Muhamad Takhim*![]() | Adang Sonjaya

| Adang Sonjaya![]() | Zamroni Salim

| Zamroni Salim![]() | Abdul Rahman

| Abdul Rahman![]() | Edwin Basmar

| Edwin Basmar![]() | Ragimun Abdullah

| Ragimun Abdullah![]() | Mudzakkir Ali

| Mudzakkir Ali![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Muslim-friendly tourism is one of the most influential halal industries, as its services encompass elements of Islamic banks, halal food, fashion, media, recreation, as well as pharmaceuticals and halal cosmetics. Therefore, this study aims to build synergy and create new patterns of developing Islamic banks and Muslim-friendly tourism through partnership networks and joint work programs in various fields to grow other halal industries in Indonesia. This study used a qualitative approach with the field research method. The research focused on two regions: Central Java and the Special Region of Yogyakarta Provinces in Indonesia. Data collection was carried out through observation, interviews, and various sources, such as journals, books, websites, and others relevant to this research. Respondents were selected through purposive sampling, i.e., the leadership of the Tourism Awareness Community Group (Pokdarwis). The study results revealed that synergy and development patterns between Islamic banks and Muslim-friendly tourism should be carried out simultaneously. Six aspects to consider in building and developing the synergy include establishing partnership cooperation, optimizing the role of Islamic bank stakeholders and Muslim-friendly tourism, improving ACES (access, communication, environmental, and service infrastructure), intensifying education and literacy of the halal industry, innovating and transforming technology, and conducting clusters for the halal industry development.

Islamic banks, Muslim-friendly tourism, simultaneous-holistic synergy

Today's halal industry development exhibits very rapid improvement [1]. This is indicated by the contribution of foreign exchange income in various countries that has reached billions of US dollars in total sales, contributing significantly to the countries' economic income [2].

The National Sharia Finance Committee [3] reported that the total Global Islamic Finance Market was US \$2.438 trillion, and in 2023, it is projected to continue to increase to US \$3.809 trillion (up 56%). Meanwhile, in the Global Islamic Commercial Banking Market sector, US \$1.721 trillion was recorded in 2017 and is estimated to reach US \$2.441 trillion in 2023 (up 41.8%). Table 1 indicates the Global Islamic Economy [4] has also reported that consumption of halal industry products has totaled US $4.903 trillion.

The Global Islamic Economy (GIE) indicator [5] in Table 2 measures the strength of the Islamic economy in 73 countries, revealing that Indonesia ranked fourth. This ranking has improved from previous years, 2018 (10th rank) and 2019 (5th rank). Six main industrial sectors are used in their measurements: Islamic finance, halal food, Muslim-friendly tourism, fashion, media and recreation, and pharmacy and cosmetics [6]. One of the six main industrial sectors is Muslim-friendly tourism, one of the most influential halal industries among the other halal industry sectors. Muslim-friendly tourism also forms the core of the halal industry [7, 8], as its existence is recognized when services incorporate elements of Islamic banks, halal food, fashion, media and recreation, as well as pharmacy and cosmetics [8].

Table 1. Total shopping for halal products worldwide

|

Halal Industry Sector |

Value (US $, Trillion, and Billion) |

Portion (%) |

|

Islamic Finance |

2.88 T |

58.74 |

|

Halal Foods |

1.17 T |

23.86 |

|

Halal Travel |

194 B |

3.96 |

|

Halal Fashion |

277 B |

5.65 |

|

Halal Media and Tourism |

222 B |

4.53 |

|

Halal Pharmacy |

94 B |

1.92 |

|

Halal Cosmetics |

66 B |

1.34 |

|

Total |

4.903 T |

100 |

Table 2. Top 10 indicators of global Islamic economy (GIE)

