Financial Market Development, Foreign Direct Investment and CO2 Emissions Nexus in Saudi Arabia: Asymmetrical Analysis

Anass Hamadelneel Adow![]()

© 2024 The author. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The financial markets and Foreign Direct Investment (FDI) could significantly determine the environment of any economy. This research investigates the asymmetrical effects of Financial Market Development (FMD), FDI, and economic growth on CO2 emissions in Saudi Arabia from 1970-2021. In the long run, the increasing economic growth and FMD elevates CO2 emissions but decreasing economic growth and FMD could not affect CO2 emissions. Increasing and decreasing FDI raises and mitigates emissions, respectively. In the short run, increasing and decreasing FDI could not affect CO2 emissions. Increasing and decreasing economic growth increase and alleviate CO2 emissions, respectively. The increasing FMD raises CO2 emissions and decreasing FMD could not affect CO2 emissions. The research recommends welcoming FDI in clean sectors and controlling pollution-oriented activities from FDI, FMD, and economic growth.

FDI, FMD, economic growth, CO2 emissions, Asymmetry

Financial market development (FMD) provides access to credit and capital in business sectors to invest the money into factories, industrial plants, transportation, or other economic activities. Thus, FMD can increase economic scale and raise energy usage. Saudi Arabia is utilizing more than 99% of energy from fossil fuels [1], which could be responsible for pollution emissions. Moreover, FMD would also provide consumer loans promoting the usage of vehicles and electrical appliances [2], which could raise pollution emissions. Moreover, FMD can finance projects related to infrastructure development, which needs heavy machinery, transportation of materials, and other activities to accelerate energy consumption. Further, interest payment on credit could prioritize short-term profits over long-term sustainability among the business community. Thus, FMD could have environmental concerns for any economy.

Along with expected negative environmental consequences, FMD could have a pleasant environmental contribution by financing green technology’s infrastructure and mitigating emissions [3]. Moreover, access to credit may enable firms to purchase energy-efficient technologies and infrastructure for the industrial sector, which could reduce industrial pollution. In addition, FMD could provide loans for R&D activities in the business sector [4], which can result in the development of environmentally friendly technologies and processes. A developed financial market can increase awareness of environmental consciousness among investors and the community, which can increase the demand for a cleaner environment and cleaner production standards. This awareness could force the industry to follow environmental regulations. FMD could also facilitate the trading of green bonds, which could be helpful in the investment in environmentally friendly projects.

Foreign Direct Investment (FDI) is also a potential determinant of pollution. Because FDI mostly establishes new factories and industries in the FDI-recipient country, which could increase energy usage and emissions. Moreover, FDI increases overall investments and income, which would raise demand for energy and pollution. In addition, foreign investors flow their investments from tight regulatory regions to lax regulatory regions to exploit the advantage of the low cost of production to remain competitive. So, FDI could transfer carbon-intensive technologies like manufacturing, mining, and chemicals to low regulated economies. Thus, FDI may generate a Pollution Haven Hypothesis (PHH) and might pollute the environment [5]. Moreover, FDI can enter in transportation business, which is an energy and pollution-intensive sector. For instance, in the particular case of Saudi Arabia, 87.2% of FDI inflows are in the transportation sector, manufacturing sector, and trading in 2022 [6]. Thus, such FDI could have environmental problems.

FDI may flow in the natural resource sector. In the case of Saudi Arabia, it may flow into the oil and gas sectors. These sectors are highly pollution-oriented sectors from their upstream to downstream business activities. For instance, exploration and extraction of such resources are pollution-oriented. Moreover, refineries of oil products, petrochemical industries, and other related products would be responsible for carbon emissions. Contrarily, FDI could also mitigate emissions. FDI might transfer the latest technologies and managerial skills to the recipient economy, which might reduce pollution in the host economy. Thus, FDI would have positive spillovers in recipient economies by promoting sustainable practices. Moreover, FDI might be invested in green technology projects and renewable energy projects. Thus, FDI would help in reducing emissions. Besides, foreign investors usually belong to developed countries and follow comparatively better environmental standards compared to recipient economies, which could help reduce emissions in recipient economies [7].

Carrying a mix of the positive and negative environmental outcomes of FDI and FMD, the net environmental effect of FDI and FMD on the recipient economy is a research question. So, the present research examines it in a case of resource-abundant Saudi economy using a maximum available dataset from 1970-2021. The Saudi literature has investigated the effect of economic growth [8-10], the effect of FDI [9, 11], and the effect of FMD [8, 9, 12, 13] on emissions. However, the investigation of the asymmetrical effects of economic growth, FDI, and FMD on CO2 emissions is missing in Saudi literature. Thus, the present study is going to fill this literature gap by using a novel non-linear cointegration technique proposed by Shin et al. [14]. The increasing macroeconomic series does not necessarily have the same effects as of decreasing macroeconomic series [14]. For instance, increasing FDI, FMD, and economic growth may increase economic activities and CO2 emissions. But it is not necessary that decreasing FDI, FMD, and economic growth could also reduce economic activities and CO2 emissions. Sometimes, decreasing FDI, FMD, and economic growth could not reduce economic activities significantly due to the Ratchet effect and thus could not reduce CO2 emissions. Therefore, it is a research question to test the asymmetrical effects of the increasing and decreasing macroeconomic series on economic or environmental performance in any economy. To answer this research question, the present research aims to investigate the asymmetrical effects of FDI, FMD, and economic growth on CO2 emissions in Saudi economy. This asymmetrical analysis would differentiate the environmental effects of increasing and decreasing FDI, FMD, and economic growth on CO2 emissions. Moreover, this analysis will be an empirical contribution to Saudi literature and could suggest the different sets of policies in times of increasing or decreasing FDI, FMD, and economic growth in the Saudi economy. For asymmetrical analyses, Shin et al. [14] provided a novel Non-linear Autoregressive Distributive Lag (NARDL) cointegration technique, which generates the increasing and decreasing series of any macroeconomic variables. The testing of the effects of increasing and decreasing series may conclude about the symmetrical or asymmetrical relationships between variables.

The present research focuses on recent studies on FDI, FMD, and emissions nexus to see the latest developments in literature on the topic. At first, the studies on large panels are discussed. Trinh et al. [15] probed the nexus between REC, and FMD in 180 economies using three decades’ dataset and found the heterogeneous effects of FMD on the energy-environment nexus, which provided the critical policy implications for achieving sustainable energy transitions and green growth related to FMD and financial institutions. Jiang and Ma [16] scrutinized 155 countries from 1960 to 2014 and documented that FMD significantly increased emissions globally. Nevertheless, the impact was insignificant in developed countries. Tran [17] investigated 148 countries from 1990-2019 and revealed that the influence of FMD on emissions was reliant on economic growth and REC. REC mitigated the emissions and increased the chance of economic growth in rich countries. The study suggested green credit policies and innovations to condense emissions. Uddin [18] investigated the moderation effect of FMD on the existence of EKC in 115 countries from 1990-2016. He found that FMD positively interacted with income and CO2 emissions and negatively interacted with income squared and CO2 emissions. Thus, FMD helped in shaping the EKC. In middle-income economies, FMD negatively interacted with income and emissions. However, in high-income economies, FMD negatively interacted with income squared and emissions. Thus, FMD could mitigate emissions without delaying economic growth.

