Daniel Mertens | Lars Klingenberger*![]() | Eric Frère | Daniel Harder

| Eric Frère | Daniel Harder![]() | Alexander Zureck

| Alexander Zureck![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This paper examines the management of environmental and social (E&S) risks within sustainable project finance. To approach this matter scientifically, a qualitative interview approach has been conducted predominantly with experts from the engaged parties of banks and project companies as part of this research. The corresponding analysis reveals that both parties use the standards for sustainability reasons and as a tool for their risk management. Moreover, growing political pressure justifies an accelerated standards application. In line with the literature, it can be confirmed that E&S standards are also introduced for reputational reasons. However, in contrast to previous findings, the relationship is perceived by the respective parties as a trusting partnership. In addition to current knowledge, there is slight disagreement over the social requirements of banks, challenging its practicability.

ESG, sustainable finance, project finance, risk management, equator principles, IFC performance standards

Countries worldwide are currently witnessing the need to address global challenges of our time, such as climate change, poverty and environment degradation [1]. As stated by the European Investment Bank, limiting world temperature increases to 2℃ – or even 1.5℃ – is still economically feasible. Yet, European Union’s climate change mitigation (CCM) investments, which amount to EUR 158 billion in 2018, are insufficient.

Especially infrastructure projects play a major role in promoting sustainability and the G20 acknowledges that it is “a key driver of economic prosperity, sustainable development, and inclusive growth” [2]. More than 60% of global greenhouse gas emissions are caused by energy, transport, building and water infrastructure sectors [3]. Announced project finance transactions have risen constantly over the last ten years. Globally, the number of projects has grown by almost 50% compared to 2015 to approx. 2,300 with a total value of $1.2 trillion in 2019, while this growth was mainly driven by an increase in renewable energy projects in developed countries [4].

However, to meet the Paris Agreement and achieve net-zero emissions in 2050 \$9.2 trillion in annual average spending on physical assets and therefore \$3.5 trillion more than today are required [5]. A G20 initiated survey found out that 95% all global projects focus on environmental sustainability and consider sustainable growth [6]. Next to the general increasing renewable energy sector, the value of Sustainable Development Goals (SDG)-relevant projects has more than doubled within one decade in developed countries, whereby non-SDG-relevant shares decreased [7].

There are several drivers for shifting toward sustainable infrastructure. Next to the pressure of climate change stated above [8], societal pressure forces the consideration of standards embedded in projects. Affected communities are demanding greater consultation in how infrastructure projects are influencing their lives. Currently, rapid change is also being driven by political forces, exemplified by the Russian invasion of Ukraine, causing the EUs ban on oil imports and seaborne oil products from Russia. Sustainable infrastructure, which according to UN’s definition, integrates ESG aspects into a project’s planning, building, and operating phase, can be the key for a successful implementation of SDG-relevant investments [9]. To foster sustainable infrastructure development, clear and global standards formulating sustainability criteria are crucial. By now, approximately 500 different sustainability standards and certificates exist [9].

Banks as financiers of infrastructure projects, might apply such standards during the lending process, as -from a bank’s perspective- sustainability and climate change related risks (e.g. climate related risks causing stranded assets) criteria are considered a credit risk. Hence, banks as lenders have begun to assess the risks associated with exposure to their loans by adopting risk management frameworks such as the Equator Principles or the IFC Performance Standards (Likewise, the novelty, high rate of adaptation and change in the very fast-moving environment of regulations and/or private sector initiatives, drive the desire for innovative research such as that conducted in this paper) [10].

Latter risk management processes follow different steps: identify the impact, evaluate, avoid, minimize, mitigate, and offset environmental and social risks in project finance transactions [11]. By following standardized approaches, involved parties of infrastructure projects gain the following benefits [9]:

• Clear and unambiguous definition of the term “sustainability and resilience”

• Project comparability

• Identification of responsible and sustainable investment opportunities among project developers, financiers, and civil society

Due to the above-mentioned rather beneficial effects of implementing sustainable frameworks into project finance, one might suggest that there is consensus among all stakeholders, including sponsors. This entire process of evaluation could ensure agreement and increase acceptance among the affected parties [11]. At the same time, unclarity concerning the agreement of stakeholders must be considered. Little is known as there is just very limited research on that specific topic. Researchers mainly focused on the following aspects of E&S frameworks:

• Financial effects of implementing sustainability frameworks

• Reasons of financial institutions for implementing E&S frameworks

• Comparison of different environment & social frameworks in project finance

• Proposals for framework adjustments

As a conclusion, the influence that E&S regulation has on sustainable project finance and the relationship between banks and project companies (PCs) has not been examined extensively. This paper aims to help to fill this research gap by getting a broader and holistic understanding of the two sides (banks and project companies) regarding E&S standards in project finance. Experiences from the past as well as current experiences are worth examining. This study is also about to explore upcoming developments both parties might illustrate in terms of sustainable project finance.

To answer this research question, expert interviews are conducted aimed to answer the following questions:

• Why are E&S standards used in project finance?

• What influence do E&S regulations have on project financing?

• What is the relationship between the bank and the project company during the application of E&S standards in sustainable project finance?

Within the expert interviews bank and project company representatives as well as a professional from the university eco system are interviewed. The research scope comprises global infrastructure projects including the water sector.

Project finance is a method of funding that can be divided into two types: non-recourse and limited-recourse structures. In the first case, lenders rely on projected cash flows that derive from the project financed (by a lender or several lenders) to repay the fund (usually a loan facility) utilized to finance the project. Contrarily, in a limited-recourse project finance lenders have an alternative mean, i.e. outside the project being financed, of securing repayments such as from a surety or from an associated project or business operation [12].

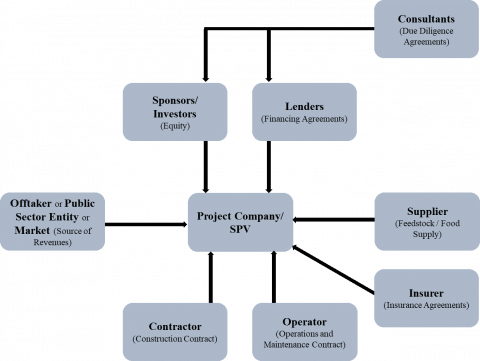

Project finance incorporates national as well as international funding for public and private projects and additionally for a combination of both, so-called public-private partnerships (PPPs) [4]. The typical structure of a project financing involves investors (one or more sponsors) and a syndicate of banks. The latter fund 70% – 80% of the project with its loans. Hence, the banking activities’ regulation significantly affects banking industry’s position on project finance through capital requirements or liquidity coverage ratios [13]. A typical (energy) project structure is demonstrated in Figure 1.

Figure 1. Structure of a typical project financing [14]

As illustrated, a project finance deal is a contractual network around the project company - also referred to as a “special purpose vehicle” (SPV). Except for the consultants, each counterparty sets up contracts with the SPV. However, each contract can include subcontracts with third parties and the provision of collateral guarantees [15]. Project financing of large projects is also characterized by the fact that many interdependencies among a few major financial institutions exist due to one underwriting bank that cooperates with other financial institutions via a consortium [16]. Project financing is further characterized by several main differences compared to corporate-based financing such as an accounting treatment, which is off-balance sheet, while business companies deal with on-balance sheets. In the case of corporate finance, the guarantees rely on the assets of the borrower. In terms of project finance, it is reduced to project assets [15]. This can also be found in the definition of project finance:

“Project financing can be defined as the financing of a project by a sponsoring firm where the cash flows of the specific project are earmarked as the source of funds from which the loan will be repaid and where the assets of the project serve as the collateral for the loan [17].”

Concerning infrastructure, large projects frequently have high socio-economic importance as finance often connects buyers and local stakeholders together in their capital or contractual structure, which might result in a conflict (e.g. offtake agreements, environmental compensation, and social programs). Local owners of resources and its territorial sovereignty are contrary to the interests of foreign exploitation [18]. On a global scale, the power industry reaches the highest project finance volume with a share of 38% of all infrastructure projects, followed by transportation (22%) and oil & gas (20%). The total project finance volume already amounted 276,950 million $ according to 2016 data [19].

