Petro Nikiforov![]() | Alla Abramova

| Alla Abramova![]() | Artur Zhavoronok*

| Artur Zhavoronok*![]() | Nataliia Bak

| Nataliia Bak![]() | Vitalii Yaremchuk

| Vitalii Yaremchuk![]() | Yurii Kulynych

| Yurii Kulynych![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The study is dedicated to the scientific justification of the need to strengthen green taxation in the context of the Green Deal implementation and the greening of EU countries based on a comprehensive analysis of the effective functioning of the green taxation system, and presents the following vectors of its improvement. Scientific approaches to the interpretation of the essence of the economic value of green taxation, taking into account the systematicity of the economic, socio-political, innovative and infrastructural goals in the conditions of modern challenges, have been studied. Based on the international system of economic indicators, in particular the Environmental Policy Stringency Index, the actual state of green taxation in EU countries was assessed. By applying a methodological approach based on comparing the cost characteristics of regulation and stimulation of the ecologically oriented business activity of business entities with the cost characteristics of the tax burden and the regulatory nature of the impact due to the use of environmental taxation objects and damage to the environment, an assessment of the effectiveness of green taxation was carried out in 12 EU countries. The architecture of the environmental taxation environment of EU countries is presented, the interrelated elements of which are defined as the legal framework of green taxation, the toolkit for the Green Deal implementation with an emphasis on green taxation, as well as systemically important market transformations capable of influencing the economic and environmental behavior of business entities by using natural resources and pollution of the natural environment under the influence of time factors, globalization changes and subsequent future uncertainties. The author's approach to increasing the efficiency and improvement of green taxation, which is expedient to implement to achieve the Green Deal goals and the formation of the environmental security system of the European region, is substantiated.

environmental security, environmental taxation, environmental policy, ecological growth, green taxation, tax policy, tax administration, Green Deal, regulatory instruments, behavioral influences, globalization, risks

Rapid negative climate changes, non-renewable loss of biodiversity and irrational consumption of natural resources in the world, in particular EU countries, require an adequate response and effective reform of the main approaches of the impact on economically active business entities within the framework of achieving stability of economic systems, social capacity of countries - the sustainable development goals.

Today, all countries of the world, aware of the urgency of the environmental security, are adopting relevant legal acts at the national level, intensively developing technological innovations, market-oriented reforms, adjusting industrial structures and achieving regional balance. The EU, competing with the USA, China can achieve the status of a global climate leader thanks to the application of special tools of economic and political regulation, in particular green taxation - measures of the behavioral influence in the form of the environmental and tax policy tools aimed at achieving the Green Deal goals and sustainable development. Accordingly, the main motive is to set prices for negative external consequences through tax interventions that increase the price of environmentally harmful resources or activities, and motivate to change economic behavior along the lines of rational use and replacement of the resource base.

The priority basis for achieving these goals should be the improvement of the regulatory mechanism for environmental protection through green taxation tools based on existing scientific, practical and methodological approaches and tools. We are talking about revising, in accordance with the system of regulatory legal acts of EU countries, tax levers of influence through tax benefits, sanctions, expansion of the tax base, etc., to harmonize and form uniform environmental business rules. In addition, the specified economic toolkit will cause changes in behavior and lead to the creation of new jobs, because tax incentives, in particular in investments - new "environmentally clean" technologies, will become an important source of employment and development of business entities. Therefore, when economic instruments bring financial income, the appropriate use of such income also serves as an important contribution to raising the income level of the population and to economic growth.

The specified arguments determined the setting of the goal within the study, which is manifested in the identification of opportunities for tax incentives for the greening of economy and development of recommendations for further development of the green taxation tools.

In the conditions of the rapid global economic, political and environmental changes caused by changes in the world system, uncertainty and the system of risks, governments of the countries of the world increasingly set themselves the task of ensuring the conditions for their economic growth [1-3].

International management experience makes it possible to clarify the essence of economic growth, which is reflected in the systematic increase of economic indicators in combination with the constant increase in indicators of the social standard of living of the population, improvement of the quality of the environment and optimization of resource and raw material supply [4, 5]. The issue of the relationship and mutual influence of economic development and the state of the ecological and resource environment has long been recognized as a direction of researches [6, 7], however, modern realities emphasize this especially acutely.

A wide galaxy of scientists and practitioners constantly discuss this issue. Some of them [8] advocate the idea of a significant boost to economic development due to the low impact of the economic activity on the environment using modern intellectual technologies, in particular information and communication technologies, biotechnology, nanotechnologies, renewable energy sources, low-carbon agriculture, waste processing, etc. Other representatives [8] are inclined to believe that a favorable environment for economic development can be created due to a complex of state and corporate, national and subnational policies, sectoral, tax, financial, regulatory, which will contribute to increasing the investments volume, and secondarily motivate the creation of jobs, development of production chains, reducing environmental impact and ecological consequences, while restoring the productive potential and productive capacity of the natural capital.

We share the opinion [9, 10] regarding the universal and exclusive ability of the use of state regulatory instruments (state finances within the framework of the state revenue generation) to influence economic results that stimulate the introduction of environmental technologies. In particular, the main idea of using taxes to overcome negative externalities dates back to 1920, when Pigou emphasized environmental taxes as key market instruments and carbon taxes in the context of climate changes.

Some scientists [11-14] share the view that the introduction of green taxation causes a number of impacts on green development on the part of economy, environment and resources. Researches [15-17] show different effects of green taxation on economic growth. Environmental tax reforms have been found to improve economic growth in a growing economy [18-20]. This improvement is due to the externality of ecological production [21] and the tax shift towards profit. In addition, a higher tax on energy will lead to the higher economic growth if labor resources are mobile and the elasticity of substitution in production between scarce factors and energy is less than one [22, 23]. However, green taxation has a negative impact on economic growth when its impact on socio-economic and environmental indicators is considered comprehensively using the general equilibrium model [24-26].

Current experience in the application of green taxation is considered in the previous works [27-29].

Cordova-Buiza et al. [30], it is justified that the state’s intervention in market processes through green taxation does not reduce, but increases its efficiency. Ecological taxation makes it possible to overcome "market failures" associated with insufficient motivation of business entities to protect the environment and preserve biodiversity, which is especially evident in developing countries. Technologies of the "smart" economy with artificial intelligence make it possible to significantly improve green taxation [31-34].

