Gunardi Lie![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The relationship between creditors and debtors is unique. Creditors need debtors as customers and bind them in credit agreements. Creditors tend to be suspicious of debtors as debtors selectively disclose information. This relationship follows the agency theory. Creditors always want a fair and equal position with other creditors. This research is unique in discussing the situation between creditors in the concept of negative pledge and pari passu pro-rata parte. Aside from that, the study also observes the relationship between creditors and debtors in credit agreements and discusses solutions that can be given by debtors to creditors so that the pari passu pro-rata parte principle can be achieved. The pari passu pro-rata parte principle is regulated in the Indonesian Civil Code article 1131 - 1132 and Law on Bankruptcy article 176 jo. 189. The methodology used is the normative juridical method, specifically hermeneutics and idiographic from the economic and financial perspective. The research concluded that debtors and creditors could ensure a fair and equal position by implementing negative pledge through Master Credit Agreement and Security Sharing Agreement. Future research should study on the role of curators and judges as key people to keep the concept of negative pledge running well.

bankruptcy, negative pledge, pari passu, pro-rata parte

Companies need funds to grow their businesses [1]. Company management can obtain funds from financial loan institutions, shareholders, or a combination of both [2]. The selection of loans or shareholder funding determines the capital structure. The capital structure will determine the cost structure of the company [3].

A loan from a financial institution is an alternative that is often chosen [4]. The cost of a bank loan is lower than the expected return for shareholders [5]. However, these loans require collateral [6]. Shareholder funding does not require collateral [7].

In addition to collateral, financial institutions as creditors will provide the covenants of the company or debtor in the credit agreement. A violation of a covenant will result in the debtor being default [8]. Creditors provide lower interest, but loans are more binding for the debtor. This shows the existence of the agency theory [9]. Financial institutions are not involved in the management of the company. Shareholders are involved in company management [10].

Creditors and debtors have a unique relationship [11, 12]. Creditors need debtors as customers. Creditors provide loans only to the good and trusted debtors. Debtors need creditors as providers of funds for growth.

Creditors do not fully trust every debtor. Creditors tend to be suspicious of debtors. Creditors have a belief that debtors tend to keep secrets from them. Due to this reason, creditors bind debtors to various financial, operational, and legal aspects [13]. A credit agreement governs all of these bindings or covenants. Creditors require various covenants to regulate a debtor’s business activities. Creditors do not inspect the debtors’ daily business activities. These covenants are under the supervision of creditors. This supervision will provide a sense of security to creditors for loans provided [14].

Creditors lend funds to debtors, but there are still doubts about the debtors’ ability to pay. Creditors ask for the maximum and best possible debtor guarantee [15]. Creditors choose debtors who can repay their loans [16]. Creditors also suspect that debtors will provide different or better terms and conditions to other creditors. Creditors believe that debtors will not be fair in the relationship between all creditors [17]. Creditors believe that debtors will provide different collateral values and types of collateral.

This research is unique and novel in providing solutions to problems between creditors and debtors based on legal principles, and the financial analysis perspective before bankruptcy occurs. The settlement of creditor and debtor problems can be anticipated earlier before bankruptcy. This research fills the gaps and solutions to creditors’ distrust of debtors.

The clauses in a credit agreement will improve the relationship between creditors and debtors. A good relationship between creditors and debtors will increase the effectiveness of economic development [18]. An explicit agreement will reduce defaults and bankruptcy disputes [19]. A mutual trust agreement will reduce unnecessary costs, such as prosecution fees for defaults, guarantee execution costs in the event of a default, and other court-related costs. Creditor and debtor problems arise when one party defaults [20]. A debtor’s default may result in bankruptcy [21].

One of the main objectives of bankruptcy law is to ensure the distribution of bankrupt assets from debtors to creditors [22]. The distribution of assets follows the principle of pari passu pro-rata parte, which means dividing bankrupt assets to creditors without collateral based on the consideration of how much the creditor claims [23]. The asset settlement process in a bankrupt company is not exactly clear and does not follow bankruptcy law principles. The principle of pari passu pro-rata parte emphasizes the distribution of debtor’s assets to pay creditors’ debts following proportional procedures [24, 25].

Law concentrates on loans with collateral, which means that the financial perspective of bankrupt company’s assets allocation is not taken into account. The main issue from the law perspective is that for each creditor to have a fair and equal position. From a legal standpoint, the transfer of the assets of insolvent enterprises appears fair, but from an economic standpoint, it is not [26, 27].

The pari passu pro-rata parte principle is an essential clause in the credit agreement. The pari passu clause is standard in international contracts, especially for unsecured debt obligations [28, 29]. To understand the pari passu clause, the meaning of this term is from Latin, namely the phrase ’pari passu’ [30]. Pari passu means ‘with equal step’ (in the same position), and it comes from the word pari, ablative of pars, which means ‘equal,’ and the word passu, ablative of passus, which means ‘step’ or stages [31, 32]. The Supreme Court held that ‘if the agent becomes insolvent, a proprietary claim would effectively give the principal priority over the agent’s unsecured creditors, whereas the principal would rank pari passu, i.e., equally, with other unsecured creditors if he only has a claim for compensation’ [33]. Thus, pari passu means being in the same condition in the same situation and having an equal position. This clause is generally included in debt agreements to protect the lender or creditor from being in a subordinated loan position [34].

With a pari passu position, no creditor has a higher rank than the others. All creditors have the same place [35, 36]. This arrangement in a credit agreement includes equal status between creditors who have guarantees or separatist creditors and does not include concurrent creditors in a pari passu position.

The principle of pari passu pro-rata parte is regulated in Article 1131 and Article 1132 of the Indonesian Civil Code [37, 38]. This principle stipulates that all creditors have the same rights over the debtor’s assets unless there are valid reasons for priority based on the criteria or position of the creditor [39].

The Pro-rata parte regulates the rights of each creditor in obtaining collateral and in voting on matters concerning the debtor. Pro-rata parte is not defined as a one-man-one-vote system, but it is based on the composition of the loan value given to the debtor. The principle of pari passu pro-rata parte is regulated in Article 189 Paragraphs (4) and (5), as well as in the explanation of Article 176 letter (1) of the Indonesia Bankruptcy Law [40].

The pro-rata principle regulates the distribution of creditors’ portions. This principle stipulates that creditors have the same position on guarantees provided by debtors based on their respective loan portions. Each creditor will get an equal share according to the amount of the loan. If Bank A has a loan to a debtor of IDR 5 billion and a total of IDR 100 billion, then the portion of Bank A is 5/100, which is 5%. The 5% portion is the portion of voting rights in deciding on the debtor’s assets. This portion is the rights of the creditor on the executed guarantee if the debtor defaults.