|

No. |

Country |

GIE |

Halal Food |

Islamic Finance |

Muslim-Friendly Travel |

Fashion |

Pharmacy and Cosmetics |

Media and Recreation |

|

1 |

Malaysia |

290.2 |

209.8 |

389.0 |

98.3 |

43.7 |

80.2 |

59.9 |

|

2 |

Saudi Arabia |

155.1 |

51.1 |

234.2 |

36.8 |

22.1 |

33.4 |

34.7 |

|

3 |

UAE |

133.0 |

104.4 |

142.5 |

78.3 |

235.6 |

72.1 |

125.3 |

|

4 |

Indonesia |

91.2 |

71.5 |

111.6 |

45.3 |

57.9 |

47.5 |

43.6 |

|

5 |

Jordan |

88.1 |

39.6 |

124.6 |

43.3 |

18.5 |

39.1 |

31.6 |

|

6 |

Bahrain |

86.9 |

42.2 |

121.9 |

31.9 |

16.7 |

33.5 |

42.3 |

|

7 |

Kuwait |

73.3 |

42.2 |

99.2 |

27.1 |

17.5 |

33.3 |

40.8 |

|

8 |

Pakistan |

70.9 |

54.7 |

91.1 |

23.6 |

30.6 |

32.5 |

12.9 |

|

9 |

Iran |

64.0 |

60.5 |

74.0 |

28.8 |

33.5 |

55.9 |

26.6 |

|

10 |

Qatar |

63.1 |

44.3 |

80.1 |

36.7 |

20.3 |

32.1 |

40.2 |

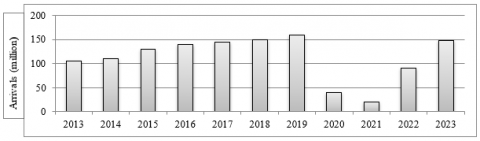

Figure 1. Projection of Muslim-friendly tourism market growth

Muslim-friendly tourism is a new development concept from the tourism industry that integrates religious and conservative motivations, making it a preferred choice of tourist destinations [2, 9]. This concept prioritizes hospitable service [10], comfort during the journey [11], adherence to sharia [12], and highlights its discrepancy with the current tourism practices that dominate the modern tourism industry [13]. Other terms used for Muslim-friendly tourism include halal tourism, Islamic tourism, halal-friendly tourist destinations, Muslim-friendly tourism destinations, and halal lifestyles [14]. The paradigm and terminology of Muslim-friendly tourism do not exclude Muslim tourists from conventional tourism activities, nor do they exclude non-Muslim tourists from specific tourist destinations. The development of Muslim-friendly tourism also aims to provide greater convenience for Muslim tourists to carry out their religious obligations when traveling [15, 16]. For non-Muslims, Muslim-friendly tourism is expected to provide safe, comfortable, and healthy travel services while introducing Islamic teachings as universal values [17, 18].

Moreover, the number of international Muslim tourists in Figure 1 grew from around 108 million in 2013 to 160 million in 2019 [19]. In 2020, the arrival of Muslims fell to 42 million due to the global impact of the pandemic, which seriously affected the travel sector. More than 90% of travel was done in the first quarter of 2020 before most destinations closed their borders. The international borders opened gradually at the end of 2021, where it was estimated that the arrival of Muslim visitors reached 26 million that year, and it is projected that the Muslim travel market will recover up to 80% in 2023 [20].

In this context, Indonesia has great potential and opportunity to develop Muslim-friendly tourism [21, 22]. Most of the population is Muslim, with 87.2% of 268 million, contributing to 13% of the world's Muslim population [23]. The bonus of natural beauty and culture is a unique attraction for domestic and foreign tourists for traveling and tourism in Indonesia [24-26]. In 2019, around 20% of the 14.92 million tourists who came to Indonesia were foreign tourists. According to the Global Muslim Travel Index (GMTI) report [19], the quality of Indonesian Muslim-friendly tourism in terms of access, communication, environment, and services ranked first among 130 Muslim-friendly tourist destinations, sharing first place with Malaysia (with a tied score of 78). In 2021, Indonesia also ranked fourth on the list of the world's 20 best Muslim-friendly tourism destinations, with a score of 73 [20].

Table 3 indicates that Indonesian Muslim-friendly tourism has decreased from first to fourth, while Malaysia remains in first place. On the other hand, the results of the merger of three Islamic banks (Bank Syariah Mandiri, Bank Negara Indonesia Syariah, and Bank Rakyat Indonesia Syariah) on February 1, 2021 [27] until now are relatively not optimal; the penetration of Islamic banks and public awareness in using Islamic bank products also remains low [28]. Islamic bank market share compared to conventional banks is 6.52%, with a composition of 64.8% owned by Sharia Commercial Banks (BUS), 32.74% by Sharia Unit Business (UUS), and 2.46% by Islamic People's Credit Banks (BPRS). This composition can be seen in Table 4.

At the financing post in Table 3 of 413.31 trillion, the composition of the working capital field was 29.37%, investment was 21.91%, and consumption was 50.71%. The placement of some of these sectors can be seen in Table 5.

Table 5 reveals that the placement of financing the Islamic bank of the halal industry was not included in the top five, even though the halal industry has a vast potential to develop [29]. Also, it can be used to support increasing the penetration of Islamic banks, inclusion and public awareness, and market share.

Various studies related to Islamic banks, halal industries, and Muslim-friendly tourism have actually been carried out in several countries, such as in Malaysia by Ab Talib et al. [30] that Islamic banks can try to encourage the manufacturing sector or the processed industry sector, which is an element of strengthening the industrial sector and halal certification. A study of Muhamed et al. [31] focused on document analysis of material related to the halal certification process and procedures. Wajdi Dusuki [32]’s research also stated that financial institutions should not only focus on maximizing profits but also contribute to overcoming socioeconomic problems by channeling financial resources efficiently and productively, thereby increasing production, investment, and trade activities. In addition, Ismail and Mohd Noor [33] emphasized Islamic finance and halal food. In Spain [29], it is stated that Islamic banks can strategically encourage working together to develop Muslim-friendly tourism products. A study in Bangladesh [34] asserted that in building a halal ecosystem, cooperation between the regulatory agency (government and bank) is needed, and the risk management and electronic trade activities (companies and banks) can promote the development of halal ecosystems together.