At the same time, many researchers believe that green taxation is environmentally beneficial, as it curbs pollution and reduces carbon emissions. Liu et al. [35] demonstrate that green taxation can contribute not only to the effect of the pollution control, but also to the reduction of environmental losses. Piciu and Tric [36] prove that green taxation can be returned to the polluters, that is, under certain conditions, an environmental tax can reduce pollution and protect the environment. Tamura et al. [37] believe that green taxation is effective for full control of carbon dioxide emissions only when a technology with a high degree of emission elimination and low cost is developed. Environmental tax shocks can stimulate carbon reduction. Wang et al. [38] demonstrate that higher levels of the environmental tax and carbon tax will contribute to greater reductions in CO2 emissions.

In terms of resources, the introduction of green taxation can also save resources to avoid their waste. The environmental tax is a factor that affects resource recovery, although the higher the environmental tax, the higher the resource recovery rate. Piciu and Trick [36, 39] believe that the environmental tax can stimulate the recycling of natural resources, and it is a significant part of the environmental policy in Europe. The environmental tax collection is beneficial for the countries with depleted resources.

The above analysis of the impact of green taxation on sustainable development mainly comes from one aspect - economic, pollution and resources. In addition, some studies begin to analyze the impact of the environmental tax on green development from two aspects. Based on the endogenous growth model, Xin [40] argue that green taxation can improve the environment quality on the one hand and increase economic welfare on the other hand. Xin [40] use econometric modeling to study the impact of green taxation in Europe. Their findings show that green growth can not only contribute to long-term economic development, but also contribute to environmental improvements. Xin [40] demonstrates that green taxation can significantly reduce carbon emissions and improve the quality of the economic environment under certain conditions using a large number of simulations.

As for scientific approaches to improve green taxation, they are most vividly systematized and highlighted by Congjuan et al. [41], who presented a set of green taxation tools, which included the following:

1) elimination of the environmentally harmful subsidies, creating tax space for green incentives;

2) provision of financial support for the green technologies’ implementation (reduction of capital costs, provision of state capital and tax benefits);

3) implementation of targeted tax incentives (tax deductions and exemptions for green technologies);

4) introduction of tax incentives that prevent the use of technologies that pollute the environment (a tax on carbon emissions or a system of trading emission quotas);

5) state investments in the "green" infrastructure (railways, sanitation, energy and public transport) through tax preferences.

There is a broad agreement among environmental economists that taxes are an indispensable tool for the effective strategy for sustainable development. However, the specifics of climate change require expanding the view of green taxation as an exclusive solution against climate change and depletion of natural resources, which increases the level of environmental danger. Under such circumstances, the urgent issue of improving green taxation should be the cooperation of the academic community of ecologists, economists, and sociologists on the way to developing completely new and unconventional instruments and approaches to tax policy.

The author's team believes that economic growth is impossible without improving the environment and preventing negative climate changes, and the effective tool for achieving these goals should still be improvement of the macroeconomic toolkit of green taxation due to its exceptional ability to have a significant impact on both short-term and long-term sustainable social -economic and ecological growth.

Based on the study of the theoretical framework, systematising the existing scientific and methodological approaches, the author's own methodological vision of the system of indicators for assessing the impact of environmental policy and green taxation on the level of economic development of countries is proposed. The use of the presented approach can be useful in making managerial decisions.

To achieve the objectives of improving green taxation in the context of the implementation of the Green Deal agreement and sustainable development, a complex of general scientific and special research methods was applied in the scientific research: theoretical generalization, induction, comparison - to identify problematic aspects of green taxation, systematization of green taxation tools; methods of analysis and synthesis - to assess the real state of the payment of these taxes and identify their subsequent trends; graphical and tabular methods - for visual illustration of the architecture of the green taxation environment; the abstract-logical method for summarizing research results and determining priority directions for increasing the effectiveness level of green taxation.

In the international practice, the Environmental Policy Stiffness Index (EPS) is used to assess the impact of the environmental policy on the country's economy as a country-a specific and internationally comparable indicator of the severity of the environmental policy. This index demonstrates the degree to which the environmental policy sets an explicit or implicit price for pollution of the natural environment or environmentally harmful behavior of business entities. The normative values presented by the index are as follows:

1) 0 – no environmental policy;

2) 6 – strict environmental policy is applied.

The calculation mechanism of this index in the structure of market regulatory instruments takes into account such taxes as CO2 tax, diesel tax, NOx tax, income tax, which clearly characterizes the tax policy of states. At the same time, it should be noted that inclusion of the income tax in the calculations indicates imposition of the concept of double tax benefits within the framework of this tax regulation.

Evaluating a critically important role of green taxation for ensuring sustainable development, there is a need to study its effectiveness, which will be conducted according to the methodical approach presented below. Its structure involves analysing a set of indicators (socio-economic preferences, environmental taxes in the GDP structure, environmental costs and investment volumes) and comparing the calculated values with the regulatory ones to establish the actual level of impact and identify areas of regulation to achieve the planned sustainable development indicators. National economic indicators of 12 EU countries (Bulgaria, Denmark, Ireland, Spain, Luxembourg, Malta, Norway, the Netherlands, Portugal, Romania, Sweden, Switzerland) are the basis of the research information base. Others were not selected as the basis of the analysis due to the lack of the official statistical data, in particular the data on tax benefits from environmental taxes, which are the basis of methodological calculations. All economic indicators are consolidated by Eurostat.

The data selected for the analysis are used to determine the share of influence and separate assessment of indicators characterizing individual processes within the framework of the environmental regulation (including methods for determining the tax burden of taxpayers as a result of green taxation, as well as determining dynamic processes). The result of the study should be the indicator of comparison of the value characteristic of regulation and stimulation of the environmentally-oriented economic activity of economically active subjects with the value characteristic of the tax burden and the regulatory nature of the impact due to the use/consumption/sale of objects of the environmental taxation and damage to the environment.

