Meshal Harbi Odah

© 2021 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Unemployment is an economic and social phenomenon that has many effects and problems that directly affect society and could result in many problems in the future. Therefore, it is one of the most significant challenges confronting the globe today, as unemployment rates have reached critical levels. The aim of the research is to predict the unemployment rate for the coming years through the Markov chains method. The current variables of a particular phenomenon are analyzed in order to predict future variables to the phenomenon itself. The results indicated that the probability of an increase in the unemployment rate in the coming period, followed by a decrease in the unemployment rate and, finally, stability. The present findings can help decision makers to make the right decisions to face the problem of unemployment.

unemployment, Markov chains, stochastic processes, transition probabilities

Unemployment is a multifaceted phenomenon with numerous facets. It is an economic phenomenon and is one of the most important economic problems faced by most countries in the world, regardless of their economic and political systems. Because of its social consequences, unemployment threatens both developed and developing countries, and it is regarded as one of the world's most serious crises at the moment.

Iraq is considered one of the countries rich in its economic resources and diversified in their forms in large quantities, which is supposed to be at the forefront of the industrialized countries and also operating levels at the highest level. According to the central Statistical Organization, the unemployment rate in Iraq in 2019 reached more than 30%, with more than 750,000 foreign workers.

The unemployment and macroeconomic projections emerged in the mid-90s. Besides, early detection of socioeconomic difficulties in order to plan for an economy-wide reduction in unemployment is critical for sound economic decision-making and sound policymaking. Particularly because of its association with the country's business cycle and its influence on monetary policy, the unemployment rate for any country is one of the key economic indicators in the financial market [1].

The process of predicting the future behavior of the studied phenomenon plays an important role in many areas such as socio-economic to reach the expected results. There are many studies looking at prediction in the previous literature. For example, Odah [2] used the ARIMA method to model the prediction of the urban population growth rate. Chakraborty et al. [3] studied unemployment Rate Forecasting by using a Hybrid approach. Vicente et al. [4] employed ARIMA models to discover the rapid increases in unemployment caused by the Spanish economic crisis. In Canada, Khan Jaffur et al. [5] demonstrated that nonlinear time series models reflect the asymmetry in the unemployment rate series better at short and long forecast horizons. Montgomery et al. [6] used the asymmetric cyclical conduct of unemployment numbers and reported that significant enhancements can be made in prediction accuracy over existing approaches. In the U.S., Nagao et al. [7] examined if data from Google Trends contribute to the unemployment rate nowcasting in comparison to the classic AR model. Feuerriegel and Gordon [8] established a paradigm of semantic paths to give comprehensive interpretability of financial news macro-economic indicators. The results showed that the approach proposed allows an exciting technique of precisionizing macroeconomic projections. Galbraith and van Norden [9] stated they found solid proof of asymmetric forecast error, which increases with the forecast horizon; it also revealed significant disparities in forecasting.

According to the above survey, not all of this literature mentions unemployment rate prediction via Markov chains. This is where the importance of research begins. Therefore, the aim of the research is to predict the unemployment rate for some coming years in Iraq using Markov chains, one of the statistical methods to find the matrix of transitional probabilities to reach the stable distribution series of probabilistic cases in which the vocabulary of the study sample is transmitted during different periods of time based on the transition probabilities series of random variables $\gamma_{n+1}$ that is independent of the previous states $\left(\gamma_{1}, \gamma_{2}, \ldots, \gamma_{\mathrm{n}-1}\right)$ provided that the state of the variable is known at the time of transition. The paper is organized as follows. Section II transitional probabilities matrix and its estimation, in the following subsections, transitional conditional probabilities and estimating transitional probabilities. Section III will be the data analysis & results, finally conclusions.

2.1 Transitional conditional probabilities

Markov chain is a method by which current variables of a particular phenomenon are analyzed in order to predict future variables of the same phenomenon. It is a special case of random processes. The Markov chain was chosen for prediction because it depends on one previous period the probability of the process happening in the future depends only one previous period without relying on all past events, Markov chain is interpreted as a sequence of states that can form a system in a period of time.

Markov processes are mainly based on transitional conditional probabilities can be expressed as follows:

$\mathrm{P}_{\mathrm{mh}}=\operatorname{Pr}\left(\gamma_{\mathrm{k}+1=\mathrm{h}} / \gamma_{\mathrm{k}=\mathrm{m}}\right) \quad 0<\mathrm{P}_{\mathrm{mh}}<1$ (1)

where, $\mathrm{P}_{\mathrm{mh}}$ represents the probability of the singular transition from the state $(\mathrm{m})$ to $(\mathrm{h})$ in a certain period of time.

