Artur Zhavoronok | Olha Popelo* | Roman Shchur | Natalia Ostrovska | Natela Kordzaia

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Households play one of the key roles in the development of the financial system of any country and the national economy in general. It is the understanding of the behavior of these economic entities in the market of financial services that makes it possible to predict the development of such a market, to understand the mechanisms of the emergence of dissipative processes in the interaction of households and financial institutions, which can form crisis phenomena in the development of such a system and restrain the innovative development of the national economy. This determines the importance and relevance of further research in this direction. Within the article, the impact of modern digital technologies on the development of financial services, in particular financial behavior of households, in the conditions of the formation and active development of the innovative economy is considered. Significant attention is paid to the specification of the methodology for determining the impact of the digitization index and the index of the model transformation of financial behavior of households. It is established that the outlined models are specific and different between various regions in any country. That is why the above method of calculation was used on the example of Ukraine. As a result, information was obtained on the digitalization index, and the transformation index of the financial behavior model of households in twenty-four regions of Ukraine. Based on the use of econometric analysis, algebraic equations of the dependence of the transformation index of the model of financial behavior of households on the digital technologies development in each of the outlined regions were determined.

innovative economy, national economy, financial behavior of households, digitalization, digital technologies, regional model of financial behavior

Today, new technologies are radically changing our lives, penetrating all spheres of human life. Such technologies ultimately form a new model of the national economy development – the innovative economy. Innovations play a key role in the development of virtually all sectors and spheres of economy; they are actively used in the social sphere. A separate specific feature of the innovative economic development is the process when innovative technologies, products give a new impetus to the development of new innovative technologies that in a short time penetrate economy and transform a significant number of economic processes, increase resource efficiency, and the effectiveness of economic systems.

A special role in the innovative development of the national economy today is played by digital technologies, which are directly related to the development of new information and communication technologies, their improvement and dissemination to various spheres of society. Such technologies play an important role in the financial system development of the most developed countries, especially in the development of services.

Active development and implementation of financial technologies are already commonplace in the operation of any banking and non-banking institutions. In fact, such technologies are already an integral component of ensuring the competitiveness of such institutions in the financial services market, as they can both improve the quality of service and increase the efficiency of their operation.

Digital technologies play an important role in the financial services provision. These innovations expand the capacity of financial institutions to provide better, more thoughtful, high-quality services to their customers, especially households. Today, no one is surprised by the opportunity to quickly make a payment, transfer funds, take a loan, get an insurance policy without visiting financial institutions. Households have experienced the positive impact of digital technologies in the field of financial services the most among all economic entities, and the development of such technologies continues, which allows us to speak with confidence about new transformations in this area in the future.

Digital technologies have not only improved the functioning of financial services, they have had a very serious impact on the transformation of financial behavior of households in general, partly changing the demand for financial services, ways to obtain them, interaction with financial institutions. Digital technologies have also helped to increase the financial inclusion level in the world, make financial services more accessible, better and easier to use. Thus, households living in different regions of the world, countries, individual territories, the opportunities to use financial services have become better. However, information and communication technologies, the level and quality of their development play an important role in providing such an opportunity. It is clear that their development in different areas differ. This situation, given the significant pace of the digital technologies development in the financial sector, also partially determines the conditions for the formation of different models of financial behavior of households, which are also affected by a wide range of factors.

Thus, we can observe different patterns of household’s financial behavior in different parts of each country, although all of them, without exception, have already been affected by digital technologies. Today, it is quite clear that digital technologies not only affect, but also objectively and irrevocably change the financial behavior of households in the market of financial services, producing new, still little-researched systemic risks for the financial system and forming various opportunities for these economic subjects to influence stability of this system. However, the understanding that the development of households in different regions of the country partially depends on regional economic factors gives reason to state that it is impossible to thoroughly study the models of financial behavior of households without taking into account regional differences between them. Thus, the matter of determining how new digital technologies affect different models of financial behavior of households that have developed in certain regions, which impact is the same for such models, and their differences are due to other factors, becomes relevant. In our opinion, the outlined issues are relevant and require new research in this area.

The article analyzes the impact of the digitization index and changes in the transformation index of regional models of financial behavior of households in certain regions of the country based on the research methodology developed by the authors. As a result, it was established that the impact of digitalization on economic processes is heterogeneous. Accordingly, different models of financial behavior of households were formed, the essence of which depends on a significant number of factors. It has been established that there is a need to develop various measures to influence households from different regions in order to encourage them to use digital technologies when using financial services.

The article has the following structure: 2. Literature review. 3. Methodology. 4. Presenting main material. 5. Conclusions.

Today, the world economy is actively digitalizing. The concept of digitization, more precisely - "digital literacy", was first used by Gilster [1] in the interpretation of computer literacy, in which this definition is defined as emphasizing critical thinking and evaluating information more than technical and procedural skills.

The digitalization of economy as an integral part of modern society is the object of study in the works [2-9], who in their research determined the current state of digital transformation, the impact of the development of digital technologies on the economic growth and well-being of the country, which makes it possible to find ways to improve the quality of various spheres of life and to determine the priority areas of the economy that are of paramount importance for the enrichment of the state.

The issue of digital literacy has intensified significantly over the last twenty or thirty years, along with the digitalization of most business activities of economic entities, while growing its role in the financial services market (in particular, the sphere of financial technologies [10-13], and in the banking business [14-18], and financial behavior of households in particular [19-26]. Peculiarities of changes in the financial behavior of households in the regional aspect have been studied in the scientific works of such scientists as [27-33], the study of which made it possible to form a holistic view of the financial behavior of households, both at the macroeconomic level (market of financial services), and in the regional aspect in the conditions of the national innovative economy development.

