Uliana Nikonenko*![]() | Diana Maksymenko

| Diana Maksymenko![]() | Vasyl Holovachko

| Vasyl Holovachko![]() | Yaroslav Golubka

| Yaroslav Golubka![]() | Olga Guk

| Olga Guk![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The primary objective of this article is to enhance the efficiency of the time management model within the accounting and auditing system while focusing on sustainable development planning. The subject of study is the sustainable development planning system of a single enterprise. The scientific goal entails formulating a model for the information functional base of time management within the accounting and auditing system, and directing efforts towards planning the sustainable development of the enterprise. The research methodology employs a contemporary method for forming structural models of information security within modern systems for sustainable development planning. This method incorporates the use of a graphical language to model functional blocks. The outcome of this research presents two pivotal structural models of the information base for time management in the accounting and auditing system and the planning for the sustainable development of the enterprise. These models represent functional blocks in the formation of an information base within the context of sustainable development. The innovativeness of the research results is manifested through the methodical approach to modeling the increase in the efficiency of time management in the accounting and auditing system, and planning the sustainable development of an enterprise. This approach, due to its novel application within the realm of time management, is deemed innovative in the article. The study, however, is limited by considering only the specifics of the sustainable development planning system of a single enterprise. Prospects for further research include broadening the modeling of time management in the accounting and auditing system, and planning the sustainable development of the enterprise.

sustainable development, sustainable development planning model, accounting and auditing time management, time management, model, system

1.1 Problem overview

To ensure the effectiveness and efficiency of time management within the system of sustainable development planning for an enterprise, it's advisable to prioritize tasks clearly, minimize the loss of working time, perfect the delegation of authority, and monitor processes related to managing working time. It's only through the well-coordinated effort of all enterprise components, a positive socio-psychological climate, successful delegation of authority, a well-organized accounting and auditing system, and a robust control system that the rational use of working time can be achieved. Consequently, this leads to effective time management within the enterprise's sustainable development planning system.

In today's highly automated and production-maximized global conditions, time management is integral to any company's success. Time management refers to the development of time management strategies and boosting their effectiveness within the company's sustainable development planning system. Effective management of the enterprise's available resources used in the process of operation forms a crucial part of this. Time, being one of the most significant yet exhaustible and non-renewable resources, is the principal subject of numerous studies. The relevance of time management across all operational levels stems from its promising potential within the system planning for sustainable enterprise development, thereby contributing to the socio-economic process in any field of activity.

Time management encompasses a set of methods for planning and organizing the work of both the entire enterprise and its employees. These methods are utilized by management to enhance working time efficiency, manage the growing volume of tasks by setting priorities, and break down large tasks and projects into separate components for delegation. The time management system aims at developing and implementing a diverse set of measures to improve time management, providing a comprehensive solution to optimizing organizational processes within the enterprise's sustainable development planning system.

1.2 Structure and formulation of the problem

The problem lies in the unimproved information provision of the accounting and audit system for time management within the context of sustainable development. The main objective of the article is to enhance the efficiency of the time management model in the accounting and auditing system while focusing on sustainable development planning. The subject of study is the sustainable development planning system of a single enterprise. The structure of the article implies addressing and developing the issues raised, reviewing the literature, detailing the methods, presenting the primary study results, discussing them, and drawing conclusions. The goals of the article include modeling the information base within the context of accounting and auditing of the time management system for sustainable development.

Time is the most valuable human resource [1, 2]. It is absolutely limited and irreplaceable, it cannot be substituted or compensated for, however, it can be effectively "converted" into certain values of life. A common problem that many managers of domestic enterprises face is the lack of time. While one can be purposeful, organized, efficient, and plan their working time rationally, they can still suffer from the poor organization of time by their subordinates and colleagues. The personal effectiveness of each employee is directly dependent on how time management processes are structured within the unit and the enterprise. In general, the appropriate use of time is key to successfully fulfilling professional duties and achieving goals.

The scientific and practical literature repeatedly emphasizes that the initial conditions for successful management are the proper organization and rational utilization of time [3, 4]. Planning the personal work of a manager involves making the right choices regarding his involvement in implementing strategic, tactical, and operational plans for production activities, establishing relationships with other organizations, making decisions, and supervising their implementation. Moreover, personal work planning involves self-improvement and establishing a rational balance between activity and rest for the manager. A manager who cannot manage time effectively is unable to see beyond the multitude of daily tasks.