Table 3. The top 10 destinations of world Muslim tourists

|

2019 |

2021 |

||||

|

Ranking |

Destination |

Value |

Ranking |

Destination |

Value |

|

1 |

Malaysia |

78 |

1 |

Malaysia |

80 |

|

1 |

Indonesia |

78 |

2 |

Turkey |

77 |

|

3 |

Turkey |

75 |

3 |

Saudi Arabia |

76 |

|

4 |

Saudi Arabia |

72 |

4 |

Indonesia |

73 |

|

5 |

United Arab Emirates |

71 |

5 |

United Arab Emirates |

72 |

|

6 |

Qatar |

68 |

6 |

Iran |

68 |

|

7 |

Morocco |

67 |

7 |

Kuwait |

66 |

|

8 |

Bahrain |

66 |

6 |

Egypt |

66 |

|

8 |

Oman |

66 |

7 |

Kazakhstan |

58 |

|

10 |

Brunei |

65 |

8 |

Uzbekistan |

65 |

Table 4. Islamic bank performance as of September 2021 (trillion)

|

Islamic Banking Industry |

Number of Institutions |

Number of Offices |

Asset |

Financing |

Liability |

|

BUS |

12 |

2.028 |

418.77 |

256.87 |

341.33 |

|

UUS |

21 |

409 |

211.57 |

145.10 |

151.79 |

|

BPRS |

165 |

670 |

15.87 |

11.34 |

10.71 |

|

Total |

198 |

3.107 |

646.21 |

413.31 |

503.83 |

Table 5. Five of the most significant business sectors for financing placement

|

No |

Sector |

Percentage |

|

1 |

Household |

48.10% |

|

2 |

Big and retail trade |

10.91% |

|

3 |

Construction |

9.24% |

|

4 |

Processing industry |

6.61% |

|

5 |

Agriculture, hunting, and forestry |

3.98% |

On the other hand, several studies have also been conducted in Indonesia, but no one has examined them specifically. Like Muhamed and Ramli [35]’s research, integrating the halal industry with the Islamic financial industry can bring customer trust and confidence in halal products and services and improve the halal business of the Islamic industry and finance. Research by Hassan et al. [36] stated that the relationship between the halal industrial ecosystem had not been maximized, and there is the potential to create awareness among various stakeholders. In Sidharta [37]’s study, it is stated that Islamic banks had not conducted effective socialization with tourist industry players, office access and ATM networks were still difficult to find, and lack of promotions carried out by Islamic banking. A study by Tieman [38] also asserted that Indonesia has great potential to develop a strong foundation for the global halal industry, supported by the most significant number of Muslims at the global level. In addition, Trimulato [39] added that Muslim friendly- tourism has great potential, and the role of Islamic banking is to develop this potential, both morally and materially, supported by the central and regional governments and other stakeholders. In the results of another study of Mubarok and Imam [40], a strategy to optimize the halal industry in Indonesia is to strengthen various sectors and increase the synergy of all elements. The research findings by Mubarok and Imam [40] also revealed that the development of the halal industry in Indonesia includes several sectors: the food and beverage sector, tourism, fashion, media and recreation, pharmacy and cosmetics, and Islamic finance and found strengths, weaknesses, opportunities, and challenges in the development of the halal industry. Moreover, Yudha and Pauzi [41]’s research results uncovered that Indonesia has great potential and market in the halal industry to become a global halal central leader, but the potential and market share have not been optimized independently.

Based on this phenomenon, halal industry development is needed by collaborating, one of which is Islamic banks and Muslim-friendly tourism that synergizes to collaborate in a partnership to progress and develop together, develop and strengthen one another. This research also provides scientific contributions to reference information for other researchers to provide references to the appropriate approach method. Practically, this research is beneficial to help overcome problems, improve performance, solve issues, and make decisions for leaders, policymakers, and other stakeholders in the halal industrial ecosystem forum to realize Indonesia as a Global Halal Epicenter.

This study used a qualitative approach with the field research method. The research object took two regions: Central Java and the Special Region of Yogyakarta Provinces, with several considerations. First, the two provinces are one of the ten provincial Muslim-friendly tourism destinations in Indonesia selected and fostered under technical guidance using the Global Muslim Travel Index [42]. Second, Central Java won the 2019 Award from Indonesia Muslim Travel Index (IMTI) [42]. Third, Yogyakarta is a special province as the City of Culture ASEAN [43]. In addition, data collection was carried out through three stages: observation, interviews, and triangulation. The observation was made to get an initial overview of the substance of the problem in this study. Then, interviews were conducted with leaders and stakeholders of Islamic banks and Muslim-friendly tourism, consisting of the Head of Bank Syariah Indonesia or Bank Syariah Indonesia (BSI), the Head of the Tourism Office, and the Chair of the Tourism Awareness Community Group (Pokdarwis) as a primary data source. Meanwhile, secondary data were obtained from journals, books, newspapers, websites, and other documents, which were relevant to this research. Meanwhile, triangulation was performed after two stages completed. Triangulation was done to obtain valid and objective data, having 'slices and links' to one another.

3.1 Bank Syariah Indonesia (BSI) and its carrying capacity

Bank Syariah Indonesia (BSI) is one of the halal industrial ecosystems. Referring to the 2019-2024 Islamic Sharia Economy Plan, one primary strategy is strengthening the halal value chain. BSI, with 19,449 employees and 1,244 sub-branch office networks spread evenly throughout Indonesia, has excellent potential to develop and strengthen the halal industry in Indonesia. Table 6 and Figure 2 indicate the total assets in 2021 that reached IDR 265 trillion with total financing of IDR 162 trillion have occupied a market share of 38.24% of Islamic banking in Indonesia [44]. This infrastructure is also one of the forces owned by Islamic banks to contribute actively to the banking industry and the national economy.

