Femilia Zahra*![]() | Muhammad Ikbal Abdullah

| Muhammad Ikbal Abdullah![]() | Muhammad Din

| Muhammad Din![]() | Fikry Karim | Andi Mattulada Amir | Nuryatni Kasim

| Fikry Karim | Andi Mattulada Amir | Nuryatni Kasim

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This research delves into the intricate dynamics of ethical decision-making within the domain of government procurement, employing the Gone theory constructs – Greed, Opportunity, Need, and Exposure – as pivotal elements in the evaluation process. In a meticulously conducted study, questionnaires were disseminated to 194 respondents in local government procurement units, spanning 12 districts in Central Sulawesi. A total of 184 respondents willingly participated, providing valuable insights into this complex landscape. Utilizing advanced statistical techniques, specifically the structural equation model through WarpPLS 7.0 software, the study unravels intriguing findings. It discerns that Greed has the potential to amplify fraudulent behavior within the government goods and services procurement evaluation, a significant revelation. Contrarily, Opportunity, Need, and Exposure do not exhibit a similar propensity to stimulate fraud in this context. Furthermore, the research unveils an influential factor: Leadership Idealism. It emerges as a potent moderating variable, effectively mitigating the inclination toward Greed-driven fraudulent activities within the government procurement evaluation process. This study significantly contributes to our understanding of the intricate interplay between psychological constructs and ethical considerations in government procurement, offering valuable insights for policymakers and practitioners alike.

ethical decision-making, government procurement, leadership idealism, fraud prevention gone theory

The introduction of e-procurement in Indonesia has not yielded a substantial reduction in corruption cases related to the procurement of goods and services. Electronic procurement (e-procurement) was expected to function as an instrument to proactively combat corruption [1]. Electronic procurement, also known as e-procurement, plays a pivotal role in the realm of e-government and e-budgeting. E-procurement leverages digital technology to streamline and enhance the procurement process within government organizations, leading to increased efficiency, transparency, and cost-effectiveness. This transformation in procurement practices has far-reaching implications for both e-government and e-budgeting initiatives. E-government, characterized by the digitization of government operations and services, benefits from e-procurement by simplifying and automating procurement procedures [2].

It enables government agencies to conduct procurement activities online, from requisition to payment, reducing paperwork and administrative overhead. Citizens and businesses can access procurement information and participate in bidding processes through online portals, fostering transparency and competition [3, 4]. E-budgeting, on the other hand, relies on accurate financial data and efficient allocation of resources. E-procurement contributes by providing real-time data on procurement transactions and expenditures, allowing budget planners to make informed decisions. It aids in tracking spending, preventing overspending, and optimizing resource allocation for government programs and projects. In essence, e-procurement aligns with the broader goals of e-government and e-budgeting by promoting transparency, accountability, and efficiency in government operations. It enhances the management of public funds, streamlines procurement processes, and empowers stakeholders with access to information, ultimately serving the public interest more effectively [5, 6].

In Indonesia, the pivotal phase in the selection of government goods and services providers is the bid evaluation process. This critical task is undertaken either by the working group or the selection committee for government goods/services providers, involving a comprehensive review and assessment of the bidding documents submitted by prospective contractors. The primary objective of this evaluation is to ascertain the winning provider. Errors in the assessment of bidding documents can lead to erroneous determinations of the auction winner. These errors, in turn, can result in subpar quality of procured goods and/or inflated prices, ultimately leading to potential financial losses for the state [1, 3-6]. The perpetration of fraudulent acts by individuals is a complex behavioral phenomenon influenced by a variety of factors [7, 8]. One of the central drivers behind fraud is the presence of compelling pressures, including the need to satisfy personal financial requirements, the desire for profit, and often, the rationalization that one's actions are not tantamount to fraud. This multifaceted dynamic finds theoretical support in the GONE theory, which posits that the foundational triggers of fraud can be distilled into four key factors: Greed, Opportunities, Need, and Exposure. Greed represents an individual's excessive desire for personal gain, compelling them to engage in fraudulent activities for financial benefit. Opportunities refer to the circumstances or situations that enable fraudulent behavior to occur, often arising from weak internal controls or lax oversight. Need underscores the motivation driven by specific financial requirements or personal pressures that push individuals toward fraudulent actions. Lastly, Exposure highlights the visibility of unethical behavior, with individuals more likely to commit fraud when they believe their actions will go unnoticed. In summary, these factors underscore the intricate interplay between psychological, situational, and environmental elements in the commission of fraudulent acts, shedding light on the multifaceted nature of fraudulent behavior in various contexts.

