Muhammad Yasir Yusuf* | Rahmat Fadhil | Teuku Saiful Bahri | Hafizh Maulana | Juli Firmansyah

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The agricultural sector is a role model that can be the basis for policymakers to integrate Islamic insurance patterns in agriculture. This research aims to design a model of the Islamic agricultural insurance system based on Islamic law in the context of Indonesia. This study is expected to contribute for Indonesian government to accommodate the implementation of the Islamic agricultural insurance system and pattern in Indonesia. This study used an expert system approach through data collection and information as a reference in the formulation of model designs, including interviews, questionnaires, direct observation, and data synthesis in the field. This research stage used a systems development conceptual model described in the research process, including planning, analysis, design, verification, validation, and building models. The research hypothesis is confirmed that Islamic agricultural insurance can be implemented based on risk and investment with tabarru’ funds (mutual financial aid funds) and investment funds. Islamic agricultural insurance is a way out for farmers, especially Muslim farmers, in ensuring agriculture management by managing the level of risk due to crop failure. Islamic agricultural insurance systems can guarantee risks that arise in agricultural businesses to provide inner peace to farmers in getting the good and right protection for businesses that run following Islamic principles. This research has resulted in innovative features and development models of Islamic agricultural insurance for the Protection and Empowerment of Farmers in Indonesia.

Islamic agricultural insurance, farmers, tabarru’, systems development conceptual model, risk

Business in the agricultural sector always faces a very high risk of uncertainty, for example, crop failures due to pests and diseases or plant-disturbing organisms, changes in environmental conditions such as climate change, drought, floods and so on [1-4]. Allowing farmers themselves to face this risk would be very unfortunate for food security and independence for an area. Even regions that often face this risk will continue to experience endless food insecurity.

For this reason, the Ministry of Agriculture of the Republic of Indonesia has rolled out an agricultural insurance program since 2015 through the Minister of Agriculture Regulation No. 40/Permentan/SR.230/7/2015 concerning Agricultural Insurance Facilities. This regulation of the Minister of Agriculture is a form of technical and operational explanation of the order of the law of the Republic of Indonesia No. 19 of 2013 concerning Protection and Empowerment of Farmers, which in article 37 paragraph (1) states "the central government and regional governments by their authorities are obliged to protect farming conducted by farmers in the form of agricultural insurance."

The idea of agricultural insurance programs in Indonesia has been carried out since the 80s (1982, 1984, 1985) by establishing a working group on harvest insurance development. However, according to Sumaryanto and Nurmanaf [5], in 1999, the development of agricultural insurance had been carried out but was still in the preparation stage, which required various instruments for its implementation. In 2011 the agricultural insurance working group was formed to formulate the Rice Farming Business Insurance (Asuransi Usaha Tani Padi (AUTP)) and Cattle/Buffalo Business Insurance (Asuransi Usaha Ternak Sapi/Kerbau (AUTS/K)). Finally, in 2015, agricultural insurance was implemented in Indonesia through two main programs, namely AUTP and then AUTS/K in 2016.

The implementation of AUTP was first pilot project in 16 provinces in 2015 with a target of 1,000,000 hectares. The implementation of pilot project began in October to December 2015 with the realization of 233,499.55 hectares or 23.35% [6]. Based on this insignificant realization target, in 2016 the AUTP target was reduced to 500 000 hectares with the realization of 499 962 hectares, and claims reached 11 107 ha.

In 2017 the target will be increased again to 1 million hectares, along with various strategies and innovations, so that 997 961 hectares will be realized with a claim of 25 028 hectares. In 2018, the target was still maintained at 1 million hectares and realized 806 199 hectares with claims of 10 754 hectares.

The Agricultural Insurance Program is targeted to be able to reach a land area of 6.5 million hectares during 2015-2019. In fact, realization until 2019 has only reached a total land area of 2.9 million hectares or 45% of the planned target [7]. The need for insurance programs hasn’t become a priority scale for farmers in farming activities, so that in its implementation it has not been achieved evenly in each region.

The low target for the implementation of AUTP during 2015-2016 based on a thematic study with a SWOT analysis [8], was due to the weak support for payment of contributions with the Regional Government. Budget (locally called APBD) and low literacy level of farmers in utilizing agricultural insurance programs.

Meanwhile for AUTS/K, the realization until 2019 tends to be more optimal. The realization of the number of cattle from 2016-2019 was 314,202 cows, or 82% of the target [6]. For AUTS/K since the program began in 2016, it is targeted to reach 120 thousand heads of cattle, but only 20 thousand heads have been realized with 697 claims. In 2017 the target is still the same at 120 thousand and the realization has increased to reach 92 176, with 3 470 claims. For the year 2018, still, with the same target of 120 thousand heads, and 88 673 heads have been successfully realized with claims reaching 1 736 heads.

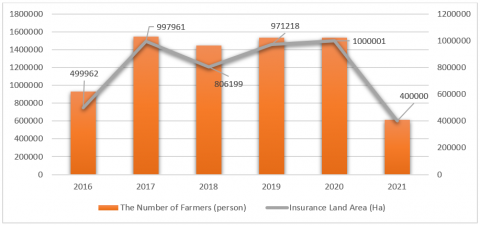

Agricultural insurance land area (AUTP) on average during 2016-2021 grew by 96.26%. However, during the Covid-19 Pandemic, the AUTP Program experienced a decrease in its target land area of 600 000 hectares. The following is a report on the number of farmers and insurance land area sourced from the Director-General of Agriculture Infrastructure and Facilities of the Ministry of Agriculture.

Figure 1. Number of farmers participating in insurance and insurance land area

Based on Figure 1 Number of farmers participating in insurance and insurance land area from Directorate of Agricultural Finance [6], the average area of agricultural land insured by farmers is 0.61 hectares. In 2018, the AUTP Program experienced a decrease in the realization of 19.18%. The decrease in the number of farmers and the area of AUTP land will occur significantly in 2021.

