Maylia Pramono Sari*![]() | Retnosari Widiastutik

| Retnosari Widiastutik![]() | Muhammad Khafid

| Muhammad Khafid![]() | Niswah Baroroh

| Niswah Baroroh![]() | Richatul Jannah

| Richatul Jannah![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The results of previous studies vary regarding the effect of company size and financial performance on disclosure of carbon emissions. This article aims to find empirical evidence of the effect of company size and financial performance on disclosure of carbon emissions by adding PROPER rating as a mediating variable as the novelty of this study. The population is 144 non-financial companies listed on the IDX in 2015-2019. The results show that company size affects PROPER rating and disclosure of carbon emissions. Meanwhile, financial performance has no effect on disclosure of carbon emissions with a PROPER rating. PROPER rating can mediate the effect of company size on disclosure of carbon emissions, but PROPER rating is not able to mediate ROA on Carbon Emissions. The implications of the findings of this research, companies, governments, investors and stakeholders in decision making related to Carbon Emission Disclosure. For example choosing a company that has a greater level of relationship with the environment or including a high-profile company as a place to invest. In addition, academics can develop models and replace financial performance proxies with other proxies related to leverage, liquidity and solvency.

carbon emission disclosure, company size, financial performance, PROPER

The world organization stated that air pollution is one of the biggest health risks in the world, only seven million deaths can be prevented, and the other 90% are still breathing polluted air with a total of almost three thousand million people. This becomes an important issue in controlling carbon emissions. The global community recognizes the importance of good governance in long-term disaster mitigation. This is also done by Indonesia. Indonesia takes an active role in the world's commitment to reducing carbon emissions. This is evidenced by Indonesia's commitment to the National Determination Contribution (NDC) to reduce greenhouse gas emissions by 26% in 2020 and 29% in 2030. This ratification increased by 41% in 2021 to the Paris Agreement 2015. Indonesia's commitment indicates that carbon emissions are important things to control since the long-term impact will affect the lives of the wider community.

Carbon emission disclosures in Indonesia are still very rarely done. This is because the disclosure of carbon emissions is still voluntary. There are research results which state that currently regulations in Indonesia are ineffective and law enforcement is low, so not all companies comply with disclosure of carbon emissions. Indonesian industry plays an active role in contributing to carbon emissions [1]. In 2014, Indonesia contributed 1.4% of the world's total CO2 carbon emissions a total of 13.5%. Considering the rapid development of industry in Indonesia, special attention is needed to manage carbon emissions from industry. It should be known that the main source of carbon emissions is the consumption of energy where this energy is the main source of driving the economy. Hence, energy reconstruction is the key to achieving the goal of mutual benefit [2].

There are many companies established in Indonesia that commit violations. PT Mahkota Indonesia committed a violation through chimney waste that was released but did not comply with quality standards. This caused air pollution to occur. In addition, PT Xing Xing Steel also polluted the air through condensed smoke mixed with black dust. This resulted in disturbances to the health of the surrounding community. The growth of carbon can increase the potential for disease through an increase in temperature, besides that, there will be a greater danger to people in industrialized areas [3].

The PROPER program in Indonesia can be claimed as a large program with quite expensive funds. However, this program is claimed to have an important role in the development of corporate sustainability reports [4-8]. Program is expected to increase the disclosure of environmental responsibility in the industrial sector. KEMENLHK report in 2019 that PROPER's success in carrying out management is proven by an increase in the innovation of 46%, recorded 542 innovations in 2018 and 794 innovations in 2019. Cost savings reached 192.63 trillion from the increase in innovation carried out in 2019.

The Ministry of Environment and Forestry of the Republic of Indonesia is an institution government appointed to be in charge of the PROPER rating program. It was formed to facilitate the company's responsibility to the environment. It is hoped that progress on environmental responsibility will be achieved by the company. The real work of this program is proven in 2019 the number of emissions from 2,147 the company reported reaching 579,107.34 tons of SO2, 392,000.8 tons of particulates, 260,357.87 tons of NO2. Meanwhile, the liquid waste discharged reached 414,886.62 tons of BOD, 863,774.4 tons of COD, 125,474.72 tons of TSS, 150,644.06 tons of oil and fat, and 1,645.58 tons of Ammonia, while the amount of B3 waste reached 64,794,326.66 tons. PROPER Report 2019 shown the progress management 60.2% has been managed properly, and 30.8% is still stored in temporary disposal.

