Zakarie Abdi Warsame*![]() | Abas Mohamed Hassan

| Abas Mohamed Hassan![]() | Ali Yusuf Hassan

| Ali Yusuf Hassan![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study delves into the effective management of inflation by analyzing its determinants, highlighting the importance of low inflation as an indicator of macroeconomic stability. The research explores the interplay between Broad Money Supply, Gross Domestic Product (GDP), and Exchange rate, within the framework of Somalia's inflation, using time series data from 1970 to 2010. An Autoregressive Distributed Lag (ARDL) model is employed to scrutinize short- and long-term elasticities. The findings reveal a strong, statistically significant, positive correlation between money supply and inflation over the long term; specifically, a modest 1% increase in money supply leads to a significant 39.35% rise in the inflation rate. Additionally, in the long run, a sizeable negative relationship between GDP and inflation is uncovered, suggesting that a 1% rise in GDP corresponds to a remarkable 261.17% decrease in the inflation rate. Granger causality tests expose a unidirectional influence—from exchange rate to inflation, money supply to exchange rate, and GDP to exchange rate. Hence, this study emphasizes the need for the Somali government to implement fiscally prudent measures that foster real GDP growth.

ARDL, GDP, inflation, money supply, Somalia

Inflation, recognized as a crucial monetary phenomenon, has attracted significant global attention due to its persistent nature. Conceptually, inflation is characterized by a continuous and sizable increase in price levels, which results in a significant diminution of purchasing power [1]. This phenomenon triggers consequential economic behaviors, prompting individuals to allocate substantial financial resources towards consumption activities. This consumption orientation places downward pressure on savings and investments, amplifying unemployment rates and hindering overall economic growth.

In addition to its national implications, inflation casts a wide influence over the international economic landscape. The phenomenon introduces a unique disruption to a country's trade dynamics, principally by raising the valuation of domestic commodities above the standard benchmarks of regional and global market prices. As a result, a country's competitive position in international trade experiences a setback [2]. This heightened pricing structure cultivates an environment where the ability to compete effectively in the global market is jeopardized.

In essence, the significance of inflation as a monetary phenomenon is underscored by its pervasive impact, prompting careful consideration among global economists. The relentless rise in prices, coupled with subsequent impacts on purchasing power, not only shapes the dynamics of domestic economies but also reverberates across the complex web of international trade relations.

In academic discourse, inflation is often portrayed as a unique form of taxation that operates without legislative intervention [3]. It is generally regarded either as a monetary phenomenon [4], or as a discernible pattern of rising prices, as outlined by references [5-7].

The escalation of conspicuous inflation rates across Africa, including Somalia, has stirred a comprehensive investigation of the underlying causes. The persistent presence of price inflation emerges as a significant concern that deeply affects various economic entities. Ensuring the stability of general price levels, a critical macroeconomic goal across nations, is essential for sustainable economic development.

Focusing on Somalia, recent years have seen a marked challenge posed by inflation. The country's susceptibility to heightened inflation is rooted in a combination of factors such as political instability, conflict, and lack of economic investment. The depreciation of the Somali shilling exacerbates this phenomenon, propelling the upward trajectory of prices. The effects of inflation negatively impact living standards in Somalia, making essential commodities increasingly inaccessible for a substantial portion of the population.

In response, the Somali government has initiated a series of measures to alleviate the adverse effects of inflation. These strategies include efforts to stabilize the currency and implement monetary policies to control the money supply. However, the effectiveness of these measures continues to be hindered by the enduring economic and political challenges that the nation faces.

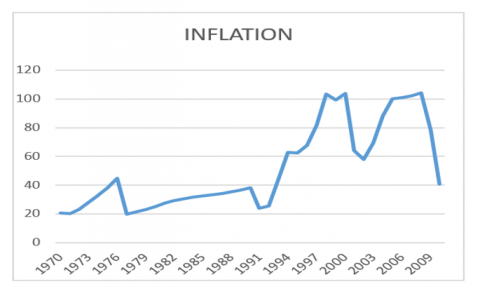

Inflation in Somalia's economic history followed a relatively stable trend until 1992, as illustrated in Figure 1. However, between 1992 and 2000, inflation experienced a significant surge due to the introduction of counterfeit currency by certain merchants, warlords, and regional state administrations. In 2001, inflation markedly decreased, possibly attributed to the citizenry's optimism about the new administration's commitment to curbing illicit activities related to money.

