Elena A. Fedchenko*![]() | Lyubov V. Gusarova

| Lyubov V. Gusarova![]() | Anastasia A. Lysenko

| Anastasia A. Lysenko![]() | Inna M. Vankovich

| Inna M. Vankovich![]() | Lubov A. Chaykovskaya

| Lubov A. Chaykovskaya![]() | Natalya V. Savina

| Natalya V. Savina![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This article aims to develop a new methodology for auditing national projects in the Russian Federation. The authors analyzed eight reports of control and accounting bodies and concluded that they lack information on assessing indicators, criteria, and effectiveness of national projects. To address this, the authors used the PMBOK approach to assess the audit results and developed a matrix for quality planning indicators and achieving project goals and results, as well as a compliance matrix for information and analytical support. The study formed an integrated approach, including strategic audit, performance audit, financial audit, and compliance audit. Limitations of the study include the complexity of national projects, which may affect the depth of analysis. Future research could explore using new technologies and adapting the methodology to changing conditions.

audit of national projects, national project audit stages, quality of project audit, supreme audit institutions, sustainable development goals

In 2015, the UN approved a common program to achieve peace and prosperity for all the people of the planet. As part of the program, an “action plan for people, planet, and prosperity” was developed, which includes 17 sustainable development goals (SDGs) and 169 targets aimed at stimulating economic growth, social inclusion, and environmental protection [1]. The implementation of these ambitious tasks rests with states, posing questions about methods to achieve SDGs and how they meet task management in the public sector. Blanc and Montero [2] highlight the need to integrate SDGs into national projects, which are presented as a project management tool in the public sector. The adaptation of SDGs to national projects can fix indicators (strategic goals) determined based on approved methodologies in national development projects. In this regard, the goals laid down in the Agenda for Sustainable Development (hereinafter referred to as the Agenda) are achieved during the implementation of national development projects. In the Russian Federation, to achieve strategic goals, state programs are developed and customized to individual events, as well as national projects and federal projects, which may be part of state projects. The implementation of state projects aims at strategic goals, while projects should help to achieve a unique result.

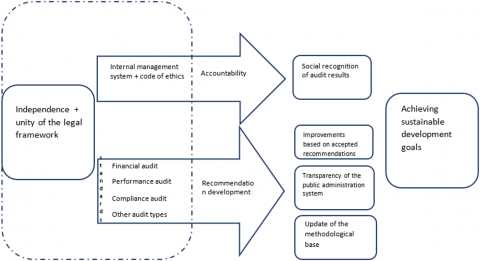

The INTOSAI Strategic Plan for 2017-2022 emphasizes the role of supreme audit institutions (SAIs) in assessing the achievement of SDGs (Figure 1).

Figure 1. The contribution of SAIs to the achievement of SDGs audit institutions [3]

Source: Compiled by the authors based on Achieving SDGs during the COVID-19 pandemic: The role of states and supreme

There is no standardized approach and unified methodology for auditing national projects. The voluntary national report compiled by the Russian SAI and presented for the first time in July 2020 at the UN Political Forum states that most of the SDGs are to some extent embedded in strategic and program documents of the Russian Federation and there are positive results (for example, SDG 1 “No poverty”, SDG 4 “Quality education”, and SDG 8 “Decent work and economic growth”). The Accounts Chamber of the Russian Federation claims that there is no sufficient understanding of the mechanism for achieving and managing SDGs [4]. There is no distinction between the specific impact of national projects on the expected effect from their implementation, while most of the country's budget expenditures are based on program-targeted financing (According to the Conclusion of the Accounts Chamber of the Russian Federation on the draft federal law "On the federal budget for 2022 and for the planning period of 2023 and 2024" [5], budget allocations, envisaged by the draft law for the implementation of 47 state programs, make up about 78% of the total planned budget allocations of the federal budget for 2022). There are typical problems in terms of target indicators: a significant number of indicators without planned values for the corresponding year; no actual values for several indicators; an excessive number of indicators that do not characterize the achievement of socio-economic development goals; underestimation of the predicted values of the state project indicators. The relevance of these issues remains, which is confirmed by the expert assessment of the Accounts Chamber of the Russian Federation [5], according to which “35 out of 47 state projects do not correspond to strategic planning documents”. There are many indicators and no actual values for several indicators, which hinders monitoring and making managerial decisions.

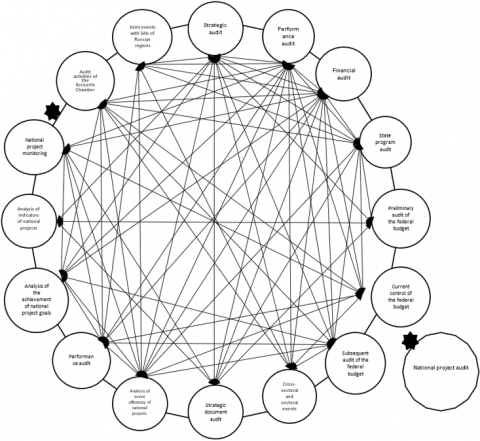

The analysis of activities of the Accounts Chamber allows forming an audit matrix for national projects (by types of activities and subject areas of the audit).

The matrix (Figure 2) proves that there is no unified approach to auditing national projects that considers all areas and stages of their implementation, including quantitative and qualitative indicators.