Yes, the value characteristic of regulation and stimulation of ecologically oriented production/consumption (GTbenefits), contains a cost characteristic of the totality of tax benefits and preferences of social and environmental orientation relative to GDP:

$\begin{aligned} & G T_{ {benefits }} =\frac{G T_{ {energy } / b f}+G T_{ {transport } / b f}+G T_{ {pollution } / b f}}{G D P}\end{aligned}$, (1)

where, GPbenefits - total indicator of socio-ecological tax preferences, which characterizes the tax policy in the regulation and stimulation of environmental processes;

GTenergy/transport/pollution/bf – total indicator of social and environmental tax benefits from the transport environmental tax, energy and pollution taxation;

GDP – gross domestic product.

Value characteristics of the tax burden of the tax and regulatory nature as a result of the use/consumption/sale of objects of the environmental taxation and damage to the environment (GTGDP), includes the cost characteristics of the totality of tax payments of the environmental orientation relative to GDP:

$G T_{G D P}=\frac{G T_{{energy }}+G T_{ {transport }}+G T_{ {pollution }}}{G D P}$ (2)

where, GTGDP – total indicator of tax payments, which characterizes the tax policy in the regulation and stimulation of environmental processes;

GTenergy/transport/pollution – total indicator of the energy/transport/pollution tax.

Therefore, comparison of the proposed indicators of the characteristics of the state regulation of environmental taxation (GTbenefits і GTGDP) makes it possible to exclude GDP from further calculations due to its inability to fully characterize the economic growth:

$\begin{aligned} & G T_{\text {optim }}=\frac{\sum G T_{ {benefits }}}{G D P} / \frac{\sum G T_{G D P}}{G D P} =\frac{\sum G T_{ {benefits }}}{\sum G T_{G D P}} \\ & \end{aligned}$ (3)

Changes in the amount of environmental costs for improving/restoring the state of the natural environment are indicators of the regulation of environmental processes (yecolog) and quality of life of the population (Qlife).

$\mathrm{y}_{ {ecolog }}=\sum_{ {exp }=1}^{exp } \mathrm{y}_{ {exp }}$, (4)

where, yecolog – total indicator of the environmental damage, which characterizes economic losses and improvement/restoration of the state of the natural environment;

yexp – environmental costs in terms of estimated resources.

Actual values of the indicator of the quality of life of the population (Qlife) determined by Eurostat [42].

The influence of green taxation on the state of the investment activity in the environmental protection and energy-saving technologies is demonstrated by the indicator of the share of environmental taxes in the total volume of investments GTinvest:

$G T_{ {invest }}=\frac{G T}{ { Ivest }_{ {ecolog }}}$ (5)

where, Investecolog– volumes of investments in the environmental protection and energy-saving technologies.

The influence of green taxation on the actual costs of liquidation of the consequences of negative impact on the natural environment is demonstrated by the indicator of the share of the environmental taxes in the total costs of liquidation of the specified consequences GTexp:

$G T_{ {exp }}=\frac{G T}{E X P_{l i q}}$ (6)

where, EXPlip – the amount of actual expenses for the elimination of the consequences of pollution of the natural environment and depletion of natural resources.

Thus, the impact of green taxation on the ecological environment and identification of its regulatory properties will be determined based on the following economic-mathematical model:

$\begin{gathered}{K}_1=\frac{\mathrm{y}_{ {ecolog } \,t}}{\mathrm{y}_{ {ecolog }\, t-1}}, K_1 \rightarrow 0 \\ K_2=\frac{G T_{ {optim }\,t}}{G T_{ {optim }\, t-1}} \\ K_3=\frac{Q { life }_t}{Q { life }_{t-1}}, K_3 \rightarrow \infty \\ {K}_4=\frac{G T_{ {invest }\, t}}{G T_{ {invest }\, t-1}}, {K}_4>1 \\ {K}_5=\frac{G T_{ {exp } \,t}}{G T_{ {exp }\, t-1}}, {K}_5>1\end{gathered}$ (7)

where, $\mathrm{K}_1$ – coefficient of dynamic changes in the volume of the environmental protection costs in the analyzed period t, from the position of the efficiency of green taxation, which is heading towards 0.

$\mathrm{K}_2$ – resulting coefficient of green taxation relative to the preferential green taxation system and the tax burden within the framework of the environmental regulation in the analyzed period t;

$\mathrm{K}_3$ – coefficient of dynamic changes in the quality of life of the population in the analyzed period t, from the standpoint of the green taxation effectiveness, which tends to $+\infty$;

$\mathrm{K}_4$ – coefficient of dynamic changes in the value indicators of investment in the environmental protection and energy-saving projects in the analyzed period t, from the standpoint of the green taxation effectiveness, which > 1;

$\mathrm{K}_5$ – coefficient of dynamic changes in costs for the elimination of the negative impact on the natural environment and in the analyzed period t, from the standpoint of the green taxation effectiveness, which > 1.

The chosen coefficients provide for the universality of application of official statistical data of the selected countries for the study, and their choice is based on their participation in the processes of reproduction and economic growth.

Regarding the interpretation of the effectiveness of the calculated values, the proposed economic-mathematical model reflects the relationships within the production processes of business entities, in particular: increase or decrease in the resulting green taxation indicator indicates a change in the structure and functionality of the applied tax policy:

1) increase in the result of the numerator of the coefficient (K2) indicates a softening of the tax policy in relation to taxpayers both in general and in relation to their specific groups as a result of stimulating processes; decrease - about the strengthening of the tax policy and about the reverse processes of regulation;

2) increase in the result of the denominator of the coefficient (K2) indicates an increase in external costs, and a decrease indicates their reduction within the framework of the selected national tax policy of the environmental regulation.

A simultaneous decrease in the tax burden and preferential opportunities may indicate a change in the tax policy in connection with the deterioration of the general economic situation and vice versa. At the same time, the increase in the tax burden and preferential opportunities indicates a change in tax policy in connection with favorable conditions in the country. Thus, any change in the indicator of each of the groups will affect the result of the group indicator, thereby reflecting the factor changes of the implemented tax policy. Comparing the dynamic phenomena of indicators with the effectiveness of green taxation determines its impact on the environmental processes. Based on this, it is possible to establish whether there is an actual regulatory influence. Thus, dynamic changes of the analyzed coefficients make it possible to characterize the tax policy of the state in the regulation of environmental processes using the applied green taxation system.

