Artur Zhavoronok* | Roman Shchur | Yuliia Zhezherun | Iryna Sadchykova | Nadiia Viadrova | Lesia Tychkovska

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

In the article, the role of the credit services market in ensuring stability of the banking system is examined. The study was carried out on the basis of a detailed comparative analysis of the development of the banking system and the credit services market of Ukraine. This approach made it possible to identify the main prerequisites for the development of such a market, and possible options for the formation of crisis phenomena in its functioning. Within the article, it is also described in detail how the credit services market can have a destructive effect on stability of the country's banking system and its financial system. For this, considerable attention is paid to the description of the economic and political environment in which commercial banks have operated in Ukraine during the last twenty years. This made it possible to specify the causes of crisis situations in the country's banking system, justify the actions of state authorities in countering the consequences of such crises. The analysis of the financial stress index as an indicator of stability of the financial system functioning made it possible to establish the cyclic nature of its changes, which proved permanent emergence of crisis situations in the development of both the credit services market and the banking system of Ukraine.

credit services market, national economy, banking system, banking institutions, stability of the banking system

The credit services market is an integral part of the development of the financial system of any country. It has already been unequivocally proven that the development of lending contributes to economic development, and therefore in most cases, governments, pursuing a policy of stimulating economic development, pay special attention to the activation of the functioning of the credit services market. For this, executive authorities have all the tools and levers.

The development of credit relations plays an important role in the development of the entire financial services industry and in the work of a significant number of financial institutions. Commercial banks are one of the largest lenders that today most actively issue loans to economic entities. For these institutions, lending is one of the biggest sources of own income and profit. This role of credit services in the activity of banking institutions contributed to the significant complication of providing such services, the formation of new institutions in the financial services market, the functioning of which is aimed exclusively at ensuring the efficiency of lending, minimizing risks in this area for commercial banks.

The credit services market is a complex system of relationships between all economic entities, which is actively developing in any circumstances. It is the objectivity of credit relations, which is an integral component of economic relations in modern society, that forms the multivariate role of lending in the national economy and, in particular, the banking system. Long-term historical experience shows that crisis phenomena in the functioning of both the global financial system and the financial systems of various countries may well occur in the credit services market and have an extremely destructive effect on the functioning of all economic systems without exception. Fluctuations in the credit services market can significantly destabilize the development of the banking system, individual banking institutions, negatively affect the stability of the functioning of the specified system. It is this situation that determines the importance of conducting new scientific research in this direction. Studying the specifics of the impact of the credit services market on the functioning and development of the banking system is extremely important from the standpoint of the state policy formation to ensure an acceptable level of stability of such a system, its ability to counter unpredictable external and internal threats. In our opinion, the outlined issues are relevant and require theoretical and methodical justification.

The market of credit services plays a special role in ensuring the stability of the banking system in those countries in which the development of the stock market is insufficient and credit transactions are actually the only source of income for banking institutions. This situation only increases the role of credit services in the development of banking institutions and the stability of their dependence on the efficiency of such a market. Accordingly, conducting research on the development of the credit services market in such countries is an important element of ensuring the stability of the functioning of their banking institutions.

Ukraine, as a country that is gradually developing its own financial system, introducing the necessary institutions for its effective functioning, in its development is permanently faced with crisis phenomena in the development of the credit services market, which over time had a multiplying negative effect on economic development and led to complex macroeconomic problems. In Ukraine, the credit services market is the most developed segment of the financial services market. The securities market does not function dynamically enough and, accordingly, the role of credit operations in the activities of banking institutions is quite high. In fact, the credit sphere is the only sphere in which banking institutions can obtain the necessary volumes of profit to ensure stable operations. That is why, for the description and research of the role of the credit services market in ensuring stability of the banking system, the use of a historical retrospective of the functioning of such a market in Ukraine is a good opportunity to conduct a thorough analysis in this direction.

The purpose of this article is to deepen theoretical and methodological provisions regarding the influence of the credit services market on ensuring stability of the banking system.

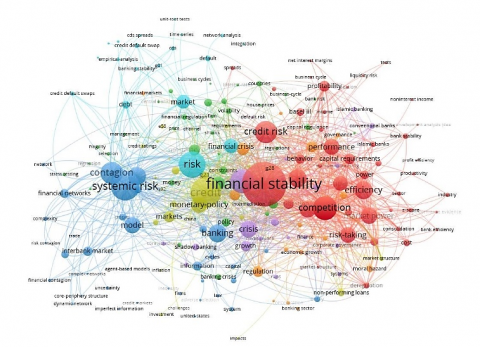

Many scientific works are devoted to the issue of innovation, investment and sustainable development of macroeconomic systems, ensuring the stability of the banking system, including the role of the credit services market in these processes. According to the results of the analysis of the available publications of the Scopus database, 409 articles were published under the keywords "credit market, banking system, stability" (Figure 1).

The first article was published with the specified keywords in 1996. Analyzing the dynamics of publication activity in this area of research, an increase in the number of articles over the last ten years is observed, namely: 2022 – 40 articles, 2021 – 33 articles, 2020 – 51 articles, 2019 – 48 articles, 2018 – 34 articles, 2017 – 42 articles, 2016 – 42 articles, 2015 – 29 articles, 2014 – 19 articles. Analyzing the publishing activity, it should be noted that the majority of articles were published in the following fields of knowledge: Economics (229 articles), Business Finance (202 articles), Business Finance (27 articles), Management (21 articles), International Relations (14 articles), Law (12 articles), etc. Among the countries where research was focused on the credit market development in the context of ensuring the stability of the banking system were: USA, England, Ukraine, China, Germany, Italy, France, Spain and others.

Figure 1. Graphic map of keywords in publications, in which titles the words “credit market, banking system, stability” is met

Source: Compiled by the author based on the analysis of the Scopus database and using the tools of the VOSviewer program

The authors Denysova et al. [1] analyzed the peculiarities of the banks' lending activities and substantiated the prerequisites for strengthening their cooperation with financial companies. In the article, internal and external innovations used in the process of the banking business digitalization are systematized. According to the results of the study, the importance of the introduction of banking innovations in the lending market as the most profitable direction of banking activity is substantiated.