The application of the pari passu principle creates confusion for other creditor [41]. The pari passu principle can only be applied if all creditors agree, and it is stated in a Master Credit Agreement (MCA) [42]. Without an MCA, this pari passu principle cannot be applied between creditors. Without an MCA arrangement, each secured creditor would have collateral rights. This is regulated in the Law of the Republic of Indonesia on Bankruptcy and Suspension of Debt Payment Obligations. The principle of pari passu holds that the position of creditors is the same. In recording the debt of a bankrupt company, the creditors have several functions, namely preference, separatist, and concurrent.

Merchandise suppliers are unsecured creditors. The position of creditors, which is regulated by the pari passu and the pro-rata parte principles, becomes an issue in a default. The role of creditors becomes a sensitive issue when calculating debt restructuring and bankruptcy [43].

Separatist creditors are secured creditors. Separatist creditors hold the right to guarantee material goods, and these creditors can sell the collateral that is guaranteed to them. Separatist creditors can directly sell and auction their collateral [44]. A bank usually is an example of a separatist creditor. Banks as creditors holding material security rights can execute the collateral if the debtor defaults on one’s obligations. Banks’ legal protection is the right to enforce the collateral following Article 55 of the Indonesia Bankruptcy and Suspension of Debt Payment Obligations Law (PKPU Law) [45].

Separatist creditors have mortgage rights and apply parate executies or the right to carry out executions as if there was no bankruptcy [46]. Separatist creditors in executing collateral cannot be hindered by a period of suspension because the position of the separatist creditor is separate from other creditors, and the collateral object is not included in the bankruptcy law [47].

Creditors have the right to have their loans repaid. This has been regulated in the credit agreement that the debtor is obliged to return the loan following the agreed period in the loan agreement. If the debtor defaults, then the creditor has the right to confiscate the collateral. The creditor has the right to sell the collateral to cover the debtor’s obligations [48].

Third-party legal protection is provided by appearing as a concurrent creditor by submitting a third-party loan to the curator in a verification meeting [49]. The suspension of debt payment obligations only applies to concurrent creditors [50]. Creditors want a fast settlement of debt, and the debtor can pay off all debts. The debtor wants a debt settlement that provides legal protection with all debtors able to obtain a refund of the receivables [51].

Many researchers and writers have changed their minds about the pari passu clause. In a market where many businesses have more advanced knowledge, pari passu clauses are considered to have no clear purpose and can result in ineffectiveness for decades [52]. The British Supreme Court has affirmed that the parties must not bind themselves to the distribution of assets to a company based on the pari passu principle [53].

In addition, many of the rules in bankruptcy law contradict the norms and principles of bankruptcy. This creates loopholes for parties who want to take advantage of the condition of bankruptcy with bad intentions [54]. The Bankruptcy Law stipulates that the right to sell, especially mortgage rights owned by creditors, can be suspended if the debtor is in a state of bankruptcy. This is different from the Mortgage Law, which gives creditors the right to execute collateral objects to pay off debtors’ debts [55, 56].

Although the pari passu pro-rata principle is ideally fair and equal in the legal perspective, in practice the principle cannot stand by itself when dealing with distribution of bankrupt assets. There is a need to find for another solution to support the legal principles, and one way is through loan agreements and negative pledge.

A loan agreement is also known as a pro-rata parte clause, which is related to pari passu. The pro-rata parte clause deals more with regulating collateral goods. When all creditors are equally based on pari passu, then the creditors have the same position, namely pro-rata parte, in obtaining collateral rights [57]. Loan agreements fall under the regime of contract law and therefore should be regulated under the Indonesian Civil Code. The agreement should fulfill requirements to be considered valid, which are: consent, capacity of the parties, objects, and legal cause, where the first two are subjective elements and the remaining are objective elements [58].

Some agreements require a negative pledge. A negative pledge is a clause in a deal that does not allow debtors to pledge their assets to any individual party [59]. In essence, a negative pledge is an agreement where the debtor is not allowed to create a security interest over the agreed or all of his asset. The economics explanation of the negative pledge is to prevent the debtor from creating uncertainties to the creditors’ end. As an illustration, say that A lend B some 1 million USD. Under a general loan agreement, A will request a security in the form of asset that allows A to have execution right in case of default. However, instead of adopting the traditional method mentioned, A will take B’s negative pledge, where B agrees not to put any of his asset as a security for other loan agreements.

A study in 2014 by Komara explains how negative pledge is a collateral model adopted from the practice in other countries outside of Indonesia [60]. Nonetheless, the implementation of negative pledge is actually facilitated in article 1338 of the Indonesian Civil Code, Freedom of Contract. Here, parties involved in the contract have the right to make an agreement that also includes the negative pledge clause. Although there are no regulations that specifically talks about negative pledge, the implementation of negative pledge can be seen often in Indonesia. We can also see the implementation of negative pledge in Indonesia from the research done by Utama, Hariyanto, and Hawin, which discusses the case of PT. Bank Mandiri [61].

PT. Bank Mandiri is one of the biggest government-owned banks in Indonesia, the bank also bears the responsibility to support and facilitate the economic growth in Indonesia. Most of the time, when businesses suffer from insolvency and even result in bankruptcy, banks as one of the companies’ loan providers, have to bear a big loss. However, as a prominent government bank, PT. Bank Mandiri must have an innovative and creative solution to provide financial assistance to business owners across Indonesia, one of which is through implementing negative pledge. The research results show that the Master Credit Agreement (MCA) regulates how banks provide companies with loan possibilities but still manage to follow the prudential principles in banking.

Furthermore, in another research done in 2017 by Putri discusses how negative pledge is often used as an alternative for World Bank when providing loans to countries by which the loan-recipient countries will not be able to provide collateral [62]. The practice by World Bank is clearly different in the business world, but Indonesian banks often use negative pledge as an alternative for providing loans. The research found that a government-owned bank, namely, Bank XYZ provide loans without personal guarantee or collaterals but under the condition of negative pledge as a covenant. The negative pledge is made under the bank’s Master Credit Agreement (MCA) and Security Sharing Agreement (SSA) regulations. Negative pledge is considered as a general collateral which is regulated in the Indonesian Civil Code article 1131, 1132 jo. 1320 - 1337, article 8(1) of the Indonesian Law of Banking bill no. 10 year 1998, and Bank Indonesia Decree of Director no. 27/162/KEP/DIR year 1995.