Acheampong et al. [19] assessed the impact of FMD on carbon intensity in 83 countries from 1980-2015 and found that FMD reduced carbon concentration in rich economies and increased in other economies. Ahmad et al. [20] explored the impact of FMD and FDI on CO2 emissions in 90 economies from 1990-2017 and reported that FMD through access, depth, and efficiency increased CO2 emissions. Conversely, FDI mitigated CO2 emissions and the EKC was also supported. Energy usage and urbanization raised emissions and trade condensed emissions. Moreover, most variables showed feedback with each other in causality analyses. Anser et al. [21] scrutinized the impact of oil prices on FMD in 81 economies and confirmed the oil curse hypothesis as FMD and oil prices raised CO2 emissions during the coronavirus crisis. Kirikkaleli and Adebayo [22] examined the effects of FMD and REC including innovation and growth in a model and found that FMD and REC reduced emissions at a global level. However, the economic progress of nations increased carbon emissions. It was suggested at the global level to raise FMD and REC to mitigate CO2 emissions.

Some studies worked on FDI, FDI, and emissions nexus in panels with regional classification. For instance, Emenekwe et al. [23] scrutinized the interconnection between FMD, income, and emissions in 37 Sub-Saharan African (SSA) nations from 2000-2016 and found that FMD reduced CO2 emissions. A one-unit increase in the FMD resulted in a 2.867% reduction in CO2 emissions. Financial subsectors like access and efficiency dimensions also reduced CO2 emissions. Moreover, the effect of income on emissions corroborated the EKC. Moreover, a bi-directional connection was substantiated between FMD and emissions. Nyeadi [24] explored the impact of FMD and FDI on pollution and REC in 44 SSA economies from 1998-2017 and documented that both mitigated emissions. FDI raised REC in poor countries and reduced REC in middle-income countries. Annor et al. [25] scrutinized the nexus between FMD and pollution in SSA from 1990-2018 and corroborated the EKC in ecological footprint and CO2 emissions models, which is moderated by human development. For high and medium human development, FMD had an inverted U-shaped effect on ecological footprint. In low human development economies, FMD reduced ecological footprint. In the CO2 emissions model, FMD showed a U-shaped effect in high human development economies and had an inverted U-shaped effect in low human development economies. Moreover, inclusive growth raised CO2 emissions.

Adams and Fotio [26] examined 36 African economies from 1990-2018 and documented that urbanization, REC, FMD, and industrialization raised CO2 emissions, which reduced environmental quality. Thus, African integration policies should be focused on the financial sector’s suitability, better urban planning, energy efficiency, and REC. Mahmood et al. [27] explored East Asia to scrutinize the effects of FMD and FDI on emissions in spatial analysis and confirmed spillover effects. The EKC was also substantiated and FDI raised emissions. FMD has an insignificant influence on emissions. Zafar et al. [4] probed the influences of education and FMD in Asia from 1990-2018 and found that income, education, and energy usage intensified the carbon emissions. However, technology and FMD reduced carbon emissions. It was suggested that investment in technology and FMD could mitigate emissions. Van and Phuong [28] focused on Southeast Asia to gauge the influence of REC, FMD, and FDI from 2000-2020 and found that FMD and FDI could not affect CO2 emission. REC reduced CO2 emissions and urbanization accelerated CO2 emissions due to enhanced mobility and industrial activities.

Literature also worked on panels of countries with economic classification. For instance, Raghutla and Chittedi [29] analyzed the effects of FMD and urbanization on sustainable economic progress in BRICS from 1998-2016. FMD, technology, and energy raised economic progress and FMD, urbanization, and technology helped reduce emissions. Moreover, the feedback between FMD and emissions was substantiated. Ganda [30] examined the combined effects of FMD and resources’ rents on carbon emissions in BRICS from 1990-2019 and corroborated a U-shaped connection in the EKC analysis. FMD from institutions and markets raised emissions. However, the interaction of FMD from institutions and markets with resources’ rents reduced emissions. Thus, FMD could reduce emissions with optimal allocation of natural resources. Baloch and Danish [31] examined BRICS from 1995-2016 and found that FMD contributed to the amplified carbon emissions. Surprisingly, environmental regulations also degraded the environment by stimulating emissions. Thus, the environmental regulations in BRICS economies were not well-designed. Dhingra [32] explored FMD, income, globalization, and GHG emissions nexus in the BRICS nations from 1991-2020. He found that FMD raised GHG emissions, and income and globalization reduced emissions in BRICS economies except China. Thus, FMD was responsible for environmental problems in these faster-growing economies, which needed attention to have pleasant effects.

Xu et al. [33] investigated the G7 to analyze the effects of FMD and REC from 1986-2019 and found that FMD raised CO2 emissions. Thus, FMD hindered progress towards environmental Sustainability. Rehan et al. [34] investigated CO2 emissions, REC, FMD, and trade nexus in G20 and some EU countries from 1990-2019 and found that REC and FMD raised CO2 emissions. Conversely, trade reduced CO2 emissions. Interestingly, developed countries increased carbon emissions more than non-developed countries. Thus, it was suggested that the FMD should support environmentally friendly technologies to mitigate CO2 emissions and thus prevent environmental damage. Shahbaz et al. [35] probed the nonlinear impact of FMD in G-7 countries with long data from 1870-2014 and found varied impacts of FMD on CO2 emissions. The relationship was found as M-shaped in 3 countries, inverted N-shaped in 3 countries, and W-shaped in Germany.

Bekun et al. [36] scrutinized the EKC including institutional quality in the analyses of E7 countries and confirmed a cointegration between income, institutional quality, trade, energy investments, and FMD. Moreover, the EKC hypothesis was validated. So, income initially worsened environmental quality and then improved it. FMD, energy investments, and trade reduced emissions. However, institutional quality raised emissions. Thus, it was suggested to adopt stringent environmental regulations for sustainable growth. Chen et al. [37] scrutinized the nexus between FMD, industrialization, and pollution in the E7 from 1996-2021 and documented that energy poverty and intensity accelerated CO2 emissions. Further, FMD initially raised emissions and reduced emissions at higher development levels. Thus, the study suggested policies for promoting energy efficiency, REC, and sustainable industrial practices in the E7 countries. Jóźwik et al. [38] scrutinized the effect of FMD on emissions from the top 11 nuclear nations from 1993-2019 and found that FMD helped reduce emissions. Moreover, the EKC was substantiated. Thus, economic growth initially worsened the environment and then improved it. However, it degraded environmental quality again at the last stage of analysis. Thus, investments in R&D for innovative solutions with nuclear energy for reducing carbon emissions could be beneficial for the environment.

