Vlora Prenaj![]() | Juliana Imeraj

| Juliana Imeraj![]() | Shkëlqesa Smajli*

| Shkëlqesa Smajli*![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The purpose of the study is to examine the financial performance of commercial banks in Albania and Kosovo. As they are considered to be the main financial institutions in both countries, facilitating individual and corporate financing, and therefore influencing a country's economic growth. The data is collected from audited financial statements of each commercial bank in Albania and Kosovo for the period 2010-2021. The regression models ‘pooled OLS’, ‘fixed effects (FE)’, and ‘random effects (RE)’ were utilized for analysis, and the Hausman test was used to compare the fixed effects model to the random effects model. Return on assets (ROA) and return on equity (ROE) of the activity of commercial banks were assessed, while independent variables included the number of banks, non-performing loans, real GDP growth, GDP per capita, consumer price inflation (percent, period average), and the unemployment rate. The results show that bank performance is positively correlated to the number of banks, real GDP growth, GDP per capita, and the unemployment rate. On the other hand, the results show that bank performance is negatively affected by inflation and non-performing loans. According to the results of the study, we can conclude that the banks in Kosovo have performed better than the banks in Albania. Moreover, from the research on the two countries, it is clear that there cannot be a good balance between economic growth and satisfactory banking performance.

commercial banks, return on assets, return on equity, Albania, Kosovo

In developing countries, where financial markets are often small or do not exist at all, the stability of the financial system depends on the banking industry. In these countries, it is the job of the banking industry to connect savers and borrowers and to act as a financial middleman by turning deposits into profitable ventures [1]. Past economic crises in many different countries have shown that problems in the banking sector can spread to the rest of the economy and cause significant problems. There is little doubt that as the banking sector's contribution to the financial system rises, so does the sector's significance for macroeconomic stability and economic expansion [2].

In the modern economy, the bank serves as an intermediary and must be profitable [3]. Most of what affects the profitability of the banking sector is what managers decide to do, not what the market does [3, 4]. Several studies suggest that there are two types of factors that affect a bank's ability to make money: internal and external factors. These studies specify ROA and ROE as the dependent variables, and consider the internal and external factors as independent variables [5, 6].

The aim of the study is to analyze the performance of commercial banks in Albania and Kosovo in terms of risk assessment and return as an important instrument for making investment and credit decisions.

While the specific objectives are:

Economic development is impossible without the development of the private sector, and banks may and are helping in this area [7]. Banks are more important in developing nations since their financial markets are undeveloped, with banks serving as the primary source of finance [8].

The study is organized into five main sections. Section 1 provides an introduction to the research topic and outlines the objectives of the study. Section 2 presents a theoretical background and an overview of the banking systems in Albania and Kosovo. Section 3 describes the research methodology, including data collection and analysis methods. Section 4 presents the results of the study, including regression analysis and key findings. Finally, Section 5 offers conclusions and recommendations based on the findings of the study.

2.1 Banking system in Albania

Central Bank - The Bank of Albania (BOA) has the authority to license and supervise banks, NBFIs, savings and loan societies and their unions, foreign exchange bureaus, and representative offices of foreign banks in accordance with the Law "On Banks in the Republic of Albania."

As of the end of 2021, the structure of the banking system in Albania consisted of 12 banks, namely: Alpha Bank Albania, American Bank of Investment, Credins Bank, United Bank of Albania, First Investment Bank, Intesa Sanpaolo Bank Albania, National Commercial Bank, OTP Bank Albania, Pro Credit Bank, Raiffeisen Bank, Tirana Bank, and Union Bank [9]. The Albanian banking industry continued to be quite consolidated, just as in previous years [10], with around 75% of the assets in the banking sector held by non-residents, of whom 57% were from the EU and 28% from non-EU nations [11]. Almost all of Albania's territory is covered by bank branches and agencies, although Tirana (capital city) has the highest concentration (42.9%) and the highest population density (31.92%) [11].

The primary banking activity soundness indicators relating to capitalization, income, and liquidity remained at satisfactory levels. The capital adequacy ratio (CAR), the most significant monitoring measure, stood at 18.02% at the end of 2021, well above the minimum requirement of 12%. Return on Average Assets (ROAA) and Return on Average Equity (ROAE), two profitability metrics, both increased during 2021, being 1.31% and 12.89%, respectively [11]. At the end of 2021, total bank assets were estimated by BOA to be around EUR 14.69 billion, an increase of almost 12.2% from 2020. A positive development for the banking industry was the decrease in the non-performing loan ratio, mainly due to an increase in the credit portfolio of about 10.2% in 2021. Long-term loans make up the majority of the entire credit portfolio as of the end of 2021, followed by short- and medium-term loans, while 51.1% of all loans are still made in foreign currencies [11].