The random variable of a probability Markov matrix is transmitted by $\mathrm{P}_{\mathrm{mh}}$ which expresses the probability of moving from the state $(\mathrm{m})$ to $(\mathrm{h})$ over one time interval, putting all these states into one table gives us a square matrix of degree $(\mathrm{k} * \mathrm{k})$. Thus, the matrix of transitional probabilities can be expressed as follows [10]:

$\mathrm{P}=\left[\begin{array}{ccc}\mathrm{p}_{11} & \mathrm{p}_{12} & \cdots & \mathrm{p}_{1 \mathrm{k}} \\ \mathrm{p}_{21} & \mathrm{p}_{22} & \cdots & \mathrm{p}_{2 \mathrm{k}} \\ \vdots & \vdots & & \vdots \\ \mathrm{p}_{\mathrm{k} 1} & \mathrm{p}_{\mathrm{k} 2 \ldots} & \mathrm{p}_{\mathrm{kk}}\end{array}\right]$ (2)

It is a positive matrix of degree $(\mathrm{k} * \mathrm{k})$ elements of non-negative.

We will find the probability of moving the singular from $(\mathrm{m})$ to $(\mathrm{h})$ by a specified amount of time (t) can be expressed as follows [11]:

$\mathrm{P}=\mathrm{P}\left\{\gamma_{\mathrm{kt}=\mathrm{h}} / \gamma_{\mathrm{k}=\mathrm{m}}\right\}$ (3)

We will express Eq. (3):

$\mathrm{P}_{\mathrm{k}+\mathrm{t}}=\mathrm{P}_{\mathrm{k}} * \mathrm{P}_{\mathrm{t}}$ (4)

where, $\mathrm{P}_{\mathrm{k}+\mathrm{t}}$ represents the transition probability matrix of a Markov chain.

2.2 Estimating transitional probabilities

To estimate a Markov chain, the transition from the state m at the time of the transition (t) to state at the time of the transition (t+1) [12].

$\operatorname{Pr}\left(\gamma_{0}, \gamma_{1}, \ldots, \gamma_{\mathrm{t}}\right)=\operatorname{Pr}\left(\gamma_{0}\right) \prod_{\mathrm{t}} \mathrm{p}\left(\gamma_{\mathrm{t}} / \gamma_{\mathrm{t}-1}\right)$ (5)

Suppose that $\eta_{\mathrm{mh}}^{(\mathrm{t})} \mathrm{equal}\left[\begin{array}{c}\gamma_{\mathrm{t}}=\mathrm{h} \\ \gamma_{\mathrm{t}-1}=\mathrm{m}\end{array}\right]$ then:

$\eta_{\mathrm{mh}}=\sum \eta_{\mathrm{mh}}(\mathrm{t})$ (6)

$\eta_{\mathrm{mh}}=\operatorname{Pr}\left(\gamma_{0}\right) \prod_{t} \operatorname{Pr}\left(\mathrm{p}_{\mathrm{mh}}^{\eta \mathrm{mh}}\right)$ (7)

$\eta_{\mathrm{mh}}=\theta_{\mathrm{m}} \mathrm{p}_{\mathrm{mh}}$ (8)

Taking the logarithm of the Eq. (7).

$\log \operatorname{Pr}\left(\gamma_{0}, \gamma_{1}, \ldots, \gamma_{\mathrm{t}} / \mathrm{n}\right)=\sum_{\mathrm{m}} \theta_{\mathrm{m}}\left(\sum_{\mathrm{h}}\left(\mathrm{P}_{\mathrm{mh}}-1\right)\right)$ (9)

where:

$\sum \eta_{\mathrm{mh}}=\hat{\theta}_{\mathrm{m}} \sum \widehat{\mathrm{P}}_{\mathrm{mh}} \quad, \sum \mathrm{P}_{\mathrm{mh}}=1$

$\sum \eta_{\mathrm{mh}}=\hat{\theta}_{\mathrm{m}}$ (10)

Finally, we get the estimation equation as shown below:

$\widehat{\mathrm{P}}_{\mathrm{mh}}=\eta_{\mathrm{mh}} / \sum_{\mathrm{h}} \eta_{\mathrm{mh}}$ (11)

Data were collected Central Statistical Organization Iraq (CSO) for the period from 2008 to 2019 through the website (http://cosit.gov.iq/en/) this period was chosen due to the political and economic conditions that Iraq went through which affected various aspects of life, including unemployment. The prediction process is carried out through the use of Markov chains by forming a transitional probability matrix, which is a square matrix called the stable transitional probability matrix of Markov chains. The data was divided into three states (high, low, stability) in order to use Markov chains to form a transitional probabilities matrix it is a square matrix (3*3) can be expressed matrix as follows:

$\mathrm{q} 1 \quad \mathrm{q} 2 \quad \mathrm{q} 3$

$\widehat{\mathrm{P}}=\begin{aligned}&\mathrm{q} 1 \\&\mathrm{q} 2 \\&\mathrm{q} 3\end{aligned}\left[\begin{array}{lll}\mathrm{p}_{11} & \mathrm{p}_{12} & \mathrm{p}_{13} \\ \mathrm{p}_{21} & \mathrm{p}_{22} & \mathrm{p}_{23} \\ \mathrm{p}_{31} & \mathrm{p}_{32} & \mathrm{p}_{33}\end{array}\right]$

where:

$\mathrm{q} 1$: The case of high unemployment rate.

$\mathrm{q} 2$: The case of low unemployment rate.

$\mathrm{q} 3$: The case of the stability unemployment rate.

$\mathrm{p}_{11}$: The possibility of high in the unemployment rate after it was high.

$\mathrm{p}_{12}$: The possibility of high in the unemployment rate after it was low.

$\mathrm{p}_{13}$: The possibility of high in the unemployment rate after it was stable.

$\mathrm{p}_{21}$: The possibility of low in the unemployment rate after it was high.

$\mathrm{p}_{22}$: The possibility of low in the unemployment rate after it was low.

$\mathrm{p}_{23}$: The possibility of low in the unemployment rate after it was stable.

$\mathrm{p}_{31}$: The possibility of stable in the unemployment rate after it was high.

$\mathrm{p}_{32}$: The possibility of stable in the unemployment rate after it was low.

$\mathrm{p}_{33}$: The possibility of stable in the unemployment rate after it was stable.

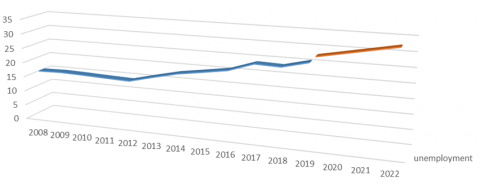

After determining the cases that the transitional matrix is going through, from high, low and stable unemployment rates, we will draw a series of unemployment rate data for the period from 2008 to 2019 as shown in the Figure 1.

Figure 1 shows that the time series of the unemployment rates in previous years, it increased according to official statistics. Where the horizontal axis represents the years of the time series and the vertical axis represents the unemployment rates of the series.

In this paragraph, we try to study the time series of unemployment rates according to the Markov series for the time period from 2008 to 2019 and with different age groups in order to convert the data into a Markov series formula The age groups were divided as a first step, represented by the class and the state to be used in the Markov chain. Several assumptions were made to include all cases and how these cases move to form the transition matrix.

Through the Table 1 below, the time series of the unemployment rate according to the Markov series is studied for different age groups ranging from 18 years to more than 46 years for males and females.

Based on these assumptions, we will show the movement of a Markov chain in the transition matrix for the years from 2008 to 2019.

Table 1. The age groups ranging from 18 years to more than 46 years for males and females

|

Class |

State |

|

18-30 |

S1 |

|

31-45 |

S2 |

|

and more 46 |

S3 |

Through the data in Table 2, the probability matrix is formed, which is a matrix of transition from any state to another state in one time unit these data describe the movement of the time series of unemployment for age groups, so we can show the estimated movement of the unemployment rate from one case to another for the years 2008 to 2019.

From Table 3, we get a random matrix, which reflects the initial assumptions about the estimated movement of unemployment rates.

Figure 1. The plot of time series for the unemployment rates of the for the period (2008 to 2019)

Table 2. Unemployment rates for the years from 2008 to 2019 distributed by age groups