Figure 2. Matrix for the audit of national projects

Source: Compiled by the authors based on the official website of the Accounts Chamber of the Russian Federation [6]

The study aims at developing evidence-based proposals and improving the methods of auditing national projects used by the control and accounting bodies. As a result of the study, it was found that the current methodology is limited to two areas: the audit of the implementation of measures and the audit of the execution of budget expenditures, which does not allow for forming an objective opinion about the quality of project implementation. We believe that the process of audit and quality control of a national project should be carried out at all stages of its life cycle. This conclusion allowed us to form a fundamentally new approach to the methodology for auditing national projects. The audit of national projects should cover the following areas: the formation of the national project, its implementation, presentation, and reporting. Based on the audit results, national projects can contribute to the achievement of the national development goals of the Russian Federation and the UN SDGs for the period until 2030.

A review of the scientific literature showed that when assessing the quality of implementation of national projects, authors tend to need to audit the quality of all stages of its life cycle: planning, assessing resource and financial support, and achieving intermediate and final results.

Gasik [7] pointed out that public administration should ensure the success of national projects while emphasizing the need for their high-quality selection and initiation. Abanda et al. [8] indicated the need to determine the national contribution to the achievement of sustainable development goals. The authors claimed that national projects are complex structures and require too many criteria, which sometimes contradict each other. This cannot but create difficulties in assessing the quality of their implementation and achievement of final goals. Fernandes [9] highlighted the need to audit the effectiveness of public spending on national projects and the role of SAIs in achieving strategic and operational development goals while emphasizing the importance of such criteria as savings, efficiency, effectiveness, and the accountability of public managers responsible for achieving the targets.

The lack of consensus on how to evaluate project quality was pointed out by Prochner and Godin [10], noting the need for more careful and transparent planning of project reporting, and improved methods for assessing and discussing the above-mentioned quality.

The importance of good planning as an analytical basis for evaluating the results of each project and the feasibility of applying the theory of change in project activities were noted by Belcher et al. [11]. The authors proposed a change process model that describes and explains how the project is expected to contribute to changes. The model proposed by the authors involves the allocation of project stakeholders and a methodology for evaluating the results, which allows for determining whether there is evidence that the project was successfully implemented.

Nabawy and Khodeir [12] mentioned the extreme complexity of infrastructure projects, which makes them difficult to manage. They also noted that the lack of effective risk analysis could lead to project failures. Based on the survey of experts on risk management and achievements in risk management evaluation, Khameneh and Taher [13] proposed a conceptual framework for measuring the effectiveness of a project risk management system using SPSS software.

In the development of these approaches, the study proposes a process approach to the audit of national projects, which provides the need to control the quality at all stages of their life cycle. In addition, the recommended methodology involves assessing the degree of achievement of national development goals and the UN SDGs as a result of the implementation of a national project.

In the course of the study, we analyzed documents for 2020 and 2021, including eight reports of the control and accounting bodies of the Russian Federation on the audit of national projects in accordance with the work plan of the Accounts Chamber as part of monitoring the implementation of national projects [14-22].

These reports mainly consist of the following sections: the grounds for holding an expert-analytical event, the subject, the object, the study period, the timing, intermediate results, conclusions, and suggestions (recommendations). To assess the conclusions (reports) of SAIs of the Russian Federation based on the audit of national projects for their compliance with the project analysis stages based on the project life cycle, the PMBOK approach was used. It considers control as its separate stage. Consequently, the control function should be extended to all stages, and the life cycle of national projects should have the following form (Figure 3).

Figure 3. The supposed life cycle of a national project

Source: Compiled by the authors based on the Project Management Body of Knowledge (PMBOK) [23]

Based on the life cycle of national projects, we suggest that the audit of national projects should assess compliance in the following steps:

I. The stage of planning the budgetary expenditures of project management, including determining needs (expectations of benefits) when setting targets and indicators in accordance with national goals.

II. The stage of executing budget expenditures of project management, including determining the effectiveness, legitimacy, and target use of public resources, establishing the level of cash execution, analyzing the limits of budget obligations, and accepting budget obligations, as well as achieving the established indicators.

III. The stage of reporting on the results of project management, including reporting data on the progress of projects and their placement in the national project management subsystem of the State Integrated Information System (SIIS) “Electronic Budget”.

The analysis of the stages ensures the complete audit of projects: from development to the legality and efficiency of budgetary funds [24]. This concept contributes to the formation of a unified and end-to-end audit of strategically important projects for the socio-economic development of the budget system of the Russian Federation.

In addition to the complete coverage of the project audit, it is important to pay attention to the consistency of scorecards, criteria, and indicators that assess the project management of budget expenditures of the Russian Federation, compliance with strategic goals and needs, analysis of resource support and activities, the final result (strategic performance) caused by the implementation of the national project. In this regard, to assess the quality of planning and determine the need, a quality matrix was applied based on the criterion of strategic performance (The criterion of strategic performance is the degree of achievement (achievability) of immediate and final results, the logic for achieving immediate and final results, the significance of the final results for target groups due to the creation and functioning of the relevant immediate results. The completeness of immediate and final results, their exhaustive list, their chronology (timeliness), the risks and opportunities for obtaining can be determined.) and the result-oriented approach (A result-oriented approach is the analysis of actual or expected immediate or final results based on the establishment of criteria and deviations from them, and the formulation of recommendations aimed at ensuring that such deviations are eliminated.) used in the strategic audit of “programs, projects/quality of processes” [25]. The scheme for applying the strategic performance criterion is shown in Figure 4.