Figure 1. Inflation in Somalia

Source: Author's calculation

From 2002 to 2007, Somalia experienced a substantial surge in inflation, likely influenced by increased spending by warlords, Islamic court authorities, faction leaders, and the introduction of counterfeiting machines. In contrast, inflation declined from 2008 to 2010, due to steady remittances, streamlined government processes, and the effect of dollarization.

Addressing the escalating inflation in Somalia necessitates coherent policy strategies, yet the challenge is compounded by the need for extensive literature. Particularly, there is a notable demand for empirical studies investigating the determinants of inflation within Somalia. Most existing research on inflation determinants in developing economies excludes Somalia. Thus, it is crucial to include Somalia in nation-specific and cross-country empirical studies. This study aims to bridge this knowledge gap and contribute to the broader global conversation on the factors influencing inflation.

The paper is structured as follows: Section 2 reviews the relevant literature, Section 3 outlines the research methodology and data, Section 4 presents the study's findings, and Section 5 concludes with policy implications.

Within the realm of inflation research, numerous empirical studies have been meticulously conducted to illuminate the various factors influencing this economic phenomenon. These studies collectively contribute to the body of knowledge by employing diverse methodologies and timeframes. Despite the extensive depth of investigation into this field, exploring the determinants of inflation remains a dynamic and ongoing endeavor.

In this extensive landscape, researchers have focused their investigations on variables to elucidate the complex dynamics of inflation. These variables include money supply, exchange rates, interest rates, inflation expectations, imported inflation, and Gross Domestic Product (GDP). However, the culmination of these studies underscores the nuanced nature of these relationships, demonstrating that they depend on contextual nuances and exhibit varying degrees of significance.

Below are several seminal studies that encapsulate these complex interactions:

Pollin and Zhu [8] delve into the interplay between economic growth and inflation across 80 countries from 1961 to 2000, utilizing a non-linear regression framework. Their findings reveal a correlation between moderate GDP growth and elevated inflation, but the relationship is not uniform across income strata.

Khalid [9] employs a bivariate VAR approach to identify the primary determinants of inflation. Their analysis highlights the crucial roles of import inflation, the deficit-GDP ratio, seigniorage, money depth, exchange rate depreciation, openness, and domestic credit.

The study conducted by Calderón and Schmidt-Hebbel [10] focuses on the influence of nonmonetary factors on inflation dynamics across 97 countries over two decades. They observe that nations adopting inflation-targeting policies and fixed exchange-rate regimes tend to experience lower inflation rates. Additionally, the integration of financial markets contributes to lower inflation.

The critical roles of inflation expectations, private sector credit, and imported inflation are revealed by Khan et al. [11], who affirm the importance of these variables as determinants of inflation.

In the context of Gulf Cooperation Council countries spanning 1970 to 2007, Kandil and Morsy [12] integrate both domestic and external factors. Government spending and money supply, along with the nominal effective exchange rate and weighted average prices of major trading partners, shape both short- and long-term inflation rates.

Within the Kenyan context, Durevall and Ndung'u [13] use a dynamic error correction model to highlight the short-term impact of money supply on inflation. In contrast, Catão and Terrones [14] underscore the relationship between budget deficits and inflation, particularly in developing nations and contexts characterized by high inflation.

Chhibber [15] examines African anti-inflationary policy instruments, investigating the relationship between exchange rates and inflation. Their findings reflect the intricate, non-linear interaction between these variables.

Furthering this discourse, Moccero et al. [16] and Bashir [17] conduct a comprehensive analysis of inflation determinants across the United States, Japan, the Euro Area, and the United Kingdom from 1960 to 2010. Their investigation underscores the critical role of unemployment and the output gap as drivers of inflation, while noting variations in the reliance on short-term inflation expectations across these economies.

Collectively, these studies shed light on the intricate facets of inflation dynamics. While some studies emphasize the centrality of variables such as money supply and exchange rates, the findings highlight the multidimensional nature of inflation's determinants. As underscored by this literature review, the path forward involves continued and nuanced investigation to enhance our understanding of these complex relationships.

