Sergey Medvedev* | Mikhail Zyryanov | Aleksander Mokhirev | Ol'ga Kunickaya | Roman Voronov | Tamara Storodubtseva | Olga Grigoreva | Igor Grigorev

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The purpose of this article is to investigate certain aspects of the current state of the Russian timber industry. The Boston Consulting Group matrix is created to illustrate the current state of the industry in a variety of sectors. The industry's growth rates in various federal districts of the country are examined. Models of changes in volume indicators of the Krasnoyarsk Territory's timber industry output, prices, and individual qualitative characteristics for round timber are obtained. This region is fascinating due to the variety of agricultural products and climatic conditions (logging despite the High North conditions). The study recognizes the significance of expanding the use of the entire tree biomass and stimulating integration associations in the forest industry.

differentiation of production conditions, forest products, modelling, timber industry, wood biomass processing

When looking at the country's timber production, it is important to keep in mind that volume indicators for nearly every manufactured good are on the rise. The "Review of the Russian Timber Industry for 2018-2019" completed by Ernst & Young — Evaluation and Consulting Services LLC [1] contains a detailed analysis of the industry's volume indicators. As the analysis shows, 2018 was one of the most successful years in Russian history, and 2019 was expected to continue the upward trend in production and output volumes. According to many experts, a variety of factors contributed to the achievement of record-breaking results in general. State support measures and a favourable market situation stood out among them. Specifically, the forecast for 2030 indicates that even higher volume indicators are possible (Figure 1) [2].

Cardboard and paper, plywood, OSB board, fibreboard, chipboard, pellets, and cellulose are among the most promising areas of wood biomass use in Russia. Similar trends also exist in international practice, where these products are in high demand and generate the highest sales volumes. The global markets, on the other hand, are experiencing some downward trends. Changes in national and regional policies, as well as slower (or even decreasing) growth rates, have all had varying degrees of impact on the forestry (timber) industry. An interesting area of research in this regard is the analysis of the prospects for the development of the domestic timber industry not only in terms of output volumes, but also in terms of revenue received, i.e. the industry's profitability. Furthermore, in the context of the timber industry, an assessment of the prospects for the development of individual regions and macro regions (federal districts) could be made. The purpose of this study is to model the current state and prospects of the Russian timber industry in terms of the use of tree biomass, taking regional features into account.

Figure 1. Timber product output from 2008 to 2030

The study was based on data on the state of the Russian timber industry [1], data from the strategy for the development of the Krasnoyarsk Territory's forest complex until 2030, Rosstat (Unified Interdepartmental Information and Statistical System (EMISS)) statistics, and the information on the day-to-day operations of timber industry enterprises in the Krasnoyarsk Territory. It is worth noting that the data are dissimilar, which makes data processing more difficult. Furthermore, there is a scarcity of separate data for individual regions and federal districts, as well as the country as a whole.

Two approaches were used to forecast the average cost of round timber:

(1) Brown's exponential smoothing method [3]. One of its benefits is that it considers the time factor: the further the actual data on the studied indicators is from the current date, the less impact they have. Similarly, in studies related to the forest industry [4, 5], this tool has proven to be one of the most reliable and accurate.

Let φ(t) be a process defined on [T0, T2]. The forecasting value F(T2+1) of the process φ(t) at the moment t=T2+1 is computed with the aid of the polynomial function:

$F(t)=\sum_{k=0}^n \frac{1}{k !} a_k(t) t^k$ (1)

where, the coefficients ak are computed through a recurrence scheme. As an example we list here the formulas for the case n=1:

$F(t+1)=a_0(t)+a_1(t)$ (2)

$a_0(t)=2 S_t^{\prime}-S_t^{\prime \prime}$ (3)

$a_1(t)=(a /(1-\alpha))\left(S_t^{\prime}-S_t^{\prime \prime}\right)$ (4)

$S_t^{\prime}=\alpha \mu(t)+(1-\alpha) S_{t-1}^{\prime}$ (5)

$S_t^{\prime \prime}=\alpha S_t^{\prime}+(1-\alpha) S_{t-1}^{\prime \prime}$ (6)

where, $\alpha \in(0,1)$ is the smoothing parameter and $S_t^{\prime}, S_t^{\prime \prime}$ are smoothing values.

(2) Seasonal fluctuations are factored into forecasting [6]. Undoubtedly, the season-dependent cost of timber should be factored into forecast models. Seasonality must also be considered because of significant climatic fluctuations in the locations where wood biomass is harvested and processed.

We used parameter k, where k is the ordinal step of the period under study, beginning in 2014 (for the price in winter 2014 k=1, in spring k=2, ..., in winter 2020 k=25, etc.).

Brown's method was used in other forecasting cases because seasonal changes were not supposed to be considered.

