Eko Budi Satoto![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study aims to determine the effect of inflation, regional minimum wages, and subsidized housing costs on the purchasing power of low-income communities needing to own a home as an intervening variable. This study uses the Structural Equation Modeling (SEM) method to analyze the data from the districts of East Java, Indonesia. Broadly speaking, this study found that the higher the need to own a home, the higher the purchasing power of Low-Income Communities because the population is increasing, so the need to own a place to live is also directly proportional. The practical implication of this study is that it can contribute useful information relating to the effect of inflation, regional minimum wages, and subsidized house prices on the purchasing power of low-income communities with a need to own a house as an intervening variable. Therefore, the government needs to control the impact caused by inflation in the form of rising bank interest rates by subsidizing it so that it remains stable. In the future, the government should include housing allowances in the minimum wage component. The government should not only subsidize house prices, but also production costs, so that the price of subsidized houses remains stable.

inflation, regional minimum wages, costs of subsidized housing, a need to own a home, purchasing power of low-income communities

Home is a primary need for humans [1]. Therefore, ideally every human being or every family should have a home [2]. However, from year to year house prices are increasing. This increase in house prices is not followed by an increase in people's income [3]. With the imbalance between housing needs and the low income of this community, developers will find it difficult to sell their products, on the other hand, people with low income will find it difficult to fulfill their primary needs in the form of a house [4].

In Quarter 2 2022, the property price index in East Java reached 100.2, up 4.4 points compared to 95.8 in Quarter 1 2022. The quarter-on-quarter increase reached 4.7 percent [5]. In contrast, according to the Chairman of the DPP of the Association of Housing and Settlement Developers throughout Indonesia (Apersi) Eddy Ganefo, this decline in purchasing power has made commercial housing sales fall 75 percent [6].

In addition to the high price of housing, another factor that hinders home purchases is inflation. According to Indonesia's Finance Minister, Sri Mulyani Indrawati, with rising inflation, it will be increasingly difficult for low-income people to own a home. Of course there is a strong reason, because when there is inflation it will be followed by bank interest rates [7].

Regional Minimum Wage (UMR) is another factor that greatly affects the ability to buy a house. The higher the UMR in a region, the higher the ability of its people to buy a house. Standard house prices that are almost evenly distributed in East Java are not followed by the UMR. This has resulted in districts with low minimum wages, such as Situbondo Regency, where the minimum wage is very small, it is very difficult to match the ability of Mojokerto Regency, where the minimum wage is very large [8].

The hope of the community to be able to buy a house is with the subsidized housing program [9]. But in reality this subsidized house is also increasingly unbalanced by the basic price of the house. So that this subsidized house is still not affordable by low-income people. This is because the selling value or price of subsidized houses remains high.

The above fact is in line with several studies [10-18] which state that Inflation, UMR, and Subsidized House Prices affect the Purchasing Power of Low-Income Communities. However, there is a research gap in research [19] showing the opposite result that Inflation, UMR, and Subsidized House Prices have no effect on the Purchasing Power of Low-Income Communities.

This study contributes to the government's decision-making related to subsidized houses. Unstable world economic turmoil has resulted in recessions in several countries, including Indonesia. The recession has increased the government's basic inflation, making it more difficult for low-income people to own a home. Novelty in the study is the need to own a house as an intervening variable because the number of people's population in Indonesia is getting higher, so the need for housing is also increasing. In addition, based on the theory of national development, there is a government obligation to facilitate the community in obtaining a sense of security to live. The launch of subsidized houses is a tangible manifestation of the government's seriousness in providing convenience, especially for low-income people in owning private houses.

From the description above, the following research questions can be formulated (1) Does Inflation affect the purchasing power of low-income people? (2) Does the Regional Minimum Wage affect the Purchasing Power of Low-Income People? (3) Does the Price of Subsidized Houses affect the Purchasing Power of Low-Income People? (4) Does Inflation affect the Need to Own a House? (5) Does the Regional Minimum Wage affect the Need to Own a House? (7) Does the need to own a house affect the purchasing power of low-income people? (8) Does Inflation affect the Purchasing Power of Low-Income People through the Need to Own a House? (6) Does the price of subsidized housing affect the need to own a house? (7) Does the need to own a house affect the purchasing power of low-income people? (8) Does inflation affect the purchasing power of low-income people through the need to own a house? (9) Does the regional minimum wage affect the purchasing power of low-income people through the need to own a house? (10) Does the price of subsidized housing affect the purchasing power of low-income people through the need to own a house?

The theory of economic development is seen as a multidimensional process that involves various fundamental changes in social structures, attitudes of society, and national institutions, as well as accelerated growth, reduction of inequality, and overcoming poverty. In essence, development reflects a complete change in the social system according to various basic needs and efforts to foster the aspirations of individuals and social groups in the system. In the early stages of economic development, according to them, the relatively large ratio of government expenditures to national income. The initial stage of the government must provide various facilities and infrastructure. In the middle stage of economic development, government investment is still needed to spur growth to take off [20-24].

Inflation is the tendency of prices to rise generally and continuously. An increase in the price of one or two goods alone is not called inflation unless the increase extends to (or results in an increase in) a large part of the price of other goods. Inflation can be divided into two types based on the factors that give rise to it. Inflation occurs as a result of the level of the economy reaching the level of full labor unemployment and rapid economic growth [25]. Inflation occurs due to an increase in production costs [26-30].

Wages are something that is obtained by labor as a form of exchange for services that have been provided to the company. The minimum wage, as regulated in government regulations No. 8 / 1981, is a wage set at the regional, sectoral, and subsectoral minimum. In this case, the minimum wage is the basic wage and benefits. The minimum basic wage is a minimally regulated basic wage both regionally, sectorally, and sub-sectorally. Meanwhile, government regulations that clearly regulated only the basic wage and do not include benefits [31-35].

Several terms can express prices or costs, for example, rates, rent, interest, premiums, commissions, wages, salaries, etc. From a marketing point of view, a price is a monetary unit or another measure (including goods and services) exchanged for the right of ownership or use of a good or service. Price is the only element of the marketing mix that provides income for the company, while the other three elements are (product, distribution, and promotion) causing costs (expenses). Price is an important point in determining a company's marketing strategy because the price has a great influence on consumers' purchasing power [36-40].

Based on the Regulation of the Minister of Public Housing of the Republic of Indonesia no. 10 of 2012 article 1, a house is a building that functions as a livable residence, a means of family development, a reflection of the dignity and dignity of its occupancy and assets for its owner. A house is not only a building (structural) but also a place of residence that meets the requirements of a decent life, viewed from various aspects of people's lives. Home is understandable as a refuge to enjoy life, rest, and revel with the family. The house's inhabitants get the first impression of their life in this world. The house must guarantee the interests of the family, that is, to growth, give the possibility to live in association with its neighbors, and more than that; the house must give tranquility, pleasure, happiness, and comfort to all events of its life [41-46].

The ability to purchase power can be summed up as the capacity of consumers to buy the number of goods requested in a market with a price level at a certain income and in a certain period. Consumers with low purchasing power or relatively small incomes will tend to consume relatively cheap products with relatively small amounts in order to meet their needs due to their resources. The government has sought to obtain credit with a relatively cheap Inflation rate from the Bank. Then the cost of taking care of a very simple house certificate has been arranged according to the housing developer. To increase public affordability, the government and banks have made policies to help low-income people by providing subsidies for Home Ownership Credit Inflation [47-52].