Today, digitalization processes are gaining significant development and are gradually penetrating all sectors of economy and public life. In general, the vast majority of research focuses on the impact of digitalization on the global financial services market [34-40]. The study of the model of functioning of the financial services market in its separate segments: deposit, credit, insurance and investment showed an important role of banking institutions in the economic development of countries [41].

An analysis of the literature shows that a significant number of scholars have devoted their work to the digital economy development in terms of innovative technologies and the transformation of the national economy. The following studies were conducted, in particular [42-56]. These scientific publications are mainly devoted to the study of the degree of the digitalization implementation in countries, in general, and certain regions, in particular, and on this basis, highlights the recommendations for the innovative development of digital economy.

In the conditions of constant globalization processes, active digitalization of the national economic systems, digitalization of the world financial market, there is a need to determine the role of digital technologies in transforming regional models of household financial behavior in the conditions that ensure sustainable economic development and enable effective innovation.

The purpose of this article is to study the features of the impact of digital technologies on the regional models’ transformation of financial behavior of households.

The research used a range of scientific methods and approaches to achieve the following goals and objectives: methods of comparison, measurement, abstraction, comparative analysis to find and organize information about household finances, development of digital technologies in the regions of Ukraine. A range of statistical and econometric methods was also used to assess the impact of the digitization index on the model transformation of financial behavior of households in all regions. The use of the cartographic method made it possible to graphically show the regional features of such influence.

The study consists of three main components: determining the transformation index of the financial behavior model of households (d1) in different regions; calculation of the digitization index in different regions (d2); assessment of the impact of the digitization index on the change of the transformation index of the financial behavior model of households in each of the outlined regions of Ukraine (d2 $\longrightarrow$ d1).

To search for the index d1 and d2 the following steps were identified:

1) formation of a set of indicators for calculations;

2) determination of the outlined indexes for each region;

3) separation of the criteria for grouping regions according to the parameter of each of the indices;

4) analysis of the regional distribution of the indicator of certain indices.

The transformation index the model of financial behavior of households will be determined on the basis of the following indicators: loans per household, million USD; consumer loans per household, USD; the share of consumer credit in the total amount of credit; loans for the purchase, construction and reconstruction of real estate per household, USD; the share of loans for the purchase, construction and reconstruction of real estate in the total amount of the loan; other loans per household, USD; the share of other loans in the total amount of the loan, mortgage loans from the total amount of loans per household, USD; loans to households for the purchase, construction and reconstruction of real estate, up to 1 year, per household, million USD; share of loans up to 1 year; loans from 1 year to 5 years per household, USD.; share of loans from 1 to 5 years; loans for more than 5 years per household, USD; share of loans over 5 years; deposits per household, USD.

The digitization index is calculated using the following parameters: the share of households that have access to Internet services at home, the percentage; share of Internet subscribers to the whole population; the share of the population that reported using the Internet for banking purposes.

Since the above indicators have different units of measurement, for further calculations we standardize them according to the following formula:

$Z_{i j}=\frac{K_{i j}-\bar{K}_j}{S_j}$ (1)

where, $\bar{K}_j=\frac{1}{m} \sum_{i=1}^m K_{i j}$ the average value for the j-th indicator of the studied industry, $S_j=\sqrt{\frac{1}{m} \sum_{i=1}^m\left(K_{i j}-K_j\right)^2}$ standard deviation of the j-th indicator of the industry.

For further calculations we use the following algorithm.

1. Calculation of the reference point.

To determine the reference point of multidimensional space, which is a vector, we apply the following rule: among all the indicators-stimulators choose the maximum, among the indicators-disincentives - the minimum.

$P_o=$ where $z_{o k}=\max z_{i k}$, if $k \in \mathrm{I} 1$,$P_o=$ where $z_{o k}=\min z_{i k}$, if $k \in \mathrm{I} 2$ (2)

2. Implementation of quantitative assessment.

Ranking of regions according to the degree of reduction of each index:

Calculation of the distance between the j-th object and the point (Ро):

$C_{o i}=\left[\sum_{k=1}^n\left(Z_{i k}-Z_{o k}\right)^2\right]^{\frac{1}{2}}$ (3)

Determining the average distance between the j-th object and the point (Ро):

$\bar{C}_{i o}=\frac{1}{m} \sum_{i=1}^m C_{i o}$ (4)

Calculation of standard deviation:

$S_o=\left[\frac{1}{m} \sum_{k=1}^m\left(C_{i o}-C_o^{-}\right)^2\right]^{\frac{1}{2}}$ (5)

Determining the value Со:

$C_o=\bar{C}_{i o}+2 \cdot S_o$ (6)

Calculation of the indicator у1:

$y_1=1-\frac{C_{i o}}{C_o}$ (7)

As a result of using this technique, we will determine the value of the transformation index of the model of financial behavior of households, and the digitalization index.

To specify the impact of the digitization index on changing the transformation model of household financial behavior, we use the algorithm of the classical method of correlation-regression analysis and specify this impact in the form of algebraic equations of the dependence between dependent and independent variables in each region of Ukraine. To do this, we use the model of nonlinear one-factor regression, the equation of which can be schematically written as follows:

$d_1=a_0+a_1^* d_2^3+a_2^* d_2^2+a_3^* d_2+e$ (8)

where, d1 is the transformation index of the financial behavior model; d2 digitization index; a0, a1, a2, a3 model parameters; ɛ statistical error.