Several companies propose negative pledge clauses not to provide separate collateral agreements to certain creditors. All debtor assets are pledged to all creditors on a pari passu basis. The execution of debtor assets in a state of default will follow the principle of pari passu pro-rata parte. All creditors have the same position towards the debtor’s assets based on the pari passu principle in a negative pledge. However, the calculation of rights to assets is based on the pro-rata parte principle. The position of the debtor is not distinguished between separatist and concurrent. Thus, the negative pledge is related to the pari passu pro-rata parte principle. The clauses will be related to the principle of balance (equality) and the principle of justice (principle of fairness).

The negative pledge clause is not fully effective in protecting creditors in obtaining the right to collateral. Others can use the “priority principle” [63]. For the negative pledge to work, the priority principle must be removed.

The determination of the right of execution of the collateral by the creditor is based on the position of the company’s debt. This theory is based on the accounting theory. The accounting theory holds that short-term debt is above long-term debt. Debt is placed above the capital. The placement of the Chart of Account (COA) records determines the priority in the order of payments. The accounting theory does not consider the collateral effect.

The position between creditors is based on the order of COA in the accounting theory. Under normal circumstances, creditor priority applies. In a state of default, all creditor’s debts become due and can be collected so that the creditor’s position becomes equal. Workers have positions as preferred creditors with privileges that prioritize payments from other creditors in the event of bankruptcy [64]. Workers’ wages are categorized as preferred creditors according to the regulations. Tax payable also is classified as preferred creditors [65, 66].

From the aforementioned discussion, it seems that there is a disharmony regarding the regulations. Regulations are silent in the possibility of using negative pledge in a loan agreement. The lack of regulatory framework on the field will invite court’s decision in providing legal certainty of the use. The decision may be in the form of analogy (argumentum per analogiam) [67], depending on how the existing regulation might fit the use of negative pledge. On the other hand, banks, by regulation, are required to comply with the precautionary principles that under Indonesian Banking Law is translated into the 5 Cs: Character, Capacity, Condition, Collateral and Capital [68]. This is to ensure that banks do not end up with too much of non-performing loan [69].

Creditors will always suspect debtors. The debtor will not disclose the precise information to the creditor. Debtors who provide valid details to creditors will not receive financing. There are two hypotheses of this research:

Hypotheses 1:

The relationship between creditors and debtors will not achieve a fair and an equal relationship

Hypotheses 2:

The relationship between creditor and creditor will not achieve a fair and an equal relationship.

This research sought to find a solution to the relationship between creditors and debtors who need but suspect each other. This research focused on solutions based on legal functions. In this case, legal functions refer to law as a system of rules and law as a contract, therefore, the methodology used is legal logical thinking (redenering). To have a better understanding of the essence and substance of the rules is through Hermeneutics and Idiographics. This methodology is often referred to as normative juridical or prescriptive research method. Peter Mahmud Marzuki defines normative qualitative method as a process to find normative regulation, legal principles or legal doctrines to answer specific legal questions presented [70].

The data collected utilized primary and secondary legal as well as other supplementary materials. Other additional materials were taken from different disciplines related to the research theme. The main framework adopted in answering the legal question is the economic analysis of law where we examine a legal problem from the perspective of economics and financial theory.

This study examines legal materials and companies that experienced corporate debt restructuring to bankruptcy. The study reviews the position of creditors in cases that occur. The problem of restructuring and bankruptcy creates problems in accordance with applicable law. Then the research looks for solutions so that creditor problems can be solved with a better method.

4.1 Legal perspective

The notion of loan-agreement itself has self-explain that it is a form of an agreement. Indonesian law categorizes loan-agreement as a named agreement, as it is one of the forms of agreement recognized by default under the civil code. As an agreement, it is regulated under Article 1320 of the Civil Code where an agreement is constituted if it fulfills four elements: consent, capacity of the parties, objects and legal cause. Banking regulation, however, puts a higher standard of legal cause element as Indonesian banking law requires a loan agreement from a financial institution to fulfill 5C principles. The five Cs are: Character, Capacity, Condition, Collateral and Capital. Collateral is essential under Indonesian banking regulation and, although some exceptions may be applied, without collateral, banks are not allowed to pass a loan. This is to ensure legal certainty of the creditors, especially taking into account that principle-agent theory might highlight the different incentives between the bank owners and the loan officers. Legal theories in general requires certainty on both creditor and debtor’s end. With certainty as the ultimate aim, negative pledge turns to be an instrument that provide certainties to the creditor.

In essence, these two forms are way of the judges in adjudicate a case without any strict regulation. A negative pledge is an agreement where the debtor is not allowed to create a security interest over a specific or all assets. Negative pledge falls under the contract law regime where trust plays a huge role in its application. Negative pledge essentially disregards the collateral element of the banking principle, where the loan will be securitized by the debtors’ promise not to encumber specific or any asset under his possession. Assuming perfect information between the debtor and creditor, negative pledge offers a more efficient alternative in a loan agreement then a loan with security as it will result in less hassle of administrative process in securitizing, and allowing debtors to retain the assets, which result in leaving debtor with more available business decision. Under Indonesian law, however, negative pledge is not per se recognized. This invites present practicalities to be a question of interpretation. In any submitted case before the court, the judge is required to interpret the approporiation of negative pledge under Indonesian Law as they are not allowed to reject a case. The judges may find the law in the form of either intepreting the law or constructing the law.

The writer will first argue on whether in understading the negative pledge, the judge need to use legal construction or interpretation. Legal construction is an approach used by the judges in adjudicate a case, yet the case is both unprecedented and constitutively regulated. In this situation, the judge would need to ‘construct’ the law, creating a judge-made law that is not a product of legislative body, but purely from judicial body. However, another situation where the case does not perfectly match the existing regulation, but in principle, the case is normatively resembled from the existing law. In this kind of case, legal construction might not be efficient since a new law is not necessarily required. Therefore, taking the context, principles and analogy from other case or the existing constitutive regulation might be a wiser decision for the judge. Apart form the efficiency, such approach will also provide future certainty as the interpretation of the judge might enlight the written law in more detail with a proper precedent basis.

Retracting back to whether negative pledge is a practical case that require interpretation or construction, the writer argues that a legal interpretation through analogical approach is a more likely approach to be used. There are some reasons for the writer to reach this conclusion. First, the determination of the approach is based on the existence of regulation. While we do not have any regulation that normatively recognize negative pledge, we have securities law and security is the embodiement of trust that the debtor would be able to pay the loan. Second, Indonesian banking regulation clearly adopts the banking precautionary principle. This is to ensure that bank does not end up with a too high non-performing loan, which in a larger scale might disrupt the national economy.