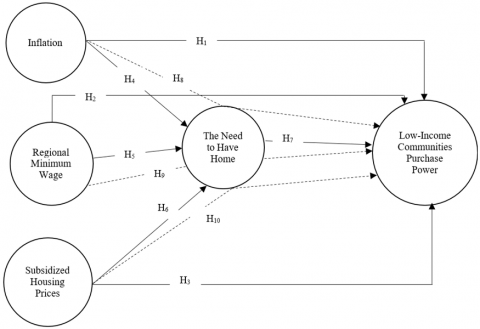

In this study, ten hypotheses will be developed. The development of this hypothesis is based on the relationship that occurs between variables. The relationship between these variables can be seen in Figure 1.

3.1 The effect of inflation on the purchasing power of low-income communities

High inflation will be a burden for all parties. With the regional minimum wage, the purchasing power of a currency becomes lower or decreases. With the decline in the purchasing power of currencies, people's ability to meet their living needs, goods, and services, will be lower. The unstable pace of the regional minimum wage will make planning difficult for the business world, not encourage people to save and invest, hinder development planning by the government, change the structure of the state budget and regional budget, and various other negative impacts that are not conducive to the overall economy. The result of the studies [41, 43, 53-55] shows that inflation affects the purchasing power of low-income people, thus,

The first hypothesis, H0: Inflation does not affect the purchasing power of low-income people, and H1: Inflation does not affect the purchasing power of low-income people.

3.2 The effect of regional minimum wage on the purchasing power of low-income communities

The demand for an increase in the minimum wage for each district every year is intended to improve the welfare of the workers. However, for companies, it is the opposite because if the minimum wage increases, the production costs incurred are quite high, so there can be inefficiencies in the company, and they will take policies to reduce the number of workers to increase the number of unemployed. The level of wages is also called the average level of work generally accepted in society for all kinds of work. The wage rate can be considered by the hour, day, week, month, or year. The result of the studies [56-60] shows that the regional minimum wage affects purchasing power of low-income people. Thus,

The second hypothesis, H0: Regional Minimum Wage does not affect the Purchasing Power of Low-Income Communities, and H1: Regional Minimum Wage affects the Purchasing Power of Low-Income Communities.

3.3 The effect of the cost of subsidized housing on the purchasing power of low-income communities

Based on the Regulation of the Minister of Public Housing of the Republic of Indonesia no. 10 of 2012, article 1 house is a building that functions as a livable place to live in, a family development facility, a reflection of the dignity of its occupants, and an asset for the owner. The price of subsidized housing is also regulated through Public Works and Human Settlements Ministerial Decree No. 242/KPTS/M/2020 concerning subsidized housing prices adjusted to the region. For the Java region, the price of subsidized housing is set at only Rp. 150.5 million, Jabodetabek Rp. 168 million. Other areas, Sumatra Rp. 150.5 million, Bangka Belitung Rp. 156.5 million, Maluku Rp. 168 million to Papua priced at Rp. 219 million. The result of the studies [40, 42, 49, 50, 61, 62] shows that subsidized house prices affect the purchasing power of low-income people. Thus,

The third hypothesis is H0: The price of subsidized housing does not affect the purchasing power of low-income people, and H1: The price of subsidized housing affects the purchasing power of low-income people.

3.4 The effect of inflation on the need to own a home

Inflation is the increase in prices generally prevailing in an economy from one period to another. Inflation can be considered a monetary phenomenon due to a decrease in the value of the monetary calculation unit of a commodity. Several adverse impacts arise from inflation, including declining economic activity, declining levels of people's prosperity, declining real income of people with fixed incomes, reducing the value of wealth in the form of money, and worsening the division of wealth. The result of the study by [41, 43, 53-55] shows that inflation affects the need to own a house. Therefore,

The fourth hypothesis, H0: Inflation has no effect on the need to own a house, and H1: Inflation affects the need to own a house.

3.5 The effect of the regional minimum wage on the need to own a home

One of the factors of subsidized housing purchase decisions is income. The high income owned by consumers will have an impact on the desire to own a home that can support their prestige and personal interests in the present and the future. Besides, ability in terms of income is also one of the main factors that can make consumers buy a house in cash or credit. The result of the studies [56-60] shows that the regional minimum wage affects the need to have a home. Thus,

The fifth hypothesis, H0: Regional Minimum Wage does not affect the need to own a house, and H1: Regional Minimum Wage affects the need to own a house.

3.6 The effect of the cost of subsidized housing on the need to own a home

Price is the only element in the marketing mix that generates sales revenue. In large companies, pricing is usually handled by divisional or product line managers. However, top management still sets goals and general policies regarding selling prices and often approves price proposals submitted by managers. The result of the studies [40, 42, 49, 50, 61, 62] shows that subsidized housing prices affect the need to own a home. Therefore,

The sixth hypothesis, H0: The price of subsidized housing does not affect the need to own a house, and H1: The price of subsidized housing affects the need to own a house.

3.7 The effect of the need to own a home on the purchasing power of low-income communities

Based on the Regulation of the Minister of Public Housing of the Republic of Indonesia no. 10 of 2012, article 1 house is a building that functions as a livable place to live in, a family development facility, a reflection of the dignity of its occupants and an asset for the owner. The price of subsidized housing is regulated through Public Works and Human Settlements Ministerial Decree No. 242/KPTS/M/2020 concerning subsidized housing prices adjusted to the region. For the Java region, the price of subsidized housing is set at only Rp. 150.5 million, Jabodetabek Rp. 168 million. Other areas, Sumatra Rp. 150.5 million, Bangka Belitung Rp. 156.5 million, Maluku Rp. 168 million to Papua priced at Rp. 219 million. The result of a studies [40, 42, 49, 50, 61, 62] shows that subsidized house prices affect on the purchasing power of low-income people. Thus,

The seventh hypothesis, H0: The price of subsidized housing affects the purchasing power of low-income people, and H1: The price of subsidized housing affects the purchasing power of low-income people.

3.8 The effect of inflation on the purchasing power of low-income communities through stock returns as an intervening variable

Inflation is a huge economic problem, especially for developing countries. The source of inflation in developing countries comes from several factors, such as the government budget deficit, which then has an impact on increasing the money supply. Judging from the main factors that cause inflation, inflation can be caused by the demand side, supply side, expectations, or a combination of these three factors. The increase in prices for goods and services continuously impacts a decrease in the value of a country's currency. It causes the purchasing power of money to become weaker. The result of the studies [12, 24, 38, 46, 47] shows that inflation affects the purchasing power of low-income people through return on shares as an intervening variable. Thus,

The eighth hypothesis, H0: Inflation does not affect the Purchasing Power of Low-Income Communities through the Need to Own a House as an Intervening variable, and H1: Inflation affects the Purchasing Power of Low-Income Communities through the Need to Own a House as an Intervening variable.

3.9 The effect of the regional minimum wage on the purchasing power of low-income communities through the need to own a home as an intervening variable

According to Article 23, paragraphs (1) and (2) of Government Regulation 36 of 2021 concerning Wages, the minimum wage is the lowest monthly wage, consisting of basic wages and non-fixed allowances. The basic wage is at least equal to the minimum wage. The minimum wage is determined based on economic and employment conditions; in other words, it is no longer based on decent living needs. The result of the studies [19, 22, 39, 63, 64] shows that the regional minimum wage affects the purchasing power of low-income communities through return on the stock as an intervening variable. Thus,

The ninth hypothesis, H0: UMR does not affect the purchasing power of low-income people through the need to own a house as an intervening variable, and H1: UMR affects the purchasing power of low-income people through the need to own a house as an intervening variable.