Leadership idealism within government institutions carries significant institutional implications, reflecting the individual behavioral system within the bureaucracy. Therefore, it is postulated that leadership idealism can either amplify or mitigate factors such as greed, opportunity, need, and exposure to fraudulent activities [9]. According to Widayat [9], if fraud within government procurement of goods and services is correlated with leadership idealism, a shift in the paradigm of ideal leadership can result in a government management system that prioritizes power interests. This shift, in turn, may lead to the emergence of corruption and power misconduct. It is crucial to recognize that an unhealthy power structure tends to cultivate individuals with opportunistic tendencies, often disregarding the adverse consequences on their thoughts, actions, and policies. The role of an idealist leader in preventing fraud within the government procurement of goods and services can set the tone for the entire procurement agency. This, in turn, can have a substantial impact on curbing fraudulent activities in government procurement, ultimately enhancing the performance of goods and services procurement for local/regional governments in Indonesia. In summary, leadership idealism's influence on bureaucratic behavior and its potential to combat fraud in government procurement have profound implications for the governance and performance of procurement processes [9].

The primary aim of this research is to investigate the influence of leadership internalization on the quality of financial reports and its consequential impact on procurement governance within public organizations. This study seeks to assess the extent to which leadership internalization affects the accuracy, transparency, and reliability of financial reporting practices in the public sector and to examine how the quality of financial reports, influenced by leadership internalization, shapes the governance of procurement processes. This study is driven by its alignment with the research objectives, its ability to capture quantitative aspects of the topic, and its practical feasibility within the public sector context. It aims to provide a comprehensive understanding of the complex relationship between leadership, financial reporting, and procurement governance, contributing valuable insights to the field. This research contributes to the existing body of knowledge by elucidating the crucial link between leadership internalization, financial reporting quality, and procurement governance. The findings will provide valuable insights for policymakers, public sector leaders, and practitioners, enabling them to make informed decisions to enhance financial transparency, accountability, and effective procurement management within government organizations.

2.1 Governance of government procurement through e-procurement

E-procurement within the public sector represents a transformative approach to the acquisition of goods and services. Several studies have underscored the advantages associated with e-procurement implementation, notably its capacity to deter or diminish undesirable behaviors among procurement actors [10, 11]. Presidential Regulation No. 4 of 2015 defines Government Procurement of Goods/Services as an extensive process commencing with needs assessment and culminating in the successful acquisition of goods/services by Ministries, Institutions, Regional Work Units, or affiliated bodies. The funding for these procurement activities can originate from state or regional budgets, or even external grants. Presidential Regulation No. 54 of 2010 further elaborates on electronic procurement, denoted as e-procurement, which involves the acquisition of goods/services facilitated by information technology and electronic transactions, all conducted in strict adherence to statutory provisions. The realm of e-procurement, as regulated by Presidential Regulation No. 54 of 2010, encompasses two essential components: e-tendering and e-purchasing. E-tendering entails a transparent provider selection process, open to all Goods/Services Providers registered in the electronic procurement system. They can participate by submitting a single bid within a predefined timeframe. In essence, e-procurement revolutionizes the traditional procurement landscape by harnessing digital technology and electronic methods, streamlining processes, and promoting transparency in the acquisition of goods and services within the public sector.

2.2 Gone theory

The Gone theory, prominently featured in fraud research, serves as the foundational framework for investigating the underlying factors driving fraudulent behavior in this study. Bologne [7] introduced the Gone theory, which refines the earlier Fraud Triangle Theory, shedding light on the motivations behind corrupt individuals engaging in fraudulent activities. The Fraud Triangle Theory, originally formulated by Cressey [12], is renowned for elucidating the triggers for fraud and is often referred to as the "fraud triangle." According to Cressey [12], the Fraud Triangle Theory identifies three essential elements consistently present in every fraudulent situation: Pressure, Opportunity, and Rationalization. Pressure signifies the external or internal forces compelling individuals towards fraudulent acts, while Opportunity relates to the existence of vulnerabilities within systems or organizations that enable fraudulent conduct. Rationalization involves the cognitive process individuals employ to justify their fraudulent actions.