The assessment of the green taxation effectiveness should be considered the satisfaction of the society with the level of quality of life for the permissible amount of the environmental damage according to the following criterion limits:

$0<K_1<1, K_2>0, K_3>1, K_4>1, K_5>1$

(optimisation of environmental protection costs, systematisation of preferential taxation in relation to the level of tax burden, improvement of living standards, reduction of costs of implementing investment programmes for projects, as well as reduction of costs associated with the elimination of the consequences of natural disasters, etc.);

$K_1>1, K_2>0, K_3>1, K_4<1, K_5>1 \text { or if } 0<K_1< 1, K_2>0,0<K_3<1, K_4>1, K_5>1$

(increased costs of environmental protection activities, insignificant level of preferential taxation with a rather high tax burden, lower living standards, increased costs of implementing investment programmes, increased costs of eliminating the consequences of natural disasters);

$K_1=0, K_3>1 \text { or if } K_1>1, K_2>0,0<K_3<1, K_4< 1, K_5<1$

(absence of environmental protection activities or their excessive level, elimination of preferential taxation with a high tax burden, lower living standards, reduced costs of investment programmes as a result of curtailing their activity, deterioration in financing of costs for eliminating the consequences of natural disasters).

It is advisable to annually evaluate the green taxation effectiveness. Under the conditions of complete or partial dissatisfaction with the results of such regulation with using the tax system, it is necessary to make the decisions regarding the tax policy correction through legal instruments, followed by assessment of the reforms carried out until the planned goals of the Green Deal and sustainable development of the EU countries are achieved.

Thus, the green taxation performance indicator is a universal tool that allows you to assess the effectiveness of environmental regulation from the point of view of taxation. We believe that based on the proposed methodical approach from the point of view of the obtained results, it becomes possible to monitor and analyze the impact of green taxation on the volume of the environmental losses, the level of the quality of life of the population, and the environmental investment activity of the studied countries and all EU member states in particular. The results of the study have the prospect of their application both at the national and EU levels. In fact, the results of the effectiveness of such taxation will make it possible to shift the imbalance of the main elements of the green taxation system in the form of the preferential and subsidiary taxation, as well as the tax burden with the subsequent adoption of taxation, and is the basis for making management decisions regarding the green taxation improvement in the EU environment.

The selected research methodology makes it possible to qualitatively analyze the impact of green taxation on sustainable development of the countries under study and, as a result, to propose measures to regulate taxation in EU countries aimed at achieving the goals of regulating the environmental processes, in particular the Green Deal and sustainable development of the countries under study.

The presence of EU countries as part of the world economic leaders should be ensured by sustainable economic development, the key components of which are social, economic and environmental stability. Accordingly, ecological stability is determined by ecological growth through the achievement of sustainable development based on increasing the ecological efficiency of production, consumption and deployment of the "green" economy in the medium and long term. The synergistic effect of the economic growth is confirmed by the fact that an important component of the sustainable development strategy of EU countries until 2050 on the way to achieving economic stability and effective adaptation to existing challenges is the implementation of the principles of the Green Deal agreement, designed to ensure the achievement of the climate balance goals.

The experience has established a particularly close dependence and mutual influence between economic and ecological growth: rapid economic development leads to the increase in the amount of pollution of the natural environment, which in turn motivates the search for tools of influence and prevention of depletion of natural resources. As a result, the implementation of measures on the ecological growth should be ensured by a stable financial system and its effective tools.

The following are the toolkit components in the European economic practice:

1) emission quotas market that companies buy or sell - stimulates business entities to reduce indicators of the environmental pollution and depletion of natural resources. Implemented through the European Emissions Trading System (ETS);

2) environmental subsidies - a source of financing assistance to business entities that will implement technologies on the environmental protection;

3) green taxation mechanism is an instrument of the behavioral influence on the individual consumption and production activity, which is implemented through the sub-instruments of pricing, benefits, standards and investments. In the EU, a relatively mature “green” tax system has already been formed with characteristic features determined by the national economic features, geographic location, social mentality, etc. The tax base can be determined according to different criteria, depending on the type of externalities that are regulated. In general, the priority goal of the green taxation is the motivation of participants to rational use of natural resources, optimization of the environmental pollution, as well as increasing tax revenues for financial implementation of opportunities to achieve the Green Deal goals.

Table 1. State indicators of the green taxation results in the EU-27 for 2013-2021

|

Indicator |

2013 Year |

2014 Year |

2015 Year |

2016 Year |

2017 Year |

2018 Year |

2019 Year |

2020 Year |

2021 Year |

|

Total tax revenues, billion euros |

4699.1 |

4813.4 |

4961.1 |

5111.5 |

5333.6 |

5535.4 |

5716.4 |

5507.2 |

6024.1 |

|

Environmental tax revenues, billion euros |

284.1 |

290.9 |

298.9 |

310.1 |

316.5 |

324.6 |

329.9 |

300.1 |

325.8 |

|

Share of the environmental tax in the total tax revenues structure, % |

6.0 |

6.0 |

6.0 |

6.1 |

5.9 |

5.9 |

5.8 |

5.5 |

5.4 |

|

Share of the environmental tax in the GDP structure, % |

2.5 |

2.5 |

2.4 |

2.5 |

2.4 |

2.4 |

2.4 |

2.2 |

2.2 |

The European green taxation system is represented by the following: taxes on energy (gasoline, diesel fuel, electricity for heating), transport, environmental pollution and taxes on resources (Figure 2). The main principle of its implementation is social justice, according to which a greater tax burden is placed on the entities that consume more and pollute the environment.

It is possible to understand the economic and financial significance of the green taxation in the EU-27 by finding out the main trends of its development (Table 1).

The analysis shows the annual absolute increase in tax revenues of EU countries, in particular green taxation. During the studied period, a slightly negative trend of decreasing their specific weight can be observed both in the structure of total tax revenues (from 6.0% in 2013 to 5.4% in 2021) and in the GDP share (from 2.5 in 2013 to 2 .2% in 2021). However, it should be noted that the studied indicators vary significantly depending on the country. Thus, in 2021, the most environmental taxes were collected in Poland (16.59 billion euros), Belgium (12.54 billion euros) and Sweden (10.24 billion euros), and the least - in Malta (0.29 billion euros), in Ireland (0.37 billion euros) and Cyprus (0.56 billion euros), which is argued by the economic activity volume. In general, the trends correspond to previous reporting periods.