The market of credit services, both historically and by its importance and weight, is the main component of the financial market. It provides the fastest access to resources. The advantages of the credit services market derive from the functional potential of the main subjects of this market - commercial banks, which not only mediate the movement of financial resources, but also to some extent produce them (Dubyna et al.) [2].

The scientists Revindo et al. [3] analyzed the rural financial system, the rural credit market and the development of micro-credit in China. As a result of the research, the authors concluded that micro-credit can significantly reduce the gap in the rural credit market and play an important role in the fight against poverty in rural areas. According to the authors, this is possible provided that some reforms are implemented both at the regional and national level of policy making.

The position of the authors Danylyshyn et al. [4] regarding increasing the financial stability of the banking system refers to improving the efficiency of banks in order to minimize the level of non-performing loans.

The financial crisis of 2014-2016 significantly affected the banking system of Ukraine. This is especially evident in liquidity indicators, as banks, aware of the unstable political and economic situation in the country, prefer liquid assets to long-term investments Boiarynova et al. [5].

A large share of problem loans is a big burden for the banking sector. The main reason for this situation is the credit expansion of the previous years before the 2014-2016 crisis, when the standards for assessing borrowers' solvency were very low. Also, this crisis affected the level of regulatory capital adequacy of the banking sector, but banks have been gradually increasing it since 2017 Zhavoronok et al. [6].

The article of scientists, namely Volosovich et al. [7] is devoted to the classification of self-regulation of the credit services market to natural persons and the definition of its features. Within the scope of the article, the authors proposed to classify self-regulation of the credit services market by models, market sectors, territory and participants. As a conclusion, scientists claim that self-regulation is an important function of the credit services market and contributes to strengthening resistance to external threats and protecting the interests of both service providers and consumers.

Dubyna et al. [8] and Vovk et al. [9] believe that granting loans and conducting credit policy is the most common operation of banking institutions. Credit transactions bring the main profit to banks. However, an analysis of the situation in the banking sector shows that many banks are experiencing financial difficulties due to extremely risky credit policies.

Marhasova et al. [10] and Popelo et al. [11] believe that it is the market of credit services that ensures the mobilization of the amount of capital sufficient for the active development of business entities in order to stimulate economic growth, provide financial support for the investment-innovation process in the state's economic system, and ensure the well-being of its citizens.

The article by Kusi et al. [12] examines the impact of foreign bank assets on banking stability in economies with strong and weak corporate governance at the country level. According to the results of the analysis, it was established that the presence of foreign banks and assets contribute to banking stability. The authors believe that policymakers must build strong corporate governance and robust regulatory regimes to improve how foreign bank operations contribute to banking stability.

The results of the research made by Amadi et al. [13] show that bank stability will increase the funding of the SDGs, and banks will be stable if they finance the SDGs. The authors prove the importance of the banks' active use of opportunities to create sustainable enterprises and develop strategies. They are confident that this will make their core banking business more venture-oriented rather than consumer-oriented.

The study of Khattak et al. [14] analyzed the impact of competition and portfolio diversification on banking stability of conventional and Islamic banks in Indonesia. The paper investigates that the Islamic banking sector is less stable compared to the conventional banking sector. The authors argue that competition in the banking sector reduces stability, and diversification increases it.

The authors of the scientific paper Amadi et al. [15] analyzed the stabilizing effect of fiscal policy on the banking system stability in Nigeria. As a result of the research, it was found that among the fiscal policy variables, taxation and public debt have a more positive impact on the banking system. Scientists also note that state funding and debt growth negatively affect stability of the banking system.

Hryhorkiv et al. [16] and Shkarlet et al. [17] prove that credit services bring big profits to the bank. With the help of the credit mechanism, self-regulation of the economic system is achieved, the rate of profit is equalized in various sectors of the national economy, etc. Credit contributes to the concentration and centralization of capital.

Ostrovska et al. [18] and Tkachuk [19] believe that an extremely important role of credit is to ensure scientific and technical progress and maintenance of the innovation process. Credit is an important source of capital investment financing. Credit relations caused the appearance of a credit mechanism, which includes the principle of lending, credit planning and credit management, terms and methods of lending, methods of its quantitative regulation.

The scientists Pan and Fan [20] investigated the current realities regarding stability of the banking system, took into account shadow banking, inter-bank lending and complex relationships between banks, and proposed a dynamic complex model of the inter-bank network with shadow banking under various network structures. As a result of research, it was concluded that the spread of systemic risks between banks is closely related to the structures of the inter-bank network.

The study of Pan and Fan [21] developed a model of the dynamic complex inter-bank network with shadow banking activity in conditions of macroeconomic fluctuations. Scientists have analyzed the impact of macroeconomic fluctuations on stability of the banking system with shadow banking activities.

The authors Blahun et al. [22] prove that the functioning of the country's banking system is the basis for ensuring its economic development and stability. According to scientists, the state of the banking system is often the cause of financial crises; therefore, ensuring its stable operation is one of the main tasks of monetary policy. The study analyzed and identified five factors that have the greatest impact on ensuring stability of the banking system.

Within the scope of the article by Subbar and Guirinsky [23] and Shkolnyk et al. [24], the authors have developed the ways to improve financial stability of the Iraqi banking system. Scientists have developed recommendations for financial stability of the banking gadget in Iraq. According to the authors, the proposed measures will be useful for practice and will contribute to the banking system stability.

The authors Gao and Fan [25], Kozmenko et al. [26], Marhasova et al. [27, 28] analyzed stability of the banking network system in the conditions of dynamic shocks of macroeconomic fluctuations. Scientists have investigated that there is an optimal ratio of investments to deposits under different scenarios of macroeconomic fluctuations, which divides the banking system into stable and unstable regions.

According to the authors Ramachann et al. [29], Rahman [30] in today's modernized banking services, customers compete for comparative time-saving options, and banking service providers compete for maximum profit. Scientists believe that in this win-win system, many factors are unpredictable, which undermine the vision of a cashless society.

Despite a considerable number of studies, the issue of the role of credit services in ensuring stability of the banking system requires further study and analysis.

