Olena Parubets*![]() | Olena Shyshkina

| Olena Shyshkina![]() | Iryna Sadchykova

| Iryna Sadchykova![]() | Yurii Yevtushenko

| Yurii Yevtushenko![]() | Artem Tarasenko

| Artem Tarasenko![]() | Ihor Potseluiko

| Ihor Potseluiko![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This article aims to identify the trends and characteristics of the credit services market's evolution amidst financial instability in Ukraine. Utilizing a range of scientific methodologies, including content analysis, comparative method, statistical calculations, and econometric modeling based on correlation-regression analysis with cubic one-factor regression models, the study delves into the underlying principles of financial instability, its essence, and primary triggers. A comprehensive statistical analysis of Ukraine's economic trends and the state of bank lending to economic entities was conducted. To enhance understanding of the credit services market's development under Ukraine's unstable economic conditions, an analysis of the influence of bank lending indicators on the key parameters depicting the national economy's dynamic was performed through econometric modeling. Findings reveal that the credit services market plays a crucial role in the economic development of countries, particularly where the securities market is underdeveloped. In Ukraine, the credit services market has acted as a catalyst for crisis phenomena in the banking system, thereby slowing its long-term development.

credit services market, credit relations, financial stability, financial system, credit institutions, commercial bank, Ukraine

The credit services market is a critical component in the economic development of any nation. In contemporary conditions, highly developed nations inherently display a sophisticated level of credit relations and the efficient operation of financial institutions providing credit services. Presently, all economic entities, including households, entrepreneurial subjects, and governmental bodies, form credit relations. The emergence of such relations is primarily driven by these entities' constant and objective need for financial resources, which may be unavailable at certain times. Conversely, to sustain their activities and ensure efficient utilization of resources, financial institutions continuously strive to provide these resources to reliable clients for income generation. This objective existence of credit relations in today's world underscores the importance and necessity of regulating their emergence and development to foster favorable conditions for further economic growth.

The credit services market plays a pivotal role in maintaining a country's financial stability. Historical evidence suggests that systemic crisis problems can originate within this market, potentially resulting in destructive trends that could negatively impact global economic development. The financial and economic crisis of 2007-2008 serves as a testament to this. Thus, the importance of the credit services market's development in the modern world is heightened, as is the need for effectively supervising credit institutions to prevent new crisis phenomena from emerging in this market's operations. This situation amplifies the urgency and appropriateness of conducting additional scientific research in this area.

The development of the credit services market is particularly crucial for countries with limited access to investment resources. In such instances, credit funds serve as the main source of financial resources for national economic development. This situation is generally characteristic of nations gradually developing their own financial markets.

It is reasonable to include Ukraine among these countries, which, amidst financial instability caused by external and internal factors, is striving to ensure banking system stability, including through the development of the credit services market. Thus, the main goal of the work is the research and description of the development features of the credit services market in the conditions of the financial instability precisely in Ukraine. To realize this goal, the following tasks were defined: 1) describe the essence of the financial instability, determine its signs; 3) justify the peculiarities of the functioning of the credit services market; 4) determine the main transformations taking place in the credit services market in the conditions of the financial instability; 5) conduct an applied study of the analysis of the development of the credit services market in Ukraine in the conditions of the unstable functioning of the financial system.

Despite the tremendously challenging military conditions for Ukrainian science, as pointed out by Novomlynets et al. [1], scientists remain undeterred in their research pursuits. They continue to explore new strategies to safeguard the nation's macroeconomic stability and enhance the resilience of the financial system against internal and external threats. This topic has been the focus of numerous scientific studies, with a noticeable increase following the 2007-2008 financial and economic crisis and the subsequent global economic recovery.

In the works of Das and Ordal [2], and Desalegn et al. [3], the relationship between macroeconomic and financial stability is examined. Leonov et al. [4] evaluated the impact of the shadow economy on the nation's macro-financial stability, while Mishra and Dubey [5] explored the importance of monetary policy tools in ensuring financial stability. Shkolnyk et al. [6] conducted an analysis on the process of guaranteeing financial system stability amidst the country's challenging economic circumstances. Gieseсke and Weber's [7] research focused on analyzing the variation in aggregate credit losses for loans granted to business entities with low financial stability, arguing that their activity is heavily influenced by the stability of the financial system in developed countries.

Gao and Fan [8] contend that ensuring the stability of national economies' development has become society's primary task. In the research, Nikiforov et al. [9] and Bogolib [10] suggest that substantial changes in the factors necessitate considering the main macroeconomic trends directly influencing each country's economy. Therefore, constant analysis of macroeconomic indicators allows the identification of strategic development priorities for the near future [2, 4, 11, 12].

The issues of ensuring macroeconomic stability are discussed in the works of Carli and Modesto [13], where they focus more on the role of fiscal policy and public debt in ensuring macroeconomic stability. Khan [14] describes the impact of macroeconomic instability on environmental development, while Radionova [12, 15] validates the characteristic features of the state's economic policy formation under macroeconomic instability.

Numerous factors can trigger macroeconomic instability, making it incredibly challenging to identify them all and prevent their destructive impact on national economic development processes. However, many countries strive to develop a level of resilience against such factors, build appropriate funds of financial resources, diversify, and enhance the instruments of state economic process regulation. Special emphasis is placed on financial sphere regulation and ensuring financial system stability and its individual indicators. Financial stability is the primary foundation for ensuring economic systems' stability, hence the plethora of theoretical and applied studies on financial stability formation and the ongoing search for new tools to ensure it in an ever-changing external world [16-19], the number of scientific works analyzing the essence and causes of financial instability surged notably after the 2007-2008 financial and economic crisis. Even today, this topic continues to be actively researched. This trend may be attributed to the increasingly pervasive influence of financial relations on economic relations and the accelerating pace of economic financialization.

Zając et al. [20], Elsayed et al. [21] as well as Makarenko and Ponomarenko [22] prove that the financial stability is a complex element for ensuring the stability of the national economy from the standpoint of its provision. The convergence of financial relations and digitization processes, formation of a system of decentralized (alternative) finance, excessive politicization of the economic life, an even greater level of the financial globalization and deepening the cooperation between financial institutions around the world have become the key problems of ensuring the financial stability. This is gradually changing the entire field of the financial services. Especially today, the development of this sphere is affected by the processes of digitalization of the economic relations, which are becoming unpredictable, and the creation and use of certain types of digital assets are difficult to regulate by state institutions.