As accurately described in the literature that the global shift in the paradigm of economic management towards sustainable development requires business entities to transform the management system and its constituent functions, especially accounting [5, 6]. The most valuable asset in the information society is qualified personnel who are interested in maximizing the profits of the enterprise. Improving the accounting and auditing system, as the information basis for the full reproduction of labor resources, leads to an increase in sustainable development.

The literature notes that accounting and auditing, as the foundation for sustainable development planning, need to be reformed for several reasons [7, 8]: firstly, it focuses on stored assets (only property is the object - resources controlled by the enterprise), and secondly, it focuses on the past (as a result of past events). At the same time, when forming personnel costs (a decrease in economic benefits in the form of asset disposal or an increase in liabilities leading to a decrease in equity (with the exception of a decrease in capital due to its withdrawal or distribution by owners)), the characteristic of an asset that "is expected to lead to obtaining economic benefits in the future" represents, in a methodological aspect, the economic essence of a special resource of an enterprise - personnel in the system of sustainable development planning.

In general, the literature shows that business entities, regardless of their type of activity, forms of ownership, or subordination, keep accounting records of property and business operations in accordance with applicable law [9, 10]. The production and economic activities of companies are provided by a totality of resources: tangible, intangible, labor, and monetary. However, the main means of production are fixed assets. These assets determine the current level of production, as the rational use of fixed assets is one of the main factors in increasing production efficiency, leading to an increase in output without additional investments. Fixed assets can influence the final results of economic activity: output, its cost, profit, profitability, and financial stability. Therefore, being aware of the availability of fixed assets, providing organizational and analytical support, and constantly monitoring their effective use is of great importance in organizing the entire production process in the sustainable development planning system.

However, the high level of informatization and sustainable innovative development have created new challenges that can serve as both additional opportunities and obstacles to the effective functioning and sustainable development of an enterprise. This requires several different approaches to the organization of sustainable development planning, including the definition and classification of organizational structures and methods and models of their formation. The scientific task is to form a model of the information functional base of time management in the accounting and auditing system and work on planning the sustainable development of the enterprise.

Gaps in the literature mostly relate to the lack of a new, effective methodical approach to ensuring sustainable development through the improvement of accounting and auditing of the time management system.

Today, it's evident that the process of business modeling has become an integral component in implementing any project related to the modernization of sustainable development planning systems. The results of these simulations are often presented using techniques such as IDEF0, DFD, and IDEF3.

Successful process modeling necessitates a close collaboration between information technology professionals and sustainability planning experts. However, this collaboration is not feasible without a common language that both parties can understand—a graphical modeling language. In this context, the DFD methodology can serve as a common language.

A Data Flow Diagram (DFD) is deployed to illustrate the information involved in sustainability planning. It can supplement the IDEF0 model to offer a more comprehensive visual representation of the ongoing operations within a sustainability planning system. The DFD outlines a set of sustainability planning processes, providing an interface to external entities beyond the modeled system and data storage. BPwin utilizes Gane-Sarson notation to construct these data flow diagrams.

In a DFD, unlike in IDEF0, each side of the work rectangle doesn't have a distinct purpose. The arrows, representing information flows, can enter and exit from any face of the rectangle, and display data, information, or documents in both printed and electronic forms. Double-headed arrows are employed to illustrate command-response type dialogs between jobs, external entities, and data storage.

The purpose of a model is dictated by the reasons for its creation, which in turn determines its usage. In our case, the objective is to establish an information base to enhance time management efficiency within the accounting and auditing system, as a part of an enterprise's sustainable development planning.

The decomposition of the DFD model can be visualized as a "puzzle" of interconnected elements, all striving to improve time management efficiency within the accounting and auditing system for sustainable enterprise development planning.

Every enterprise must consistently elevate its level of maturity in sustainable development. If an enterprise has never conducted a maturity assessment, the initial evaluation can be done through brainstorming, without the need for external consultation. Subsequent assessments to elevate maturity levels can be organized on a planned basis, opting for an annual cycle of enhancement and evaluation. It's crucial to note that any enterprise assessment should commence with a business process analysis, investigating its alignment with the overall sustainable business development strategy. Therefore, a common graphical language to perceive the current and final results of such work is of significant importance for making balanced management decisions.