Figure 4. The scheme for applying strategic audit criteria [25]

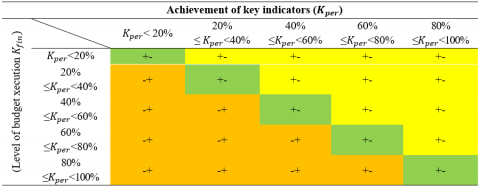

The recommended quality matrix determining the planned achievement of strategic goals was based on the qualitative and quantitative indicators of the summary of national projects, namely: the established national development goals of the Russian Federation on a par with the targets characterizing their achievement; the planned and actual values of key indicators of national projects aimed at the systematic achievement of socially significant results and tasks; the planned and spent financing of national projects within the federal budget. To establish the achievement of the key indicators of national projects, we used the performance indicator coefficient (Kper) and the coefficient of financing performance (Kfin). At the end of the financial year, the quality matrix is presented in Table 1.

Table 1. The general planning quality matrix

|

|

Key indicators fulfilled ($K_{p e r}$ ≥ 100%) |

Key indicators not fulfilled ($K_{p e r}$ < 100%) |

|

Funding fulfilled ( $K_{fin}$ = 100%) |

+ |

- (inefficient use of budgetary funds/insufficient need identification/poor quality of planning) |

|

Funding not fulfilled ($K_{fin}$ < 100%) |

+ (efficient use of budget funds – SGA 104) |

- (insufficient need identification/poor quality of planning) |

Source: Compiled by the authors

where, $K_{per}$ is the achievement of key indicators (performance ratio of indicators);

$K_{fin}$ is the level of budget execution (budget execution ratio).

To calculate such indicators as Kfin and Kper, we used the following formulas:

$K_{per}=\frac{\mathrm{F}_{ind}}{\mathrm{P}_{ind}} * 100 \%$ (1)

where, $F_{i n d}$ is the actual value of a key indicator; $P_{ind}$ is the target value of a key indicator.

$K_{f i n}=\frac{\mathrm{F}_{f i n}}{\mathrm{P}_{f i n}} * 100 \%$ (2)

where, $F_{fin}$ is the actual value of budget execution;

$P_{fin}$ is the target level of funding.

If the achievement of a non-specified key indicator is assessed, but the overall achievement of national project indicators is determined, then Kper is converted into the Kper General indicator ($O K_{per}$):

$\mathrm{O} K_{p e r}=\frac{\sum K_{p e r}}{\sum \Pi * 100 \%}$ (3)

where, $\sum \Pi$ is the number of key indicators of national projects.

The overall quality level is determined by the following formula:

$K_q=O K_{p e r} * \frac{K_{f i n}}{100}$ (4)

where, $K_q$ is the overall level of quality.

The value of $K_q$ should be one.

For the needs of assessment at the end of the financial year, a detailed planning quality matrix was compiled (Table 2).

Based on the criterion of strategic performance, this matrix allows helps better analyze the achievement/non-achievement of indicators and funding and strategic goals.

While considering the reports of the Accounts Chamber of the Russian Federation for 2020-2021, we assessed the compliance of audit objectives for each expert-analytical activity and their achievement (non-achievement). Due to the generalization of analytical materials, a matrix was compiled to achieve the goals and results of the audit of national projects (Table 3) and a matrix of compliance with the information and analytical support for the audit of national projects (Table 4).

Table 2. The detailed planning quality matrix

where,

Source: Compiled by the authors

Table 3. The matrix of achieving goals and results of the audit of national projects

|

Report |

Goals |

Goal achievement |

|

Izotova [17] |

Goal 1. Assessment of the regulatory legal and methodological framework governing the development, adjustment, monitoring, and control over the implementation of national projects |

+ |

|

Goal 2. Assessment of the expected results of the national project, the possibilities of achieving its goals, and the risks of their implementation |

+- |

|

|

Goal 3. Assessment of the progress of the national project and its actual results, including in terms of achieving the stated goals (indicators) of national projects |

+- |

|

|

Bogomolov [15] |

Goal 1. Assessment of the regulatory and methodological framework governing the development, adjustment, monitoring, and control over the implementation of national projects |

+ |

|

Goal 2. Assessment of the expected results of the national project and opportunities for achieving the goals and risks of implementing the project |

+ |

|

|

Goal 3. Assessment of the progress and the actual results obtained, including in terms of achieving the stated goals (indicators) of the national project |

+- |

|

|

Izotova [16] |

Goal 1. Analysis and assessment of the regulatory and methodological framework governing the development, adjustment, monitoring, and control over the implementation of the national project |

+- |

|

Goal 2. Assessment of the expected results of the national project, the possibility of achieving goals, and the risks of their implementation |

+ |

|

|

Goal 3. Assessment of the implementation of national projects (federal projects), as well as the actual results obtained, including in terms of achieving the goals (indicators) set |