Thereby, infrastructure contributes significantly to the economic situation of a national economy, signaling environmental and social requirements might have far-reaching consequences and serve as enabler for lasting change.

2.1 Socioenvironmental factors and risks

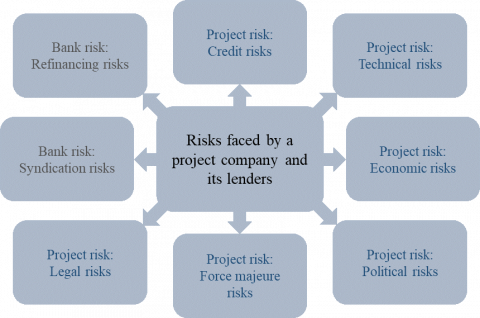

Sustainable infrastructure projects can make a decisive contribution to a better environment and social conditions. Project finance always bears specific project-related risks. Those can either be bank risks or project company risks. While syndication and refinancing risks are bank-related, credit, technical, political, or even risk of force majeure are associated with projects, illustrated in Figure 2.

Figure 2. Project finance risks [20]

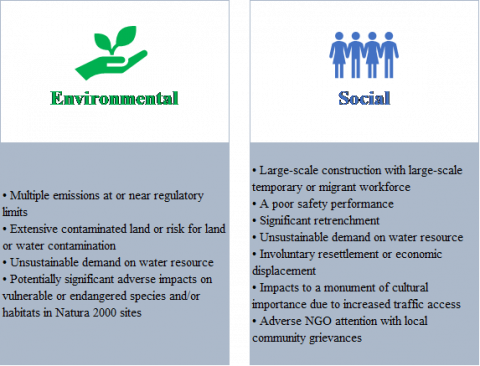

In terms of socioenvironmental factors and their related risks, firstly, one needs to understand environmental and social issues -illustrated in Figure 3- on their own. By starting with the first, such themes are multiple emissions at or near regulatory limits, extensive contaminated land, and potentially significant adverse impacts on vulnerable or endangered species or habitats. On the other hand, social considerations cover a poor safety performance, significant retrenchment, involuntary resettlement, or economic displacement [21].

Figure 3. Environmental and social related issues [21]

Consequently, these mentioned issues may become a serious risk. Interestingly, financial institutions see E&S-related risks as a material issue, especially within the banking sector. Particularly reputational risks are considered a threat since they can lead to severe damage to a company’s brand [22]. Climate-related credit risks can lower the valuation of assets and may physically lead to a higher expected default in climate-vulnerable sectors. Industries particularly affected by this are e.g. tourism and agriculture. Market risks, however in terms of E&S matters are higher energy and commodity prices. Consequently, due to significant weather disasters, credit ratings of borrowers, including sovereigns, could be downgraded [10].

2.2 Underlying tensions in sustainable project finance

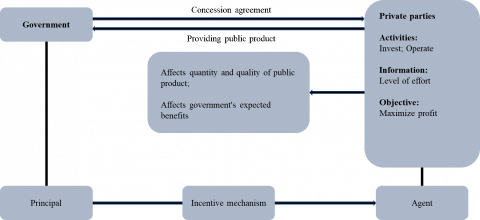

Generally, in projects, and especially in PPPs, risks must be fully assigned to and be managed for a project to succeed, regardless of who bears the risk [23]. Project stakeholders as the risk bearer may not all strive for the same project goals. Hence, as provided by the Principal-Agent Theory, as a result, there is a mismatch amongst project participants in terms of their dedication to the project’s success [24]. Even during a PPP project implementation -illustrated in Figure 4-, the government as the principal who acts as the project owner and supervisor, might not be as good informed as the project company (Agent) who is responsible for executing the project. Hence, the government can’t be sure whether aligned decisions focused on the success of the project are being made [25].

Figure 4. Principal-Agent Relationship in a PPP project [25]

This could lead to two issues: On the one hand, there are construction risks (e.g., “is the land stable?”; “Will the concrete last?”) and on the other hand, there are external factors that influence the implementation (e.g. weather conditions) [23]. While one side may evaluate a certain risk as low, the other one might know that this is an underestimation but refuses to intervene even though it would handle the risk better, i.e. forcing to save money whilst putting the project outcome at risk [24]. Another information asymmetry might occur between lenders and borrowers of capital. With their knowledge of economic sectors, regulations and market developments, banks gain a competitive advantage via information due to the extensive and efficient lending operations [26].

The Principal-Agent conflict is also applicable in terms of project contractual design. The relationship between different participants of a project is determined in detailed and via complex contracts. In the process, the risk that some will carry out activities unnoticed in order to enrich themselves grows with the number of project participants [27]. It could be avoided if contract clauses are well-developed, demonstrating expected occurrences, and allocate responsibility and risks to those who can best control them [28].

To mitigate those problems, behavior-based contracts and outcome-based contracts have been developed. When the principal can totally prescribe and monitor the agent’s acts, the first option is preferable. Given asymmetries between agent and principal, this, is not the case. In this case, the latter contract type is the one to be decided for. Project management monitoring for instance, is either not feasible or too costly. When the principle only knows the result of an agent’s work rather than the effort itself, a moral hazard occurs, and the agent may decide that it is in its best interests to limit any efforts on behalf of the principal or to prioritize other tasks [27].

Against the background of Behavioral Theory of the firm, it must first be noted that people are not perfectly rational actors. Since humans have only limited rationality, they cannot always make their decisions based on optimization criteria. Often, however, it is not the maximization criterion that plays a role, but the criterion of satisfaction [29]. In contrast, the concept of economic rationality should be described as: “Rational action can be understood as the action of an actor who, under all given conditions and situations, calculatingly adjusts his own habits of action with regard to his goals in view [30].”

The definition allows the implication that there would be no need for stable organizational structures if there were no limits to rationality [31]. This leads to the following consequences for compliance within E&S initiatives: if, for example, a company carries out a project in a country in which it has not been active before, the company’s knowledge is very likely to be incomplete or is only limited fit to local conditions. This could apply to labor law or environmental regulations and be due to limited knowledge and insufficient information. If the financing bank then imposes its requirements on the borrower (the company), the borrower might see the requirements as incompatible with its ideas, so that a conflict arises. Furthermore, information search is costly, causing managers restraining themselves from seeking alternative options when problems arise. Another reason for conflict and confusion within a firm is that sustainability is a complex topic, which is often misunderstood, and which could also lead to uncertainty and risk within a company [32].

On the other side, a bank, having not yet financed projects in a region could also stick to its generally applicable rules without adapting them (in part) to local conditions. The BTF contends that such managerial decisions are influenced based on past performance. Therefore, the Bank might stick to the information that is available and to already applied procedures. As a result, the project company may never be able to implement these requirements on the ground, as the Bank is sticking to its predefined moral standards, which are considered not feasible in some parts of the world (e.g. stakeholder participation). In this regard, the availability of local contacts for a project to advise the respective project side becomes a must, as it acts or can act rationally only to a limited extent.

Currently, many standards developed by International Finance Corporation (IFC), European Bank for Reconstruction and Development (EBRD), European Investment Bank (EIB), Asian Development Bank, various export credit agencies and others have been published, causing potential confusion for involved parties [33]. In addition to already existing platforms, several financial institutions around the world have also voluntarily created their own networks or initiatives [10]. However, it is becoming apparent that some are more likely to be applied than others. As one of the most applied ones, namely the Global Reporting Initiative Sustainability Reporting Standards (GRI), Principles for Responsible Investment (PRI) and Equator Principles (EP) are the key initiatives as displayed in Table 1 [34]. As this paper deals with project finance, investment initiatives such as PRI are less relevant. In terms of project finance, regulatory frameworks set the stage for establishing the majority of risk issues that need to be taken care of [21].