3.10 The effect of the cost of subsidized housing on the purchasing power of low-income communities through the need to own a home as an intervening variable

The Modest Subsidized Housing Development Program was established to expand opportunities for people to obtain housing and reduce social inequality because the price is adjusted to the purchasing power of some low-income groups. The size of a very simple house has been regulated in the Regulation of the State Minister for Public Housing Number 07/PERMEN/M/2008. Result of studies [15, 44, 45, 48, 65-67] shows that subsidized house prices affect the purchasing power of low-income people through the need to own a house as an intervening variable. Therefore,

Tenth hypothesis: H0: The price of subsidized housing does not affect the purchasing power of low-income people through the need to own a house as an intervening variable, and H1: The price of subsidized housing affects the purchasing power of low-income people through the need to own a house as an intervening variable.

Figure 1. Conceptual framework

The population in this study is cities in East Java Province in 2022. The Saturated Sample method/Census Method is used in taking the sample. It is a technique for determining a sample with all members of the population selected as the sample [68]. The reason for using this method is that there are 38 regencies/cities in East Java Province.

The following formula is used to measure inflation:

Inflation rate = Inflation – Inflation-1 (1)

The following formula is used to measure Regional Minimum Wage:

RMW = RMW t – RMW t-1 (2)

The following formula is used to measure the Costs of Subsidized Housing:

HRS = HRSt – HRSt-1 (3)

The formula used to measure the variable “A need to own a home” is the Distribution of Household Percentage According to Regency/ City and the Status of Ownership of Residential Buildings in East Java Province, as follows:

Home Status= Home Statust – Home Statust-1 (4)

The formula used to measure the variable Purchasing Power of Low-Income People is as follows:

Purchasing Power Index= Purchasing Power Index – Purchasing Power Index-1 (5)

The data analysis technique used in this study is structural equation modeling (SEM) analysis. SEM is used to cover the regression's weaknesses [69].

East Java Province is one of the centers of economic growth with a fairly high population in Indonesia, where the population has increased yearly. This increase in population growth has stimulated the growth of housing construction in East Java Province, especially small types with subsidized facilities, which can be seen from the increasing number of developers in East Java Province, totaling 32 developers who are members of the East Java REI association, the Jember Commissariat. The City Planning System implemented in East Java Province provides many opportunities for developers to work together to build properties, in this case, houses. This development makes it easier for people to find a place to live. Therefore, a consumer must be selective in choosing a developer. The need for housing is, of course, inseparable from the trend of population growth and the provision of housing based on the number of houses. Development progress (economic) of East Java Province is a relatively high growth rate, where in 2021 it will reach 3.61% and in 2022 it will reach 5.58% so that the average is above national growth.

After analyzing the research data, the next stage is to process descriptive statistical data of research variables. The results of the descriptive statistical data processing of research variables appear in Table 1.

The inflation variable shows an average value (mean) of 0.62. The lowest value of inflation is -0.16, and the highest is 1.44. The standard deviation is 0.43. The regional minimum wage variable shows an average value (mean) of 2,501,048. The lowest value of the regional minimum wage variable is 1,850,671, and the highest value is 4,375,479. The standard deviation is 805,140. The Subsidized House Price variable shows an average value (mean) of 149,289,474. The lowest value of the subsidized house price variable is 140,000,000, and the highest is 150,500,000. The standard deviation is 3,008,168. The variable needs to own a house shows an average value (mean) of 5.11. The lowest value of the Need to have a Home variable is 0.29, and the highest is 31.74. The standard deviation is 6.88. The purchasing power variable of low-income communities shows an average value (mean) of 0.74. The lowest value of the low-income people's purchasing power variable is 0.66, and the highest value is 0.88. The standard deviation is 0.06.

The discriminant validity test uses the cross-loading value. An indicator is declared to meet discriminant validity if the indicator's cross-loading value on the variable is the largest compared to other variables.

Table 1. Descriptive statistical results

|

Description |

Inflation |

Regional Minimum Wage |

Subsidized House Prices |

The Need to Own a Home |

Purchasing Power of Low-Income People |

|

Min |

-0.16 |

1,850,671 |

140,000,000 |

0.29 |

0.66 |

|

Max |

1.44 |

4,375,479 |

150,500,000 |

31.74 |

0.88 |

|

Mean |

0.62 |

2,501,048 |

149,289,474 |

5.11 |

0.74 |

|

Std.Dev |

0.43 |

805,140 |

3,008,168 |

6.88 |

0.06 |

Source: Processed in 2022

Based on the data presented in Table 2, it can be seen that each indicator in the research variable has a cross-loading value > Rtable. Based on the results obtained, the variables used in this study already have good discriminant validity in compiling their respective variables.

The reliability test with the composite reliability above can be strengthened by using the Cronbach alpha value if the Cronbach alpha value is > 0.7. The following is the Cronbach alpha value of each variable.

Table 2. Discriminant validity

|

Variable |

Cross-Loading Value |

Rtable |

Description |

|

Inflation (X1) |

1.000 |

0.266 |

Valid |

|

Regional minimum wage (X2) |

1.000 |

0.266 |

Valid |

|

Subsidized house prices (X3) |

1.000 |

0.266 |

Valid |

|

The need to have a home (Z) |

1.000 |

0.266 |

Valid |

|

Purchasing power of low-income people (Y) |

1.000 |

0.266 |

Valid |

Source: Processed in 2022

Table 3. Reliability test result

|

Variable |

Cronbach Alpha |

|

Inflation (X1) |

1.000 |

|

Regional minimum wage (X2) |

1.000 |

|

Subsidized house prices (X3) |

1.000 |

|

The need to have a home (Z) |

1.000 |

|

Purchasing power of low-income people (Y) |

1.000 |

Source: Processed Data, 2022

Based on the data presented in Table 3, it can be seen that the Cronbach alpha value of each research variable is > 0.7. Thus, these results indicate that each research variable has met the requirements for the Cronbach alpha value, so it can be concluded that all variables have a high level of reliability.

A multicollinearity test was conducted to determine the relationship between indicators. To find out whether formative indicators experience multicollinearity by knowing the VIF value. If VIF values are between 5 and 10, the indicator does not have multicollinearity. The following are the results of the multicollinearity test for each of the variables in this study.

Based on Table 4, the results of the multicollinearity test show that the VIF value is below 10. Therefore, there is no multicollinearity for each of the research variables.

Table 4. Variance inflation factors

|

Variable |

VIF |

|

Inflation (X1) |

1.195 |

|

Regional minimum wage (X2) |

1.307 |

|

Subsidized house prices (X3) |

1.270 |

|

The need to have a home (Z) |

1.316 |

Source: Processed Data, 2022

Based on the data processing, the results can be used to answer the hypothesis in this study. Hypothesis testing in this study was carried out by looking at the T-Statistics values and P-Values. The research hypothesis can be stated to reject the Null Hypothesis (H0) if the P-Values value <0.05. The following are the results of hypothesis testing obtained in this study through the inner model.