The methodology proposed by Danko was used to position the competitiveness of Russian regions in the Boston Consulting Group (BCG) matrix [7]. The Boston Consulting Group Matrix (BCG Matrix), also referred to as the product portfolio matrix, is a business planning tool used to evaluate the strategic position of a firm’s brand portfolio. The BCG Matrix is one of the most popular portfolio analysis methods. It classifies a firm’s product and/or services into a two-by-two matrix. Each quadrant is classified as low or high performance, depending on the relative market share and market growth rate. The horizontal axis of the BCG Matrix represents the amount of market share of a product and its strength in the particular market. By using relative market share, it helps measure a company’s competitiveness. The vertical axis of the BCG Matrix represents the growth rate of a product and its potential to grow in a particular market. In addition, there are four quadrants in the BCG Matrix:

Question marks: Products with high market growth but a low market share.

Stars: Products with high market growth and a high market share.

Dogs: Products with low market growth and a low market share.

Cash cows: Products with low market growth but a high market share.

The assumption in the matrix is that an increase in relative market share will result in increased cash flow. A firm benefits from utilizing economies of scale and gains a cost advantage relative to competitors. The market growth rate varies from industry to industry but usually shows a cut-off point of 10% – growth rates higher than 10% are considered high, while growth rates lower than 10% are considered low.

The Microsoft Office Excel software product was used to process the data.

After analysing the revenue received by Russian timber industry enterprises from the sale of goods, products, works, and services (net of value-added tax, excise taxes, and other similar mandatory payments), a BCG matrix was created (Figure 2). The problem with making this matrix was choosing the data to put in it. Instead of the conventional data used in this tool, the study used the following axes: the domestic timber industry's share of global revenue (X-axis), and the growth rate of enterprise revenue (Y-axis). The size of the circle that corresponds to each commodity product was determined by the amount of revenue generated by enterprises. Table 1 contains the initial data for the analysis.

Figure 2. BCG matrix for Russia's basic timber products in 2019

For the avoidance of doubt, it should be stated that certain errors in the calculation are possible when dealing with the revenue derived from the production of certain types of products. This is because the indicator in US currency was calculated using the RUB/USD average exchange rate for the same period (2017 – RUB 58.3/1 USD, 2018 – RUB 62.93/1 USD, 2019 – RUB 64.62/1 USD).

Table 1. Characteristics of timber product manufacturing in Russia

|

Name of the manufactured products |

Annual revenue, USD billion |

Growth rate |

Share in global revenue |

|

|

|

2017 |

2018 |

2019 |

2019/2018 |

|

|

|

Logging |

1.317 |

1.500 |

1.297 |

86.48 |

0.57 |

|

Lumber |

2.063 |

2.156 |

2.114 |

98.04 |

1.60 |

|

Plywood |

2.165 |

2.476 |

2.135 |

86.21 |

2.82 |

|

Chipboard |

0.956 |

1.022 |

1.073 |

104.98 |

4.09 |

|

Fibreboard |

0.559 |

0.640 |

0.737 |

115.16 |

1.68 |

|

Joinery |

0.519 |

0.443 |

0.434 |

98.01 |

1.28 |

|

Wooden containers |

0.023 |

0.022 |

0.022 |

96.66 |

0.08 |

|

Cellulose and wood pulp |

1.996 |

2.601 |

2.052 |

78.89 |

2.47 |

|

Paper and cardboard |

4.322 |

4.959 |

5.069 |

102.21 |

1.56 |

|

Furniture |

2.124 |

2.248 |

2.182 |

97.08 |

0.50 |

Some interesting conclusions can be drawn based on the data obtained (Figure 2).

(1) The most interesting on the market in 2019 for domestic enterprises were cellulose, wood pulp, plywood, and chipboard. They had a sizable global market share (in comparison to the entire domestic timber industry), and chipboard revenue increased in 2019.

(2) The highest revenue growth is seen in the production of fibreboard, which, with a large share of global revenue, indicates the line's prospects in the domestic market.

(3) Despite high total profitability, a significant drop in revenue for pulp and plywood indicates downward trends in the domestic market, necessitating immediate intervention and regulation. Simultaneously, responses to the crisis should come not only from the government, but, above all, from business owners.

(4) Paper and cardboard production, as well as lumber and joinery production, should all be considered stable. Certainly, these lines need to be developed, but they are not at the top of the list in terms of severity. The situation is similar in the furniture industry. In fact, although the country's share of the global market is small, the total amount of income generated in the country does not allow for the discussion of a severe crisis in the sub-sector to be justified. The situation is getting worse with the release of wooden containers. Volumes are negligible compared to global output for objective and market-specific reasons. However, objectively speaking, this line should and has the potential to generate significantly more revenue for the industry.