The financing scheme segment offered by BSI is four: the wholesale business segment, small and medium enterprise (SME), consumer, and micro [27]. The wholesale business segment provides financing services to government-owned enterprises, both public and regional, state institutions, banks and non-bank financial institutions, multinational companies, regional government, syndicated financing, hospitals, universities, and securities. The SME segment serves financing to private business entities, educational institutions other than higher education and clinics, cooperatives, BMT linkage patterns, and/or plasma core. Next, the consumer business segment is offered to the community with a consumptive/multipurpose purpose for ownership of homes, vehicles, gold installments, and other gold and multipurpose, including financing government programs. Meanwhile, the micro business segment is for individual customers and micro-entrepreneurs, including the distribution of subsidized financing for the community to support government programs. The performance of the financing scheme of each business segment is explained in Table 7.

Of the four segments, the scheme covering the halal industry was the SME and micro business segments. However, the implementation of financing was uneven to the five halal industries, limited to Islamic financial institutions, such as cooperatives and Baitul Mal Wat Tamwil (BMT), halal food, and halal fashion. Meanwhile, Muslim-friendly tourism, pharmacy and media, and recreation had not been fully touched. Likewise, the realization of financing channeled is still far below the two other segments (wholesale and consumer businesses), where in 2021, it reached 49.4 trillion and 82.7 trillion, while SME and micro businesses were 18.3 and 16.3 trillion. Moreover, identification, collaboration, cooperation, and an increase in financing ceilings with other halal industries need more intensive recognition and attention.

Figure 2. The market share of the Islamic banking industry as of December 2021

Table 6. Indonesia Islamic bank financing structure in 2021 (million)

|

Description |

2020 |

2021 |

|

Murabahah receivables |

89,844,090 |

101,685,560 |

|

Istishna receivables |

637 |

359 |

|

Receivables to Lease Ijarah |

39,167 |

101,570 |

|

Reserve loss of impairment and allowance for accounts receivable losses |

(3,294,706) |

(3,450,506) |

|

Qardh loan-Neto |

9,054,373 |

9,081,400 |

|

Mudharabah financing-Neto |

2,598,787 |

1,592,314 |

|

Musyarakah financing-Neto |

50,896,175 |

53,903,123 |

|

Total |

149,138,523 |

162,913,820 |

3.2 Muslim-friendly tourism in Central Java and special region of Yogyakarta Provinces

The development of Muslim-friendly tourism in these two provinces refers to Central Java Governor Regulation Number 6 of 2015 and the Special Region of Yogyakarta Regulation Number 1 of 2019 concerning Amendments to the Regional Regulation of the Special Region of Yogyakarta Number 1 of 2012 concerning the Master of Tourism Development Region of the Special Region of Yogyakarta 2012-2025.

The regulation explicitly has not fully regulated Muslim-friendly tourism. However, the existing tourist destinations in broad outlines have carried out the development and governance, referring to the IMTI and GMTI criteria in terms of access, communication, environment, and tourism services (ACES) [45, 46].

Table 7. Indonesian Islamic bank business segmentation (trillion)

|

Financing Business Segment |

2020 |

2021 |

Fluctuations (%) |

Explanation |

|

Wholesale |

48.0 |

49.4 |

Up 2.70% |

Government-Owned Enterprises |

|

SME |

25.1 |

18.3 |

Down 27.02% |

Private-Owned Enterprises, Sharia Cooperatives |

|

Consumer |

65.0 |

82.7 |

Up 27.30% |

Consumption/multipurpose |

|

Micro business |

14.4 |

16.3 |

Up 13.64% |

Halal Ecosystems (Islamic Boarding Schools, Mosque, and Halal Communities) |

Table 8. Service criteria (score <3)

|

Criteria |

Sub-Criteria |

Indicator |

Central Java |

Yogyakarta |

|

Communication |

Muslim Visitor Guide |

Availability of guidance for Muslim tourists |

2 |

3 |

|

Stakeholder Education |

Holding a workshop or training and seminar on Muslim-friendly tourism for stakeholders |

3 |

3 |

|

|

Environment |

Commitment to Muslim- friendly Tourism |

Commitment to running and developing Muslim-friendly tourism |

3 |

3 |

|

Service |

Mosque |

Availability of worship places |

3 |

3 |

|

|

Attraction |

Availability of Islamic heritage sites/Islam-related attractions and cultural & local attracts |