For many years, analysts, designers, and task setters have utilized modeling methodologies like DFD, IDEF0, and IDEF3. The graphical models produced by these methodologies facilitate visibility, transparency, and thus, a clear understanding of the problem by both the client and the executor in sustainable development planning.

Let's take the example of "Zara", a company with extensive operations in Europe's retail sector, to illustrate a sustainable development planning system. Prior to applying the chosen modeling methodology, it's essential to conduct a thorough SWOT analysis to identify potential issues in the sustainability planning system.

The DFD method was chosen for its ability to represent the simulation graphically and innovatively, compared to IDEF methods. DFD encourages a functional approach to sustainable development and will form the basis of our information model, built on the results of the SWOT analysis.

The choice of Zara was based on the company's willingness to provide data for analysis. Initially, a SWOT analysis is conducted, and then a model is built using DFD based on the analysis findings.

The objectives of this modeling exercise are to create an information foundation that enhances time management within the framework of sustainable development, with a specific focus on accounting, auditing, and the time management system.

Before starting the simulation, a SWOT analysis should be carried out in order to identify the weaknesses of the enterprise in the framework of sustainable development (Table 1).

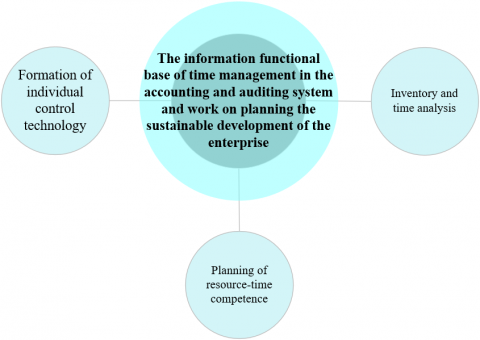

The enterprise is currently facing several issues related to the information support system, accounting and auditing, and time management. To address these problems, we have established three key processes that will contribute to achieving our modeling goal, which is to create an "Information Functional Base for Time Management in the Accounting and Auditing System and Work on Planning the Sustainable Development of the Enterprise" (Figure 1).

Table 1. SWOT-analysis in the framework of sustainable development (Developed by the author)

|

S |

W |

O |

T |

|

Effective use of models and mechanisms in activities |

Inefficient information support |

Planning opportunities through new technologies |

The threat of a worsening post-pandemic environment |

|

Creativity and creativity of staff |

Time Management Issues |

Opportunities to enter new markets |

The threat of reducing the digitalization of society |

|

High yield |

Poor performance of the accounting and auditing system |

Business expansion opportunities as a result of sustainable development |

Threat of reference to inflation |

Figure 1. Modeling processes according to a defined goal (Developed by the author)

As a result of our study, we have developed a structural model of the information base to ensure sustainable development through enhanced time management efficiency (Figure 2).

The first process is the "Formation of Individual Control Technology". This process involves individual time management technology that takes into account several mechanisms. These include the biological clock, which determines when maximum activity occurs during the day; intellectual engineering, which involves the use of knowledge about human potential and the dominant hemisphere of the brain; psychological hours, where a psychological time perspective is distinguished; and a style of human behavior that reflects the individual's moral and ethical standards and guides their behavior in different life situations within the context of sustainable development.

The second process is "Planning of Resource-Time Competence". Resource-time competence refers to an adequate perception of time, the ability to plan time effectively, the capacity to rationally redistribute time priorities and limits of interpersonal communication, and the observance of time management principles, including the delegation of authority in social communications. In communication, resource-time competence determines the adequacy of the subjective assessment of the time and space of interpersonal interaction, as well as the ability for optimal interaction, taking into account the time limits of communication, and empathy in expanding or removing the temporal boundaries of communicative control within the context of sustainable development.

The third process is "Inventory and Time Analysis". This process involves the comprehensive examination and evaluation of existing resources and their allocation over time, allowing for more effective planning and utilization of resources to ensure sustainable development.