The decrease in the realization of AUTP from the observations found that the number of field officers in most locations was considered to be still lacking compared to the area of rice fields registered with insurance. This causes information and assistance to farmers to be less than optimal, especially in assessing damage during crop failure. On the other hand, the budget for the implementation of agricultural insurance is still inadequate, especially for locations with a large area of registered rice fields, financing for the recruitment of field officers and insurance premium financing assistance for farmers

In addition, there are some weaknesses in the implementation of agricultural insurance in Indonesia. First, field socialization is felt to be still not very massive, especially to understand farmers about the benefits, procedures, and benefits of this agricultural insurance program [9-13]. Even though the government, in coordination with related institutions at the district/city level, has programmed several agendas for the socialization of agricultural insurance throughout the year, including providing a special budget allocation for a separate agricultural insurance socialization program. But the involvement of parties outside government institutions seems to be programmed in an integrated and continuous way. The socialization process can lead to local community interaction which can build a social connectivity and intense agricultural innovation [14].

Second, the issue of halal-haram (lawful-forbidden) agricultural insurance systems developed at this time. Indonesian society which is religious and sensitive with halal-haram practices based on Islamic principles causes this agricultural insurance program to be a separate question. Some people are not willing to take part in the agricultural insurance program because it contradicts their beliefs which are not in accordance with Islamic law. For this reason, the Islamic agricultural insurance system model needs to be formulated conceptually.

Based on the study with soft system methodology [15], there is a moral hazard that philosophically occurs in the practice of agricultural insurance with concept transfer of risk of farming land. The action of change with the Islamic agricultural insurance system changes the concept of transfer risk to become sharing of risk between farmers and the insurance institution in the management of tabarru’ funds.

The agricultural sector is necessary managed effectively because it plays a key role to fulfill the supply of foodstuff and raw material [16]. The main contribution of this research is to offer a conceptual framework for Islamic agricultural insurance governance, with a systems development conceptual model. This study aims to design an Islamic agricultural insurance system model based on Islamic law in the Indonesian context. The expert system approach in the formulation of this model is expected to provide some critical perspectives to sharpen the results and formulation of the initial concept. In the end, of course, the resulting model can be more applicable in the practice of agricultural insurance development in Indonesia from an Islamic perspective.

2.1 Agricultural insurance in other countries

The current system of crop insurance in the United States was established in 1938. The most often insured crops are corn, soybeans, and wheat, about 80% of the total area, is insured. In some countries (e.g., the USA and Canada), crop insurance and, to a smaller extent, livestock insurance is the primary public policy mechanism for reducing. Farmer's exposure to yield and/or revenue risk [17]. The total value of premiums in 2008/09 was almost $ 10 billion. The insurance coverage is 50% of the average yield and 55% of the expected crop prices in the basic CAT (Catastrophic) program. This basic coverage is fully subsidized by the state [18].

One form of agricultural insurance currently being developed is weather-index insurance (weather index insurance-AIC), developed by the International Finance Corporation (IFC). This type of insurance has been applied in several countries such as Thailand, India, Mexico, Kenya, and Malawi. It is still under-represented in insurance coverage in developing countries, even though the agricultural sector in developing countries is relatively large compared to manufacturing and services [19].

In the European Union, individual states use very different systems of agricultural insurance. The diversity of approaches and institutional arrangements to agricultural risk management is given by the heterogeneity of risks that threaten Europe's farmers. In general, the higher risk of crop damage occurs in southern European countries, with particularly high risks of drought and other significant effects of extreme weather events. Hail plays an essential role in the Central European countries, and concerning climate change, more frequent occurrences of drought and local torrential rains are predicted [18].

Fact, implementing agricultural insurance led to a variety of schemes in any other Countries. The agricultural insurance system in France was developed more than forty years ago under state supervision [20]. Agricultural insurance in France has grown since the 2004 reforms, where more than 60% of the agricultural area is insured. In another case in Germany, more than 80% of agricultural areas are insured [21]. Agricultural insurance in Latin America is relatively developed compared to other regions such as Africa and many Asian countries. Agricultural insurance in Latin America has grown in recent years, but agricultural insurance is not distributed evenly between countries in Latin America. The supply of agricultural insurance products in this region is relatively increasing compared to other regions based on the number of insurance companies [22].

2.2 Islamic agricultural insurance

Research on the design of Islamic agricultural insurance doesn’t aim to contradict Western or conventional insurance concepts running in the world. Accessibility of conventional insurance products in Muslim majority countries became questionable in the eyes of Islamic due to the prohibited elements of Riba (interest), Gharar (uncertainty), and Maisir (gambling) in insurance transactions [23]. Islamic insurance is an alternative and has different concepts from conventional insurance based on the idea of business philosophy, social solidarity, cooperation, Surplus underwriting, and joint compensation for member losses.

Farming systems are seen as holistic systems managed by farmers by implementing the best management practices to maximize the benefits or minimize the risks of farming [24]. In order to minimize risk, Agricultural insurance is one form of disaster mitigation against crop failure by transferring or sharing risks in farming activities concerning farmer protection. The function is an effort to stabilize the level of income of farmers by reducing the level of loss experienced by farmers due to loss of yield so that farmers feel safe in farming [25]. So, agricultural insurance is an effort by the government to improve the skills and management of agriculture/livestock in reducing the dependence of farmers from other party financiers (creditors) who are sometimes even troublesome, including to help farmers by providing support for production costs or business capital after disasters. This effort is very important in maintaining the availability of food resources for the community in the long run.

Islamic agricultural insurance was initiated to develop the model of Rice Farming Business Insurance (AUTP) and Cattle/Buffalo Business Insurance (AUTS/K) in Indonesia. The implementation of agricultural insurance aims to protect, mitigate risk, and awareness of risks that threaten agricultural or agricultural activities. Islamic agricultural insurance system seeks to develop insurance management based on the principles of mutual risk sharing and mutual support through enhanced society links according to Islamic concept [23]. In addition, the developed Islamic agricultural insurance will build a farm protection scheme by providing opportunities for business expansion with a model investment scheme through Islamic financing.

As the Comparison, we will review the implementation of agricultural insurance and a new design of Islamic agricultural insurance (Table 1).