+- |

|

|

Shilkov [21] |

Goal 1. Assessment of the development of the national project and its analysis as a document that ensures the achievement of national goals and objectives provided for by Decree No. 204 |

+ |

|

Goal 2. Monitoring the implementation of federal projects as part of the national project “Small and Medium Enterprises” |

+- |

|

|

Goal 3. Assessment of the results of the national project and its impact on the achievement of strategic goals |

+- |

|

|

Men [19] |

Goal 1. Assess the quality and sufficiency of the regulatory and methodological framework governing the implementation of national project activities “Culture”, the monitoring and control of the achievement of goals, objectives, results, and indicators of federal projects |

+ |

|

Goal 2. Assess the progress of the implementation of the national project “Culture”, as well as the actual results obtained, including in terms of the established goals and objectives |

+- |

|

|

Goal 3. Assess expected results, opportunities to achieve goals, and risks of implementing national, federal, and regional projects |

+- |

|

|

Zaytsev [22] |

Goal 1. Assessment of the regulatory and methodological framework governing the development, adjustment, monitoring, and control of the implementation of the national project |

+- |

|

Goal 2. Assessment of the expected results of the national project, the opportunities for achieving goals, and the risks of implementing the national project |

+- |

|

|

Goal 3. Assessment of the progress of implementation, as well as the actual results obtained, including in terms of achieving the stated goals (indicators) of the national project |

+- |

|

|

Bogomolov [14] |

Goal 1. Assessment of the regulatory and methodological framework governing the development, adjustment, monitoring, and control over the implementation of the Comprehensive Plan |

+ |

|

Goal 2. Assessment of the opportunities to achieve the expected results and objectives of the Comprehensive Plan |

+ |

|

|

Goal 3. Assessment of the implementation of the Comprehensive Plan, including the achievement of target indicators and established performance results |

+- |

|

|

Kaulbars and Orlova [18] |

Goal 1. Assessment of the regulatory and methodological framework (considering the changes) necessary for the implementation of the national project |

+- |

|

Goal 2. Assessment of the activities of the national project, its indicators to achieve the goals and objectives of Decree No. 204 in the field of environment and the risks of implementing the project |

+ |

|

|

Goal 3. Assessment of the progress of the national project, the effect obtained from its implementation, including in terms of achieving the stated goals and indicators, as well as the national development goals of the Russian Federation |

+- |

Source: Compiled by the authors based on the official website of the Accounts Chamber of the Russian Federation [6]

Table 4. The compliance matrix of information and analytical support for the audit of national projects

|

Report |

Analysis of the planning stage of budget expenditures and needs identification |

Analysis of the execution stage of budget expenditures |

Analysis of the reporting stage |

Strategic audit |

Financial audit |

Performance audit |

|

Izotova [17] |

+- |

+ |

- |

+- |

+ |

- |

|

Bogomolov [15] |

- |

+- |

- |

+- |

+ |

- |

|

Izotova [16] |

+- |

+ |

- |

+- |

+ |

- |

|

Shilkov [21] |

+ |

+ |

- |

+- |

+- |

- |

|

Men [19] |

+ |

+- |

- |

+- |

+- |

- |

|

Zaytsev [22] |

+- |

+ |

- |

- |

+- |

- |

|

Bogomolov [14] |

+- |

+ |

- |

+- |

+- |

- |

|

Kaulbars and Orlova [18] |

+- |

+ |

- |

+- |

+ |

+- |

Source: Compiled by the authors based on the official website of the Accounts Chamber of the Russian Federation [6]

For the study, we studied eight analytical reports of the SAI of the Russian Federation based on the audit of national projects. Based on the audit of national projects, such reports demonstrate that audit activities do not consider the stage of reporting, including interim. The planning stage of budget expenditures and the determination of needs are analyzed within a limited number of audit activities. In addition, the elements of performance audit are not given due attention. This does not allow for a comprehensive assessment of national projects with due regard to all risks and opportunities, as well as the socio-economic effect that determines the achievement of strategic goals (solution of strategic problems) and the satisfaction of needs (expected benefits) as root cause problems.

Based on the results of the analysis, the following conclusions were drawn:

– Progress reports on the implementation of national projects, as a rule, include two main areas of assessment: the implementation of measures and the execution of budget expenditures;

– Having identical goals and subjects of expert and analytical activities, all reports contain specific content caused not by the features of national projects but by different methodological approaches and subject areas of the audit;

– There is no assessment of project management, the activities of project managers and executors, the influence of external factors on the implementation of national projects, or the socio-economic effect on the achievement of the stated results based on the needs revealed (expected benefits).

It is worth mentioning that shortcomings in the reports on the audit of national projects indicate not only the absence of a unified audit methodology but also the insufficient quality of targets and tasks when carrying out relevant activities. This does not allow fully auditing national projects. The analysis of reports emphasizes the need to develop proposals for making changes to existing audit methods and, based on such proposals, to form a methodology for auditing national projects.

Based on the identified shortcomings of the analyzed reporting materials, we present methodological recommendations for drawing a report on the audit of national projects.