The Gone theory, an evolution of the Fraud Triangle Theory, introduces four core factors as the root causes of fraud: Greed, Opportunities, Need, and Exposure. Greed pertains to the insatiable desire for wealth and avarice that can manifest in individuals from various backgrounds. Opportunities refer to the structural vulnerabilities within organizations or communities that create openings for fraudulent behavior. Need reflects a mindset characterized by perpetual consumerism and unending material desires. Lastly, Exposure entails the limited deterrence effect of punitive measures against corrupt individuals, with minimal repercussions failing to dissuade both potential perpetrators and society at large. In summary, the Gone theory enriches our understanding of the multifaceted drivers of fraud, encompassing a broader spectrum of factors that go beyond the confines of the Fraud Triangle Theory. It delves into the complexities of human motivations and organizational vulnerabilities, offering a comprehensive perspective on the phenomenon of fraud [7].

2.3 Hypothesis development

An individual's behavior to engage in fraudulent behavior is influenced by a complex interplay of factors. Cressey's Triangle Fraud Theory [12] identifies three pivotal elements that aptly explain the motivations behind fraudulent acts: pressure, opportunity, and rationalization. In contrast, Bologne's [7] Gone Theory, the theoretical framework underpinning this research, introduces a more comprehensive set of factors: Greed, Opportunity, Need, and Exposure, which serve as rationales for corrupt individuals to commit fraud. The first factor, Greed, encapsulates an insatiable desire for material wealth, rendering individuals myopic to the moral consequences of their actions. This compelling factor propels individuals to employ any means necessary to satiate their material cravings [8]. Consequently, the higher the intensity of one's greed, the greater the propensity to engage in fraudulent activities. In light of this, our research hypothesis is formulated as follows:

H1: Greed has a significant influence on fraudulent behavior in the evaluation of government procurement.

In Bologne's [7] Gone Theory, the second crucial factor attributed to the causation of fraud is Opportunity. Opportunity is universally acknowledged as a pivotal component in the realm of fraudulent activities, as emphasized by Albrecht et al. [13]. It is considered a key triggering factor for fraudulent behavior. The level of Opportunity available plays a substantial role in influencing the likelihood of fraud or fraudulent acts. Consequently, individuals exposed to higher levels of opportunity are more prone to engaging in fraudulent activities. This shows that opportunity, as a central element in Bologne's [7] Gone Theory, is recognized for its role in creating conditions conducive to fraudulent acts. It is a fundamental factor that warrants investigation in the context of evaluating government procurement practices [7, 13]. This perspective underscores the significance of Opportunity in the context of fraudulent conduct. Therefore, the research hypothesis is postulated as follows:

H2: Opportunity has a significant impact on fraudulent behavior in the evaluation of government procurement.

In the context of fraudulent behavior, Bologne's [7] Gone Theory introduces the third significant factor: Need. This factor acknowledges the intrinsic human propensity for needs and desires, which can act as a compelling force driving individuals toward fraudulent actions. People's unrelenting needs can become a powerful motivator, pushing them to resort to fraudulent means to fulfill their necessities. This shows that the need factor, as outlined in Bologne's GONE Theory, recognizes the fundamental role of human needs in motivating fraudulent actions. It is a crucial dimension to consider when assessing fraud within the context of government procurement processes [7]. The intensity of these needs directly correlates with the potential for engaging in fraudulent conduct. Consequently, individuals facing higher levels of need are more susceptible to committing fraudulent acts. As a result, our research hypothesis is postulated as follows:

H3: Need has a significant influence on fraudulent behavior in the evaluation of government procurement.

In the realm of fraudulent activities, the concept of low penalties, often referred to as Exposes, pertains to the repercussions or consequences faced by individuals found guilty of committing fraud [8]. This underscores the critical role of the exposure factor in the context of fraud prevention within government procurement processes. A comprehensive examination of punitive measures is essential to understanding and mitigating fraudulent activities [8]. Low penalties imply that perpetrators of fraud encounter minimal punitive measures, which, in turn, can fail to serve as an effective deterrent against the repetition of fraudulent acts. This is a significant concern, as lenient punishments do not guarantee that fraud will not recur, whether by the same offender or by others. The hypothesis derived from this notion is as follows:

H4: Exposes has a significant influence on fraudulent behavior in the evaluation of government procurement.

Tappen et al. [14] assert that leadership idealism revolves around the virtuous character of a leader, enabling them to wield power effectively and efficiently for the betterment of their constituents. These idealistic leaders are characterized by their readiness to engage in constructive discourse, even when confronted with differing opinions. They maintain unwavering confidence, exude optimism, harbor positive outlooks, and exhibit the courage to assume risks for their decisions. Tappen et al. [14] further posit that such leaders must possess essential traits, including knowledge, self-awareness, effective communication skills, vitality, clearly defined objectives, and a penchant for taking decisive actions. Notably, a higher level of leadership idealism correlates with a diminished propensity for individuals to engage in fraudulent activities.