Table 1. Review of the implementation of agricultural insurance and Islamic agricultural insurance

|

Comparative Description |

Agricultural Insurance |

Islamic Agricultural Insurance |

Source |

|

Business Philosophy |

Transfer of Risk |

Sharing of Risk |

[26] |

|

Farmer Protection |

Protected farmers from harvest failure as the scheme is risked shifting that guarantee farmers to obtain compensation due to a loss. |

Protect farmer's systems based on mutual protection. Farming protection would be morally and rationally irrefutable |

[15, 27, 28] |

|

Concepts |

conventional insurance is based on taking material gain on behalf of others. The operational framework of conventional insurance is based on risk assumption |

Islamic Insurance operation is based on the concepts of taawun (mutual help or cooperation), solidarity, trusteeship, and brotherhood |

[23, 29] |

|

Guarantee risk |

The agricultural insurance scheme is based on indemnity of the rice production cost. |

Islamic agricultural protection system which involves a joint guarantee scheme in providing possible indemnity or contingency cost |

[29, 30] |

|

Implementation |

The implementation of AUTP and AUTS/K are intended to protect farmers in carrying out the business of rice and livestock farmers, providing working capital assistance with insurance claim mechanisms |

Islamic Agricultural insurance is designed to cushion farmers against loss of crops and livestock due to adverse weather or financial loss due to price volatility. |

[28, 31, 32] |

|

Surplus underwriting |

Surplus underwriting is the right of the insurance company as a claim reserve. |

Surplus underwriting becomes the rights of participating farmers which will be managed through investment in the mudharabah and wakalah schemes. |

[26, 33] |

Islamic insurance is an effort to protect each other and help one of several people/parties through investment in assets and/or tabarru' (mutual financial aid) that provides a pattern of return to face certain risks through a contract (agreement) by Islam. So, the basic principle in Islamic insurance is not transferring risk as practiced in conventional insurance, but instead sharing the risk of fellow insurance participants [22, 34-36]. Tabarru' (seeking blessing) is an agreement that is a transaction that is not intended to obtain profit/non-profit transactions (non-profit oriented) [37-39]. This transaction aims to help do good (tabarru' comes from the word birr in Arabic, which means goodness).

This research used an expert system approach, which collects critical data and information in the formulation of model design through interviews, questionnaires, direct observation, and synthesis of data in the field. Experts who are competent to provide ideas and thoughts have expertise based on formal education (bachelor) in the field studied, based on experience and work history, and practitioners in fields related to agricultural insurance and Islamic economics. The experts selected in this study were 9 people consisting of the National Sharia Board-Indonesian Ulema Council (Dewan Syariah Nasional-Majelis Ulama Indonesia (DSN-MUI)), the Ministry of Agriculture of the Republic of Indonesia, Indonesian Center for Agriculture Social Economic and Policy Studies (Pusat Sosial Ekonomi dan Kebijakan Pertanian (PSEKP)), PT. JASINDO (Indonesian insurance services), lecturer at Universitas Syiah Kuala, lecturer in Universitas Islam Negeri Ar-Raniry, Aceh Ulema Consultative Council (Majelis Permusyawaratan Ulama Aceh), agricultural insurance researcher and insurance practitioner.

An expert system approach can be developed in the model's interactive dialogue process through the process of condensation, data presentation, and drawing conclusions or verification [40]. Decision-making systems with an expert approach are also commonly carried out using the fuzzy multi-criteria decision analysis (MCDA) methodology on agri-food companies [41].

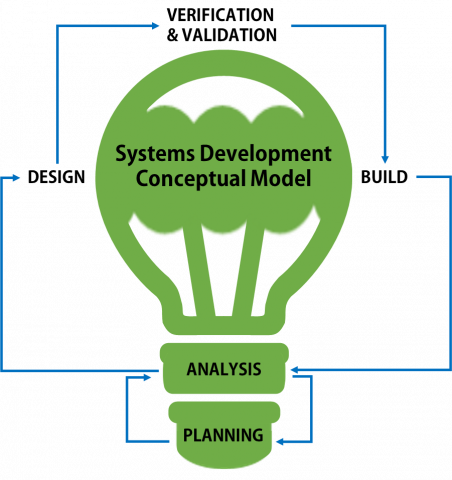

In formulating expert opinions, this study used a conceptual model development system as shown in Figure 2. This system is a development of Soft Systems Methodology (SSM) [42-46] and System Development Life Cycle (SDLC) [47-50].

Figure 2. Systems development conceptual model

The system development conceptual model is built with structured stages with an expert system approach. Based on Figure 3, the interpretation procedure for each system is carried out which includes Planning, Analysis, Design, Verification, and Validation to build the design of the Islamic agricultural insurance model framework. The planning stage is an important element for the formulation of problems and research objectives in Indonesia. It also studies the existing issues and challenges that can be resolved in the future.

The participation rate of farmers in conventional agricultural insurance programs is still low and is only concentrated in Java Regions [7]. On the other hand, endemic areas with a high level of risk need to get mitigation protection through insurance products. The design of sharia agricultural insurance is considered necessary to provide opportunities for the development of Islamic financial product features that are developing in Indonesia, especially the dominance of Muslim farmers. Another perspective to create the paradigm of agricultural development that is free from moral hazard behaviour is established through Indonesian farmers’ local wisdom, which mostly is a community of Muslim farmers [15].

The analysis phase reviews various policies and collects references and expert consultations to obtain various studies, studies, policies, and views before designing the system to be implemented, namely the pattern of Islamic agricultural insurance. Islamic agricultural insurance policies with the concept of mutual help have the wisdom values of Indonesian Muslim farmers can prevent moral hazard behavior.

Islamic financing policies through the Sharia Farmer Business Credit (locally called KUR-TANI) program have been implemented in based on regulatory and institutional manner. This arrangement refers to the Regulation of the Minister of Agriculture Number 12/2020 concerning KUR-TANI Facilities and the Regulation of the Coordinating Ministry for Economic Affairs Number 1/2022 concerning Guidelines for the Implementation of KUR. Regulations and policies can be strengthened in an integrated manner with the development of Islamic Agricultural financing with profit sharing schemes, working capital, and financing guarantee institutions.

The Islamic agricultural insurance system is designed based on financial features consisting of risk based Islamic Agriculture insurance and Risk and investment based Islamic agricultural insurance. The results of the draft model refer to the Regulation of the Coordinating Ministry for Economic Affairs, the Minister of Agriculture, The Financial Services Authority (locally called OJK) and the Fatwa of the National Sharia Council of the Indonesian Ulema Council.