From the results of the research hypothesis testing model, it can be seen the direct influence and indirect influence of the relationship between variables.

The results of testing the direct influence of relationships between variables can be seen in the following Table 5.

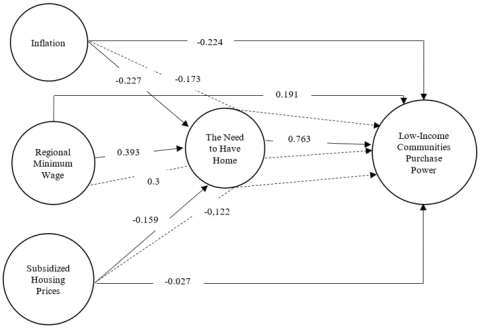

Based on the direct influence testing from Figure 2 and Table 5, it can be seen that the path coefficient of inflation on the purchasing power of low-income people is β = -0.224, which is negative. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So based on the calculated value of path coefficients and p-values on the influence relationship between variables, inflation has a significant negative effect on the purchasing power of low-income communities.

Figure 2. Test result

Table 5. Influence between variables

|

Variable |

Path Coefficients |

P-value |

Result |

|

Inflation – Purchasing power of low-income people |

-0.224 |

0.000 |

Significant |

|

Inflation – The need to have a home |

-0.227 |

0.000 |

Significant |

|

Regional minimum wage – Purchasing power of low-income people |

0.191 |

0.000 |

Significant |

|

Regional minimum wage – The need to have a home |

0.393 |

0.000 |

Significant |

|

Subsidized house prices – Purchasing power of low-income people |

-0.027 |

0.000 |

Significant |

|

Subsidized house prices – The need to have a home |

-0.159 |

0.000 |

Significant |

|

The need to have a home – Purchasing power of low-income people |

0.763 |

0.000 |

Significant |

|

Inflation – The need to have a home – purchasing power of low-income people |

-0.173 |

0.000 |

Significant |

|

Regional minimum wage – The need to have a home – purchasing power of low-income people |

0.300 |

0.000 |

Significant |

|

Subsidized house prices – The need to have a home – purchasing power of low-income people |

-0.122 |

0.000 |

Significant |

Source: Processed Data, 2022

The value of the path coefficients of inflation on the need to own a house is β = -0.227, which is negative. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So based on the calculated value of path coefficients and p-values on the influence relationship between variables, inflation significantly negatively affects the need to own a house.

The value of the regional minimum wage path coefficients on the purchasing power of low-income communities is β = 0.191, which is positive. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So, based on the calculated value of path coefficients and p-values on the influence relationship between variables, the regional minimum wage significantly positively affects the purchasing power of low-income communities.

The path coefficients of the regional minimum wage on the need to own a house are β = 0.393, which is positive. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So, based on the calculated value of path coefficients and p-values on the influence relationship between variables, the regional minimum wage significantly positively affects the need to own a house.

The path coefficients of subsidized house prices on the purchasing power of low-income people are β = -0.027, which is negative. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So based on the calculated value of path coefficients and p-values on the influence relationship between variables, subsidized house prices significantly negatively affect the purchasing power of low-income communities.

The path coefficients of subsidized house prices for the need to own a house are β = -0.159, which is negative. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So based on the calculated value of path coefficients and p-values on the influence relationship between variables, subsidized house prices significantly negatively affect the need to own a home.

The value of the path coefficients of the need to own a house on the purchasing power of low-income people is β = 0.763, which is positive. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So based on the calculated values of path coefficients and p-values on the influence relationship between variables, the need to own a house significantly positively affect the purchasing power of low-income communities.

The value of the path coefficients of inflation on the purchasing power of low-income people through the need to own a house is β = -0.173, which is negative. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So based on the calculated value of path coefficients and p-values on the influence relationship between variables, inflation has a significant negative effect on the purchasing power of low-income communities through the need to own a home.

The value of the regional minimum wage path coefficients on the purchasing power of low-income communities through the need to own a home is β = 0.300, which is positive. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So based on the calculated value of path coefficients and p-values on the influence relationship between variables, the regional minimum wage has a significant positive effect on the purchasing power of low-income communities through the need to own a home.

The path coefficients of subsidized house prices on the purchasing power of low-income people through the need to own a house are β = -0.122, which is negative. H0 is rejected because the p-values are less than 0.05, namely 0.000 so that H1 is accepted, which means that it shows a significant effect. So, based on the calculated value of path coefficients and p-values on the influence relationship between variables, subsidized house prices significantly negatively affect the purchasing power of low-income communities through the need to own a home.

6.1 The effect of inflation on the purchasing power of low-income communities

The results of the research hypothesis testing show that inflation significantly negatively affects the purchasing power of low-income people by looking at the significance level of 0.000. This means that the higher the inflation, the lower the purchasing power of low-income people. High inflation can weaken the economy, increase production costs, reduce investment levels, and reduce the purchasing power of people owning subsidized housing. Developers can benefit from inflation. This is achieved if the income earned is higher than production costs. Inflation has a negative effect on people's welfare because inflation affects the prices of people's needs. Inflation that occurs when income is fixed or even decreases will cause the purchase of subsidized housing to decrease. Inflation is usually followed by an increase in bank interest rates. This can cause home installments to rise, resulting in payment defaults. Therefore, people with low income will rethink buying a house. Likewise, banks will find it difficult to provide mortgages to buyers, especially those with low incomes. Therefore, the government must control inflation and the increase in bank interest rates. This can be done by subsidizing bank interest rates, so that they are stable. This is in line with studies [44-46, 70-72] shows that inflation affects the purchasing power of low-income people.

6.2 The effect of regional minimum wage on the purchasing power of low-income communities

The results of the research hypothesis testing show that the regional minimum wage significantly positively affects the purchasing power of low-income communities by looking at the significance level of 0.000. This means that the higher the regional minimum wage will increase the purchasing power of low-income communities. The regional minimum wage rate increase also means that workers' income has increased. Increased income, in turn, will increase the purchasing power of subsidized housing. According to the quantity theory, a 1 percent increase in the money growth rate causes a 1 percent increase in the inflation rate. According to Fisher's model theory, a 1 percent increase in the inflation rate causes, in turn, a 1 percent increase in the nominal interest rate. Therefore, in setting the Regional Minimum Wage, the government must consider and include housing allowances. Thus, in the future, the Regional Minimum Wage will increase so that people's needs for housing will be met. This is in line with studies [52, 55, 73-77] shows that the regional minimum wage affects on the purchasing power of low-income communities.

6.3 The effect of costs of subsidized housing on the purchasing power of low-income communities

The results of the research hypothesis testing show that subsidized house prices significantly negatively affect the purchasing power of low-income people by looking at the significance level of 0.000. This means that the higher the price of subsidized housing, the lower the purchasing power of low-income people. Price is an important supporting factor needed by subsidized housing competing with other products, where prices indicate that subsidized housing is easy to find and reach for all groups. When a subsidized house has a good price, of course, it will increase the purchasing power of subsidized houses. When the cost of producing houses rises, the government should increase the subsidization of houses, so that prices remain affordable. This is in line with studies by [14, 17, 21, 23, 28] shows that subsidized house prices affect the purchasing power of low-income people.