Widayat [9] extends this notion by highlighting the pivotal role of leadership idealism within an organizational framework. He contends that the idealism of a leader, when aligned with the system in place, plays a determinative role in shaping the conduct of individuals within the organization. When leadership idealism is positive, it has the potential to transform individuals, even if some within the group exhibit undesirable qualities. Conversely, when leadership idealism is negative, it can exert a detrimental influence on individuals, notwithstanding their inherent quality and competence.

Within government institutions, the idealism of leadership holds institutional ramifications, serving as a reflection of the collective behavioral ethos of the bureaucracy. Consequently, leadership idealism is hypothesized to wield influence over key factors associated with fraudulent behavior, namely, greed, opportunity, need, and exposure to fraud. This shows that leadership idealism, as elucidated by Tappen et al. [14] and Widayat [9], emerges as a crucial determinant in shaping individual behaviors and, by extension, in mitigating the propensity for fraudulent actions across various factors within government institutions. This leads to the formulation of the following research hypotheses:

H5: A high level of leadership idealism will mitigate the influence of the greed factor on fraudulent behavior.

H6: A high level of leadership idealism will reduce the impact of the opportunity factor on fraudulent behavior.

H7: A high level of leadership idealism will diminish the significance of the need factor in fraudulent behavior.

H8: A high level of leadership idealism will attenuate the role of the exposure factor in fraudulent behavior.

The research design adopted for this study was a cross-sectional survey, aiming to collect data at a single point in time from respondents representing various districts and the city of Palu in Central Sulawesi from September to October 2022. The sampling strategy involved a census of all available procurement units within the specified region. Questionnaires were distributed to all eligible procurement unit representatives, ensuring comprehensive coverage. This approach is known as a census or a full enumeration, where data is collected from the entire population rather than a sample.

The questionnaire used in the study was designed to collect responses related to the evaluation of local government goods and services procurement. It likely included questions covering various aspects such as the perception of factors contributing to fraud, the role of leadership idealism, and other relevant variables. The questionnaire was likely pre-tested and refined to ensure clarity, validity, and reliability. Data collection involved the dissemination of questionnaires to the target respondents. This was primarily carried out online using the Google Forms application, which is a convenient and efficient tool for administering surveys. Respondents were provided with the questionnaire link, and they had the opportunity to complete it electronically. In total, 194 questionnaires were distributed to representatives from 12 districts and Palu City within Central Sulawesi. Out of the 194 questionnaires distributed, 184 respondents completed the questionnaire, and these 184 questionnaires were used for processing. The response rate for this study is approximately 94.8%. This means that nearly 94.8% of the questionnaires distributed were completed and deemed usable for data analysis. It indicates a high level of participation from the targeted respondents, suggesting that the study received a substantial and representative sample of responses from the population under investigation. A response rate of 94.8% is generally considered very good and enhances the reliability and validity of the study's findings.

The collected data was subjected to statistical analysis using structural equation modeling (SEM). Specifically, WarpPLS 7.0 software was utilized for data analysis. SEM is a robust statistical technique used to assess the relationships among multiple variables and evaluate complex structural models. In this context, SEM would have been employed to analyze the interplay between various factors such as greed, opportunity, need, exposure, and leadership idealism in the evaluation of government procurement.

Table 1 displays the results of the reliability analysis for six constructs in the study. It confirms their internal consistency, meeting established criteria for reliability. Table 1 displays composite reliability values exceeding 0.70 and Cronbach's alpha values above 0.70, indicating strong reliability of the measurement instrument for variables. This ensures dependable measurement instruments, vital for accurate and valid study outcomes in structural equation modeling. This consistency in results on repeated measurements underscores instrument reliability. Two criteria assess whether the outer model meets convergent validity for reflective constructs: (1) loadings above 0.70, and (2) significant p-values (> 0.05). However, loading factors of 0.60-0.70 remain acceptable [15].