Some studies investigate the FDI, FMD, and emissions nexus in the countries with different level of development. For instance, Geyikci et al. [39] analyzed the cointegration between FMD and emissions in 13 developing countries. FMD accelerated CO2 emissions and energy usage. It was suggested that the effects of FMD on energy usage and emissions should be considered in tracing financial policies. Habiba and Xinbang [40] analyzed the effect of various dimensions of FMD in developed and emerging economies from 2000-2018 and documented that aggregated and disaggregated FMD compacted CO2 emissions in all countries. In contrast, financial institutions reduced emissions in developed economies and raised emissions in emerging economies. Thus, it was suggested to adopt REC to mitigate emissions. Kim et al. [41] explored the effects of institutions on the nexus between FMD and the environment. They found that FMD hindered green technology growth and increased energy usage and emissions. However, this effect is moderated by institutions. Thus, less competitive FMD lend more to the households and increase emissions. Otherwise, a competitive FMD lends to the private sector by promoting green technology development and reducing emissions. Thus, institutions could shape the relationship between FMD and emissions by promoting competition in the financial market. Akan [42] scrutinized the impact of FMD including energy usage in the model from 1990-2021. He also highlighted the importance of concentrating on the effects of FMD through energy consumption on emissions. The research proposed that the impact of FMD and financial institutions on emissions should be controlled by promoting energy efficiency. Irfan et al. [43] evaluated and substantiated the mitigating impact of energy efficiencies on pollution in 55 mixed economies from 1992-2017 and also substantiated the EKC. Moreover, financial markets in developed economies and financial institutions in developing economies both played the moderating effect.

Literature has also conducted studies for single country. For instance, Shen et al. [44] scrutinized the influence of green investments and FMD on carbon emissions in China from 1995-2017. They originated that energy use and FMD accelerated carbon emissions. Green investments reduced CO2 emissions. It was suggested by the authors to promote green investments and clean regulations for the financial market. Yuan et al. [45] reconnoitered the nexus between FMD and the environment in China from 2000-2019. The authors found that higher FMD reduced carbon emissions in rich provinces by increasing FDI. Moreover, during financial recessions, financial markets reduced emissions. However, in post-recession, financial markets enhanced decoupling through technological improvements. Topcu [46] explored the effects of FMD in China regarding sustainability, production, and consumption and found that FMD reduced emissions. Considering political corruption's negative externality on FMD, the results were found opposite. Thus, enhancing FMD would have a significant environmental benefit clubbing with governance and anti-corruption indicators. Khanday et al. [47] scrutinized the effect of institutions on the interconnection between FMD and pollution in India and documented that FMD and institutional quality positively influenced environmental sustainability. However, economic growth raised emissions. Thus, the PHH was corroborated in India, which explained that institutions initially helped FMD in reducing emissions. Later, financial system inefficiencies raised emissions. Ngcobo and De Wet [48] examined FMD, income, and REC nexus in South Africa from 1990-2021. The authors found that both FMD and economic growth raised REC. Thus, this research suggested policy reforms to enhance REC infrastructure reducing the country's heavy reliance on coal and improving environmental sustainability.

A recent trend of literature has suggested the application of asymmetrical analysis to inquire the nexus betweenFMD, and emissions. For instance, Boufateh and Saadaoui [49] examined the asymmetrical influence of FMD on emissions in 22 African countries from 1980-2014 and found that positive FMD shocks reduced emissions while financial instability increased CO2 emissions. Moreover, the EKC was supported. The study suggested the African governments to implement durable policies to develop financial systems, fund green projects with less vulnerable to negative shocks, and improve long-term financial development to reduce market imperfections and pollution. Xu et al. [50] analyzed the impact of FMD in Europe from 2000-2020 and substantiated that increasing interest rates reduced CO2 emissions. Conversely, bank credit increased CO2 emissions in some industries. Thus, tight monetary policy could reduce environmental problems and a higher credit ratio would harm the environment. Mar’I et al. [51] probed the effect of FMD in 5 major polluting economies from 1990-2019 and found the asymmetrical impacts of FMD on pollution. Hence, financial institutions and FMD affected CO2 emissions in different ways. Thus, the study emphasized to promote environmentally sound financial products to mitigate the positive shocks from increasing CO2 emissions. Khoza and Biyase [52] explored the finance-emission nexus by examining the asymmetrical effects of FMD in South Africa and revealed that FMD promoted environmental quality. The financial institutions raised emissions. These results suggested devising strategies that align financial markets and institutions with the same environmental objectives to promote capital allocation in environmentally friendly projects.

This section highlights the importance of FMD, FDI, and economic growth in determining emissions in the large panels, regional panels, panels of the countries with economic classification, the panels of the countries with level of development, and country-specific studies. Most of the literature has explored the symmetrical effects of FMD, FDI, and economic growth on emissions. A few recent studies worked on this relationship with asymmetrical analyses. Moreover, the testing of the asymmetrical effects of FMD, FDI, and economic growth on emissions is missing in Saudi literature. Thus, the present study contributes to Saudi literature by testing the asymmetrical effects of FMD, FDI, and economic growth on carbon emissions.

FMD can affect the environment of any economy. For instance, FMD increases the credit, which may have a scale effect. This scale effect might increase economic activities and would raise energy consumption and pollution consequently. Moreover, FMD could finance energy-intensive products [2], which would lead to emissions. However, the FMD could also reduce emissions by financing clean projects and technologies [3]. The exact macroeconomic effects of FMD on pollution is an empirical question, which is investigated for Saudi Arabia in this research. Moreover, FDI could also play an effective role in the promotion of clean technologies as FDI might transfer the technology to any FDI recipient economy. Moreover, foreign investors from developed countries are using comparatively better environmental standards in production [7], which would reduce emissions. However, FDI can also be done in a pollution-oriented industry as per arguments of the PHH [5]. Like, foreign investors are investing in economies with relaxed ecological regulations to save the cost of production and to remain more competitive in the market. Thus, the exact macroeconomic impact of FDI is also an empirical question in any economy. Lastly, we cannot ignore the role of income in determining the emissions. In addition, the recent literature has hypothesized the asymmetrical effect of financial development on emissions [49-52]. Following the literature, we are also hypothesizing the asymmetrical effects of all independent variables on carbon emissions in the following way:

$\text{C}{{\text{E}}_{t}}=f\left( \text{GDPC}{{\text{P}}_{t}},~\text{GDPC}{{\text{N}}_{t}},\text{FMD}{{\text{P}}_{t}},\text{FMD}{{\text{N}}_{t}},\text{FDI}{{\text{P}}_{t}},\text{FDI}{{\text{N}}_{t}} \right)$ (1)