Scientists [3, 23-25] note that the main factors that exert the most significant influence on the formation of the financial stability in the financial markets include: accelerated creation of the innovative financial companies; strengthening the political pressure on the adoption of economic decisions; insufficiently quick recovery of the markets after financial crises; the pandemic and its consequences; ongoing; digital inequality of jurisdictions; formation of the global ecosystem of cryptoassets; emergence of the digital currencies of central banks; legal uncertainty in the application of the emerging digital legislation.

The scientific articlesoutline the features of applying a cognitive approach to determining the essence of the financial services market, model the financial influence of the political-oligarchic interests of the state-sponsored enterprises on the formation and implementation of the financial policy in the state, and also reveal the conceptual principles of assessing, forecasting and modeling the harmony of the economic development of regions [16, 26-31].

The credit services market plays a special role in ensuring the financial stability of the state. The studies consider the specific issues of the development of such a market within the national financial services markets and its impact on the national economy functioning [32-39]. At the same time, despite the fact that the scientific literature today has already produced a fairly significant number of scientific works in the direction of studying the essence of credit relations [40-43], their role in ensuring the stable economic development of the countries [44-46], the issues on the complex impact of such a market on ensuring the financial stability remain insufficiently researched, especially in the conditions of the modern digitalization processes of the financial relations.

General and special methods of the scientific research became the methodological basis of the research.

The methods of the theoretical research (content analysis, abstraction, analysis, synthesis) were used when considering the essence of the financial stability and its features. The historical retrospection method is used in the study of the peculiarities of the development of the credit services market in Ukraine, description of the economic conditions in which the country developed during the entire independence period.

The methods of measurement, comparison, and comparative analysis were used when conducting an empirical study of the features of the development of the credit services market and its role in ensuring the economic development. The index method was used for a detailed examination of the patterns of changes in economic and macro-financial indicators. This made it possible to analyze the dynamics of their change over a certain period of time. Especially the use of the index method was justified when comparing the trends of economic development and the functioning of the financial system of Ukraine in a certain period. This method was also used to analyze the development of the credit services market. The analysis of the rates of change of individual indicators made it possible to determine their situational change each year during 2006-2021. In this case, the calculations were made according to the formula:

$E I=\frac{E I^t}{E I^{t-1}}$ ,

where EI - macroeconomic, financial indicator (GDP, volume of bank lending, exchange rate of the national currency, volume of average salary);

ЕІt - value of the macroeconomic, financial indicator in the current period (period t);

ЕІt-1 - value of the macroeconomic, financial indicator in the previous to the current period (t-1).

To deepen the understanding of the specifics of the bank lending impact on the economic development of the country, the dependence of the development of the credit services market on the macroeconomic and financial indicators, in the article, the econometric modeling methods are used to describe: the impact of the bank lending volumes on the country's GDP; the impact of the bank lending volume to the households on the Ukraine's GDP; the impact of the bank lending volume to business entities on the GDP of Ukraine; the influence of rates of change in the bank lending volume on the rates of change in Ukraine's GDP; the influence of rates of change in the bank lending volume to the households on the rates of change in Ukraine's GDP; the influence of the rates of change in the bank lending vouleme to business entities on the rates of change in Ukraine's GDP.

Using the correlation-regression analysis, the cubic one-factor econometric models were built, which were implemented based on the use of the least squares’ method, and therefore the calculation equation of such a model.

$\hat{\mathrm{y}}=\hat{\alpha}_0+\hat{\alpha}_1 \mathrm{x}^3+\hat{\alpha}_2 \mathrm{x}^2+\hat{\alpha}_3 \mathrm{x}$, (1)

where, $\hat{\mathrm{y}}$ - value of the dependent variable in the calculation model (GDP - gross domestic product of Ukraine; RCGDP - rate of change in GDP);

х - value of the independent variable (Bl - bank lending; Blh - bank lending volume to individuals; BlEn - bank lending volume to business entities; RCBL - the rate of change in the bank lending volume; RCBlh - rate of change in the bank lending volume to individuals; RC BlЕn - rate of change in the bank lending volume to business entities);

$\hat{\alpha}_0, \hat{\alpha}_1, \hat{\alpha}_2, \hat{\alpha}_3$ - model parameters.

To search for model parameters $\hat{\alpha}_0, \hat{\alpha}_1, \hat{\alpha}_2, \hat{\alpha}_3$, it is necessary to determine such a y-value, which would best correspond to the real dependence between the indicators. In this case, the error of the difference between the real value of y and its calculated indicator should be minimal, i.e.,

$\varepsilon=y-\hat{y} \rightarrow \min$, (2)

where, у - value of the dependent variable of the actually existing dependence between two indicators;

ɛ - error.

$\mathrm{y}=\alpha_0+\alpha_1 \mathrm{x}^3+\alpha_2 \mathrm{x}^2+\alpha_3 \mathrm{x}+\varepsilon$, (3)

So,

$\varepsilon=y-\left(\hat{a}_0+\hat{a}_1 * x^3+\hat{a}_2 * x^2+\hat{a}_3 * x\right) \rightarrow \min$. (4)

Using the outlined formula, the staged application of correlation-regression analysis, it is possible to specify the algebraic form of the calculation model (dependencies $\hat{\mathrm{y}}$ from х) let’s find the parameters of this equation ($\hat{\alpha}_0, \hat{\alpha}_1, \hat{\alpha}_2, \hat{\alpha}_3$) and define dependence of one parameter on another in the form of an algebraic equation. Technically, the modeling was carried out with the help of ordinary statistical programs, in which it is possible to build regression models and conduct correlation analysis (determine indicators of determination, correlation and the value of F-statistics). In the sample, 16 observations were identified, each observation is a reflection of statistical information about an economic indicator at the end of the year for which such an indicator is recorded in the presented analytical data.

The information base for the scientific research is based on statistical and analytical data provided by the State Statistics Service of Ukraine and the National Bank of Ukraine. In particular, based on the data of the State Statistics Service, information on the gross domestic product of Ukraine was summarized. The open data of the National Bank of Ukraine regarding financial statistics made it possible to use systematized information on the volume of bank lending, lending to various economic entities by banking institutions.