3.1 Data

Data from 1970 to 2010 were used to construct a time series for analysis. The set of readily available data establishes sampling observations. The data was obtained from the Organization of Islamic Cooperation (OIC - SESRIC) and the World Bank. The variables used in this study are GDP deflator (a measure of inflation), money supply, exchange rate, and gross domestic product (GDP).

Among the pantheon of variables, the selection we present bears the mantle of being the most fitting contender to portray the underlying determinants of inflation within the context of Somalia. The rationale behind this discerning choice is firmly rooted in the pragmatic reality that several other pertinent variables, most notably the interest rate, remain conspicuously absent from the realm of available data within Somalia's data ecosystem. Consequently, the meticulously curated variables stand as the lodestones that steer our analysis, illuminating the intricate web of inflation dynamics within this distinctive economic milieu (Table 1).

Table 1. Definition of variables

|

Variables |

Code |

Measurement |

Sources |

|

Inflation |

INF |

Annual growth rate of the GDP deflator |

WB |

|

Money supply |

MS |

Broad money (current LCU) |

WB |

|

Exchange rate |

EXC |

Exchange rate (LCU per US$) |

WB |

|

Economic growth |

GDP |

Real Gross Domestic Product (Constant 2010 $US) |

SESRIC |

3.2 Model specification

Titled "Determinants of Inflation in Somalia", this study delves into various factors. In this exploration, we will use inflation as the key focus, the variable we are trying to understand. We will also consider the Exchange rate, Money supply, and Gross Domestic Product as our explanatory factors.

Our primary goal here is to provide a more precise measurement of how Somalia's money supply (MS), GDP, and exchange rate (EXR) influence inflation. By doing this, we aim to grasp better how inflation works in the short and long term for the country. To help us with this, we will use an approximate theoretical model as our framework.

$\mathrm{INF}=(\mathrm{MS}, \mathrm{GDP}, \mathrm{EXC})$ (1)

The above regression model was translated into a regression equation as stated below:

$\mathrm{INF}=\beta_0+\beta_1 \mathrm{MS}+\beta_2 \mathrm{GDP}+\beta_3 \mathrm{EXC}+\mu$ (2)

where,

INF= Inflation

MS = Broad Money Supply

GDP = Gross Domestic Product

EXG = Exchange Rate

$\beta_0$ = Intercept

$\beta_1, \beta_2$, and $\beta_3$ = are coefficients of the explanatory variables, and each, as expected ≠ 0

μ = is Stochastic error term.

The variables are employed in their log form to avoid problems with non-normality, heteroskedasticity, and mis specified functional form. The model is as follows:

$\mathrm{LINF}_{\mathrm{t}}=\beta_1 \mathrm{LMS}_{\mathrm{t}}+\beta_2 \mathrm{LGDP}_{\mathrm{t}}+\beta_3 \mathrm{LEXC}_{\mathrm{t}}+\mu_t$ (3)

This investigation utilizes two analytical methodologies: the Autoregressive Distribution Lag (ARDL) and the Error Correction Model (ECM). In order to ensure the suitability and reliability of the ECM before its implementation, a series of rigorous Unit Root and Cointegration tests are planned. This preliminary phase is geared towards establishing the foundation of our time series data generation process.

To elaborate, our primary objective is to ascertain whether the variables outlined in Eq. (1) exhibit a consistent stationary behavior or if they exhibit fluctuations. This pivotal step is critical in shaping the groundwork for subsequent proficient econometric modelling endeavors. To this end, we have employed the Augmented Dickey-Fuller (ADF) test, drawing upon Eq. (2) as our reference point, to scrutinize the presence of non-stationary tendencies meticulously.

$\Delta \mathrm{X}_{\mathrm{t}}=\beta_0+\beta_1 \mathrm{X}_{\mathrm{t}-1}+\sum_{i=1}^n \alpha_i \Delta X_{t-1}+\varepsilon_t$ (4)

where, n is the number of lags incorporated into the model, meaning: $\varepsilon_t \sim \operatorname{NID}\left(0, \sigma^2\right)$ and Xt reflects each variable in Eq. (4) for MS, EXR, GDP, and INF.