Figure 2. Structural model of the information base for ensuring sustainable development by improving the efficiency of time management (Developed by the author)

The third process is "Inventory and Time Analysis". This process involves a thorough inventory and analysis of time, which aids in identifying time losses, strengths and weaknesses of work styles, areas of time spending, the amount of time required to complete tasks, and factors that either stimulate or limit productivity. Working time strengths need to be identified and utilized, while weaknesses require cause identification and the development of measures to eliminate them.

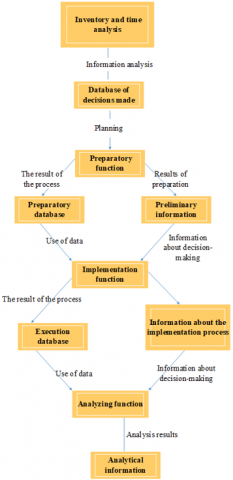

This "Inventory and Time Analysis" process is complex and needs to be broken down into additional functional components, each with its own modeling (Figure 3). Hence, let's consider the main sub-processes for implementation:

The first sub-process is the "Preparatory Function". This involves determining the types of time costs of the company's operation, clearly formulating them into logically independent categories for observation and recording. Additional categories (parameters) for quality assessment of time costs are defined. Planning the time inventory process (total duration, frequency, resources for conducting, etc.) is crucial, as is defining a coding system and quantitative presentation of inventory results. Preparing relevant forms is also part of this sub-process.

The second sub-process is the "Implementation Function". This involves measuring the time spent during a selected period, regularly filling in relevant forms. Preliminary grouping of obtained data and their preparation for further analysis is required. This includes assessment of time costs by qualitative parameters and calculation of necessary quantitative indicators to ensure sustainable development.

The third sub-process is the "Analyzing Function". This involves the analysis of time costs depending on the scale of tasks set for inventorying work costs (by type, operation, task), costs for non-work activities, and costs for temporary obstacles. Also considered are the quality of time spent on work, interference, and extra-work activity. The analysis result is formed based on the general purpose of the study (description of time costs; patterns of time spending that determine effective or inefficient use of time). Development of methods to combat time loss and recommendations for improving time use efficiency to ensure sustainable development are also part of this sub-process.

Figure 3. Functional decomposition of inventory and time analysis-Provisioning model (Developed by the author)

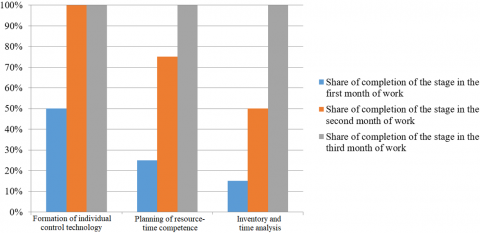

Figure 4. Periodization of sustainable development (Developed by the author)

For the chosen enterprise, sustainable development is achieved in three months of implementing these proposed processes. This is the duration it took the management to complete each stage of the modeling (Figure 4).

Implementing time management technology at the "Zara" enterprise contributes to resolving many issues in the field of time management and personnel management, followed by the development of recommendations for their solution. This necessitates structural modeling of the information basis of the time management system. The conducted research enabled the building of the information base of the time management system at the enterprise, defining its main tasks, principles, influencing factors, functions, methods, and elements.

Discussing the results of the study, it should be noted that a comparative characteristic with similar ones should be carried out as part of the discussion process.

Today, many scientists [11, 12] note that time management is a somewhat abstract category. They justify their opinion by the fact that the basis of any management process is influence, since it is not possible to influence time, and therefore it cannot be controlled. The only thing that is subject to each person is to learn how to build his life, taking into account his two main features: limitedness and irrecoverability.

Other scientists [13-15] have come to the conclusion that well-organized time management also gives employees the realization that the inefficient use of working time is not only a loss of the company's management, but also their own, which can lead to a significant reduction in performance and, as a result, to reduction of wages. The development of any enterprise directly depends on how its employees plan and organize their activities, taking into account time constraints. The use of the principles and technologies of time management in practice helps to increase the efficiency of the enterprise, reduces the loss of time and ensures the achievement of the desired results.