Let's start the research with the substantiation of the financial instability essence. To do this, we will also consider the content of the "macroeconomic instability" category, since the largely dissipative development of the financial system is quite often accompanied by the stochastic economic processes.

Macroeconomic instability is a state of the country's economic system in which the fluctuating processes are strong and the results of their influence are unpredictable. Macroeconomic instability is characterized by the classic process of economic development as a cybernetic system, in which the crisis phenomena gradually emerge, develop, deepen and destructively change the trajectory of the economic development. From the standpoint of the systemic approach, the theory of synergy, economic systems develop according to the described scheme. However, rather radical changes in the economic space functioning, which are determined not by one, but by many factors, are characteristic of the macroeconomic instability.

In a significant number of the scientific works, the essence of macroeconomic instability is considered through the specification of the macroeconomic stability content itself. For example, the International Monetary Fund defines the macroeconomic stability as a state of the economy in which the key economic relationships are in balance, for example, between the domestic demand and production, balance of payments, fiscal revenues and expenditures, as well as savings and investments [8]. It is logical to assume that all outlined processes are not inherent to the state of macroeconomic instability. However, in reality, economic processes are quite closely related to each other and macroeconomic instability does not occur at one moment when all the above signs already exist. The signs of instability are formed and develop gradually, but the macroeconomic instability is faster, but not instantaneous.

If we analyze the main signs of the macroeconomic instability, they should include the following: imbalances in the capital markets; devaluation of the national currency; violation of the balance of payments; gradual growth of the inflation index; rising unemployment; decrease in the gross domestic product.

In fact, with the macroeconomic instability, we observe the deterioration of all macroeconomic indicators, which collectively characterize the state of the economic system in a certain period. In today's realities and taking into account the signs of the macroeconomic instability, it can be stated that it is primarily related to the financial instability, which has a destructive effect on the national economy development in general. Financial instability is a state of the financial system in which there are unforeseeable, negative trends in the functioning of financial institutions, their clients and markets in general. Financial instability by its very nature is a complex phenomenon for a comprehensive analysis of the causes and consequences of its occurrence. Today, in the scientific literature there is a significant number of the scientific publications, which study the essence of this phenomenon, the reasons for its occurrence and the means of countering the consequences that arise during the financial instability period. For example, the Federal Reserve System defines the financial stability as follows: “financial stability is about building a financial system that can function in good times and bad, and can absorb all the good and bad things that happen in the U.S. economy at any moment; it isn't about preventing failure or stopping people or businesses from making or losing money. It is just helping to create conditions where the system keeps working effectively even with such events” [47]. However, despite numerous efforts, reliable preventive tools for preventing the occurrence of financial crises have not yet been developed, although their number is increasing, and their effectiveness is increasing with each financial crisis. The threat of the financial crises and, accordingly, macroeconomic instability is determined by the fact that crisis phenomena in the financial system quickly spread to the functioning of world financial markets and this can lead to the world economy rcession.

The Federal Reserve System also provides another definition of the financial stability, namely: “a financial system is considered stable when banks, other lenders, and financial markets are able to provide the households, communities, and businesses with the financing they need to invest, grow, and participate in a well-functioning economy - and can do so without making the system more vulnerable to sharp downturns. In contrast, in an unstable system, an economic shock is likely to have much larger effects, disrupting the credit flow and leading to larger-than-expected declines in the employment and economic activity” (Nikiforov et al. (2022)). Thus, analyzing the essence of this approach to understanding the financial stability, it can be stated that the main attention is paid to credit services in it. That is, directly the financial stability level in the country depends significantly on the development of the credit relations.

In general, if the financial stability is present in the country, the following occurs: financial system effectively transforms free funds of citizens and businesses into loans and investments; financial system is liquid and capitalized, and therefore resistant to crisis phenomena; payments and settlements are made on time and in full; participants of the financial system carefully assess risks and manage them; difficulties of financial institutions do not extend to the system as a whole.

Macroeconomic and financial instability are not new processes, phenomena that we have been observing for the past twenty years, similar crisis phenomena in the world economy occur periodically. In most cases, their causes are different, but the consequences are the same. The consequence of any economic crisis is the deterioration of the level of social and economic security of the population. If financially possible, governments use available funds to reduce the destructive impact of the crisis phenomena on the current state of economic entities. However, in the countries that are at the stage of market economy development, the economic and financial crises occur with greater losses, a decrease in the level of the national economy development, and a sharp decline in the economic and financial security of the country. In such countries, the Central Banks do not cope with the functions entrusted to them to ensure the stability of the national currency, and this triggers a chain reaction of the entire mechanism of the macroeconomic instability. Restoring the pre-crisis indicators of the development is also difficult.

Ukraine is a country that periodically faces financial and economic crises in its development. Today, the country is in a state of a severe war with the Russian Federation, which has an extremely destructive effect on its economic development. However, before the war, the country also periodically experienced the stages of economic recession, the reasons for which were completely different. In fact, we can state with confidence that every seven years Ukraine experiences a period of the financial instability, which is accompanied by a sharp deterioration of the country's macroeconomic development. That is why the example of Ukraine is quite interesting for researching the peculiarities of the emergence of financial crises, the development of the credit services market in the conditions of financial instability.

During thirty years of its own independence, Ukraine went through difficult periods of its own economic development. In particular:

1) the first half of the 90s - the difficult macroeconomic situation in the country was due to the termination of the Soviet Union, the processes of hyperinflation, devaluation negatively affected the socio-economic development of society, destruction of the established economic ties, criminalization of the economic relations, barter operations, low efficiency state institutions contributed to the deepening of the economic crisis;

2) the end of the 1990s - financial instability was associated with the default in the Russian Federation, devaluation of the ruble, which, due to the close economic ties between the countries, also affected the stability of the national currency of Ukraine - the hryvnia. For the first time since its introduction in the country (1996), its devaluation was observed. However, due to the country's low level of the involvement in the world economy, the underdevelopment of the financial system, individual fluctuations within its borders did not have a significant impact on the country's economic development;