|

q3 |

q2 |

q1 |

States |

|

21.3 |

13 |

25.7 |

2008 |

|

19.3 |

14.7 |

23.1 |

2009 |

|

20.7 |

17.5 |

22.9 |

2010 |

|

18.8 |

20.2 |

21.3 |

2011 |

|

16.2 |

23.8 |

26.6 |

2012 |

|

19.5 |

25.3 |

24.2 |

2013 |

|

20.1 |

24.7 |

25.4 |

2014 |

|

22.3 |

25.9 |

22.7 |

2015 |

|

21.8 |

25.7 |

26.8 |

2016 |

|

22.6 |

26.4 |

25.7 |

2017 |

|

24.3 |

25.2 |

28.3 |

2018 |

|

24.9 |

26.3 |

28.9 |

2019 |

Table 3. The estimated movement for the years from 2008 to 2019

|

q3 |

q2 |

q1 |

q0 |

qi-1/qi |

|

0 |

0 |

0 |

0 |

q0 |

|

0 |

0.17 |

0.22 |

0.61 |

q1 |

|

0.46 |

0.2 |

0.34 |

0 |

q2 |

|

0.43 |

0.57 |

0 |

0 |

q3 |

Figure 2. Time series of high unemployment rates

Table 4. Stable distribution steps

|

Matrix $P_{m h}$ |

Matrix (M.L.E) |

|

$p_{11}$ |

0.31 |

|

$p_{12}$ |

0.47 |

|

$p_{13}$ |

0.263 |

|

$p_{21}$ |

0.51 |

|

$p_{22}$ |

0.221 |

|

$p_{23}$ |

0.321 |

|

$p_{31}$ |

0.17 |

|

$p_{32}$ |

0.20 |

|

$p_{33}$ |

0.7 |

|

Stable Distribution |

Step (9) |

|

q1 |

0.997 |

|

q2 |

0.002 |

From Table 4, the results show that the probability of a rise in the unemployment rate is (0.997) and the probability of a decrease in the unemployment rate (0.002) while the probability of stability zero. Therefore, the unemployment rate is probability too high in the foreseeable future, and then the unemployment rate begins to low and finally, stability according to the Markov transition series.

According to Figure 2, the time series of unemployment rates will continue to high and this is due to the economic conditions that most countries are going through due to the current economic recession because of its social effects.

In this paper, through the results of the research, we conclude that unemployment rates will be high in the coming years and for all age groups that were divided in the Table 1. According to the current results from Table 4, it is evident the probability of a rise in the unemployment rate is (0.997) and the probability of a decrease in the unemployment rate (0.002), while the probability of stability is zero. Thus, the unemployment rate is high in the foreseeable future, and then the unemployment rate begins to fall, and finally, stability. Therefore, we recommend the relevant authorities to review this study to know the predictive possibilities in the future and find solutions to address the high rates of unemployment among all age groups in question, because unemployment has a lot of effects on society.

[1] Blanchard, O.J., Leigh, D. (2013). Growth forecast errors and fiscal multipliers. American Economic Review, 103(3): 117-120.

[2] Odah, M.H. (2020). Comparison of Box-Jenkins models predicting Iraq’s population growth rate. In IOP Conference Series: Materials Science and Engineering, 928(4): 042045.

[3] Chakraborty, T., Chakraborty, A.K., Biswas, M., Banerjee, S., Bhattacharya, S. (2021). Unemployment rate forecasting: A hybrid approach. Computational Economics, 57(1): 183-201. https://doi.org/10.1007/s10614-020-10040-2

[4] Vicente, M.R., López-Menéndez, A.J., Pérez, R. (2015). Forecasting unemployment with internet search data: Does it help to improve predictions when job destruction is skyrocketing? Technological Forecasting and Social Change, 92: 132-139. https://doi.org/10.1016/j.techfore.2014.12.005

[5] Khan Jaffur, Z.R., Sookia, N.U.H., Nunkoo Gonpot, P., Seetanah, B. (2017). Out-of-sample forecasting of the Canadian unemployment rates using univariate models. Applied Economics Letters, 24(15): 1097-1101. https://doi.org/10.1080/13504851.2016.1257208

[6] Montgomery, A.L., Zarnowitz, V., Tsay, R.S., Tiao, G.C. (1998). Forecasting the US unemployment rate. Journal of the American Statistical Association, 93(442): 478-493. https://doi.org/10.2307/2670094

[7] Nagao, S., Takeda, F., Tanaka, R. (2019). Nowcasting of the US unemployment rate using Google Trends. Finance Research Letters, 30: 103-109. https://doi.org/10.1016/j.frl.2019.04.005

[8] Feuerriegel, S., Gordon, J. (2019). News-based forecasts of macroeconomic indicators: A semantic path model for interpretable predictions. European Journal of Operational Research, 272(1): 162-175. https://doi.org/10.1016/j.ejor.2018.05.068

[9] Galbraith, J.W., van Norden, S. (2019). Asymmetry in unemployment rate forecast errors. International Journal of Forecasting, 35(4): 1613-1626. https://doi.org/10.1016/j.ijforecast.2018.11.006

[10] Rykov, V.V., Balakrishnan, N., Nikulin, M.S. (2010). Mathematical and Statistical Models and Methods in Reliability: Applications to Medicine, Finance, and Quality Control. Springer Science & Business Media.

[11] Knill, O. (1994). Probability and Stochastic Processes with Applications. Havard Web-Based, 5.

[12] Eberle, A., Marinelli, C. (2007). Stability of sequential Markov chain Monte Carlo methods. In ESAIM: Proceedings, 19: 22-31.