$\text{GDPC}{{\text{P}}_{t}}=\mathop{\sum }_{j=1}^{t}GDPC_{j}^{+}=\mathop{\sum }_{j=1}^{t}\text{max}\left(\Delta GDP{{C}_{j}},0 \right)$ (2)

$\text{GDPC}{{\text{N}}_{t}}=\mathop{\sum }_{j=1}^{t}GDPC_{j}^{-}=\mathop{\sum }_{j=1}^{t}\text{min}\left(\Delta GDP{{C}_{j}},0 \right)$ (3)

$\text{FMD}{{\text{P}}_{t}}=\mathop{\sum }_{j=1}^{t}FMD_{j}^{+}=\mathop{\sum }_{j=1}^{t}\text{max}\left(\Delta FM{{D}_{j}},0 \right)$ (4)

$\text{FMD}{{\text{N}}_{t}}=\mathop{\sum }_{j=1}^{t}FMD_{j}^{-}=\mathop{\sum }_{j=1}^{t}\text{min}\left(\Delta FM{{D}_{j}},0 \right)$ (5)

$\text{FDI}{{\text{P}}_{t}}=\mathop{\sum }_{j=1}^{t}FDI_{j}^{+}=\mathop{\sum }_{j=1}^{t}\text{max}\left(\Delta FD{{I}_{j}},0 \right)$ (6)

$\text{FDI}{{\text{N}}_{t}}=\mathop{\sum }_{j=1}^{t}FDI_{j}^{-}=\mathop{\sum }_{j=1}^{t}\text{min}\left(\Delta FD{{I}_{j}},0 \right)$ (7)

All positive and negative series are generated by using the methodology of Shin et al. [14] in the following way:

In the above equations, GDPCt is GDP per person in constant Saudi Riyals (SR). FMDt is a credit to the private sector as a percentage of GDP. FDIt is FDI net inflows as a percentage of GDP. All data on these macroeconomic variables are collected from the World Bank [53] and Saudi Central Bank [54]. CEt is tCO2 emissions per person, which is sourced from the Global Carbon Atlas [55]. All series are converted into natural logarithms except FDI, which contains mixed of positive and negative values. All data is collected from 1970-2021. Eqs. (2), (4), and (6) capture the partial sum of positive changes in GDP, FMD, and FDI, respectively, to generate the increasing series of variables. Moreover, Eqs. (3), (5), and (7) capture the partial sum of negative changes in GDP, FMD, and FDI, respectively, to generate the decreasing series of variables. Thus, the Shin et al. [14] methodology helps to generate increasing and decreasing series of GDP, FMD, and FDI to test the asymmetrical effects of these series on CO2 emissions. The generated series in Eqs. (2)-(7) are used in Eq. (1) to claim an asymmetrical hypothesized model. Before proceeding to further analysis, the unit root would be tested by using Ng and Perron's [56] statistics in the following way:

$M Z_a^d=\left\lceil\frac{X_T^d}{T}\right\rceil^2 / 2 K-f_0 / 2 K$ (8)

$M S B^d=\left[\frac{k}{f_0}\right]^{1 / 2}$ (9)

$M Z_t^d=M Z_a^d \cdot M S B^d$ (10)

$M P T_T^d=\left[c^2 \cdot K \cdot \frac{Y_T^d}{f_0}+\frac{1-c}{T} \cdot \frac{Y_T^d}{f_0}\right]$ (11)

The hypothesized asymmetrical model in Eq. (1) will be regressed by applying the ARDL framework of Pesaran et al. [57]:

$\begin{aligned} \Delta \mathrm{CE}_t=a_0+a_1 & {CE}_{t-1}+a_2 G D P C P_{t-1} \\ & +a_3 G D P C N_{t-1}+a_4 F M D P_{t-1} \\ & +a_5 F M D N_{t-1}+a_6 F D I P_{t-1} \\ & +a_7 F D I N_{t-1}+\sum_{i=1}^{n-1} b_{1 i} \Delta C E_{t-i} \\ & +\sum_{i=0}^{n-1} b_{2 i} \Delta G D P C P_{t-i} \\ & +\sum_{i=0}^{n-1} b_{3 i} \Delta G D P C N_{t-i} \\ & +\sum_{i=0}^{n-1} b_{4 i} \Delta F M D P_{t-i} \\ & +\sum_{i=0}^{n-1} b_{5 i} \Delta F M D N_{t-i} \\ & +\sum_{i=0}^{n-1} b_{6 i} \Delta F D I P_{t-i} \\ & +\sum_{i=0}^{n-1} b_{7 i} \Delta F D I N_{t-i}+\Omega_{1 t}\end{aligned}$ (12)

Eq. (12) may be termed as NARDL. The linear ARDL of Pesaran et al. [57] is transformed into the NARDL of Shin et al. [14] by using the increasing and decreasing series from Eqs. (2)-(7). The variables CEt-1, GDPCPt-1, GDPCNt-1, FMDPt-1, FMDNt-1, FDIPt-1, and FDINt-1 are regressed in Eq. (12) to apply the Wald test to verify cointegration in the model with a null hypothesis (a1=a2=a3=a4=a5=a6=a7=0). The rest lagged-differenced variables in Eq. (12) are regressed to remove possible endogeneity in the model to have robust results [57]. Later, the long-run effects can be calculated by following the normalizing procedure. Then, we can convert Eq. (12) into (13) by replacing the error correction term (ECTt-1) in the following way:

$\begin{aligned} \Delta \mathrm{CE}_t=a_8 E C T_{t-1} & +\sum_{i=1}^{n-1} b_{1 i} \Delta C E_{t-i} \\ & +\sum_{i=0}^{n-1} b_{2 i} \Delta G D P C P_{t-i} \\ & +\sum_{i=0}^{n-1} b_{3 i} \Delta G D P C N_{t-i} \\ & +\sum_{i=0}^{n-1} b_{4 i} \Delta F M D P_{t-i} \\ & +\sum_{i=0}^{n-1} b_{5 i} \Delta F M D N_{t-i} \\ & +\sum_{i=0}^{n-1} b_{6 i} \Delta F D I P_{t-i} \\ & +\sum_{i=0}^{n-1} b_{7 i} \Delta F D I N_{t-i}+\Omega_{1 t}\end{aligned}$ (13)

Eq. (13) will be regressed and the short run association will be validated by the parameter of (ECTt-1). Then, the estimated coefficients of variables will be utilized for short-run effects.

Table 1 shows descriptive statistics and most of the series are under-dispersed as their standard deviations are lesser than their means. The starting points of all increasing and decreasing series are the first values of the linear series. So, the minimum value of the increasing and maximum value of the decreasing series are equal.