In pursuit of our defined goal, the ARDL model emerged as a pivotal tool in this study. ARDL bounds testing has exhibited marked advantages over conventional cointegration tests across several dimensions. A distinctive trait of ARDL lies in its versatility, accommodating variables of differing orders of integration – be it I(0), I(1), or a hybrid thereof [7]. Moreover, the ARDL approach adapts adeptly to modeling frameworks, flexibly incorporating an optimal number of lag terms that capture the essence of data generation.

One of ARDL's distinguishing attributes lies in its ability to harmonize short-term adjustments with long-term equilibrium dynamics by formulating an error correction mechanism (ECM). This synthesis is accomplished through a streamlined linear transformation, effectively encapsulating the underlying interaction without obfuscating excessive long-run information. ARDL's efficacy is notably accentuated compared to alternatives like the Johansen and Juselius methodology, particularly in small sample settings.

Within the framework of a multivariate model, the intricate interplay between Inflation, Broad money supply, Gross Domestic Product, and Exchange rate assumes the following delineation:

$\mathrm{LINF}_{\mathrm{t}}=\beta_0+\beta_1 \mathrm{LMS}_{\mathrm{t}}+\beta_2 \mathrm{LGDP}_{\mathrm{t}}+\beta_3 \mathrm{LEXC}_{\mathrm{t}}+\varepsilon_t$ (5)

where, LINFt is the Log of inflation, LMSt is the log of money supply, LGDPt is the log of gross domestic product, LEXCt is the log of exchange rate and εt is the error term. We employed the ARDL model to assess the short- and long-run cointegration between the explained and explanators. Based on the empirical findings [6], the mathematical expression for ARDL cointegration can be written as follows:

$\begin{aligned} & \Delta \mathrm{LINF}_{\mathrm{t}} =\alpha_0+\beta_1 \mathrm{LINF}_{\mathrm{t}-1}+\beta_2 \mathrm{LMS}_{\mathrm{t}-1}+\beta_3 \mathrm{LGDP}_{\mathrm{t}-1} +\beta_4 \mathrm{LEXC}_{\mathrm{t}-1}+\sum_{\mathrm{i}=0}^{\mathrm{q}} \Delta \alpha_1 \mathrm{LINF}_{\mathrm{t}-\mathrm{k}} \sum_{\mathrm{i}=0}^{\mathrm{p}} \Delta \alpha_2 \mathrm{LMS}_{\mathrm{t}-\mathrm{k}} +\sum_{\mathrm{j}=0}^{\mathrm{p}} \Delta \alpha_3 \mathrm{LGDP}_{\mathrm{t}-\mathrm{k}} \sum_{\mathrm{i}=0}^{\mathrm{p}} \Delta \alpha_4 \mathrm{LEXC}_{\mathrm{t}-\mathrm{k}}+\varepsilon_{\mathrm{t}-\mathrm{k}}\end{aligned}$ (6)

In the equation, α0 represents the constant term, while α1 – α4 are the short-term variables' coefficients. Similarly, β1 to β4 signify the long-term elasticity parameters. The parameters q and p denote the optimal lags for the explained and explanatory variables. The symbol Δ indicates the first difference, reflecting the short-term variables, and εt represents the error term. The ARDL cointegration methodology initiates with bound testing.

The null hypothesis (H0) posits that β1 = β2 = β3 = β4 = 0, suggesting the absence of cointegration among the long-term variables. Conversely, the alternative hypothesis (H1) asserts that β1 ≠ β2 ≠ β3 ≠ β4 ≠ 0, indicating the presence of cointegration among these variables. Evaluating the null hypothesis involves employing Critical values and Wald-F statistics. If the calculated Wald-F statistics surpass the upper bound of critical values, it signifies the rejection of the null hypothesis, signaling a long-term connection among the variables. Conversely, if the Wald-F statistics fall within the critical bounds, it suggests a lack of long-term linkage between the variables.