3 |

- |

The criteria guidelines measure the existence and completeness of Muslim-friendly tourist destinations by giving a score of 1-5. The greater the score obtained, the greater the availability of the completeness of Muslim-friendly tourism facilities. ACES criteria are described in sub-criteria and indicators that can be explained as follows: (1) Access is the ease of access to tourist destinations with air, sea, and land transportation modes. Air access is the availability of airlines, both domestic and international. Sea access is the availability of sea travel route services. Meanwhile, land access is the availability of train and other transport services in the city and between cities/provinces, and adequate infrastructure, including road quality, CCTV, street lighting, directions, and other supporters; (2) Communication assesses and considers Muslim-friendly tourism facilities with five sub-criteria, including Muslim visitor guides, stakeholder education, marketing media, tourism guides, and digital marketing; (3) Environmental criteria focus on evaluating the arrival of the number of domestic and foreign tourists, the availability of Wi-Fi/internet networks, and regulations. In this case, the quantity of extensive Muslim visits will signal and be attractive to other Muslims about the convenience of a destination tourist destination. Wi-Fi/strong internal network availability is in several places, pages, and tour stories in various forms of website platforms, applications, and others. Government regulations prove the government's seriousness and commitment to implementing Muslim-friendly tourism; (4) Services include several facilities that support Muslim tourists to continue to meet their religious needs, including halal restaurants, representative mosques/mushola, international airports, hotels with water-friendly facilities, and attractions/tourist attractions in nature, culture, and artificial, equipped with basic Muslim tourism needs. Comfort guarantees and halal in each section are evidenced by a halal certificate from the authority as a value-added in attracting Muslim tourists.

The implementation of the Muslim-friendly tourism of Central Java and the Special Region of Yogyakarta Provinces from each ACES criteria had a mean, reaching scores of 4 and 5. Nevertheless, some criteria still obtained scores of 2 and 3, i.e., communication criteria for indicators of availability of guidance for Muslim tourists and organizing workshops, training, and seminars, criteria for the environment in government commitment, and service criteria for availability of worship and availability of Islamic heritage site (attraction). It can be seen in Table 8.

Table 8 demonstrates that there was still a score below 4. In this case, Muslim-friendly tourism stakeholders are expected to improve services in the future.

3.3 The synergy of Islamic banks and Muslim-friendly tourism

Islamic banks are one of the Islamic finance sectors with a strategic role in the halal industry development in Indonesia. Naturally, Islamic banks play an active role in becoming supporters and drivers in strengthening Muslim-friendly and other halal tourism. The development of Muslim-friendly tourism is also one of the efforts to generate the value of benefits that contribute to state income and improve community welfare [47, 48].

The currently in Figure 3 applied pattern of Islamic bank cooperation and the halal industry is in the partial form of financing, where only a few halal industries, such as halal food and fashion, have not yet been covered in other halal industries; there is no sustainable joint commitment yet. Alternatively, suppose only Islamic banks collaborate with two other halal industries (halal pharmaceuticals and media). In that case, it also will not provide multiple positive impacts on the development of other halal industries since the four halal industries are characteristic (one by one).

Figure 3. Partial synergy

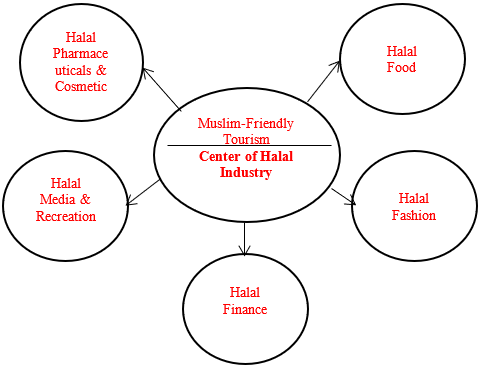

New forms and patterns of halal industry development can be started from the development of Muslim-friendly tourism. Islamic banks conduct cooperation and work together with Muslim-friendly tourism. Figure 4 gives point that muslim-friendly tourism is also a significant component of the halal industry. Why is it? First, Muslim-friendly tourism involves and mobilizes human transfer from one place to another, so it requires excellent service to synergize with other government and private institutions/organizations. The second is to foster motivation that positively impacts the emergence of other halal industries as in Figure 5. If a country develops Muslim-friendly tourism, it will automatically also develop five other halal industries. Logically, if Muslim tourists when visiting a place to eat, they need halal food. When going to make financial transactions, they will look for Islamic banks. When they intend to shop for fashion, they will look for halal fashion for themselves and souvenirs. When tired, not feeling well, or even wanting to dress up and decorate, they look for halal medicine and cosmetics. They need halal media and recreation for news, films, entertainment, and others.

Figure 4. Six halal industrial ecosystems

Islamic banks and Muslim-friendly tourism initiated cooperation, collaboration, and working together to build links and matches that strengthen each other, mutually beneficial, and mutual support among stakeholders in a halal industry partnership.

Figure 5. Simultaneous-holistic synergy

Islamic banks and Muslim-friendly tourism in Figure 6 realize the simultaneous-holistic synergy, among others, first by building a partnership cooperation connection in a forum and a halal industry. This connectivity will open the space for Islamic banks and Muslim-friendly tourism. The development of ample sharia space in the economy is not enough to rely on the market (commercial sector) but also on an integrated ecosystem and connect to the social sector so that it can achieve broader penetration, both local and global. Second, optimizing the role of Islamic bank stakeholders and Muslim-friendly tourism in accordance with statements [49-54] that five parties involved: academicians, business, community, government, and media (ABCGM), called Penta helix.

Academics are a source of knowledge that plays a role in conducting research for developing prototype Islamic bank services and Muslim-friendly tourism that is relevant to the development of science and technology. Businesses, both individuals and business entities, play a role as people who carry out and maintain value-added and build networks with other businesses. The community has a role as an accelerator promoting and creating social civilization and change, creating good and impressive images and services. The government acts as a policy maker, regulation, coordinator, and supervisor of the halal industry ecosystem. Meanwhile, the media plays an essential role in building a brand image of social change being built in the community so that access to information is easily obtained and on target. Ease of access to information will invite and add new collaborators to create social changes that impact the community jointly. Here, the role of Islamic banks can facilitate in identifying Muslim-friendly tourism stakeholders.