A wide range of theoretical and statistical methods will be used in the article to implement scientific research. In particular, to describe the impact of the credit services market on the banking system stability, methods of comparison, abstraction, analysis, logical generalization, and a systemic approach will be applied.

The analytical part of the research will be based on the use of classical statistical and econometric methods. In particular, the analysis of modern trends in the development of the banking system in Ukraine will be carried out on the basis of open analytical information and using a set of statistical criteria. The study of the specifics of the influence of such a market on the outlined type of system will be carried out through the use of econometric methods, which will allow formalizing such influence and determining algebraic equations of the dependence between various indicators that characterize both the development of the credit services market and the state of the banking system of Ukraine. In the article, methodological provisions of the regression analysis will be applied, namely the construction of cubic one-factor regression models of the influence of some indicators on changes in other parameters, namely, the influence of lending volumes on the assets of banking institutions, the influence of loan volumes on the capital of banking institutions.

The cubic one-factor regression model can be presented in a generalized form as follows:

$\mathrm{y}=\alpha_0+\alpha_1 x^3+\alpha_2 x^2+\alpha_3 x+\varepsilon$, (1)

where, у – the value of the dependent variable;

х – the value of the independent variable;

a0, a1, a2, a3, – parameters of the model;

ɛ – an error.

The calculation model of the influence of the independent variable on the change of the dependent parameter can be presented in the following form:

$y=\widehat{\alpha}_0+\hat{\alpha}_1 x^3+\hat{\alpha}_2 x^2+\hat{\alpha}_3 x+\varepsilon$. (2)

By its content, the calculation model should maximally reproduce the dependencies between economic processes that occur in reality. That is why the indicator of the dependent variable and the calculated indicator of the dependent variable should be maximally identical. Mathematically, this can be written as:

$\varepsilon=y-\hat{y}$. (3)

Therefore, at the minimum value of ɛ, the value will be as close as possible to the value y.

$\varepsilon=y-\left(a_0+\hat{a}_1 * x^3+\hat{a}_2 * x^2+\hat{a}_3 * x\right.$ (4)

That is, the condition becomes important ε→min. Expression (3) can be written as follows:

$\left(y-\left(a_0+\hat{a}_1 * x^3+\hat{a}_2 * x^2+\hat{a}_3 * x\right)\right) \rightarrow \min$ (5)

Considering that an array of statistical data is used in the calculation of regression models and the number of observations is large, we can write expression (5) in the following form:

$\sum_{i=1}^n\left(y-\left(a_0+\hat{a}_1 * x^3+\hat{a}_2 * x^2+\hat{a}_3 * x\right)\right)^2 \rightarrow$ $\min$. (6)

Using mathematical transformations, we get that to determine the parameters of the cubic one-factor regression model, it is necessary to solve the following system of equations:

$\left\{\begin{array}{l}a_3 \sum x_i^3+a_2 \sum x_i^2+a_1 \sum x_i+n a_0=\sum y_i \\ a_3 \sum x_i^4+a_2 \sum x_i^3+a_1 \sum x_i^2+a_0 \sum x_i=\sum x_i y_i \\ a_3 \sum x_i^5+a_2 \sum x_i^4+a_1 \sum x_i^3+a_0 \sum x_i^2=\sum x_i^2 y_i \\ a_3 \sum x_i^6+a_2 \sum x_i^5+a_1 \sum x_i^4+a_0 \sum x_i^3=\sum x_i^3 y_i\end{array}\right.$ (7)

After solving this equation, we can find the parameters a0, a1, a2, a3in the cubic one-factor regression model. In the models that will be considered in this article, Vl – the total volume of loans granted by banking institutions to all economic entities is selected as an independent variable; dependent variables - Ab – total assets of banking institutions in Ukraine; Cb – the total capital of all banking institutions in Ukraine.

The use of cubic one-factor regression models will allow deepening theoretical and applied aspects of the functioning of both the credit services market and its impact on ensuring stable development of the banking system of Ukraine within the scope of the study. Statistical arrays of information made publicly available by the National Bank of Ukraine (NBU) will be used to implement the relevant calculations [31].

Figure 2. The impact of the credit services market on stability of the banking system

Source: Generated by authors based on https://bank.gov.ua [31]

We will begin the study with an analysis of certain theoretical provisions of the functioning of the credit services market and its role in ensuring stability of the banking system.

Historically, in Ukraine, among all financial institutions in the credit services market, banking institutions occupy the leading positions. At the same time, there are a number of non-bank financial intermediaries, including credit unions, financial companies, and pawnshops. However, each of the outlined types has its own, specific features of the functioning; and they have occupied separate niches in the outlined market, in which banking institutions are not interested in working for various reasons (complexity of legislation, increased risks, insufficient level of profitability, etc.).

It should be specified that the development of non-bank credit institutions in Ukraine is quite low. Despite the growth in the number of such institutions and the total volume of their assets, their role in the development of the credit services market remains insignificant. At the same time, after the change in the institutional model of regulating the activity of these institutions, their number begins to decrease due to increased requirements for their credit activities. Thus, today we are observing the process of an even greater decline in the role of non-banking institutions in the development of the Ukrainian credit services market. Accordingly, their role in ensuring the stability of the banking system itself is insignificant, and, taking into account the financial assets of such institutions, they cannot seriously affect the level of financial stability in the country. Precisely, taking into account what has been outlined in this article, the main attention will be focused on the activities of banking institutions, their functioning on the market of credit services. In fact, the importance of these financial institutions for the development of such a market determines the importance of the credit services market in ensuring stability of the banking system.

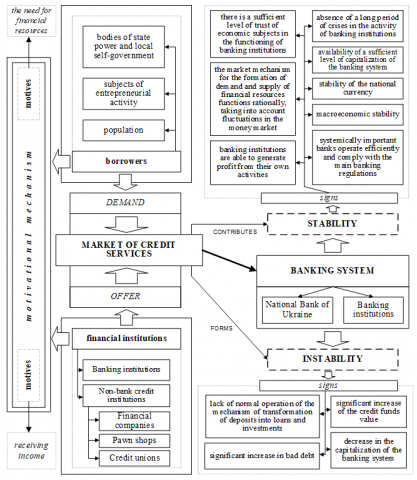

In Figure 2, the model of the interaction between the credit services market and the banking system is presented. During its construction, the modern trends in the development of these objects in Ukraine were primarily taken into account.

