Dewandaru, G., Nagayev, R., Nkoba, M.A. (2019). The impact of social and environmental sustainability on financial performance: A global analysis of the banking sector. Journal of Multinational Financial Management, 49: 35-53. https://doi.org/10.1016/j.mulfin.2019.01.002

[33] Owusu-Manu, D., Pärn, E., Donkor-Hyiaman, K., Edwards, D., Blackhurst, K. (2016). The relative importance of mortgage pricing determinants in mortgage affordability in Ghana: An expost attribution. Journal of Engineering, Design and Technology, 14(3): 563-579. https://doi.org/10.1108/JEDT-06-2014-0040

[34] Hummel, K., Laun, U., Krauss, A. (2021). Management of environmental and social risks and topics in the banking sector - An empirical investigation. The British Accounting Review, 53(1): 100921. https://doi.org/10.1016/j.bar.2020.100921

[35] Jan, A., Marimuthu, M., Bin Mohd, M.P., Isa, M. (2019). The nexus of sustainability practices and financial performance: From the perspective of Islamic banking. Journal of Cleaner Production, 228: 703-717. https://doi.org/10.1016/j.jclepro.2019.04.208

[36] Masukujjaman, M., Siwar, C., Alam, A., Bashawir, A., Er, A. (2016). Economy-environment nexus for development: Is Bangladesh on the right track? International Journal of Advanced Applied Sciences, 3(2): 25-29.

[37] Goel, R.K., Saunoris, J.W. (2016). Virtual versus physical government decentralization: Effects on corruption and the shadow economy. Public Budgeting & Finance, 36(4): 68-93. https://doi.org/10.1111/pbaf.12105

[38] Ikram, M., Sroufe, R., Rehman, E., Shah, S.Z.A., Mahmoudi, A. (2020). Do quality, environmental, and social (QES) certifications improve international trade? A comparative grey relation analysis of developing vs. developed countries. Physica A: Statistical Mechanics and Its Applications, 545: 123486. https://doi.org/10.1016/j.physa.2019.123486

[39] Jebarajakirthy, C., Shankar, A. (2021). Impact of online convenience on mobile banking adoption intention: A moderated mediation approach. Journal of Retailing and Consumer Services, 58: 102323. https://doi.org/10.1016/j.jretconser.2020.102323

[40] Mungai, E.M., Ndiritu, S.W., Da Silva, I. (2022). Unlocking climate finance potential and policy barriers — A case of renewable energy and energy efficiency in Sub-Saharan Africa. Resources, Environment and Sustainability, 7: 100043. https://doi.org/10.1016/j.resenv.2021.100043

[41] Doku, I., Ncwadi, R., Phiri, A. (2021). Examining the role of climate finance in the Environmental Kuznets Curve for Sub-Sahara African countries. Cogent Economics & Finance, 9(1): 1965357. https://doi.org/10.1080/23322039.2021.1965357

[42] Zandi, G., Haseeb, M. (2019). The importance of green energy consumption and agriculture in reducing environmental degradation: Evidence from sub-Saharan African countries. International Journal of Financial Research, 10(5): 215-227. https://doi.org/10.5430/ijfr.v10n5p215

[43] Ali Warsame, A., Hassan Abdi, A. (2023). Towards sustainable crop production in Somalia: Examining the role of environmental pollution and degradation. Cogent Food & Agriculture, 9(1): 2161776. https://doi.org/10.1080/23311932.2022.2161776

[44] Warsame, A.A., Sheik-Ali, I.A., Barre, G.M., Ahmed, A. (2023). Examining the effects of climate change and political instability on maize production in Somalia. Environmental Science and Pollution Research, 30(2): 3293-3306. https://doi.org/10.1007/s11356-022-22227-1

[45] Chatzitheodorou, K., Skouloudis, A., Evangelinos, K., Nikolaou, I. (2019). Exploring socially responsible investment perspectives: A literature mapping and an investor classification. Sustainable Production and Consumption, 19: 117-129. https://doi.org/10.1016/j.spc.2019.03.006