4.1 Descriptive statistics and the correlation coefficients of the study variables

Table 2. Descriptive statistics of the variables

|

Stats |

LINF |

LMS |

LEXC |

LGDP |

|

Mean |

1.643653 |

10.49170 |

2.583631 |

9.338153 |

|

Median |

1.580355 |

11.01703 |

3.242831 |

9.351814 |

|

Maximum |

2.017743 |

11.72787 |

4.503791 |

9.426749 |

|

Minimum |

1.298635 |

8.591065 |

0.798063 |

9.222716 |

|

Std. Dev. |

0.242329 |

1.082551 |

1.483100 |

0.061832 |

Table 3. Correlation coefficients of the study variables

|

Variables |

LINF |

LMS |

LEXC |

LGDP |

|

LINF |

1 |

|

||

|

LMS |

0.778120 |

1 |

|

|

|

LEXC |

0.798035 |

0.954791 |

1 |

|

|

LGDP |

-0.053461 |

0.362272 |

0.158052 |

1 |

Table 2 indicates the results obtained under descriptive statistical analysis. It shows the mean and median of each variable used in this study. Also, it demonstrates the standard deviation, maximum, minimum values and other important information regarding our study variables. Findings show the mean of inflation (1.64), money supply (16.71), exchange rate (2.58), and GDP (9.34). Furthermore, money supply and Gross Domestic Product have the greatest maximum values of (11.73) and (9.43), respectively. The exchange rate has the highest standard deviation (1.48), indicating that its normal values are far from its mean.

Based on the correlation test in Table 3, real GDP is negatively related to inflation. Contrary to this, money supply and exchange rate positively correlate with Somalia's inflation rate.

4.2 Unit root test

The stability of time series data is discerned through the constancy of their mean, standard deviation, and autocovariance. In the realm of macroeconomic variables, achieving stationarity is often challenging. Utilizing non-stationary data for regression analysis can lead to misleading outcomes. To address this, a unit root test is employed to examine the presence of stationarity [18].

Given the nature of our study involving time series data, it becomes imperative to assess the stationarity of the data. To accomplish this, a unit root test is executed. This test utilizes the Augmented Dickey Fuller (ADF) and Phillips-Perron methods to ascertain whether the variables within the model exhibit stationarity. The results are compared against critical values established at the 5% significance level. When the calculated value surpasses these critical values, the null hypothesis is dismissed, indicating the presence of stationarity. Conversely, if the null hypothesis holds, it implies the presence of a unit root, signifying non-stationarity in the variable.

Table 4. Unit root test

|

Variables |

T-Statistics At Level |

|

|

ADF |

PP |

|

|

LINF |

-2.6951* |

-2.1362* |

|

LMS |

-0.6354 |

-0.7761 |

|

LEXC |

-1.4028 |

-1.9151 |

|

LGDP |

-1.8920 |

-2.0539 |

|

|

At First Difference |

|

|

ΔLINF |

-4.0079** |

-4.0336** |

|

ΔLMS |

-6.5815*** |

-6.5812*** |

|

ΔLEXC |

-4.2406*** |

-4.3585*** |

|

ΔLGDP |

-6.5821*** |

-6.5862*** |

All variables are differenced stationary, as shown by the unit root findings in Table 4. This can be demonstrated by looking at each variable's ADF and PP test data, which all fall below the 95% ADF and PP critical values. Because of this, we can conclude that none of the series is at rest. In the first difference, however, as shown in Table 4, all variables are stationary. Since all variables are assumed to be stationary at the first difference, we can say that they are all of integrated order one, denoted in this context by the letter I(1). As indicated in our equation, the cointegration relation between LINF and its explanatory factors implies that we can move on to stage two of testing the long-run and short-run elasticities of variables.

4.3 Cointegration bounds test

The F-statistic value of (5.171702) in Table 5 is greater than the upper and lower critical values at a significance level of 5 per cent. The outcome of the Bound test supports the existence of a long-run cointegrating relationship between inflation and other contributing factors of inflation in Somalia. This also permits the ECM to proceed.

Table 5. F-bounds test

|

F-Statistic |

Level of Significance |

Bounds Test Critical Values |

|

|

|

|

I (0) |

I (1) |

|

5.171702 |

1% |

3.65 |

4.66 |

|

5% |

2.79 |

3.67 |

|

|

|

10% |

2.37 |

3.2 |

4.4 ARDL long-run and short-run results with diagnostics

The long-run results, as depicted in Table 6, show substantial insights into the dynamics between money supply, GDP, and inflation. Our findings reveal a long-run, statistically significant, positive association between money supply and inflation within the Somali context. Specifically, an incremental 1% upswing in Somalia's money supply translates into a 39.35% surge in the long-term inflation rate.