The data of Figure 2 should be considered in more detail. So, the credit services market and the banking system are large macroeconomic systems that develop and interact with each other. If the credit services market is an environment in which relations between borrowers and creditors take place, through which various financial institutions enter within the country, then the banking system is primarily a collection of all banking institutions, including the central bank (National Bank of Ukraine (NBU)). Thus, it can be clearly stated that stability of the banking system as a whole depends on the activity of banking institutions in the credit services market, their involvement in the development of such a market, the volume of active lending operations performed by banks and their specific weight in the income formation of these institutions.

However, the issue remains open, what is the stability of the banking system in general? Let's consider this issue in more detail in order to understand exactly the role of the credit services market in its provision.

Stability of the banking system is directly related to the state's policy of ensuring overall financial stability in the country. In the vast majority of countries, this task is entrusted to the work of central banks, in Ukraine - to the NBU. In the countries where commercial banks play a key role in the development of the entire financial system, their stable operation is a guarantee of financial stability in the country.

Analyzing the essence of financial stability, the NBU notes that the following occurs in the state economy under financial stability:

– the financial system effectively transforms free funds of citizens and businesses into loans and investments;

– the financial system is liquid and capitalized, and therefore resistant to crisis phenomena;

– payments and settlements are made on time and in full;

– participants of the financial system carefully assess risks and manage them;

- the difficulties of individual financial institutions do not extend to the system as a whole [31].

In fact, each of the outlined points can be ensured only on the basis of stable development of commercial banks in the financial system of Ukraine. Moreover, most of these features are directly related to the credit operations of these institutions and the quality of the credit portfolio formed by them.

For banking institutions of Ukraine, the development of credit services is an important area of business, which forms the majority of revenues. This is due to a number of peculiarities of the functioning of the Ukrainian banking system and the historical conditions of its formation. Among them are the following:

1) the underdevelopment of the investment services market, the lack of an alternative for economic entities to raise funds for their own development (the exception is large companies that have access to external financing);

2) the underdevelopment of the credit services market at the beginning of the 21st century, since the financial system of Ukraine until that time was in a difficult period of macroeconomic instability and gradually its development became stable;

3) the existence of a significant demand of economic entities for credit services, especially from households that did not have access to these resources;

4) after the Orange Revolution, the investment climate in Ukraine became more attractive for financial institutions, which led to the active entry of foreign banking institutions into the Ukrainian market, which actively began to develop the credit line of activity;

5) the important role of state banks in the development of the banking system, which began to actively lend to business entities;

6) quite effective policy of the NBU in terms of regulation of the activities of banking institutions, their provision of credit services in Ukraine, promptness of legislative changes in this area, etc.

In this way, banks took their leading position in the development of the entire financial system of Ukraine. As the historical development of these institutions over the next twenty years showed, this situation had both positive and negative consequences for the development of the entire financial system. During this period, the banking system, as a whole, as well as the national economy of Ukraine, went through an extremely difficult period of their own development. It was during this period that the financial crisis of 2007-2008 took place all over the world, the Orange Revolution, the Revolution of Dignity, the annexation of Crimea, the war in Donbas and a new war with Russia took place in Ukraine. All these complex political, economic and social processes always affect the development of the financial system, its stability, including had a destructive effect on the development of the banking system. And in fact, the most complex destructive processes in the functioning of this system were always related to credit operations, the effectiveness of banks' activities in this direction. For a more in-depth analysis of the outlined changes, we will use statistical data on the banking system functioning in Ukraine.

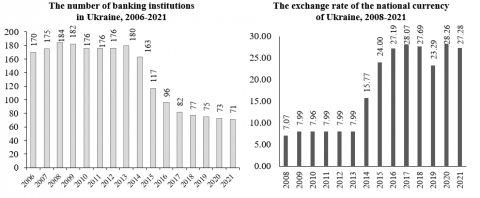

In Figure 3, the basic information about individual indicators of the development of banking institutions in Ukraine in 2006-2021 I presented. So, by the end of 2021, 71 commercial banks were operating in Ukraine. At the same time, in 2006, there were 170 such institutions. The main reason for the decrease in the number of banks is a radical change in banking legislation after the Revolution of Dignity, when the country's financial system was on the verge of collapse. With the support of the International Monetary Fund and international experts, a complex and comprehensive reform of the banking sector was carried out in the country, which was aimed at increasing the financial stability level of commercial banks and the financial system of Ukraine in general.

Figure 3. Main performance indicators of banking institutions in Ukraine

Source: generated by authors based on https://bank.gov.ua [31]

During the reform of the banking system, a number of complex problems were identified, which have been forming within such a system for a long time and have a negative impact on its stable development. The activity of banking institutions specifically in the field of lending has become one of the most difficult problems, the consequences of the solution of which continue to this day. First of all, during the analysis of the activities of banking institutions, it was found that a significant number of them are engaged in lending to the persons affiliated with their activities. Loans were issued to the enterprises, the owners of which, as it turned out later, were individuals who were directly involved in making decisions in banking institutions regarding lending. As a result, such business entities did not repay the loans taken, which significantly worsened the credit portfolio of banking institutions and the level of their financial stability. As a result of the reform, the banking system was cleansed of dubious financial institutions, a significant number of criminal cases were opened, total closure and recognition of insolvent banking institutions took place, which also played an important role in the development of the entire banking system, were systemically important for the economy development, but had a dubious reputation.

Consequences of the reform were ambiguous. However, it was necessary. As a result, there remained commercial banks that met new requirements of the NBU regarding the conduct of banking activities. A special role during the reform was given to ensuring the transparency of banks' activities, the disclosure of all their ultimate beneficiaries. Positive aspects of the reform include the increase in the level of financial stability of banks, the stabilization of their activities, and the development of their own capitalization increase plan for each banking institution. As further experience proved, all these measures were correct and really allowed to give a new impetus to the banking system development. This is confirmed by the fact that it was after the reform of this system that commercial banks in the country demonstrated the best indicators of their own activity, and the volumes of net profit that were declared were the highest during the entire period of the specified system operation.