3) 2004-2005 - the period of the Orange Revolution, changing the country's development vector to the European one, increasing the level of the economic cooperation with EU countries, deepening the ties in various spheres of the national economy, especially the financial one. A significant number of foreign financial groups bought out or created banking institutions and the share of foreign capital in the banking system increased significantly. This period can be called a period of the financial stability. After the Orange Revolution, the country received a new impetus to the economic development, especially due to the attraction of significant amounts of foreign investment;

4) 2007-2008 - the financial and economic crisis led to negative consequences for the economy development of Ukraine. Among all European countries, Ukraine faced the greatest difficulties. The liberalization of the financial legislation and active development of the economy in 2000-2005 led to the gradual involvement of the Ukrainian economy in the world economy. This allowed, on the one hand, to ensure the economic development of the country, especially in 2005-2007. However, on the other hand, it also reduced the level of the financial security of the country, affected the ability to counteract external destructive factors that were forming in the global financial system. Accordingly, the consequences of the global crisis of 2008-2009 were particularly difficult for the financial system of Ukraine, there was a significant devaluation of the national currency, inflation increased, the financial condition of banking institutions and their ability to fulfill their obligations significantly worsened. The financial system of Ukraine was not ready to deal with external threats, and therefore, unlike other countries, Ukraine had no experience of dealing with such financial and economic destructions. Thanks to the cooperation with the IMF, it was possible to restore the stability of the country's financial system and return to the period of economic development. However, the consequences of the financial crisis of 2007-2008 the country's financial system still feels it;

5) 2014-2015 is a period of the extremely difficult political, social and economic imbalances for the country. The Revolution of Dignity played a special role in the formation of crisis phenomena in the financial system and the national economy. In fact, the crisis of this period was caused exclusively by the internal social events with a fairly stable development of the world economy. The existential crisis of the Ukrainian nation in 2014 led to the rapprochement of the country with the EU, the signing of an agreement on a free trade zone, and, accordingly, the annexation of the Crimea by the Russian Federation, and the war in the East of the country. This period became a time of significant transformations of both Ukrainian society and the economy in general. The result of the described events was a difficult financial situation in the country, which was accompanied by the devaluation of the national currency by more than four times, closure and liquidation of a number of commercial banks, the nationalization of the country's largest commercial bank (PrivatBank), and the loss of their own business by banking institutions in Crimea, in the East of Ukraine. As a result of the financial crisis, the rate of economic development of the country has also decreased sharply, and there is a significant decline in the level of social and economic security of citizens. However, during 2016-2021, the country experienced a gradual recovery of the country's economy. The reform of the banking system had a positive effect on the financial stability of the country in general.

6) 2022 - the war with the Russian Federation, which is accompanied by a decline in the country's economic development, loss of part of the country's territory, mass migration of citizens, significant destruction of the infrastructure and the death of Ukrainians. The war had a destructive effect on all spheres of the Ukrainian society. Today, you can observe the devaluation of the hryvnia (the official exchange rate of the hryvnia fell from UAH 27.0 per 1 USD in 2021 to UAH 36.56 per 1 USD by the end of 2022).

Thus, taking into account the outlined historical aspects of the development of Ukraine, it can be argued that permanent financial and economic crises are inherent in its economic development. In this case, it is possible to claim that such crisis situations are cyclical, although the reasons for their occurrence are different. That is why the economic development of Ukraine and its credit services market should be analyzed in the context of the functioning of such a market during the periods of the macroeconomic and financial instability.

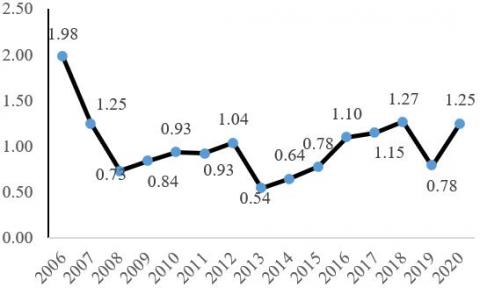

We will analyze the main trends of the economic development of Ukraine over the past fifteen years. In Figure 1, the information specifically about the rates of change of the main economic indicators that occurred in 2006-2021 is presented. The outlined indicators even better reflect the peculiarities of the turbulent economic development of Ukraine in the specified period and record the declines and rises of the national economy. Let's consider the presented information in more detail.

Thus, it can be stated that the rate of change in the volume of real GDP of Ukraine decreased the most during periods of complex social and political events in the country (2009, 2014-2016). The pace of the level of average wages actually shows the same trajectory of change. In 2021, this indicator in Ukraine increased by 1.47 times, according to the State Statistics Service of Ukraine.

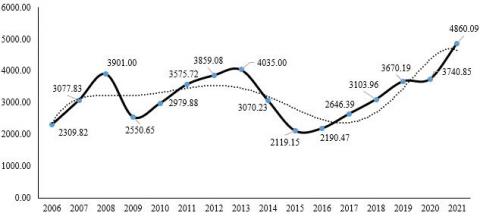

For a deeper understanding of the peculiarities of the macroeconomic development of Ukraine, the GDP volume per person and the corresponding rates of change of this indicator were determined. At the end of 2021, one citizen of Ukraine accounted for 4.860.09 USD. This is the highest indicator for the entire period of the economic development of the country. In 2020, this figure was 3,740.85 US dollars, which is lower than in 2013. This only confirms that in reality the recovery of the country after complex social upheavals is quite difficult and takes a long time. At the same time, information on the rates of change in GDP per person attests to the turbulent nature of such changes.

In the described case, when determining the real incomes of citizens, only one factor that devalues monetary incomes was taken into account - the exchange rate of the national currency. At the same time, the inflatiom level in Ukraine at different periods acquired quite critical values, which also had a negative impact on the level of the social and economic security of citizens. It is quite logical that in critical periods for the country's economy, the prices rose significantly and then the rates of their change gradually decreased. The highest level of inflation in the country was officially recorded in April 2015 - 114. However, official information in Ukraine, especially in the part of analyzing price changes, does not always correspond to the realities observed by Ukrainians. In difficult periods of the economic decline, state authorities often carried out certain manipulations with the calculation methodology for this indicator. Therefore, the official statistics do not reflect real inflation indices. However, as a result, the significant price fluctuations for various goods and services were observed in the country until 2016. After the introduction by the National Bank of Ukraine of strict approaches to ensuring the price stability, the inflation level slowed down significantly.