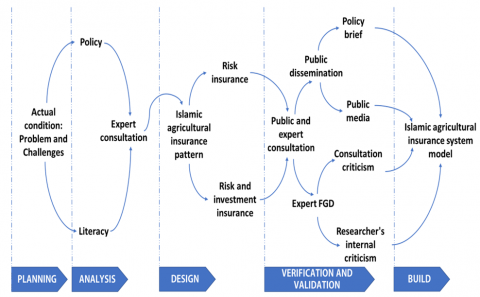

The fourth stage is the process of verification and validation of various steps that have been formulated through public and expert consultation. This activity includes public dissemination through policy briefs and public media, then using expert Focus Group Discussion (FGD) in the form of consultation critics and internal criticisms of researchers. The final stage is to formulate a model of the Islamic agricultural insurance system as a whole, and these steps are shown in Figure 3.

The concept of managing Islamic agricultural insurance funds is one model to provide loss protection to farmers that will encourage the growth of national economic income and also create jobs for people who need capital in agriculture [51]. Islamic agricultural insurance based on gathering expert opinion through public dissemination (policy briefs and public media) and expert focus group discussions (FGD) (consultation critics and internal research critics) obtained two management models, namely Risk insurance and Risk insurance with investment. This means that the existence of the Islamic agricultural insurance model will open space for Islamic financial institutions to provide capital in agriculture because its form is risk mitigation in agriculture.

Figure 3. Research thinking framework

The Islamic agricultural insurance fund management system can be carried out in two forms, namely: risk insurance and risk and investment insurance.

Risk-Based Islamic Agricultural Insurance. The risk-based insurance pattern is a form of insurance management in agriculture that purely uses a tabarru' contract (a contract of mutual assistance), where premium contributions are only devoted to the social interests of farmer/livestock groups affected by disasters or land and livestock losses. Tabarru' contract is a contract or transaction that contains an agreement with the aim of helping each other without any conditions of reward from the other party. All premiums are earmarked for a collection of grants for fellow farmers, which will be used if farmers experience losses or crop failures. Risk-based sharia agricultural insurance is limited to risk mitigation activities from the collection of farmer and rancher contributions collected in the tabarru' fund investment account.

Risk and investment based Islamic agricultural insurance. Risk and Investment-based agricultural insurance is a form of agricultural insurance management which consists of tabarru' funds (mutual financial aid funds) and investment funds. In the Risk and Investment insurance management pattern, premium contributions will be entered into a tabarru' account and an investment account. Investment accounts are carried out separately for later use in agricultural investment activities with contracts and profit-sharing schemes between farmers and insurance companies. The existence of investment profits through underwriting surplus can provide added value for farmers and insurance companies.

4.1 Risk-based Islamic agriculture insurance

A risk-based insurance pattern is one form of insurance management in agriculture that purely uses a tabarru’ contract (contract for mutual financial aid). Tabarru’ contract is a contract or transaction that contains an agreement to help without any conditions for compensation from other parties [52, 53]. Premium contributions are only devoted to the social interests of members affected by disaster or loss. All premiums are intended to collect grants for fellow farmers, which will be used if among the farmers' experience loss or crop failure. The risk insurance management scheme can be seen in Figure 4.

Figure 4. Risk-based Islamic agriculture insurance pattern

The contribution of premiums to agricultural insurance not only comes from farmers, but the government also contributes to the gift of premiums insurance. This is an implementation of the Law of the Republic of Indonesia No. 19 of 2013 concerning the Protection and Empowerment of Farmers and in more detail explained through Regulation of the Minister of Agriculture of the Republic of Indonesia No. 40 of 2015 related to agricultural insurance facilities, one of which regulates premiums paid with the State Budget (APBN/central government) and/or Regional Budget (APBD/local government).

The premium sources are divided into two models. First, the basis of premiums comes from the 80% central government; 20% of local governments and farmers are exempted from the obligation to pay premiums. This model is the ideal model that shows the alignments of the government (central and regional) to develop agriculture in Indonesia. Second, the source of premiums is sharing between the government and farmers, 80% of the tabarru’ premium (mutual financial aid) from the government and 20% of the tabarru’ premium from farmers. Tabarru’ premiums from the government can be obtained from the central government and/or local governments. All insurance premiums will be collected in a tabarru’ account, which the insurance company will then invest by Islamic principles. Insurance companies can take wages (ujrah) based on the management of tabarru’ fund's insurance customers with the provision of tabarru’ fund's bookkeeping must be separate from other funds. The investment proceeds from tabarru’ funds must be the collective right of participants by recording on tabarru' accounts (joint financial assistance).

Regarding investment returns, insurance companies can obtain profit sharing based on mudharabah or mudharabah musytarakah contract, or obtain ujrah (fees) based on wakalah bil ujrah contracts (contract with agency fees). The arrangement of wakalah bil ujrah transfers power by one person as the first party to another person as the second party in the matters represented. The second party (the representative of the first party) only carries out something limited to the power or authority is given by the first party by getting the reward from what has been done. But if the power has been carried out as required, then all risks and responsibilities for implementing the order are fully charged to the first party or the grantor [53-56]. In the management of tabarru’ funds with profit-sharing agreements (mudharabah/musytarakah) that give power to the company as mudharib (a trusted party) to manage the investment of tabarru’ fund's participants according to their authority or authority. In return, the company will be given a profit-sharing (ratio) the amount agreed upon previously; for example, 80% returned to the investment account and 20% to the company's profit (Figure 5).

Figure 5. Investment account of Islamic agricultural insurance

Mudharabah's contract is a form of cooperation between two or more parties. The owner of capital (shahibul amal) entrusts a certain amount of money to the manager/company (mudharib) with an agreement initially. This form confirms cooperation with the contribution of one hundred percent capital from the owner of capital and expertise from the manager. While mudharabah musytarakah contracts where the fund owners consist of many people who provide funds to be developed by second parties (companies/banks) in sectors considered profitable, sometimes specific sectors [57, 58]. The fund owners permit the manager to combine their funds into one, including the manager's funds. Furthermore, the manager gives permission to the fund owners to withdraw all their funds or part of them based on certain conditions.