To find the outlined effect we will use the calculation equation of the following type:

$\hat{d}_1=\hat{a_0}+\hat{a_1} * d_2^3+\hat{a_2} * d_2^2+\hat{a}_3 * d_2$ (9)

where, $\hat{d_1}-$ calculated value of the transformation index of the financial behavior model; $\hat{a}_0$, $\hat{a_1}$, $\hat{a}_2$, $\hat{a}_3$ – calculated values of model parameters.

Thus, using the statement, that $\varepsilon=d_1-\hat{d}_1 \rightarrow \min$.

Accordingly:

$\sum_{i=1}^n\left(d_1-\left(\hat{a_0}+\hat{a_1} * d_2^3+\hat{a_2} * d_2^2+\hat{a_3}\right)\right)^2 \rightarrow \min$ (10)

Thus, with the help of mathematical calculations, and considering this statement, we will find the parameters $\hat{a}_0$, $\hat{a_1} \hat{a_1}, \hat{a_2}, \hat{a_3}$ and specify algebraic equations of the influence of $d_2$ on $d_1$.

To understand the strength of the influence of d2 on d1, we also analyze the value of the correlation coefficient by the following formula:

$R=\sqrt{1-\frac{\sum\left(d_i-\hat{d}_i\right)^2}{\sum\left(d_i-\bar{d}_i\right)^2}}$ (11)

Therefore, using the presented above method of study, we will conduct a research. As a separate case, we propose to consider the development of the financial services market of Ukraine and determine the impact of modern information and communication innovations on the change of regional models of financial behavior of households.

According to the presented methodology, to assess the impact of digital technologies on the change of this type of behavior, it is necessary to determine two coefficients: d1 – the transformation index of financial behavior of households and d2 – digitization index, i.e. a generalized indicator of digital technologies Let's start to define the outlined indices.

Note that the topic of the article is the direction of scientific interest of the team of authors who have already conducted research in this area. The matter of the method substantiation to calculate the transformation index of financial behavior of households has already been studied, and the results were published in another scientific journal [52]. That is why within the framework of this article, these results will be used in fragments in order to provide an opportunity for further analysis in this direction. In the Table 1, information on the change in the transformation index of financial behavior of households is presented.

According to the results of the calculations, such regions as Kirovohrad (1,033), Sumy (1,029) and Chernihiv (1,049) were included among the leading regions in terms of the level of transformation of the financial behavior of households. These regions are characterized by positive changes during the analyzed period, which explains the highest value of the indicators.

The regions with an above-average level of transformation of financial behavior include: Vinnytsia (1.020), Volyn (1.005), Zhytomyr (1.019), Kyiv (1.001), Luhansk (1.002), Mykolaiv (1.011), Poltava (1.020), Rivne (1.015), Ternopil (1,001), Khmelnytskyi (1,006) and Cherkasy (1,006) regions. The above-mentioned regions are characterized by positive changes in the financial behavior of households, as they have a transformation index slightly higher than the average value for Ukraine.

Zaporizhzhia, Ivano-Frankivsk, Kharkiv, Kherson and Chernivtsi regions are included in the group of regions with a value of the indicator of the level of transformation of the financial behavior of households below the average. These regions are characterized by a slight deterioration of indicators over the analyzed period.

The group of regions with a low level of financial behavior transformation includes Dnipropetrovsk (0.978), Donetsk (0.969), Zakarpattia (0.970), Lviv (0.973) and Odesa regions (0.940). These regions have the lowest indicators in Ukraine and are characterized by a significant decrease in 2020 compared to 2016.

Table 1. Indicators of the index of financial behavior of households in regions of Ukraine in 2016-2020 (d1)

|

Region |

2016 |

2017 |

2018 |

2019 |

2020 |

|

Vinnytsia |

0.249 |

0.238 |

0.239 |

0.242 |

0.254 |

|

Volyn |

0.261 |

0.250 |

0.251 |

0.272 |

0.262 |

|

Dnipropetrovsk |

0.308 |

0.293 |

0.293 |

0.386 |

0.302 |

|

Donetsk |

0.271 |

0.258 |

0.256 |

0.277 |

0.263 |

|

Zhytomyr |

0.249 |

0.236 |

0.239 |

0.239 |

0.254 |

|

Transcarpathian |

0.257 |

0.240 |

0.239 |

0.231 |

0.249 |

|

Zaporizhzhia |

0.285 |

0.273 |

0.272 |

0.326 |

0.280 |

|

Ivano-Frankivsk |

0.259 |

0.247 |

0.246 |

0.254 |

0.258 |

|

Kyiv |

0.998 |

0.951 |

0.953 |

0.997 |

0.999 |

|

Kirovohrad |

0.243 |

0.232 |

0.233 |

0.224 |

0.251 |

|

Luhansk |

0.247 |

0.237 |

0.239 |

0.236 |

0.247 |

|

Lviv |

0.310 |

0.301 |

0.302 |

0.404 |

0.301 |

|

Mykolayiv |

0.260 |

0.246 |

0.249 |

0.265 |

0.263 |

|

Odesa |

0.312 |

0.292 |

0.288 |

0.354 |

0.293 |

|

Poltava |

0.267 |

0.256 |

0.259 |

0.302 |

0.272 |

|

Rivne |

0.254 |

0.244 |

0.244 |

0.250 |

0.258 |

|

Sumy |

0.251 |

0.241 |

0.242 |

0.252 |

0.259 |

|

Ternopil |

0.253 |

0.240 |

0.239 |

0.229 |

0.253 |

|

Kharkiv |

0.280 |

0.266 |

0.268 |

0.319 |

0.278 |

|

Kherson |

0.261 |

0.248 |

0.247 |

0.259 |

0.260 |

|

Khmelnytsky |

0.257 |

0.245 |

0.246 |

0.258 |

0.259 |

|

Cherkasy |

0.258 |

0.245 |

0.245 |

0.253 |

0.259 |

|

Chernivtsi |

0.257 |

0.244 |

0.242 |

0.240 |

0.251 |

|

Chernihiv |

0.245 |

0.236 |

0.238 |

0.238 |

0.257 |

Source: calculated by the authors on the basis of information from the State Statistics Service of Ukraine: http://www.ukrstat.gov.ua/

Using the research methodology, we will also determine the indicator d2 – digitization index. The results of the calculations are presented in Table 2.