Third, improvement of ACES (access, communication, environment, and services) infrastructure. ACES, as explained above, is an indicator used to measure and assess the availability of Muslim-friendly tourism. The more complete the availability of ACES criteria, Muslim-friendly tourist destinations will be more representative. In this case, Islamic banks play a role in providing injections of financial services and financing in providing these ACES criteria. The fourth is the intensity of the education and literacy of the halal industry. The collaboration of the implementation of this program is carried out by holding a variety of work programs together periodically in Halal fest, such as seminars, workshops, bazaars, exhibitions, scholarships, and others. The fifth is innovation and technology transformation. Here, Islamic banks and Muslim-friendly tourism also need constantly innovating service providers in accordance with the times. Digital innovation will change existing business activities. Also, the expansion of marketing and market access is carried out by digitalizing marketing. Adapting this technology will create a new offer to existing customers to be more loyal, and data collection will then be recorded, which ends in deep learning customer engagement always to provide an appropriate and satisfying service.

Sixth is a cluster of halal industry development. The synergy of Islamic banks and Muslim-friendly tourism will encourage the growth of other halal industries, either the food sector, clothing, pharmacy, media, and recreation, or even the new halal industry. This halal industry cluster is carried out in two large clusters: goods (physical products) and services (non-physical products/services). Physical products are related to food consumption, fashion, pharmacy (drugs), and cosmetics. Meanwhile, services focus on finance, tourism, health care, and media. Clustering is supported by stakeholders that will facilitate the identification of the halal industry to develop it. The halal cluster must also be guaranteed easy access to various other halal industrial products, such as banking access, financing, and others, to support business activities and other halal cluster expansions.

Figure 6. Stages of simultaneous-holistic synergy

The form of "simultaneous-holistic synergy" (together at the same time) is an ideal form of synergy, is minimalist with maximum results, and will provide multiple positive impacts, which in turn will expand and accelerate the potential of various other halal industry sectors. It can even open up new employment opportunities for the community around Muslim-friendly tourism destinations in the form of food, fashion, pharmacy or media, and other halal recreation and industries, which in turn will improve and make Indonesia the world's halal epicenter.

This study concludes that the pattern of Islamic bank synergy and the halal industry is conducted in two ways: partial synergy and simultaneous-holistic synergy. Partial synergy is a collaboration carried out by Islamic banks, which has been performed in each halal industry, minus Muslim-friendly tourism. Meanwhile, simultaneous-holistic synergy is also a collaboration between Islamic banks and Muslim-friendly tourism in developing and improving ACES-based criteria services. Islamic banks and Muslim-friendly tourism should make this second pattern in conducting synergy in the future since Muslim-friendly tourism is the center of the halal industry, which will simultaneously provide multiple impacts of the emergence of other halal industries (food, fashion, pharmacy, and media and recreation).

Halal industry development through simultaneous-holistic synergy patterns is carried out in the following ways: building a connection between partnership cooperation, optimizing the role of Islamic bank stakeholders and Muslim-friendly tourism, improvement of ACES (access, communication, environmental, and service infrastructure), the intensity of education and literacy of the halal industry, innovation and technology transformation, and conducting clusters for the halal industry development.

[1] Nurrachmi, R. (2016). The global development of halal food industry: A survey. Tazkia Islamic Finance and Business Review, 11(1): 39-56. https://doi.org/10.30993/tifbr.v11i1.113

[2] Moshin, A., Brochado, A., Rodrigues, H. (2020). Halal tourism is traveling fast: Community perceptions and implications. Journal of Destination Marketing & Management, 18: 100503. https://doi.org/10.1016/j.jdmm.2020.100503

[3] KNKS. (2019). Menjadikan Indonesia Sebagai Pusat Ekonomi Syariah Dunia. Insight, 1: 1-19.

[4] Dinar Standard. (2020). State of the global islamic economy report 2020/2021. Dubai: Dubai Islamic Economic Development Center, and Salam Gateway.

[5] Dinar Standard. (2019). State of the global islamic economy report: Driving the islamic economy revolution 4.0. Dubai International Financial Centre, 1-174. Retrieved 28 March, 2020.

[6] Dinar Standard. (2022). State of the Global Islamic Economy Report 2021/2022. In State of the Global Islamic Economy Report 2020/21. Retrieved 18 May, 2022.

[7] Fahan, A. (2019). Wisata Halal Bisa Membuat Indonesia Sebagai Pusat Industri Halal Dunia. Retrieved 14 April, 2019.

[8] Bank Indonesia. (2019). Industri Halal Indonesia. Retrieved 20 May, 2020.