Unlike investment principles, especially the EP are highly relevant, as they compose a “voluntary code of conduct for assessing, managing and reporting environmental and social impacts in project finance” [35]. These principles are applicable, among others, for projects with total project capital costs of $10 million or more [36]. With currently 123 financial institutions from 37 countries associated with the association, the EP (developed by the IFC, a subsidiary of the World Bank) cover the majority of international project finance debt within developed and emerging markets [37]. Covering a wide-ranging content, the EP serve as guideline and framework in terms of risk management, covering the determination, assessment and management of environment and social risks in projects. In 2019, project finance transactions in emerging markets amounted to over 80% [38]. Since the EP have been limited to project finance only until 2013, the EP covers, after the EP3 revision, project-related corporate loans and bridge loans [39].

Regardless of whether these sustainable finance initiatives were developed and adopted by central banks, regulators and international development agencies (e.g. United Nations Environment Programme (UNEP) or EBRD) or by industry associations (e.g. The Equator Principles Association), it should be noted that the most common initiatives are generally increasingly aligned with each other [33]. Interestingly though, most developed countries rely on their banks’ voluntary code of conduct to promote green banking practices, with a focus on information transparency, whereas developing countries tend to utilize more regulatory techniques [10]. Furthermore, financial institutions in developed countries provide higher-quality sustainability reports and in comparison, vs. government-owned institutions, private-sector organizations have higher-quality sustainability reporting [40].

Table 1. Applied E&S initiatives by banks [34]

|

Incentives including predefined ESG definitions |

Number of responses |

|

The Global Reporting Initiative (GRI’s Sustainability Reporting Standards) |

21 |

|

Principles for Responsible Investment |

20 |

|

Equator Principles |

17 |

|

UNEP FI – Principles for Responsible Banking |

13 |

|

Natural Capital Protocol – Supplement (Finance) |

3 |

Analyzing e.g. the EP, but also the EBRD framework, it can be seen that both have adopted a set of performance requirements (EBRD) or principles (EP) with environmental and social requirements, especially for projects. The other approaches tend to describe general E&S considerations for financial transactions or create experience-sharing networks, such as the Sustainable Banking Network (SBN), which “advocates for regulators and banking associations from emerging markets to promote sustainable finance in line with international best practices” [41]. With its 38 members, the SBN represents $43 trillion (85 percent) of emerging market banking assets. These and other figures illustrate that the issue of sustainability and ESG has become more important in the financial sector and for banks particular. In both cases (EP & EBRD), each project needs to be reviewed and divided into three categories.

Category A projects are classified as having the greatest potential for social and environmental harm, with environmental and social risks and/or impacts that are multiple, irreversible, or unprecedented, while Category B projects have limited adverse social and environmental risk and/or impacts. In this case, there are few risks and impacts that are generally site-specific, largely reversible, and easily managed through mitigation measures. Where there are minimal or no adverse E&S risks and/or impacts, Category C is appropriate [36].

To understand the benefits and also the impacts of sustainability standards, it is important to first understand the potential environmental and social risks and factors that can be mitigated through appropriate frameworks and their management. The purpose of sustainability standards is to highlight the importance of the social and environmental impacts of projects to investors upfront [42, 43]. When used properly, the standards can help integrate the assessment of projects' human rights and environmental impacts into project financing. For example, if investors cannot demonstrate that the project will be built and operated in accordance with established social and environmental criteria, financial institutions that have signed and committed to the Equator Principles will not provide loans or advisory services [36]. To ensure this, the risks of projects under the umbrella of the DPs (and generally most sustainability frameworks) must follow a specific risk assessment structure, divided into the three main steps of Screening, Reviewing & Monitoring [44].

In a first step, each project proposal is classified into one of the three categories mentioned above according to the expected environmental and social impacts. The extent and scope of the environmental and social impact assessment and the public consultation are then based on the category assigned to the respective project [45].

Since the EP themselves do not state a list with projects that fall under each category, it is up to the financial institution to rate each financed project. Nevertheless, OECD’s very similar common approaches declare e.g. thermal power stations of more than 300 megawatts, construction of motorways or municipal wastewater treatment plants of more than 150,000 population equivalent to be examples of category a projects [46].

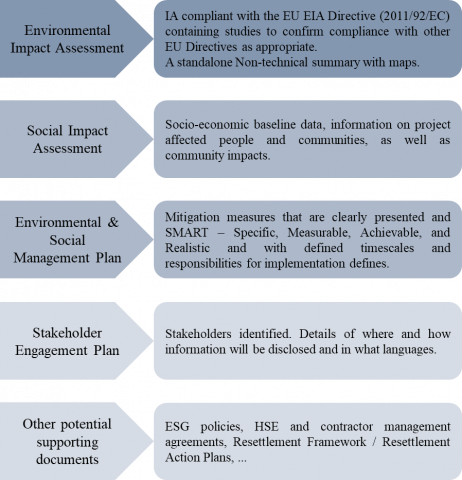

Based on these categorizations, different assessments have to be made and different documents have to be filed in order to fulfill the requirements, such as an environmental and social assessment or the implementation of an E&S management system or the demonstration of an effective stakeholder engagement in case of a category A project. In general, for projects that have the potential for significant adverse environmental and/or social impacts (Category A), the also similar EBRD PRs require steps as displayed in Figure 5. Thus, an E&S management plan with measurable mitigation measures as well as a consideration of stakeholders, including a grievance mechanism, are compulsory.

One study found that 14% of all projects were classified as Category A, 23% as Category B, and 29% as having no significant E&S impacts [47]. The remaining projects were not classified. Given that fossil energy and mining projects, which are considered the highest risk projects, account for only a quarter of all projects, it is not surprising that the number of category A and B projects is relatively small [47]. In HSBC's case, there are only two Category A projects in 2020 with a total value of \$171 million and 12 Category B projects (total value of \$938 million) of all project finance loans [48].

Figure 5. Category A projects - documentation required to meet EBRD PRs [21]

Once the appraisal is completed, the financial institutions must monitor the development of the project. Based on these results, environmental and social considerations must be included in the financing documents. To ensure continuous consideration of environmental and social aspects, the lender monitors the client's compliance with certain obligations [44].

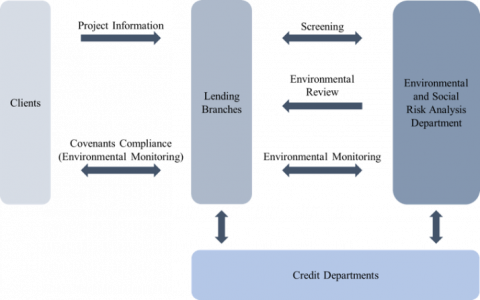

The general interactions between all involved parties of a E&S risk assessment can be illustrated as per Figure 6:

Figure 6. Flow chart of E&S risk assessment [44]

3.1 Implementation of sustainability frameworks

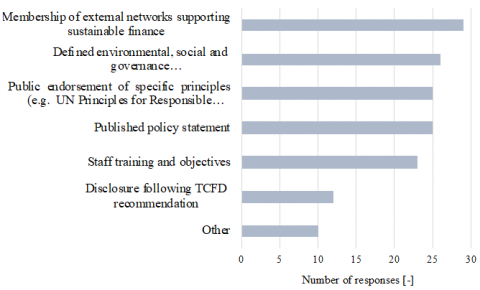

Being asked about their strategies on sustainability, most banks replied that they participate in external networks supporting sustainable finance and that they have defined their ESG objectives. In line with the membership in networks, public endorsement of specific principles ranks third [34].

The application of such sustainability frameworks is common amongst financial institutions. Most of the risk factors that should be handled in the development and implementation of a project are determined by regulatory frameworks [21]. Several reasons about what the driving forces behind those frameworks are, have been discussed in the literature. One argument is to level the playing fields for project finance when private financial institutions are involved [42]. Others argue that the development of principles combined with sharing knowledge and best practices is the objective [10]. This is illustrated in Figure 7 below.