Examining the green taxation structure (Table 2), it was established that the predominant revenues come from energy taxes (from 77.7% in 2013 to 78.4% in the reporting period) and transport taxes (18.69% in 2013 and 18.1% - in 2021). The smallest share falls on taxes for the natural environment pollution - only about 3.4-3.5%.

A special point in view of the current situation is that the total added value of green taxation in the EU-27 is constantly decreasing, in particular due to the lack of indexation of minimum tax rates and a significant amount of tax benefits (air and sea transportation), causing an uneven tax burden. From another point of view, the role of green taxation as a budget-forming mechanism is called into question, since the increase in tax rates, revision of the structure of tax benefits in the short-term perspective will ensure the increase in tax revenues, but in the long-term they will play a regulatory role, motivating business entities to increase investments in the environmental protection and resource-saving projects, thereby encouraging global technological transformations.

Such facts give rise to the next problematic situation - the ability of individual countries to compensate for the deficit of the state budget, given the high share of revenues from the transport fuel tax in the total amount of tax revenues (Lithuania (89%), the Czech Republic and Poland (73%) and Estonia (72%) [42].

We believe that the low level of revenues from the green taxation combined with the economic efficiency of these tools for solving environmental problems can play a greater role in solving environmental problems at the national and international levels.

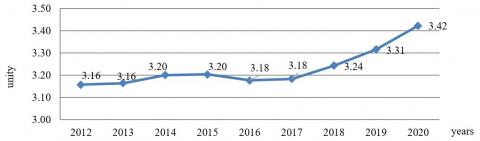

The analysis and assessment of the environmental policy and its impact on the economy of EU countries, which is carried out based on the Environmental Policy Stringency Index, is presented in Figure 1 [8].

Table 2. Specific weight of elements of the environmental taxation in the EU-27 for 2013-2021

|

Indicator |

2013 Year |

2014 Year |

2015 Year |

2016 Year |

2017 Year |

2018 Year |

2019 Year |

2020 Year |

2021 Year |

|

Energy taxes, % |

77.7 |

77.8 |

77.5 |

77.8 |

77.7 |

77.7 |

77.8 |

77.4 |

78.4 |

|

Transport taxes, % |

18.9 |

18.8 |

19.0 |

18.8 |

18.9 |

19.1 |

18.9 |

19.0 |

18.1 |

|

Taxes on Pollution/Resources, % |

3.4 |

3.4 |

3.5 |

3.4 |

3.4 |

3.2 |

3.3 |

3.6 |

3.5 |

The presented data in Figure 1 show that in EU countries during the period under study, the environmental policy of an average level of stringency is applied and is on average 3.42 in 2020 against 3.16 in 2012. According to the results of 2020, the highest value of the indicator was observed in France (4.89), and the lowest - in Slovakia and Spain (2.5). During previous years, similar trends were observed, which is argued by national strategies. Thus, the average indicator of the tax policy within the framework of the Environmental Policy Stringency Index of the studied countries makes it possible to assert available process of greening, including tax systems and application of a loyal version of it in practice. In general, the implemented environmental policy of EU countries tends to increase the impact on their economies, which is confirmed by scientific and theoretical approaches presented above.

Based on the methodology for evaluating the effectiveness of green taxation chosen for the analysis, a study of the green taxation effectiveness in the EU-12 was carried out, the results of which are presented in the Table 3.

Based on the received data on the evaluation of the green taxation effectiveness in Table 3, it can be concluded that the current mechanism of tax regulation of the environmental processes of the EU-12 is characterized by the unstable character, which changes during the studied time from an effective to a partially effective state. As a result, there is a need to soften the tax policy by adjusting the balance of tax benefits and subsidies relative to the tax burden level of taxpayers in the form of green taxation, which in the long run should reduce costs for the environmental protection (K1), optimization of the preferential taxation (K2), increasing indicators of the quality of life of the population (K3), increasing investment activity in the environmental protection (K4), as well as minimizing the costs of eliminating consequences of pollution and depletion of natural resources (K5). The final data demonstrate the effectiveness of the presented methodological approach to assessing the impact of green taxation and define the main directions for further regulation and correction of financial instruments of influence.

We believe that green taxation is an environmentally safe and socially inclusive way of economic growth, due to the effective use of natural resources and minimization of emissions of pollutants, as well as reducing the impact on the environment. Today, green taxation in the EU is not harmonized, it is differentiated in the competences of the member states, which determines the problematic environment of its regulation. Therefore, to regulate the green taxation effectiveness, it is necessary to solve a number of problems.

As for inconsistency of the outdated norms of the Energy Taxation Directive [8] with the legal framework and objectives of the EU climate and energy policy (weak link between minimum fuel tax rates and its energy content or CO2 emissions), the studies show that the countries with high and with highly differentiated (relative to CO2 emissions) tax rates have achieved the greatest success in reducing CO2 emissions.

Disturbance of the balance of the tax burden and taxation conditions for various types of transport in connection with the set of tax benefits for fuel used in international aviation and maritime transport, as well as their inconsistency with the EU's climate goals. Low rates and volumes of investment in clean technologies.

Plastic taxation (Spain and Italy, for example, plan to introduce a plastic tax of €0.45 per kilogram from 2023, although the EU levy is €0.80 per kilogram from 2021. On the other hand, the United Kingdom in April 2022 introduced a tax of £0.20 per kg).

Formation of the tax mechanism of the environmental regulation in EU countries does not require application of drastic measures to reform national tax systems, because having the tools of the environmental orientation, they need conceptualization from the position of the environmental factor and harmonization of the current tax legislation for a possible further assessment of effective functioning.

The global aging of the nation, search for alternatives and ways to increase tax payments, in particular through the transition system from labor taxes to the environmental taxation, is a strong argument for improving the green tax application. The need to modernize green taxation is reinforced by the fact that the volume of energy consumption is due to Russia's aggression against Ukraine, because EU countries import more than 40% of gas, 27% of oil, and 46% of coal imports from Russia.