Most of the liabilities of the banking system come from customer deposits, which make up 80.8% (81.3% in December 2020) of the whole. The total value of deposits in the system increased during 2021 by 10.25%, reaching EUR 11.87 billion. Domestic currency's percentage of total deposits dropped from 49.5% in December 2020 to 41.1% [11]. Given that demand deposits and current accounts made up a larger percentage of total deposits, the maturity structure changed to short-term maturities, while time deposits fell in comparison as a result of the market's ongoing decline in interest rates. The top 10 depositors in December 2021 made up 6.8% of all deposits in the banking sector, up from 5.2% in December 2020. The performance of the other larger depositor groups exhibits a comparable growth trend. Household deposits continue to make up the majority of the banking system's deposits, accounting for 80.05% of all deposits, albeit declining by about 2.4 percentage points from the previous year. Businesses' accounts grew by 25.2% more than families' accounts did (8.1% vs. 8.1%) in 2021. In December 2021, the loan to deposit ratio was 45.39% (December 2020: 47.33%), reflecting an asset-liability structure that makes it easier to maintain liquidity and may offer lending incentives [11].

2.2 Banking system in Kosovo

The performance of the banking sector in Kosovo has changed over the years. Commercial banks play an important role in the financial system, which affects the development of a country's economy. The analysis of financial statements by means of ratios is a very useful way to verify the ongoing business of a commercial bank and its position in relation to the competition.

The Central Bank of Kosovo regulates the entire financial system. There are 11 commercial banks operating in Kosovo: Nova Ljubljanska Banka, Bank for Business, Turkiye Cumhuriyeti Ziraat Bankasi, Economic Bank, Raiffeisen Bank Kosovo, ProCredit Bank, TEB SH.A, National Commercial Bank Kosovo, BKT, Turkiye Is Bankasi, Komercijalna Banka ad Beograd, and Banka Credins Kosovo [12].

The Kosovar financial sector is heavily dominated by international banking groups. The largest are Raiffeisen, ProCredit Group, and Nova Ljubljanska Banka. This foreign exposure gives the banking sector a fairly stable perspective and financial knowledge from abroad [10].

In the framework of the indicators that measure the performance of the banking sector, at the end of the second quarter of 2021, the sector is found to have increased stability through the improvement of the level of liquidity, capitalization, profitability, as well as the higher quality of the credit portfolio [13]. The banking sector continues to be at a satisfactory level during 2021, exceeding the minimums required by regulations compared to Q2 2020 [13]. According to the CBK, this capital level result was inherited from previous years.

The banking sector in Kosovo during the second quarter of 2021 managed to make a profit of 12.3 million euros more compared to the same quarter of the previous year. This happened as a result of the increase in income compared to the increase in expenses [13]. Income from interest on loans of 56.8 million euros, as well as non-interest income of 5.2 million euros, which consists of commissions and fees, mainly influenced the increase in income [13]. The banking sector in Kosovo is primarily funded by non-financial corporations and household deposits [14]. The financial system has, in the history of its operation, successfully faced the biggest challenge caused by COVID-19 [15]. This recovery of the banking system is considered to have occurred as a result of government support measures. However, the uncertainty of the banking system continues even further into the future. In addition to the pandemic, the outbreak of the war in Ukraine has also had a major impact.

Due to the large number of commercial banks in Kosovo and Albania, the study is based on a review of the financial statements of those banks. The information is collected from the audited financial statements for the years 2010 through 2021, which are available on each commercial bank's website.

Regression methods ‘pooled OLS’, ‘fixed effects (FE)’ and ‘random effects (RE)’ were used for analysis. Ordinary least squares regression has been used in many studies of bank profitability [16-18]. Also, fixed effects and random effects were used by many researchers, such as [6, 19-23].

The Hausman test was performed to test the fixed effects model against the random effects model. Based on the results of the test, a decision would be made on whether to accept or reject the null hypothesis. The alternative hypothesis was accepted if the test's p-value was less than 0.05 (H1: Fitted FE model).