6.4 The effect of inflation on the need to own a home

The results of the research hypothesis testing show that inflation significantly negatively affects the need to own a home by looking at the significance level of 0.000. This means that the higher the inflation, the lower the need to own a house. In investment, the goods used to invest are very necessary. Inflation is a condition that causes prices to rise. This makes the economic situation reduce productive activities. Rising prices of building materials will cause building construction to cost a lot, so unstable inflation will affect investment in the property sector in the economy. The inflation rate can be used as an indicator to determine the economic conditions in an area. If inflation occurs, there will be an increase in the cost of producing goods, which will affect the investment climate and investment. This is in line with studies [44-46, 70-72] shows that inflation affects the need to own a house.

6.5 The effect of regional minimum wage on the need to own a home

The results of the research hypothesis testing show that the Regional Minimum Wage has a significant positive effect on the Need to Own a Home by looking at the significance level of 0.000. The higher the regional minimum, the higher the need for home ownership. The relationship is directly proportional, so if there is an increase in income, then this will result in the demand for houses being better and actually increasing. The size of one's income affects one's purchasing power, including a house. The higher the income, the more diverse the desires of consumers. This is in line with studies [52, 55, 73-77] shows that the regional minimum affects on the need to own a house.

6.6 The effect of costs of subsidized housing on the need to own a home

The results of the research hypothesis testing show that subsidized housing prices significantly negatively affect the need to own a home by looking at the significance level of 0.000. This means that the higher the price of subsidized housing, the lower the need to own a home. The development of the property sector can be seen from the movement of residential property prices. The trend of movement in residential property prices in Indonesia is reflected in the Residential Property Price Index. An increase in property prices will respond to an increase in demand. An increase in demand for credit will be followed by an increase in housing prices, as reflected in the Residential Property Price Index. Government subsidies, in addition to being given directly to house prices, should also be given to the price of construction materials. Thus inflation can still have a positive effect on the need to own a house. This is in line with studies [14, 17, 21, 23, 28] shows that subsidized housing prices affect the need to own a home.

6.7 The effect of the need to own a home on the purchasing power of low-income communities

The results of the research hypothesis testing show that the need to own a house significantly positively affects the purchasing power of low-income communities by looking at the significance level of 0.000. This means that the higher the need to own a house will increase the purchasing power of low-income people. Everyone, including low-income people, need the existence of decent housing. Home is a basic human need besides food and clothing. In general, the need for housing will be more difficult to fulfill than the fulfillment for clothing and food, which tend to be easier to obtain, especially for low-income communities. However, if people need houses more and more, it will motivate people to buy houses even though they have low incomes. The factor that causes low-income people to buy houses is that people get convenience from the government and developers who provide subsidies to low-income people. While another factor because the house is a primary need of society. In order for the price of subsidized housing to remain stable, subsidies to house prices and subsidies to production material prices are increased. This will make the price of subsidized housing have a positive effect on the need to own a house. This is in line with studies [40, 42, 49, 50, 61, 62] shows that subsidized house prices affect on the purchasing power of low-income people.

6.8 The effect of inflation on the purchasing power of low-income communities through the need to own a home

The results of the research hypothesis testing show that inflation significantly negatively affects the purchasing power of low-income communities through the need to own a home by looking at the significance level of 0.000. This means that the higher the inflation, the lower the purchasing power of low-income people through the need to own a house. The increase in the prices of goods and services has caused the purchasing power of low-income people to fall. The declining purchasing power of low-income people will reduce the need for housing. Conversely, if there is deflation, it means that there has been a decrease in the prices of goods and services. The decline in the prices of these goods and services has increased the purchasing power of low-income earners. This increase in people's purchasing power will impact the housing needs of low-income people. In a crisis inflation is inevitable. But its impact can be minimized by keeping bank interest rates by way of subsidies stable. This is in line with studies [27, 31, 78-80] shows that inflation affects the purchasing power of low-income people through the need to have a home.

6.9 The effect of regional minimum wage on the purchasing power of low-income communities through the need to have a home

The results of testing the research hypothesis using Smartpls show that the regional minimum wage significantly positively affects the purchasing power of low-income communities through the need to own a home by looking at the significance level of 0.000. This means that the higher the inflation, the purchasing power of low-income people will increase through the need to own a house. An increase in the wage rate can increase the demand for money with both transactional and speculative motives, so interest rates will also rise. Therefore, increasing the wage rate will increase the interest rate, assuming that the money supply remains stable. When there is an increase in interest rates, deposit and credit rates for subsidized mortgage loans also increase so that later these interest rates will affect the fluctuations in the purchasing power of low-income people through the need to own a home. This is in line with studies [30, 35, 80-83] show that the regional minimum wage affects on the purchasing power of low-income communities through the need to own a home.

6.10 The effect of costs of subsidized housing on the purchasing power of low-income communities through the need to own a home

The results of the research hypothesis testing show that subsidized house prices significantly negatively affect the purchasing power of low-income people through the need to own a house by looking at the significance level of 0.000. This means that the higher the price of subsidized housing, the lower the purchasing power of low-income people through the need to own a home. The public expects that the price of subsidized housing in Indonesia will increase in the future because the increase in housing demand/demand almost always exceeds the increase in housing supply. Subsidized house prices are considered relatively affordable by low-income people with limited purchasing power, causing a low public response (in the form of buying subsidized houses) to the expectation that house prices will tend to increase in the future. In order to stabilize the price of subsidized housing, subsidies are not only given to the price, but also to the production materials or building materials. This is in line with studies [52, 84-89] shows that subsidized house prices affect the purchasing power of low-income people through the need to own a house.

The results showed that low-income people are influenced by inflation rates related to interest rates, regional minimum wages related to financial capability, and house prices set by the government. The results showed that the regional minimum wage has a significant positive effect on the purchasing power of low-income people in owning a house. This is because the greater the regional minimum wage, the greater the ability to pay subsidized housing installments for low-income people. This research illustrates that the higher the need to own a house, the higher the purchasing power of low-income people because the population is increasing, so the need to have a place to live is also directly proportional. The results showed a significant negative effect between inflation and subsidized housing prices on the need to own a house and the purchasing power of low-income people. Meanwhile, inflation and regional minimum wage are factors that negatively affect the purchasing power of low-income people to own a house. Therefore, the government needs to control the impact caused by inflation in the form of rising bank interest rates by subsidizing it so that it remains stable. In the future, the government should include housing allowances in the minimum wage component. The government should not only subsidize house prices, but also production costs, so that the price of subsidized houses remains stable.

The practical implication of this study is that it can contribute useful information relating to the effect of inflation, regional minimum wages, and subsidized house prices on the purchasing power of low-income communities with a need to own a house as an intervening variable. This study can also provide additional information for the government concerning providing low-cost, quality housing for low-income communities. This study has limitations that affect its results, namely the focus of the study, which is still focused on one type of house, namely subsidies. A suggestion for future researchers is to expand the types of housing provision, for example, commercial housing with low-interest rates. Furthermore, it is expected that future researchers will add more research samples years in order to be able to describe conditions more concretely. For example, it uses a range of research periods to several years for the research funders or the other parties contributing to research realization.

[1] Ramadhan, A.S., Handoko, L.B. (2015). Rancang bangun sistem keamanan rumah berbasis arduino mega 2560. Techno.COM, 15(2): 117-124. https://core.ac.uk/download/pdf/35382339.pdf.