1. We propose to determine the goals indicated in the report in accordance with the stages of project analysis: I. The stage of planning the budgetary expenditures of project management, including determining needs (expectations of benefits) when setting targets and indicators in accordance with national goals. II. The stage of executing budget expenditures of project management, including determining the efficiency, legitimacy, and target orientation of public resources, establishing the level of cash execution, analyzing the limits of budget obligations, and accepting budget obligations. III. The stage of reporting on project management, including reporting data on the progress of projects and their placement in the national project management subsystem of the SIIS “Electronic Budget”. Each goal includes sub-goals that dwell on the directions of the audit with due regard to the specifics of national projects.

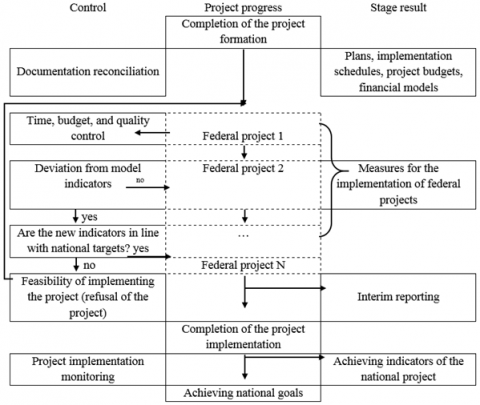

2. When achieving the goals set, it is necessary to consider the process of implementing national projects (Figure 5).

The process-based approach in the audit of national projects helps to consider each stage of their life cycle.

3. To cover the entire cycle of public resources (from project development to the final result), strategic audit, financial audit, and performance audit are applied.

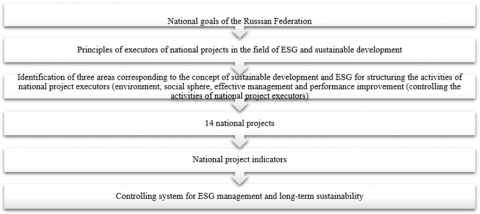

4. The assessment of project implementation should include an assessment of ESG factors (environmental, social, governance) based on the principles of environmental and social responsibility to achieve SDGs and other socially significant values, including an assessment of external and internal factors affecting the implementation of national projects. The main task of evaluating ESG factors is to determine the long-term ESG priorities that are the most significant for the processes of implementing national projects. In this regard, the implementation of national projects should be characterized by a systemic approach to integrating ESG factors and aspects of sustainable development into all areas of activity and reflected in a structure that includes elements for the effective implementation of national goals and SDGs (Figure 6).

Figure 5. The process-based approach to implementing national projects

Source: Compiled by the authors based on Novikova and Sozonova [26]

Figure 6. The structure of implementing national projects in the sphere of ESG and sustainable development

Source: Compiled by the authors based on the ESG strategy of the official website of PAO “Sberbank” [27]

The structure reflects the approach to defining socially significant goals for the integration of social, environmental, and managerial responsibility with due regard to SDGs, going down from the most significant areas, i.e., the national goals of the Russian Federation. The activities of national project performers should be based on the ESG principles for the implementation of such projects.

5. The report on the audit of national projects should include the results of applying the theory of change for the strategic audit of national projects based on the compilation of a problem tree, a list of stakeholders, a draft transformation mechanism, a map of results, assumptions and risks, as well as the formation of additional indicators (if needed). The theory of change allows identifying cause-and-effect relationships between needs and immediate results and describes “how the expenses lead to the desired immediate results and the immediate results cause the expected end results” [28].

6. Since the audit of state projects includes an analysis of their project component [29], it is possible to apply the methods for assessing the formation and implementation of state projects to national projects. In this regard, the final assessment of national projects formed and implemented based on the proposed structure (Table 5).

Table 5. The final assessment of the formation, implementation, and reporting of national projects

|

ASSESSING THE FORMATION OF THE NATIONAL PROJECT |

|||||||

|

Assessing a set of indicators... |

Assessing the stability of a set of indicators... |

Assessing the dynamics of indicators... |

Assessing the indicators..., without actual values for the fiscal year... |

Total |

|||

|

1 |

2 |

3 |

4 |

5 |

|||

|

ASSESSING THE IMPLEMENTATION OF THE NATIONAL PROJECT |

|||||||

|

Assessing the achievement of… indicators… |

Assessing the implementation of milestones... |

Assessing cash execution... |

Assessing the changes made to the consolidated budget breakdown... |

Assessing the dynamics of receivables... |

Assessing the commissioning of facilities... |

Total |

|

|

Achievement of indicators... |

For reference: the share of completed indicators... |

||||||

|

1 |

2 |

3 |

4 |

5 |

6 |

7 |

|

|

ASSESSING THE REPORTING OF THE NATIONAL PROJECT |

|||||||

|

Assessing the achievement of… indicators… |

Assessing the measures taken to minimize key risks... |

Assessing the formation of information on the achievement of indicators of the national project... |

Assessing the formation of information on financial support for the implementation of the national project |

Total |

|||

|

Socially important results... |

Tasks that are not socially significant results |

||||||

|

1 |

2 |

3 |

4 |

5 |

|||

Source: Compiled by the authors on the basis of Methodology for assessing the formation and implementation of the Russian state projects within the framework of the subsequent control over the execution of the federal budget [29]

7. The final provisions of the report should include proposals (recommendations) drawn up based on the applied audit methods, containing specific measures to achieve the established goals of the national project, national goals of the Russian Federation, and SDGs.