Negative pledge essentially allows one to receive a loan without any asset collateral, as the collateral offered is merely in a non-asset form, the promise that the asset will not be used as a security for other loan. From the perspective of economics, with the assumption of clear calculation of risk, negative pledge is a more efficient option than collateral. The legal theory would agree this principle. While the regulatory framework provides a clear guideline on collateral and encumberement, Indonesian banking law does not regulate collateral as an absolute requirement. This norm itself has opened a door for interpretation. Third, the negative pledge, as a part of a loan agreement, remains within the scope of contract law regime. The freedom-of-contract principle is therefore applicable and both parties should be left to be the ones to decide whether the negative pledge is acceptable or not, not the judicial body. A negative construction that disallows negative pledge would be quite patrilineal that might result in unknown economics efficiency in the society. Therefore, interpretation within the scope of legal and economic theory that support the existence of negative pledge is a desired approach by the society. Present normative laws are suffice to accommodate the possibility of applying negative pledge, and construction is not required.

As mentioned before that from a legal perspective, the distribution of bankrupt assets may seem fair and equal. However, through economic and financial perspective the same conclusion may not be reached. Therefore, there is a need to incorporate both standpoints in order to have a better understanding of the issue.

4.2 Economic and financial perspective

Looking through the relationship between debtors and creditors, debtors obtain loans from creditors by providing collateral. Creditors need collateral to reduce credit risk. This collateral can be executed if the debtor defaults. Arrangements regarding execution procedures at the time of default are stated in the credit agreement.

Creditors will ask for the highest possible collateral coverage. The higher the coverage ratio, the more the creditors believe that the loan will be secure. Creditors ignore other information and focus on the collateral value obtained. The debtor will try to provide minimum collateral. Small collateral will allow the debtor to get additional loans. Additional loans can use the remaining assets that have not been pledged as collateral. As a result, creditors suspect that the coverage ratio is not the same between creditors.

Creditors who just made the last loan will get a worse collateral asset. However, creditors still need debtors. A bank needs debtor as consumers. The comparison of collateral coverage and type of collateral per creditors is described in Figure 1. Each creditor provides different loan facilities with different collateral and different collateral ratios. This creates problems of justice and balance.

The leverage ratio is a comparison between debt and capital. The comparison of collateral coverage is the ratio of total assets divided by total debt. This collateral coverage is related to the leverage ratio. The explanation of this calculation is in Table 1.

The covenant regarding collateral coverage reflects the ratio of total assets to total debt. Total assets are total debt plus equity. This covenant clause has a calculation basis. The covenant concerning leverage ratio and collateral coverage is referred to as total assets and equity and leverage ratio.

In a credit agreement, the covenant regarding leverage ratio is related to collateral coverage. The debtor’s leverage ratio is 10x, so the maximum collateral coverage ratio is 110%. If the debtor’s leverage ratio is 10x, the collateral coverage ratio is unlikely to reach 120%. A collateral coverage ratio of 120% can only provide a leverage ratio of 4x. This is explained in Table 1.

Table 1. Calculation of leverage and collateral coverage

|

No. |

Leverage (Debt / Equity) |

Maximum Collateral Coverage (Total Debt + Equity) / Total Debt) |

|

1. |

10 times |

11/10 x 100%= 110.00% |

|

2. |

8 times |

9 / 8 x 100% = 112.50% |

|

3. |

6 times |

7 / 6 x 100% = 116.67% |

|

4. |

4 times |

5 /4 x 100% = 120.00% |

|

5. |

2 times |

3 /2 x 100% = 150.00% |

The leverage ratio is a comparison between total debt or liabilities to equity. In addition, the collateral coverage ratio is the ratio of total assets to total debt. Total assets are the sum of total debt and equity. This is illustrated in Figure 2.

However, creditors do not believe that they can get good assets by obtaining a high collateral coverage ratio. Creditors tend to ask for a lot of collateral with a high level of collateral coverage. The debtor may not be able to provide a high collateral coverage ratio. The number of liabilities and equity limits the number of creditor assets. Thus, the debtor may not offer a lot of collateral and with a small number of assets. Creditors try to get a high collateral coverage ratio. If the debtor gives it, the debtor is likely to make a double or triple pledge on the same asset. Creditors and Debtors have different positions. The creditor is the master, and the debtor is the agent. Between agents and masters have different views. This is in line with Agency Theory.

Figure 1. Comparative of collateral coverage and collateral type

A double pledge or triple pledge is a fraud or violation of the credit agreement. The same asset is given as collateral to more than one creditor. This violation may lead to default for failing to provide guarantees to creditors. Creditor collateral must be free from guarantees to parties other than following the laws and regulations regarding guarantees.

Figure 2. Leverage ratio

In reality, cases of double pledges or triple pledges still occur in the real world. These cases have increased creditors’ distrust of debtors. The cost of granting credit is getting higher because of the higher risk. The collateral value determines the cost of credit. High credit costs result in high production costs. High production costs become a burden on society.

Creditors want to get the same position as other creditors according to the type of loan. Creditors like to have rights to the company’s assets following a loan, especially at the time of default. This is in line with the pari passu pro rata parte principle.

The principle of a negative pledge will provide a solution to achieve the pari passu pro-rata parte principle. Debtors do not pledge certain assets to certain creditors. All debtor assets become collateral to creditors. All creditors have equal rights to the debtor’s assets, including current, fixed, and other assets.

4.3 Agreements in negative pledge

As previously discussed, negative pledge is presently not directly regulated. However, there are two regimes of law that indirectly regulate negative pledge, which are contract and banking law. From the contract law point of view, a negative pledge is part of the loan agreement provisions and therefore shall be deemed as a valid clause as long as it fulfills the element of an agreement. Both parties in the loan agreement should have agreed that negative pledge is accepted as a collateral for creditor, which is a fulfillment of the element of consensus. Capability, on the other hand, is a subjective element and depend on the parties. As long as the individuals are not minor and is not under any form of guardianship, then they are capable. The third elements, the specific object clause, is clearly fulfilled as the loan agreement would specify the details of the agreement. The last element, the legal cause, however, would be a more debatable element. The non-existence of direct regulation of negative pledge invite a deeper analysis, mainly on economics point of view, that turns to be the main discussion of this section.