(5) The logging industry is the greatest source of concern, according to the results. A highly downward trend is being created by the combination of low profitability in comparison to world practice and a decrease in revenue when compared to the previous period. If the first is well–known and widely justified [8], the second is a relatively new trend that requires more research.

The anticipated decline in revenue associated with the release of various timber industry products can be structured. Russia's forest industry is highly varied. Different regions are distinguished by indicators that are even opposed. In this context, it would be more appropriate to consider changes in indicators of federal districts rather than individual regions.

The wood biomass was used as the basis for the study (Table 1), which included the key timber industry products mentioned earlier. The North-Western Federal District (46%) plays the most important role in the revenue structure of federal districts, according to the analysis (Figure 3). Similarly, the Central and Volga Federal Districts should be considered the most powerful, accounting for 24 and 17% of the country's total revenue, respectively. The share of the Siberian Federal District, on the other hand, is quite low. This is most likely due to a lack of data on specific manufactured products, particularly slab materials.

Figure 3. Enterprise revenues earned from the production of basic timber products by Russian federal districts

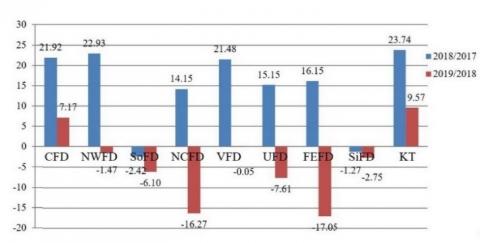

The growth rate of this indicator for the federal districts in 2018-2019 was investigated by looking at the rate of change in revenue (Figure 4). As can be seen, except for the Central Federal District, revenue decreased in 2019 compared to 2018.

It is important to note that the opposite trends are often true in federal districts. Thus, in the Siberian Federal District, where revenue is generally declining, the Krasnoyarsk Territory saw an increase in this indicator in 2018 and 2019. Despite being lower than in 2018, the increase in 2019 was higher than the total for the Central Federal District.

Figure 4. Enterprise revenue growth rate from the production of basic timber products by Russian federal districts, %

Note: CFD - Central Federal District, NWFD - North-Western Federal District, SoFD - Southern Federal District, NCFD - North Caucasus Federal District, VFD - Volga Federal District, UFD - Ural Federal District, FEFD - Far Eastern Federal District, SiFD - Siberian Federal District, KT - Krasnoyarsk Territory.

In our opinion this is due to that the Krasnoyarsk Territory is distinguished by a variety of relevant parameters:

- a large forest base;

- the presence of a multitude of industry players, both large and small on a national scale;

- the development of deep processing;

- the availability of large investment projects;

- wide differentiation by climatic conditions (from the High North to the steppes in the south of the region).

There appear to be several issues that need to be addressed in addition to the positive aspects that have been highlighted. The development of the logging sector is one of the issues that the country as a whole is dealing with. Due to the system-forming nature of its operations – its products serve as raw materials for all other timber industry enterprises – there are virtually no nearby, and thus inexpensive, raw materials. This creates difficulties in supplying round wood to enterprises at reasonable prices.

There is a Forestry Development Strategy until 2030 in place for the Krasnoyarsk Region [9]. This strategy calls for a series of measures to boost the region's timber industry. Additionally, a forecast of the future development of the production of individual goods is included. Some parameters proposed to be achieved, however, raise concerns. To begin, the achievement of certain indicators about the advancement of deep processing appears dubious. This is nearly impossible without a significant increase in capacity. Simultaneously, the raw material base for a significant increase in high-quality product production is either too far away or unavailable for efficient production.

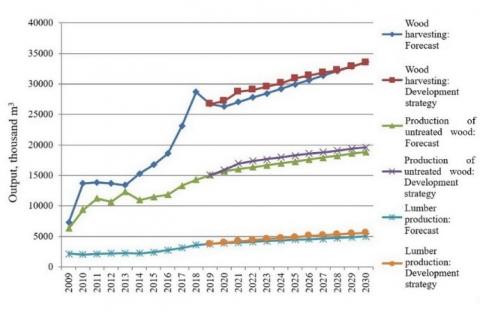

Figure 5. Comparison of forecasted changes in logging and lumber outputs in the Krasnoyarsk territory

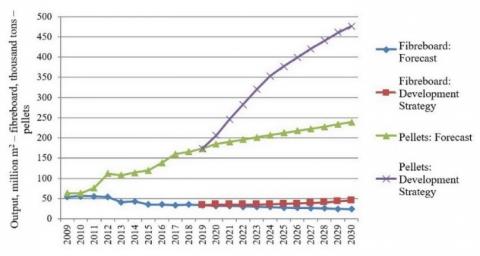

Figure 6. Comparison of forecasted changes in fibreboard and pellet outputs in the Krasnoyarsk territory

Meanwhile, the forecast for wood harvesting and lumber production in the region's Forestry Development Strategy is quite reasonable (Figure 5). While discrepancies with the values obtained as a result of the study of production development prospects using the exponential smoothing method do occur, they are not significant. In this regard, significant market fluctuations and other external variables (such as the current situation with the COVID-19 pandemic) can have a significant impact on the industry's prospects. The forecasts for the development of deep processing (Figure 6), for example, the production of fibreboard and pellets, represent another situation. The Forestry Development Strategy's forecast appears overly optimistic.