The establishment of this ministry, which has a controlling function is expected to increase the company's environmental disclosure responsibility. This is driven by the PROPER rating which gives an overview of the quality level of corporate responsibility to the environment. In addition, a study conducted the carbon management has a significant positive effect on corporate financial performance [9]. This assumes that the PROPER rating can be a mediator in increasing carbon emission disclosures getting stronger.

The disclosure of carbon emissions has a significant impact on the government and society. The development of carbon emission research has been done a lot to see the effect of industrial activities on carrying out environmental responsibilities. Several studies on carbon emissions were conducted by [10-21]. Those studies used various measurement variables such as environmental disclosure, profitability, company size, company age, industry type, institutional ownership, financial decline, etc.

Research conducted by the researches [11, 14, 16] found that company size significantly positively affects environmental disclosure. Carbon emission disclosures. In contrast, the research conducted by the research [22] found that company size does not affect carbon emission disclosures. The results of research conducted by the research [22] find that financial performance has a significant positive effect on environmental disclosure. The findings are different from the research conducted by the researches [11, 14], who found that financial performance does not affect environmental disclosure. Other empirical evidence is from the research conducted by the researches [10, 21] found that financial performance has a significant positive effect on carbon emission disclosure. It is different from research conducted by the research [12], which finds that financial performance does not affect carbon emission disclosure.

The research above indicates inconsistency between the research results and the variables the researchers will analyze. Updating other variables that become factors in conducting carbon emission disclosures was necessary. Based on several analyzes of the PROPER program that the government has implemented to increase corporate responsibility in managing the environment, the researchers raised the PROPER rating as a mediating variable in influencing carbon emission disclosures in companies that receive the PROPER rating. The objective of this study is to know the factors that influence carbon emission disclosure as a dependent variable.

Legitimacy theory explains the importance of aligning the picture of values adopted by the company and society. Because companies need to take responsibility for operations carried out in communities that have an impact on the environment [23, 24]. Meanwhile, the stakeholder theory developed by the research [25] explains: regarding organizational management related to ethics in business, which discusses related to the interests of the parties directly affected or indirectly by the company's operational system. The contribution of this research is to add to the empirical research literature related to the role of PROPER ratings on the relationship between carbon emission disclosures and their constituent determinants as a novelty in this research.

Company size is a reflection of the level of corporate operational activities. The larger the size of a company, the company will increasingly consider the quality of its resources. The community finds large-sized companies as established companies compared to small-scale companies. Companies with large sizes tend to have higher pressure from the community and stakeholders. Legitimacy theory explains that there is pressure from external parties, both social and political, so companies will be more likely to disclose information. Research of the researches [11, 14, 16, 26-29] proved that companies with larger size would more and more improve the performance of environmental responsibility disclosure report.

H1. Company Size has a significant positive effect on the PROPER rating

Companies with good financial performance are considered competent in managing the companies well, and Stakeholder theory explains that companies need to pay attention to other interests. Companies with good financial performance can easily make voluntary disclosures so that pressure from outside can respond well. Thus, this makes it easier for companies to fulfill their responsibilities in environmental disclosure.

H2. Financial Performance has a significant positive effect on the PROPER rating

Company size indicates the level of activity and utilization of resources consumed by the companies in their operations. Legitimacy is an organizational concept that adopts strategies to remove gaps, such as changing relevant public perceptions using social disclosures [23, 30]. Thus, the larger the company's size, the community will assume the company uses a lot of resources, which will generate waste due to the company's operational activities. Thus, the relationship between company size and carbon emission disclosure is significantly positive. It is in line with the previous research conducted by the researches [10, 12, 21], who found evidence that company size has a significant positive effect on carbon emission disclosure.

H3. Company size has a significant positive effect on Carbon Emission Disclosure

Financial performance, the company will be considered good in managing the effectiveness of the company's activities, and it will give the company healthy financial structures. Thus, the companies can disclose carbon emissions. Stakeholder theory explains that an approach needs to be taken to stakeholder parties so that the company's attention is focused on profit goals and other factors [25]. This study is supported by previous research which found empirical evidence that financial performance has a significant positive effect on carbon emission disclosure.

H4. Financial Performance has a significant positive effect on Carbon Emission Disclosure

The PROPER rating is a corporate assessment program in carrying out its responsibilities in terms of environmental management carried out by the minister of the environment. With stakeholder interests influencing the company, it is necessary to fulfill the responsibilities of other parties. Thus, the PROPER rating is a program carried out by the government to control the disclosure of environmental responsibility. The more an industry gets a good rating, the more it will show an increase in exposure to carbon emissions which is part of environmental responsibility. Research conducted by the researches [31, 32] found that the PROPER rating can significantly affect carbon emission disclosure.