Table 6. Long-run estimates of coefficients

|

Variables |

Coefficient |

|

C |

2.2854 |

|

(3.9591) *** |

|

|

LMS |

0.3935 |

|

(2.9404) *** |

|

|

LEXC |

-0.1387 |

|

(0.0947) |

|

|

LGDP |

-2.6117 |

|

(0.6885) *** |

|

|

Reset test |

2.5516 [0.1210] |

|

Serial correlation |

0.6066 [0.7384] |

|

Heteroskedasticity |

9.8895 [0.2729] |

|

Normality |

0.2009 [0.9044] |

Note: ***, **,* Indicate significance levels at 1%, 5%, and 10%. The T-statistics are reported in (..), p-values are in [..]

Furthermore, the compelling influence of GDP on inflation unfolds, demonstrating a robust, negative relationship in the long run. Our study discloses that a 1% enhancement in GDP corresponds to a remarkable 261.17% reduction in the inflation rate within Somalia's economic milieu. On a different note, our investigation finds that the exchange rate's impact on Somalia's inflation rate remains inconsequential. Of significance, the constant coefficient underscores that the GDP deflator retains a fixed value of 2.285, regardless of variations in independent variables.

The outcome concerning money supply corroborates the stance advocated by classical economists, aligning with the quantity theory of money. As espoused by classical economic thought, an augmented money supply stimulates economic investment through increased credit availability, fostering elevated employment levels. This surge in investment and employment opportunities subsequently spurs aggregate demand, inevitably leading to heightened inflationary pressures.

Our insights regarding GDP mirror the findings of past studies, notably [19-21], corroborating the proposition that real Gross Domestic Product wields a negative impact on inflation within the long-term trajectory.

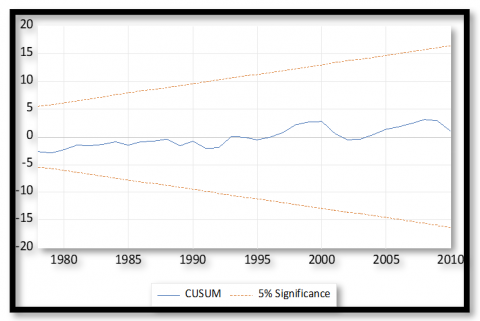

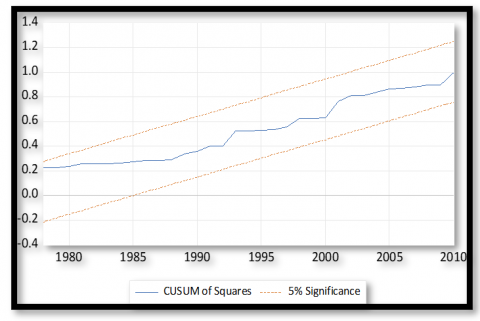

Turning to the diagnostic checks, our ARDL model emerges robust. The absence of serial correlation, heteroscedasticity, model misspecification, and normality concerns underscore the model's robustness. Additionally, the stability of ARDL model coefficients over the observed period is confirmed through the CUSUM and CUSUM-square tests, as visually presented in Figures 2 and 3.

Shifting the focus to short-run dynamics, the computed short-run elasticities, extracted from the coefficients of the first-differenced variables, present valuable insights, as documented in Table 7. Our findings underscore a positive and statistically significant interconnection between lagged inflation and present inflation in Somalia. This implies that an escalation in the inflation rate during the prior year cascades into a corresponding rise in the current year's inflation rate.

Further enriching this short-term narrative, our study illuminates the impact of lagged GDP on inflation. A 1% upswing in the preceding year's GDP is associated with a substantial 108.21% inflation uptick.

The pivotal error correction coefficient, underscored by its negative value and statistical significance, substantiates the hypothesis of long-run equilibrium interaction between inflation and its underlying determinants. At an approximate annual rate of 60.13%, our findings suggest that inflation possesses an inherent mechanism for self-correction, propelling it back to the path of long-term equilibrium.

