Sudarnice Sudarnice![]() | Nuri Herachwati

| Nuri Herachwati![]() | Udin Udin*

| Udin Udin*![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Small and medium-sized enterprises (SMEs) must improve their performance to remain competitive in an unstable market, especially during the digital era and the COVID-19 pandemic crisis. This study investigates the influence of bank financing and government support on SME performance, with entrepreneur competence as a mediator. Data were collected from a sample of SMEs through questionnaires distributed to 115 owners and interviews with SME stakeholders. The data were analyzed using factor analysis and principal component analysis, followed by structural equation modeling (SEM) and the Partial Least Square (PLS) program. The results show that bank financing and government support do not directly affect SME performance, but entrepreneur competence mediates the relationship.

entrepreneur competence, bank financing, government support, SME performance, structural equation modeling (SEM), Partial Least Square (PLS)

Small and medium enterprise (SME) plays a significant role in improving the economy, and has become one of the driving forces of economic movement in Indonesia. According to Mustikasari and Noviardy [1], SME is a pillar of the Indonesian economy, and expanding this sector can contribute significantly to national economic growth. With approximately 99% of business activities in Indonesia being represented by SME, and over 98% of these categorized as micro-businesses [1], it is evident that SME is widely dispersed across the country. To improve the economy, it is important for the government to encourage the development of SME and create a competitive advantage for them to compete with other business sectors. However, it is a challenging task to create a competitive advantage in the world of SME. Business actors must be able to understand the environment, consumer desires, and existing transformations to compete effectively. Therefore, the continuous development of SME must be encouraged and supported to ensure they remain competitive and make a substantial contribution to the economy.

According to data obtained from the Ministry of Cooperatives and small and medium enterprises in Figure 1, the number of SMEs in Indonesia has been on the rise every year. However, there has been a decrease in the number in 2020 and 2021. In Southeast Sulawesi Province, data from 2019 to 2021 shows an increase in SMEs. However, when comparing urban districts based on Ministry of Cooperatives and SME data, Buton Selatan Regency had only 10 registered SMEs, the lowest number. Furthermore, field data shows that despite having a potential for development and support from banks and the government, Buton Selatan Regency only has 1,052 officially registered SMEs out of a total of 5,253 actors who are experiencing development (Department of Cooperatives and SME Buton Selatan, 2022).

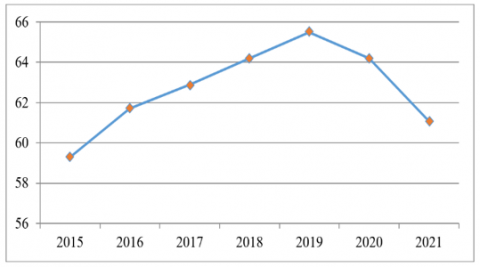

Figure 1. Quantity of SMEs development in Indonesia

Source: Ministry of Cooperatives and SMEs in 2022

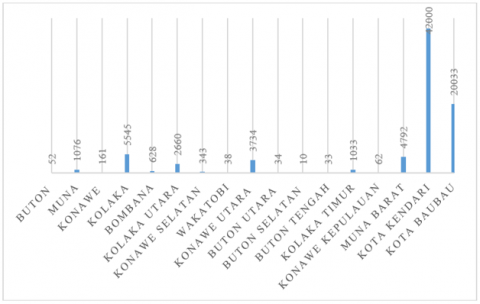

The difference in SME data between Buton Selatan Regency and the Ministry, as shown in Figure 2, can be attributed to the constraints faced by the Newly Expanded Regency, which affect SME development in the region. Limited entrepreneurial competence, access to financing, capital, and financial behavior also impact the willingness of SME actors to obtain permits for their businesses.

Although limited access to financing is still a constraint for SME, other data reveals that these sectors have relatively sufficient access to financing. However, due to unilateral and illogical policy issues, accessible funding cannot generate vertical progress within the sector. Therefore, it is necessary to identify mediation between government support and bank financing in underdeveloped or new expansion areas in Indonesia as the focus of this study. In addition, the mediating variable that plays a role between the financial capabilities of banks and the government on the SME performance in this study is the entrepreneurial competence.