Figure 7. Banks positioning of sustainability strategies [34]

However, one should not forget that these adoptions of codes of conduct are still voluntary. Hence, financial institutions are convinced of their reputational benefits, which result from such actions as large projects, contain high reputational risks [16]. Therefore, firms primarily use them as signaling devices for exhibiting positive credentials, intending to improve their company’s reputation and organizational legitimacy in general [49].

In terms of project finance, such frameworks are considered as very useful because of an assurance that all parties involved are in agreement and that acceptance is growing. It furthermore can substitute the old “the polluter pays” principle [11]. Especially for countries with rather weak environmental and social governance and legislation systems (referred to as non-designated countries in the EP), these standards have the ability to overcome transnational problems and regulatory failures that governments are incapable of [50].

Moreover, E&S initiatives provide banks with a precise guideline about the procedure, which is a unique characteristic of the EP [42]. This helps manage financial risks or mitigate credit risks [51]. Those guidelines are perceived as a guarantee by banks since they prove that their financed projects are conducted in a “manner that is socially responsible and reflect sound environmental management practices” [52].

Despite its many benefits, sustainability frameworks are also criticized for several reasons. Among other deprecated aspects, the lack of transparency is the most mentioned one [51, 53]. In general, the EP framework within the context of risk management practice is severely limited in terms of addressing the lender’s specific vulnerabilities to socio-environmental risks over the non-recourse credit term [54]. More specifically, the following limitations exist [51]:

Lack of transparency

Limited scope of the EPs

Lack of accountability and liability

Inadequate monitoring

Lack of implementation and enforcement

Practical failure

Sanctions (lack of proper governance mechanisms)

Exit-Door strategies

Freeriding and adverse selection

Critics of the EP argue that during the E&S impact assessment, banks and civic society continue to have disagreements about the quality and the extent of their services. Hence, a non-transparent behavior has led to an inconsistent application of the principles, which made it difficult to measure compliance levels and their impact on the ground [53].

Since only just about 5% of EPFIs publish all the information required by the EP guidelines, this impression is confirmed [35]. However, while transparency can help address behavioral biases and improve market efficiency, it is not the sole solution [55].

Besides transparency, accountability and liability are lacking when EPFIs categorize projects and judge the reporting and assessment criteria. The public cannot challenge the rating decision when, for instance, a project is rated as “B” instead of “A”, which influences the risk assessment process [56].

Despite the adoption of EP, banking practices have not effectively changed. Weak enforcement mechanisms, along with weak implementation and disclosure requirements, gave banks little incentives to fully commit to the support of a socioenvironmental-friendly project finance [16]. Moreover, it is problematic that the same banks that are leaders in EP and sustainability, including HSBC and Barclays, are also involved in the over-leveraged, risky behavior that precipitated the 2008 financial crisis [39].

In order to enhance the framework especially regarding transparency, liability and enforcement, one suggestion is to increase the enforceability of such instruments within the regulatory and prudential frameworks since the past has shown that financial institutions will not voluntarily consider profound countermeasures [10]. Another recommendation is to establish a compliance institution, similar to IFC’s Compliance Advisor/Ombudsman, which can be contacted to review non-compliance complaints [57]. Beyond that, it is recommended to give a voice to both project-affected communities and local regulators. EPFIs and borrowers could be held accountable by communities in case of failing their socioenvironmental requirements under a third-party-beneficiary theory in US contract law. The most interested party in compliance, the local society, would gain a much stronger enforcement power [58]. By inserting a provision indicating that borrowers would, when appropriate, finance technical support for local government regulators, the Equator Principles could empower local regulators [57].

3.2 Project participants and their expectations of the standards

After a critical discussion of the framework itself was presented and suggestions were given in the previous chapter, this chapter examines the participants of financed projects using E&S frameworks. Here, the relationship between the bank as the lender and the project company as the borrower are described. The starting point is the question to be answered: Why is there tension between these two parties? The answer is multifaceted. By applying E&S standards in an infrastructure project, both involved parties, the bank as the lender on the one hand and the project company as the borrower on the other hand, have their own interests, have limited rational capacities or lack certain information.

As we know, large infrastructure projects may cause adverse consequences for societies and the environment, such as resettlement of communities or deforestation, which are often linked to conflicts due to their strategic significance [59]. Therefore, potential conflicts between the two parties may arise from the following two aspects:

Different perceptions by banks and project companies regarding the interpretation of the framework

Ambiguity of the frameworks

The general starting point is the bank’s initial assessment of the environmental and social risks within its due diligence, e.g. as part of principle 2 in the EP, which is already conducted by the project company. Subsequently, the EPFI requires the client to “conduct an appropriate Assessment process […], to the EPFI’s satisfaction” [40]. This vague formulation allows room for interpretation as to when the EPFI’s satisfaction has been reached. Furthermore, because of their short-term interest in completing a project, it is clear that banks only have a limited ability to threaten to withdraw financing if borrowers persistently fail to meet their obligations [57].

Additionally, it can further be questioned to what extent banks (which are usually operating from a country other project’ region) can introduce effective measures toward the borrowing project company even if the bank itself might be committed to comply with high E&S standards [60]. In order not to simultaneously raise its own risk exposure that a project might fail, an EPFI has limited remedies in the event of compliance violations by the lender [60].

As lenders are unable to monitor progress themselves due to lacking capacities, the institution’s clients are required to offer warranties and assurances that environmental and social issues will be managed successfully under the Environmental and Social Review Procedures [59].

Project companies partly accuse banks or third-party advisors of interpreting standards and requests too stringently. According to borrowers, the scope of due diligence can be much broader than anticipated and requested documentation can go beyond requirements set in the past [21]. This might either arrive from limited in-house capacities from the lender or generally different perceptions, respectively risk evaluations. Issues in dispute may be, for example, that PCs argue they comply with national law and do not see the necessity to do more. Furthermore, it is not understood why further stakeholder meetings are needed when public hearings have already taken place [21].

Consequently, in order to eliminate the before mentioned ambiguities between banks and project companies, the editors of E&S frameworks should seek a communication and information exchange especially with its clients and members, but also with other project stakeholders by incorporating the concept of ‘conflict-sensitivity’ into the new standards [61]. Investigations into whether opinions actually diverge or whether they are predominantly uniform are to be clarified by the expert interviews presented in the next chapter.

3.3 Stakeholder perceptions regarding E&S risk management in project finance

Many different aspects in terms of socioenvironmental standards in project finance have been researched. As constituted, several frameworks, principles, standards and initiatives exist. Development banks, export credit agencies or commercial banks have partly developed their own requirements. However, compared in more detail, they are predominantly aligned with each other, as Amirkhanova argues [33].

Park et al. [10] compare green banking policy interventions by different financial institutions divided into developed and developing countries as well as into mandatory and voluntary codes of conducts. They conclude that developed countries rather rely on a voluntary code of conduct. Contrarily, developing countries tend to utilize more regulatory ways to encourage green banking [10]. By comparing annual reports of 100 financial institutions, it was demonstrated that financial institutions from developed countries report on sustainability in a higher quality [40]. Distinguished between privately and government-owned institutions, the quality of sustainability reporting of the latter is worse [40].

Various reasons for implementing E&S frameworks by financial institutions have been identified. One of them is that adoption of standards signals positive credentials to improve company reputation and organizational legitimacy in general [49]. Especially voluntary principles such as the Equator Principles rely on its evolving character and its adaptability to changing industry and market needs [62].

In contrast to the positive effects, E&S frameworks such as the Equator Principles are also considered “a fig leaf” or are also called greenwashing since it allows banks to shift their attention away from what they do wrong in terms of environmental and social matters toward what little (5% of their business) they do right [39]. Finger concludes that greenwashing only applies to developed countries (with even a negative effect on the performance of adopters). For developing countries, on the other hand, it has a positive effect and can be seen as a strategic decision [63].