Fibreboard production in the region has been declining annually because of a global decline in demand. The region's enterprises are also shifting away from producing this product and toward other options. The practice demonstrates that a portion of the raw materials used to manufacture fibreboard is redirected to pellet, pulp, and paper manufacturing. Climate-related factors, in particular, had a significant impact on the wood fuel market in 2019, with the volume of orders for these products declining significantly. Russia's pellet market is expected to grow by 1-3% annually [1]. However, even if global demand for the product grows by 5% annually, it is unlikely that regional output will triple as predicted in the Regional Forestry Development Strategy. There are already plans in place for the development of existing and new production facilities. Undoubtedly, they will have an effect on regional output, but not in a dramatic way.

Table 2 contains data on the actual output volumes of a number of the region's basic timber products. Additionally, it includes forecast values from the Forestry Development Strategy [9] and calculations made during the forecasting process by the authors' team using Brown's exponential smoothing method. Throughout the study, predictive models for the examined groups of goods were developed, and the average approximation errors for forecasting were calculated (Table 3). Following the estimation of the average approximation error (all <10%), it was determined that all the models obtained were reasonable.

As previously stated, wood resources play a critical role in the development of the region's timber industry. However, the cost varies greatly depending on the location where they are used (processing enterprise). The town of Lesosibirsk is one of the most important wood processing centres in the Krasnoyarsk Territory (and the country). When round timber prices (prices for spruce and fir are used as examples) in Lesosibirsk are analysed, the following trend emerges: the resource is most affordable in the winter (Figure 7). This is due to the seasonal variation in supply and demand. If the annual processing volume of round wood is roughly the same, then the delivery of that wood from cutting areas varies greatly throughout the year. Winter logging roads contribute to the development of winter transportation infrastructure. The increased volume of wood transport during this season can be attributed in part to the availability of good winter roads that reduce the cost of delivering timber from the forest area to end users. Natural and climatic factors can affect the quality of roads and the amount of wood that can be moved during the winter [10]. For instance, extended autumn and/or early spring periods significantly reduce the operating season of winter logging roads [11]. Simultaneously, while the volume of wood delivered to consumers is minimal during the spring thaw, the price of timber is at its peak. This occurs when there are no roads, or they are in poor condition, as well as when the timber harvesting processes are not complicated. During the summer, when roads are normalised and the Yenisei River is used for delivery (which is extremely advantageous for timber floating), transportation volumes increase and transportation costs decrease. These variables have a direct effect on the price of goods on the market. The wood cost goes up in the autumn. The primary factor is transportation, which become more complicated as natural conditions deteriorate. Thus, it is clear that the volume of supply and, consequently, the cost of round timber is highly dependent on seasonal natural and climatic factors throughout the year.

However, there should be no disregard for market forces in determining the price of commercial timber. Inflation and a general increase in enterprise costs, such as the cost of leased equipment, fuel, and so on, imply a systematic increase in round wood prices (Figure 8). Between 2014 and 2020, the average price of round timber (spruce and fir) almost doubled in the Krasnoyarsk Territory. The increased haul (distance) of harvesting resources from the forest area was a significant factor in this case. Given the longer distances that logged vehicles must travel in challenging natural and climatic conditions, the cost and, consequently, the amount they carry will continue to rise.

Another downward trend associated with the further expansion of logging production into the forest is a decline in the size and quality of harvested wood (Figure 9) [12, 13]. The decline in weighted average diameter has a direct impact on not only the logging industry, but also on the entire timber industry. There is a good reason for this dependence. Indeed, the lower quality of raw materials impedes the production of high-quality products.

The study forecasted changes in round timber (spruce and fir) prices in the Krasnoyarsk Territory (Figure 10, Table 4).

Figure 7. How the average cost of round timber (Spruce and Fir) in the Krasnoyarsk territory varies by Season, RUB

Figure 8. How the Average Cost of Round Timber (Spruce and Fir) in the Krasnoyarsk Territory Varied in 2014-2019, RUB

Figure 9. Change and linear trends in the weighted average diameter of harvested wood in the Krasnoyarsk territory

Figure 10. Forecast of the average cost of round timber (Spruce and Fir) in the Krasnoyarsk territory until 2025

Forecast models of the cost of round timber (spruce and fir) (Yp) were obtained during the study for each approach:

- Brown's model: Yp=2611.50+38.28 · k.