Figure 2. Data from the Ministry of Cooperatives and SMEs for 2023

Entrepreneurial competence is the ability of business actors to obtain, apply, and expand resources for business purposes in a specific context [2]. When business owners and managers develop their entrepreneurial competence, they can use innovative methods to overcome company issues, enabling them to leverage these difficulties [3]. As a result, highly proficient entrepreneurs can improve their businesses, leading to enhanced capabilities of SMEs [4].

According to Sefiani [5], SME performance is the outcome of work carried out by an individual within the company, through personal assignments over a specific period of time, which must be aligned with the company's values and standards. Therefore, this study assesses SMEs' performance in terms of several factors, including profit, social expenditure, extra work, and additional value-added output [6].

Measuring the performance of SME can be a challenging and paradoxical task due to the diverse capabilities and characteristics of each organization. Previous research has suggested using financial indicators, but others have emphasized the significance of non-financial indicators. While financial quantification is crucial, it needs to be complemented with other performance indicators to gain a comprehensive understanding of the organization's overall performance [5, 6]. However, small businesses often lack the financial resources required to provide an accurate and objective description of their business results, making self-reporting criteria related to competence factors necessary to measure their performance [7]. This is particularly important if SME do not maintain their records, as obtaining historical and objective data can become difficult. Additionally, recorded financial data may not always accurately reflect business performance from the owner's perspective [5]. Therefore, this study quantifies SME performance based on multiple factors, including profit, additional work, social budget, and added value output [8].

Although there is a direct impact of entrepreneur competence on SME performance that has been studied extensively, including Bendary and Minyawi [8], Oraya and Maina [9], the impact of mediation needs to be documented categorically. Since the performance of SMEs is the benefit of various aspects such as financial services and government promotions, this aspect can be influenced by other mediating variables. This study investigates the lease–debt relationship for Belgian small and medium-sized enterprises (SMEs). Traditional finance theory suggests that leases and corporate debt are substitutes: both leases and debt are fixed, contractual obligations that reduce the firm's debt capacity. More use of leases should therefore be associated with less non-lease debt financing. However, some empirical studies find that for large firms, leases and debt are complements. A theoretical explanation for this so-called “leasing puzzle” is based on the tax advantage of leasing over debt. However, in Belgium, tax differences between lessor and lessee do not affect the choice between leases and debt, because the lessee is considered to be the fiscal owner of the assets. He may write off these assets for tax purposes, and the interest part of the lease payments are deductible from his taxable income. Leases and debt can therefore be expected to be substitutes.

Therefore, the specific objectives of this study are to examine (1) the relationship between bank financing and SME performance; (2) the impact of government support on SME performance; (3) the impact of bank financing on entrepreneur competence; (4) the impact of government support on entrepreneur competence; (5) the impact of entrepreneur competence on the performance of SMEs; (6) the impact of entrepreneur competence mediation on the relationship between bank financing and SME performance; (7) the impact of entrepreneur competence mediation on the relationship between performance of SME and government support.

2.1 Bank financing on SME performance

Efforts to provide financial services to companies at affordable prices are very important for the company's operations. Ibor et al. [10] found that bank financial services, such as loans, leasing, and letters of credit, have a positively significant impact on the development and performance of SMEs [11, 12]. In this study, the effect of bank financial services on the SME performance is examined, with a particular emphasis on leasing and letters of credit. These are some of the additional external financing options for SMEs because bank loans are known significantly impact SME performance [13]. Several studies have shown that increasing the quantity of loans supplied to companies significantly improves SME performance. Ayuba and Zubairu [14] reported a significant impact of bank loans on SME development. At the national level, bank financing is not limited to traditional interest-bearing loans but can also include interest-free loans, factoring, leasing, and letters of credit [12].