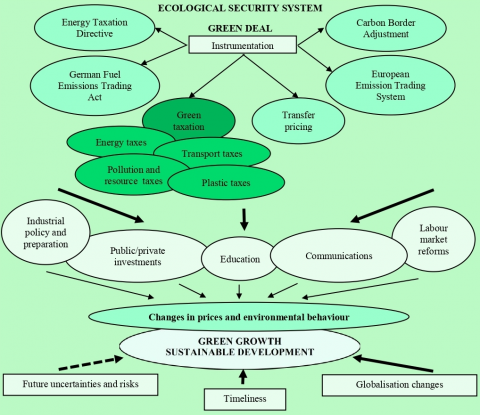

These arguments determine the need to modify and update the economy design, in particular, tax instruments of the environmental nature and their environmental architecture, which have been formed today (Figure 2).

The market mechanism cannot automatically overcome climate and natural challenges, that is why EU governments must take the initiative. Strengthening factors of influence on the achievement of the green taxation goals and within the framework of stable economic growth should be as follows: strict state control, public and private investment, advanced technological, innovative level and effective industrial policy, communication environment and green information technologies, labor market reform, as well as active awareness consumers and environmental education, taking into account the conditions of urgency, globalization changes, future uncertainties and risks.

Table 3. Dynamics of the research indicators on the green taxation effectiveness in the EU-12 for 2018-2020

|

Indicator |

2016 Year |

2017 Year |

2018 Year |

2019 Year |

2020 Year |

|

|

0.9780 |

1.0420 |

1.0393 |

1.0308 |

1.0111 |

|

|

0.9842 |

0.9780 |

1.0337 |

1.0220 |

1.1409 |

|

|

1.0077 |

1.0575 |

0.8690 |

1.0235 |

0.9738 |

|

|

1.4685 |

1.0502 |

0.3917 |

1.0159 |

0.9543 |

|

|

1.0525 |

1.0031 |

0.9970 |

1.0119 |

0.9632 |

|

Efficiency level |

Effective |

Partially effective |

Partially effective |

Partially effective |

Partially effective |

Efforts to use green taxation to combat climate change vary across countries. Comprehensive mapping and comparison of interventions and identification of good practice can help streamline efforts and improve policy learning. Therefore, we believe that the priority tasks of improving the green taxation should be:

1. Revision of the Energy Taxation Directive in accordance with the Green Deal (by vectors of the tax base, differentiation of tax rates and their indexation, as well as tax benefits).

2. Expansion of the scope of application and revision of certificates for certain imported goods with intensive CO2 emission (for aluminum, iron, fertilizers, cement already exist).

3. Search for effective incentives for investments in clean technologies through tax incentives.

4. Tax credits for research and development for small and medium-sized businesses (through the system of reducing taxation of wages and production costs).

5. Implementation of plastic taxation in all EU countries.

6. Stimulating the implementation of grant programs in taxation of green investments in leading sectors (agriculture, renewable or low-carbon energy sources, energy-efficient buildings, public pedestrian and bicycle paths, electric vehicle infrastructure).

7. IT transformations to deepen data exchange between tax authorities of EU countries to track supply chains, real value, careful study of the transfer pricing model along with revision of the conditions of application of indirect taxes and customs duties.

8. IT transformations to strengthen cooperation of inventors, investors and business sectors.

9. Incentives that reward the emissions reduction behavior with tax credits or even tax exemptions. Within transport taxation, the challenge is to develop an effective tax mechanism aimed at supporting the use of electric vehicles and other alternatives (as opposed to vehicles running on fossil fuels) by reducing the annual tax rates on such vehicles, sales tax or full exemption from taxation. The structure of these taxes can be expected to change over time, especially after the sales ban goes into effect.

10. Development of national road maps of EU countries regarding the use of tax revenues in the form of green tax for the environmental protection purposes and measures.

11. Ensuring long-term fiscal sustainability requires governments to continuously strategically forecast future revenues and liabilities, environmental factors and socio-economic trends to adapt financial planning accordingly.

Only in a complex, the specified components will be able to stimulate sustainable economic development, reduce intensity of pollution, control resource intensity and consumption of natural resources. Achieving the economic growth targets and Green Deal goals requires further research into the stated issues, identification of constantly emerging new factors of influence and development of climate change, technologies and means of influencing them.

After conducting research, it was established that the main idea of the environmental reforms should be to achieve a balance between the amount of the environmental tax revenues (under the influence of tax benefits, rates, expansion of the tax base, revision of the EU quota trading system) and the amount of consumption of natural resources, because the non-renewability of some of them in the future will reduce the tax base of green taxation.

A literal review of the researched issues established that concepts of green taxation differ depending on the ambition level they set before themselves as the driving force of socio-economic transformations. Along with this, they are systematized according to the following vectors: green taxation should stimulate economic growth through the system by reducing emissions, contrary to the idea that the environmental sustainability is a limitation for ever-growing GDP; low-carbon investments in the technology and infrastructure can be a source of job creation in the context of economic recovery; tax regulation of "green" investments will become not only a source of new jobs, but also a new engine of the socio-economic growth.

After analyzing the key economic indicators, it was found that green taxation is an important and effective tool in solving the environmental problems and raising the environmental safety level by influencing the environmentally harmful behavior and generating revenues for budgets of countries to finance the following measures related to climate change, renewable natural resources. The insignificant budgetary role of the environmental taxation does not reduce the value of this economic-regulatory mechanism, but strengthens its opportunities on the path of industrial development and investments in it, contributing to the ecological economy development.

The study of the Environmental Policy Stringency Index -in EU countries for 2012-2020 made it possible to establish the fact that the environmental policy is of a medium stringency level (an average of 3.42 percent of the limit value of 0-6). The applied study of the methodology for evaluating the green taxation effectiveness of EU countries revealed that the current mechanism of tax regulation of the environmental processes of the EU-12 is characterized by an unstable nature, which changes during the studied time from an effective to a partially effective state. The use of the specified methodical approach creates opportunities for constant monitoring of the green taxation system and ensures timely management decisions to achieve the planned goals.