Table 1. Reliability

|

Construct |

Criteria |

Composite Reliability |

Cronbach's Alpha |

Information |

|

Fraud.E |

>0.70 |

0.925 |

0.905 |

Reliable |

|

Greed |

>0.70 |

0.825 |

0.758 |

Reliable |

|

Opprtun |

>0.70 |

0.743 |

0.812 |

Reliable |

|

Need |

>0.70 |

0.838 |

0.755 |

Reliable |

|

Exposes |

>0.70 |

0.722 |

0.732 |

Reliable |

|

Leader |

>0.70 |

0.714 |

0.733 |

Reliable |

The measurement results indicate that the construct indicators for fraud (FE5, FE6, and FE9) in the evaluation of government procurement of goods/services all exhibit loading values exceeding 0.60. Similarly, the indicators for the Greed construct (G1 and G3) surpass the 0.60 threshold, as do the indicators for the Opportunity construct (O1, O2, O3, O4, O5, and O6). The Need construct indicators (N1, N2, N3, and N4) also exhibit loading values greater than 0.60, as do the Expose construct indicators (E1, E2, E3, E4, E5, and E6), and the leadership idealism construct indicators (IP1, IP2, IP3, and IP4). However, certain other indicators with loading values below 0.60 should be eliminated from the model before further testing. The indicators included in the research model demonstrate strong convergent validity, signifying their ability to consistently collect data in a manner that aligns with measuring the same construct.

Indications of the fulfillment of discriminant validity are also evident in the AVE root values, which exceed the correlations with other constructs. The AVE root results in the diagonal column reveal that all variables possess higher AVE roots compared to the correlations with other constructs. The cross-loading values of the AVE root suggest that the instrument in this study likely satisfies discriminant validity criteria [15]. The analysis of the structural model using WarpPLS 7.0 displays the measurement results of the complete structural equation model, as depicted in Figure 1.

Figure 1. Output WarpPLS 7.0-full model

The indications of the fit model used in this study based on the output of the WarpPLS version 7.0 program are the Average Path Coefficient (APC), Average R-square (ARS) and Average Variance Inflation Factor (AVIF), Average adjusted R-squared (AARS), and Average full collinearity VIF (AFVIF). According to Kock [16], the first criterion for fulfilling the goodness of fit of a model is that the ρ-value for APC as well as ARS and AARS must be significant at the 0.05 level (ρ-value < 5). The second criterion is that the AVIF and AFVIF values are not more than 5 (AVIF and AFVIF < 5). The following is the output of the fit model in Table 2.

The model fit indicators used in this study, based on the output from the WarpPLS version 7.0 program, include the Average Path Coefficient (APC), Average R-square (ARS), Average Variance Inflation Factor (AVIF), Average adjusted R-squared (AARS), and Average full collinearity VIF (AFVIF). According to Kock [16], the first criterion for assessing the goodness of fit of a model is that the ρ-value for APC, as well as ARS and AARS, must be significant at the 0.05 level (ρ-value < 0.05). The second criterion is that the AVIF and AFVIF values should not exceed 5 (AVIF and AFVIF < 5). The following table (Table 2) presents the output of the fit model.

Table 2. Measurement of the fit model

|

Parameter |

Score |

Limitation |

Conclusion |

|

Average Path Coefisient (APC) |

0.256, p<0.001 |

P<0.05 |

Model fit |

|

Average R-square (ARS) |

0.162, p<0.017 |

P<0.05 |

Model fit |

|

Average adjusted R-squared (AARS) |

0.152, p<0.022 |

P<0.05 |

Model fit |

|

Average Variance InflationFactor (AVIF) |

1.484 |

Acceptable if<=5, ideally <=3.3 |

Model fit |

|

Average full collinearity VIF AFVIF) |

1.058 |

Acceptable if<=5, ideally <=3.3 |

Model fit |

Based on the output in Table 2, the fit model exhibits the following values: APC=0.256, p<0.001, ARS=0.162, p<0.017, AARS=0.152, p<0.022, AVIF=1.484 (acceptable if <= 5, ideally <= 3.3), and AFVIF=1.058 (acceptable if <= 5, ideally <= 3.3). WarpPLS guidelines specify that ρ-values for APC and ARS should be less than 0.05 (indicating significance), and AVIF and AFVIF values, as indicators of multicollinearity, should be less than 5. Following these guidelines, it can be concluded that the research model fits well.

The next step in testing is to evaluate the hypotheses, aiming to address the research questions posed. Hypothesis testing will be conducted using the Structural Equation Modeling (SEM) analysis tool within the WarpPLS version 7.0 program. Table 3 shows the hypothesis testing for each research model.