- Seasonally adjusted model: Yp=1442.3· k0.2712.

where, k is the ordinal step of the period under study, beginning in 2014 (for the price in winter 2014 k=1, in spring k=2, ..., in winter 2020 k=25, etc.).

The average approximation error for the forecast values obtained through the models was calculated. It was 9.3 % in the first case and 4.89 % in the second. Both values are below 15%, indicating that the model is reasonable. The increased value with exponential smoothing over the second model is due to the method of calculation and significant seasonal price fluctuations.

The analysis of the data obtained reveals that the exponential smoothing method allows for the assumption of a marginally higher average annual price for the round timber under study. The second model, on the other hand, clearly depicts peak values and seasonal price fluctuations. This is vital for production planning and the economic activities of wood-buying enterprises.

Table 2. Forecast models and average approximation errors for changed output of certain timber products

|

Name of the manufactured goods |

Forecast model |

Average approximation error, % |

|

Woo harvesting |

Yp=17573.51+728.33 · k |

9.60 |

|

Untreated wood |

Yp=11918.58+316.82 · k |

7.73 |

|

Lumber |

Yp=2673.32+106.81 · k |

5.30 |

|

Fibreboard |

Yp=42.60-0.89 · k |

8.83 |

|

Pellets |

Yp=120.68+5.36 · k |

9.67 |

Table 3. Comparison of forecast values of timber production indicators in the Krasnoyarsk territory according to the forestry development strategy and those obtained by exponential smoothing forecasting method