Table 1. Descriptive statistics

|

Series |

Mean |

SD |

Minimum |

Maximum |

|

CEt |

2.6928 |

0.2176 |

2.0029 |

3.0383 |

|

GDPCPt |

12.3476 |

0.3916 |

11.2814 |

12.8757 |

|

GDPCNt |

10.2206 |

0.5632 |

9.6493 |

11.2814 |

|

FMDPt |

4.3445 |

1.3826 |

1.9951 |

6.5854 |

|

FMDNt |

0.5239 |

0.5867 |

-0.2731 |

1.9951 |

|

FDIPt |

28.6430 |

12.0535 |

0.1369 |

45.1119 |

|

FDINt |

-27.9855 |

11.4869 |

-42.3312 |

0.1369 |

As per the discussed methodology, the Ng-Perron test is applied to all series and reported in Table 2. It corroborates the non-stationarity of all series on the level. However, the stationarity of all series is corroborated by the first differences.

Table 2. Unit root test

|

Series |

MZa |

MZt |

MSB |

MPT |

|

CEt |

-7.6514 |

-2.2684 |

0.1999 |

8.0028 |

|

GDPCPt |

-7.3152 |

-2.2965 |

0.2251 |

7.2895 |

|

GDPCNt |

-7.5005 |

-1.9005 |

0.3125 |

8.0962 |

|

FMDPt |

-2.2211 |

-0.8022 |

0.4667 |

13.2145 |

|

FMDNt |

-4.9661 |

-1.4211 |

0.3065 |

16.5967 |

|

FDIPt |

-5.5944 |

-1.6667 |

0.2854 |

7.6549 |

|

FDINt |

-7.4996 |

-2.2387 |

0.1922 |

8.2141 |

|

ΔCEt |

-26.1123*** |

-4.7144*** |

0.1268*** |

3.0021*** |

|

ΔGDPCPt |

-25.7415*** |

-4.6125*** |

0.1415*** |

2.8965*** |

|

ΔGDPCNt |

-25.5966*** |

-3.4963*** |

0.1621*** |

2.9662*** |

|

ΔFMDPt |

-24.9967*** |

-3.6122*** |

0.1452*** |

2.7941*** |

|

ΔFMDNt |

-25.7456*** |

-4.6152*** |

0.1402*** |

3.1111*** |

|

ΔFDIPt |

-25.9025*** |

-4.7152*** |

0.1256*** |

2.8856*** |

|

ΔFDINt |

-25.5214*** |

-3.7414*** |

0.1159*** |

2.9964*** |

Note: *** is showing stationarity at a 1% significance level.

Using Eq. (12), the ARDL equation is regressed and tested for cointegration by applying the Bound test in Table 3. The F-value (5.6352) from this test is higher compared to the critical value at a 1% significance level. It proves the cointegration in Eq. (12). Moreover, diagnostic tests are also supported the statistical validity of regression by carrying a p-value of all diagnostic tests more than 0.1.

Table 3. Cointegration analysis

|

Dependent Variable |

F-Statistic |

Hetero |

Serial Corr. |

Normality |

Function |

|

ΔCEt |

5.6352 |

1.3964 (0.2667) |

0.2036 (0.7962) |

0.1635 (0.8999) |

2.0133 (0.1987) |

|

At |

1% |

5% |

10% |

|

|

|

Bound-statistic |

3.65-4.66 |

2.79-3.67 |

2.37-3.20 |

|

|

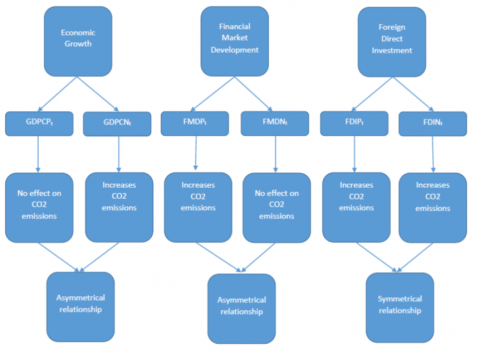

After corroborating the cointegration, the result of Eq. (12) can be used for long-run effects in Table 4. GDPCPt has an insignificant effect (p-value is more than 0.1) on CO2 emissions. Thus, the increasing economic growth is not helping reduce emissions and also not accelerating CO2 emissions. So, the effect of increasing economic growth is environmentally neutral. However, GDPCNt has a positive effect (p-value is less than 0.1) on CO2 emissions. Thus, the decreasing economic growth is helping reduce CO2 emissions. So, the effect of economic growth on CO2 is found asymmetrical. The effect of decreasing economic growth has a pleasant effect on the environment. It is possible that decreasing economic growth would result in lower industrial production due to lower demand. It reduces energy consumption from fossil fuels in Saudi Arabia from the production side. It also reduces CO2 emission consequently as 99% of energy is sourced from fossil fuels in Saudi Arabia. Moreover, lower income and production also resulted in lower transportation activities, and CO2 emissions were reduced from the transportation sector. Other than the production-sided CO2 emissions reduction, the reduced economic growth also reduced consumer spending, which reduced CO2 emissions from the consumption side. Thus, lowering economic growth reduces overall CO2 emissions in the economy and has a pleasant environmental effect.

Table 4. Long run results

|

Variables |

Coefficient |

SE |

T-Value |

P-Value |

|

GDPCPt |

1.8544 |

5.2031 |

0.3564 |

0.7231 |

|

GDPCNt |

0.9685 |

0.4829 |

2.0052 |

0.0526 |

|

FMDPt |

0.5478 |

0.1878 |

2.9163 |

0.0051 |

|

FMDNt |

-0.2854 |

0.7661 |

-0.3725 |

0.7211 |

|

FDIPt |

0.3667 |

0.1868 |

1.9633 |

0.0602 |

|

FDINt |

0.2965 |

0.1291 |

2.2969 |

0.0278 |

|

Intercept |

-5.6321 |

20.3545 |

-0.2767 |

0.7921 |

FMDNt has an insignificant effect (p-value is more than 0.1) and FMDPt has a positive effect (p-value is less than 0.1). Thus, the effect of FMD on CO2 emissions is asymmetrical and only increasing FMD is raising CO2 emissions. But decreasing FMD carries no environmental effect. This result may be claimed due to Ratchet effect. The increasing FMD is increasing economic activities. However, decreasing FMD does not reduce economic activities to reduce CO2 emissions. Increasing FMD provides more credit to the business sector to expand production by buying new machinery, which utilizes more fossil fuels and increases CO2 emissions. Moreover, FMD also provides consumption-purpose loans to buy vehicles, build houses, and buy electrical appliances, which increase fossil fuel consumption and contribute to CO2 emissions. Moreover, increasing consumption is also increasing demand for industrial products, which again puts pressure on the environment by increasing industrial production. On the whole, increasing industrial production, consumption, and transport due to credit supported by increasing FMD is raising fossil fuel consumption in Saudi Arabia.