In the process of auditing national projects, it seems optimal to implement an integrated approach, including a strategic audit of the project component of state projects; performance audit based on an assessment of the immediate and final results of the implementation of project activities in relation to the costs incurred; financial audit aimed at verifying the legitimacy and targeted nature of the expenditures made within the framework of national projects; compliance audit based on an assessment of the compliance of project activities with established requirements.

During the planning audit, it is necessary to conclude the decision to initiate a national project. This conclusion is consistent with the conclusions of Velasquez and Hester [30], who proposed the use of multi-criteria methods in deciding whether to launch a project.

We cannot but agree with Marnada et al. [31] who emphasized the need for a more flexible, dynamic, and scalable approach to project management. The authors revealed that uncontrolled changes could potentially lead to delays and cost overruns on the project, which is significant for auditing the execution stage of a national project.

Regarding the audit of reporting data on the progress of projects (analysis of the reporting stage), Głodziński [32] believes that when evaluating the effectiveness of a project, it is necessary to use a horizontal (with an emphasis on the scope of analysis) and a vertical approach based on methodological assessment. Both approaches complement each other. The horizontal approach is associated with focusing on project stakeholders, available resources, possible methods, measures, or systems to support the project implementation, as well as the need to analyze both financial and non-financial criteria and factors for the project's success. The latter are most consistent with the goals of national projects. It is also important to assess the achievement of the desired results of the project, which complies with our conclusion about the need to assess the final result (strategic performance) as the effect of implementing the national project. However, the horizontal approach does not allow assessing the project structure that considers direct and indirect benefits and results of the national project (economic, social and environmental, etc.). This shortcoming is compensated by the vertical approach that focuses on the methodological development of assessment and includes three main areas: 1) assessment methods are built into project management methodologies/methods (PMBoK, Prince 2, APM); 2) the development of the project as an element of increasing its efficiency; 3) the project assessment process, including financial and non-financial criteria.

While describing differences in the project-based approach in the public sector, Volden and Welde [33] proposed to assess the effectiveness of a public project according to six criteria, considering the operational, tactical, and strategic levels of project success. At the operational and tactical level, it is proposed to evaluate only the effectiveness in terms of costs, time and quality, regardless of whether the project objectives are achieved. At the strategic level, the authors recommend applying such criteria as other impacts (positive and negative side effects from project implementation), relevance (preserved need for the project), sustainability (maintenance of benefits throughout the project), and benefits-costs (cost-benefit analysis). These proposals are consistent with the study results in terms of the need to conduct strategic, financial, and performance audits, which will cover the entire cycle of using public resources (from project development to obtaining the final result).

Summing up the discussion, we note that the results of our study develop and combine the conclusions of individual authors on evaluating the effectiveness of the implementation of national projects. A distinctive feature of this work is the complexity of methodological approaches to the audit of national projects. We believe that the methodology used by SAIs should include an independent assessment of the reasonable volume and timing of project expenditures (analysis of the planning stage), the results of actions and efficient use of federal and other resources (analysis of the execution stage), and the quality of reporting data on the progress of projects (analysis of the reporting stage).

Based on the study results, it was revealed that the current methodology for auditing national projects is carried out according to two main assessment areas: the realization of measures and the execution of budget expenditures. The failure to achieve the key indicators of national projects may be largely due to the insufficient quality of planning the intermediate and final results of the project and the lack of standardized approaches to assessing the risks of failure to achieve intermediate results. In reports on the implementation of national projects, there is no assessment of project management, the activities of project managers and executors, the influence of external factors on the implementation of national projects, or the socio-economic effect on the achievement of the stated results based on the needs revealed (expected benefits). These limitations do not allow fully auditing national projects.

This study aimed at determining the main directions for developing the audit methodology of national projects. As a result, we concluded that this methodology should completely cover the entire use of public resources: from the development of a national project to the final result. In this regard, audit stages are as follows: the assessment of planning quality and the execution of reporting data on the progress of the project. Such an integrated approach can become part of a strategic audit of the design part of government programs. Public authorities will receive a tool for assessing the effectiveness of the immediate and final results of the implementation of the national project activities in conjunction with the costs incurred. The methodology provides for assessing the impact of the results of the implementation of the national project on the achievement of national development goals and the UN SDGs.

The presence of limitations associated with the inability to assess all aspects of the national project may cause an incorrect assessment of the results of the audit. The way out of the situation could be the standardization of approaches to the audit of national projects of varying complexity.

Further research should determine the methods used in audit grouped by the following components: methods for organizing the audit process, including the formation of working documents/plans, developing and agreeing on criteria; methods for obtaining/requesting information; methods for generating audit evidence from the information received through its special processing and additional actions on the audited object; methods for generating final documents based on the audit results. Improving methods does not necessarily imply the development of a new method but allows enhancing the performance of methods by considering or applying new aspects.

The article is based on the studies conducted at the expense of budgetary funds under the state assignment of the Financial University on the topic “Development of a new methodology for auditing national projects”.

[1] United Nations General Assembly. (2015). https://unctad.org/system/files/official-document/ares70d1_ru.pdf, accessed on May 3, 2022.

[2] Blanc, D.L., Montero, A.G. (2020). Some considerations on external audits of SDG implementation. UN official website DESA Working Paper No. 166 ST/ESA/2020/DWP/166. https://www.un.org/ru/desa/some-considerations-external-audits-sdg-implementation, accessed on Aug. 8, 2022.