As the scientists note [16-18] in their study results, social and environmental accounting and auditing is essential for sustainable development. Thus, it should be noted that the concepts of social accounting and environmental accounting have not acquired logical completeness in Ukraine in the form of complex knowledge systems. Accordingly, the symbiosis of these types of accounting in such a complex as sustainable development accounting has been studied. Despite this, after studying scientific and regulatory sources, we have the opportunity to form a definition of a new type of accounting: “accounting for sustainable development”, which means a system of accounting and analytical support for identifying, measuring, registering, accumulating, generalizing, storing information about environmental - social status and activities that will provide users with information and allow establishing a balance between meeting social needs, protecting the interests of future generations, including their need for a safe and healthy environment and the financial and economic development of the enterprise.

In general, scientists [19, 20] in their results note that a well-built and effectively debugged time management system has a positive impact on the activities of the enterprise and allows you to gain competitive advantages in the market. The consistent application of time management technologies in the practice of domestic enterprises can increase labor productivity at the enterprise and, consequently, increase the pace of economic development.

Discussing our results of the study in the article, we note that it has a number of differences. The innovativeness of the obtained research results is revealed through the prism of a methodical approach to modeling the increase in the efficiency of time management in the accounting and auditing system and work on planning the sustainable development of an enterprise.

Discussing the stages of our study, we can draw the following diagram (Figure 5).

The similarities in our study appear with the agreement of the idea of the connection between time management and ensuring the sustainable development of the enterprise. The difference lies in the approach. The approach presented in the article is innovative due to its new use within time management.

Figure 5. Diagram of the stages of obtaining research results

The restrictions concerned the fact that we took into account the specifics of Zara and its type of activity. Discussing the practical implications of the results obtained, it should be noted that in situations of decision-making on time and accounting with an audit of an enterprise and its business processes. The advantages of our model are its information content and accessibility.

To sum up, the ability to manage your time largely determines your future as a leader. It largely determines what awaits you - success or failure in sustainable development planning. Time is an irreplaceable and non-renewable resource. It is your most valuable sustainability planning asset. It cannot be accumulated and its losses cannot be recovered. Everything you do takes time. The better you use it, the more effective your sustainability planning will be. Time management is equally important for maintaining health and increasing personal efficiency in sustainability planning. How well you manage your time and your life determines what your inner state will be - for example, peace, harmony and well-being. Feeling like you don't own your time is one of the biggest triggers for stress, anxiety, and depression. The more successfully you organize and control the main events of the enterprise, the better you can ensure sustainable development.

As a result, two key structural models of the information base of time management in the accounting and auditing system and work on planning the sustainable development of the enterprise were presented.

The study has a limitation by taking into account the specifics of the sustainable development planning system of only one enterprise. Prospects for further research involve expanding the modeling of time management in the accounting and auditing system and work on planning the sustainable development of the enterprise.

[1] Sylkin, O., Shtangret, A., Ogirko, O., Melnikov, A. (2018). Assessing the financial security of the engineering enterprises as preconditions of application of anti-crisis management: practical aspect. Business and Economic Horizons, 14(4): 926-940. https://doi.org/10.15208/beh.2018.63

[2] Hryhoruk, P., Khrushch, N., Grygoruk, S. (2019). Model for assessment of the financial security level of the enterprise based of the desirability scale. In SHS Web Conference, 65. https://doi.org/10.1051/shsconf/20196503005

[3] Bondaruk, T., Medynska, T., Nikonenko, U., Melnychuk, I., Loboda, N. (2023). Fiscal policy as a guarantee of sustainable development under military conditions. International Journal of Sustainable Development and Planning, 18(4): 1097-1102. https://doi.org/10.18280/ijsdp.180412

[4] Nikonenko, U., Shtets, T., Kalinin, A., Dorosh, I., Sokolik, L. (2022). Assessing the policy of attracting investments in the main sectors of the economy in the context of introducing aspects of industry 4.0. International Journal of Sustainable Development and Planning, 17(2): 497-505. https://doi.org/10.18280/ijsdp.170214

[5] Sylkin, O., Kryshtanovych, M., Zachepa, A., Bilous, S., Krasko, A. (2019). Modeling the process of applying anti-crisis management in the system of ensuring financial security of the enterprise. Business: Theory and Practice, 20: 446-455. https://doi.org/10.3846/btp.2019.41

[6] Saleh, A.J., Alazzam, F.A.F., K.K.A.R., Zavalna, Z. (2020). Legal aspects of the management of cryptocurrency assets in the national security system. Journal of Security and Sustainability Issues, 10(1): 235-247. https://doi.org/10.9770/jssi.2020.10.1(17)