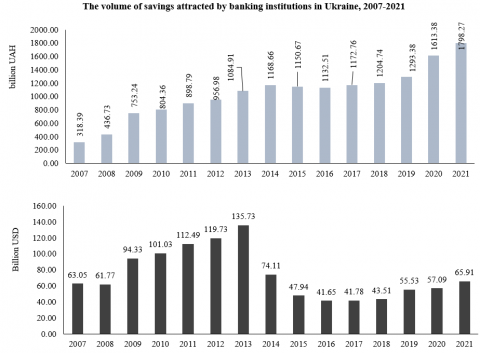

However, as a result of the reform, there were also certain negative consequences, both for the banking system and for the national economy development. Naturally, the decrease in the number of banking institutions, their recognition as insolvent led to the freezing of the customers’ deposits of these institutions. If individuals received their deposits back over time, real sector enterprises and financial institutions lost them. Insurance companies and non-state pension funds, which by law must keep their own financial resources in banks, are left in a difficult situation. Thus, this situation sharply reduced the level of trust in commercial banks and led to a significant outflow of funds from the banking system, and, accordingly, the volume of credit and investment operations decreased. In Figure 2 it is shown that in 2014-2016 there is a decrease in the amount of assets, involved savings.

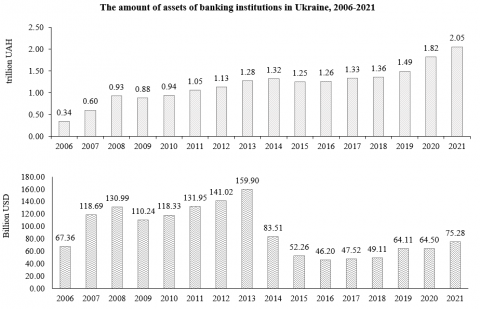

The period of reforming the banking system was also difficult, since the reform took place against the background of a difficult macroeconomic situation in the country, the devaluation of the national currency by more than three times (Figure 3). Accordingly, this led to the savings’ devaluation of economic entities. If you look at the main indicators of the the banking system development of Ukraine in dollars USA, which is more correct, as it corresponds to the real economic state of the country, then, as can be seen from Figure 3, the situation looks even more complicated. For example, the volume of assets of all commercial banks in 2021 amounted to 75.28 billion USD, although in 2013 it was 159.9 billion USD. The amount of savings at the end of 2021 was 65.91 billion USD. This is actually the indicator of 2006, when this indicator was equal to 63.05 billion USD. In 2013, the volume of deposits attracted by banks amounted to 135.73 billion USD.

Thus, it can be concluded that credit operations of banking institutions, the efficiency of their provision affect not only the development of individual commercial banks, but also affect the functioning of the entire banking system, can contribute to the emergence of crisis shocks that are difficult to overcome without worsening the macroeconomic situation in the country. Also, the consequence of reforming the country's banking system was the development and updating of methodical approaches to assessing stability of the country's financial system and its banking sector. The regulator has clearly established that banking institutions play a key role in stable development of the country's financial system and identified those segments in the activity of commercial banks in which crisis phenomena may occur. The credit sphere is defined as one of the most prone to producing dissipative processes in the functioning of the country's financial system.

In general, if we analyze the peculiarities of the development of the credit services market and the activities of financial institutions on it, we can clearly distinguish two groups of factors that exert the greatest influence on the functioning of such a market. The first group should include all endogenous factors that are formed inside financial institutions that provide credit services, their existence and influence are determined by the specific features of the functioning of the banking institution itself (scale of activity, type of banking institution, ownership of capital, chosen business model of development, qualifications of employees , accessibility to financial innovations, etc.). The second group should include exogenous factors that are formed in the economic space in which banking institutions operate. If endogenous factors are factors of subject influence, individual influence of a banking institution, then exogenous factors are systemic factors that have a macroeconomic, macro-financial nature. The regulation of the process of formation of such factors, regulation of the specifics of their influence is an important component of the monetary policy implemented by central banks. The number of exogenous factors is extremely large, they are highly interconnected, and all financial institutions are highly interconnected by financial relations, and that is why the occurrence of any fluctuations in the economic system immediately and quickly affects the development of banking institutions as the largest sub entities of the financial services market. Exogenous factors that influence the development of the credit services market include the discount rate, mandatory reserve norms, regulatory requirements for the activities of these institutions. An important role is played by purely economic indicators, namely: the level of average wages, the stability of the national currency, the inflation index, etc.

In Ukraine, to analyze the stability of the financial system, since 2008, the financial stress index (FSI) has been calculated, which characterizes the level of its instability in a certain period. This index is determined on the basis of 20 indicators grouped by five sub-indices (Figure 4).

Figure 4. Methodological features of determining the financial stress index

Source: generated by authors based on https://bank.gov.ua [31]

Each sub-index indicated in Figure 4, assigned an initial weight according to the volume and impact on the country's financial sector. The allocation of the banking sector sub-index within this index once again confirms an important role of the banking system in ensuring stability of the financial system. However, the financial stress index itself in general also quite reasonably characterizes the level of stability of the banking system, since the results of banking institutions are actually analyzed within each of its outlined sub-indices. This situation is related to the fact that commercial banks are, as already mentioned, the largest financial institutions in the country, which own the largest amount of financial assets. Today, these institutions play a key role in the development of not only the market of credit services, but also the market of deposit, investment services, and services in the field of settlement and cash services. They also exert an important influence on the functioning of the foreign exchange market and the sphere of public finance.

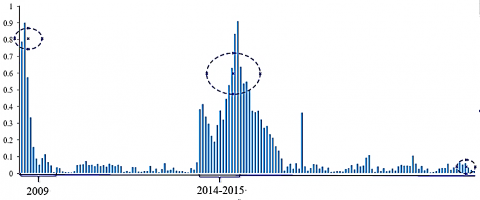

The NBU considers the financial stress index as an indicator reflecting the level of tension in the financial sector of Ukraine. The FSI takes on values from 0 to 1, where 0 is the complete absence of stress, and 1 is the highest level of stress [32]. In Figure 5, the value of the specified index for 2009-2021 is presented. Let's analyze the trends of changes in this index in more detail.