Bank offers various financial services, one of which is a letter of credit, which is a payment mechanism widely used in business. It serves as a guarantee for the seller of goods or services that the buyer will be able to pay the relevant amount. However, a letter of credit can also be used as a financing option for companies facing cash flow problems. With the help of technology, some banks and beneficiaries now use paperless letters of credit, which are a more efficient and convenient alternative [15]. Any form of a letter of credit can help promote international business. Furthermore, for local purchases as well as small financial needs, SME owner-managers are able to use bank-issued credit cards to purchase goods or services over their account balance.

Another financial service offered by commercial banks is leasing. Although leasing is frequently used as a source of financing, there is a need for more research to be conducted, particularly in developing countries, to better understand the effects of leasing on SME performance [16]. Furthermore, the SME capital structure literature has not given much consideration to leasing [17]. Some literature has discussed lease financing and corporate debt, which are considered as indicators of a negative correlation between debt and lease financing [17]. Empirical studies have shown that commercial bank financing has a notable positive impact on SME performance [10, 12, 14].

H1: The performance of SMEs is positively impacted by bank financing

2.2 Government support on SME performance

To enhance SME performance, it is crucial to receive government support. A conducive business environment, which includes services like premises and marketing facilities, can motivate the sector. The level of government support directly affects the pace of SME development, as demonstrated by previous research [18, 19]. Tax relief, incentives, and proper supervisory structures are also essential government support measures that positively impact SME performance [5, 18, 20].

Although government intervention alone cannot be the sole determinant of SME performance, it remains a significant factor [21]. Companies require help from the government in both financial as well as non-financial forms. For instance, if there is no assistance from the government in the public-private interaction, the motivation of the SME sector may decrease, according to a report from the OECD in 2004. The government may assist entrepreneurs in creating a platform that encourages SME innovation [22]. Furthermore, government support can be achieved by fostering a conducive environment for healthy competition. According to Zhu et al. [18], competition fairness, laws and regulations, as well as tax burden are some areas of government support that impact SME performance as perceived by owner-managers.

Furthermore, the importance of government support for SME performance cannot be overstated, and one of the key attributes that it offers is structure. This structure includes authoritative social behavior guidelines, encompassing systems, norms, as well as rules [23]. The government can provide assistance to SME in establishing a comfortable institutional structure and arrangements, which is essential for their success, irrespective of the economic conditions [19].

H2: Government support has a positive impact on SME performance

2.3 Entrepreneur competence on SME performance

Competence has been defined with two important meanings by Boyatzis et al. [24], the behavior exhibited by an individual and a minimum standard of performance. Furthermore, competence is considered a fundamental trait that yields successful action or improved work performance [24, 25]. Nevertheless, the tendency to attribute a halo effect to more effective people can arise when competence is depicted as a single construct [26]. Therefore, entrepreneurs should be aware of their behavior's potential positive or negative impact, and it is crucial to understand business success through entrepreneurial competence [27-31].

As Man et al. [3] reported, ten areas of entrepreneurial competence were identified: capabilities in opportunity, relationship, human, analysis, creativity, operationalization, strategy, commitment, personal strength, and learning. The attributes cited in the study are self-knowledge, persistence, assertiveness, planning, independence, establishing networks, and opportunity-seeking [30]. Additionally, risk-taking, as well as initiation were recognized as key entrepreneur competence traits that contribute to the success of an operator [32]. These traits, including risk-taking, persuasion, independence, and initiation, are commonly used to define entrepreneurial competencies in various studies [3, 33-35].

The performance of SME is significantly influenced by entrepreneurial competence [36, 37]. This competence not only has a direct effect on SME performance but also acts as a mediator between financial services as well as SME performance. Specifically, the relationship between financial services and SME development is partly mediated by entrepreneurial competence [38]. Moreover, Sarwoko et al. [39] revealed the role of entrepreneurial ability in mediating the SME performance relationship, showing the significance of this characteristic in predicting SME success.