Both FDIPt and FDINt have positive effects (p-value is less than 0.1) on CO2 emissions, which corroborates the PHH in Saudi Arabia. This result also corroborates the symmetrical effect of FDI on CO2 emissions. The positive effect of increasing and decreasing FDI in increasing and decreasing CO2 emissions, respectively, elaborates that FDI is floating in energy-intensive and pollution-oriented projects in Saudi Arabia. For instance, 87.2% of FDI inflows in Saudi Arabia have been attracted by the transportation sector, manufacturing sector, and trading in 2022. Thus, FDI developed the industrial infrastructure, which increases the production activities in the industrial sector and fossil fuel consumption. Moreover, FDI also boosts transportation projects, which directly increases fossil fuel consumption. In addition, FDI in trade also raises the trading activities and fossil fuel resultantly, which contributes to CO2 emissions. Figure 1 displays the summary of long-run results.

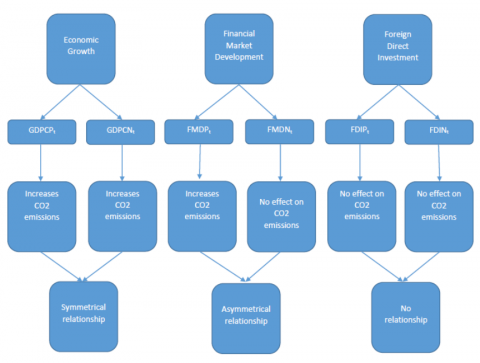

Table 5 shows the short-run results from Eq. (13) and corroborates the short relationship in the model with a negative parameter of ECTt-1 (p-value less than 0.1). In the short run, both ΔGDPCPt and ΔGDPCNt have positive effects (p-value is less than 0.1) on CO2 emissions, which corroborates the symmetrical effect of growth on emissions. Thus, increasing economic growth accelerates emissions in the short run, and decreasing growth is mitigating emissions. So, rising growth is increasing production, consumption, and transportation activities in the kingdom, which are raising fossil fuel consumption. Contrarily, decreasing growth is decreasing production, consumption, and transportation activities and is mitigating emissions.

Figure 1. Summary of long-run results

Figure 2. Summary of short-run results

Table 5. Short run results

|

Variables |

Coefficient |

SE |

T-Value |

P-Value |

|

ΔCEt-1 |

0.1488 |

0.0586 |

2.5386 |

0.0157 |

|

ΔGDPCPt |

0.2605 |

0.1106 |

2.3549 |

0.0214 |

|

ΔGDPCNt |

0.3575 |

0.1434 |

2.4936 |

0.0281 |

|

ΔFMDPt |

0.4843 |

0.1404 |

3.4493 |

0.0016 |

|

ΔFMDNt |

0.4002 |

0.8223 |

0.4867 |

0.6358 |

|

ΔFDIPt |

-0.1733 |

0.4666 |

-0.3714 |

0.7036 |

|

ΔFDINt |

0.0537 |

0.1628 |

0.3298 |

0.7541 |

|

ECTt-1 |

-0.2851 |

0.1651 |

-1.7269 |

0.0722 |

ΔFMDNt has an insignificant effect (p-value is more than 0.1) and ΔFMDPt has a positive effect (p-value is less than 0.1) on CO2 emissions, which validates the asymmetrical effect of FMD. It corroborates that increasing FMD is providing loans for production, consumption, and transportation activities, which are increasing fossil fuel consumption. The effects of ΔFDIPt and ΔFDINt are found insignificant (p-value more than 0.1). Thus, FDI could not harm the environment in the short run. Figure 2 displays the summary of short-run results.

FDI, FMD, and economic growth are potential determinants of environmental quality. Thus, this research investigates the effects of these factors on CO2 emissions in Saudi Arabia. Moreover, all factors could have asymmetrical effects on CO2 emission because of the possible Ratchet effect. The present research uses data from 1970 to 2021 for analysis. Moreover, the NARDL technique is applied to investigate asymmetrical relationships. In the long run, increasing economic growth raises emissions but decreasing economic growth does not reduce emissions, which corroborates the asymmetrical relationship. Thus, increasing economic growth raises production, consumption, trading, and transportation activities. These increasing activities increase fossil fuel consumption as Saudi 99% of energy is consumed from fossil fuels. Nevertheless, the decreasing economic growth could not affect emissions in the long run. The impact of economic growth is found positive and symmetrical in the short run. Increasing FMD raises CO2 emissions in the long and short run, which corroborates the asymmetrical effect in both periods. FMD is proxy by credit. Thus, increasing FMD provides more credit to the business sector to expand production by buying new machinery, consumers to buy vehicles, houses, and electrical appliances, and also finance the transport and trading sectors. Both increasing and decreasing FDI raise and mitigate emissions, respectively, in the long run. But FDI could not affect emissions in the short run. The long-run result corroborates the PHH. It is matched with the fact that FDI is flowing in the transportation sector, manufacturing sector, and trading activities in Saudi Arabia. Thus, increasing FDI is responsible for raising CO2 emissions.

The research suggests that the Saudi government should increase the taxes on FDI in pollution-oriented sectors and increase subsidies for FDI in environmentally friendly sectors. Moreover, the government should trace tight environmental standards for foreign investment in the country to avoid PHH in the economy. So, the effect of FDI on the environment could be pleasant. Similarly, the government should discourage the financing of pollution-oriented production and consumption activities by putting a carbon tax to internalize the environmental costs of CO2 emissions. Moreover, low-interest loans should be provided to the FDI in green projects for renewable energy production, clean technology, and sustainable infrastructure. The government should encourage green bonds to finance projects with positive environmental outcomes.

The authors extend their appreciation to Prince Sattam Bin Abdulaziz University for funding this research work (Grant No.: PSAU/2024/02/28917).

[1] Mahmood, H., Alkhateeb, T.T.Y., Furqan, M. (2020). Oil sector and CO2 emissions in Saudi Arabia: Asymmetry analysis. Humanities and Social Sciences Communications, 6(1): 0088. https://doi.org/10.1057/s41599-020-0470-z

[2] Zhang, Y.J. (2011). The impact of financial development on carbon emissions: An empirical analysis in China. Energy Policy, 39(4): 2197-2203. https://doi.org/10.1016/j.enpol.2011.02.026

[3] Frankel, J.A., Romer, D. (1999). Does trade cause growth? American Economic Review, 89(3): 379-399. https://doi.org/10.1257/aer.89.3.379

[4] Zafar, M.W., Zaidi, S.A.H., Mansoor, S., Sinha, A., Qin, Q. (2022). ICT and education as determinants of environmental quality: The role of financial development in selected Asian countries. Technological Forecasting & Social Change, 177: 121547. https://doi.org/10.1016/j.techfore.2022.121547

[5] Copeland, B.R., Taylor M.S. (1995). Trade and the environment: A partial synthesis. American Journal of Agricultural Economics, 77: 765-771. https://doi.org/10.2307/1243249

[6] Ministry of Investment. (2024). Saudi Arabia Foreign Direct Investment Report. https://misa.gov.sa/app/uploads/2024/03/saudi-arabia-foreign-direct-investment-report-january-2024.pdf.