Analyzing the data of Figure 1, we’d like to note that the exchange rate of the national currency is one of the most important macro-financial parameters, as it affects other indicators of the country's economic development (GDP, the level of average wages), and reflects the real situation in the country's economy. At the beginning of the hryvnia introduction in Ukraine, the exchange rate was 1.87 UAH for 1 USD. Today, at the end of 2022, it is UAH 36.85 per 1 USD (official market rate - UAH 40.8 per 1 USD). For almost thirty years, the value of the national currency devalued more than twenty times, and this mainly happened during the periods of the difficult economic development of the country.

Let's consider in more detail the essence of the credit services market, peculiarities of its functioning in various conditions of the macroeconomic development of the country. In general, among all the components of the national market of financial services, the credit services market in Ukraine has always been distinguished by the significant rates of development, active involvement of the credit institutions of various types in the processes of granting loans to economic entities. Accordingly, the disruptions in this market functioning negatively affected the stability of the country's financial system and, accordingly, the national economy. A similar situation was observed both in 2008-2009, and in 2014-2015.

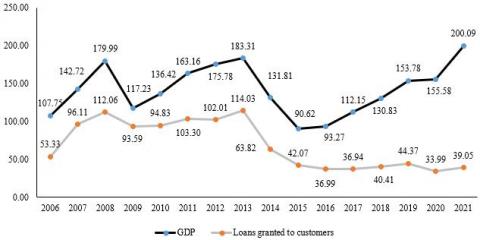

We will conduct a study of trends in the national economy development in Ukraine, and the bank lending volume to economic entities (Figure 2).

The analysis of the bank lending volume in Ukraine without taking into account the activities of other financial companies in the credit services market is due to the fact that such institutions are not sufficiently developed in Ukraine. Until 2008-2009, their number was insignificant, and after 2009, financial companies began to quickly occupy those niches in the financial services market in which banking institutions did not want to work, however, in the overall volume of lending to the population and business entities, the role of financial companies, credit unions, pawnshops and other credit institutions that also provide loans to the economic entities in Ukraine remains insignificant and does not have an important impact on the development of the country's national credit services market.

We’d like to note that, taking into account the data in Figure 2, that at the end of 2021, the banking institutions in Ukraine issued loans for the total amount of 39.05 billion USD. Analyzing the dynamics of this indicator, it can be stated that in the country at the end of 2021, the volume of loans issued by banks to their clients was one of the lowest for the entire period for which the study is being conducted. Undoubtedly, the change in the national currency value in such a case plays an important role, but it is also determined by the presence of significant disparities in the development of the credit services market in Ukraine in general. The analysis of the indicator of the bank loans volumes per person also proves that in reality, after the difficult period of 2014-2015, when a sharp decline in the bank lending volume was observed, in 2020-2021 this decline is even deeper. This testifies not to the decisive impact of the economic situation in the country on the development of the banking system, but to systemic crisis phenomena in the functioning of the credit services market.

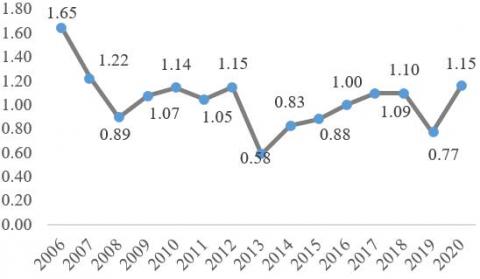

The analysis of the GDP volumes and loans issued by commercial banks to their clients in 2006-2021 shows that, despite the rather cyclical nature of changes in the country's GDP indicator, the volume of bank lending recovered after a sharp decline in 2013 with difficulty and for a long period. Thus, after the bifurcation point in 2013, the credit services market in Ukraine entered a stage of the prolonged recession in its development. At the same time, the trend of the GDP volumes and bank lending changed in different ways. The increase in the volume of such lending, or its decrease, no longer played a key role in the economic development of Ukraine in 2015-2021.

The study of the rates of macroeconomic indicators, namely changes in the exchange rate of the national currency, the level of inflation, and the level of average wages, confirms their cyclical change in Ukraine in 2006-2021. Yes, the cyclicality is not strict, but the periodicity of declines and increases in the values of the outlined parameters is clear. Taking into account the war and its consequences for the economy of Ukraine in 2022 and in the following years, it is quite possible to predict a decline in macroeconomic indicators after their recovery in 2016-2021. Statistical and analytical information confirms that the credit services market in Ukraine will continue to function in the conditions of the financial instability.

The rate of change in the GDP of Ukraine in 2006-2021

Rates of change in average wages in 2006-2021

GDP volume per person in 2006-2021, USD

The rate of change in GDP per person in 2006-2021, USD

Figure 1. Rates of change in the macroeconomic indicators in Ukraine in 2006-2021

Source: Compiled based on the statistical data of the National Bank of Ukraine (https://bank.gov.ua)

The volume of Ukraine's GDP and the volume of loans issued by banking institutions, billion USD

Growth rate of GDP and volume of bank loans

Figure 2. Development of bank lending in the conditions of the macroeconomic dynamics

Source: Compiled based on the statistical data of the National Bank of Ukraine (https://bank.gov.ua)

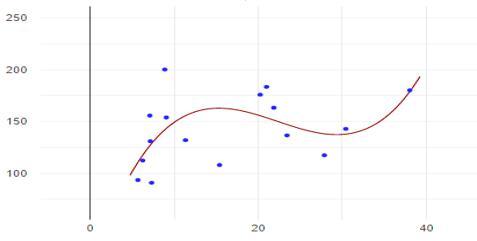

To deepen the understanding of the relationship between the economic development of the country and the functioning of the credit services market, we will model the relationship between the relevant indicators, namely: the level of GDP of Ukraine, the volume of bank lending, the volume of bank lending to business entities, the volume of bank lending to households and relative indicators that reflect the rates of change of the above-mentioned economic and financial parameters. The correlation-regression method was used for modeling, which made it possible to determine the cubic one-factor models that reflect the dependence between two indicators. When modeling, we will take into account the following assumptions: the presented official information on the economic development and development of the credit services market of Ukraine is correct and well prepared; the information was accumulated during 2006-2020. according to a single and identical methodology. The simulation results are presented in Figure 3.

Thus, the analysis of the information obtained during the simulation gives grounds for drawing the following conclusions.