Table 2. Dynamics of the digitization index (d2) in Ukraine’s regions, 2016-2020

|

Name of the region |

2016 |

2017 |

2018 |

2019 |

2020 |

|

Vinnytsia |

0.207 |

0.191 |

0.349 |

0.513 |

0.326 |

|

Volyn |

0.229 |

0.264 |

0.141 |

0.211 |

0.337 |

|

Dnipropetrovsk |

0.807 |

1.000 |

0.948 |

0.998 |

0.985 |

|

Donetsk |

0.345 |

0.370 |

0.431 |

0.630 |

0.602 |

|

Zhytomyr |

0.152 |

0.119 |

0.041 |

0.243 |

0.340 |

|

Transcarpathian |

0.555 |

0.017 |

0.436 |

0.328 |

0.396 |

|

Zaporizhzhia |

0.614 |

0.588 |

0.531 |

0.535 |

0.547 |

|

Ivano-Frankivsk |

0.579 |

0.602 |

0.314 |

0.556 |

0.538 |

|

Kyiv |

0.744 |

0.673 |

0.708 |

0.704 |

0.738 |

|

Kirovohrad |

0.250 |

0.325 |

0.150 |

0.207 |

0.143 |

|

Luhansk |

0.375 |

0.376 |

0.377 |

0.448 |

0.399 |

|

Lviv |

0.495 |

0.429 |

0.354 |

0.401 |

0.295 |

|

Mykolayiv |

0.570 |

0.600 |

0.534 |

0.597 |

0.593 |

|

Odesa |

0.451 |

0.334 |

0.457 |

0.541 |

0.709 |

|

Poltava |

0.260 |

0.288 |

0.411 |

0.124 |

0.278 |

|

Rivne |

0.116 |

0.451 |

0.373 |

0.106 |

0.166 |

|

Sumy |

0.386 |

0.573 |

0.643 |

0.547 |

0.475 |

|

Ternopil |

0.516 |

0.538 |

0.302 |

0.320 |

0.369 |

|

Kharkiv |

0.361 |

0.587 |

0.437 |

0.463 |

0.641 |

|

Kherson |

0.621 |

0.232 |

0.335 |

0.246 |

0.479 |

|

Khmelnytsky |

0.006 |

0.374 |

0.068 |

0.097 |

0.071 |

|

Cherkasy |

0.183 |

0.260 |

0.223 |

0.363 |

0.399 |

|

Chernivtsi |

0.519 |

0.615 |

0.529 |

0.420 |

0.480 |

|

Chernihiv |

0.306 |

0.259 |

0.404 |

0.349 |

0.241 |

Source: calculated by the authors on the basis of information from the State Statistics Service of Ukraine: http://www.ukrstat.gov.ua/

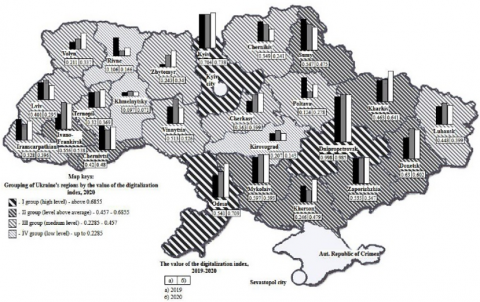

Depending on the value of digitization index of the regions of Ukraine in 2020, we propose to distinguish four groups of such regions, namely:

Group I - regions with a high level of the digital technology development: Dnipropetrovsk (0.985), Kyiv (0.738), Odesa (0.709).

Group II - regions with above average level of the digital technology development: Donetsk (0.602), Zaporizhia (0.547), Ivano-Frankivsk (0.538), Mykolaiv (0.593), Sumy (0.475), Kharkiv (0.641), Kherson (0.479), Chernivtsi (0.480).

Group III - regions with an average level of the digital technology development: Vinnytsia (0.326), Volyn (0.337), Zhytomyr (0.340), Transcarpathian (0.396), Luhansk (0.399), Lviv (0.295), Poltava (0.278), Ternopil (0.369), Cherkasy (0.399), Chernihiv (0.241).

Group IV - regions with a low level of the digital technology development: Kirovohrad (0.143), Rivne (0.166), Khmelnytsky (0.071).

To do this, we’ll use the appropriate method of the distribution of all regions (Table 3).

We present the obtained results of grouping using the cartographic method (Figure 1).

Thus, the group of regions with a high index of digitalization includes the following ones: Dnipropetrovsk, Kyiv, Odesa, among which the highest rate was recorded in Dnipropetrovsk region (0.985). In the outlined regions, the indicators of this index are higher than average. The following regions were included in the group with a digitization index above average: Donetsk, Zaporizhia, Ivano-Frankivsk, Mykolaiv, Sumy, Kharkiv, Kherson, Chernivtsi. This indicator in these regions is more than the average value as a whole, which indicates that such regions are developing rapidly in the digital direction and are gradually moving to the group of leaders in the index of the households’ digitalization.