[7] Alazzam, F.A.F., Salih, A.J., Amoush, M.A.M., Khasawneh, F.S.A. (2023). The nature of electronic contracts using blockchain technology-Currency bitcoin as an example. Revista De Gestão Social E Ambiental, 17(5): e03330. https://doi.org/10.24857/rgsa.v17n5-014

[8] Al Azzam, F. (2019). The adequacy of the international cooperation means for combating cybercrime and ways to modernize it. JANUS.NET e-Journal of International Relations, 10(1). https://doi.org/10.26619/1647-7251.10.1.5

[9] Chapman, E., Rogers, L., Kay, A. (2021). Toward just and sustainable cities: Identifying key areas for urban, peri-urban and rural sustainability collaborative initiatives. International Journal of Environmental Impacts, 4(1): 36-48. https://doi.org/10.2495/EI-V4-N1-36-48

[10] Liu, J.L., Li, K. (2019). An information system of clinical pathway management based on the integration between knowledge management and learning organization. Ingénierie des Systèmes d’Information, 24(5): 473-480. https://doi.org/10.18280/isi.240503

[11] Kuznyetsova A., Sydorchenko, T., Zadvorna, O., Nikonenko, U., Khalina, O. (2021). Assessment of aspects of the COVID-19 crisis in the context of ensuring economic security. International Journal of Safety and Security Engineering, 11(6): 615-622. https://doi.org/10.18280/ijsse.110601

[12] Popelo, O., Shaposhnykov, K., Popelo, O., Hrubliak, O., Malysh, V., Lysenko, Z. (2023). The influence of digitalization on the innovative strategy of the industrial enterprises development in the context of ensuring economic security. International Journal of Safety and Security Engineering, 13(1): 39-49. https://doi.org/10.18280/ijsse.130105

[13] Yashiro, H., Hayashin, T. (2021). Analysis on impact of compact city progress on seismic risk fluctuation. International Journal of Environmental Impacts, 4(1): 25-35. https://doi.org/10.2495/EI-V4-N1-25-35

[14] Yemelyanov, V., Nikonenko, U., Sytnyk, Y., Okhrimenko, I., Shulga, A. (2022). A model for countering the information and technical threats of intellectual capital management of innovation-oriented systems in the engineering sector. Ingénierie des Systèmes d’Information, 27(5): 799-806. https://doi.org/10.18280/isi.270513

[15] Danko, L., Bednář, P., Matošková, J. (2017). Managers’ activities within cultural and creative clusters: an essential element for cluster development in the Visegrád countries. Creativity Studies, 10(1): 26-42. https://doi.org/10.3846/23450479.2016.1266049

[16] Bazyliuk, V., Shtangret, A., Sylkin, O., Bezpalko, I. (2019). Comparison of institutional dynamics of regional development publishing and printing activities in Ukraine: methodological and practical aspects. Business: Theory and Practice, 20: 116-122. https://doi.org/10.3846/btp.2019.11

[17] Dudin, M., Burkaltseva, D., Reznikova, O., Betskov, A., Kilyaskhanov, H., Guk, O., Zotova, S. (2018). The impact of conflict on economic security of the enterprise. International Journal of Engineering and Technology (UAE), 7: 283-290. https://doi.org/10.14419/ijet.v7i3.14.16907

[18] Alazzam, F.A.F., Alshunnaq, M. F. N. (2023). Formation of creative thinking of a lawyer in modern conditions of development including the influence of COVID-19 pandemic. Creativity Studies, 16(1): 315-327. https://doi.org/10.3846/cs.2023.16117

[19] Tulchynska, S., Popelo, O., Pohrebniak, A., Borysenko, O., Redko, K., Koba, V. (2023). Innovative and investment activities of enterprises within eco-industrial parks in the circular economy context. International Journal of Sustainable Development and Planning, 18(1): 79-89. https://doi.org/10.18280/ijsdp.180108

[20] Nikonenko, U., Hanushchyn, S., Boikivska, G., Andriichuk, Y., Kokhan, V. (2020). Influence of world commodity prices on the dynamics of income of exporting countries of natural resources under globalization. Business: Theory and Practice, 21(1): 440-451. https://doi.org/10.3846/btp.2020.12202