1. The bank lending lending in Ukraine does not determine economic development to a significant extent, that is, Ukraine does not observe the classic model of the prominent role of lending in ensuring the national economy development. The closeness of the relationship between such parameters as the GDP of Ukraine and the volume of loans issued by banking institutions to economic entities is low (R2=0.35). At the same time, the rates of change of both the economic development of the country and bank lending are quite similar and interrelated, which indicates rather that the credit services market during the crisis of 2014-2015 suffered greater losses than the economy of the country in general and at similar rates of recovery, this market returns to the pre-crisis years in an extremely difficult and longer period. However, the very fact that the closeness of the relationship between the outlined indicators is R2=0.76, and nothing more, proves again that with the same trends of changes in the rates of GDP and bank lending, there is a rather significant difference between the growth trends of these indicators.

2. The closeness level of the relationship between the bank lending volume to households and the GDP volume is insignificant (R2=0.28), which indicates the underdevelopment of the bank lending to the population, especially in the field of long-term lending. The low volume of the mortgage lending to citizens in Ukraine shows that this sector is not developed, and the greatest demand among citizens is for short-term loans to meet primary life needs, credit cards, etc. At the same time, the stable and gradual increase in the volume of loans received by households from banking institutions allows us to assert the existence of the demand from citizens for the outlined credit products (R2=0.78).

3. Lending to business entities is insufficient in Ukraine on the part of banking institutions, which complicates both the development of this sector and the provision of active social and economic development of the country. The modeling results indicate that there is no strong relationship between the GDP level and the volume of bank loans of enterprises (R2=0.29).

The analysis of the results of the interaction between the GDP rates and the bank crediting of business entities obtained during modeling shows a low level of such interaction (R2=0.67), which indicates the different rates of change of these indicators and confirms that against the background of the constant GDP growth in Ukraine, the specified volumes of lending are quite difficult to recover, and the rate of such recovery is an order of magnitude lower than the rate of the GDP growth. The outlined situation demonstrates that in Ukraine, the enterprises for their own development use in most cases other sources of financial resources, among which, in the first place, the own funds of business entities are used, large enterprises attract funds in the international capital markets. At the same time, small and medium-sized enterprises remain in the most difficult situation, for which the possibilities of attracting additional investments are extremely insignificant, especially with insufficient amounts of bank lending for their activities.

|

Impact of the bank lending volumes on the GDP of UkraineGDP=0.002Bl3-0.01Bl2-0.89Bl+173.24 R2 = 0.35 |

Impact of the bank lending volumes to households on the GDP of UkraineGDP=0.019Blh3-1.24Blh+24.86Blh+5.58 R2 = 0.28 |

|

|

Impact of the bank lending volume to business entities on the GDP of Ukraine GDP=-0.0003BlEn3+0.077BlEn2-4.41BlEn+202.61 R2 = 0.29 |

Impact of the rates of change in the bank lending volume on the rates of change on the GDP in Ukraine RCGDP=-1.04 RCBL3+2.99RCBL2-1.84RCBL+0.96 R2 = 0.76 |

|

|

Rate of change in bank lending to individuals |

Rate of change in bank lending to business entities |

|

|

Impact of the rates of change in the bank lending volume to households on the rates of change on the GDP in Ukraine RCGDP=0.48RCBlh3-2.33RCBlh2+3.81RCBlh-0.82 R2 = 0.78 |

Impact of the rate of change in the bank lending volume to business entities on the rate of change in the GDP of Ukraine RCGDP=-1.88RCBlЕn3+5.82 RCBlЕn2-4.85RCBlЕn+1.96 R2 = 0.67 |

|

|

Bl - bank lending; GDP - gross domestic product of Ukraine; Blh - bank lending volume to individuals; BlEn - bank lending volume to business entities; RCBL - the rate of change in the bank lending volume; RCGDP - rate of change in GDP; RCBlh - rate of change in the bank lending volume to individuals; RC BlЕn - rate of change in the bank lending volume to business entities |

||

Figure 3. Results of modeling the impact of bank loans on the country's GDP

Source: Compiled on the basis of statistical data of the National Bank of Ukraine (https://bank.gov.ua)

The research carried out within the article provides grounds for asserting that the credit services market is an important component of ensuring the development of the national economy. It is within this market that financial resources are formed, which are important for economic entities. However, in difficult economic conditions, this market is also subject to the destructive influence of various factors that change not only the development trends of this market, but also its role in the development of the country's economy.

In the article, the theoretical and applied provisions of the development of the credit services market in the conditions of the financial instability are described in detail. It was determined that in the periods of sharp and significant economic decline, the credit services market ceases to perform its classical functions, and on the contrary becomes a source of new crisis phenomena within the limits of both the financial system of the country and the national economy in general. These new crisis phenomena quickly spread not only to the credit activity of economic entities, but quickly cover the functioning of the entire banking system of the country. Especially such processes take place in countries where the market of financial services is being formed and is in the initial stages of its own formation.

For a more detailed description of the features of the development of the credit services market in the conditions of financial instability, an analysis of the development of such a market was carried out in Ukraine in 2006-2021 - a country characterized by periodic crisis phenomena in the economy. It was on the example of such an analysis that it became possible to describe the specifics of the impact of the specified market on the country's economy. As a result, it was found that lending does not play a key role in the development of the national economy in Ukraine, which significantly hinders such development, taking into account the underdevelopment of the stock market in the country and the lack of opportunities for business entities to attract the financial resources from other sources. Also, the results of such an analysis prove that the specified market depends on the development of the economic situation in the country, is subject to the rapid impact of crisis phenomena and takes a long time to recover to pre-crisis positions.

Further research in this area may be related to the analysis of specific monetary instruments and their use to ensure the development of the credit services market in conditions of financial instability.

This research is carried out within the framework of the scientific project “Transformation of the households’ behavior in the financial services market in the context of digitalization” with the support of the Ministry of Education and Science of Ukraine.