H5. The PROPER rating has a significant positive effect on Carbon Emission Disclosure

Large-sized companies will encourage companies to improve their resources to realize the efficiency of corporate performance. Research of [20] explained that companies with large sizes would be more capable of making environmental disclosures than companies with middle or small levels. Legitimacy theory explains the importance of companies in equalizing perceptions between company goals and external parties' goals. Therefore, with good environmental responsibility disclosures, the companies are concerned about the responsibilities of other parties. The researches [12, 16, 21, 26, 27, 29] found evidence that company size can have a significant positive effect on environmental performance. Therefore, the researchers assume a significant positive relationship between company size and carbon emission disclosure mediated by PROPER rating.

H6. The PROPER rating can mediate the effect of Company Size on Carbon Emission Disclosure

Financial performance can show the effectiveness and efficiency of the company in generating profits through the use of assets owned by the company. Companies with good financial performance would make voluntary disclosures easily compared to companies with poor financial performance. Stakeholder theory explains the existence of external forces that require attention from the companies so that the companies need to fulfill the interests of each party. With this, it is assumed that if the companies have good financial performance, the disclosure of environmental responsibility will increase to fulfill the responsibility to stakeholders. Previous research conducted by Gatimbu and Wabwire [22] found empirical facts that financial performance has a significant positive effect on the disclosure of corporate environmental performance. Therefore, the researchers assume that there is a significant positive relationship between the PROPER rating as a factor that mediates the increase in carbon emissions in obtaining a better rating for the benefit of stakeholders.

H7. The PROPER rating can mediate the effect of Financial Performance on Carbon Emission Disclosure

This study was quantitative research with a research sample of non-financial companies listed on the Indonesia Stock Exchange (IDX) during the 2015-2019 time period. The population of this study is all non-financial companies listed on the Indonesian Stock Exchange. While the sample was taken from non-financial companies during the 2015-2019 periodic with a purposive sampling method. The companies used as samples are non-financial companies, have a PROPER rating, have consecutive financial reports during the study period, and disclose at least one policy related to emissions carbon.

Based on these criteria, the number of sample companies that can be collected is as many as 30 companies or 144 observations as can be seen in Table 1. Criteria The sample companies include PROPER ratings and are listed on the Indonesia Stock Exchange for 5 consecutive years, as well as disclosing carbon emissions in the environmental responsibility report/sustainability report.

Table 1. Sampling Criteria

|

Sample Criteria |

Total |

|

Companies listed on the Indonesia Stock Exchange (IDX) in 2015-2019 |

713 |

|

Companies belong to the financial sector |

(94) |

|

Non-financial companies that were not included in the Performance Rating Program (PROPER) rating given by the Ministry of the Environment of the Republic of Indonesia for the period 2015-2019 |

(503) |

|

Non-financial companies that did not report consecutive financial statements in the 2016-2019 period |

(56) |

|

Companies that do not disclose carbon emissions (at least one policy related to carbon emissions) explicitly or implicitly |

(30) |

|

Samples that meet the criteria |

30 |

|

Total units during analysis during the observation period 2015-2019 (5 years) |

150 |

|

Outlier |

6 |

|

Total data analysis units |

144 |

Source: Secondary data processed (2021)

Table 2. Definitions and indicators of research variables

|

No. |

Variables |

Definition |

Indicators |

|

1. |

Company size (Size) |

Company size is a measurement made by comparing the size of one company with other companies that use total assets or various other measurements from the company (Riyanto, 2008). |

Size = Ln (Total Asset) |

|

2. |

Financial Performance |

Return on Assets (ROA) is a measure of corporate effectiveness in generating profits by utilizing corporate assets. |

Net Profit ∑ The asset of the year+ ∑ previous year's assets/2 (average asset) |

|

3. |

PROPER Rating |

The Ministry of Environment (2018) defined PROPER rating as a program given to companies as a form of acknowledgment of the existence of the law of action and reaction that has been carried out by companies. |

Looking at the Decree of the Ministry of Environment:

|

|

4. |

Carbon Emission Disclosure |

Choi et al [12] explained that carbon emission disclosure is one type of environmental disclosure that has the scope of disclosure of green house gases and energy use as well as performance and strategies on the target to conduct risk reduction that has an impact on climate. |

Content analysis by calculating corporate disclosure based on the theory of Choi, et al. [12] $\mathrm{CED}=\frac{\text { Total items disclosed }}{18}$ |

Source: Various references, processed on 2021

While the definitions and indicators of the research variables are presented in Table 2 which presents in detail the variables used in this study along with the meaning and method of measurement. There are five variables used in this study the size of the company (size), the level of debt (leverage), financial performance, rating PROPER, and the level of disclosure of carbon emissions.