Literature highlights also what financial effects appear due to an implementation of E&S frameworks. It was discovered that in respect of market share, adopters outperform the global project finance market [64]. Non-adopters are not, however, banned from lending syndicates [64]. In addition, the performance of banks in terms of environmental and corporate governance raises shareholder value. In contrast, the banks’ social performance decreased it [65].

Due to short-term reputational reasons resulting from the introduction of EP, an examination of banks’ adoption of EP shows an increase in funding activity and slightly improved profitability. However, none of the profitability or other performance indicators are significantly affected in the period of 5 years after the introduction of EP [63].

Some law articles took up the matter of compliance in E&S standards. It is seen as problematic that compliance is completely dependent on the subjective assessment of the bank [66]. The requirement "to the EPFI’s satisfaction" is still part of the Equator Principles [36]. Even if banks are good at monitoring compliance, they are not good at enforcing it [57]. Ong, criticizes that already the required monitoring procedure in Principle 9 of the EP, which enables clients to appoint an external expert for monitoring compliance, leaves room for abuse [60].

If the project company permanently fails to meet the standards, the bank, due to its short-term interest, has limited options to threaten to withdraw the financing [57]. Similarly, the standards do not urge banks to take countermeasures. There is no delisting procedure, and failure to comply with the EPs has no civil or criminal consequences [67]. Audits and disclosures by banks would help. Without them, and thus equipped with little accountability, banks will not be able to improve their reputation [68].

Having discussed the sustainability principles from several perspectives, however, little research has been conducted by now about the direct relationship between banks and PC regarding the sustainable project finance process and which discussions arise from different perceptions about its requirements and its compliance.

Solely Cousins describes that clients or project companies frequently perceive lender standards and requests as being overly stringent. These opinions may be the result of a lack of in-house capacity or of ingrained attitudes that call the process into question [21]. Borrowers typically are wondering about upcoming discussions, while complying already with national law [21]. Discussions like these arise due to perceived high standards by the borrower. However, strict requirements are not always in the banks’ interest. With higher requirements, the bank runs the risk of imposing higher financial hurdles on the PC, increasing the risk of default. This could prevent repayment of the loan [66].

Within this work, the authors are using a qualitative research design as the aim is not a quantification of data but rather the focus is on the description of a subject’s experience and the meaning of a phenomenon [69]. Semi-structured expert interviews are conducted as this allows being flexible regarding the sequence of the questions and to influence the course of the interview if needed [70, 71].

The aim of these expert interviews is to retrieve specific knowledge that cannot be obtained from other sources [72]. Within this work, ten experts were selected. A snowball sampling technique was used in order to get access to further potential interview partners. This technique shows to be effective within areas where interview partners are not easily accessible [73]. Since the diversity of samples generated via this method has repeatedly been questioned [74], it was combined with a purposive sampling technique [75].

Due to regional distances, some of the interviews were conducted via video call. The remaining ones were conducted in person. The interviews generally lasted 30 - 40 minutes.

The following table gives an overview of the interviews and their partners. Interviewed bank employees were labeled with the ID “B”, project company staff got the ID “P” and the ID “S” was given to the one professor (scientist). With the clear goal of comparing the perspectives of involved parties with regards to their assessment and perception of environmental and social risk management in sustainable project finance, the experts have been selected based on the requirement of profound expertise in their field outlined in the table below. The average experience is >10 years. Key information regarding the expert interviews are summarized in Table 2.

The analysis of the expert interviews was carried out using a content-structuring qualitative content analysis according to Mayring and Fenzl [76]. The purpose of the content-structuring technique is to filter out certain aspects of the material under predetermined criteria of order or to assess the material based on certain criteria [77]. The structuring approach was applied since content-related aspects of the interview material are of particular interest for this work.

Two different categorization techniques can be used: inductive or deductive. Inductive means that the categories are developed directly from the data. In contrast, in deductive categorization, the categories are established in a theory-driven manner prior to the analysis of the material [78].

A mixture of categorizations is used, while a deductive one was primarily applied, followed by an inductive one. This progression has been chosen in order to not only base the coding frame on theoretical assumptions but also to leave space for a flexible coding frame once new aspects are discovered within the material [79]. The qualitative content analysis was conducted with the help of the software MAXQDA according to the instructions of Kuckartz and Rädiker [80].

Table 2. Expert overview

|

ID |

Position |

Project region |

Experience in E&S risk management in project finance |

Interview duration |

|

B1 |

Banker |

Global |

25 years |

31 min |

|

P1 |

Project company expert |

Germany, Kuwait, Balkan, China |

37 years |

44 min |

|

B2 |

Banker |

EMEA |

20 years project finance |

30 min |

|

P2 |

Project company expert |

Burkina Faso |

11 years |

28 min |

|

S1 |

Scientist |

Global |

16 years |

55 min |

|

P3 |

Project company expert |

Balkan, Middle East |

11 years |

39 min |

|

B3 |

Banker |

Global |

9 years |

35 min |

|

P4 |

Project company expert |

Southeast Asia |

3 years |

47 min |

|

P5 |

Project company expert |

Europe, Asia (India, China), North-/ South America |

30 years |

46 min |

|

B4 |

Banker |

Southern Africa |

> 25 years |

43 min |

Subsequently to transcribing the interviews, a coding system for the present texts had to be developed. Firstly, the main categories were developed deductively based on the literature (with the exceptions of two main categories, which were inserted inductively afterwards). All subcategories were then developed inductively. In total, 351 codings of 24 (sub-) categories were assigned to all ten interviews. Due to a large number of categories and codings, it was decided to focus mainly on those categories essential to answering the research question. Each of the following main and subcategories helped in answering one of the three sub-questions:

1.1 Reasons for an application → Why are E&S standards used in project finance?

1.2 Effects of the standards → What influence do E&S regulations have on project financing?

4 Relationship Bank - Project Company → What is the relationship between the bank and the project company during the application of E&S standards in sustainable project finance?

4.1 Unity

4.2 Disagreement

4.3 Potential for improvement

The categories (4.1 Utility, 4.2 Disagreement, 4.3 Potential for improvement) belong to the 4th category and help in answering the third sub-question. The following chapter represents the key findings of the above-mentioned categories. Furthermore, insights of the other categories are used to enhance the later discussion.

5.1 Relevant results

Why are E&S standards used in project finance?

To primarily understand the reasons -illustrated in Table 3- for an application of E&S standards in the field of sustainable project finance, interviewees gave several reasons, which can be divided into three main topics: Internal company reasons, external company reasons and project-related reasons. Increasing attention to the topic of sustainability and sustainable financing can not only be perceived today but also in the responses of the interviewees. Both studied stakeholder groups, banks and PCs, state that climate protection, biodiversity and the protection of human rights are important as external reasons for an application of standards. Besides such E&S reasons, political pressure (e.g. due to the EU taxonomy) is also cited as causing the standards to be applied more widely. This, as argued by B2, speeds up the implementation of such standards. Otherwise, a voluntary introduction would take longer. Overall, banks cited more external influences as reasons compared to internal ones.

Table 3. Reasons for banks and project companies to apply E&S standards

|

Banks |

Project companies |

|

|

However, risk management reasons are mentioned for internal purposes. Thereby, adverse consequences can be mitigated. While sustainable practices are also used to some extent as a marketing argument by banks, PCs that use E&S standards have a competitive advantage if more environmental and social friendly technologies or products are required. One further important internal reason for banks is a better, or no bad, reputation due to the standards. Interviewees have argued that a bank’s reputation is very important. Financial institutions want to avoid reputational damage at all costs, as this affects them directly. Therefore, managing their reputation is very important for banks. P1, on the other hand, disproves this argument and describes that banks are more committed to the standards rather than fearing for their reputation. Project-specific reasons cited include avoiding E&S risks from project inception to operation, as well as creating boundary conditions for each project. The latter also clarifies for all participants what is required - as B4 describes. In summary, all those arguments can also be categorized into reasons relating to banks and PCs. Overall, the conclusion is that banks as well as PCs use E&S standards in project finance due to sustainability reasons and as a tool for risk management in order to minimize adverse social and environmental impacts within a project. Another driving force is politics since it encourages the implementation of such frameworks, which results in a better reputation for both sides. Legal certainty and defined boundary conditions are furthermore helpful. While banks see sustainability as a potential marketing argument, PCs may gain a competitive advantage when offering socioenvironmental solutions.