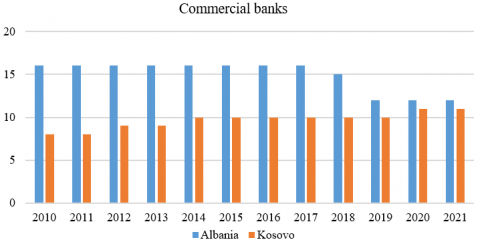

Figure 1 shows the number of commercial banks operating in Albania and Kosovo. When compared to Kosovo, Albania appears to have a greater number of commercial banks. The earliest years, particularly from 2010 to 2017, are when countries' differences in the number of banks are greatest. However, the number of banks has expanded in Kosovo recently while falling in Albania. As a result, in 2021, we can observe that Kosovo has 11 banks whereas Albania only has 12.

The activity of commercial banks was evaluated using dependent variables such as return on assets (ROA) and return on equity (ROE). While the number of banks, non-performing loans, real GDP growth (%), GDP per capita, consumer price inflation (percent, period average), and unemployment rate were used as independent variables.

Figure 1. Commercial banks in banking system in Albania and Kosovo

Source: Bank of Albania (2021), Central Bank of Kosovo (2021)

Table 1 below presents the variables used in the analysis, as well as the authors who have used these variables in their research.

Table 1. Variables used in analysis

|

Variables |

Descriptions |

References |

|

Dependent |

||

|

ROA |

The return on assets (%) |

Akbaş [1]; Osuagwu [24]; Ali & Ali [25] |

|

ROE |

The return on equity (%) |

Ferrouhi [26], Kumar et al. [27]; Ahmed & Bhuyan [28] |

|

Independent |

||

|

Internal determinants |

||

|

FIN_BANK |

Number of banks in countries |

Kumar et al. [27] |

|

NPLR |

Nonperforming loans ratio (percent of gross loans, end of period) |

Roman & Dănuleţiu [29]; Kumar et al. [27] |

|

External determinants |

||

|

GDP |

Real GDP growth (percent) |

Ongore & Kusa [30]; Derbali [19] |

|

GDP per capita |

Gross domestic product per capita |

Căpraru & Ihnatov [31] |

|

INF |

Consumer price inflation (percent, period average) |

Akbaş [1]; Petria et al. [32] |

|

UNRATE |

Unemployment rate (percent, period average) |

Abreu & Mendes [33], Kumar et al. [27] |

3.1 Empirical model

"Fixed effects" and “random effects” models were also used in the regression analysis for performance. ROA and ROE connection panel data general model includes the number of banks (FIN_BANK), non-performing loan ratio (NPLR), real GDP growth (GDP), gross domestic product per capita (GDP per capita), inflation (INF), and unemployment rate (UNRATE).

The two models below were estimated:

$ROA_{i t}=\beta_1+\beta_2FIN\_BANK _{i t}+\beta_3 NPLR _{i t}+\beta_4 G D P_{i t}+\beta_5 GDPpercapita _{i t}+\beta_6 I N F_{i t}+\beta_7 UNRATE _{i t}+\omega_{i t}$ (1)

$R O E_{i t}=\beta_1+\beta_2 FIN\_BANK_{i t}+\beta_3 N P L R_{i t}+\beta_4 G D P_{i t}+\beta_5 GDPpercapita_{i t}+\beta_6 I N F_{i t}+\beta_7 UN R A T E_{i t}+\omega_{i t}$ (2)

where, ROAit is return on assets of bank i in time period t; ROEit is return on equity of bank i in time period t; NPLRit is non-performing loans ratio of bank i in time period t; GDPit is gross domestic product i in time period t; GDPpercapitait is gross domestic product per capita i in time period t; UNRATEit is unemployment rate i in time period t; INFit is inflation i in time period t; FIN_BANKit is number of banks i in time period t.

Table 2 shows a summary of the descriptive statistics for the dependent and independent variables that were used to determine how well the banks under study performed. During the 2010-2021 research period, the variables changed significantly. ROA has a mean of 1.435, ranging from a minimum of 0.10 to a maximum of 2.80. Meanwhile, ROE appears to be more volatile, having a mean of 13.40 and ranging from a low of 0.80 to a maximum of 22.50.

The mean of the numbers of banks is 12.29, with a minimum of 8 and a maximum of 16. The mean and median of the non-performing loan ratio are 10.20 and 8.20, respectively. The Real GDP growth rate has an average of 3.071 and a standard deviation of 3.450, while the gross domestic product per capita ranges between 3010 and 17245. Inflation has a mean around 2.050, while the unemployment rate has a mean of 21.50 and a median of 21.27.