[9] Prayuda, R., Syafrinaldi, Akbar, D., Nurman, Sary, D.V. (2022). Development of Penyengat Island area as an international tourism area based on heritage tourism. International Journal of Sustainable Development and Planning, 17(4): 1367-1371. https://doi.org/10.18280/ijsdp.170434

[10] Al-Ansi, A., Han, H. (2019). Role of halal-friendly destination performances, value, satisfaction, and trust in generating destination image and loyalty. Journal of Destination Marketing & Management, 13: 51-60. https://doi.org/10.1016/j.jdmm.2019.05.007

[11] Aji, H.M., Muslichah, I., Seftyono, C. (2021). The determinants of Muslim travellers’ intention to visit non-Islamic countries: a halal tourism implication. Journal of Islamic Marketing, 12(8): 1553-1576. https://doi.org/10.1108/JIMA-03-2020-0075

[12] Mohsin, A., Ramli, N., Alkhulayfi, B.A. (2016). Halal tourism: Emerging opportunities. Tourism Management Perspectives, 19: 137-143. https://doi.org/10.1016/j.tmp.2015.12.010

[13] Yazid, F., Kamello, T., Nasution, Y., Ikhsan, E. (2020). Strengthening sharia economy through halal industry development in Indonesia. Paper presented at the International Conference on Law, Governance and Islamic Society (ICOLGIS 2019), Atlantis Press. https://doi.org/10.2991/assehr.k.200306.187

[14] Bustamam, N., Suryani, S. (2021). Potensi pengembangan pariwisata halal dan dampaknya terhadap pembangunan ekonomi daerah provinsi riau. Jurnal Ekonomi KIAT, 32(2): 146-162. https://doi.org/10.25299/kiat.2021.vol32(2).8839

[15] Cuesta-Valiño, P., Bolifa, F., Núñez-Barriopedro, E. (2020). Sustainable, smart and muslim-friendly tourist destinations. Sustainability, 12(5): 1778. https://doi.org/10.3390/su12051778

[16] Wingett, F., Turnbull, S. (2017). Halal holidays: exploring expectations of Muslim-friendly holidays. Journal of Islamic Marketing, 8(4): 642-655. https://doi.org/10.1108/JIMA-01-2016-0002

[17] Paramarta, V., Dewi, R., Rahmanita, F., Hidayati, S., Sunarsi, D. (2021). Halal tourism in Indonesia: Regional regulation and Indonesian ulama council perspective. International Journal of Criminology and Sociology, 10: 497-505. https://doi.org/10.6000/1929-4409.2021.10.58

[18] Samori, Z., Rahman, F. (2013). Establishing shariah compliant hotels in Malaysia: Identifying opportunities, exploring challenges. West East Journal of Social Sciences, 2(2): 95-108.

[19] Mastercard & CrescentRating. (2019). Global Muslim Travel Index 2019.

[20] GMTI. (2021). Global Muslim Travel Index 2021. Mastercard-Crescent Rating, (July), 31-62. Retrieved 15 January, 2022.

[21] Musa, A., Halim, H., Khalidin, B., Ibrahim, A. (2021). What determines Muslim-friendly tourism in aceh? Iqtishadia, 14(1): 81-106. https://doi.org/10.21043/iqtishadia.v14i1.9438

[22] Santoso, S., Hadibrata, B., Nurhidajat, R., Widyanty, W., Fatmawati, A.A., Ubaidillah, R., Isa, S.M. (2021). Study On Development Strategies of Muslim-Friendly Tourism Ecosystem. SSRN Electronic Journal, 12: 1-12. https://doi.org/10.2139/ssrn.3875184

[23] Badan Pusat Statistik. (2021). Catalog: 1101001. Statistik Indonesia 2021. Retrieved 20 April, 2022.

[24] Jaelani, A. (2017). Halal tourism industry in Indonesia: Potential and prospects. International Review of management and Marketing, 7(3): 25-34.

[25] Khairi, M., Darmawan, D. (2021). The relationship between destination attractiveness, location, tourism facilities, and revisit intentions. Journal of Marketing and Business Research, 1(1): 39-50. https://doi.org/10.56348/mark.v1i1.32

[26] Soeroso, A., Susilo, Y.S. (2014). Traditional Indonesian gastronomy as a cultural tourism attraction. Journal of Applied Economics in Developing Countries, 1(1): 45-59.

[27] BSI. (2021b). Laporan Tahunan 2021: Energi Baru untuk Indonesia: PT Bank Syariah Indonesia, Tbk.

[28] Achdiat, I. (2021). Outlook Industri Jasa Keuangan Syariah Tahun 2022: Peluang & Tantangan. KNEKS Komite Nasional EKonomi dan Keuangan Syariah.

[29] Martín, J.C., Orden-Cruz, C., Zergane, S. (2020). Islamic finance and halal tourism: An unexplored bridge for smart specialization. Sustainability, 12(14): 5736. https://doi.org/10.3390/su12145736

[30] Ab Talib, M.S., Ai Chin, T., Fischer, J. (2017). Linking Halal food certification and business performance. British Food Journal, 119(7): 1606-1618. https://doi.org/10.1108/BFJ-01-2017-0019

[31] Muhamed, N.A., Ramli, N.M., Abd Aziz, S., Yaakub, N.A. (2014). Integrating islamic financing and halal industry: A survey on current practices of the selected Malaysian authority bodies. Asian Social Science, 10(17): 120-126. https://doi.org/10.5539/ass.v10n17p120

[32] Wajdi Dusuki, A. (2008). Understanding the objectives of Islamic banking: A survey of stakeholders' perspectives. International Journal of Islamic and Middle Eastern Finance and Management, 1(2): 132-148. https://doi.org/10.1108/17538390810880982

[33] Ismail, A.G., Mohd Noor, M.A. (2016). Halal finance and halal foods: Are they falling apart? Acta Universitatis Danubius (Economica), 12(3): 113-126.