The data collection techniques used documentation and content analysis techniques based on the annual reports. The results of data analysis were obtained and analyzed using descriptive analysis and path analysis, and the Sobel test with the tools of IBM SPSS Statistics 25 and the Sobel test calculator. The Sobel test is used to determine whether a variable carrier can mediate the effect of an independent variable on the dependent variable. The hypothesis testing used the Sobel value test after the data met the assumptions of the classical assumption test criteria which are normality, multicollinearity, autocorrelation, and heteroscedasticity test.

4.1 Descriptive statistical analysis

This study's descriptive statistical analysis shows the mean, maximum, minimum, and standard deviation values of the research variables. The results of the descriptive statistical analysis are shown in Table 3 Classic Assumption Test. From Table 3. It can be seen that the companies used as samples are on the average medium-sized company (13.10), with a moderate level of profitability (0.09), a moderate PROPER rating (3.29), and reported 7-8 carbon emission items as required [12].

Table 3. Descriptive statistical analysis

|

|

N |

Minimum |

Maximum |

Mean |

Std. Deviation |

|

SIZE |

144 |

10.284 |

16.477 |

13.10237 |

.805083 |

|

ROA |

144 |

-.449 |

1.983 |

.09275 |

.241628 |

|

PROPER |

144 |

2 |

5 |

3.29 |

.566 |

|

CED |

144 |

0.056 |

0.889 |

0.37577 |

.218103 |

|

Valid N (listwise) |

144 |

|

|

|

|

Source: Processed secondary data, 2021

The classical assumption test is conducted to meet the normative requirements before conducting the research hypothesis analysis. The normality test is carried out by using the Kolmogorov-Smirnov (K-S) test, which is indicated by a residual value of 0.053 (α > 0.05), so the data are concluded to have a normally distributed component. The multicollinearity test shows the VIF value < 0.10. It is assumed that the data are free from multicollinearity. The Run Test examines the autocorrelation in the distribution of data values and obtains a residual value of 0.870, indicating that the data are free from autocorrelation. The heteroscedasticity value shows a significance number >0.05. It is concluded that the data are free from heteroscedasticity.

The coefficient of determination test is conducted to determine the effect of the research model on the dependent variable. The adjusted R2 value is 0.194. From the analysis result, it can be concluded that the effect of company size, financial performance, and PROPER rating on carbon emission disclosures has an effect of 19.4%. Meanwhile, the remaining 80.6% is influenced by variables outside the research model.

4.2 Path analysis

The path analysis test aims to indirectly determine the relationship's size from the dependent variable. This analysis is carried out by regressing the effect of the intervening variable on the independent variable. Furthermore, regression is carried out from the dependent variable to the independent and intervening variables. The analysis results are presented in Table 4 and Table 5. The value of sig <0.05 indicates a significant effect, while the value of Unstandardized Coefficients indicates the direction of the effect. Figure 1 shows the model research result.