The correlation matrix of dependent and independent variables is shown in Table 3. The results show a statistically significant positive correlation between ROA and ROE (0.96), as well as a statistically significant positive correlation between ROA and UNRATE. There is a statistically significant negative correlation between ROE and FIN_BANK (-0.66) and NPLR (-0.77). On the other hand, there is a statistically significant positive correlation between ROE and UNRATE (0.67). There is a strong positive correlation between FIN_BANK and NPLR (0.84), while with UNRATE there is a strong negative relationship (-0.83). A statistically significant positive correlation exists between the real GDP rate and INF (0.45), but between GDP per capita and UNRATE there is a statistically significant negative correlation.

Table 2. Descriptive statistics of variables, 2010-2021

|

Variables |

Mean |

Median |

SD |

Minimum |

Maximum |

|

ROA |

1.435 |

1.350 |

0.7429 |

0.100 |

2.800 |

|

ROE |

13.40 |

13.50 |

5.916 |

0.800 |

22.50 |

|

FIN_BANK |

12.29 |

11.50 |

3.029 |

8.000 |

16.00 |

|

NPLR |

10.20 |

8.200 |

7.030 |

1.900 |

23.50 |

|

GDP |

3.071 |

3.450 |

3.040 |

-5.300 |

9.100 |

|

GDP per capita |

6455 |

4299 |

4473 |

3010 |

17245 |

|

INF |

2.050 |

1.850 |

1.580 |

-0.500 |

7.300 |

|

UNRATE |

21.50 |

21.27 |

8.120 |

11.47 |

35.26 |

Notes: ROA = Return on assets; ROE = Return on equity; FIN_BANK = Number of banks; NPLR = Non-performing loan ratio; GDP = Real GDP growth (%); GDP per capita= Gross domestic product per capita; INF = Inflation, UNRATE = Unemployment rate.

Table 3. Correlation matrix of variables, 2010-2021

|

Variables |

ROA |

ROE |

FIN_BANK |

NPLR |

GDP |

GDP per capita |

INF |

|

ROE |

0.9640*** |

1.0000 |

|

|

|

|

|

|

FIN_BANK |

-0.6657** |

-0.6798** |

1.0000 |

|

|

|

|

|

NPLR |

-0.7799*** |

-0.7233** |

0.8441** |

1.0000 |

|

|

|

|

GDP |

0.2519 |

0.2654 |

-0.1974 |

-0.2268 |

1.0000 |

|

|

|

GDP per capita |

-0.1881 |

-0.1676 |

0.2608 |

0.0082 |

-0.0134 |

1.0000 |

|

|

INF |

-0.2786 |

-0.2337 |

-0.0559 |

0.0114 |

0.4468* |

-0.0503 |

1.0000 |

|

UNRATE |

0.6585* |

0.6778* |

-0.8033** |

-0.5654* |

0.1481 |

-0.6739** |

-0.1193 |

Notes: ROA = Return on assets; ROE = Return on equity; FIN_BANK = Number of banks; NPLR = Non-performing loan ratio; GDP=Real GDP growth; GDP per capita = Gross domestic product per capita; INF = Inflation; UNRATE = Unemployment rate.

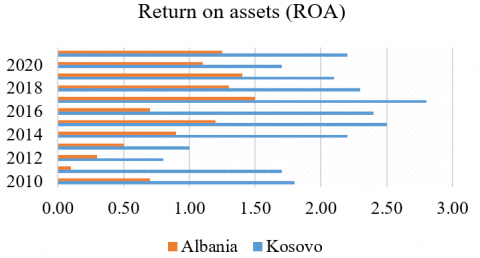

The financial performance of banks in Albania and Kosovo as assessed by ROA from 2010 to 2021 is shown in Figure 2. The displayed graph compares the ROAs of the two nations, with Kosovo appearing to have the highest ROA performance. Although Kosovo has a smaller GDP per capita than Albania, according to ROA, it has had the best financial performance over the duration of the study.

Figure 2. Return on assets (ROA) of commercial banks in Albania and Kosovo (2010-2021)

Source: World Bank Group (2016) [34], World Bank Group (2022) [35]

Table 4 shows the results of multiple regression using "fixed effects (FE)," "random effects (RE)," and "pooled OLS" models. The models examined the relationship between FIN_BANK, NPLR, real GDP growth, GDP per capita, INF, and UNRATE and the performance of the bank as measured by ROA.

The Hausman test was used in the Table 5 to determine which of the estimated models was more appropriate. Based on the results of the test, a decision was made about whether or not to accept the zero hypothesis.