[2] Hamzah, R. (2020). Penerapan azas kekeluargaan dan keadilan pada penyelesaian kredit bermasalah pada pembiyaan perumahan di Indonesia. Journal of Economic, Bussines and Accounting, 3(2): 404-411. https://doi.org/10.31539/costing.v3i2.1141

[3] Rahayuningtyas, E.F., Rahayu, F.N., Azhar, Y. (2021). Prediksi harga rumah menggunakan general regression neural network. Jurnal Informatika, 8(1): 59-66. https://doi.org/10.31294/ji.v8i1.9036

[4] Aditya, A.M. (2013). Strategi pemasaran pembiayaan KPR syariah bersubsidi bagi masyarakat berpenghasilan rendah di bank BTN Syariah. Latifah Rizki Ramadhana, 12-26. https://digilib.uns.ac.id/dokumen/detail/63315/Strategi-Pemasaran-Pembiayaan-KPR-Syariah-Bersubsidi-bagi-Masyarakat-Berpenghasilan-Rendah-di-Bank-BTN-Syariah.

[5] Pasar Properti Q2 2022 Kembali Bergairah, Terutama Rumah Di Jawa Timur. (2022). https://www.rumah.com/areainsider/jawa-timur/article/rumah-di-jawa-timur-15118, accessed Apr. 19, 2023.

[6] Supriyadi, E. (2017). Penurunan Daya Beli Guncang Sektor Perumahan. https://ekonomi.republika.co.id/berita/osvb9o368/penurunan-daya-beli-guncang-sektor-perumahan.

[7] Ika, A. (2022). Sri mulyani: Jika Inflasi Tinggi, Masyarakat Semakin Sulit Beli Rumah. https://money.kompas.com/read/2022/07/06/203000226/sri-mulyani--jika-inflasi-tinggi-masyarakat-semakin-sulit-beli-rumah-, accessed on Apr. 19, 2022.

[8] Mutia, A. (2022). Daftar Lengkap UMK Jawa Timur 2023, Surabaya Terbesar. https://databoks.katadata.co.id/datapublish/2022/12/08/daftar-lengkap-umk-jawa-timur-2023-surabaya-terbesar, accessed on Apr. 19, 2023.

[9] Widyastuti, E., Handayani, S. (2013). Analisis faktor-faktor yang mempengaruhi keputusan pembelian rumah subsidi dengan menggunakan analisis regresi. Prosiding Seminar Nasional Statistika, 111-121. http://eprints.undip.ac.id/40289/1/A06_Erni_Widiastuti.pdf

[10] Chapman, B., Lindenmayer, D.B. (2019). A novel approach to the sustainable financing of the global restoration of degraded agricultural land. Environmental Research Letters, 14(12). https://doi.org/10.1088/1748-9326/ab5deb

[11] Fransisca, J., Ahalik, A. (2021). Effect of PSAK 72 implementation in property and real estate’s financial health. Research in Management Accounting & Control, 4(2): 106-117. https://doi.org/10.33508/rima.v4i2.3529

[12] Jovanka, P., Goran, K., Ć., Goran, J., Dragan, M. (2020). Uncertainty in SMEs’ assessment of coronavirus pandemic risk impact on agri-food sector in Western Balkans. Ekonomika Poljoprivrede, 67(2): 445-460. https://doi.org/10.5937/ekopolj2002445P

[13] Khomutenko, A. (2020). Quantification of the economic effect from the management of state finance of Ukraine. World Financial Review, 4(65): 69-86. https://doi.org/10.35774/sf2020.04.069

[14] Leombroni, M., Piazzesi, M., Schneider, M., Rogers, C. (2021). Inflation and the price of real assets. NBER Working Paper No. 26740. https://doi.org/10.2139/ssrn.3535330

[15] Malik, M.A.S., Zafar, M., Ullah, S., Ullah, A. (2021). Role of behavioral biases in real estate prices in Pakistan. Real Estate Management and Valuation, 29(1): 41-53. https://doi.org/10.2478/remav-2021-0005

[16] Neupane, P.C. (2021). Tourism governance in the aftermath of COVID-19: A case study of Nepal. Gaze Journal of Tourism and Hospitality, 12(1): 44-69. https://doi.org/10.3126/gaze.v12i1.35676

[17] Tufail, S., Batool, S. (2013). An analysis of the relationship between inflation and gold prices: Evidence fromPakistan. Lahore Journal of Economics, 18(2): 1-35. https://doi.org/10.35536/lje.2013.v18.i2.a1

[18] Zhang, J., Leoncini, R., Tsai, Y. (2018). Intellectual property rights protection, labour mobility and wage inequality. Economic Modelling, 70: 239-244. https://doi.org/10.1016/j.econmod.2017.11.006

[19] Segarra-Oña, M. del V., Peiró-Signes, Á., Verma, R., Miret-Pastor, L. (2012). Does environmental certification help the economic performance of hotels? Evidence from the Spanish hotel industry. Cornell Hospitality Quarterly, 53(3): 242-256. https://doi.org/10.1177/1938965512446417

[20] Ng, K.F., Lo, H.K., Huai, Y. (2017). Robust public-private partnerships for joint railway and property development. Frontiers of Engineering Management, 4(4): 437-450. https://doi.org/10.15302/j-fem-2017068

[21] Balk, B.M., Rambaldi, A.N., Rao, D.S.P. (2022). Macro-economic measures for a globalized world: Global growth and inflation. Macroeconomic Dynamics, 26(2): 314-360. https://doi.org/10.1017/S1365100520000152

[22] Kaluge, D. (2019). Multifactor on macroeconomic fundamentals to explain the behavior of sectoral indices in the Indonesian stock exchange. Entrepreneurship and Sustainability Issues, 7(1): 44-51. https://doi.org/10.9770/jesi.2019.7.1(4)

[23] Lee, H.K.N. (2021). International Real Estate Review. International Real Estate Review, 24(2): 221-251. https://doi.org/10.53383/100321

[24] Meneses, Y.E., Flores, R.A. (2016). Feasibility, safety, and economic implications of whey-recovered water in cleaning-in-place systems: A case study on water conservation forthe dairy industry. Journal of Dairy Science, 99(5): 3396-3407. https://doi.org/10.3168/jds.2015-10306

[25] Sukirno, S. (2016). Makro Ekonomi Teori Pengantar. PT. Rajawali Pers.

[26] Tanrıvermiş, H. (2020). Possible impacts of COVID-19 outbreak on real estate sector and possible changes to adopt: A situation analysis and general assessment on Turkish perspective. Journal of Urban Management, 9(3): 263-269. https://doi.org/10.1016/j.jum.2020.08.005

[27] Eze, U.C., Lim, Y.Y. (2013). Indicators in the purchase of housing properties. Journal of Southeast Asian Research, 2013: Article ID 432043. https://doi.org/10.5171/2013.432043

[28] Magweva, R., Sibanda, M. (2020). Inflation and infrastructure sector returns in emerging markets—panel ARDL approach. Cogent Economics & Finance, 8: Article ID 1730078. https://doi.org/10.1080/23322039.2020.1730078

[29] Mpakaniye, J.P. (2019). Effect of temporary differences on deferred tax in the banking sector in Rwanda. SSRNElectronic Journal. https://doi.org/10.2139/ssrn.3358577

[30] Okon, E.O. (2018). Poverty in Nigeria: A social protection framework for the most vulnerable groups of internally displaced persons. American International Journal of Social Science Research, 2(1): 66-80. https://doi.org/10.46281/aijssr.v2i1.169