[34] Nisha, N., Iqbal, M. (2017). Halal ecosystem: Prospect for growth in Bangladesh. International Journal of Business and Society, 18(S1): 205-222.

[35] Muhamed, N.A., Ramli, N.M. (2018). Towards integrated halal sectors and Islamic financing: The academia perspectives. In: Muhammad Hashim, N., Md Shariff, N., Mahamood, S., Fathullah Harun, H., Shahruddin, M., Bhari, A. (eds) Proceedings of the 3rd International Halal Conference (INHAC 2016). Springer, Singapore. https://doi.org/10.1007/978-981-10-7257-4_15

[36] Hassan, M.K., Rabbani, M.R., Chebab, D. (2021). Integrating Islamic finance and Halal industry: Current landscape and future forward. International Journal of Islamic Marketing and Branding, 6(1): 60-78. https://doi.org/10.1504/IJIMB.2021.117594

[37] Sidharta, R.B.F.I. (2017). Optimalisasi peran perbankan syariah dalam mendukung wisata halal. Jurnal Distribusi, 5(2): 1-14. https://doi.org/10.29303/ distribusi.v5i2.29

[38] Tieman, M. (2011). The application of in supply chain management: In-depth interviews. Journal of Islamic Marketing, 2(2): 186-195. https://doi.org/10.1108/17590831111139893

[39] Trimulato, T. (2021). Linkage sharia banking and sharia fintech to support halal industry in Indonesia. The Annual International Conference on Islamic Economics and Business (AICIEB), pp. 138-151. https://doi.org/10.18326/aicieb.v1i0.15

[40] Mubarok, F.K., Imam, M.K. (2020). Halal industry in Indonesia; Challenges and opportunities. Journal of Digital Marketing and Halal Industry, 2(1): 55-64. https://doi.org/10.21580/jdmhi.2020.2.1.5856

[41] Yudha, A.T.R.C., Pauzi, N.S. (2020). The synergy model for strengthening the productivity of Indonesian halal industry. al-Uqud: Journal of Islamic Economics, 4(2): 186-199. https://doi.org/10.26740/al-uqud.v4n2.p186-199

[42] Soedigno, V.R., Hidayat, S.E., Beik, I.S., Sofyan, R., AHmad, H., Rahmoto, W., Ayyash, Y. (2020). Laporan Perkembangan Pariwisata Ramah Muslim Daerah in Komite Nasional Ekonomi dan Keuangan Syariah (KNEKS). Jakarta.

[43] AMCA. (2018). Embracing the Culture of Prevention to Enrich ASEAN Identity. Retrieved 24 October, 2018.

[44] BSI. (2021). Sejarah Perseroan - Bank Syariah Indonesia. https://ir.bankbsi.co.id/corporate_history.html.

[45] Mastercard-Crescentrating. (2022). Global Muslim Travel Index 2022 Report. Retrieved 22 October, 2022.

[46] Ratnasari, R.T., Gunawan, S., Mawardi, I., Kirana, K.C. (2021). Emotional experience on behavioral intention for halal tourism. Journal of Islamic Marketing, 12(4): 864-881. https://doi.org/10.1108/JIMA-12-2019-0256

[47] Hosany, S., Gilbert, D. (2010). Measuring tourists’ emotional experiences toward hedonic holiday destinations. Journal of Travel Research, 49(4): 513-526. https://doi.org/10.1177/0047287509349267

[48] Oliveira, E., Panyik, E. (2015). Content, context and co-creation: Digital challenges in destination branding with references to Portugal as a tourist destination. Journal of Vacation Marketing, 21(1): 53-74. https://doi.org/10.1177/1356766714544235

[49] Amrial, A., Adrian, A., Muhamad, E. (2017). Penta helix model: A sustainable development solution through the industrial sector. Social and Human Sciences, 14: 152-156.

[50] Calzada, I., Cowie, P. (2017). Beyond smart and data-driven city-regions? Rethinking stakeholder-helixes strategies. Regions Magazine, 308(4): 25-28. https://doi.org/10.1080/13673882.2017.11958675

[51] Antipova, T. (2021). Advances in Digital Science: ICADS 2021 (Vol. 1352): Springer Nature.

[52] Ostrom, E. (2020). Beyond Markets and States: Polycentric Governance of Complex Economic Systems Shaping Entrepreneurship Research (pp. 353-392): Routledge. https://doi.org/10.1257/aer.100.3.641

[53] Štefenberga, D., Sloka, B. (2019). The role of innovation in sustainable regional development: Case of Latvia. Paper presented at the Proceedings of the International Scientific Conference “Rural Development”.

[54] Widowati, S., Ginaya, G., Triyuni, N.N. (2019). Penta helix model to develop ecotourism: Empowering the community for economic and ecological sustainability. International Journal of Social Sciences and Humanities, 3(2): 31-46. https://doi.org/10.29332/ijssh.v3n2.288