The author's vision of the architecture of the green taxation environment is presented, which demonstrates the need for synergistic participation of legal (Energy Taxation Directive, German Fuel Emissions Trading Act, Carbon Border Adjustment, European Emission Trading System), economic (Transfer Pricing, Green Taxation, Industrial Policy and Preparation, Public/Private Investments) and other components, taking into account the conditions of urgency, globalization changes, future uncertainties and risks.

The author's vision of the green taxation improvement is proposed for its possible use as a tool of the behavioral influence on the achievement of the Green Deal goals and formation of the environmental security system of EU countries in particular.

[1] Costello, C.B. (2016). Economic security. In the American Woman, 2003-2004: Daughters of a Revolution: Young Women today. Palgrave Macmillan New York. pp. 291-308. https://doi.org/10.1007/978-1-137-11600-0_14

[2] Dergaliuk, B., Popelo, O., Tulchynska, S., Kharchenko, Y., Khanin, S., Tkachenko, T. (2021). Systemic approach to assessing sustainable development of the regions. Journal of Environmental Management and Tourism, 3(51): 742-753. https://doi.org/10.14505/jemt.v12.3(51).13

[3] Dubyna, M., Kholiavko, N., Zhavoronok, A., Safonov, Y., Krylov, D., Tochylina, Y. (2022). The ICT sector in economic development of the countries of Eastern Europe: A comparative analysis. WSEAS Transactions on Business and Economics, 19: 169-185. https://doi.org/10.37394/23207.2022.19.18

[4] Garafonova, O., Marhasova, V., Tulchynska, S., Popelo, O., Yaroshenko, I., Semykhulyna, I. (2022). Modeling the harmony of economic development of regions in the context of sustainable development. International Journal of Sustainable Development and Planning, 17(2): 441-448. https://doi.org/10.18280/ijsdp.170209

[5] Tymchenko, O., Sybirianska, Yu., Abramova, A. (2019). The approach to tax debtors’ segmentation. Ikonomicheski Izsledvania, 28(5): 103-119.

[6] Kholiavko, N., Popova, L., Marych, M., Hanzhurenko, I., Koliadenko, S., Nitsenko, V. (2020). Comprehensive methodological approach to estimating the research component influence on the information economy development. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, 4: 192-199. https://doi.org/10.33271/nvngu/2020-4/192

[7] Lagodiienko, N., Popelo, O., Tulchynska, S., Radin, A.M., Moskalenko, A. (2021). Methodical approach to forecasting the intensification of innovative development of regions using the Mathcad program. International Journal of Circuits, Systems and Signal Processing, 15: 1591-1601. https://doi.org/10.46300/9106.2021.15.171

[8] OECD. (2024). Environmental policy: Environmental policy stringency index. https://doi.org/10.1787/env-data-en.

[9] Gramkow, C., Anger-Kraavi, A. (2018). Could fiscal policies induce green innovation in developing countries? The case of Brazilian manufacturing sectors. Climate Policy, 32(58): 246-257. https://doi.org/10.1080/14693062.2016.1277683

[10] Gramkow, C. (2020). Green fiscal policies as an armory of instruments to recover growth sustainably. Studies and Perspectives Series-Brasília, 1-56. https://repositorio.cepal.org/bitstream/handle/11362/45418/1/S2000005_en.pdf.

[11] Alexander, K. (2010). International regulatory reform and financial taxes. Journal of international Economic Law, 13(3): 893-910. https://doi.org/10.1093/jiel/jgq036

[12] Danylyshyn, B., Dubyna, M., Zabashtanskyi, M., Ostrovska, N., Blishchuk, K., Kozak, I. (2021). Innovative instruments of monetary and fiscal policy. Universal Journal of Accounting and Finance, 9(6): 1213-1221. https://doi.org/10.13189/ujaf.2021.090601

[13] Kotlán, I., Němec, D., Kotlánová, E., Skalka, P., Macek, R., Machová, Z. (2021). European green deal: Environmental taxation and its sustainability in conditions of high levels of corruption. Sustainability, 13(4): 1981. https://doi.org/10.3390/su13041981

[14] Tsai, W.H., Chu, P.Y., Lee, H.L. (2019). Green activity-based costing production planning and scenario analysis for the aluminum-alloy wheel industry under Industry 4.0. Sustainability, 11(3): 756. https://doi.org/10.3390/su11030756

[15] Borrego, A.C., Abreu, R., Carreira, F.A., Caetano, F., Vasconcelos, A.L. (2023). Environmental taxation on the agri-food sector and the farm to fork strategy: The Portuguese case. Sustainability, 15(16): 12124. https://doi.org/10.3390/su151612124

[16] Kovalska, L., Popelo, O., Tulchynska, S., Garafonova, O., Khanin, S. (2021). Methodical approach to assessing the innovative development efficiency of the regional economic systems in the conditions of the creative economy development. WSEAS Transactions on Environment and Development, 17: 685-695. https://doi.org/10.37394/232015.2021.17.66

[17] Popelo, O., Shaposhnykov, K., Popelo, O., Hrubliak, O., Malysh, V., Lysenko, Z. (2023). The influence of digitalization on the innovative strategy of the industrial enterprises development in the context of ensuring economic security. International Journal of Safety and Security Engineering, 13(1): 39-49. https://doi.org/10.18280/ijsse.130105

[18] Qin, J., Yang, K., Ding, X. (2023). Can the reform of the transfer tax system affect corporate green innovation—Evidence from China’s “BT to VAT” reform. Sustainability, 15(4): 2986. https://doi.org/10.3390/su15042986

[19] Rekunenko, I., Zhuravka, F., Nebaba, N., Levkovych, O., Chorna, S. (2022). Assessment and forecasting of the Ukraine’s financial security: Choice of alternatives. Problems and Perspectives in Management, 20(2): 117-134. https://doi.org/10.21511/ppm.20(2).2022.11

[20] Shmygol, N., Galtsova, O., Shaposhnykov, K., Bazarbayeva, S. (2021). The environmental management policy: Assessment of ecological and energy indicators and effective regional management (On the example of Ukraine). Polityka Energetyczna, 24(4): 43-60. https://doi.org/10.33223/epj/143836

[21] Environmental Taxes. (2022). What tax departments can expect from the European Green Deal. https://hub.kpmg.de/environmental-taxes-english?utm_campaign=TAX%20-%20Studie%20-%20Environmental%20Taxes&utm_source=aem.