What influence do E&S regulations have on project financing?

The implementation of E&S standards can cause several consequences and effects for the banks, project companies, but also the project itself. Interestingly, PCs rather state negative consequences while banks emphasize the positive effects.

Concerning a bank’s strategy, frameworks have the potential to shift a bank’s intention away from a purely financial perspective towards a more socioenvironmental orientation. Additionally, entire projects with a certain amount of fossil resources have been restructured with a reduced share of carbon. Interviewee B2 compares it to a wave that you cannot escape from, causing a complete reorientation of the industry. This causes the banks to find new ways and strategies to meet the standards and their requirements.

Besides a change in banks’ strategies, standards have even led to higher quality requirements in a project compared to those requirements set by the tender. P5 stated that he had experienced that, using the example of the effluent quality of a wastewater treatment plant, higher requirements were demanded for structural changes and thus higher quality requirements. This was done at the insistence of the bank and was not included in the tender in this form. However, the effects can also influence the decision-making for bidding processes. In case several bidders have different financiers, their loan requirements may differ. This could lead to advantages for those bidders with fewer or more lenient demands. In order to increase the comparability, P3 is in favor of all bidders considering these standards with the same requirements. This way, PCs that meet these standards would not lose a project because they meet the standards and are thus more expensive than companies that do not meet them. As the interviews reveal, the standards also serve as guidelines, giving instructions for concrete actions and thereby increasing clarity for all participants. Furthermore, it created a common understanding among different occupation groups such as accountants, lawyers and engineers. All relevant effects of the standards are summarized in Table 4.

All in all, the answers to the second research questions are multifaceted. General effects conclude both a change in banks’ strategy (exclusion of non-sustainable projects and move away from purely financial benefits) and a change of banks’ behavior towards its customers. Customers must follow a bank’s sustainable guidelines for getting a financing or a loan. The standards influence a common understanding between different professional groups, express expectations of the participants from each other and lead to higher project requirements. Positive effects occur due to an avoidance of wrong decisions (as a tool for risk management) and protect a loss of value of the project (if the standards are not met). However, negative effects arise from a complicated project process. Additionally, E&S standards increase the offer costs for tenderers compared to those who do not meet the same E&S requirements and leads to a distortion of competition.

Table 4. Effects of the standards

|

General effects |

|

|

Advantages |

|

|

Dis-advantages |

|

What is the relationship between the bank and the project company during the application of E&S standards in sustainable project finance?

After discussing the reasons for introducing and the effects due to E&S standards, the relationship between banks and the project companies is examined. At first, the interviews showed that the relationship, in general, is considered to be close as well as intensive. It relies on a dependency in which the PC rather depends on the bank than vice versa due to the necessity of financing. One can also describe it as a “working relationship in a dialog”, as P2 did.

As banks are organized differently, some of them have a deeper technical knowledge about E&S which supposedly improves the quality of the project regarding that. Moreover, regional constellations also play a role. Due to different economic and political situations and languages, the relationship can become more complicated. P5 argued that a German PC and a German bank usually harmonize well with each other. Similarly for a French PC and a German bank. However, as soon as a different economic or political situation or a different language is added, the relationship becomes more complicated - for example with a Turkish bank and German company. This is a greater challenge than initially suspected. However, the more professional and serious the business relationship, the more helpful it is.

Overall, however, it is noticeable that all interviewees describe the general relationship as very good (with a few exceptions, which are described below). Both groups argue that a relationship based on trust and partnership is essential for the cooperation and for a joint project implementation. Nevertheless, experience has shown that it is advisable to address problems openly, otherwise trust disappears. In case a banking syndicate is operating, P3 expressed that good experiences have been made with a global facility agent who is appointed by all banks and acts as one central contact person for the project company.

As mentioned above, some disagreements exist, too. The efforts arising from applying E&S standards are often connected to relatively high costs for the company in charge of the project. Hence, on the one hand, such corporations may try to meet the socioenvironmental requirement with the minimum possible effort, which leads to a worse quality and therefore cannot be in the bank’s interest. On the other hand, PCs argue that in part the banks have too high requirements which are difficult or impossible to implement (especially for social matters). These high requirements and the resulting, as excessive perceived, effort on the part of the PC to protect the environment and society aptly describe the Principal-Agent problem. The bank demands the protection of E&S aspects, but since the PC has other interests (e.g. minimizing costs or increasing profits), it tries not to pursue the bank’s interest with the high effort.

Nevertheless, PCs argue that they are partially dependent on information by third parties or authorities that do not always cooperate so they are not able to deliver the desired documents. This can cause problems between both parties if no compromise is found. P3 reinforces this argument by saying that theoretical requirements from e.g. IFC standards are not compatible with practical implementation. From his experience, this can lead to problems if the bank is not willing to compromise at this point. Three areas were identified as opportunities for improvement: Communication & transparency, bank staffing and changing behavior. For the beginning, more open communication and a clear definition of realistic expectations would have a positive impact. The same applies to better ensuring a high level of transparency regarding financing contracts as well as disclosure of how funds are used. Secondly, P2 argues that banks have too few staff for the number of projects: “my observation is that some are quite overstretched in terms of their ESG staff, so maybe they don’t have enough.” Equal treatment of all PC by the banks is suggested as an advantage for future projects concerning a changed behavior. Otherwise, offers by companies following the standards are more expansive than those who do not. Banks hope that PCs will get more involved in advance and do baseline studies up-front if necessary. In addition, Grievance measures should be implemented from the outset. Thus, the relationship between the bank and the PC can be summarized as shown in Table 5.

In conclusion, the relationship between the banks and the project companies is described as close and intensive. As a dependency and a working relationship, regional constellations, however function differently. There is a consensus on the assessment of the mutual relationship during the project, which is described as very good. Moreover, it is considered trustworthy and cooperative. There is disagreement, however, that the banks' social requirements in particular are too high and unrealistic. This could be improved by a better communication and transparency. Reducing the burden on a bank’s employees could also improve cooperation.

Table 5. Key aspects of the relationship between the bank and the PC

|

General description |

|

|

Unity |

|

|

Disagreement |

|

|

Potential for improvement |

|

5.2 Discussion of results & research limitations

Analogous to the global cross-sector ESG trend, banks are also rethinking their business strategies. For example, the standards are causing bank strategies to change by excluding non-sustainable projects from the project finance portfolio. This phenomenon, that a large part of the banking industry is moving in the direction of sustainability, can be well explained by the Institutional Theory that is considered relevant for E&S standards as it emphasizes the role of external influences on an organization. Since E&S approaches are so well received on the market and banks see these opportunities, banks that are not yet involved, do not want to miss this trend and are also jumping on the bandwagon. The institutional pressure is too great.

Overall, the impression that banks refrain from purely profit-driven motivations is strengthening. Among other things, respondents cite the avoidance of wrong decisions resulting in a loss of project value as a beneficial consequence of adoption. What could not be deduced from literature, , was that standards lead to better comparability of offers by applying the same framework conditions to providers. However, if a bank that requires lower E&S requirements finances a PC, a greater distortion of competition within the PCs would be created. Higher conditionality also means increasing bidding costs for bidders. On the lender side, overburdening a single bank employee with too many projects does not help projects to be adequately managed either, as one interviewee indicated.