[1] Novomlynets, O., Marhasova, V., Tkalenko, N., Kholiavko, N., Popelo, O. (2023). Northern outpost: Chernihiv polytechnic national university in the conditions of the Russia-Ukrainian war. Problems and Perspectives in Management, 21: 1-9. http://doi.org/10.21511/ppm.21(2-si).2023.05

[2] Das, M., Ordal, H. (2022). Macroeconomic stability or financial stability: How are capital controls used? Insights from a new database. Journal of Financial Stability, 63: 101067. http://doi.org/10.1016/j.jfs.2022.101067

[3] Desalegn, T.A., Zhu, H., Borojo, D.G. (2023). Economic policy uncertainty, bank competition and financial stability. Journal of Financial Economic Policy, 15(3). http://doi.org/10.1108/JFEP-04-2022-0106

[4] Lyeonov, S., Tiutiunyk, I., Vasekova, M., Dziubenko, O., Samchyk, M. (2022). Tax, investment, institutional and social channels of economic shadowing: Challenges for the macro-financial stability and good governance. Public and Municipal Finance, 11(1): 128-141. http://doi.org/10.21511/pmf.11(1).2022.11

[5] Mishra, A., Dubey, A. (2022). Inflation targeting and its spillover effects on the financial stability in emerging market economies. Journal of Policy Modeling, 44(6): 1198-1218. https://doi.org/10.1016/j.jpolmod.2022.10.003

[6] Shkolnyk, I., Kozmenko, S., Kozmenko, O., Orlov, V., Shukairi, F. (2021). Modeling of the financial system’s stability on the example of Ukraine. Equilibrium. Quarterly Journal of Economics and Economic Policy, 16(2): 377-411. https://doi.org/10.24136/eq.2021.014

[7] Giesecke, K., Weber, S. (2004). Cyclical correlations, credit contagion, and portfolio losses. Journal of Banking & Finance, 28(12): 3009-3036. https://doi.org/10.1016/j.jbankfin.2003.11.002

[8] Gao, Q., Fan, H. (2020). Effect of the dynamic macroeconomic fluctuation on the stability of a banking network system with scale-free structure. Mathematical Problems in Engineering, 2020: 7158506. https://doi.org/10.1155/2020/7158506

[9] Nikiforov, P., Greshko, R., Marych, M., Marusiak, N., Kharabara, V., Gladchuk, O. (2022). Mutual influence of fiscal and monetary policy in the context of ensuring macro-financial stability of the state. Management Theory and Studies for Rural Business and Infrastructure Development, 44(4): 435-442. https://doi.org/10.15544/mts.2022.43

[10] Bogolib, T. (2015). Fiscal policy as an instrument of the macroeconomic stability. Economic Annals-XXI, 3-4(1): 84-87.

[11] Johnson Worlanyo Ahiadorme. (2022). Monetary policy in search of the macroeconomic stability and inclusive growth. Research in Economics, 76(4): 308-324. https://doi.org/10.1016/j.rie.2022.08.002

[12] Radionova, I. (2016). Procedural approach to the macroeconomic policy analysis: Content and application. Economic Annals-XXI, 156(1-2): 8-21. https://doi.org/10.21003/ea.V156-0004

[13] Carli, F., Modesto, L. (2022). Sovereign debt, fiscal policy, and macroeconomic instability. Journal of Public Economic Theory, 24(6): 1386-1412. https://doi.org/10.1111/jpet.12578

[14] Khan, M. (2019). Does macroeconomic instability cause environmental pollution? The case of Pakistan economy. Environmental Science and Pollution Research, 26: 14649-14659. https://doi.org/10.1007/s11356-019-04804-z

[15] Radionova, I. (2015). Macroeconomic policy features analysis under macroeconomic instability. Economic Annals-XXI, 1-2(1): 11-14. http://ea21journal.world/index.php/ea-v147-03/

[16] Tkachuk, I., Hladchuk, O., Vinnychuk, O. (2022). Impact of changes in macroeconomic indicators on banking indicators in Ukraine. Management Theory and Studies for Rural Business and Infrastructure Development, 44(4): 461-481. https://doi.org/10.15544/mts.2022.46

[17] Danylyshyn, B., Dubyna, M., Zabashtanskyi, M., Ostrovska, N., Blishchuk, K., Kozak, I. (2021). Innovative instruments of monetary and fiscal policy. Universal Journal of Accounting and Finance, 9(6): 1213-1221. http://doi.org/10.13189/ujaf.2021.090601

[18] Kozmenko, S., Shkolnyk, I., Kozmenko, O., Orlov, V., Shukairi, F. (2021). Modeling of the financial system’s stability on the example of Ukraine. Equilibrium. Quarterly Journal of Economics and Economic Policy, 16(2): 377-411. https://www.ceeol.com/search/article-detail?id=975692.

[19] Piatnytskyi, D. (2014). Assessment of financial stability: Indicators and composite indices in Ukrainian and international practice. Economic Annals-XXI, 3-4(2): 51-54. http://ea21journal.world/index.php/ea-v140-13/.

[20] Zając, A., Balina, R., Kowalski, D. (2023). Financial and economic stability of energy sector enterprises as a condition for poland’s energy security-legal and economic aspects. Energies, 16: 1442. https://doi.org/10.3390/en16031442

[21] Elsayed, A.H., Naifar, N., Nasreen, S. (2023). Financial stability and monetary policy reaction: Evidence from the GCC countries. The Quarterly Review of Economics and Finance, 87: 396-405. https://doi.org/10.1016/j.qref.2022.03.003

[22] Makarenko, M., Ponomarenko, O. (2014). Ukraine’s balance of payments financial account as an indicator of economic stability. Економічний часопис - ХХІ, 7-8(2): 40-43. https://www.ceeol.com/search/article-detail?id=273100.

[23] Mabkhot, H., Al-Wesabi, H.A.H. (2022). Banks’ financial stability and macroeconomic key factors in gcc countries. Sustainability, 14: 15999. https://doi.org/10.3390/su142315999

[24] Subbar, H.H., Guirinsky, A.V. (2020). Technical ways to developed the financial stability of the banking system in Iraq. International Journal of Advanced Science and Technology, 29(1): 7-10. http://sersc.org/journals/index.php/IJAST/article/view/2973.