Table 4. The test result for path analysis Sub I coefficient

|

Model |

Unstandardized Coefficients |

Standardized Coefficients |

t |

Sig. |

||

|

B |

Std. Error |

Beta |

||||

|

|

(Constant) |

.558 |

.745 |

|

.749 |

.455 |

|

1 |

SIZE |

.208 |

.057 |

.296 |

3.652 |

.000 |

|

|

ROA |

.121 |

.190 |

.052 |

.637 |

.525 |

a. Dependent Variable: PROPER Source: Processed secondary data, 2021

Table 5. The test result of path analysis Sub II coefficient

|

Model |

Unstandardized Coefficients |

Standardized Coefficients |

t |

Sig. |

||

|

B |

Std. Error |

Beta |

||||

|

|

(Constant) |

-4.724 |

.799 |

|

-5.915 |

.000 |

|

|

SIZE |

.187 |

.064 |

.237 |

2.940 |

.004 |

|

1 |

ROA |

.011 |

.203 |

.004 |

.053 |

.958 |

|

|

PROPER |

.336 |

.090 |

.298 |

3.727 |

.000 |

a. Dependent Variable: CED_Y

Source: Processed secondary data, 2021

Sources: Processing date 2021

Figure 1. Model of research result

4.3 Sobel test

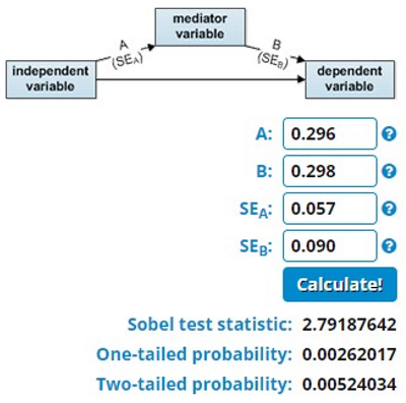

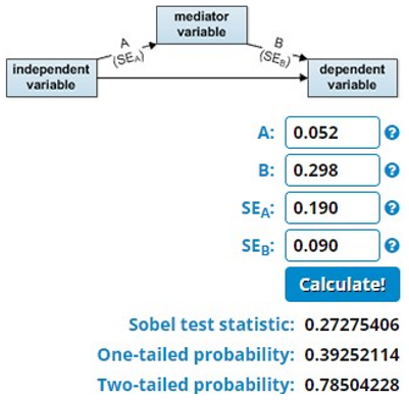

The result of the Sobel test shows the relationship effect between the mediating variable used to influence the relationship between the independent and dependent variables. This study uses the Sobel test calculator for the significance of mediation through www.danielsoper.com to know the relationship between variables mediated by PROPER ratings. The result of the Sobel test is as follows in Figure 2 and Figure 3:

Sources: Processing secondary date 2021

Figure 2. Company size

Sources: Processing secondary date 2021

Figure 3. Financial performance

Table 6. Summary of research hypothesis results

|

Hypothesis |

Explanation |

Regression Coefficient |

t-test |

Sig. |

Results |

|

H1 |

Company size has a significant positive effect on the PROPER rating |

0.208 |

3.652 |

0.000 |

Accepted |

|

H2 |

Financial Performance does not have a significant positive effect on the PROPER rating |

0.121 |

0.637 |

0.525 |

Rejected |

|

H3 |

Company size has a significant positive effect on Carbon Emission Disclosures |

0.187 |

2.940 |

0.004 |

Accepted |

|

H4 |

Financial Performance does not have a significant positive effect on Carbon Emission Disclosures |

0.011 |

0.053 |

0.958 |

Rejected |

|

H5 |

The PROPER rating has a significant positive effect on Carbon Emission Disclosure |

0.336 |

3.727 |

0.000 |

Accepted |

|

H6 |

The PROPER rating can significantly mediate Company Size on Carbon Emission Disclosure |

|

|

|

Accepted |

|

H7 |

PROPER rating is not able to mediate significantly Financial Performance on Carbon Emission Disclosure |

|

|

|

Rejected |

Source: The analysis results processed by the authors, 2021

Based on Table 6, research on the effect of SIZE has a significant positive effect on PROPER ratings (Sig. 0.000). This provides support and verification of the theory of legitimacy in which companies make environmental disclosures in response to external interests outside the company and by the social contract. Because the larger size of the company will encourage the strong influence of the community to put pressure on the company. So, the legitimacy of the community plays an important role for large companies. Research of Modugu and EBOIGBE [28] explained that large companies require greater costs to increase stakeholder trust and are more subject to public scrutiny. Thus, the results of this study support previous research conducted by the researches [11, 14, 16, 26-29].

This study obtains empirical evidence that financial performance does not affect the PROPER ratings (sig. 0.525). Thus, the stakeholder theory cannot confirm a significant positive relationship between the effect of financial performance on the PROPER rating. The researchers assume that the existence of company budgeting systems makes financial performance not affect environmental disclosure. In addition, when companies want to increase consumer trust, the researchers assume that the companies will increase the image of the disclosure of social aid. Researches [11, 14, 33, 34] support findings that financial performance does not affect environmental disclosure.

This study shows that SIZE has a significant positive effect on the disclosure of carbon emissions (sig. 0.004). Company size shows the level of company operational activities that are more complex than small companies. Large companies tend to get greater pressure from the public, this is because the resources used by these companies are more than others. Research of [35] describe the disclosure of carbon emissions and political pressure from stakeholders. Thus, the larger the SIZE of the company, it will encourage companies to disclose carbon emissions caused by the public interest. Disclosure of carbon emissions is a form of legitimacy strategy to comply with existing social norms in society so that the social contract is fulfilled. This study follows the previous researches of [26, 27, 29, 34].