Concerning the BTF, the stance on complying with the standards and the effort connected to it, contrary to the benefits, is not the same for all project members from one firm. While some colleagues see the beneficial effects of the standards for the environment, for the society, but also for the own company, other project company employees rather see the difficulties in meeting the bank’s requirements knowing of the advantages just mentioned. Here the rationality of individuals is different. Hence, the bounded rationality applies here. In order to counteract the assumption of past performance and uncertainty (third BTF assumption), one interviewed bank decided to establish internal interdepartmental discussions to avoid routine and to review its own actions. Past experience should not solely determine actions in the present or in the future.

Although the interviewees stated that banks sometimes stopped financing entire projects when PCs violated the guidelines, careful verification of compliance with the standards is difficult or expensive, similar to what is described in the literature [58]. It is expensive because the bank usually does not have the appropriate staff and therefore has to hire consultants. Regular audits have made a great deal of difference here, as one PC employee described. It should also be remembered that if the bank withdraws financing because the PC does not meet the standards, it will incur considerable costs (e.g. costs for hedges against interest rate or currency risks), which is why higher lender standards are not always in the banks' own interests.

Overall, the relationship between the bank and the PC is described as a close and intensive dependency or business relationship. Other than suspected, all respondents attested a very good relationship characterized by trust and partnership. This is controversial as several les positive views could be found in the literature of Cousins [21]. Occasionally, too high social requirements of the banks, in particular, were mentioned as worthy of discussion, which PCs cannot meet or can only meet with great difficulty. Apparently, the required grievance mechanism seems to be a point of discussion. For example, one participant in this study stated that there are cultural areas in which involvement of the local population is not desired. Under these circumstances, and without the willingness to compromise on the part of the bank, it is difficult to meet the set requirements. This already represents a suggestion for improvement, which could improve the relationship: Better communication. Greater transparency and increased staff deployment by the banks were also mentioned.

Limitation of research

The governance factor, which is often considered in the course of ESG when talking about sustainability, is not part of the scope of this paper. Since governance, or more precisely corporate governance (CG), comprises the management and supervision of a company, this does not apply to the object of investigation of this research question. Predominantly the different attitudes and perceptions of banks and PCs regarding environmental and social standards shall be presented and discussed. In these, no requirements regarding governance are mentioned. In some cases, the standards have the effect of changing internal company matters and thus CG aspects, e.g. operational restructuring, but the origin of the motives is not the management behavior of the company itself but is externally based and thus not attributable to CG.

The two stakeholder groups of banks and PCs were interviewed during the expert interviews. Other stakeholders, such as project-affected communities (PAC), host country governments or NGOs, as well as initiators of standards (policy-makers and regulators could also have been interviewed. However, the focus of this research was intentionally limited to the two groups mentioned. This work aims at presenting the users of the standards and consequently, the main protagonists. NGOs could have reported on implementation assessments and PACs on direct social and partly environmental impacts, but this was not the scope of this work.

The interview groups were differentiated into bankers, PC staff, and academics in order to represent the fundamentally different perceptions of the three occupational groups. Differentiating banks into those that have implemented an E&S framework for a longer period of time and those that have implemented it more recently or not at all, might have indicated the effects due to implementation more strongly. Since four bank employees were interviewed in this study, the number was deemed too small for a more minor breakdown to be appropriate.

Summary of the most important results and their integration into the overall context

Based on the superordinated research question formulated in the introduction, what the understandings and perceptions of banks and PCs regarding E&S standards in project finance are, the Principal-Agent Theory and Behavioral Theory of the Firm were deemed relevant for this paper. Adapted from the literature, it was assumed that most banks want to address the issue of sustainability more by joining a network as well as by defining and implementing E&S goals in project finance. However, different conflicts of interest and goals inevitably lead to discussions between the bank and the PC, as the latter see higher requirements as a burden.

In order to answer the research question, a qualitative research method has been chosen. Ten expert interviews were conducted with employees of banks, PCs and one professor. The results indicate that sustainability aspects as well as political pressure are the main reasons why financial institutions have introduced sustainable standards. Effects at banks resulting from the frameworks are mainly found in a changed strategy (excluding e.g. non-sustainable projects and adapted organizational structure) as well as an approach to E&S aspects (stronger attention to consequences due to a changed risk assessment). PCs see advantages in an improved comparability of bids, while a more complicated project process and higher bid costs are seen as negative. Lastly, it can be said that, contrary to expectations, all respondents claimed the relationship to be very good and based on partnership. The few points of discussion concentrate on too high social demands and a lack of willingness to compromise. Regarding the limitations outlined in previous sections, the scope of ESG, number, type and diversification of stakeholder group, alongside the focus of the study should be re-emphasized.

Prospect of future research

The results obtained in this paper lead to further questions. For example, there was disagreement as to whether the standards are applied equally across regions. Future research could find out whether the relationship between banks and PCs is the same in developed and developing countries or whether there are different regional reasons for adoption. Similarly, it could be discussed whether the adoption date of a bank’s E&S standards changes the ratio. That is, whether the financial institution’s higher experience with the frameworks has made the relationship with PCs better or worse over time.

In addition, there are now more positions within the PC that are dedicated to the topic of sustainability. However, it is unclear whether there is unanimity within the entire PC about the usefulness of taking these standards into account. It is possible that the local employees are in favor of these standards because they directly see the effects, while the management, due to their distance, denies the benefits and only sees the costs. This could be investigated scientifically.

Recommended course of action

Some recommendations for action can also be made for stakeholders based on this work. Since some respondents indicated significant differences in the various banking requirements, a unification of diverse standards would provide relief. However, it should be noted that reasonable and realistic requirements are taken into account, which are supported by both sides and at the same time represent a motivation to achieve higher goals. Likewise, instead of rigid limit values, ranges could be applied, possibly resulting in a point system in which poorer values are tolerated provided that good results compensate for them. To this end, institutions such as the World Bank and the EBRD could cooperate more closely and thus harmonize their requirements or possibly agree on the same standards. As a consequence, this would require training for the banks’ advisors and PCs since many advisors have different requirements for PCs and present the results to the bank.

A predefined time frame in which the standards are routinely reviewed and brought up to the "state of the art" should also be introduced. The previously criticized lack of transparency may be relatively easy to improve through simplified standards in the future. Like banks, which do not want to impose too much on their customers, banks could also implement more transparent E&S targets with few but clear rules. Banks should increase their staff or hire more consultants to monitor projects. Malpractices could then be detected more quickly and communication to the PC could be strengthened. On the side of PCs, if companies are really interested in improving environmental and social conditions, they could conduct more extensive studies in advance to better assess the negative impact of the project and to initiate appropriate countermeasures at the earliest stage possible.

In addition, consideration could be given to how E&S or ESG targets can be measured and rewarded in the future. One idea here could be to define these targets alongside financial indicators as a goal within the bonus payment for responsible managers. This would create a financial incentive that could potentially increase motivation for the benefit of a sustainable environment and society. There are already initial approaches to this, but it could and should be used more intensively.

Another way to integrate sustainability into project financing is to incorporate E&S requirements from the standards or the standards directly into the project request for proposal (RFP). In doing so, countries tendering projects or consultants supporting countries must ensure that the PCs or the financing banks actually comply with them. This would ensure that all PCs have the same starting point and the same requirements, and that no bidder is cheaper because it does not take the requirements into account (subject of further research).

Overarchingly, the growing trend of sustainable finance is clearly noticeable, which is also being driven forward in the project finance business. What was considered a niche a few years ago will establish itself as a mass-market in the near future. Nonetheless, there are immense challenges ahead and investment gaps to be closed in terms of infrastructure projects for the water sector as well as for the transport and energy sectors. However, these sectors have to potential to contribute to a better and more sustainable world. Starting, for example, with a serious consideration of already existing tools such as E&S standards and continuing with their further development.