Figure 5. The value of the financial stress index (monthly) in Ukraine

Source: generated by authors based on https://bank.gov.ua [32]

So, the dynamics of the financial stress index in Ukraine during 2009-2021 confirms complex processes in the development of the country's financial system and its permanent state of crisis. In fact, the value of this index coincides with the ups and downs of the country's economic development. After the global financial crisis of 2007, the national currency in Ukraine devalued from UAH 5.05 to UAH 8.00, commercial banks lost significant funds due to inefficient credit policies, massive provision of foreign currency loans to clients who had no foreign exchange earnings and found themselves in a difficult situation. This led to significant losses in the banking system as a whole, which recovered over the next three years from such shocks. In general, by 2013, the specified system had already reached pre-crisis indicators and was actively developing, lending to the real sector of economy. However, the Revolution of Dignity and the political crisis again significantly reduced the pace of the country's economic development. The financial stress index in 2014-2015 reflected the difficult period of the financial system development, when its values approached the generally critical limit of 1.0 points. In fact, during this period, the specified index reached its maximum negative value in more than twenty years.

In the future, the country's financial system developed under permanent conditions of minor fluctuations. Today, it is quite clear that the financial stress index will again approach 1 in 2022, given the war with the Russian Federation and the difficult economic situation of the country. In fact, this period will be characterized by all the signs of macroeconomic instability, rising inflation, devaluation of the national currency, etc. However, taking into account the reform of the banking system, there are reasons to hope that the functioning of commercial banks in general will be stable in such difficult conditions, and there will be no mass bank failures. It is logical to allow the exit of commercial banks with Russian capital. This is very important for supporting the country's economy, providing social security for the population.

As noted, the financial stress index contains a significant number of indicators in its structure, but the impact of the rate of the banking system development on this indicator is undeniable. This is confirmed by statistical indicators and historical features of the banking system of Ukraine. We will analyze current trends in the development of the credit services market. As noted, the credit activity is one of the most important areas of the activity of banking institutions, which determines the high level of probability of crisis situations in this area.

The credit services market of Ukraine in its development repeats the development trends of the entire financial system of the country. However, at the same time, in certain years, crisis situations in this market were so deep that, in fact, banking institutions simply stopped any lending to economic entities. This had a very negative impact on the country's economic development and significantly slowed down its pace. In Figure 6, the information on the volume of loans issued by commercial banks in Ukraine in 2006-2021 is presented. This is the volume of all loans received by all economic entities during the outlined period. Analysis of the trend of this indicator in the national currency proves that there is a certain cyclicality in the provision of loans by banks. Of course, it is determined by the generally cyclical development of the country's financial system. However, the analysis of this indicator is already in dollars. The USA, which is a more real indicator, demonstrates a difficult situation in the development of the credit services market, which, it is quite clear today, will only worsen. Consequences of the war with the Russian Federation for this market will still have to be investigated.

So, at the end of 2021, the volume of loans issued by banks amounted to UAH 39.05 billion, which is lower than in 2006. That is, during the last twenty years, the credit services market in Ukraine has not actually developed, the real volumes of lending to the country's economy have not increased, which restrains the development of the country in general. The highest rate of lending was recorded in 2013 – 114.03 billion USD.

Figure 6. Analytical information about modern trends in the development of the credit services market of Ukraine

Source: generated by authors based on https://bank.gov.ua [32]

Analysis of the trend in the development of the credit services market in 2006-2021 shows that after the peak period of the maximum volume of lending, which was provided by commercial banks, in 2014 there is a sharp decline in the volume of such lending. As already mentioned, this is caused by a significant devaluation of the national currency, the strength of which was artificially supported by the NBU until 2013. However, after difficult economic and political situation of 2014-2015, economy of Ukraine suffered a significant destruction and, accordingly, the provision of loans was suspended by banking institutions.

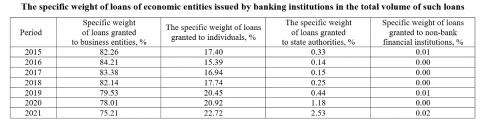

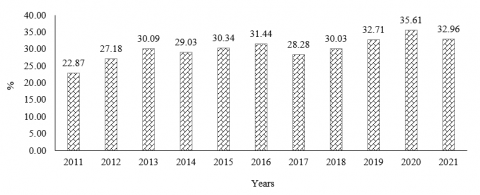

If we consider the structure of the banks' loan portfolio by subjects to which these institutions granted loans, we can see that the main borrowers are subjects of the entrepreneurial activity. In 2015, more than 82.0% of all loans were granted to these entities. However, the 2015-2021 trend shows that business lending in Ukraine by banking institutions gradually decreased, which was accompanied by an increase in loans issued to the population and state authorities. If in 2015 the specific weight of loans to individuals was 17.4%, then in 2021 it will be 22.72%. The growth is quite substantial. This shows that banking institutions in Ukraine consider the sphere of lending to the population as a promising direction for obtaining income, which is determined by high credit rates and the growing demand of the population for loan resources. In Figure 7, the information on the level of credit rates for loans offered to individuals is provided. Interest rates are really high compared to similar credit products in developed countries. However, the demand even for such loans remains consistently high.

Figure 7. The level of interest rates on loans to the population

Source: generated by authors based on https://bank.gov.ua [32]

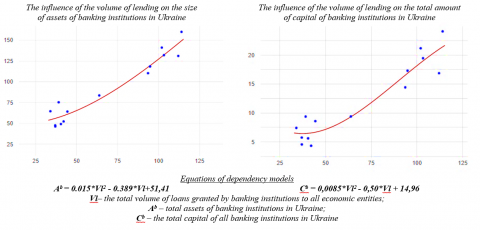

We will conduct a study of the impact of the volume of loans provided by banking institutions in Ukraine on the main parameters of the banking system functioning. This will confirm the importance of the credit services market and its significant impact on stable development of such a system. To do this, we will use the described method of determining cubic one-factor regression models of the influence of one indicator on the change of another. Let's build the following correlation models:

1) the influence of the volume of loans on the volume of assets in the banking system of Ukraine;

2) the influence of the volume of loans on the total amount of capital of banking institutions.