|

Year |

Wood harvesting |

Release of untreated wood |

Lumber production |

Fibreboard |

Pellets |

|

|

|

|

|

|

Forecast (F) |

Development Strategy (DS) |

Forecast (F) |

Development Strategy (DS) |

Forecast (F) |

Development Strategy (DS) |

Forecast (F) |

Development Strategy (DS) |

Forecast (F) |

Development Strategy (DS) |

|

|

2009 |

7349.7 |

6301.4 |

2206.4 |

53.8 |

62.3 |

|

|

|

|

|

|

2010 |

13688.8 |

9340.1 |

2047.5 |

56.4 |

62.9 |

|

|

|

|

|

|

2011 |

13865.9 |

11240.2 |

2183.9 |

55.2 |

76.6 |

|

|

|

|

|

|

2012 |

13700.9 |

10684.4 |

2237.6 |

53.05 |

111.71 |

|

|

|

|

|

|

2013 |

13402.9 |

12308 |

2292.4 |

40.8 |

107.1 |

|

|

|

|

|

|

2014 |

15289.3 |

10973 |

2227.3 |

42.68 |

114.02 |

|

|

|

|

|

|

2015 |

16711.2 |

11508.6 |

2418.3 |

35 |

119.3 |

|

|

|

|

|

|

2016 |

18597.5 |

11804.4 |

2791.7 |

34.9 |

138 |

|

|

|

|

|

|

2017 |

23150.6 |

13330.1 |

3136.6 |

33.5 |

160.6 |

|

|

|

|

|

|

2018 |

28641.6 |

14271.5 |

3606.7 |

34.75 |

164.9 |

|

|

|

|

|

|

2019 |

26731 |

15048.4 |

3760 |

33.7 |

174 |

|

|

|

|

|

|

2020 |

26313.5 |

27245.9 |

15720.4 |

15951.4 |

3919.0 |

4000 |

32.1 |

34.5 |

185.0 |

206 |

|

2021 |

27041.8 |

28731.6 |

16037.2 |

16972.2 |

4025.8 |

4230 |

31.2 |

35 |

190.4 |

246 |

|

2022 |

27770.1 |

29025.0 |

16354.0 |

17350.0 |

4132.6 |

4420 |

30.3 |

35 |

195.7 |

282 |

|

2023 |

28498.4 |

29586.0 |

16670.8 |

17680.0 |

4239.4 |

4590 |

29.5 |

35.2 |

201.1 |

320 |

|

2024 |

29226.8 |

30125.0 |

16987.7 |

17988.0 |

4346.2 |

4750 |

28.6 |

35.8 |

206.5 |

353 |

|

2025 |

29955.1 |

30954.0 |

17304.5 |

18281.0 |

4453.0 |

4905 |

27.7 |

36.9 |

211.8 |

377 |

|

2026 |

30683.4 |

31369.0 |

17621.3 |

18560.0 |

4559.8 |

5050 |

26.9 |

37.4 |

217.2 |

399 |

|

2027 |

31411.8 |

31869.0 |

17938.1 |

18822.0 |

4666.6 |

5190 |

26.0 |

39 |

222.5 |

420 |

|

2028 |

32140.1 |

32231.0 |

18254.9 |

19093.0 |

4773.4 |

5340 |

25.2 |

40 |

227.9 |

440 |

|

2029 |

32868.4 |

32887.0 |

18571.8 |

19386.0 |

4880.2 |

5470 |

24.3 |

42.6 |

233.3 |

460 |

|

2030 |

33596.8 |

33500.0 |

18888.6 |

19642.0 |

4987.0 |

5590 |

23.4 |

45 |

238.6 |

476 |

Table 4. Forecast of the average cost of round timber (spruce and fir) in the Krasnoyarsk territory for 2020-2025 (Exponential smoothing method/seasonally adjusted model), RUB/m3

|

Year |

Season |

|||

|

Winter |

Spring |

Summer |

Autumn |

|

|

2020 |

3568.38 / 3231.89 |

3606.66 / 3938.82 |

3644.9 /3356.12 |

3683.21 / 3502.06 |

|

2021 |

3721.49 / 3373.71 |

3759.76 / 4076.91 |

3798.04 / 3490.72 |

3836.31 / 3633.37 |

|

2022 |

3874.59 / 3501.91 |

3912.86 / 4202.17 |

3951.14 / 3613.19 |

3989.42 / 3753.20 |

|

2023 |

4027.69 / 3619.23 |

4065.97 / 4317.11 |

4104.24 / 3725.85 |

4142.52 /3863.69 |

|

2024 |

4180.79 / 3727.64 |

4219.07 / 4423.53 |

4257.34 / 3830.38 |

4295.62 / 3966.40 |

|

2025 |

4333.90 / 3828.60 |

4372.17 / 4522.81 |

4410.45 / 3928.04 |

4448.72 / 4062.50 |

This study may be expanded in the future, and it appears obvious to consider options for improving the effectiveness of the timber industry in this regard. According to the authors, the primary focus should be on:

- logging;

- supplying secondary wood raw materials to enterprises;

- targeted cultivation on forest plantations [14];

- stimulating deep processing of wood.

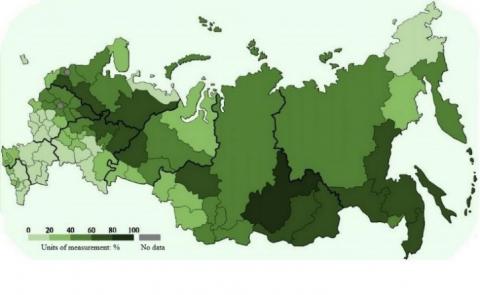

Figure 11. Forest share vs. the area of the constituent entity in Russia [15]

According to the availability of forest resources in each region (see Figure 11), the country's regions are differentiated. This feature dictates the need for joint integration projects, as well as the growth of the domestic timber market, logistics, and infrastructure.

The development of large integration structures may be the answer to several issues relating to the identified key lines. They could operate under state control (reducing the volume of illegal transactions and actions in the forest area). This measure would enable greater profitability (as the example of foreign partners demonstrates) through the pooling of resources and the ability to solve more global problems through collective efforts rather than individual enterprise efforts. Timber industry clusters are one example of such structures. They have already been established in several locations [16, 17]. However, due to the number of activities and the nature of local processes, they cannot be considered complex integration entities that raise the quality of their activities to a qualitatively higher level, as is the case in Finland [18, 19], for example.

On the other hand, there is an approach that assists small and medium-sized forestry businesses that is already in place and is being extensively worked on. In other countries, it has also worked well, and it is clear that it has a lot of advantages in Russia [20, 21]. The main thing that makes small businesses different from large ones is that they can adapt and be successful in solving a wide range of issues. Thus, in times of global change, the capacity to adapt and diversify production may be a factor in determining the development thrust of public policy [22].

The merits of either of these two paths for industrial development are debatable. However, it is ultimately this factor that determines the unique development features of the Russian timber industry such as volumes, prices, product assortment and quality, exports/imports, etc.

As a result of the study, a model of the Russian timber industry's current state and prospects for development in the context of wood biomass use was created. Additionally, the regional context was considered. The differences between the country's federal districts were examined, with a particular emphasis on the Krasnoyarsk Territory's timber industry. The obtained models accurately reflect the current state of the industry (BCG matrix), indicating that significant issues exist in the logging industry. In this regard, it should be noted that, even though the country has significant reserves of forest resources, the efficiency with which they are used is very low. The small amounts of revenue generated from product sales on a global scale attest to this. It is necessary to emphasize the important role played by the North-Western Federal District in the Russian timber industry, which produces products that account for the largest share of revenue in the country's total output scale. At the same time, revenue in all federal districts fell significantly in 2019 (and was expected to fall further in 2020). Moreover, certain regions are expanding both the physical and financial indicators of their timber industry operations. The Krasnoyarsk Territory serves as an example. For this region, forecast models for the growth of output of specific (key) timber industry products have been developed. It should be noted that some forecasts deviate significantly from the development indicators that are officially planned.