H3: There is an influence of bank financing on entrepreneur competence

H4: There is an influence of government support on entrepreneur competence

H5: There is an influence of entrepreneur competence on SME performance

H6: There is a mediating role for entrepreneur competence in the relationship between bank financing and SME performance

H7: There is a mediating role for entrepreneur competence in the relationship between government support and SME performance

3.1 Research place

The study location is in areas especially in the stage of development, such as Buton Selatan Regency as a new expansion area in Indonesia.

3.2 Samples and data collection method

This study focuses on 1,549 SMEs that receive financial assistance from banks and the government. The sampling method used is purposive sampling, which involves selecting sample members based on specific criteria [40]. According to Williams et al. [41], determining the minimum number of samples is calculated based on the formula, namely n = (5-10 x the number of indicators used), so the number of samples used is 115 SMEs.

The distribution of questionnaires was sent directly and online to each leader. In addition, the data obtained by interviews are also used as a support and reinforcement of the questionnaire results.

3.3 Measures

SME performance is measured using three-item indicators adapted from Lingesiya [42], Sefiani [5]. Entrepreneur competence is measured using four items adapted from Kyndt and Baert [43], Mishra and Zachary [44]. Bank financing is measured using 3 item indicators adopted from Cámara and Tuesta [11], Yazdanfar and Öhman [45]. Government support also uses three indicator items adapted from Khanal et al. [20], Zhu et al. [18] (Table 1).

Table 1. Variables measurement

|

Variables |

Indicators |

Sources |

|

SME Performance |

Profitability, social engagement, and an increase in employees |

Lingesiya [42], Sefiani [5] |

|

Entrepreneur Competence |

Initiation, independence, persuasion, as well as risk-taking |

Kyndt and Baert [43], Mishra and Zachary [44] |

|

Bank Financing |

Loans, leases, and letters of credit |

Cámara and Tuesta [11], Yazdanfar and Öhman [45]. |

|

Government Support |

Motivation, tax breaks, and institutional structure |

Khanal et al. [20], Zhu et al. [18] |

The response rate for the questionnaire distributed to all respondents where we took 10 x the number of indicators so that the number of targeted samples was 170 respondents. However, of the 170 questionnaires distributed, only 115 (67.6%) were eligible for analysis, while 55 (32.4%) respondents did not fill out the questionnaire. The action taken to minimize non-response bias is to give the questionnaire directly to the SME owner then all questionnaire items are designed as exogenous variables in a 5-point Likert scale, ranging from 1 (strongly disagree) to 5 (strongly agree) designed to understand the dependent variable and mediation.

3.4 Data analysis technique

Factor analysis using principal component analysis and structural equation modeling (SEM) using the PLS program are the two methods used for data analysis. According to Kline [46], A multivariate statistical method called PLS compares numerous dependent and independent variables.

In terms of respondent gender, the data indicates that the majority of SMEs in Buton Selatan Regency are led by females. This means that improving the performance in Buton Selatan Regency should take into consideration the female gender as the dominant actors in the sector. Table 2 provides descriptive data on the gender of the respondents.

Table 2. Respondents' descriptive based on gender

|

Gender |

Frequency |

Percentage (%) |

|

Male |

43 |

37.39 |

|

Female |

72 |

62.61 |

|

Total |

115 |

100 |

In this study, the educational level of respondents is a significant factor that influences the capabilities and competencies of human resources in fulfilling their duties and responsibilities. The low level of education is identified as a key reason for the underperformance of SMEs in Buton Selatan Regency. For a detailed overview of the respondents' education, refer to Table 3.

Table 3. Respondents' descriptive based on education

|

Educational level |

Frequency |

Percentage (%) |

|

SD (Elementary School) |

14 |

12.17 |

|

SMP (Middle School) |

22 |

19.13 |

|

SMA (High School) |

41 |

35.65 |

|

D3 (College) |

21 |

18.26 |

|

S1 (University) |

17 |

14.78 |

|

Total |

115 |

100 |

Table 3 shows that SMEs with high school education dominate the SMEs in Buton Selatan Regency. In contrast, those with diploma/graduate level education are very few because, based on facts in the field, people who have already attended college prefer to look for other jobs, such as teachers and other office workers outside the Buton Selatan Regency area. The same is true for SMEs with elementary school education as the fewest respondents. This shows that the lower a person's education, the higher the fear of risk in running SMEs, especially those related to bank financing.