Table 3. Hypothesis testing

|

No. |

Hypothesis |

Path Coefficient |

P-Value |

Result |

|

1 |

Greed→Fraud |

0.51 |

0.01 |

Accepted |

|

2 |

Opportunity→Fraud |

0.01 |

0.45 |

Rejected |

|

3 |

Need→Fraud |

0.04 |

0.35 |

Rejected |

|

4 |

Expose→Fraud |

0.03 |

0.38 |

Rejected |

|

5 |

Greed*leader→Fraud |

0.34 |

0.01 |

Accepted |

|

6 |

Opportunity*leader →Fraud |

-0.30 |

0.01 |

Accepted |

|

7 |

Need*leader →Fraud |

0.03 |

0.40 |

Rejected |

|

8 |

Expose*leader →Fraud |

0.10 |

0.17 |

Rejected |

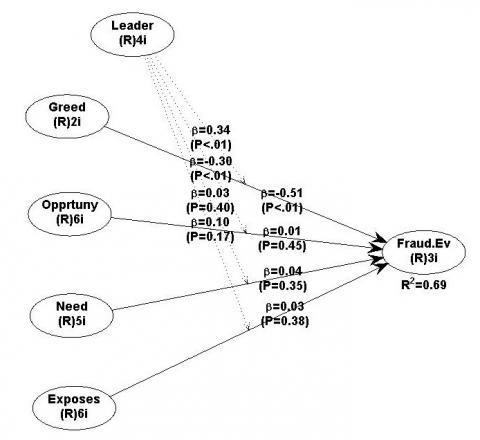

The initial hypothesis posits that greed influences fraud during the assessment of Government Procurement of Goods/Services. Analysis conducted using WarpPLS 7.0, as depicted in Table 3 and Figure 1, reveals a coefficient value of 0.51 for the path from greed to Fraud evaluation, with a significance value of ρ<0.01. These findings confirm that greed indeed impacts fraud within the context of government procurement of goods/services. Consequently, Hypothesis 1 is supported, with a coefficient of determination reaching 0.29. These results align with Dewani and Chariri's research [8], affirming that higher levels of greed correspond to an increased propensity for fraud. This underscores the notion that greed can exert influence on the evaluation outcomes of Regional Government Procurement, potentially leading to dysfunctional behavior within the realm of local government procurement assessments.

The second hypothesis posits that opportunity exerts an influence on fraud during the assessment of government procurement of goods/services. Examination of the results generated by WarpPLS 7.0 reveals a coefficient value of 0.01 for the path from opportunity to Fraud evaluation, with a significance value of ρ=0.45. These outcomes suggest that opportunity does not play a significant role in influencing fraud within the context of government procurement of goods/services. Consequently, Hypothesis 2 is not supported, with a coefficient of determination standing at 0.29. The findings from this study indicate that the utilization of opportunities in the assessment of government procurement of goods and services does not contribute to an increase in fraud within the evaluation of local government procurement of goods/services. This can be seen as indicative of a well-structured and tightly controlled procurement system, reducing the likelihood of the procurement team engaging in fraudulent activities during the evaluation process of government goods/services procurement.

The third hypothesis posits that the need factor influences fraud within the context of evaluating government procurement of goods/services. Based on the findings derived from WarpPLS 7.0, the coefficient value for the path from need to Fraud evaluation is 0.04, with a significance value of ρ=0.35. These results suggest that need does not exert a significant impact on fraud within the assessment of government procurement of goods/services. Consequently, Hypothesis 3 is not supported, yielding a coefficient of determination of 0.29. The outcomes of this study indicate that the individual needs of the evaluation team members in the assessment of government procurement of goods and services do not lead to an increase in fraud during the evaluation of local government procurement of goods/services. This may exemplify the presence of an electronically implemented procurement system with robust controls, minimizing the inclination of regional government procurement evaluation teams to engage in fraudulent activities during the evaluation process, even when driven by individual needs.

The fourth hypothesis posits that exposure (expose) affects fraud within the context of evaluating government procurement of goods/services. Based on the findings derived from WarpPLS 7.0, the coefficient value for the path from expose to Fraud evaluation is 0.04, with a significance value of ρ=0.38. These results suggest that exposure does not exert a significant impact on fraud within the assessment of government procurement of goods/services. Consequently, Hypothesis 4 is not supported, yielding a coefficient of determination of 0.29. The outcomes of this study indicate that the personal exposure level of the evaluation team members in the assessment of government procurement of goods and services does not lead to an increase in fraud during the evaluation of local government procurement of goods/services. This may exemplify the presence of an effective procurement system that discourages the procurement team's inclination to commit fraud during the evaluation process, even when influenced by their personal exposure levels [17-19].