[3] Department of International and Regional Cooperation. (2020). Dostizhenie TsUR v usloviyakh pandemii COVID-19: Rol gosudarstv i vysshikh organov audita [Achieving SDGs during the COVID-19 pandemic: The role of states and supreme audit institutions]. https://ach.gov.ru/upload/pdf/Covid-19-SDG.PDF?ysclid=l7wagqwndr752907937, accessed on Apr. 30, 2022.

[4] Bakhmatova, A.K., Sarishvili, M.G. (2021). Mekhanizm dostizheniya tselei ustoichivogo razvitiya v Rossii: Problemy i puti ikh resheniya [The mechanism for achieving sustainable development goals in Russia]. Fundamentalnye Issledovaniya, 3: 12-16. https://doi.org/10.17513/fr.42973

[5] Accounts Chamber of the Russian Federation. (2021). https://ach.gov.ru/upload/iblock/6b5/ri0r740i1d07jo95gl09nzi0jocm33or.pdf.

[6] Accounts Chamber of the Russian Federation. (n.d.). Ofitsialnyi sait [The official website]. https://ach.gov.ru/, accessed on May 7, 2022.

[7] Gasik, S. (2016). National public projects implementation systems: How to improve public projects delivery from the country level. Procedia – Social and Behavioral Sciences, 226: 351-357. https://doi.org/10.1016/j.sbspro.2016.06.198

[8] Abanda, F.H., Chia, E.L., Enongene, K.E., Manjia, M.B., Fobissie, K., Pettang, U.J.M.N., Pettang, C. (2022). A systematic review of the application of multi-criteria decision-making in evaluating nationally determined contribution projects. Decision Analytics Journal, 5: 100140. https://doi.org/10.1016/j.dajour.2022.100140

[9] Fernandes, H. (2013). Performance auditing by the portuguese court of auditors. Tékhne, 11(1): 41-49. https://doi.org/10.1016/j.tekhne.2013.05.004

[10] Prochner, I., Godin, D. (2022). Quality in research through design projects: Recommendations for evaluation and enhancement. Design Studies, 78: 101061. http://dx.doi.org/10.1016/j.destud.2021.101061

[11] Belcher, B.M., Claus, R., Davel, R., Ramirez, L.F. (2019). Linking transdisciplinary research characteristics and quality to effectiveness: A comparative analysis of five research-for-development projects. Environmental Science and Policy, 101: 192-203. http://dx.doi.org/10.1016/j.envsci.2019.08.013

[12] Nabawy, M., Khodeir, L.M. (2021). Achieving efficiency in quantitative risk analysis process – Application on infrastructure projects. Ain Shams Engineering Journal, 12(2): 2303-2311. https://doi.org/10.1016/j.asej.2020.07.032

[13] Khameneh, A., Taher, A. (2016). Offering a framework for evaluating the performance of project risk management system. Procedia – Social and Behavioral Sciences, 226: 82-90. http://dx.doi.org/10.1016/j.sbspro.2016.06.165

[14] Bogomolov, V.N. (2019). Report on the interim results of the expert-analytical event "Monitoring the implementation of the comprehensive plan for the modernization and expansion of the main infrastructure for the period until 2024". https://ach.gov.ru/upload/iblock/772/77228f831f35f05e7d7f4f428665d40f.pdf.

[15] Bogomolov, V.N. (2020). Report on the interim results of the expert-analytical event "Monitoring the progress of measures of the national project "Safe and high-quality roads". https://ach.gov.ru/upload/iblock/89e/89ed0cf9644289ee6bddbfff8da78186.pdf.

[16] Izotova, G.S. (2020). Report on the interim results of the expert-analytical event "Monitoring the implementation of national project activities "Education", necessary to fulfill the tasks set in Decree of the President of the Russian Federation No. 204. https://ach.gov.ru/upload/medialibrary/news/%D0%9E%D0%B1%D1%80%D0%B0%D0%B7%D0%BE%D0%B2%D0%B0%D0%BD%D0%B8%D0%B5_2020-01-15.pdf.

[17] Izotova, G.S. (2020). Report on the interim results of the expert-analytical event "Monitoring the implementation of national project activities "Science", necessary to fulfill the tasks set in Decree of the President of the Russian Federation No. 204. https://ach.gov.ru/upload/iblock/5a5/5a58a9ddd73fefb7df5c0435b4a16d96.pdf.

[18] Kaulbars, A.A., Orlova, S.Y. (2020). Report on the results of the expert-analytical event "Monitoring the implementation of national project activities "Environment", including the timeliness of their financial support, the achievement of goals and objectives, milestones, as well as the quality of management" (with consideration of the interim report at a meeting of the Collegium of the Accounts Chamber of the Russian Federation) (additional objects of the expert-analytical event, i.e. executive authorities of 85 constituent entities of the Russian Federation are determined in the program). https://ach.gov.ru/upload/iblock/697/6974665033576448bae98baa0e9626e4.pdf.