As for the management of tabarru’ funds using a wakalah bil ujrah contract (wakalah fees or agency fees), namely by giving power of attorney to the company as a participant representative to manage tabarru' (mutual financial aid) and/or participant investment funds, according to the power or authority given with rewards in the form of ujrah (fees). According to the fatwa (religious decree) of the National Sharia Board-Indonesian Ulema Council No.52/DSN-MUI/III/2006 concerning wakalah bil ujrah contract on Islamic insurance, wakalah contract (agency contract) is trustful (yad amanah) and not dependent (yad dhaman), so that the representative does not bear the risk of investment losses by reducing the fee has been received, except due to carelessness or default. Insurance companies as representatives do not have the right to share the investment return because the contract used is a wakalah contract. The pattern of implementation can be seen in Figure 6.

Suppose there is a surplus underwriting of tabarru’ funds, according to the religious decree of the National Sharia Board-Indonesian Ulema Council No.53/DSN-MUI/III/2006. In that case, some alternatives may be made as follows:

The choice of one of the alternatives above must be approved in advance by the participant and set forth in the contract. The underwriting surplus is the difference between the total contributions of participants in tabarru’ funds plus the increase in reinsurance assets after deducting payment of compensation/claims, reinsurance contributions, and increase in technical reserves in a certain period [59]. Related to the Islamic insurance pattern (risk), the management of surplus underwriting uses a third alternative, in which the surplus funds can be saved in part as a reserve fund of as much as 20% and can be shared in other parts by insurance companies as much as 50% and participants 30%, as long as agreed by the participants. Conversely, if there is an underwriting deficit or a difference in tabarru’ funds, then the insurance company is obliged to overcome the shortage in the form of qardh (loan). Qardh refunds to insurance companies are set aside from tabarru’ funds.

Figure 6. The Management of Islamic agricultural insurance with Risk and Investment insurance

4.2 Risk and investment based Islamic agricultural insurance

Risk and investment-based Islamic agricultural insurance is one form of agricultural insurance management consisting of tabarru’ funds (mutual financial aid funds) and investment funds (Figure 6). Suppose the agricultural insurance with a risk pattern is only intended for tabarru’ funds, then in the risk and investment insurance management pattern. In that case, premium contributions will be entered into two accounts: the tabarru’ and investment accounts (saving accounts). The contribution of Risk and Investment insurance premiums consisting of tabarru’ funds and investment funds, the pattern of funding sources can also be divided into two models.

First, the source of premium tabarru’ from the government and investment from farmers. Tabarru’ funds 80% from the Central Government / Regional Government and 20% investment funds from farmers. Second, the source of the premium tabarru’ is sharing between the government and farmers in the form of a premium tabbaru’ source (mutual financial aid premium) from the government of 80% and Farmers 20%, plus farmers provide another 20% additional cost as an investment fund for themselves in the future will come in the form of a savings account. Therefore the total percentage of funds collected is 120%.

Tabarru’ funds (mutual financial aid funds) are managed and invested by companies to be used when disasters occur. The funds are used as grants with fellow farmers to be used (paid to farmers) when the harvest fails. Investment returns from Tabarru’ funds can be shared between the company and the farmers following the initial agreement if surplus underwriting occurs. Companies can benefit from mudharabah or mudharabah musytarakah patterns.

The investment returns from investors' funds in investment accounts between companies and farmers use the wakalah bil ujrah (agency fees) pattern where companies can get service fees from investment management of investor funds, which are taken from profits handed over to investors in accordance with the agreement. As a product to provide support for sustainable farming and at the same time as an alternative funding scheme relating to transferring or sharing risk (transfer or distribution of risk) in farming activities. Agricultural insurance has several benefits for farmers, among others. First, they provide awareness to farmers of the risk of crop failure or failure of livestock business [3, 60, 61]. Second, encouraging farmers to improve their skills and improve management of farming/livestock businesses [62, 63]. Third, reducing the dependence of farmers on other parties' financiers which sometimes makes it difficult and helps farmers to be able to provide production costs or livestock business capital after a disaster [64, 65]; and Fourth, increasing farmers' income from the success of farming and livestock businesses on an ongoing basis [66].

Islamic-based agricultural insurance is a way out for Muslim farming communities in ensuring agricultural management by managing the level of risk that can occur due to crop failure. There are two models of Islamic agricultural insurance management, namely risk-based insurance and risk-based insurance with investment. The pattern of Islamic insurance based on the risk of insurance is one form of insurance management in agriculture that purely uses a tabarru' contract (mutual financial aid contract), where the source of funds can be obtained from two models. First, the premium tabarru' comes from the government, in the form of tabarru' funds (mutual financial aid funds) 80% (central government) and 20% (local governments). This means that the tabarru' funds (mutual financial aid funds) are 100% government grants. Second, the premium tabarru’ is obtained from sharing between the government (80%) and farmers (20%).

Furthermore, for the Islamic-based insurance model for risk-based investment, the contribution of each party's premium (government and farmers) will be entered into two accounts, namely tabarru' (social) and investment (saving) accounts. Insurance companies (mudharib) can take advantage of the management of tabarru’ funds in return for their services if they use a wakalah bil ujrah contract (wakalah fees or agency fees) but are not entitled to obtain investment returns. There are two models of risk-based and investment-based Islamic insurance funds. First, the source of premium tabarru' (mutual financial aid premiums) from the government and investment from farmers. Tabarru’ funds 80% from central/local government) and 20% investment funds from farmers. Second, the source of premium tabarru' (mutual financial aid premium) sharing between the government and farmers in the form of premium tabarru’ sources (mutual financial aid premium) from the government 80% and farmers 20%, plus farmers provide another 20% additional cost as investment funds for himself in the future in the form of a savings account.

The existence of Islamic-based agricultural insurance is a must for achieving one of the government's goals to defend and encourage farmers to be more confident in the government's alignments for farmers. The pattern of Islamic agriculture insurance guarantees risks that can arise in agriculture within the sharia frame to provide inner peace to farmers who want their agricultural land to get good and correct protection based on Islamic principles.