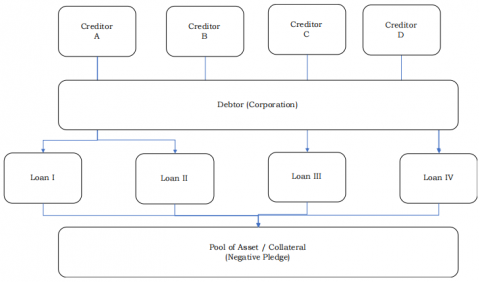

The negative pledge requires the abolition of the creditor’s special rights. Creditors must waive priority principle rights, net-off rights, and other preferential rights. Creditors have the same position as at the time of bankruptcy. All debtor assets become collateral to all creditors. Debtors do not differentiate between secured and unsecured creditors or between trade payable and loan payable. The schematic system is depicted in Figure 3. All creditors have collateral for company assets and creditor rights are based on the same loan amount and loan ratio. So that there are no creditors who are exaggerated in the ratio and type of loan. Each creditor knows the position of the other creditors.

Covenants for all creditors are the same. All creditors have the same covenants, such as leverage, collateral coverage, shareholding, dividend payouts, positive covenants, negative covenants, and affirmative covenants. A credit agreement is the same for all creditors. Creditors will know the number of existing creditors and the amount of a loan. Creditors allow new credit facilities as long as the leverage ratio is below the specified amount stated in the credit agreement.

Figure 3. Negative pledge

This credit agreement is known as a Master Credit Agreement (MCA). Every creditor who wants to provide a loan will sign this agreement. Each new creditor entering it will sign this agreement. The debtor will notify the new creditor of the existing creditors.

Debtors offer MCA to all creditors. If the debtor already has a loan, then all the agreements are combined into one. The contents of this agreement incorporate all covenants and clauses contained in all contracts. After this merger, each new creditor will co-sign the MCA. This clause opens the entry of new creditors with an obligation to notify the existing creditors. The debtor only informs them and does not require consent. New creditors will also get a list of the existing creditors and the loan amount. Thus, all creditors have the same position in the agreement. Creditors will not suspect each other. MCA regulates credit agreements. MCA complies with the pari passu principle.

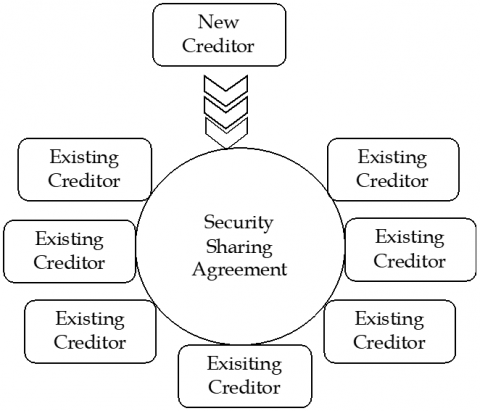

In addition to the MCA, creditors will sign a negative pledge agreement or Security Sharing Agreement (SSA). This SSA will stipulate that all debtor assets are collateral for all creditors in the MCA. Creditors have collateral but do not have specific collateral. Collateral in SSA is a mutual guarantee. Creditor supervision is the responsibility of all creditors. Figure 4 describes the SSA scheme.

The debtor agrees to the collateral. This agreement is called the Security Sharing Agreement (SSA). All debtor assets become one pool of assets that are pledged as collateral. All creditors are entitled to this pool of assets—the distribution of rights based on the portion of the loan that has been used. SSA complies with the pro-rata parte principle. Creditors may appoint a trustee as the manager of the MCA and SSA.

MCA and SSA are forms of implementation of the negative pledge principle. MCA and SSA also comply with the pari passu pro-rata parte principle. Creditors must leave certain privileges and rights to the collateral. Creditors have confidence that they are on the same level as other creditors.

With MCA and SSA, debtors and creditors will be more efficient in the loan agreement process. Credit and guarantee agreements already exist, so there are no additional fees for making agreements. Old and new creditors have confidence and trust in the debtor.

Figure 4. Security sharing agreement

The concept of MCA and SSA is common after debtors and creditors agree on a restructuring proposal. The restructuring proposal is signed by the creditors who agree to the debt restructuring with the debtor. The concept of MCA and SSA is moved to an earlier stage and is beneficial to all parties before bankruptcy occurs.

Debtors who have good performance and a good reputation can start offering negative pledges to creditors. The principle of the negative pledge will save the cost and time of debtors and creditors. Not all creditors can accept this negative pledge principle. Debtors rather than creditors offer standard clauses. A violation of the law regarding standard clauses does not apply here.

The implementation of a negative pledge must follow the regulations of the financial authorities in each country. Some financial rules require explicit guarantees for lending. Creditors, especially banks, will find it challenging to meet these requirements.

This implementation can be in the form of a combination of particular collateral to creditors and negative pledges. This implementation is a transition period before fulfilling the 100% negative pledge. The mixture can be 50% special or collateral to creditors, and 50% is a negative pledge. This combination is only for the value of the guarantee. The contents of the agreement remain the same as the MCA. The interests of creditors are guaranteed by the contents of the MCA credit agreement. Covenants governing debtors stay the same between creditors under the MCA. This scenario can still achieve the pari passu pro rata parte principle. The difference only occurs in the collateral owned by 50%.

From the law and economics theory perspective, a legal fortification of negative pledge through interpretation is desired and therefore, shall be adopted. The normative facts that the legal regime for negative pledge is already available yet, judicial interpretation is required. In a deeper analysis of the relationship between debtors and creditors, debtors and creditors have a dilemmatic relationship. Creditors need debtors, but creditors do not trust debtors. Creditors are not involved in the day-to-day management of the debtor’s business. The creditors do not trust the debtor in the credit agreement. Creditors and debtors have different positions. The relationship between debtors and creditors does not achieve the principle of fairness and equality. Meanwhile, the relationship between creditors also do not achieve the principles of fairness and equality.

The credit agreement fulfills the principle of fairness and equality is to provide a negative pledge principle in the credit agreement. Debtors can apply the negative pledge principle to all creditors.

The negative pledge will ensure open communication between creditors. identical creditor positions, identical loan guarantees, and an equal loan to creditor ratio. There are no hidden issues, ensuring that creditors receive their just compensation. The implementation of the negative pledge principle fulfills the pari passu pro rata parte principle.