According to Table 4's results for random effects (RE), we may get the conclusion that the NPLR coefficient is negative and has a statistically significant role in determining ROA. Our results are in accordance with those obtained by Osuagwu [24]. NPLR is an important determinant of banking profitability [25]. Also, INF has a negative effect on banks profitability, measured by ROA. However, Căpraru and Ihnatov [26] reach a different conclusion, claiming that inflation has a positive and statistically significant effect on ROA.

On the other hand, other determinants such as: FIN_BANK, real GDP growth, and GDP per capita have a positive relationship with ROA. According to Nuhiu et al. [8], real GDP growth appears to have a positive effect on ROA. Derbali (2021) [19] suggests that higher real GDP growth has a significant influence on bank profitability. Positive results between GDP per capita and ROA are also according to Căpraru and Ihnatov [31], which concludes that GDP per capita has a statistically significant effect on ROA. While Anbar and Alper [36] have not found a relationship between ROA and real GDP growth. The results also showed that UNRATE has a positive relationship with ROA and is a statistically significant determinant.

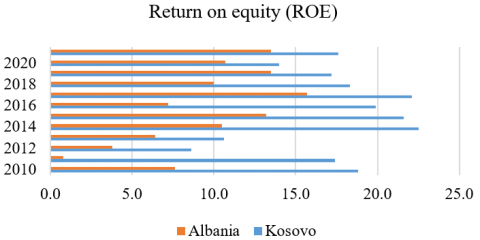

Figure 3 displays the financial performance of banks in Kosovo and Albania from 2010 to 2021, according to ROE. The two countries' ROEs are contrasted in the graph, with Kosovo appearing to have the best ROE performance.

Figure 3. Return on equity (ROE) of commercial banks in Albania and Kosovo (2010-2021)

Source: World Bank Group (2016) [34], World Bank Group (2022) [35]

Table 4. Panel results for ROA as dependent variables, 2010-2021

|

Explanatory variables |

ROA |

ROA |

ROA |

|

(FE) |

(RE) |

(OLS) |

|

|

Constant |

−0.4102 (1.9101) |

−0.4571 (1.8880) |

−0.5388 (1.9155) |

|

Internal determinants |

|||

|

FIN_BANK |

0.0954 (0.0981) |

0.1102 (0.0938) |

0.1360 (0.0911) |

|

NPLR |

-0.0603 |

-0.0711** |

-0.0900*** |

|

|

(0.0365) |

(0.0319) |

(0.0241) |

|

External determinants |

|||

|

GDP |

0.04357 (0.0325) |

0.0441 (0.0319) |

0.0452 (0.0326) |

|

GDP per capita |

3.2181 (3.8473) |

7.1268 (3.7351) |

1.3945 (3.734) |

|

INF |

−0.0878 (0.0761) |

−0.0973 (0.0734) |

−0.1138 (0.0725) |

|

UNRATE |

0.0610 (0.0354) |

0.0595* (0.0347) |

0.0569 (0.0353) |

|

R2 |

0.8169 |

0.680 |

0.8036 |

|

Adjusted R2 |

0.7812 |

0.617 |

0.7342 |

Notes: ROA = Return on assets; ROE = Return on equity; FIN_BANK = Number of banks; NPLR = Non-performing loan ratio; GDP = Real GDP growth; GDP per capita= Gross domestic product per capita; INF = Inflation; UNRATE = Unemployment rate.

Table 5. Testing and selecting the model for ROA

|

Hypothesis |

The P value for the Hausman test |

Best fitted model |

|

|

H0: Fitted RE model |

H1: Fitted FE model |

0.425 |

H1: Fitted RE model |

Note: Random effects model (RE), Fixes effects model (FE).

The results of multiple regression using “fixed effects (FE)”, “random effects (RE)” and “pooled OLS” models are showed in Table 6. The models examined the relationship between the bank's performance as measured by ROE and the variables FIN_BANK, NPLR, real GDP growth, GDP per capita, INF, and UNRATE.

In the Table 7, the Hausman test was performed to assess which of the estimated models was more acceptable. Based on the test's results, the zero hypothesis was either accepted or rejected.

According to the RE model data in Table 6 that was presented, the independent variable of FIN_BANK has a positive relationship with ROE. Our results are in accordance with those obtained by Kumar et al. [26]. The positive relationship is also between real GDP growth, GDP per capita, and ROE [33]. Real GDP growth is considered positive and statistically significant for profitability as measured by ROE. While GDP per capita has a positive but weak influence on ROA [29]. Real GDP growth is one of the most often used macroeconomic indicators since it measures the entire economic activity within an economy [37].