The fifth through eighth hypotheses introduce leadership idealism as a moderating variable, positing that it can either amplify or mitigate the impact of greed, opportunity, need, and exposure on fraudulent behavior. Upon analyzing the results using WarpPLS 7.0, it becomes evident that the ρ value for hypothesis 5 is less than 0.01. This finding suggests that leadership idealism can indeed moderate the relationship between greed and fraud. These outcomes underscore the pivotal role of leadership in fraud control within the government procurement evaluation process. The leadership's influence can significantly shape the outcomes of government procurement evaluations. Hence, if the leader promotes individual-oriented values and reinforces greed, it is likely to lead to increased fraudulent behavior in the evaluation process. Conversely, when the leader adopts an organization-oriented approach, it can act as a deterrent to the procurement evaluation team's greed, thereby reducing the incidence of fraud in government procurement evaluations.

The testing of hypotheses 6, 7, and 8 did not yield significant results, as indicated by the insignificant p-values. Consequently, it can be concluded that hypotheses 6, 7, and 8 should be rejected. The findings of this study suggest that leadership idealism does not act as a moderator for the relationships between opportunity, need, exposure, and fraudulent behavior in the evaluation of regional government procurement. This observation reflects the effectiveness of the electronically implemented procurement system with its robust control mechanisms. An ideal leader, in the context of this integrated system, plays a significant role in curbing potential dysfunctional behaviors. The system itself offers extensive oversight capabilities, allowing leadership to monitor and detect any fraudulent activities within the local government procurement evaluation team. Consequently, the temptation to engage in fraudulent practices during the evaluation process remains minimal, even in the face of individual needs among team members [17, 20].

In conclusion, several findings align with the research hypothesis. Greed is found to be a significant factor in elevating the occurrence of fraud in the assessment of government procurement processes for goods and services. Conversely, the factors of opportunity, necessity, and exposure do not exhibit a substantial influence on the increase of fraud within the evaluation of government goods and services procurement. These outcomes underscore the effectiveness of a robust government procurement system, which effectively curtails opportunities for fraudulent activities in the assessment phase of government procurement for goods and services. Furthermore, the leadership's idealism emerges as a highly influential factor in diminishing the propensity for greed-driven fraudulent behavior during the evaluation of government procurement processes for goods and services.

This study contributes to the theoretical understanding of fraud within government procurement by identifying the critical role of greed and the moderating influence of leadership idealism. It provides insights into how these factors affect fraud in the evaluation phase. Reinforcement of the Fraud Triangle: By confirming the significance of greed, this research reinforces the elements of the Fraud Triangle Theory in the context of government procurement, highlighting its continued relevance as a theoretical framework.

As practical implications, the findings underscore the importance of implementing effective government procurement systems, which can substantially reduce opportunities for fraudulent activities during evaluation. Policymakers can use this insight to strengthen procurement procedures and controls. Moreover, public sector organizations can use the knowledge that leadership idealism plays a crucial role in reducing greed-driven fraud. Leadership development programs may focus on cultivating idealism, ethics, and integrity among leaders to create a more fraud-resistant environment.

This study presents certain limitations that warrant consideration. Firstly, the findings are context-specific, primarily derived from a particular geographic region and government context. As a result, applying these findings universally to other regions or nations should be approached cautiously, recognizing that variations in cultural, regulatory, and institutional factors may influence the dynamics of fraud in government procurement differently. Therefore, future research should aim to replicate these findings across diverse contexts to assess the robustness and generalizability of the identified relationships. Additionally, the study relied on self-reported data, a common approach in survey-based research. However, self-reported data are subject to potential measurement bias due to factors like social desirability or recall inaccuracies. Researchers should be mindful of these limitations when interpreting the results, and future studies may explore alternative data collection methods or employ triangulation techniques to enhance the reliability and validity of the findings.

To address these limitations and advance the understanding of fraud in government procurement, several promising avenues for future research emerge. Firstly, conducting cross-cultural studies that investigate variations in the relationships between greed, leadership idealism, and fraud across different national and cultural contexts can enrich our knowledge of these dynamics. This approach will shed light on the extent to which cultural factors influence fraud behaviors and the efficacy of leadership interventions. Moreover, longitudinal studies tracking changes in procurement systems and fraud patterns over time can offer valuable insights into the effectiveness and sustainability of reforms. By examining how fraud evolves in response to policy changes and organizational adaptations, researchers can provide evidence-based recommendations for long-term fraud prevention and detection strategies. Qualitative research methods, such as interviews and case studies, can complement quantitative findings by providing in-depth insights into the motivations and behaviors of individuals involved in government procurement. Finally, future research should explore the development and evaluation of intervention strategies or anti-fraud programs that leverage leadership idealism to mitigate fraud risks in government procurement settings, offering practical solutions for enhancing the integrity of procurement processes.