In contrast with Singapore and The Netherlands, there is no specific regulation on negative pledge in Indonesia, however, ad hoc judges in bankruptcy courts have the rights to law making (rechtsvinding) through argumentum per analogiam or legal construction when there are third party resistance. This study has limitations regarding banking regulations that apply in each country. Research can be conducted to study the roles of curators and ad hoc judges in the cases of the distribution of bankrupt asset. Aside from that, further research can compare banking regulation between countries along with the administrative regulation with regard to securities. Laws regarding the implementation of negative pledges to the rules of each country can also be developed.

The funders had no role in study design, data collection, analysis, decision to publish or manuscript preparation.

[1] Rosińska-Bukowska, M., Zielinska-Lont, K., Nacewska-Twardowska, A., Brózda-Wilamek, D., Tomasz, M., Matuszewska-Pierzynka, A. (2020). Asia's global expansion: business and financial aspects. Wydawnictwo Uniwersytetu Łódzkiego.

[2] Amraoui, M., Jianmu, Y., Bouarara, K. (2018). Firm’s capital structure determinants and financing choice by industry in Morocco. International Journal of Management Science and Business Administration, 4(3): 41-51. https://doi.org/10.18775/ijmsba.1849-5664-5419.2014.43.1005

[3] Ramli, N.A., Latan, H., Solovida, G.T. (2019). Determinants of capital structure and firm financial performance—A PLS-SEM approach: Evidence from Malaysia and Indonesia. Quarterly Review of Economics and Finance, 71: 148-160. https://doi.org/10.1016/j.qref.2018.07.001

[4] Gassler, H., Pointner, W., Ritzberger-Grünwald, D., Dinges, M. (2018). Funding growth and innovation in Austria-financing conditions for SMEs and start-ups. Financial Stability Report, 36(May): 56-72. http://ec.europa.eu/DocsRoom/documents/15582/attachments/1/translations.

[5] Dogru, T., Sirakaya-Turk, E. (2017). The value of cash holdings in hotel firms. International Journal of Hospitality Management, 65: 20-28. https://doi.org/10.1016/j.ijhm.2017.05.004

[6] Adamu, I.Y. (2018). Idea of collateral and guarantor in Islamic bank financing. SEISENSE Journal of Management, 1(5): 49-57. https://doi.org/10.5281/zenodo.1474664

[7] Atkinson, N. (2020). Corporate liability, collateral consequences, and capital structure.

[8] Li, X. (2021). Creditor control rights in debt covenant violations and renegotiation: evidence from private debt agreements (Doctoral dissertation, Loughborough University). https://doi.org/10.26174/thesis.lboro.14807586.v1

[9] Ria, R., Nuryatno, M. (2018). Influence of Audit Quality, Pattern of Loans Concentration and Company Size to Banking Loans (Agency Problem of Creditor–Debtor at Manufacture Company in Indonesia). International Journal of Economics and Financial Issues, 8(4), 172-176. https://www.econjournals.com/index.php/ijefi/article/view/6283

[10] Vitolla, F., Raimo, N., Rubino, M. (2020). Board characteristics and integrated reporting quality: An agency theory perspective. Corporate Social Responsibility and Environmental Management, 27: 1152-1163. https://doi.org/10.1002/csr.1879

[11] Singh, K. (2019). The relationship between banker and customer. International Journal of Trend in Scientific Research and Development, 3(3): 1535-1537. https://doi.org/10.31142/ijtsrd23441

[12] Sgambati, S. (2019). The art of leverage: A study of bank power, money-making, and debt finance. Review of International Political Economy, 26(2): 287-312. https://doi.org/10.1080/09692290.2018.1512514

[13] Gyongyosi, G., Verner, E. (2018). Financial crisis, creditor-debtor conflict, and political extremism, Beiträge zur Jahrestagung des Vereins für Socialpolitik 2018: Digitale Wirtschaft. International Financial Markets II, F19-V3. http://hdl.handle.net/10419/181587

[14] Confessor, K.L.A., Santos, J.F. (2020). Covenants of Brazilian debentures: What is your role and what contributes to its use? International Journal of Business Management and Economic Research, 11(1): 1703-1709. http://www.ijbmer.com/docs/volumes/vol11issue1/ijbmer2020110101.pdf

[15] Sriwati. (2021). Legal protection for the creditor under the cross default and cross collateral clause in a credit agreement. Konfrontasi: Jurnal Kultural, Ekonomi, dan Perubahan Sosial, 8(1): 12-22. https://doi.org/10.33258/konfrontasi2.v8i1.137

[16] Ritonga, H.M., Hasibuan, H.A., Siahaan, A.P.U. (2017). Credit assessment in determining the feasibility of debtors using profile matching. International Journal of Business and Management Innovation, 6(1): 73-79. https://doi.org/10.31227/osf.io/ajd9z

[17] Albanez, T., Schiozer, R. (2021). The signaling role of covenants and the speed of capital structure adjustment under poor creditor rights: Evidence from domestically and cross listed firms in Brazil. Journal of Multinational Financial Management, 63: 100704. https://doi.org/10.1016/j.mulfin.2021.100704

[18] Abusharbeh, M.T. (2017). The impact of the banking sector on economic growth: An empirical analysis from the Palestinian economy. Journal of Emerging Issues in Economics, Finance, and Banking, 6(2): 2306-2316. https://doi.org/10.32479/ijefi.7369

[19] Johan, S. (2020). Material Adverse Change: An Alternative Solution to Suspension of the Debt Payment. Humaniora, 11(3): 211-218. https://doi.org/10.21512/humaniora.v11i3.6606

[20] Kurniawati, L., Sudarwanto, A.S. (2019). Legal protection for creditors due to debitor default in bank loan agreements. The International Journal of Social Sciences and Humanities Invention, 6(11): 5698-5701. https://doi.org/10.18535/ijsshi/v6i11.02

[21] Kovacova, M., Kliestik, T., Kubala, P., Valaskova, K., Radišić, M.M., Borocki, J. (2018). Bankruptcy models: Verifying their validity as a predictor of corporate failure. Polish Journal of Management Studies, 18(1): 167-179. https://doi.org/10.17512/pjms.2018.18.1.13

[22] Casey, A.J. (2020). Chapter 11’s Renegotiation Framework and The Purpose of Corporate Bankruptcy. Columbia Law Review, 120(7): 1709-1770. https://dx.doi.org/10.2139/ssrn.3353871

[23] Kamahayani, M., Margono, F.X.S. (2020). Penerapan asas pari passu pro rata parte terhadap pemberesan harta pailit PT. Dhiva Inter Sarana dan Richard Setiawan (Studi Kasus Mahkamah Agung Republik Indonesia Nomor 169 PK/PDT.SUS-PAILIT/2017). Jurnal Hukum Adigama, 3(1): 71-91. https://doi.org/10.24912/adigama.v3i1.8892