This research is limited to the concept and model framework offered for the development of Islamic agricultural insurance policies in Indonesia. The next analysis that must be deepened is the actuarial calculation of the features of Islamic agricultural insurance financial products that accommodate aspects of risk management, company profits, and willingness of farmers to pay Islamic agricultural insurance premiums.

The authors thank the Aceh Regional Secretary Economic Bureau, the Regional Development Planning Board (BAPPEDA) Aceh and Lembaga Pengelola Dana Pendidikan (LPDP), Riset Inovatif Produktif (RISPRO) Tata Kelola/Kebijakan, the Ministry of Finance of the Republic of Indonesia.

[1] FAO (Food and Agriculture Organization). (2011). Agricultural Insurance in Asia and the Pacific Region. RAP Publication 2011/12. FAO. Bangkok. http://www.fao.org/3/i2344e/i2344e00.htm, accessed on May 20, 2019.

[2] Boer, R. (2012). Climate insurance as guarantees protection of farmers' resilience to climate change. Bogor: Centre for Climate Risk and Opportunity Management in Southeast Asia and Pacific Bogor Agricultural University (CCROM SEAP-IPB).

[3] Jiuhardi, J., Hasid, Z., Darma, S., & Darma, D. C. (2022). Sustaining Agricultural Growth: Traps of Socio–Demographics in Emerging Markets. Opportunities and Challenges in Sustainability, 1(1): 13-28. https://doi.org/10.56578/ocs010103.

[4] Pasaribu, S.M. (2010). Developing rice farm insurance in Indonesia. Agriculture and Agricultural Science Procedia, 1: 33-41. https://doi.org/10.1016/j.aaspro.2010.09.005

[5] Sumaryanto, S., Nurmanaf, A.R. (2007). Strategic development of agricultural insurance on rice farming in Indonesia. Forum Penelitian Agro Ekonomi, 25(2): 89-103. http://dx.doi.org/10.21082/fae.v25n2.2007.89-103

[6] Directorate General of Agricultural Infrastructure and Facilities, Ministry of the Agriculture Republic of Indonesia. (2021). Performance report 2021. Jakarta: Center for Agricultural Data and Information System, https://www.pertanian.go.id/home/index.php?show=repo&fileNum=553, accessed on May 20, 2022.

[7] Directorate of Agricultural Financing. (2016). Strategic plan of the directorate of agricultural financing for 2015-2019. Jakarta: Center for Agricultural Data and Information System. http://sakip.pertanian.go.id/admin/file/RENSTRA%20DIT.PEMBIAYAAN%202015-2019%20REVISI%202.pdf, accessed on Sept. 18, 2022.

[8] Directorate General of Budget Financing and Risk Management. (2016). Thematic study of the directorate of budget for the economic and maritime sector 2016. Jakarta: Ministry of Finance ff The Republic of Indonesia, https://anggaran.kemenkeu.go.id/api/Medias/b2e27e2b-7d8d-43c5-8cd6-9cf741640d78, accessed on Sept. 18, 2022.

[9] Wahyudi, I. (2015). Rice farm insurance trial scheme and factors related to farmer participation in AUTP program. Undergraduate Thesis, Bogor (ID): Institut Pertanian Bogor (in Indonesia). https://repository.ipb.ac.id/handle/123456789/77549.

[10] Kawanishi, M., Guritno, C.S., Farid, F.Y. (2016). Assessment of farmer demand for crop insurance: a case study in Indonesia. Japanese Journal of Risk Analysis, 26(1). 31-39. https://doi.org/10.11447/sraj.26.31

[11] Siswadi, B., Syakir, F. (2016). Farmers response to government programs regarding rice farming insurance (AUTP). Semarang: Prosiding Seminar Nasional Pembangunan Pertanian 2016, Fakultas Pertanian Universitas Brawijaya. https://fp.ub.ac.id/semnas/Paper/29_asuransi_padi-bambang_siswadi_(169-177).pdf.

[12] Sayugyaningsih, I. (2018). The Factors that affecting the farmers in Joining Rice Farm Insurance (AUTP) in Kaliori Sub-district, Rembang. Undergraduate Thesis, Bogor: Departemen Agribisnis Fakultas Ekonomi dan Manajemen, Institut Pertanian Bogor. https://repository.ipb.ac.id/handle/123456789/94675.

[13] Yusuf, M.Y., Fadhil, R., Bahri, T.S., Maulana, H. (2021). Comparison study of agricultural insurance government subsidy and farmers’ self-subsistent premium in Indonesia. Economia Agro-Alimentare/Food Economy, 23(2): 1-24. https://doi.org/10.3280/ecag2-2021oa12184

[14] Jiuhardi, J., Hasid, Z., Darma, S., Darma, D.C. (2022). Sustaining agricultural growth: Traps of socio–demographics in emerging markets. Opportunities and Challenges in Sustainability, 1(1): 13-28. https://doi.org/10.56578/ocs010103

[15] Fadhil, R., Yusuf, M.Y., Bahri, T.S., Maulana, H., Fakhrurrazi, F. (2021). Precaution strategy of moral hazard practice in agricultural insurance in Indonesia: An approach of soft systems methodology. Economía Agraria y Recursos Naturales, 21(2): 79-99. https://doi.org/10.7201/earn.2021.02.04

[16] Wibowo, T., Siregar, H., Rustiadi, E., Hardiyanto, A.T. (2022). The analysis of sub-national fiscal risk in Indonesia. International Journal of Sustainable Development and Planning, 17(7): 2183-2188. https://doi.org/10.18280/ijsdp.170718

[17] Mahul, O., Stutley, C.J. (2010). Government Support to Agricultural Insurance Challenges and Options for Developing Countries. Washington DC: World Bank. https://doi.org/10.1596/978-0-8213-8217-2

[18] Vilhelm, V., Špička, J., Valder, A. (2015). Public support of agricultural risk management-situation and prospect. Agris on-line Papers in Economics and Information, VII(2): 93-102. https://doi.org/10.7160/aol.2015.070209

[19] NRAC (National Rural Advisory Council). (2012). Feasibility of agricultural insurance product in Australia for weather related production risk. Department of Agriculture and Water Resources Publication 2012/09. Australian Government. Canberra. https://www.agriculture.gov.au/ag-farm-food/drought/assistance/mfrp/agricultural-insurance-feasibility/feasability, accessed on Feb. 16, 2020.