This study shows that ROA does not affect carbon emission disclosure (sig. 0.958). This hypothesis cannot confirm the stakeholder theory, that is, the influence of external parties, one of which is the government. The researchers assume that funds are allocated for other disclosures besides the environment to increase profitability. In addition, each company allocates funds at the beginning of the period so that during the current period, the company no longer needs to allocate more funds if financial performance improves. The cost burden of the company in carrying out its responsibilities, as well as the interchange they will get, will become the considerations in disclosing carbon emissions. Thus, the hypothesis testing found insignificant results. The result of this study is in line with the researches of [9, 12, 21].

The research result finds that the PROPER rating can significantly positively affect carbon emission disclosures (sig. 0.000). This study can confirm the stakeholder theory and legitimation theory in which one of the interested parties is the government. Stakeholder pressure forces the company to fulfill the existing social contract. The existence of regulations that the government applies through PROPER rating control pushes companies to disclose carbon emissions as part of their environmental responsibility. Environmental management through the PROPER rating could support the availability of more comprehensive information. It means that the PROPER rating can push the role of increasing carbon emission disclosure to encourage an increase in the PROPER rating. It is in line with the researches of [31, 32, 36].

The results of this study indicate that the PROPER rating can mediate the effect of company size on the disclosure of carbon emissions. This study can verify the legitimacy theory regarding the equal distribution of perceptions between companies and stakeholders. The PROPER rating is a form of pressure from external parties that force large companies to disclose wider and better carbon emissions than small companies because large companies have more stakeholders and greater demands from the community. Society would pressure companies to disclose environmental responsibility with better quality and more detail [37]. Thus, it will reduce the potential for unexpected losses due to external parties. Implementing good environmental responsibility by companies will be reflected in an increased PROPER rating.

The results of this study indicate that the PROPER rating cannot mediate the effect of ROA on the disclosure of carbon emissions. This shows that stakeholder theory cannot verify the influence between variables. The researcher's assumptions indicate that there are considerations caused by the costs that must be incurred by the company. The company annually allocates finances for the disclosure of environmental responsibility and the insignificant effect on financial performance on environmental disclosures which are still voluntary. Thus, the government's pressure is only limited to the defense rating. This can be proven by the total average rating owned by the companies which amounts to 3. This means that even though financial performance increases, it will not be able to improve the performance of environmental responsibility disclosure. Another reason is that there is no clear rationale for the company's reasons for disclosing carbon emissions. So institutional factors in the form of isomorphism dominate more than rational reasons.

This study concludes that SIZE affects environmental disclosure performance (PROPER) while ROA does not affect environmental disclosure (PROPER). SIZE affects the disclosure of carbon emissions (CED), while ROA does not affect the disclosure of carbon emissions (CED). The PROPER rating variable can have a significant positive effect on the disclosure of carbon emissions. The PROPER rating variable can mediate SIZE, while the PROPER rating cannot mediate ROA. The contribution of this research is to add to the empirical research literature related to the role of PROPER ratings on the relationship between carbon emission disclosures and their constituent determinants as a novelty in this research. In addition, the research results provide support for the legitimacy of the theory. The limitation of this study is that these results indicate that stakeholder theory cannot verify the influence between variables.

The research implications are divided into practical and theoretical. The practical implication is that investors, governments, and other stakeholders can use research findings as a basis for future decision-making. For example, consider the size of the company related to the disclosure of carbon emissions and a good proper rating in choosing a place to invest for investors. The theoretical implications of the research are suggestions for further researchers to choose companies with a greater degree of relationship to the environment or include high-profile companies. Because the responsibilities and pressures from stakeholders will be greater compared to companies that are less associated with potential environmental damage. Second, the next researcher develops a research model using other proxies of financial performance not only profitability but using leverage, liquidity, solvency, and others. In addition, other mediating variables can also be used.

[1] Rokhmawati, A., Gunardi, A., Rossi, M. (2017). How powerful is your customers’ reaction to carbon performance? Linking carbon and firm financial performance. International Journal of Energy Economics and Policy, 7(6): 85-95. http://www.zbw.eu/econis-archiv/bitstream/11159/1403/1/1010646664.pdf.