[46] van Dooren, B., Galema, R. (2018). Socially responsible investors and the disposition effect. Journal of Behavioral and Experimental Finance, 17: 42-52. https://doi.org/10.1016/j.jbef.2017.12.006

[47] Newell, G., Lin Lee, C. (2012). Influence of the corporate social responsibility factors and financial factors on REIT performance in Australia. Journal of Property Investment & Finance, 30(4): 389-403. https://doi.org/10.1108/14635781211241789

[48] Bennett, M.S., Iqbal, Z. (2013). How socially responsible investing can help bridge the gap between Islamic and conventional financial markets. International Journal of Islamic and Middle Eastern Finance and Management, 6(3): 211-225. https://doi.org/10.1108/IMEFM-Aug-2012-0078

[49] Browner, B.D., Jupiter, J., Krettek, C., Anderson, P.A. (2015). Skeletal Trauma: Basic Science, Management, and Reconstruction (Fifth edition). Elsevier Saunders, PA.

[50] Meena, D., Das, P., Kumar, S., Mandal, S., Prusty, A., Singh, S., Akhtar, M., Behera, B., Kumar, K., Pal, A., Mukherjee, S. (2013). Beta-glucan: An ideal immunostimulant in aquaculture (A review). Fish Physiology and Biochemistry, 39: 431-457. https://doi.org/10.1007/s10695-012-9710-5

[51] Ali, M., Raza, S.A., Puah, C.H., Amin, H. (2019). Consumer acceptance toward takaful in Pakistan: An application of diffusion of innovation theory. International Journal of Emerging Markets, 14(4): 620-638. https://doi.org/10.1108/IJOEM-08-2017-0275

[52] Aziz, S., Husin, M.M., Hussin, N., Afaq, Z. (2019). Factors that influence individuals’ intentions to purchase family takaful mediating role of perceived trust. Asia Pacific Journal of Marketing and Logistics, 31(1): 81-104. https://doi.org/10.1108/APJML-12-2017-0311

[53] Husin, M.M., Ab Rahman, A. (2016). Do Muslims intend to participate in Islamic insurance? Analysis from theory of planned behaviour. Journal of Islamic Accounting and Business Research, 7(1): 42-58. https://doi.org/10.1108/JIABR-03-2014-0012

[54] Shaikh, I.M., Bin Noordin, K., Arijo, S., Shaikh, F., Alsharief, A. (2020). Predicting customers’ adoption towards family takaful scheme in Pakistan using diffusion theory of innovation. Journal of Islamic Marketing, 11(6): 1761-1776. https://doi.org/10.1108/JIMA-02-2018-0037

[55] Hair, J.F., Risher, J.J., Sarstedt, M., Ringle, C.M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1): 2-24. https://doi.org/10.1108/EBR-11-2018-0203

[56] Zhu, W., Zhu, Z., Fang, S., Pan, W. (2017). Chinese students’ awareness of relationship between green finance, environmental protection education and real situation. Eurasia Journal of Mathematics, Science and Technology Education, 13(7): 3753-3769. https://doi.org/10.12973/eurasia.2017.00757a

[57] Otali, M., Monye, C. (2017). Implementation of green finance as a catalyst for green infrastructure development in Nigeria. Journal of Contemporary Research in the Built Environment, 7(2): 51-64.

[58] Shafique, O., Majeed, A. (2020). Factors influencing bankers’ intention to adopt green finance in Pakistan. Review of Economics and Development Studies, 6(4): 773-785. https://doi.org/10.47067/reads.v6i4.277

[59] Bose, I., Gupta, V. (2017). Green HRM practices in private health care & banking sectors in India. Indian Journal of Industrial Relations, 53(1): 48-58. https://www.jstor.org/stable/26536436

[60] Tu, T.T.T., Dung, N.T.P. (2017). Factors affecting green banking practices: Exploratory factor analysis on Vietnamese banks. Journal of Economic Development, 24(2): 4-30. https://doi.org/10.24311/jed/2017.24.2.05