[31] Bao, W., Tao, R., Afzal, A., Dördüncü, H. (2022). Real estate prices, inflation, and health outcomes: Evidence from developed economies. Frontiers in Public Health, 10: 1-6. https://doi.org/10.3389/fpubh.2022.851388

[32] Benigno, P., Nisticò, S. (2020). Non-neutrality of open-market operations. American Economic Journal: Macroeconomics, 12(3): 175-226. https://doi.org/10.1257/mac.20180030

[33] Cheng, Y., Liu, C., Yang, H., Zhang, H. (2021). The structure of commercial forests “tending to become economic forests”: An analysis of causes based on labor cost effects and relative-revenue effects. Scientia Silvae Sinicae, 57(7): 184-193. https://doi.org/10.11707/j.1001-7488.20210720

[34] Lopez, L.A., Yoshida, J. (2022). Estimating housing rent depreciation for inflation adjustments. Regional Science and Urban Economics, 95: Article ID 103733. https://doi.org/10.1016/j.regsciurbeco.2021.103733

[35] Peralta, S., dos Santos, J.P. (2020). Who seeks reelection: Local fiscal restraints and political selection. Public Choice, 184: 105-134. https://doi.org/10.1007/s11127-019-00702-7

[36] Cao, J., Huang, B., Lai, R.N. (2015). On the effectiveness of housing purchase restriction policy in China: A difference in difference approach. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2584275

[37] Cohn, S. (2021). The Tax Revolt. In All Societies Die. Cornell University Press. https://doi.org/10.7591/cornell/9781501755903.003.0029

[38] Haeba, A.A., Umar, A., Asis, M., Makassar, A. (2021). The influence of the level of public awareness and public understanding of the rules on the achievement of locally generated revenue (PAD) targets through the property tax (PBB) collection process. In Proceedings of the International Conference on Industrial Engineering and Operations Management, pp. 3756-3763.

[39] Li, L., Wan, W.X. (2021). The effect of expected losses on the Hong Kong property market. Journal of Real Estate Finance and Economics. https://doi.org/10.1007/s11146-021-09851-3

[40] Sumirat, E., Nidar, S.R.,Herwany, A., Wiryono, S.K. (2020). Risk impact besides capital structure and investment valuation into public housing project’s investment rate. Academy of Strategic Management Journal, 19(5): 1-11.

[41] Ma, L., Liu, H.J., Edwards, D.J., Sing, M.C.P. (2021). Housing price dynamics on residential construction: A case study of the Australian property sector. Structural Change and Economic Dynamics, 59: 525-532. https://doi.org/10.1016/j.strueco.2021.10.001

[42] Bhattacharjee, A., Bhowmik, M., Chiranjit, P., Das Chowdhury, B., Debnath, B. (2021). Rubber tree seed utilization for green energy, revenue generation and sustainable development – A comprehensive review. Industrial Crops and Products, 174: Article ID 114186. https://doi.org/10.1016/j.indcrop.2021.114186

[43] Gotama, K.R., Anastasia, N. (2021). The impact of Corona Virus Disease 2019 (COVID-19) on Indonesia Property Stock Index. Petra IJBS International Journal of Business Studies, 4(2): 85-96. https://doi.org/10.9744/ijbs.4.2.85-96

[44] Ngangnchi, F.H., Joefendeh, R. (2021). External debt, public investment and economic growth in Cameroon. International Journal of Finance Research, 2(4): 260-273. https://doi.org/10.47747/ijfr.v2i4.461

[45] Ngangnchi, F.H., Joefendeh, R., Innocent, L. (2022). External debt, public investment and economic growth in Cameroon. International Journal of Economics and Financial Research, 8(1): 23-29. https://doi.org/10.32861/ijefr.81.23.29

[46] Pienaar, W.J. (2019). Guidelines for the choice of road projects by government. Tydskrift vir Geesteswetenskappe, 59(1): 126-141. https://doi.org/10.17159/2224-7912/2019/v59n1a9

[47] Bilousova, O.S. (2019). Assessing the impact of tax reforms on the long-term sustainability of public finances. Statistika Ukrainy, 86(3): 25-37. https://doi.org/10.31767/su.3(86)2019.03.03

[48] Chau, K.W., Lai, L. W.C., Liang, J., Ng, F.F., Wong, K.T. (2021). The negative impact of public sector-led redevelopment projects on the prices of old and new housing units in high density urban areas. International Journal of Construction Management, 21(11): 1156-1164. https://doi.org/10.1080/15623599.2019.1604113

[49] Demko, V.S. (2020). Economic influence of multiplicative effect of investment charges of industry of tourist services. Scientific Bulletin of Polissia, 2(21): 145-154. https://doi.org/10.25140/2410-9576-2020-2(21)-145-154

[50] Mlambo, C. (2022). Politics and the natural resource curse: Evidence from selected African states. Cogent Social Sciences, 8: Article ID 2035911. https://doi.org/10.1080/23311886.2022.2035911

[51] Ross, J.M. (2018). The Effect of Property Reassessments on Fiscal Transparency and Government Growth: Evidence from Virginia. Mercatus Working Paper. https://doi.org/10.2139/ssrn.3211643

[52] Ross, J.M., Mughan, S. (2018). The effect of fiscal illusion on public sector financial management. Public Finance Review, 46(4): 635-664. https://doi.org/10.1177/1091142116676360

[53] Atreya, A., Czajkowski, J. (2019). Graduated flood risks and property prices in galveston county. Real Estate Economics, 47(3): 807-844. https://doi.org/10.1111/1540-6229.12163

[54] Porumb, V.A., Maier, G., Anghel, I. (2020). The Impact of Building Location on Green Certification Price Premiums: Evidence from Three European Countries. Journal of Cleaner Production, 272: 122080. https://doi.org/10.1016/j.jclepro.2020.122080

[55] Prakash, K.B., Abimannan, K.J., Sudhagar, P., Divyabharath, P., Rajesha, S.K., Mohan, M.S. (2021). Influence of fiber volume and fiber length on thermal and flexural properties of a hybrid natural polymer composite prepared with banana stem, pineapple leaf, and s-glass. Advances in Materials Science and Engineering, 2021(6329400): 1-11. https://doi.org/10.1155/2021/6329400

[56] Chang, B.H., Sharif, A., Aman, A., Suki, N.M., Salman, A., Khan, S.A.R. (2020). The asymmetric effects of oil price on sectoral islamic stocks: New evidence from quantile-on-quantile regression approach. Resources Policy, 65: 101571. https://doi.org/10.1016/j.resourpol.2019.101571

[57] Hsu, S.H., Chen, T.J., Lin, S.Y., Chang, C.O. (2020). Did housing prices drop dramatically after the Kaohsiung gas explosions? Academic Economic Papers, 48(1): 33-68.