Forecasts of changes in harvested wood quality indicators (diameter) and prices for round wood (business spruce and fir) are obtained for the logging industry's difficulties mentioned. It stands to reason that their dynamics are multidirectional. However, whether the former or the latter occurs, all industries that rely on wood raw materials will suffer to some extent [23, 24]. This reintroduces the issue of low-quality wood being included in the turnover, such as forest care obtained during logging and secondary wood resources. They have the potential to be used effectively to ensure the long-term success and effectiveness of the Russian agricultural complex in the not-too-distant future [25-29].

The project «Development of an efficient technology for the processing of woody biomass in the climatic conditions of the Far North» is supported by the Krasnoyarsk Regional Fund.

[1] Baginian, K. (2021). Russian Forest Sector Overview, 2018-2019. EY. https://www.ey.com/en_ru/industrial-products/russian-forest-sector-overview-2018-2019, accessed on Apr. 12, 2022

[2] Government of the Russian Federation. (2018). Decree of the Government of the Russian Federation dated 20 September 2018 No. 1989-r "Strategy for the Development of the Timber Industry in Russia until 2030." http://government.ru/docs/34064/, accessed on Apr. 12, 2022.

[3] Lebedeva, M.Y. (2008). Analysis of how to apply Brown's method to marketing research forecasting. Marketing in Russia and Overseas, 4: 19-31. https://www.elibrary.ru/item.asp?id=11572663.

[4] Zozulya, V.V. (2011). Methodology of forming a system of taxes and other obligatory payments for the use of forest natural resources. Doctor of Economics thesis. Financial Academy, Moscow. https://www.dissercat.com/content/metodologiya-formirovaniya-sistemy-nalogov-i-inykh-obyazatelnykh-platezhei-za-polzovanie-les, accessed on Apr. 12, 2022

[5] Pozdnyakova, M.O., Medvedev, S.O., Mokhirev, A.P. (2019). Modelling of individual aspects of timber industry enterprise sustainable development based on increased availability of wood resources. Fundamental Research, 12(2): 280-284.

[6] Byvshev, V.А. (2008). Econometrics. Finance and Statistics, Moscow. https://www.elibrary.ru/item.asp?id=29055032, accessed on Apr. 12, 2022

[7] https://cyberleninka.ru/article/n/ispolzovanie-matritsy-bkg-v-otsenke-arhitektury-potentsiala-konkurentnogo-pozitsionirovaniya-regionov-rossiyskoy-federatsii-na, accessed on Apr. 12, 2022.

[8] Runova, E.M., Sorokin, D.S. (2007). Profitability of forest management as exemplified by forestry enterprises of the Middle Angara region. Coniferous Boreal Zones, 24(1): 134-139. https://doi.org/10.3390/f11040370

[9] First Deputy Governor of the Territory. (2020). Krasnoyarsk Territory Government Resolution "On Approving the Krasnoyarsk Territory Forestry Development Strategy until 2030." http://government.ru/docs/34064/, accessed on Apr. 12, 2022.

[10] Kunnas, J., Myllyntaus, T. (2022). Lessons from the past? A survey of finnish forest utilisation from the mid-eighteenth century to the present. Environment and History, 28(4): 645-670. https://doi.org/10.3197/096734020X15900760737121

[11] https://cyberleninka.ru/article/n/planirovanie-srokov-ekspluatatsii-zimnih-lesovoznyh-dorog-na-osnove-analiza-statistiki-klimaticheskih-dannyh, accessed on Apr. 12, 2022.

[12] Medvedev, S.O., Bezrukikh, Y.А., Zelenskaya, T.V., Melnikova, E.V. (2019). Secondary wood resources as a building block for timber industry clusters to develop. Resources, Information, Supply, Competition, 4: 107-112. https://www.elibrary.ru/item.asp?id=41593594.

[13] https://cyberleninka.ru/article/n/sovershenstvovanie-metodiki-programmnogo-opredeleniya-obyoma-partii-kruglyh-lesomaterialov-dlya-povysheniya-tochnosti-rezultatov, accessed on Apr. 12, 2022.