Table 6. Panel results for ROE as dependent variables, 2020-2021

|

Explanatory variables |

ROE |

ROE |

ROE |

|

(FE) |

(RE) |

(OLS) |

|

|

Constant |

−9.6435 (18.357) |

−9.7759 (17.783) |

−9.7786 (17.781) |

|

Internal determinants |

|

||

|

FIN_BANK |

0.8821 (0.9434) |

0.9238 (0.8472) |

0.9247 (0.8457) |

|

NPLR |

−0.4519 (0.3508) |

−0.4825** (0.2267) |

−0.4831** (0.2237) |

|

External determinants |

|

||

|

GDP |

0.3216 (0.3128) |

0.3233 (0.3033) |

0.3234 (0.3033) |

|

GDP per capita |

0.0004 (0.0003) |

0.0004 (0.0003) |

0.0004 (0.0003) |

|

INF |

−0.5378 (0.7314) |

−0.5645 (0.6742) |

−0.5651 (0.6734) |

|

UNRATE |

0.6639* (0.3403) |

0.6597** (0.3284) |

0.6596 (0.3284)* |

|

R2 |

0.7334 |

0.660 |

0.7331 |

|

Adjusted R2 |

0.7119 |

0.617 |

0.6389 |

Notes: ROA = Return on assets; ROE = Return on equity; FIN_BANK = Number of banks; NPLR = Non-performing loan ratio; GDP = Real GDP growth; GDP per capita= Gross domestic product per capita; INF = Inflation; UNRATE = Unemployment rate.

Table 7. Testing and selecting the model for ROE

|

Hypothesis |

The P value for the Hausman test |

Best fitted model |

|

|

H0: Fitted RE model |

H1: Fitted FE model |

0.886 |

H0: Fitted RE model |

Note: Random effects model (RE), Fixes effects model (FE).

But the coefficient of NPLR is negative and a statistically significant variable in determining ROE. The same findings can be found in research [27].

A negative relationship also exists between INF and ROE, although it is not statistically significant. The same results can be found in the authors' research [32]. Whereas for UNRATE, the model’s results showed a positive relationship and were statistically significant factors in determining ROE. UNRATE effects according to Abreu and Mendes [33], also play a role in determining bank profitability.

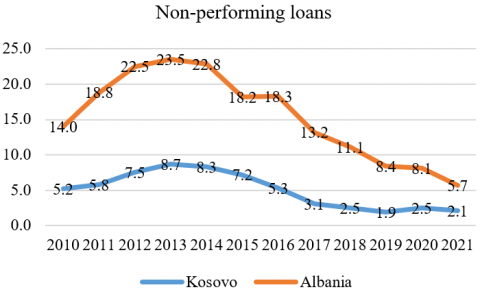

Figure 4. Non-Performing Loans (%) for Albania and Kosovo (2010-2021)

Source: World Bank Group (2016) [34], World Bank Group (2022) [35]

Figure 4 shows the non-performing loans ratio for banks in Albania and Kosovo, during the period 2010-2021. Two crucial performance metrics, ROA and ROE demonstrated that Kosovo dominated with the best bank performance. The ratio of non-performing loans, is another crucial indicator, which demonstrates that banks in Albania face a very high rate compared to banks operating in Kosovo.

This paper examines the performance assessment of commercial banks in Kosovo and Albania. Based on the obtained results, we were able to identify how the commercial banks are performing in Albania and Kosovo. The research focused on the profitability of commercial banks operating in Albania and Kosovo, for the period 2010-2021. Regression methods ‘pooled OLS’, ‘fixed effects (FE)’ and ‘random effects (RE)’ were used for analysis, and the Hausman test was performed to test the fixed effects model against the random effects model. The number of banks (FIN BANK), non-performing loan ratio (NPLR), real gross domestic product growth (GDP), gross domestic product per capita (GDP per capita), inflation rate (INF), and unemployment rate (UNRATE), are all included in the generic panel data model in connection to performance measures such as ROA and ROE).

Based on the results of random effects (RE), as measured by ROA, we derive the conclusion that the NPLR coefficient is negative and has a statistically significant importance in determining ROA. Also, INF has a negative relationship with ROA. On the other hand, other determinants such as: FIN_BANK, real GDP growth, and GDP per capita have positive relationships with ROA. The results also showed that UNRATE has a positive relationship with ROA and is a statistically significant determinant.

Whereas, according to the random effects (RE) of the result of ROE presented, the coefficient of FIN_BANK is positive demonstrating a positive relationship with ROE. The positive relationship is also present between GDP, GDP per capita, and ROE. But the coefficient of NPLR is negative and a statistically significant factor in determining ROE.