[7] Birdsall, N., Wheeler, D. (1993). Trade policy and industrial pollution in Latin America: Where are the pollution havens? The Journal of Environment & Development, 2: 137-149.

[8] Abro, A.A., Alam, N., Murshed, M., Mahmood, H., Musah M., Rahman A.K.M.A. (2023). Drivers of green growth in the Kingdom of Saudi Arabia: Can financial development promote environmentally sustainable economic growth? Environmental Science and Pollution Research, 30(9): 23764-23780. https://doi.org/10.1007/s11356-022-23867-z

[9] Mahmood, H. (2022). The spatial analyses of consumption-based CO2 emissions, exports, imports, and FDI nexus in GCC countries. Environmental Science and Pollution Research, 29(32): 48301-48311. https://doi.org/10.1007/s11356-022-19303-x

[10] Mahmood, H., Furqan, M. (2021). Oil rents and greenhouse gas emissions: Spatial analysis of Gulf Cooperation Council countries. Environment, Development and Sustainability, 23(4): 6215-6233. https://doi.org/10.1007/s10668-020-00869-w

[11] Omri, A., Euchi, J., Hasaballah, A.H., Al-Tit, A. (2019). Determinants of environmental sustainability: Evidence from Saudi Arabia. Science of the Total Environment, 657: 1592-1601. https://doi.org/10.1016/j.scitotenv.2018.12.111

[12] Alkhateeb, T.T.Y., Alkahtani, N.S., Mahmood, H. (2018). Green human resource management, financial markets and pollution nexus in Saudi Arabia. International Journal of Energy Economics and Policy, 8(3): 33-36.

[13] Xu, Z., Baloch, M.A., Danish, K., Meng, F., Zhang, J., Mahmood, Z. (2018). Nexus between financial development and CO2 emissions in Saudi Arabia: Analyzing the role of globalization. Environmental Science and Pollution Research, 25: 28378-28390. https://doi.org/10.1007/s11356-018-2876-3

[14] Shin, Y., Yu, B., Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multiplier in an ARDL framework. In Festschrift in Honor of Peter Schmidt: Econometric Methods and Applications. Springer Science and Business Media: New York, NY, USA.

[15] Trinh, H.H., Sharma, G.D., Tiwari, A.K., Vo, D.T.H. (2022). Examining the heterogeneity of financial development in the energy-environment nexus in the era of climate change: Novel evidence around the world. Energy Economics, 116: 106415. https://doi.org/10.1016/j.eneco.2022.106415

[16] Jiang, C., Ma, X. (2019). The impact of financial development on carbon emissions: A global perspective. Sustainability, 11(19): 5241. https://doi.org/10.3390/su11195241

[17] Tran, T. (2023). Financial development and environmental quality: Differences in renewable energy use and economic growth. Polish Journal of Environmental Studies, 32(3): 2855-2866. https://doi.org/10.15244/pjoes/157652

[18] Uddin, M.M.M. (2020). Does financial development stimulate environmental sustainability? Evidence from a panel study of 115 countries. Business Strategy and the Environment, 29(6): 2871-2889. https://doi.org/10.1002/bse.2591

[19] Acheampong, A.O., Amponsah, M., Boateng, E. (2020). Does financial development mitigate carbon emissions? Evidence from heterogeneous financial economies. Energy Economics, 88: 104768. https://doi.org/10.1016/j.eneco.2020.104768

[20] Ahmad, M., Jiang, P., Majeed, A., Raza, M.Y. (2020). Does financial development and foreign direct investment improve environmental quality? Evidence from Belt and Road countries. Environmental Science and Pollution Research International, 27(19): 23586-23601. https://doi.org/10.1007/s11356-020-08748-7

[21] Anser, M.K., Khan, M.A., Zaman, K., Nassani, A.A., Askar, S.E., Abro, M.M.Q., Kabbani, A. (2021). Financial development, oil resources, and environmental degradation in pandemic recession: To go down in flames. Environmental Science and Pollution Research International, 28(43): 61554-61567. https://doi.org/10.1007/s11356-021-15067-y

[22] Kirikkaleli, D., Adebayo, T.S. (2020). Do renewable energy consumption and financial development matter for environmental sustainability? New global evidence. Sustainable Development, 29(4): 583-594. https://doi.org/10.1002/sd.2159

[23] Emenekwe, C.C., Onyeneke, R.U., Nwajiuba, C.U. (2021). Financial development and carbon emissions in Sub-Saharan Africa. Environmental Science and Pollution Research International, 29(13): 19624-19641. https://doi.org/10.1007/s11356-021-17161-7

[24] Nyeadi, J.D. (2022). The impact of financial development and foreign direct investment on environmental sustainability in Sub-Saharan Africa: Using PMG-ARDL approach. Ekonomska IstražIvanja, 36(2): 6270. https://doi.org/10.1080/1331677x.2022.2106270

[25] Annor, L.D.J., Robaina, M., Vieira, E. (2023). Financial development, inclusive growth, and environmental quality: Emerging markets perspective. Environment, Development and Sustainability, 1-27. https://doi.org/10.1007/s10668-023-04198-6

[26] Adams, S., Fotio, H.K. (2022). Economic integration and environmental quality: Accounting for the roles of financial development, industrialization, urbanization and renewable energy. Journal of Environmental Planning and Management, 67(3): 688-713. https://doi.org/10.1080/09640568.2022.2131510

[27] Mahmood, H., Furqan, M., Bagais, O.A. (2018). Environmental accounting of financial development and foreign investment: Spatial analyses of East Asia. Sustainability, 11(1): 13. https://doi.org/10.3390/su11010013

[28] Van, K.V.T., Phuong, T.N.L. (2023). Factors affecting the environmental quality: The role of renewable energy consumption and the financial market. International Journal of Energy Economics and Policy, 13(3): 586-591. https://doi.org/10.32479/ijeep.14373

[29] Raghutla, C., Chittedi, K.R. (2020). Financial development, energy consumption, technology, urbanization, economic output and carbon emissions nexus in BRICS countries: An empirical analysis. Management of Environmental Quality, 32(2): 290-307. https://doi.org/10.1108/meq-02-2020-0035

[30] Ganda, F. (2022). The nexus of financial development, natural resource rents, technological innovation, foreign direct investment, energy consumption, human capital, and trade on environmental degradation in the new BRICS economies. Environmental Science and Pollution Research International, 29(49): 74442-74457. https://doi.org/10.1007/s11356-022-20976-7

[31] Baloch, M.A., Danish, N. (2022). CO2 emissions in BRICS countries: What role can environmental regulation and financial development play? Climatic Change, 172(1-2): 9. https://doi.org/10.1007/s10584-022-03362-7