The third group of regions with an average level of digitalization includes the following regions: Vinnytsia, Volyn, Zhytomyr, Transcarpathian, Luhansk, Lviv, Poltava, Ternopil, Cherkasy, Chernihiv. These regions are characterized by the processes of gradual digital development. The last and fourth groups include Kirovohrad, Rivne and Khmelnytsky regions, where the digitization index remains quite low.

Table 3. Grouping of regions by the digitization index

|

Group |

The value of the digitization index |

Range of values |

Areas |

|

І |

High |

≥0.6855 |

Dnipropetrovsk, Kyiv Odesa |

|

ІІ |

Above average |

≥0.457 <0.6855 |

Donetsk, Zaporizhia, Ivano-Frankivsk, Mykolaiv, Sumy, Kharkiv, Kherson, Chernivtsi |

|

ІІІ |

Average |

≥0.2285 <0.457 |

Vinnytsia, Volyn, Zhytomyr, Transcarpathian, Luhansk, Lviv, Poltava, Ternopil, Cherkasy, Chernihiv |

|

ІV |

Low |

<0.2285 |

Kirovohrad, Rivne, Khmelnytsky |

Source: proposed by the authors

Source: proposed by the authors

Figure 1. Grouping of Ukraine’s regions by the value of the digitization index, 2020

Table 4. The impact of digitalization on the transformation of regional models of financial behavior of households in Ukraine

|

Region |

Model |

R |

|

Vinnytsia |

d1ˆ=55.4075d23-49.7141d22+14.4442d2-1.0971 |

0.99 |

|

Volyn |

d1ˆ=774.1808d23-565.8089d22+130.403d2-9.05 |

0.79 |

|

Dnipropetrovsk |

d1ˆ=841.1808d23-2293.9672d22+2078.4461d2-625.1433 |

0.51 |

|

Donetsk |

d1ˆ=116.2734d23-158.9d22+70.4287d2-9.9063 |

0.97 |

|

Zhytomyr |

d1ˆ=-57.8692d23+30.0743d22-3.8174d2+0.3505 |

0.98 |

|

Transcarpathian |

d1ˆ=-42.9072d23+42.5397d22-10.6747d2+0.409 |

0.95 |

|

Zaporizhzhia |

d1ˆ=339.8378d23-568.2741d22+315.4677d2-57.8378 |

0.44 |

|

Ivano-Frankivsk |

d1ˆ=-289.6698d23+416.676d22-193.4485d2+28.8741 |

0.64 |

|

Kyiv |

d1ˆ=976.4336d23-1933.0914d22+1269.5435d2-275.5461 |

0.70 |

|

Kirovohrad |

d1ˆ=1278.1848d23-925.1717d22+212.7668d2-15.0762 |

0.94 |

|

Luhansk |

d1ˆ=-1879.8241d23+2353.9684d22-977.007d2+134.7273 |

0.99 |

|

Lviv |

d1ˆ=26.7821d23-26.6515d22+8.2948d2-0.5095 |

0.55 |

|

Mykolayiv |

d1ˆ=-5886.3913d23+10076.1521d22-5741.2269d2+1089.1296 |

0.43 |

|

Odesa |

d1ˆ=-5.1911d23+7.516d22-3.419d2+0.7891 |

0.74 |

|

Poltava |

d1ˆ=7.9526d23-5.6978d22+1.0206d2+0.2499 |

0.96 |

|

Rivne |

d1ˆ=3.7139d23-3.4106d22+0.9163d2+0.1839 |

0.92 |

|

Sumy |

d1ˆ=-42.2388d23+60.4781d22-28.0494d2+4.492 |

0.55 |

|

Ternopil |

d1ˆ=31.9263d23-39.6174d22+15.8373d2-1.7734 |

0.46 |

|

Kharkiv |

d1ˆ=15.8484d23-25.7538d22+13.5561d2-2.0094 |

0.54 |

|

Kherson |

d1ˆ=-0.1562d23+2.3587d22-2.2869d2+0.8127 |

0.48 |

|

Khmelnytsky |

d1ˆ=222.6926d23-99.9633d22+6.2968d2+0.2226 |

0.99 |

|

Cherkasy |

d1ˆ=-229.5534d23+192.6122d22-51.1188d2+4.5791 |

0.95 |

|

Chernivtsi |

d1ˆ=68.0287d23-109.949d22+58.8441d2-10.1838 |

0.99 |

|

Chernihiv |

d1ˆ=-1487.1249d23+1407.2667d22-434.1843d2+44.0284 |

0.94 |

Source: calculated by the authors

According to the methodology, we will now search for the analytical relationship between d1 and d2, i.e. define algebraic equations that will characterize the impact of the digitization index on the change in the transformation index of the household financial behavior. For this, as noted, the methodology of correlation-regression analysis was used. The search results are presented in Table 4.

The study of the digitalization impact on the model transformation of financial behavior of households during 2016-2020 gives grounds to note the growth of such impact, strengthening the role of digital technologies in the development of financial services and changing household demand for these services. Covid-19 can be identified as one of the biggest drivers of such active digitalization of the financial sphere. The pandemic was a catalyst, firstly for financial institutions, in particular, banking institutions, which had to accelerate the creation of new services and products to maintain their market position and adapt to new environmental challenges, and secondly, for consumers of these services, including households. The results of 2020 showed that behavior of these economic entities has changed significantly, and if previously a significant proportion of them did not use online services and did not plan to do so in the future, the pandemic forced them to turn to online banking and other digital technologies, and financial institutions.