A negative relationship also exists between INF and ROE. Whereas for UNRATE, the model’s results showed a negative relationship and were a statistically significant factor in determining ROE.

Since the ROA and ROE for banks of Kosovo are much higher compared to banks operating in Albania, and with the lower percentage of non-performing loans, the question arises as to why the banks in Kosovo do not provide loans with a lower interest rate. Then businesses will have easier access to credit, and this will stimulate economic development. While the existing banks in Kosovo lend at high-interest rates, even though they have a very high rate of return on capital and return on assets compared to banks in the region, the market for new banks should be opened as soon as possible. This would also change the monopoly that has been created between some of the main banks operating in Kosovo, working only to increase their profits.

Banks in Albania have recorded lower ROA and ROE profitability ratios than their counterparts in Kosovo. Even though Albania's banking system has gotten better, this difference in performance can be explained by their attempts to get a bigger share of the loan and deposit market by offering better interest rates and lower fees for their services. Also, it's important to note that the Albanian banking industry has been more competitive than the Kosovo banking industry over the same time period. This is shown by the fact that there are more banks in Albania. Also, it's clear that Albania's higher NPLR ratio has caused its profitability to drop even more.

Commercial bank performance analysis is important, especially when examined over a longer period of time. In our future studies, we consider that it is necessary to examine the financial sector before and after COVID-19. Due to the short period of time following COVID-19, we are now unable to assess this.

[1] Akbaş, H.E. (2012). Determinants of bank profitability: An investigation on turkish banking sector. Öneri Dergisi, 10(37): 103-110.

[2] Sayilgan, G., Yildirim, O. (2009). Determinants of profitability in turkish banking sector: 2002-2007. International Research Journal of Finance and Economics, 28: 2007-2014.

[3] Ngweshemi, L.E., Isiksal, A. (2021). Analysis of the factors affecting bank profitability: Evidence of tanzania commercial banks. Sustainable Economic Development, 39(8): 4768. https://doi.org/10.25115/eea.v39i8.4768

[4] Olweny, T., Shipho, T.M. (2011). Effect of banking sectoral factors on the profitability of commercial banks Kenya. Economics and Finance Review, 1(5): 1-30. http://wwww.businessjournalz.org/efr

[5] Berger, A.N., Humphrey, D.B. (1997). Efficiency of financial institutions: International survey and directions for future research. European Journal of Operational Research, 98(2): 175-212. https://doi.org/10.1016/S0377-2217(96)00342-6

[6] Athanasoglou, P.P., Delis, M., Staikouras, C. (2006). Determinants of bank profitability in the South Eastern European region. Bank of Greece Working Paper.

[7] Morina, F., Özen, E. (2020). Does the commercial bank's loans affect economic growth? Empirical evidence for the real sector economy in Kosovo (2005-2018). International Journal of Sustainable Development and Planning, 15(8): 1205-1222. https://doi.org/10.18280/ijsdp.150807

[8] Nuhiu, A., Hoti, A., Bektashi, M. (2017). Determinants of commercial banks profitability through analysis of financial performance indicators: Evidence from Kosovo. Business: Theory and Practice, 18: 160-170. https://doi.org/10.3846/btp.2017.017

[9] Bank of Albania. (2021). Bank of Albania. https://www.bankofalbania.org.

[10] Deloitte. (2021). CEE banks steering through the pandemic. Accelerated consolidation triggered by COVID-19 turbulence, Hungary.

[11] Bank of Albania. (2021) Annual supervision report. https://www.bankofalbania.org.

[12] Central Bank of Kosovo. (2022). Central bank of the republic of Kosovo. https://bqk-kos.org/?lang=en.

[13] Central Bank of Kosovo. (2021). Quarterly assessment of the financial system. Department of Economic Analysis and Financial Stability. Prishtine: Central Bank of the Republic of Kosovo. https://bqk-kos.org.

[14] Central Bank of Kosovo. (2020). Financial stability report. Central Bank of Kosovo, Department of Economic Analysis and Financial Stability. Prishtine: Central Bank of Republic of Kosovo. https://www.bqk-kos.org.

[15] Central Bank of Kosovo. (2021). Stability Financial Report. Central Bank of Republic of Kosovo, Prishtina.