[2] Wu, Y., Zhang, K., Xie, J. (2020). Bad greenwashing, good greenwashing: Corporate social responsibility and information transparency. Management Science, 66(7): 3095-3112. https://doi.org/10.1287/mnsc.2019.3340

[3] Dong, H., Xue, M., Xiao, Y., Liu, Y. (2021). Do carbon emissions impact the health of residents? Considering China’s industrialization and urbanization. Science of the Total Environment, 758: 143688. https://doi.org/10.1016/j.scitotenv.2020.143688

[4] García, F., Guijarro, F., Oliver, J. (2021). A multicriteria goal programming model for ranking universities. Mathematics, 9(5): 1-17. https://doi.org/10.3390/math9050459

[5] Kurniadi, A.P., Aimon, H., Amar, S. (2022). Analysis of green economic growth, biofuel oil consumption, fuel oil consumption and carbon emission in Asia Pacific. International Journal of Sustainable Development and Planning, 17(7): 2247-2254. https://doi.org/10.18280/ijsdp.170725

[6] Adetama, D.S., Fauzi, A., Juanda, B., Hakim, D.B. (2022). A policy framework and prediction on low carbon development in the agricultural sector in Indonesia. International Journal of Sustainable Development and Planning, 17(7): 2209-2219. https://doi.org/10.18280/ijsdp.170721

[7] Esra, N.K. (2022). Incentives for sustainability: relationship between renewable energy use and carbon emissions for Germany and Finland. Opportunity and Challenge in Sustainability, 1(1): 29-37. https://doi.org/10.56578/ocs010104

[8] Olviana, T., Nendissa, D.R., Pellokila, M.R., Lerik, M.D.C., Khoiriyah, N. (2022). Vertical Market Integration and Behavioral Variations of Medium-Quality Rice Prices Before and During Covid-19. Journal of Urban Development and Management, 1(1): 58-66. https://doi.org/10.56578/judm010107

[9] Egbunike, F.C., Emudainohwo, O.B. (2017). The role of carbon accountant in corporate carbon management systems: A Holistic approach. Indonesian Journal of Sustainability Accounting and Management, 1(2): 90. https://doi.org/10.28992/ijsam.v1i2.34

[10] Ahmadi, A., Bouri, A. (2017). The relationship between financial attributes, environmental performance and environmental disclosure: Empirical investigation on French firms listed on CAC 40. Management of Environmental Quality: An International Journal, 28(4): 490-506. https://doi.org/10.1108/MEQ-07-2015-0132

[11] Ayoib, C.A., Peter, O.N. (2015). Directors culture and environmental disclosure practice of companies in Malaysia. International Journal of Business Technopreneurship, 5(1): 99-114. https://www.researchgate.net/publication/281277014_Directors_Culture_and_Environmental_Disclosure_Practice_of_Companies_in_Malaysia.

[12] Choi, B., Lee, D., Psaros, J. (2013). An analysis of Australian company carbon emission disclosures. Pacific Accounting Review, 25(1): 58-79. https://doi.org/10.1108/01140581311318968

[13] Ching, H., Gerab, F. (2017). Social responsibility journal sustainability reports in Brazil through the lens of signaling, legitimacy and stakeholder theories. Social Responsibility Journal, 13: 95-110. https://doi.org/10.1108/SRJ-10-2015-0147

[14] Fajarini, S.W.I., Triasih, A. (2020). Determinants of the quantity of environmental disclosure in Australian companies. KnE Social Sciences, 2020: 1327-1342. https://doi.org/10.18502/kss.v4i6.6684

[15] Fernandes, S.M., Bornia, A.C., Nakamura, L.R. (2019). The influence of boards of directors on environmental disclosure. Management Decision, 57(9): 2358-2382. https://doi.org/10.1108/MD-11-2017-1084

[16] Fonta, S., D’Amico, E., Coluccia, D., Solimene, S. (2015). Does environmental performance affect companies’ environmental disclosure? https://doi.org/10.1108/MBE-04-2015-0019

[17] Giannarakis, G., Konteos, G., Sariannidis, N., Chaitidis, G. (2017). The relation between voluntary carbon disclosure and environmental performance: The case of S&P 500. International Journal of Law and Management, 59(6): 784-803. https://doi.org/10.1108/IJLMA-05-2016-0049

[18] Kalu, J.U., Buang, A., Aliagha, G.U. (2016). Determinants of voluntary carbon disclosure in the corporate real estate sector of Malaysia. Journal of Environmental Management, 182: 519-524. https://doi.org/10.1016/j.jenvman.2016.08.011

[19] Liu, Y.S., Yang, J.H. (2018). A longitudinal analysis of corporate greenhouse gas disclosure strategy. Corporate Governance (Bingley), 18(2): 317-330. https://doi.org/10.1108/CG-11-2016-0213