Regional analysis of the impact of the digitization index and the model transformation of financial behavior of households in some regions of Ukraine shows the ambiguous impact of digital technologies on the financial services development in the regions, which is directly related to the pace of such technologies in these regional features of financial behavior of households in them, their propensity to use these technologies, the level of financial inclusion, financial literacy, etc. This conclusion confirms, first of all, the value of the correlation coefficient, which shows that in some regions the relationship between the digitization index and the transformation index of the model of financial behavior of households is insignificant.

Within the article, the role of digital technologies in the transformation of regional models of financial behavior of households is analyzed. The study found that within the national economy an important role is played by innovation processes, which are largely due to the digitalization processes of financial relations in all developed countries. The results of the study showed that such processes affect the model of financial behavior of households, which in innovative economies takes on a different meaning and form. Accordingly, in the article, by understanding the regional differences in the models of financial behavior of households, it is relevant to specify such a transformation, proposed a method for determining the impact of the digitization index and a model of financial behavior of households. To test this methodology, information on the financial services development and the state of the digital technologies use in different regions of Ukraine was used. The analysis showed that this impact is ambiguous among all regions, but there are trends to refer to the role of digital technologies in the financial services transformation. It is also established that digitalization processes are inevitable in the current conditions of innovation economy in many countries, the acceleration of their development is due to the Covid-19 pandemic, and the impact on the model of household financial behavior is objective and will increase in the future as a result of the invention and use of new digital technologies.

We also note that the conducted scientific research was based exclusively on statistical information provided by the State Statistics Service of Ukraine and the National Bank of Ukraine. The digitization index was calculated based on those indicators that are available and characterize the development of the digital society in Ukraine. the list of such indicators is limited and, taking into account the active development of the digital economy, already needs to be expanded.

The article also uses statistical data on the interaction of these economic entities with banking institutions to describe the models of financial behavior of households, since the market of non-banking financial services in the country is not developed and does not exert a significant influence on the main trends of the functioning of the entire sphere of financial services.

Further scientific research in this direction may be related to the search and justification of differentiated directions of development of the digital society in regions with different rates of digitalization. Also interesting may be studies that relate to a more detailed consideration of models of financial behavior of households in the regions for different categories of such subjects, taking into account the number of persons in households, the level of their incomes, expenses, territory of residence, etc.

This research is carried out within the framework of the scientific project “Transformation of the households’ behavior in the financial services market in the context of digitalization” with the support of the Ministry of Education and Science of Ukraine.

[1] Gilster, P. (1997). Digital literacy. New York: Wiley Computer Publications.

[2] Irtyshcheva, I., Stehnei, M., Popadynets, N., Bogatyrev, K., Boiko, Y., Kramarenko, I., Senkevich, O., Hryshyna, N., Kozak, I., Ishchenko, O. (2021). The effect of the digital technology development on economic growth. International Journal of Data and Network Science, 5(1): 25-36. https://doi.org/10.5267/j.ijdns.2020.11.006

[3] Martin, A. (2008). Digital Literacy and the “Digital Society”. In C. Lankshear, M. Knobel (Eds.), Digital Literacies: Concepts, Policies, and Practices. New York: Peter Lang: 151-176.

[4] Matt, C., Hess, T., Benlian, A. (2015). Digital transformation strategies. Business & Information Systems Engineering, 57(5): 339-343. https://doi.org/10.1007/s12599-015-0401-5

[5] Reis, J., Amorim, M., Melão, N., Matos, P. (2018). Digital transformation: A literature review and guidelines for future research. In: Rocha, Á., Adeli, H., Reis, L.P., Costanzo, S. (eds) Trends and Advances in Information Systems and Technologies. WorldCIST'18 2018. Advances in Intelligent Systems and Computing, vol. 745. Springer, Cham. https://doi.org/10.1007/978-3-319-77703-0_41

[6] Sebastian, I.M., Ross, J.W., Beath, C.M., Mocker, M., Moloney, K., Fonstad, N.O. (2017). How big old companies navigate digital transformation. MIS Quarterly Executive 16(3): 197-213.

[7] Shaposhnykov, K., Kochubei, O., Grygor, O., Protsenko, N., Vyshnevska, O., Dzyubina, A. (2021). Organizational and economic mechanism of development and promotion of IT products in Ukraine. Estudios de Economía Aplicada, 39(6). https://doi.org/10.25115/eea.v39i6.5264

[8] Tulchynska, S., Popelo, O., Vovk, O., Dergaliuk, B., Kreidych, I., Tkachenko, T. (2021). The resource supply of innovation and investment strategies of the microeconomic systems modernization in the conditions of digitalization. WSEAS Transactions on Environment and Development, 17: 819-828. https://doi.org/10.37394/232015.2021.17.77

[9] Zybareva, O., Kravchuk, I., Pushak, Y., Verbivska, L., Makeieva, O. (2021). Economic and legal aspects of the network readiness of the enterprises in Ukraine in the context of business improving. Estudios de Economía Aplicada, 39(5). https://doi.org/10.25115/eea.v39i5.4972

[10] Azarenkova, G., Shkodina, I., Samorodov, B., Babenko M., Onishchenko I. (2018). The influence of financial technologies on the global financial system stability. Investment Management and Financial Innovations, 15(4): 229-238. https://doi.org/10.21511/imfi.15(4).2018.19

[11] Ivashchenko, A., Britchenko, I., Dyba, M., Ye, P., Yu., S., Yu, V. (2018). Fintech platforms in SME’s financing: EU experience and ways of their application in Ukraine. Investment Management and Financial Innovations, 15(3): 83-96. https://doi.org/10.21511/imfi.15(3).2018.07

[12] Shkolnyk, I., Kozmenko, S., Kozmenko, O., Orlov, V., Shukairi, F. (2021). Modeling stability of the financial system on the example of Ukraine. Equilibrium. Quarterly Journal of Economics and Economic Policy, 16(2): 377-411. https://doi.org/10.24136/eq.2021.014