[14] Ashraf, J., Pandey, R., de Jong, W. (2017). Assessment of biophysical, social and economic drivers for forest transition in Asia-Pacific region. Forest Policy and Economics, 76: 35-44. https://doi.org/10.1016/j.forpol.2016.07.008

[15] Chen, T.L., Kim, H., Pan, S.Y., Tseng, P.C., Lin, Y.P., Chiang, P.C. (2020). Implementation of green chemistry principles in the circular economy system towards sustainable development goals: Challenges and perspectives. Science of the Total Environment, 716: 136998. https://doi.org/10.1016/j.scitotenv.2020.136998

[16] Kurbanov, E., Konijnendijk, C. (2009). Tempus project results in establishment of Povolgie forest cluster. EFI News, 17(3): 12-13. https://www.elibrary.ru/item.asp?id=20543365, accessed on Apr. 12, 2022.

[17] Sakhanov, V.V., Korotkov, S.A., Fitchin, A.А. (2016). The Central Region's timber industry: the state, problems, and prospects for innovative renewal. Scientific Review: Theory and Practice, 7: 129-140. https://www.elibrary.ru/item.asp?id=26537420.

[18] Medvedev, S., Mokhirev, A., Rjabova, T. (2022). The added value of products is a key factor in the development of the forest industry. In: IOP Conference Series: Earth and Environmental Science, 988(3): 032048. http://dx.doi.org/10.1088/1755-1315/988/3/032048

[19] Bykanova, O.A., Akhmadeev, R.G., Glubokova, N.Y., Kravchuk, I.S. (2018). The global market of round wood: financial aspects. Bulgarian Journal of Agricultural Science, 24(1): 8-16.

[20] Ingemarson, F. (2002). Small-scale forestry in Sweden: owners' objectives, silvicultural practices and management plans. Sveriges lantbruksuniv, Acta Universitatis Agriculturae Sueciae. Silvestria.

[21] Tomič, A., Šupín, M. (2019). The increasing website traffic of Woodworking Company using digital marketing methods. Acta Facultatis Xylologiae Zvolen Res Publica Slovaca, 61(2): 153-161.

[22] Tambi, A.A., Morkovina, S.S., Grigoriev, I.V., Grigoriev, V.I. (2019). Development of the circular economy in Russia: biofuel market. Forestry Engineering Journal, 9(4): 173-185. http://dx.doi.org/10.34220/issn.2222-7962/2019.4/19

[23] Medvedev, S.O., Mokhirev, A.P., Pozdnyakova, O.O. (2019). Modelling of qualitative characteristics of wood resources as a key element in the development of timber enterprises. Wood-Working Industry, 3: 3-10. https://www.elibrary.ru/item.asp?id=41347962, accessed on Apr. 12, 2022.

[24] Mokhirev, A., Gerasimova, M., Pozdnyakova, M. (2019). Finding the optimal route of wood transportation. In: IOP Conference Series: Earth and Environmental Science, 226(1): 012053. https://doi.org/10.1088/1755-1315/226/1/012053

[25] Tomter, S.M., Kuliešis, A., Gschwantner, T. (2016). Annual volume increment of the European forests—description and evaluation of the national methods used. Annals of Forest Science, 73(4): 849-856. https://doi.org/10.1007/s13595-016-0557-2

[26] Pozdnyakova, M.O., Mokhirev, A.P., Medvedev, S.O. (2019). Analyses of the factors affecting the economic efficiency of timber industry enterprises. Fundamental Research, 5: 94-98. http://biblioteka.sibsau.ru/pdf/izdv/izdv_sibgtu/Bezrukikh_Upravlenie_2018.pdf, accessed on Apr. 12, 2022

[27] McDowell, N.G., Allen, C.D., Anderson-Teixeira, K., Aukema, B.H., Bond-Lamberty, B., Chini, L., Clark, J.S. Dietze, M., Grossiord, C., Hanbury-Brown, A., Hurtt, G. C., Jackson, R.B., Johnson, D.J., Kueppers, L., Lichstein, J.W., Ogle, K., Poulter, B., Pugh, T.A.M., Seidl, R., Turner, M.G., Uriarte, M., Walker, A.P., Xu, C. (2020). Pervasive shifts in forest dynamics in a changing world. Science, 368(6494): eaaz9463. https://doi.org/10.1126/science.aaz9463

[28] Grigoreva, O., Runova, E., Ivanov, V., Alyabyev, A., Hertz, E., Voronova, A., Shadrina, S., Grigorev, I. (2021). Influence of different forest management techniques on the quality of wood. Journal of Renewable Materials, 9(12): 2175-2188. https://doi.org/10.32604/jrm.2021.016387

[29] Grigoreva, O., Runova, E., Ivanov, V., Savchenkova, V., Hertz, E., Voronova, A., Shvetsova, V., Grigorev, I., Lavrov, M. (2021). Comparative analysis of thinning techniques in pine forests. Journal of Forestry Research, 33: 1145-1156. https://doi.org/10.1007/s11676-021-01415-8