[20] Monteiro, S.M.S., Aibar-Guzmán, B. (2010). Determinants of environmental disclosure in the annual reports of large companies operating in Portugal. Corporate Social Responsibility and Environmental Management, 17(4): 185-204. https://doi.org/10.1002/csr.197

[21] Uyar, A., Karaman, A.S., Kilic, M. (2020). Is corporate social responsibility reporting a tool of signaling or greenwashing? Evidence from the worldwide logistics sector. Journal of Cleaner Production, 253: 119997. https://doi.org/10.1016/j.jclepro.2020.119997

[22] Gatimbu, K.K., Wabwire, M.J. (2016). Effect of corporate environmental disclosure on financial performance of firms listed at Nairobi securities exchange. Kenya. International Journal of Sustainability Management and Information Technologies, 2(1): 1-6. https://doi.org/10.11648/j.ijsmit.20160201.11

[23] Deegan, C. (2002). Introduction: The legitimising effect of social and environmental disclosures – a theoretical foundation. Accounting, Auditing & Accountability Journal, 15(3): 282-311. https://doi.org/10.1108/09513570210435852

[24] Dowling, J., Pfeffer, J. (1975). Organizational legitimacy: Social values and organizational behavior. Pacific Sociological Review, 18: 122-136. https://doi.org/10.2307/1388226

[25] Freeman, R.E. (2004). The stakeholder approach revisited. Zeitschrift Für Wirtschafts - Und Unternehmensethik, 5(3): 228-241. https://doi.org/10.5771/1439-880x-2004-3-228

[26] Dibia, N.O., Onwuchekwa, J.C. (2015). Determinants of environmental disclosures in Nigeria: A case study of oil and gas companies. International Journal of Finance and Accounting, 4(3): 145-152. https://doi.org/10.5923/j.ijfa.20150403.01

[27] Ohidoa, T., Omokhudu, O.O., Oserogho, I.A.F. (2016). Determinants of environmental disclosure. International Journal of Advanced Academic Research | Social & Management Sciences, 2(8): 2488-9849. https://www.ijaar.org/articles/Volume2- Number8/Social-Management-Sciences/ijaar-sms-v2n8- aug16-p1.pdf.

[28] Modugu, K., EBOIGBE, S.U. (2017). Corporate attributes and corporate disclosure level of listed companies in Nigeria: A post-IFRS adoption study. Journal of Finance and Accounting, 5(2): 44-52. https://doi.org/10.12691/jfa-5-2-3

[29] van de Burgwal, D., Vieira, R.J.O. (2014). Environmental disclosure determinants in Dutch listed companies. Revista Contabilidade & Finanças - USP, 25(64): 60-78. https://www.scielo.br/j/rcf/a/sYqkPMpzyP3g8DDTCC4 BCtz/?format=pdf&lang=en.

[30] Gray, R., Kouhy, R., Lavers, S. (1995). Corporate social and environmental reporting A review of the literature and a longitudinal study of UK disclosure. Accounting, Auditing & Accountability Journal, 8(2): 47-77. https://doi.org/10.1108/09513579510146996

[31] Al-Tuwaijri, S.A., Christensen, T.E., Hughes, K.E. (2005). The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.405643

[32] Dawkins, C., Fraas, J.W. (2011). Coming clean: The impact of environmental performance and visibility on corporate climate change disclosure. Journal of Business Ethics, 100(2): 303-322. https://doi.org/10.1007/s10551- 010-0681-0

[33] Berzosa, A., Bernaldo, M.O., Fernández -Sanchez, G. (2017). Sustainability assessment tools for higher education: An empirical comparative analysis. Journal of Cleaner Production, 161: 812-820. https://doi.org/10.1016/j.jclepro.2017.05.194

[34] Uyar, A., Karaman, A.S., Kilic, M. (2021). Institutional drivers of sustainability reporting in the global tourism industry. Tourism Economics, 27(1): 105-128. https://doi.org/10.1177/1354816619886250

[35] Liu, C.N., Cheng, Y. (2011). Global university rankings and their impact. In Leadership for World-Class Universities: Challenges for Developing Countries. https://doi.org/10.4324/9780203842171

[36] Croucher, G., Woelert, P. (2016). Institutional isomorphism and the creation of the unified national system of higher education in Australia: an empirical analysis. Higher Education, 71: 439-453. https://doi.org/10.1007/s10734-015-9914-6

[37] Ching, H.Y., Gerab, F. (2017). Sustainability reports in Brazil through the lens of signaling, legitimacy and stakeholder theories. Social Responsibility Journal, 13(1): 95-110. https://doi.org/10.1108/SRJ-10-2015-0147