[13] Zveryakov, M., Kovalenko, V., Sheludko, S., Sharah, E. (2019). FinTech sector and banking business: competition or symbiosis? Economic Annals-XXI, 175(1-2): 53-57. https://doi.org/10.21003/ea.V175-09

[14] Chmutova, I., Vovk, V., Bezrodna, O. (2017). Analytical tools to implement integrated bank financial management technologies. Economic Annals-XXI, 163(1): 95-99. http://dx.doi.org/10.21003/ea.V163-20

[15] Marhasova, V., Kovalenko, Yu., Bereslavska, O., Muravskyi, O., Fedyshyn, M., Kolesnik, O. (2021). Instruments of monetary-and-credit policy in terms of economic instability. International Journal of Management, 11(5): 43-53.

[16] Mints, O., Marhasova, V., Hlukha, H., Kurok, R., Kolodizieva, T. (2019). Analysis of the stability factors of Ukrainian banks during the 2014–2017 systemic crisis using the Kohonen self-organizing neural networks. Banks and Bank Systems, 14(3): 86-98. https://doi.org/10.21511/bbs.14(3).2019.08

[17] Onikiienko, S., Polishchuk, Ye., Ivashchenko, A., Kornyliuk, A., Demchyshak, N. (2021). Prior credit assessment of long-term SME projects with non-standard cash flows. Banks and Bank Systems, 16(2): 148-158. https://doi.org/10.21511/bbs.16(2).2021.14

[18] Tkachuk, I. (2017). Asset operations of Ukrainian banks on the current stage of the banking system development. Banks and Bank Systems, 12(1-1): 119-127. https://doi.org/10.21511/bbs.12(1-1).2017.04

[19] Białowolski, P (2019). Economic sentiment as a driver for the household financial behavior. Journal of Behavioral and Experimental Economics, 80: 59-66. https://doi.org/10.1016/j.socec.2019.03.006

[20] Chetty, R. (2015). Behavioral economics and public policy: A pragmatic perspective. The American Economic Review, 105: 1-33.

[21] Dubyna, M., Popelo, O., Kholiavko, N., Zhavoronok, A., Fedyshyn, M., Yakushko, I. (2022). Mapping the literature on financial behavior: a bibliometric analysis using the VOSviewer program. WSEAS Transactions on Business and Economics, 19: 231-246. https://doi.org/10.37394/23207.2022.19.22

[22] Grable, J., Joo, S.H., Kruger, M. (2020). Risk tolerance and household financial behavior: A test of the reflection effect. IIMB Management Review, 32(4): 402-412. https://doi.org/10.1016/j.iimb.2021.02.001

[23] Jolls, C., Sunstein, C.R., Thaler, R.H. (1998). A behavioral approach to law and economics. 50 Stanford Law Rev. 1471 (1998), Available at SSRN: https://ssrn.com/abstract=2292029.

[24] Henrich, J. (2000). Does culture matter in economic behavior? Ultimatum game bargaining among the Machiguenga of the Peruvian Amazon. American Economic Review, 90(4): 973-979. https://doi.org/10.1257/aer.90.4.973

[25] Shkvarchuk, L., Slav’yuk, R. (2019). Financial behavior of households in Ukraine. Journal of Competitiveness, 11(2): 144-159. https://doi.org/10.7441/joc.2019.03.09

[26] Waliszewski, K., Warchlewska, A. (2021). Comparative analysis of Poland and selected countries in terms of the household financial behavior during the COVID-19 pandemic. Equilibrium. Quarterly Journal of Economics and Economic Policy, 16(3): 577-615. https://doi.org/10.24136/eq.2021.021

[27] Bernasek, A., Bajtelsmit, V.L. (2002). Predictors of the women’s involvement in household financial decision-making. Financial Counseling and Planning, 13(2): 39-48.

[28] Agarwal, S., Amromin, G., Ben-David, I., Chomsisengphet, S., Evanoff, D.D. (2011). Financial Counseling, Financial Literacy, and Household Decision Making. Financial Literacy: Implications for Retirement Security and the Financial Marketplace.UK: Oxford University Press.

[29] Dinga, E., Pop, N., Dimitriu, M., Milea, C. (2011). Modeling the financial behavior of population (1) –conceptual assignations. Romanian Journal of Economic Forecasting, 14(3): 239-254.

[30] Fatykhov, A.І. (2011). Financial behavior of social groups of the population of a large city in modern Russian society. Extended abstract of PhD dissertation.

[31] Doya, K. (2008). Modulators of decision-making. Nat. Neurosci, 11(4): 410-416. https://doi.org/10.1038/nn2077

[32] Fonseca, R., Mullen, K.J., Zamarro, G., Zissimopoulos, J. (2012). What explains the gender gap in financial literacy? The Role of Household Decision. The Journal of Consumer Affairs, 46(1): 90-106. https://doi.org/10.1111/j.1745-6606.2011.01221.x

[33] Sarwar, A., Afaf, G. (2014). Comparison between psychological and economic factors affecting the decision-making behavior of individual investors. American Journal of Business and Management, 3(2): 77-94.