[1] Vaidya, K., Sajeev, A.S.M., Callender, G. (2006). Critical factors that influence e-procurement implementation success in the public sector. Journal of Public Procurement, 6(1/2): 70-99. https://doi.org/10.1108/JOPP-06-01-02-2006-B004

[2] Warsono, H., Yuwono, T., Putranti, I. (2023). Analyzing technology acceptance model for collaborative governance in public administration: Empirical evidence of digital governance and perceived ease of use. International Journal of Data and Network Science, 7(1): 41-48. https://doi.org/10.5267/j.ijdns.2022.12.008

[3] Zahra, F., Abdullah, M.I., Kahar, A., Din, M., Nurfalah, N. (2021). Preventing procurement fraud in e-purchasing for Indonesian local governments. The Journal of Asian Finance, Economics and Business, 8(2): 505-511.

[4] Zahra, F., Rohman, A., Chariri, A., Karim, F. (2017). Does e-procurement solve Indonesia local government budgetary slack through its adaptive culture. International Journal of Civil Engineering and Technology, 8(8): 1001-1010.

[5] Iqbal, M., Seo, J. (2008). E-governance as an anti-corruption tool: Korean Case. Korean Local Information, 11(2): 51-78.

[6] Zahra, F., Abdullah, M., Din, M., Thahir, H., Harun, H., Ali, J. (2022). The role of e-purchasing in government procurement fraud reduction through expanding market access. International Journal of Data and Network Science, 6(1): 179-184. http://dx.doi.org/10.5267/j.ijdns.2021.9.010

[7] Bologne, J. (1993). Handbook on Corporate Fraud: Prevention, De1ec1ion, and Investigation. Oxford: Butterworth-Heinemann.

[8] Dewayani, R.A., Chariri, A. (2015). Money laundering dan keterlibatan wanita (artis): Tantangan baru bagi auditor investigatif. Diponegoro Journal of Accounting, 4(3): 45-50.

[9] Widayat, P.A. (2014). Kepemimpinan profetik. AKADEMIKA: Jurnal Pemikiran Islam, 19(1): 18-34.

[10] Neupane, A., Soar, J., Vaidya, K. (2014). An empirical evaluation of the potential of public e-procurement to reduce corruption. Australasian Journal of Information Systems, 18(2): 21-44. https://doi.org/10.3127/ajis.v18i2.780

[11] Neupane, A., Soar, J., Vaidya, K., Yong, J. (2012). Role of public e-procurement technology to reduce corruption in government procurement. In Proceedings of the 5th International Public Procurement Conference (IPPC5), pp. 304-334.

[12] Cressey, D.R. (1953). Other People's Money; A Study of the Social Psychology of Embezzlement. New York: Free Press.

[13] Albrecht, W.S., Albrecht, C.C., Albrecht, C.O. (2004). Fraud and corporate executives: Agency, steward ship and broken trust. Journal of Forensic Accounting, 5(1): 109-130.

[14] Tappen, R.M., Davis, F.A., Tradewell, G.T. (1995). Nursing leadership and management: Concepts and practice. Journal for Nurses in Professional Development, 11(5): 280.

[15] Ghozali, I., Latan, H. (2014). Partial Least Squares Konsep Metode dan Aplikasi Menggunakan Program WarpPLS 4.0. Semarang: Badan Penerbit Universitas Diponegoro.

[16] Kock, N. (2020). WarpPLS user manual: Version 7.0. Texas: ScriptWarp Systems.

[17] Bakri, M.I., Mattulada, A., Abdullah, M.I., Karim, F., Kahar, A., Din, M., Zahra, F., Furqan, A.C. (2022). The management of school operational assistance (SOA) through tax administration at Tojo Una Una’S financial and asset management agency. Research Horizon, 2(4): 476-487. https://doi.org/10.54518/rh.2.4.2022.476-487

[18] Husnah, H., Ichwan, M.I. (2023). Economic and investment opportunities in local level: Exploring economic development in an Indonesian regency. Research Horizon, 3(1): 37-49. https://doi.org/10.54518/rh.3.1.2023.640-657

[19] Susanto, H., Lusttilanang, P., Suwarno, S., Restianto, Y. (2023). The influence of independence, experience, and competence on audit quality mediated by the effectiveness of e-audit. Research Horizon, 3(4): 348-361.

[20] Din, M., Paranoan, S., Azdar, F., Ralis, G. (2022). The effect of accrual-based accounting training and assistance on the knowledge improvement of financial report management at local government units. Economic and Business Horizon, 1(2): 1-12.