[24] Winanto, Sulistiyono, A., Muryanto, Y.T. (2019). Analysis of equality on the creditor standing principle on the process of arrangement and settlement of bankruptcy assets in Indonesia. 3rd International Conference on Globalization of Law and Local Wisdom, 358(ICGLOW 2019): 286-288. https://doi.org/10.2991/icglow-19.2019.71

[25] Fauzi, A. (2020). Legal satisfaction for the creditors to obtain a return of the credit from the debtor. Budapest International Research and Critics Institute (BIRCI-Journal): Humanities and Social Sciences, 3(1): 428-436. https://doi.org/10.33258/birci.v3i1.788

[26] Lipschütz, I., Schwarz, M.E. (2020). Fairness Vs. Economic Efficiency: Lessons from an Interdisciplinary Analysis of Talmudic Bankruptcy Law. Review of Law and Economics, 16(3): 45-57. https://doi.org/10.1515/rle-2016-0070

[27] Morozova, O., Kichalyuk, O. (2021). On the issue of bankruptcy of a peasant (farm) economy. In E3S Web of Conferences, 273: 08036. https://doi.org/10.1051/e3sconf/202127308036

[28] Gohil, A.S. (2020). The ‘Great Game’ of sovereign debt restructuring: Solving the holdout problem. A Critical Analysis of the Pari Passu and Collective Action Clauses in International Sovereign Bond Contracts. Journal of Law and Jurisprudence, 26-54. https://doi.org/10.14324/111.2052-1871.125

[29] Shubhan, M.H. (2020). Legal protection of solvent companies from bankruptcy abuse in Indonesian legal system. Academic Journal of Interdisciplinary Studies, 9(2): 142-148. https://doi.org/10.36941/ajis-2020-0031

[30] NML Capital Ltd et al. vs. the Republic of Argentina, Nos 08 Civ 6978 (TPG), 09 Civ 1707 (TPG), and 09 Civ 1708 (TPG) (SDNY 11 November 2012). https://www.supremecourt.uk/cases/uksc-2010-0040.html

[31] Kim, S.H. (2014). Pari passu: The nazi gambit. Capital Markets Law Journal, 9(3): 242-250. https://doi.org/10.1093/cmlj/kmu015

[32] Olivares-Caminal, R. (2017). The definition of indebtedness and the consequent imperilling of the pari passu, negative pledge, and cross-default clauses in sovereign debt instruments. Capital Markets Law Journal, 12: 164-179. https://doi.org/10.1093/cmlj/kmx021

[33] FHR European Ventures LLP and Others vs. Cedar Capital Partners LLC [2014] UKSC 45 at 1. See also Knighthead Master Fund LP and Others vs. the Bank of New York Mellon and another [2014] EWHC 3662 (Ch) at 2. https://en.wikipedia.org/wiki/FHR_European_Ventures_LLP_v_Cedar_Capital_Partners_LLC

[34] Olivares-Caminal, R. (2017). The definition of indebtedness and the consequent imperilling of the pari passu, negative pledge, and cross-default clauses in sovereign debt instruments. Capital Markets Law Journal, 12: 164-179. https://doi.org/10.1093/cmlj/kmx021

[35] Jokubauskas, R., Swierczynski, M., Balsiukiene, A. (2021). A stay of individual enforcement actions as a basis for effectie restructuring proceedings. International Compartive Jurisprudence, 7(1): 115-125. https://doi.org/10.13165/j.icj.2021.06.009

[36] Galvis, S.J. (2017). Solving the pari passu puzzle: The market still knows best. Capital Markets Law Journal, 12(2): 204-214. https://doi.org/10.1093/cmlj/kmx019

[37] Yono, S., Sulistiyono, A., Mashdurohatun, A., Sari, R.M. P. (2020). Reconstruction of separate-creditor positions in the process declaring bancruptcy in indonesia based on justice value. Scholars International Journal of Law, Crime and Justice, 3(11): 334-341. https://doi.org/10.36348/sijlcj.2020.v03i11.001

[38] Rusiana, A., Wiwoho, J., Sulistiyono, A., Indonesia, S., Indonesia, S., Indonesia, S. (2020). The legal status of appraisal of materials guarantee for bancruptcy process of indonesia. Journal of Social Sciences Research, 16: 1-12. https://doi.org/10.24297/jssr.v16i.8787

[39] Sunarmi, Yunara, E., Simaremare, S.P., Nasution, B. (2021). Reviewing the comparison of the legal bankruptcy system between indonesia and the netherlands. Turkish Journal of Computer and Mathematics Education (TURCOMAT), 12(6): 2290-2296. https://doi.org/10.17762/turcomat.v12i6.4834

[40] Simanjuntak, H.A. (2019). Penyelesaian utang debitur terhadap kreditur melalui kepailitan. Justiqa, 1(1): 8-16. http://dx.doi.org/10.36764/justiqa.v1i1.221

[41] Coyle, J. (2018). Interpreting Contracts Without Context. American University Law Review, 67(6): 1673-1717. https://ssrn.com/abstract=3155486

[42] Hartenfels, H. (2018). European Master Agreement (EMA)–structure and new developments. Keynote speech Financial stability and the ECB, 225. https://www.ecb.europa.eu/pub/pdf/other/ecb.escblegalconferenceproceedings201812.en.pdf

[43] Johan, S. (2021). Separatist creditors’ problems on the postponement of debt payment obligations based on the Supreme Court’s decree number 30/KMA/SK/I/2020. Fiat Justisia: Jurnal Ilmu Hukum, 15(3): 207-220. https://doi.org/10.25041/fiatjustisia.v15no3.1956

[44] Prastika, K.S.D., Marwanto, Sukranatha, A.A.K. (2017). Kedudukan kreditur dalam perjanjian kredit dengan jaminan hak milik atas tanah berdasarkan Undang-Undang Nomor 4 Tahun 1996 tentang hak tanggungan beserta benda-benda yang berkaitan dengan tanah. Kertha Semaya: Jurnal Ilmu Hukum, 5(1): 1-14. https://ojs.unud.ac.id/index.php/kerthasemaya/article/view/40234

[45] Lie, G., Saly, J.N., Gunadi, A., Tirayo, A.M. (2019). Problematika UU No. 37 Tahun 2004 tentang kepailitan dan PKPU terhadap bank sebagai kreditor separatis. Jurnal Bakti Masyarakat Indonesia, 2(2): 159-168. https://doi.org/10.24912/jbmi.v2i2.7242