As a result of the relevant calculations, we will get the following regression models, which are presented in Figure 8.

Figure 8. The impact of the credit services market on stability of the banking system

Source: generated by authors based on https://bank.gov.ua [32]

Therefore, the analysis of Figure 8 gives reason to draw the following conclusions. Stability of the banking system lies in the gradual development of banking institutions in Ukraine, their ability to provide income and profit. Accordingly, the growth of assets of such institutions is one of the signs of the development of the entire banking system. Analysis of statistical data shows that loans in the volume of assets of banking institutions occupy a rather significant part. That is why their development is determined to a large extent by the development of the credit services market, the gradual increase in the volume of loans issued by banks to various entities. Econometric modeling of the impact of loans on bank assets confirms this. The regression model built as a result of the analysis is adequate, since the value of the coefficient of determination is 0.93, which indicates a high level of influence of one indicator on another parameter.

Also, conducting an econometric analysis made it possible to establish that credit operations and their volume are also directly related to the amount of capital of banking institutions. The obtained regression model is adequate, since the coefficient of determination is 0.9, and the correlation coefficient is 0.94. Thus, it can be argued that the increase in the volume of credit operations also leads to a gradual increase in the capital of banking institutions, which, in turn, contributes to the increase of stability of banking institutions to the influence of various factors. As a result, it ensures the stability of the entire banking system of the country.

The conducted calculations only confirm the important role of the credit services market in ensuring stability of the banking system of Ukraine, and the development of such a system is impossible without credit services.

The article examines the role of the credit services market in ensuring stable development of the banking system. Using the example of the functioning of banking institutions in Ukraine, the role of this market in the development of the entire financial system of the country is clearly analyzed. As a result, certain theoretical provisions of the influence of lending and the stability of the banking system were deepened, and a thorough analysis of modern trends in the functioning of the banking system of Ukraine and its credit services market was carried out.

Conducting a study based on a retrospective analysis of the development of the credit services market in the long-term allowed to identify certain patterns of such development, single out and describe the factors that affect the functioning of banking institutions and, in general, to clarify the prerequisites for the formation of crisis phenomena in the work of the banking system. The study also made it possible to establish and justify the important dependence between credit services of banking institutions, their stability, stability of the banking system and the development of the financial system. It has been established that countries in which lending is the main source of attracting resources for the development of economic entities are particularly vulnerable to the emergence of crisis situations in this direction, and therefore the issue of finding mechanisms for identifying, determining and preventing aggregate credit risk remains relevant for state institutions specific to individual banking institutions, and the systemic credit risk of the banking sector.

A detailed examination of the development of the credit services market in Ukraine allows us to formulate the main measures to ensure the further development of this market. These include the following: ensuring the financial stability of banking institutions through constant monitoring of their financial activities and the implementation of modern preventive methods of analyzing their work; coordination of the financial policy in the country with the main measures of the economic policy implemented by the government; implementation of measures to gradually reduce the cost of borrowed funds, which remain expensive in the country; impossibility of inflation growth due to a sharp increase in the availability of loan funds; increasing the transparency of the activities of non-bank credit institutions; activation of the mortgage market, which has been developing chaotically and unsystematically in the country for the past ten years, etc. It should be noted that the development of the credit services market requires the search for optimal measures to activate its functioning and at the same time ensure price stability in the country. As evidenced by the retrospective of the development of the financial services market of Ukraine, the fact that the inflation index is within acceptable limits is an important component of maintaining macroeconomic stability in the country and the level of social and economic security of citizens. However, it is extremely difficult to ensure the economic development of the country, as well as the banking system, without the effective functioning of the credit services market.

[1] Denysova, A., Vovk, V., Rudoi, K., Kyrychenko, T. (2021). Management and legal aspects of the symbiosis of banking institutions and fintech companies in the credit services market in the context of digitization. Estudios de Economia Aplicada, 39(7). https://doi.org/10.25115/eea.v39i7.5013

[2] Dubyna, M., Zhavoronok, A., Kudlaieva, N., Lopashchuk, I. (2021). Transformation of the household credit behavior in the conditions of digitalization of the financial services market. Journal of Optimization in Industrial Engineering, 14(1): 97-102.

[3] Revindo, M.D., Gan, C. (2017). Credit market and micro-credit services in rural China. Microfinance In Asia, 93-146. https://doi.org/10.1142/9789813147959_0004

[4] Danylyshyn, B., Dubyna, M., Zabashtanskyi, M., Ostrovska, N., Blishchuk, K., Kozak, I. (2021). Innovative Instruments of Monetary and Fiscal Policy. Universal Journal of Accounting and Finance, 9(6): 1213-1221.

[5] Boiarynova, K., Popelo, O., Tulchynska, S., Gritsenko, S., Prikhno, I. (2022). Conceptual Foundations of Evaluation and Forecasting of Innovative Development of Regions. Periodica Polytechnica Social and Management Sciences, 30(2): 167–174. https://doi.org/10.3311/PPso.18530

[6] Zhavoronok, A., Popelo, O., Shchur, R., Ostrovska, N., Kordzaia, N. (2022). The role of digital technologies in the transformation of regional models of households’ financial behavior in the conditions of the national innovative economy development. Ingénierie des Systèmes d’Information, 27(4): 613-620. https://doi.org/10.18280/isi.270411

[7] Volosovich, S., Krivosheeva, V. (2016). Self-regulation of the credit services market for individuals. Economic Annals-XXI, 158(3-4): 79-82. https://doi.org/10.21003/ea.V158-18

[8] Dubyna, M., Popelo, O., Kholiavko, N., Zhavoronok, A., Fedyshyn, M., Yakushko, I. (2022). Mapping the Literature on Financial Behavior: a Bibliometric Analysis Using the VOSviewer Program. WSEAS Transactions on Business and Economics, 19: 231-246.