[22] Bank of England. (2021). Key elements of the 2021 biennial exploratory scenario: Financial risks from climate change. https://www.bankofengland.co.uk/stress-testing/2021/key-elements-2021-biennial-exploratory-scenario-financial-risks-climate-change.

[23] Shaposhnykov, K., Kochubei, O., Grygor, O., Protsenko, N., Vyshnevska, O., Dzyubina, A. (2021). Organizational and economic mechanism of development and promotion of IT products in Ukraine. Estudios de EconomÍa Aplicada, 39(6): 3-14. https://doi.org/10.25115/eea.v39i6.5264

[24] Lagodiienko, V., Popelo, O., Zybareva, O., Samiilenko, H., Mykytyuk, Y., Alsawwafi, F.M.A.S. (2022). Peculiarities of the management of the foreign economic activity of enterprises in current conditions of sustainability. International Journal of Sustainable Development and Planning, 17(4): 1215-1223. https://doi.org/10.18280/ijsdp.170420

[25] Lagovska, O., Ilin, V., Kotsupatriy, M., Ishchenko, M., Verbivska, L. (2020). Priority directions of the tax policy change in the information sphere. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, 3: 183-190. https://doi.org/10.33271/nvngu/2020-3/183

[26] Liutikov, P., Abramova, A., Shaposhnykov, K., Zhavoronok, A., Skvirskyi, I., Lukashev, O. (2021). Ecosystem of VAT Administration in e-commerce: Case of the eastern Europe countries. Estudios de Economía Aplicada, 39(5): 3-15. http://doi.org/10.25115/eea.v39i5.4909

[27] Lei, Z., Huang, L., Cai, Y. (2022). Can environmental tax bring strong porter effect? Evidence from Chinese listed companies. Environmental Science and Pollution Research, 29(21): 32246-32260. https://doi.org/10.21203/rs.3.rs-612715/v1

[28] Matti, S., Nässén, J., Larsson, J. (2022). Are fee-and-dividend schemes the savior of environmental taxation? Analyses of how different revenue use alternatives affect public support for the Sweden's air passenger tax. Environmental Science & Policy, 132: 181-189. https://doi.org/10.1016/j.envsci.2022.02.024

[29] Zhao, A., Wang, J., Sun, Z., Guan, H. (2022). Environmental taxes, quality of technology innovation and company’s performance in China—A test of effects based on the porter hypothesis. Economic Analysis and Policy, 74: 309-325. https://doi.org/10.1016/j.eap.2022.02.009

[30] Cordova-Buiza, F., Paucar-Caceres, A., Quispe-Prieto, S.C., de León-Panduro, C.V.P., Burrowes-Cromwell, T., Valle-Paucar, J.E. (2022). Strengthening collaborative food waste prevention in Peru: Towards responsible consumption and production. Sustainability, 14(3): 1050. https://doi.org/10.3390/su14031050

[31] Marhasova, V., Garafonova, O., Popelo, O., Tulchynska, S., Pohrebniak, A., Tkachenko, T. (2022). Environmentalization of Production as a direction of ensuring sustainability of production activities of enterprises and increasing their economic security. International Journal of Safety and Security Engineering, 12(2): 159-166. https://doi.org/10.18280/ijsse.120203

[32] Nusinova, O., Tulchynska, S., Popelo, O., Marhasova, V., Zhygalkevych, Z. (2021). Monitoring of the ecological condition of the regional economic systems in the context of sustainable development. Journal of Environmental Management and Tourism, 12(5): 1220-1228. https://doi.org/10.14505//jemt.v12.5(53).06

[33] Pîrvu, D., Duţu, A., Mogoiu, C.M. (2021). Clustering tax administrations in the European Union member states. Transylvanian Review of Administrative Sciences, 63: 110-127. http://doi.org/10.24193/tras.63E.6

[34] Pohrebniak, A., Borysenko, O., Tulchynska, S., Popelo, O., Redko, K., Koba, V. (2023). Innovative and investment activities of enterprises within eco-industrial parks in the circular economy context. International Journal of Sustainable Development and Planning, 18(1): 79-89. https://doi.org/10.18280/ijsdp.180108

[35] Liu, C.G., Cai, W., Zhang, C.X., Ma, M., Rao, W., Li, W. (2018). Developing the ecological compensation criterion of industrial solid waste based on emergency for sustainable development. Energy, 157: 940-948. https://doi.org/10.1016/j.energy.2018.05.207

[36] Piciu, G.C., Tric, C.L. (2012). Assessing the impact and effectiveness of the environmental taxes. Procedia Economics and Finance, 3: 728-733. https://doi.org/10.1016/S2212-5671(12)00221-3

[37] Tamura, H., Nakanishi, R., Hatono, I., Umano, M. (1996). Is the environmental tax effective for the total emission control of carbon dioxide? Systems analysis of the environmental – economic model. IFAC Proceedings Volumes, 29(1): 5435-5440. https://doi.org/10.1016/S1474-6670(17)58546-8

[38] Wang, B., Liu, L., Huang, G., Li, W., Xie, Y. (2018). Effects of the carbon and environmental tax on power mix planning – A case study of Hebei province, China. Energy, 143: 645-657. https://doi.org/10.1016/j.energy.2017.11.025

[39] Piciu, G.C., Tric, C.L. (2012). Trends in the evolution of the environmental taxes. Procedia Economics and Finance, 3: 716-721. https://doi.org/10.1016/S2212-5671(12)00219-5

[40] Xin, B. (2019). Impact of the environmental tax on green development: A nonlinear dynamical system analysis. PLoS One, 14(9): e0221264. https://doi.org/10.1371/journal.pone.0221264

[41] Congjuan, L., Abulimiti, M., Jinglong, F., Haifeng, W. (2022). Ecologic service, economic benefits, and sustainability of the man-made ecosystem in the Taklamakan desert. Frontiers in Environmental Science, 10: 813-932. https://doi.org/10.3389/fenvs.2022.813932

[42] Kaldor, N. (1985). Economics without Equilibrium. New York, Routledge. https://doi.org/10.4324/9781003069713