Figure 2. CUSUM test

Figure 3. CUSUM square test

Table 7. Short-run ECM results

|

Variables |

Coefficient |

|

ΔLINFt-1 |

0.4031 |

|

(2.7835) *** |

|

|

ΔLMS |

-0.0586 |

|

(2.9404) |

|

|

ΔLEXC |

-0.0910 |

|

(0.0578) |

|

|

ΔLGDPt-1 |

1.0821 |

|

(0.4840) ** |

|

|

ECTt-1 |

-0.6013 (-5.4135) *** |

Note: ***, **,* Indicate significance levels at 1%, 5%, and 10%. The T-statistics are reported in (..), p-values are in [..]

4.5 Granger causality test

To determine the direction of causality between variables, we conducted the Granger causality test shown in Table 8. We observed unidirectional causation from exchange rate to inflation and money supply to exchange rate. There are no bidirectional causal associations detected among our variables. In addition, there is evidence of unidirectional causation between gross domestic product and exchange rate.

Table 8. Granger causality test

|

Null Hypothesis: |

Obs |

F-Statistic |

Prob. |

|

LMS → LINF |

39 |

2.11449 |

0.1363 |

|

LINF → LMS |

39 |

0.32553 |

0.7244 |

|

LGDP → LINF |

39 |

0.48793 |

0.6181 |

|

LINF → LGDP |

39 |

1.68420 |

0.2007 |

|

LEXC→ LINF |

39 |

5.69390 |

0.0074 |

|

LINF → LEXC |

39 |

0.23428 |

0.7924 |

|

LGDP → LMS |

39 |

0.26432 |

0.7693 |

|

LMS→ LGDP |

39 |

0.05637 |

0.9453 |

|

LEXC→ LMS |

39 |

1.22978 |

0.3050 |

|

LMS → LEXC |

39 |

6.55780 |

0.0039 |

|

LEXC → LGDP |

39 |

0.37833 |

0.6879 |

|

LGDP → LEXC |

39 |

3.33717 |

0.0475 |

→ signifies that variable "X" does not granger cause variable "Y"

In this study, we have embarked on a thorough exploration of the factors that shape inflation trends in Somalia, covering the period from 1970 to 2010. Our data, sourced from reputable institutions like the World Bank, IMF, SESRIC, and the Central Bank of Somalia, has enabled us to delve into the determinants that drive inflation in the Somali context. Our attention has been focused on money supply, exchange rates, and Gross Domestic Product (GDP) as explanatory variables, while inflation is the dependent variable.

We have employed the Autoregressive Distributed Lag (ARDL) framework, explicitly using the bounds-testing method. This method has proven its versatility, as it can be applied irrespective of the integration order of the regressors, setting it apart from other similar tests.

Our examination of the unit root test results revealed that none of our variables were stationary at the base level. However, a transformation occurred, and all variables achieved stationarity at a higher level. This laid the foundation for our subsequent exploration of cointegration relationships using the bound test, which yielded compelling evidence of long-run cointegration between inflation and its determinants, setting the stage for our exploration of error correction mechanisms.

Zooming into the long-term view, our findings revealed significant insights. We discovered a strong, positive, statistically significant connection between money supply and inflation. To put it into perspective, a 1% increase in the money supply resulted in a 39.35% rise in the inflation rate. This emphasizes the impact of monetary expansion on inflation. In contrast, GDP emerged as a powerful player, showcasing a remarkable negative relationship with inflation. Notably, a 1% growth in GDP corresponded to a substantial 261.17% drop in the inflation rate within the Somali context. On the other hand, the link between exchange rates and inflation revealed itself to be insignificant in the long run.

Shifting the focus to the short run, our findings illuminated the influence of both lagged inflation and lagged GDP on the present inflation rate. We observed a positive and statistically significant relationship between these variables and short-term inflation. Our emphasis on dynamic stability aligned seamlessly with the error-correction term's role, which exhibited statistical significance and carried a negative coefficient, aligning well with the equilibrium-seeking nature of cointegrating equations.

The Granger causality test uncovered unidirectional causal patterns in tandem with these empirical insights. Exchange rates influence inflation, much like money supply on exchange rates and GDP on the exchange rate.

Steering toward policy implications, our study underscores the paramount role of real GDP growth as a tool for Somali policymakers to tackle inflation effectively. This determinant emerged as a robust influencer throughout our research period. This implies that initiatives fostering real GDP growth can control inflation trends substantially.