[58] Sanderson, D.C., Shakurina, F., Lim, J. (2019). The impact of sale and leaseback on commercial real estate prices and initial yields in the UK. Journal of Property Research, 36(3): 245-271. https://doi.org/10.1080/09599916.2019.1642370

[59] Tajani, F., Morano, P., Torre, C.M., Di Liddo, F. (2017). An Analysis of the Influence of Property Tax on Housing Prices in the Apulia Region (Italy). Buildings, 7(3): 67. https://doi.org/10.3390/buildings7030067

[60] Yen, B.T.H., Mulley, C., Shearer, H., Burke, M. (2018). Announcement, construction or delivery: when does value uplift occur for residential properties? Evidence from the gold coast light rail system in Australia. Land use policy, 73: 412-422. https://doi.org/10.1016/j.landusepol.2018.02.007

[61] Motoryn, R.М., Motoryna, Т.М., Prykhodko, К.R. (2021). How the structure of GDP of ukraine responded to COVID-19. Statistics of Ukraine, 92(1): 16-25. https://doi.org/10.31767/su.1(92)2021.01.02

[62] Kamau, S., Barrios, E., Karanja, N.K., Ayuke, F.O., Lehmann, J. (2017). Spatial variation of soil macrofauna and nutrients in tropical agricultural systems influenced by historical charcoal production in South Nandi, Kenya. Applied Soil Ecology, 119: 286-293. https://doi.org/10.1016/j.apsoil.2017.07.007

[63] Laurini, M.P., Mauad, R.B., Aiube, F.A.L. (2020). The impact of co-jumps in the oil sector. Research in International Business and Finance, 52: 101197. https://doi.org/10.1016/j.ribaf.2020.101197

[64] Damoah, I.S., Mouzughi, Y., Kumi, D.K. (2020). The effects of government construction projects abandonment: Stakeholders’ perspective. International Journal of Construction Management, 20(5): 462-479. https://doi.org/10.1080/15623599.2018.1486172

[65] Dent, P. (2019). Local Authority Property Management: Initiatives, Strategies, Re-Organisation And Reform (1st ed.). London: Routledge. https://doi.org/ 10.4324/9780429432873-6

[66] Gautam, A., Lodha, G., Potdar, K., Mohanty, B., Vadera, M.L. (2020). Comprehensive reality screening of GST in real estate sector of India. Journal of Talent Development and Excellence, 12(3s): 1193-1204.

[66] Chang, B.H., Sharif, A., Aman, A., Suki, N.M., Salman, A., Khan, S.A.R. (2020). The asymmetric effects of oil price on sectoral islamic stocks: New evidence from quantile-on-quantile regression approach. Resources Policy, 65: 101571. https://doi.org/10.1016/j.resourpol.2019.101571

[68] Ghozali, I. (2018). Aplikasi Analisis Multivariate Dengan Program IBM SPSS 25. Semarang: Universitas Diponegoro.

[69] Ghozali, I. (2014). Structural Equation Modeling Metode Alternatif dengan Partial Least Square (PLS) (4th ed.). Semarang: Universitas Diponegoro.

[70] Aduwo, G.A., Olayeye, O.O. (2019). Effects of international public sector accounting standards on financial accountability in Nigeria public sector. European Journal of Accounting, Auditing, and Finance Research, 7(3): 41-54.

[71] Azizov, A. (2021). Innovation development and entrepreneurship management in tourism of Azerbaijan: Current trends and priorities. Marketing and Management of Innovations, 4: 104-120. https://doi.org/10.21272/mmi.2021.4-09

[72] Kimani, E.N., Kuria, B.T., Ngigi, M.M. (2021). Analysis of spatial factors affecting rental house prices: A case study of Nyeri Town Constituency, Kenya. Journal of Geosciences and Geomatics, 9(3): 110-123. https://doi.org/10.12691/jgg-9-3-2

[73] Lupenko, Y. (2021). Theoretical and methodological support of economic development of agricultural sector and rural areas. Ekonomika APK, 320(6): 6-15. https://doi.org/10.32317/2221-1055.202106006

[74] Zoria, O., Yasnolob, I., Galych, O., Cherchatyi, O., Tiutiunnyk, Y., Tiutiunnyk, S., Dugar, T., Kalian, O., Mokiienko, T. (2022). Theoretical and methodological principles of investment support for innovation-oriented development of agrarian production. Journal of Environmental Management and Tourism, 12(3): 695-706. https://doi.org/10.14505/jemt.v13.3(59).10

[75] Snieska, V., Venckuviene, V., Masteikiene, R. (2016). The prognostics for credit shocks (financial crisis) and insights for mitigating consequences. Engineering Economics, 27(1): 47-55. https://doi.org/10.5755/j01.ee.27.1.9533

[76] Ekemode, B.G. (2021). A fresh look at the inflation-hedging attributes of residential property investments in emerging markets: Evidence from Nigeria. Property Management, 39(3): 419-438. https://doi.org/10.1108/PM-03-2020-0020

[77] Tham, K.W., Said, R., Adnan, Y. (2021). The dynamic relationship between inflation and non-performing property loans in Malaysia. Journal of Surveying, Construction and Property, 12(1): 36-44. https://doi.org/10.22452/jscp.vol12no1.4

[78] Cohen, V., Burinskas, A. (2020). The evaluation of the impact of macroeconomic indicators on the performance of listed real estate companies and reits. Ekonomika, 99(1): 79-92. https://doi.org/10.15388/ekon.2020.1.5

[79] Doan, T.T.T. (2020). Profitability of real estate firms: Evidence using GMM estimation. Management Science Letters, 10: 327-332. https://doi.org/10.5267/j.msl.2019.8.038

[80] Malmendier, U. (2021). Exposure, experience, and expertise: Why personal histories matter in economics. NBER Working Paper No. w29336. https://doi.org/10.2139/ssrn.3935524

[81] López-Santana, M., Rocco, P. (2021). Fiscal federalism and economic crises in the United States: Lessons from the COVID-19 pandemic and great recession. Publius: The Journal of Federalism, 51(3): 365-395. https://doi.org/10.1093/publius/pjab015

[82] Malmendier, U. (2021). FBBVA lecture 2020 exposure, experience, and expertise: Why personal histories matter in economics. Journal of the European Economic Association, 19(6): 2857-2894. https://doi.org/10.1093/jeea/jvab045

[83] Shazmin, S.A.A., Sipan, I., Sapri, M., Ali, H.M., Raji, F. (2017). Property tax assessment incentive for green building: Energy saving based-model. Energy, 122: 329-339. https://doi.org/10.1016/j.energy.2016.12.078

[84] Fedosov, V., Tymchenko, O., Babichenko, V. (2019). Tax transformations effects. Financial and Credit Activity: Problems of Theory and Practice, 2(29): 462-475. https://doi.org/10.18371/fcaptp.v2i29.172216

[85] Lien, N. P. (2018). How does governance modify the relationship between public finance and economic growth: A global analysis. VNU Journal of Economics and Business, 34(5E). https://doi.org/10.25073/2588-1108/vnueab.4165

[86] Martin, C., Hulse, K., Pawson, H. (2018). The changing institutions of private rental housing: An international review. AHURI Final Report No. 292. Australian Housing and Urban Research Institute Limited, Melbourne. https://doi.org/10.18408/ahuri-7112201

[87] Pallavi, V. (2018). An incidence of property tax-A case study of effect on real estate sector in Mysore city. International Journal of Civil Engineering and Technology, 9(2): 340-348.

[88] Parambath, Z., Udawatta, N. (2017). A framework for property developers to survive in a recession. In AUBEA 2017: Australasian Universities Building Education Association Conference 2017, pp. 411-418. https://doi.org/10.29007/cfr2

[89] Tsvakirai, C. (2017). The role of plant breeders’ rights in an evolving: Peach and nectarine fresh fruit sector. South African Journal of Science, 113(7/8): 1-6. https://doi.org/10.17159/sajs.2017/20160339