[16] Trujillo-Ponce, A. (2013). What determines the profitability of banks? Evidence from Spain. Accounting & Finance, 53(2): 561-586. https://doi.org/10.1111/j.1467-629X.2011.00466.x

[17] Socol, A., Danuletiu, A.E. (2013). Analysis of the romanian banks'performance through roa, roe and non-performing loans models. Annales Universitatis Apulensis: Series Oeconomica, 15(2): 594.

[18] Javaid, S., Anwar, J., Zaman, K., Ghafoor, A. (2011). Determinants of bank profitability in Pakistan: Internal factor analysis. Journal of Yasar University, 23(6): 3794-3804. http://joy.yasar.edu.tr.

[19] Derbali, A. (2021). Determinants of the performance of Moroccan banks. Journal of Business and Socioeconomic Development, 1(1): 102-117. https://doi.org/10.1108/JBSED-01-2021-0003.

[20] Vong, P.I., Chan, H.S. (2009). Determinants of bank profitability in Macao. Macau Monetary Research Bulletin, 12(6): 93-113.

[21] Staikouras, C.K., Wood, G.E. (2004). The determinants of European bank profitability. International Business & Economics Research Journal (IBER), 3(6): 3699. https://doi.org/10.19030/iber.v3i6.3699

[22] Prenaj, V., Miftari, I., Krasniqi, B. (2023). Determinants of the capital structure of non-listed companies in Kosovo. Economic Studies (Ikonomicheski Izsledvania), 32(1): 36-50. https://www.iki.bas.bg/Journals/EconomicStudies/2023/2023-1/03_Vlora-Prenaj.pdf.

[23] Desai, R. (2021). Impact of priority sector lending on financial profitability: Segment wise panel data analysis of Indian banks. Management & Accounting Review (MAR), 20(1): 19-38. https://ir.uitm.edu.my/id/eprint/47752/

[24] Osuagwu, E.S. (2014). Determinants of Bank Profitability in Nigeria. http://dx.doi.org/10.2139/ssrn.4100483

[25] Ali, A., Ali, B.J. (2022). Disparity in Total Resources Growth and Its Impact on the Profitability: An Analytical Approach. Planning, 17(5): 1441-1447.

[26] Ferrouhi, E.M. (2018). Determinants of banks’ profitability and performance: An overview. Contemporary Research in Commerce and Management, 4: 61-74. https://mpra.ub.uni-muenchen.de/id/eprint/89470

[27] Kumar, V., Thrikawala, S., Acharya, S. (2021). Financial inclusion and bank profitability: Evidence from a developed market. Global Finance Journal, 53: 100609. https://doi.org/10.1016/j.gfj.2021.100609

[28] Ahmed, R., Bhuyan, R. (2020). Capital structure and firm performance in Australian service sector firms: A panel data analysis. Journal of Risk and Financial Management, 13(9): 214. https://doi.org/10.3390/jrfm13090214

[29] Roman, A., Danuletiu, A.E. (2013). An empirical analysis of the determinants of bank profitability in Romania. Annales Universitatis Apulensis: Series Oeconomica, 15(2), 580-593.

[30] Ongore, V.O., Kusa, G.B. (2013). Determinants of financial performance of commercial banks in Kenya. International Journal of Economics and Financial Issues, 3(1): 237-252.

[31] Căpraru, B., Ihnatov, I. (2014). Banks’ profitability in selected Central and Eastern European countries. Procedia Economics and Finance, 16: 587-591. https://doi.org/10.1016/S2212-5671(14)00844-2

[32] Petria, N., Capraru, B., Ihnatov, I. (2015). Determinants of banks’ profitability: evidence from EU 27 banking systems. Procedia Economics and Finance, 20: 518-524. https://doi.org/10.1016/S2212-5671(15)00104-5

[33] Abreu, M., Mendes, V. (2001). Commercial bank interest margins and profitability: Evidence for some EU countries. In Pan-European Conference Jointly Organised by the IEFS-UK & University of Macedonia Economic & Social Sciences, Thessaloniki, Greece, May, 34(2): 17-20.

[34] World Bank Group. (2016). Rebalancing for stronger growth. World Bank Group.

[35] World Bank Group. (2022). Steering Through Crises. Regular Economic Report, No.21.

[36] Anbar, A., Alper, D. (2011). Bank specific and macroeconomic determinants of commercial bank profitability: Empirical evidence from Turkey. Business and Economics Research Journal, 2(2): 139-152.

[37] Said, R.M., Tumin, M.H. (2011). Performance and financial ratios of commercial banks in Malaysia and China. International Review of Business Research Papers, 7(2): 157-169. https://doi.org/10.2139/ssrn.1663612