[9] Vovk, O., Kravchenko, M., Popelo, O., Tulchynska, S., Derhaliuk, M. (2021). Modeling the Choice of the Innovation and Investment Strategy for the Implementation of Modernization Potential. WSEAS Transactions on Systems and Control, 16: 430-438. https://doi.org/10.37394/23203.2021.16.38

[10] Marhasova, V., Tulchynska, S., Popelo, O., Garafonova, O., Yaroshenko, I., Semykhulyna, I. (2022). Modeling the harmony of economic development of regions in the context of sustainable development. International Journal of Sustainable Development and Planning, 17(2): 441-448. https://doi.org/10.18280/ijsdp.170209

[11] Popelo, O., Tulchynska, S., Revko, A., Butko, M., Derhaliuk, M. (2022). Methodological Approaches to the Evaluation of Innovation in Polish and Ukrainian Regions, Taking into Account Digitalization. Comparative Economic Research. Central and Eastern Europe, 25(1): 55-74. https://doi.org/10.18778/1508-2008.25.04

[12] Kusi, B.A., Agbloyor, E.K., Simplice, A.A., Abor, J. (2022). Foreign bank and banking stability in Africa: does strong and weak corporate governance systems under different regulatory regimes matter? Journal of Financial Economic Policy, 14(2): 207-241. https://doi.org/10.1108/JFEP-02-2021-0044

[13] Amadi, A., Adetiloye, K., Babajide, A., Amadi, I. (2021). Banking system stability: A prerequisite for financing the Sustainable Development Goals in Nigeria. Banks and Bank Systems, 16(2): 103-118. https://doi.org/10.21511/bbs.16(2).2021.10

[14] Khattak, M.A., Hamid, B.A., Islam, M.U., Ali, M. (2021). Competition, diversification, and stability in the Indonesian banking system. Buletin Ekonomi Moneter dan Perbankan, 24: 59-88. https://doi.org/10.21098/BEMP.V24I0.1481

[15] Amadi, A.N., Adetiloye, K.A., Omankhanlen, A.E., Amadi, I.P., Nwodimmah, P. (2021). The stabilization effects of fiscal policy on banking system stability in Nigeria. Asian Economic and Financial Review, 11(10): 805-815. https://doi.org/10.18488/JOURNAL.AEFR.2021.1110.805.815

[16] Hryhorkiv, V., Buiak, L., Verstiak, A., Hryhorkiv, M., Verstiak, O., Berdnuk, A. (2019). Mining Credit Interest Rate Data from Multiple Data Sources. 9th International Conference on Advanced Computer Information Technologies: 265-268. https://doi.org/10.1109/ACITT.2019.8780034

[17] Shkarlet, S., Dubyna, M., Vovk, V., Noga, M. (2019). Financial service markets of the Eastern Europe: a compositional model. Economic Annals-XXI, 176(3-4): 26-37.

[18] Ostrovska, N., Hrapko, N. (2014). Condition and dynamics of lending analysis in Ukraine (2011-2013). Economic Annals-XXI, 9-10(2): 15-18.

[19] Tkachuk, I. (2017). Asset operations of Ukrainian banks on the current stage of banking system development. Banks and Bank Systems, 12(1-1): 119-127. https://doi.org/10.21511/bbs.12(1-1).2017.04

[20] Pan, H., Fan, H. (2021). Stability of the Banking System with Shadow Banking on Different Inter-bank Network Structures. Discrete Dynamics in Nature and Society, 6650327. https://doi.org/10.1155/2021/6650327

[21] Pan, H., Fan, H. (2020). Research on the Stability of the Banking System With Shadow Banking Under Macroeconomic Fluctuation. Frontiers in Physics, 85: 338. https://doi.org/10.3389/fphy.2020.00338

[22] Blahun, I., Blahun, I., Blahun, S. (2020). Assessing stability of the banking system based on fuzzy logic methods. Banks and Bank Systems, 15(3): 171-183. https://doi.org/10.21511/bbs.15(3).2020.15

[23] Subbar, H.H., Guirinsky, A.V. (2020). Technical ways to the development of financial stability of the banking system in Iraq. International Journal of Advanced Science and Technology, 29(1): 7-10.

[24] Shkolnyk, I., Frolov, S., Orlov, V., Datsenko, V., Kozmenko, Ye. (2022). The impact of financial digitalization on ensuring the economic security of a country at war: New measurement vectors. Investment Management and Financial Innovations, 19(3): 119-138. https://doi.org/10.21511/imfi.19(3).2022.11

[25] Gao, Q., Fan, H. (2020). Effect of the Dynamic Macroeconomic Fluctuation on the Stability of a Banking Network System with Scale-Free Structure. Mathematical Problems in Engineering, 7158506. https://doi.org/10.1155/2020/7158506

[26] Kozmenko, S., Shkolnyk, I., Kozmenko, O., Orlov, V., Shukairi, F. (2021). Modeling of the financial system’s stability on the example of Ukraine. Equilibrium. Quarterly Journal of Economics and Economic Policy, 16(2): 377-411. https://doi.org/10.24136/eq.2021.014

[27] Marhasova, V., Kovalenko, Yu., Bereslavska, O., Muravskyi, O., Fedyshyn, M., Kolesnik, O. (2020). Instruments of Monetary-And-Credit Policy in Terms of Economic Instability. International Journal of Management, 11 (5): 43-53.

[28] Marhasova, V., Garafonova, O., Popelo, O., Tulchynska, S., Pohrebniak, A., Tkachenko, T. (2022). Environmentalization of Production as a direction of ensuring the sustainability of production activities of enterprises and increasing their economic security. International Journal of Safety and Security Engineering, 12(2): 159-166. https://doi.org/10.18280/ijsse.120203

[29] Ramachann, N., Al-muqaimi, S.K., Al-hajri, N.R. (2022). Characteristics of audit committee and banking sector performance in Oman. J. Corp. Gov. Insur. Risk Manag., 9(S1), 263-273. https://doi.org/10.51410/jcgirm.9.1.17

[30] Rahman, A. M. (2022). Can voluntary insurance be a new product in bank-led e-banking: Statistical analysis of customers’ preferences in Bangladesh-economy? J. Corp. Gov. Insur. Risk Manag., 9(S1), 215-228. https://doi.org/10.51410/jcgirm.9.1.14

[31] National Bank of Ukraine: official site. https://bank.gov.ua/ua/stability/about. Financial Stress Index. https://bank.gov.ua/ua/stability

[32] Financial Stress Index. https://bank.gov.ua/ua/stability.