[20] Shadbolt, N.M., Olubode-Awasola, F., Grad, D., Dooley, E. (2010). Risk - an opportunity or threat for entrepreneurial farmer in global food market. International Food and Agribusiness Management Review, 13(1): 75-96.

[21] Mitu, N.E. (2007). Agricultural insurance in Romania: Present and future aspect. Munich Personal RePec Archive (MPRA), University of Craiova, Faculty of Economics and Business Administration, 198-206. http://mpra.ub.uni-muenchen.de/10773/, accessed on May 21, 2019.

[22] World Bank. (2010). Agricultural insurance in Latin America, developing the market (English). Report No. 61963-LAC. Washington DC: World Bank. http://documents.worldbank.org/curated/en/179701468277786453/Agricultural-insurance-in-Latin-America-developing-the-market, accessed on Feb. 16, 2020.

[23] Akhter, W., Pappas, V., Khan, S.U. (2017). A comparison of Islamic and conventional insurance demand: Worldwide evidence during the Global Financial Crisis. Research in International Business and Finance, 42: 1401-1412. http://dx.doi.org/doi:10.1016/j.ribaf.2017.07.079

[24] Erlyna, W.R., Masyhuri, M., Irham, I., Suryantini, A. (2022). The sustainability model of dryland farming in food-insecure regions: structural equation modeling (SEM) approach. International Journal of Sustainable Development and Planning, 17(7): 2033-2043. https://doi.org/10.18280/ijsdp.170704

[25] Ismanto, K. (2009). Sharia Insurance: Overview of Islamic Legal Principles. Yogyakarta: Pustaka Pelajar.

[26] OJK (The Financial Services Authority Republic of Indonesia). (2014). Hand Book the Financial Services Authority. Jakarta: OJK.

[27] Pasaribu, S.M. (2014). Application of Agricultural Insurance in Indonesia. Jakarta: IAARD Press.

[28] Sulaiman, A.A., Candradijaya, A., Syakir, M. (2018). Insurance for farmer protection: Indonesian experience. Journal of Agriculture and Research, 4(12): 14-22. https://doi.org/10.53555/ar.v4i12.2595

[29] Hussain, M.M., Pasha, A.T. (2011). Conceptual and operational differences between general takaful and conventional insurance. Australian Journal of Business and Management Research, 1(2): 23-28.

[30] Ambarawati, G.A.A., Wijaya, M.A.M., Budiasa, W. (2018). Risk mitigation for rice production through agricultural insurance: Farmer’s perspectives. Jurnal Manajemen & Agribisnis, 15(2): 128-135. http://dx.doi.org/10.17358/jma.15.2.129

[31] Atah, U.I., Mohammed, M.O., Adawiyya, E.R., Adeyemi, A.A. (2019). Proposed secured bay-salam model for financing agriculture by Islamic banks. International Journal of Management and Applied Research, 6(4): 182-195. https://doi.org/10.18646/2056.64.19-013

[32] Htay, S.N.N., Sadzali, N.S., Amin, H. (2015). An analysis of the viability of micro health takaful in Malaysia. Qualitative Research in Financial Markets, 7(1): 37-71. https://doi.org/10.1108/QRFM-09-2013-0030

[33] Maysami, R.C., Golriz, H., Hedayati, H. (1997). Pragmatic interest-free banking: Metamorphosis of the Iranian financial system. Journal of International Banking Law, 12: 92-108.

[34] Hidayat, S.E, Rafeea, A.M. (2014). Public awareness towards takaful concept and principles: A survey in Bahrain. International Journal of Excellence in Islamic Banking & Finance, 4(2): 1-16. https://doi.org/10.12816/0010778

[35] Mubarrak, H. (2016). Insurance controversy in Indonesia: Study the Indonesian Ulema Council (MUI) Fatwa about Social Insurance Administration Organization (BPJS). TSAQAFAH: Jurnal Peradaban Islam, 12(1): 105-130, https://dx.doi.org/10.21111/tsaqafah.v12i1.370

[36] Husin, M.M., Rahman, A.A. (2016). Do Muslims intend to participate in Islamic insurance? Analysis from theory of planned behavior. Journal of Islamic Accounting and Business Research, 7(1): 42-58. https://doi.org/10.1108/JIABR-03-2014-0012

[37] Habib, F., Shaukat, M. (2016). Shariah appraisal of the takaful model based on ‘tabarru’ (donation). Journal of Islamic Banking and Finance. 33(3): 65-83.

[38] Irkhami, N. (2017). A study on the implementation of dual contracts of Tabarru and Tijarah on Shari'ah insurance industries in Indonesia. Journal of Islamic Finance, 6(2): 45-57.

[39] Billah, M.M. (2019). Experience in Fire Takaful in: Islamic Insurance Products. Palgrave Macmillan, Cham. https://doi.org/10.1007/978-3-030-17681-5_8

[40] Safitri, K.I., Abdoellah, O.S., Gunawan, B., Parikesit, P., Suparman, Y. (2022). Environmental certification schemes based on political ecology: Case study on urban agricultural farmers in Bandung metropolitan area, Indonesia. Journal of Urban Development and Management, 1(1): 67-75. https://doi.org/10.56578/judm010108

[41] Puška, A., Stojanovic, I. (2022). Fuzzy multi-criteria analyses on green supplier selection in an agri-food company. Journal of Intelligent Management Decision, 1(1): 2-16. https://doi.org/10.56578/jimd010102

[42] Basahel, S., Córdoba-Pachón, J.R. (2021). An enhanced use of Soft Systems Methodology (SSM) in Mode 2 to explore online distance education in Saudi Arabia. Journal of the Operational Research Society, 73(9): 1935-1948. https://doi.org/10.1080/01605682.2021.1963194

[43] Hanafizadeh, P., Mehrabioun, M., Mostasharirad, A. (2021). The necessary and sufficient conditions for the solution of soft systems methodology. Philosophy of Management, 20: 135-166. https://doi.org/10.1007/s40926-020-00149-7