[32] Dhingra, V.S. (2023). Financial development, economic growth, globalisation and environmental quality in BRICS economies: Evidence from ARDL bounds test approach. Economic Change and Restructuring, 56(3): 1651-1682. https://doi.org/10.1007/s10644-022-09481-6

[33] Xu, D., Sheraz, M., Hassan, A., Sinha, A., Ullah, S. (2022). Financial development, renewable energy and CO2 emission in G7 countries: New evidence from non-linear and asymmetric analysis. Energy Economics, 109: 105994. https://doi.org/10.1016/j.eneco.2022.105994

[34] Rehan, M., Gungor, S., Qamar, M., Naz, A. (2023). The effects of trade, renewable energy, and financial development on consumption-based carbon emissions (Comparative policy analysis for the G20 and European Union countries). Environmental Science and Pollution Research International, 30(33): 81267-81287. https://doi.org/10.1007/s11356-023-28156-x

[35] Shahbaz, M., Destek, M.A., Dong, K., Jiao, Z. (2021). Time-varying impact of financial development on carbon emissions in G7 countries: Evidence from the long history. Technological Forecasting & Social Change/Technological Forecasting and Social Change, 171: 120966. https://doi.org/10.1016/j.techfore.2021.120966

[36] Bekun, F.V., Gyamfi, B.A., Köksal, C., Taha, A. (2023). Impact of financial development, trade flows, and institution on environmental sustainability in emerging markets. Energy & Environment, 35(6): 3253-3272. https://doi.org/10.1177/0958305x221147603

[37] Chen, K., Qammar, R., Quddus, A., Lyu, N., Alnafrah, I. (2024). Interlinking dynamics of natural resources, financial development, industrialization, and energy intensity: Implications for natural resources policy in emerging seven countries. Resources Policy, 90: 104809. https://doi.org/10.1016/j.resourpol.2024.104809

[38] Jóźwik, B., Gürsoy, S., Doğan, M. (2023). Nuclear energy and financial development for a clean environment: Examining the N-shaped environmental Kuznets curve hypothesis in top nuclear energy-consuming countries. Energies, 16(22): 7494. https://doi.org/10.3390/en16227494

[39] Geyikci, U.B., Çınar, S., Sancak, F.M. (2022). Analysis of the relationships among financial development, economic growth, energy use, and carbon emissions by co-integration with multiple structural breaks. Sustainability, 14(10): 6298. https://doi.org/10.3390/su14106298

[40] Habiba, U., Xinbang, C. (2022). The impact of financial development on CO2 emissions: New evidence from developed and emerging countries. Environmental Science and Pollution Research International, 29(21): 31453-31466. https://doi.org/10.1007/s11356-022-18533-3

[41] Kim, D.H., Wu, Y.C., Lin, S.C. (2022). Carbon dioxide emissions, financial development and political institutions. Economic Change and Restructuring, 55(2): 837-874. https://doi.org/10.1007/s10644-021-09331-x

[42] Akan, T. (2023). Explaining and modeling the mediating role of energy consumption between financial development and carbon emissions. Energy, 274: 127312. https://doi.org/10.1016/j.energy.2023.127312

[43] Irfan, M., Mahapatra, B., Ojha, R.K. (2023). Energy efficiency and carbon emissions in developed and developing economies: Investigating the moderating role of financial development. Journal of Quantitative Economics, 21(2): 437-455. https://doi.org/10.1007/s40953-023-00346-x

[44] Shen, Y., Su, Z.W., Malik, M.Y., Umar, M., Khan, Z., Khan, M. (2021). Does green investment, financial development and natural resources rent limit carbon emissions? A provincial panel analysis of China. Science of the Total Environment, 755: 142538. https://doi.org/10.1016/j.scitotenv.2020.142538

[45] Yuan, R., Liao, H., Wang, J. (2022). A nexus study of carbon emissions and financial development in China using the decoupling analysis. Environmental Science and Pollution Research International, 29(58): 88224-88239. https://doi.org/10.1007/s11356-022-21930-3

[46] Topcu, M. (2024). Financial market development and carbon emissions: The transmission mechanisms and the role of political corruption. Finance Research Letters, 59: 104716. https://doi.org/10.1016/j.frl.2023.104716

[47] Khanday, I.N., Wani, I.U., Tarique, M. (2023). Do financial development and institutional quality matter for ecological sustainability in the long run? Evidence from India. Management of Environmental Quality, 34(6): 1668-1689. https://doi.org/10.1108/meq-01-2023-0002

[48] Ngcobo, R., De Wet, M.C. (2024). The impact of financial development and economic growth on renewable energy supply in South Africa. Sustainability, 16(6): 2533. https://doi.org/10.3390/su16062533

[49] Boufateh, T., Saadaoui, Z. (2020). Do asymmetric financial development shocks matter for CO2 emissions in Africa? A nonlinear panel ARDL-PMG approach. Environmental Modeling & Assessment, 25(6): 809-830. https://doi.org/10.1007/s10666-020-09722-w

[50] Xu, B., Li, S., Afzal, A., Mirza, N., Zhang, M. (2022). The impact of financial development on environmental sustainability: A European perspective. Resources Policy, 78: 102814. https://doi.org/10.1016/j.resourpol.2022.102814

[51] Mar’I, M., Seraj, M., Tursoy, T. (2023). Investigating the causality between financial development and carbon emissions: A quantile-based analysis. Environmental Science and Pollution Research International, 30(40): 92983-93001. https://doi.org/10.1007/s11356-023-28971-2

[52] Khoza, S., Biyase, M. (2024). The symmetric and asymmetric effect of financial development on ecological footprint in South Africa: ARDL and NARDL approach. Frontiers in Environmental Science, 12: 7977. https://doi.org/10.3389/fenvs.2024.1347977

[53] World Bank. (2024). World Development Indicators. The World Bank, Washington DC, United States. https://databank.worldbank.org/source/world-development-indicators/Series/NE.GDI.FTOT.ZS.

[54] Saudi Central Bank. (2024). Saudi Arabian Monetary Agency Yearly Statistics. https://www.sama.gov.sa/Pages/PageNotFoundError.aspx?requestUrl=https://www.sama.gov.sa/en-US/EconomicReports/Pages/YearlyStatistics.aspx.

[55] Global Carbon Atlas. (2024). http://www.globalcarbonatlas.org/en/CO2-emissions, accessed on Jul. 20, 2024.

[56] Ng, S., Perron, P. (2001). Lag length selection and the construction of unit root tests with good size and power. Econometrica, 66: 1519-1554. https://doi.org/10.1111/1468-0262.00256

[57] Pesaran, M.H., Shin, Y., Smith, R.J. (2001). Structural analysis of vector error correction models with exogenous I(1) variables. Journal of Econometrics, 97: 293-343. https://doi.org/10.1016/S0304-4076(99)00073-1