Nevertheless, amidst these valuable insights, we remain aware of certain limitations that may have nuanced our findings. Limited historical data availability could have masked certain intricacies of inflation in Somalia. Furthermore, our macroeconomic lens missed micro-level factors driving inflation dynamics.

Future research avenues hold promise for addressing these limitations and further enriching our understanding of Somalia's inflation landscape. Enhanced datasets capturing finer nuances could offer a clearer picture. A comprehensive exploration of macro and micro determinants would provide a more holistic understanding. Additionally, evaluating the impact of diverse policy interventions on inflation dynamics could pave the way for tailored strategies in response to Somalia's unique challenges. In summary, our study contributes significantly, and future inquiries stand poised to uncover additional layers of insight in this critical domain.

[1] Lim, Y.C., Sek, S.K. (2015). An examination on the determinants of inflation. Journal of Economics, Business and Management, 3(7): 678-682. https://doi.org/10.7763/JOEBM.2015.V3.265

[2] Ruzima, M., Veerachamy, P. (2015). A study on determinants of inflation in Rwanda from 1970–2013. International Journal of Management and Development Studies, 4(4): 390-401.

[3] Friedman, M. (1963). Inflation: Causes and Consequences. New York: Asia Publishing House.

[4] Kemmerer, E.W. (1942). The ABC of Inflation. New York: McGraw-Hill.

[5] Ackley, G. (1978). Microeconomics: Theory and Policy. New York: Collier Macmilan.

[6] Shapiro, E. (1944). Macroeconomic Analysis, 5th Ed. New Delhi: Galgotia Publisher.

[7] Johnson, H.E. (1970). Essays in Monetary Economic, 2nd Ed. Cambridge: Harvard University Press.

[8] Pollin, R., Zhu, A. (2006). Inflation and economic growth: A cross-country nonlinear analysis. Journal of Post Keynesian Economics, 28(4): 593-614. https://doi.org/10.2753/PKE0160-3477280404

[9] Khalid, A.M. (2005). Economic growth, inflation, and monetary policy in Pakistan: Preliminary empirical estimates. The Pakistan Development Review, 44(4): 961-974. https://www.jstor.org/stable/41261140.

[10] Calderón, C., Schmidt-Hebbel, K. (2008). What drives inflation in the world? Documentos de Trabajo (Banco Central de Chile), (491): 1.

[11] Khan, A.A., Ahmed, Q.M., Hyder, K. (2007). Determinants of recent inflation in Pakistan. Research Report No.66. Islamabad: Pakistan Institute of Development Economics. https://mpra.ub.uni-muenchen.de/id/eprint/16254.

[12] Kandil, M., Morsy, H. (2011). Determinants of inflation in GCC. Middle East Development Journal, 3(2): 141-158. https://doi.org/10.1142/S1793812011000351

[13] Durevall, D., Ndung'u, N.S. (2001). A dynamic model of inflation of Kenya, 1974-96. Journal of African Economies, 10(1): 92-125. https://doi.org/10.1093/jae/10.1.92

[14] Catão, L., Terrones, M.E. (2001). Fiscal deficits and inflation a new look at the emerging market evidence. IMF Working Paper No. 65. https://ssrn.com/abstract=879583.

[15] Chhibber, A. (1991). Africa's rising inflation: Causes, consequences, and cures. World Bank Publications.

[16] Moccero, D., Watanabe, S., Cournède, B. (2011). What drives inflation in the major OECD economies? https://doi.org/10.1787/18151973

[17] Bashir, D.F. (2011). Determinants of inflation in Pakistan: An econometric analysis using Johansen co-integration approach. Australian Journal of Business and Management Research, 1(5): 71-82.

[18] Gujarati, D.N. (2022). Basic Econometrics. Prentice Hall.

[19] Tsegay, H. (2014). Determinants of recent inflation: The case of Ethiopia. Doctoral Dissertation, Mekelle University.

[20] Kibrom, T. (2008), The sources of inflationary experience in Ethiopia: MSc Thesis. Addis Ababa University.

[21] Menji, S. (2008). Determinants of recent inflation in Ethiopia. MSc Thesis, Mekelle University. https://mpra.ub.uni-muenchen.de/id/eprint/29668.