[25] Mussina, A., Albekova, S. (2018). Development of the methodology for the comprehensive assessment of banking services quality. Banks and Bank Systems, 13(1): 37-48. https://www.ceeol.com/search/article-detail?id=695366

[26] Boiarynova, K., Popelo, O., Tulchynska, S., Gritsenko, S., Prikhno, I. (2022). Conceptual foundations of the evaluation and forecasting of the innovative development of regions. Periodica Polytechnica Social and Management Sciences, 30(2): 167-174. https://doi.org/10.3311/PPso.18530

[27] Marhasova, V., Tulchynska, S., Popelo, O., Garafonova, O., Yaroshenko, I., Semykhulyna, I. (2022). Modeling the harmony of economic development of regions in the context of sustainable development. International Journal of Sustainable Development and Planning, 17(2): 441-448. https://doi.org/10.18280/ijsdp.170209

[28] Burlutskiy, S., Burlutska, S., Marhasova, V., Sakun, O. (2019). The relationship between short-term fluctuations and stages of economic cycle: The case of Ukraine. Revista Espacios, 40(10): 1-8. https://dspace.nuft.edu.ua/jspui/handle/123456789/32038.

[29] Shkarlet, S., Dubyna, M., Vovk, V., Noga, M. (2019). Financial service markets of the Eastern Europe: A compositional model. Economic Annals-XXI, 176(3-4): 26-37. https://doi.org/10.21003/ea.V176-03

[30] Tkachuk, I. (2017). Asset operations of Ukrainian banks on the current stage of banking system development. Banks and Bank Systems, 12(1-1): 119-127. http://dx.doi.org/10.21511/bbs.12(1-1).2017.04

[31] Tkachuk, І., Kobelia, М., Popelo, О., Zhavoronok, А., Vinnychuk, О. (2023). Modelling financial influence of political and oligarchic interests of the governed-sponsored enterprises on the creation and implementation of the financial policy in the state. Journal of Hygienic Engineering and Design, 42: 271-279.

[32] Ostrovska, N., Hrapko, N. (2014). Condition and dynamics of lending analysis in Ukraine (2011-2013). Economic Annals-XXI, 9: 15-18.

[33] Vovk, V., Denysova, A., Rudoi, K., Kyrychenko, T. (2021). Management and legal aspects of the symbiosis of banking institutions and fintech companies in the credit services market in the context of digitization. Estudios de Economía Aplicada, 39(7): https://doi.org/10.25115/eea.v39i7.5013

[34] Dubyna, M., Popelo, O., Kholiavko, N., Zhavoronok, A., Fedyshyn, M., Yakushko, I. (2022). Mapping the literature on financial behavior: A bibliometric analysis using the VOSviewer program. WSEAS Transactions on Business and Economics, 19: 231-246. https://wseas.com/journals/bae/2022/a425107-008(2022).pdf.

[35] Dubyna, M., Zhavoronok, A., Kudlaieva, N., Lopashchuk, I. (2021). Transformation of the household credit behavior in the conditions of digitalization of the financial services market. Journal of Optimization in Industrial Engineering, 14(1): 97-102. http://dx.doi.org/10.22094/JOIE.2020.677835

[36] Popelo, O., Dubyna, M., Zhavoronok, A., Lopashchuk, I., Fedyshyn, M. (2023). Development of the credit market of Ukraine under macroeconomic instability. Public and Municipal Finance, 12(1): 33-47. http://dx.doi.org/10.21511/pmf.12(1).2023.04

[37] Unynets-Khodakivska, V., Dubyna, M., Panchenko, O., Bazilinska, O., Matskiv, V., Lobko, O. (2022). Features of the formation and transformation of the household credit behavior under macroeconomic instability. International Journal of Sustainable Development and Planning, 17(7): 2075-2087. https://doi.org/10.18280/ijsdp.170708

[38] Andriushchenko, K., Ishchenko, M., Sahaidak, M., Tepliuk, M., Domina, O. (2019). Prerequisites for the creation of the financial and credit infrastructure of the support for agricultural enterprises in Ukraine. Banks and Bank Systems, 14(2): 63-75. http://dx.doi.org/10.21511/bbs.14(2).2019.06

[39] Akin, G.G., Aysan, A.F., Borici, D., Yildiran, L. (2013). Regulate one service, tame the entire market: Credit cards in Turkey. Journal of Banking & Finance, 37(4): 1195-1204. https://doi.org/10.1016/j.jbankfin.2012.11.016

[40] Mints, O., Marhasova, V., Hlukha, H., Kurok, R., Kolodizieva, T. (2019). Analysis of the stability factors of Ukrainian banks during the 2014 -2017 systemic crisis using the Kohonen self-organizing neural networks. Banks and Bank Systems, 14(3): 86-98. https://doi.org/10.21511/bbs.14(3).2019.08

[41] Volosovich, S., Krivosheeva, V. (2016). Self-regulation of the credit services market for individuals. Economic Annals-XXI, 158(3-4(2)): 79-82. http://doi.org/10.21003/ea.V158-18

[42] Hryhorkiv, V., Buiak, L., Verstiak, A., Hryhorkiv, M., Verstiak, O., Berdnuk, A. (2019). Mining credit interest rate data from multiple data sources. In Proceedings of the 9th International Conference on Advanced Computer Information Technologies, pp. 265-268. http://dx.doi.org/10.1109/ACITT.2019.8780034

[43] Zhavoronok, A., Popelo, O., Shchur, R., Ostrovska, N., Kordzaia, N. (2022). The role of digital technologies in the transformation of regional models of households’ financial behavior in the conditions of the national innovative economy development. Ingénierie des Systèmes d’Information, 27(4): 613-620. https://doi.org/10.18280/isi.270411

[44] Tori, C.R., Tori, S.L. (2001). Exchange market pressure, trade, sovereign credit ratings, and U.S. exports in banking services. Atlantic Economic Journal, 29: 48 -62. http://doi.org/10.1007/BF02299931

[45] Chmutova, I., Vovk, V., Bezrodna, O. (2017). Analytical tools to implement integrated bank financial management technologies. Economic Annals-XXI, 163(1-2(1)): 95-99. http://doi.org/10.21003/ea.V163-20

[46] Du, D. (2017). U.S. credit-market sentiment and global business cycles. Economics Letters, 157: 75-78. https://doi.org/10.1016/j.econlet.2017.05.039

[47] Navarro, C.E.B., Tomé, R.M.B. (2022). Structural stability analysis in a dynamic IS-LM-AS macroeconomic model with inflation expectations. International Journal of Differential Equations, Hindawi, 2022: 1-21. https://doi.org/10.1155/2022/5026061