[1] European Commission. (2021). 'Fit for 55': delivering the EU's 2030 Climate Target on the way to climate neutrality. https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52021DC0550&from=EN.

[2] G20 Development Working Group (DWG). (2019). Key Elements of Quality Infrastructure for Connectivity Enhancement towards Sustainable Development. https://www.mofa.go.jp/mofaj/gaiko/g20/osaka19/pdf/documents/en/g20dwg_qi_key_elements_final_en.pdf.

[3] New Climate Economy. (2016). The Sustainable Infrastructure Imperative (978-0-9906845-9-6). http://newclimateeconomy.report/2016/wp-content/uploads/sites/4/2014/08/NCE_2016Report.pdf.

[4] United Nations. (2021). The Sustainable Development Goals Report 2021. https://unstats.un.org/sdgs/report/2021/The-Sustainable-Development-Goals-Report-2021.pdf.

[5] McKinsey. (2022). The net-zero transition: What it would cost, what it could bring. https://www.mckinsey.com/capabilities/sustainability/our-insights/the-net-zero-transition-what-it-would-cost-what-it-could-bring.

[6] Global Infrastructure Hub. (2021). G20 Quality Infrastructure Investment Case - Study Survey. https://cdn.gihub.org/umbraco/media/4011/report_g20-iwg-qii-survey_march-iwg-2021.pdf.

[7] United Nations. (2020). World investment report 2020. https://unctad.org/system/files/official-document/wir2020_en.pdf.

[8] Hebb, T. (2019). Investing in Sustainable Infrastructure. In: Arvidsson, S. (eds) Challenges in Managing Sustainable Business. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-319-93266-8_11

[9] Egler, H.P., Frazao, R. (2015). SUSTAINABLE INFRASTRUCTURE AND FINANCE - How to Contribute to a Sustainable Future. http://unepinquiry.org/wp-content/uploads/2016/06/Sustainable_Infrastructure_and_Finance.pdf.

[10] Park, H., Kim, J.D. (2020). Transition towards green banking: Role of financial regulators and financial institutions. Asian Journal of Sustainability and Social Responsibility, 5(1): 5. https://doi.org/10.1186/s41180-020-00034-3

[11] Mohamadi, F. (2021). Introduction to Project Finance in Renewable Energy Infrastructure: Including Public-Private Investments and Non-Mature Markets (1st ed.). Cham: Springer International Publishing.

[12] Bristol-Alagbariya, E.T. (2020). IFC environmental & social performance standards: Soft law project & company financing partnerships towards good environmental governance, business sustainability and sustainable development in developing countries. International Affairs and Global Strategy, 81: 51-68. https://doi.org/10.7176/iags/81-07

[13] Ma, T. (2016). Basel III and the future of project finance funding. Michigan Business & Entrepreneurial Law Review, 6(1): 109-126. https://doi.org/10.36639/mbelr.6.1.basel

[14] Deluz, C.N. (2010). Generic Project Finance Methodology. https://www.moodys.com/researchdocumentcontentpage.aspx?docid=PBC_127446.

[15] Gatti, S. (2013). Project Finance in Theory and Practice - Designing, Structuring, and Financing Private and Public Projects (2nd ed.). Amsterdam: Elsevier/AP, Academic Press.

[16] Haack, P., Schoeneborn, D., Wickert, C. (2012). Talking the talk, moral entrapment, creeping commitment? Exploring narrative dynamics in corporate responsibility standardization. Organization Studies, 33(5-6): 815-845. https://doi.org/10.1177/0170840612443630

[17] John, T.A., John, K. (1991). Optimality of project financing: Theory and empirical implications in finance and accounting. Review of Quantitative Finance and Accounting, 1(1): 51-74. https://doi.org/10.1007/bf02408406

[18] Müllner, J. (2017). International project finance: review and implications for international finance and international business. Management Review Quarterly, 67(2): 97-133. https://doi.org/10.1007/s11301-017-0125-3

[19] Project Finance International. (2016). League tables. In J. Müllner (Ed.), International Project Finance: Review and Implications for International Finance and International Business.

[20] Röver, J.H. (2013). Security in Project Finance. Paper presented at the Secured Lending in Commercial Transactions - Trends and Perspectives, London.

[21] Cousins, D. (2015). Implementing Environmental and Social Risk Management on the Ground: Interfaces Between Clients, Investment Banks, Multi-laterals, Consultants and Contractors: A Case Study from the EBRD. In: Wendt, K. (eds) Responsible Investment Banking. CSR, Sustainability, Ethics & Governance. Springer, Cham. https://doi.org/10.1007/978-3-319-10311-2_5

[22] Mulder, I., Hunt, P.C. (2010). UNEP FI CEO Briefing • Demystifying materiality: hardwiring biodiversity and ecosystem services into finance. https://www.unepfi.org/fileadmin/documents/CEO_DemystifyingMateriality.pdf.

[23] de Palma, A., Leruth, L., Prunier, G. (2012). Towards a principal-agent based typology of risks in public-private partnerships. Reflets et Perspectives de la vie éConomique, 51(2): 57-73. https://doi.org/10.2139/ssrn.1475518

[24] Shrestha, A., Tamošaitienė, J., Martek, I., Hosseini, M.R., Edwards, D.J. (2019). A principal-agent theory perspective on PPP risk allocation. Sustainability, 11(22): 6455. https://doi.org/10.3390/su11226455

[25] Wang, Y., Liu, J. (2015). Evaluation of the excess revenue sharing ratio in PPP projects using principal–agent models. International Journal of Project Management, 33: 1317-1324. https://doi.org/10.1016/j.ijproman.2015.03.002

[26] Jeucken, M. (2010). Sustainable Finance and Banking (1 ed.). Boston, MA: Routledge.

[27] Farrell, L.M. (2003). Principal-agency risk in project finance. International Journal of Project Management, 21(8): 547-561. https://doi.org/10.1016/S0263-7863(02)00086-8

[28] Charoenngam, C., Yeh, C.Y. (1999). Contractual risk and liability sharing in hydropower construction. International Journal of Project Management, 17(1): 29-37. https://doi.org/10.1016/S0263-7863(97)00064-1

[29] Bonazzi, G., Tacke, V. (2014). Geschichte des Organisatorischen Denkens (2 ed.). Wiesbaden: Springer VS.

[30] Schnebel, E. (2017). Wirtschaftsethik im Management: Rationalität und Verantwortung in organisationalen Handlungen. München: Springer Fachmedien.

[31] March, J.G., Simon, H.A. (1959). Organizations. New York: Wiley.

[32] Kirchoff, J.F., Omar, A., Fugate, B.S. (2016). A behavioral theory of sustainable supply chain management decision making in non-exemplar firms. Journal of Supply Chain Management, 52(1): 41-65. https://doi.org/10.1111/jscm.12098

[33] Amirkhanova, E., Vogelsberger, R. (2015). Challenges and advantages of IFC performance standards: ERM experience. In: Wendt, K. (eds) Responsible Investment Banking. CSR, Sustainability, Ethics & Governance. Springer, Cham. https://doi.org/10.1007/978-3-319-10311-2_3

[34] Coleton, A., Brucart, M.F., Gutierrez, P., Tennier, F.L., Moor, C. (2020). Sustainable Finance - Market Practices. https://www.eba.europa.eu/sites/default/documents/files/document_library/Sustainable%20finance%20Market%20practices.pdf.

[35] Weber, O. (2014). Equator principles reporting: Do financial institutions meet their goals? https://www.cigionline.org/static/documents/no38.pdf.

[36] The Equator Principles Association. (2020). About - The Equator Principles. https://equator-principles.com/about/352/.

[37] The Equator Principles Association. (2020). The Equator Principles. https://equator-principles.com/wp-content/uploads/2021/02/The-Equator-Principles-July-2020.pdf.

[38] Houérou, P.L. (2019). Creating markets for sustainable finance: Driving measurable change. In Sustainable Banking Network (SBN) (Ed.), Global Progress Report.