[46] Anggraeny, I., Fauzia, A., Esfandiari, F., Hidayah, N. P., Al-Fatih, S., Ayu, I.K. (2021). Execution of Mortgage Object Against Bankruptcy Debtors. In 2nd International Conference on Law Reform (INCLAR 2021), 75-79 https://doi.org/10.2991/assehr.k.211102.170

[47] Lawalata, I.L.D. (2017). Pemenuhan hak eksekusi kreditur separatis dalam penjaminan dari perspektif undang-undang kepailitan. Akmen Jurnal Ilmiah, 14(2): 369-380. https://e-jurnal.nobel.ac.id/index.php/akmen/article/view/30

[48] Saptanti, N., Sulistiyono, A., Harahap, B. (2021). Debt guarantee charging based on the justice principal. Journal of Advances in Social Science and Humanities, 7(4): 1461-1467. https://doi.org/10.15520/jassh.v7i4.593

[49] Putri, N.P.W.A., Artha, I.G. (2020). Perlindungan hukum pihak ketiga pada perkara kepailitan. Kertha Negara, 8(3): 1-12. https://ojs.unud.ac.id/index.php/Kerthanegara/article/view/61563

[50] Dewi, W.W., Tjatrayasa, I.M. (2017). Akibat hukum penundaan kewajiban pembayaran utang terhadap status sita dan eksekusi jaminan ditinjau dari Undang-undang Nomor 37 Tahun 2004. Kertha Semaya: Jurnal Ilmu Hukum, 5(1): 1-6. https://ojs.unud.ac.id/index.php/kerthasemaya/article/view/19129

[51] Fitria, A. (2018). Penundaan kewajiban pembayaran utang sebagai salah satu upaya debitor mencegah kepailitan. Lex Jurnalica (Journal of Law), 15(1): 18-28. https://ejurnal.esaunggul.ac.id/index.php/Lex/article/view/2291

[52] Baird, D.G. (2017). Pari passu clause and the skeuomorph problem in contract law. Duke Law Journal Online, 67: 84-101. https://scholarship.law.duke.edu/dlj_online/31/

[53] Niven, P. (2017). The anti-deprivation rule and the pari passu rule in insolvency. Insolvency Law Journal, 25(1877): 5-28. https://www.buddlefindlay.com/insights/the-anti-deprivation-rule-and-the-pari-passu-rule-in-insolvency/

[54] Disemadi, H.S., Gomes, D. (2021). Perlindungan hukum kreditur konkuren dalam perspektif hukum kepailitan di Indonesia. Jurnal Pendidikan Kewarganegaraan Undiksha, 9(1): 123-134. https://doi.org/10.23887/jpku.v9i1.31436

[55] Christy, E., Wilsen, W., Rumaisa, D. (2020). Kepastian hukum hak preferensi pemegang hak tanggungan dalam kasus kepailitan. Kanun Jurnal Ilmu Hukum, 22(2): 323-344. https://doi.org/10.24815/kanun.v22i2.14909

[56] Husni, R.M.T. (2020). Kedudukan kreditur hak tanggungan dalam kepailitan. Supremasi Hukum, 16(2): 104-113. https://doi.org/10.33592/jsh.v16i2.747

[57] Olivares-Caminal, R. (2017). The definition of indebtedness and the consequent imperilling of the pari passu, negative pledge, and cross-default clauses in sovereign debt instruments. Capital Markets Law Journal, 12: 164-179. https://doi.org/10.1093/cmlj/kmx021

[58] Sinaga, N.A. (2018). Peranan asas-asas hukum perjanjian dalam mewujudkan tujuan perjanjian. Binamulia Hukum, 7(2): 107-120. https://doi.org/10.37893/jbh.v7i2.20

[59] Matri, D. (2017). Re-evaluation: Collectivisation of creditor protection through private governance. Covenants and Third-Party Creditors, 147-165. https://doi.org/10.1007/978-3-319-62036-7_9

[60] Komara, A. (2014). Tinjauan Yuridis Obligasi Sebagai Objek Dalam Pernyataan Penjaminan Negatif (Negative Pledge). http://repository.uinjkt.ac.id/dspace/handle/123456789/24972.

[61] Utama, D.I.S. Hariyanto, Hawin, M. (2015). Tinjauan yuridis fasilitas kredit modal kerja yang dijamin kondisi negative pledge dalam operasional di pt. BANK MANDIRI (PERSERO) TBK. http://etd.repository.ugm.ac.id/penelitian/detail/92134

[62] Putri, S.A. (2017). Analisis penerapan negative pledge sebagai jaminan dalam pemberian kredit pada pt bank xyz tbk = Practical review of negative pledge as a loan security at pt bank x tbk. https://lontar.ui.ac.id/detail?id=20444994&lokasi=lokal

[63] Bjerre, C.S. (1999). Secured transactions inside out: Negative pledge covenants, property, and perfection. Cornell Law Review, 84(2): 305. https://scholarship.law.cornell.edu/clr/vol84/iss2/1

[64] Crabb, J. (2020). Lawmaking in Argentina on hold as country and creditors await debt restructuring. International Financial Law Review. https://pesquisa.bvsalud.org/global-literature-on-novel-coronavirus-2019-ncov/resource/pt/covidwho-823968

[65] Sonhaji, S. (2018). The position of the workers’ or laborers’ severance pay and other rights in the bankruptcy of a company. Diponegoro Law Review, 3(2): 165. https://doi.org/10.14710/dilrev.3.2.2018.165-181

[66] Ramadayanti, S.L. (2020). Position of Tax Debt and Labour Right: Legal Review. Journal La Sociale, 1(4): 1-8. https://doi.org/10.37899/journal-la-sociale.v1i4.131

[67] Mertokusumo, S. (2007). Penemuan Hukum: Sebuah Pengantar.

[68] Wahyuni, N. (2018). Penerapan prinsip 5C dalam pemberian kredit sebagai perlindungan bank. Lex Journal: Kajian Hukum & Keadilan, 1(1): 1-20. https://doi.org/10.25139/lex.v1i1.236

[69] Eprianti, N. (2019). Penerapan prinsip 5C terhadap tingkat non performing financing (Npf). Amwaluna: Jurnal Ekonomi dan Keuangan Syariah, 3(2): 252-266. https://doi.org/10.29313/amwaluna.v3i2.4645

[70] Marzuki, P. M. (2006). Penelitian Hukum (2nd Edition). Kencana Prenada Media Group. P. 35.