[19] Men, M.A. (2020). Report on the results of the expert-analytical event "Monitoring the implementation of national project activities "Culture", necessary to fulfill the tasks set in Decree of the President of the Russian Federation of May 7, 2018 No. 204 "On the national goals and strategic objectives of the development of the Russian Federation for the period until 2024" (interim deadline - September 2019). https://ach.gov.ru/upload/iblock/77e/77ea0bfe2808074636b77dcdfee57569.pdf.

[20] Orlova, S. (2021). Byulleten Schetnoi palaty [The bulletin of the Accounts Chamber] No. 6(283). https://ach.gov.ru/statements/byulleten-schetnoy-palaty-6-283-2021-g.

[21] Shilkov, D. (2021). Report on the interim results of the expert-analytical event "Monitoring the implementation of the national project "Small and medium enterprises and support for individual entrepreneurial initiatives". https://ach.gov.ru/upload/iblock/7a1/smjjwo88mnis7dsqit49cg1omzgnmq5d.pdf.

[22] Zaytsev, D.A. (2020). Report on the intermediate results of the expert-analytical event "Analysis of the planning and implementation of national project activities "Labor productivity and employment support", including an assessment of the balance of goals, objectives, indicators, activities and financial resources, as well as its compliance with the long-term goals of the socio-economic development of the Russian Federation". https://ach.gov.ru/upload/iblock/316/316dfb87833f8a900e3672099f4fd75d.pdf.

[23] Project Management Institute. (2017). Rukovodstvo k Svodu Znanii po Upravleniyu Proektom (Rukovodstvo PMBOK) [A Guide to the Project Management Body of Knowledge (PMBOK guide)]. 6th ed. Project Management Institute, Newtown Square. https://biconsult.ru/files/datavault/PMBOK-6th-Edition-Ru.pdf?ysclid=l9obr5xly9253056250, accessed on Nov. 3, 2022.

[24] Stepashin, S.V. (2008). O nekotorykh zadachakh vysshikh organov gosudarstvennogo finansovogo kontrolya v usloviyakh perekhoda k novomu kachestvu upravleniya razvitiem [On some tasks of supreme audit institutions during the transition to development management of new quality]. https://www.iep.ru/files/text/other/05_stepa.pdf, accessed on May 4, 2022.

[25] Accounts Chamber of the Russian Federation. (2020). Standart vneshnego gosudarstvennogo audita (kontrolya). SGA 105. Strategicheskii audit (utv. postanovleniem Kollegii Schetnoi palaty Rossiiskoi Federatsii ot 10.11.2020 No. 17PK) [The Standard of external state audit (control). SGA 105. The Strategic audit (approved by the Collegium of the Accounts Chamber of the Russian Federation of November 10, 2020 No. 17PK)]. https://ach.gov.ru/upload/iblock/d57/d573b890bbe331d3707d2c98a4bf20f1.pdf.

[26] Novikova, O.V., Sozonova, E.E. (2021). Pokazateli otsenki rezultativnosti i effektivnosti realizatsii innovatsionnykh proektov [Indicators for evaluating the effectiveness and efficiency of the implementation of innovative projects]. Kontrolling, 3(81): 28-35.

[27] Sberbank. (2022). “Stremleniya ESG” ofitsialnogo saita PAO “Sberbank” [The ESG strategy of the official website of PAO “Sberbank”]. https://www.sberbank.com/ru/sustainability, accessed on May 17, 2022.

[28] INTOSAI. (2019). Rukovodstvo GUID 3910 - Osnovnyye kontseptsii audita dostizheniya rezul'tatov [GUID 3910 - Central concepts for performance auditing]. https://www.eurosai.org/handle404?exporturi=/export/sites/eurosai/.content/documents/others/ISSAI/Guid-3910-Central-Concepts-for-Performance-Auditing_RU.pdf, accessed on May 2, 2022.

[29] Accounts Chamber of the Russian Federation. (2022). Metodika otsenki kachestva formirovaniya i realizatsii GP RF v ramkakh osushchestvleniya posleduyushchego kontrolya za ispolneniem federalnogo byudzheta (utv. Kollegiei Schetnoi palaty RF, protokol ot 09.03.2022 No. 11K (1536) [Methodology for assessing the formation and implementation of the Russian state projects within the framework of the subsequent control over the execution of the federal budget (approved by the Collegium of the Accounts Chamber of the Russian Federation, protocol of March 9, 2022, No. 11K (1536)]. https://ach.gov.ru/upload/iblock/296/4r9ragntmtl8so7j56btl2uyuf33bw7x.pdf.

[30] Velasquez, M., Hester, P.T. (2013). An analysis of multi-criteria decision-making methods. International Journal of Operations Research, 10(2): 56-66.

[31] Marnada, P., Raharjo, T., Hardian, B., Prasetyo, A.P. (2021). Agile project management challenge in handling scope and change: A systematic literature review. Procedia Computer Science, 197(2): 290-300. https://doi.org/10.1016/j.procs.2021.12.143

[32] Głodziński, E. (2018). Project assessment framework: Multidimensional efficiency approach applicable for project-driven organizations. Procedia Computer Science, 138: 731-738. http://dx.doi.org/10.1016/j.procs.2018.10.096

[33] Volden, G.H., Welde, M. (2022). Public project success? Measuring the nuances of success through ex post evaluation. International Journal of Project Management, 40(4): 703-714. https://doi.org/10.1016/j.ijproman.2022.06.006