[34] Dubyna, M., Zhavoronok, A., Kudlaieva, N., Lopashchuk, I. (2021). Transformation of the household credit behavior in the conditions of digitalization of the financial services market. Journal of Optimization in Industrial Engineering, 14: 195-201. https://doi.org/10.22094/joie.2020.677835

[35] Gupta, S., Kanungo, R. (2022). Financial inclusion through digitalization: Economic viability for the bottom of the pyramid (BOP) segment. Journal of Business Research, 148: 262-276. https://doi.org/10.1016/j.jbusres.2022.04.070

[36] Kozmenko, O., Shkolnyk, I. (2008). The peculiarities of the financial market development in Ukraine. Investment Management and Financial Innovations, 5(1): 104-112. http://dx.doi.org/10.21511/imfi.5(1).2008.01

[37] Vasile, V., Panait, M., Apostu, S.A. (2021). Financial inclusion paradigm shift in the post pandemic period. Digital-divide and gender gap. International Journal of Environmental Research and Public Health, 18(20): 10938. https://doi.org/10.3390/ijerph182010938

[38] Vovk, V., Denysova, A., Rudoi, K., Kyrychenko, T. (2021). Management and legal aspects of the symbiosis of banking institutions and fintech companies in the credit services market in the context of digitization. Estudios de Economía Aplicada, 39(7). https://doi.org/10.25115/eea.v39i7.5013

[39] Shkolnyk, I.O. (2008). Peculiarities of the financial markets’ functioning in developing countries in the context of financial globalization. Actual Problems of Economics, 6: 63-66.

[40] Tsindeliani, I.A., Proshunin, M.M., Sadovskaya, T.D., Popkova, Z.G., Davydova, M.A., Babayan, O.A. (2022). Digital transformation of the banking system in the context of sustainable development. Journal of Money Laundering Control, 25(1): 165-180. https://doi.org/10.1108/JMLC-02-2021-0011

[41] Shkarlet, S., Dubyna, M., Vovk, V., Noga M. (2019). Financial service markets of Eastern Europe: A compositional model. Economic Annals-XXI. 176(3-4): 26-37. https://doi.org/10.21003/ea.V176-03

[42] Barro, R. (1991). Economic growth in a cross section of countries. The Quarterly Journal of Economics, 106(2): 407-443, https://doi.org/10.2307/2937943

[43] Filyppova, S., Kovtunenko, Y., Filippov, V., Voloshchuk, L., Malin, O. (2021). Sustainable development entrepreneurship formation: System-integrated management tools. E3S Web of Conferences, 255: 01049. https://doi.org/10.1051/e3sconf/202125501049

[44] Filyppova, S., Okulich-Kazarin, V., Kibik, O., Shamborovskyi, G., Cherkasova, S. (2019). Influence of the market of business intellectual services on the innovation safety of EU countries. Journal of Security and Sustainability, 9(1): 347-360. https://doi.org/10.9770/jssi.2019.9.1(26)

[45] Gross, T., Rebelo, S. (1990). Public policy and economic growth: Developing neoclassical implications. Journal of Political Economy, 98(5): 126-150. https://doi.org/10.1086/261727

[46] Yu, H., Mohylevska, O., Romanova, L., Feschenko, O. (2019). Innovative concept of the national economy development. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, 2: 137-145. https://doi.org/10.29202/nvngu/2019-2/20

[47] Ivanchenkova, L., Skliar, L., Pavelko, O., Yu, C., Kuzmenko, H., Zinkevych, A. (2019). Improving accounting and analysis of innovative costs. International Journal of Innovative Technology and Exploring Engineering, 9(1): 4003-4009.

[48] Kholiavko, N., Popova, L., Marych, M., Hanzhurenko, I., Koliadenko, S., Nitsenko. V. (2020). Comprehensive methodological approach to estimating the research component influence on the information economy development. Naukovyi Visnyk Natsionalnoho Hirnychoho Universytetu, 4: 192-199. https://doi.org/10.33271/nvngu/20204/192

[49] Bengt-Åke, L., Björn, J., Sloth, A.E., Bent, D. (2002). National systems of building production, innovation and competence. Research Policy, 31(2): 213-231. https://doi.org/10.1016/S0048-7333(01)00137-8

[50] Mudrak, R., Lagodiienko, V., Lagodiienko, N. (2018). Impact of aggregate expenditures on the volume of the national production. Economic Annals-XXI, 172(7-8): 44-50. https://doi.org/10.21003/ea.V172-08.

[51] Paryzkyy, I. (2018). State policy of the innovative development of the national economy: Situation and issues of implementation. Journal of Advanced Research in Law and Economics, 9(8): 2721-2732. https://doi.org/10.14505//jarle.v9.8(38).21

[52] Popelo, O., Dubyna, M., Kholiavko, N., Panchenko, O., Tarasenko, A. (2022). Features of the transformation of the regional models of the households’ financial behavior. Management Theory and Studies for Rural Business and Infrastructure Development, 44(1): 117-124. https://doi.org/10.15544/mts.2022.12

[53] Prokopenko, O., Eremenko, Y., Omelyanenko, V. (2014). Role of the international factor in the innovation ecosystem formation. Economic Annals-XXI, Corpus ID: 56150036.

[54] Sharif, N. (2006). Emergence and development of the national innovation systems concept. Research Policy, 35(5): 745-766. https://doi.org/10.1016/j.respol.2006.04.001

[55] Shtuler, I., Cherlenyak, I., Domyshche-Medyanik, A., Voitovych, S. (2017). Conditions of the formation and stimulation of the activators of the innovative development of Ukraine. Problems and Perspectives in Management, 15(4): 150-160. https://doi.org/10.21511/ppm.15(4).2017.13

[56] Melnyk, V., Zhytar, M., Shchur, R., Kriuchkova, N., Solodzhuk, T. (2021). Assessment of the performance of the financial architecture of Ukrainian economy: budgetary, stock and social aspects. WSEAS Transactions on Business and Economics, 18: 386-395. https://doi.org/10.37394/23207.2021.18.39