[44] Paucar-Caceres, A., Cavalcanti-Bandos, M.F, Quispe-Prieto, S.C., Huerta-Tantalean, L.N., Werner-Masters, K. (2021). Using soft systems methodology to align community projects with sustainability development in higher education stakeholders' networks in a Brazilian university. Systems Research and Behavioral Science, 39(4): 750-764. https://doi.org/10.1002/sres.2818

[45] Shahabi, A., Azar, A., Radfar, R., Asadifard, R.A. (2020). Combining soft systems methodology with interpretive structural modeling and system dynamics for network orchestration: Case study of the formal science and technology collaborative networks in Iran. Systemic Practice and Action Research, 33: 453-478. https://doi.org/10.1007/s11213-019-09490-z

[46] Fadhil, R., Qanytah, Q., Hastati, D.Y., Maarif, M.S. (2018). Development strategy for a quality management system of Gayo coffee agro-industry using soft systems methodology. Periodica Polytechnica Social and Management Sciences, 26(2): 168-178. https://doi.org/10.3311/PPso.11341

[47] Sadler, H. (2020). ER2C SDMLC: enterprise release risk-centric systems development and maintenance life cycle. Software Quality Journal, 28: 1755-1787. https://doi.org/10.1007/s11219-019-09452-7

[48] Ahmed, L., Quddus, N., Kannan, P., Peres S.C., Mannan, M.S. (2020). Development of a procedure writers’ guide framework: Integrating the procedure life cycle and reflecting on current industry practices. International Journal of Industrial Ergonomics, 76: 102930. https://doi.org/10.1016/j.ergon.2020.102930

[49] Moore, N. (2015) Systems development life cycle (SDLC). Systems Development Life Cycle Cheat Sheet. https://www.techtarget.com/searchsoftwarequality/definition/systems-development-life-cycle.

[50] Fadhil, R., Djatna, T., Maarif, M.S. (2017). Analysis and design of a human resources performance measurement system for the nutmeg oil agro-industry in Aceh. Journal of Regional and City Planning, 28(2): 99-110. https://doi.org/10.5614/jrcp.2017.28.2.2

[51] Effendi, J. (2018). Islamic insurance: A potential niche market of Indonesia. Al-Iqtishad: Journal of Islamic Economics, 10(1): 207-230. https://doi.org/10.15408/aiq.v10i1.5330

[52] Sarah, M., Mahri, A.J.W., Cakhyaneu, A. (2019). Efficiency of tabarru’ fund management at islamic insurance companies in Indonesia. In the 2nd International Conference on Islamic Economics, Business, and Philanthropy (ICIEBP) Theme: “Sustainability and Socio Economic Growth”, KnE Social Sciences, pp. 440-452. https://doi.org/10.18502/kss.v3i13.4222

[53] Ha, M., Rahman, A., Seman, A. (2018). Society’s Understanding of Family Takaful. Rahman, A. (Ed.) Emerald Publishing Limited, 151-166. https://doi.org/10.1108/978-1-78756-283-720181010

[54] Abdullah, A., Yaacob, H. (2012). Legal and sharia issues in the application of Wakalah-waqf model in takaful industry: An analysis. Procedia-Social and Behavioral Sciences, 65: 1040-1045. https://doi.org/10.1016/j.sbspro.2012.11.239

[55] Khan, F. (2015). Islamic Banking in Pakistan: Shariah-Compliant Banking and the Quest to Make Pakistan More Islamic. London, Roudledge. https://doi.org/10.4324/9781315670249

[56] Puspitasari, N. (2015). Hybrid contract and funds efficiency management of Islamic general insurance company (study in Indonesia). Procedia-Social and Behavioral Sciences, 211: 260-267. https://doi.org/10.1016/j.sbspro.2015.11.033

[57] Abubakar, L., Handayani, T. (2019). Venture capital regulation reform: revitalization of venture capital as an alternatives financing mentorship and partnership based. Journal of Private and Commercial Law, 3(1): 8-19. https://doi.org/10.15294/jpcl.v3i1.18531

[58] Jaenudin, D., Firdaus, A., Afendi, F.M., Possuma, B.T. (2015). Analysis of Ta’awun fund model best practice from Indonesia. IKONOMIKA: Jurnal Ekonomi dan Bisnis Islam, 3(2): 139-166. https://doi.org/10.24042/febi.v3i2.3497

[59] POJK (Peraturan Otoritas Jasa Keuangan). (2016) Concerning financial health of insurance companies and reinsurance companies with sharia principles. Lembaran Negara Republik Indonesia Tahun 2016 No. 305. Otoritas Jasa Keuangan, (in Indonesia).

[60] Yanli, Z. (2009). An introduction to the development and regulation of agricultural insurance in China. The Geneva Papers on Risk and Insurance - Issues and Practice, 34(1): 78-84. https://doi.org/10.1057/gpp.2008.39

[61] Thomas, A., Leichenko, R. (2011). Adaptation through insurance: lesson from the NFIP. International Journal of Climate Change Strategies and Management, 3(3): 250-263. https://doi.org/10.1108/17568691111153401

[62] Pasaribu, S.M. (2010). Developing rice farm insurance in Indonesia. Agriculture and Agricultural Science Procedia, 1: 33-41. https://doi.org/10.1016/j.aaspro.2010.09.005

[63] Abdullah, A.M., Auwal, A.G., Darham, S., Radam, A. (2014). Farmers willingness to pay for crop insurance in north west Selangor integrated agricultural development area (IADA) Malaysia. Journal of ISSAAS, 20(2): 19-30.

[64] Collier, B., Skees, J., Barnett, B. (2009). Weather index insurance and climate change: Opportunities and challenges in lower income countries. The Geneva Papers on Risk and Insurance-Issues and Practice, 34(3): 401-424. https://doi.org/10.1057/gpp.2009.11

[65] Singla, S., Sagar, M. (2012). Integrated risk management in agriculture: Inductive research. Journal of Risk Finance, 13(3): 199-214. http://dx.doi.org/10.1108/15265941211229235

[66] Ridlwan, A.A. (2016). Implementation Akad Muzara'ah in Islamic bank: An alternative to access capital agricultural sector. Iqtishoduna: Jurnal Ekonomi Islam, 7(1): 34-48.