In addition, the demographic factor of human resources that is important and can be used as a benchmark for the productivity capabilities of SMEs is the age of 31 – 40 years. Descriptive data about the respondents' age is shown in Table 4.

Table 4. Respondents' descriptive by age

|

Age |

Frequency |

Percentage (%) |

|

21 - 30 years |

28 |

24.35 |

|

31 - 40 years |

52 |

45.22 |

|

41 - 50 years |

27 |

23.48 |

|

Over 50 years |

8 |

6.96 |

|

Total |

115 |

100 |

Individuals with a relatively young age tend to have better physical endurance than those who are relatively old. Apart from that, the category (age 31 – 40 years) is also a characteristic of the Millennials generation, which has a very independent personality, because they no longer have to depend on others. However, this does not support SMEs in Buton Selatan Regency to be more productive in business administration or legality because only a small number of SMEs are recorded in the Ministry of Cooperatives and Small data Medium Enterprises, which indicates the need for further research.

Table 5. Respondents' descriptive based on income

|

Revenue |

Frequency |

Percentage (%) |

|

< IDR 2,500,000 |

12 |

10.43 |

|

IDR 2,500,000 – IDR 5,000,000 |

38 |

33.04 |

|

IDR 5,000,000 – IDR 10,000,000 |

29 |

25.22 |

|

> IDR 10,000,000 |

36 |

31.30 |

|

Total |

115 |

100 |

Based on the income in Table 5, it is dominated by types of businesses in the medium category because the most income is > IDR 10,000,000, namely 36 people. This means that the income of SME actors in Buton Selatan Regency is greatly influenced by the income earned, so they only take care of some of the administration or legality of their business. This can be a reference for further research on enhancing the SME performance, especially in new expansion areas.

Based on the PLS method analysis with help from SmartPLS 3.3 software, the outer model measurement model with reflective indicators has a validity value (loading above 0.5) of the constructs measured by convergent and discriminant validity, while construct reliability is measured by composite reliability. Table 6 shows the outcomes of the quantification model testing.

The results of convergent validity are carried out by checking the system's reliability, which is characterized by a loading factor value > 0.7 which is said to be reliable. Table 7 shows the loading factor results.

Based on Table 6 it shows that all variables have a Cronbach's Alpha coefficient value > 0.6 so that the indicators for each variable are declared valid and can be used as a further testing tool. The results of convergent validity are carried out by checking the reliability of the system which is marked by a loading factor value > 0.7 which is said to be reliable. Data collection was carried out via an online survey developed between August and December 2022. The measurement variables and data collected were provisionally separated at two different time points to avoid potential problems associated with single informant bias and common methods. The initial stage consisted of collecting answers given by SME owners about the variables "bank financing channels, government support, entrepreneurial competency and SME performance". This number of observations is sufficient to achieve an acceptable level of statistical power using the PLS technique.

The r-square (reliability indicator) of the dependent construct and the t-statistic value of the path coefficient test are examined in order to evaluate the suggested research model. A better prediction model is one with a greater r-square value. The path value coefficient plays a key role in the hypothesis test.

Table 6. Construct validity and reliability

|

Cronbach's Alpha |

rho_A |

Composite Reliability |

Average Variance Extracted (AVE) |

|

|

Bank Financing |

0.764 |

0.765 |

0.864 |

0.679 |

|

Entrepreneur Competence |

0.898 |

0.904 |

0.922 |

0.666 |

|

Government Support |

0.793 |

0.801 |

0.878 |

0.706 |

|

SMEs Performance |

0.903 |

0.908 |

0.928 |

0.722 |

Table 7. Result for outer loadings

|

Bank Financing |

Entrepreneur Competence |

Government Support |

SMEs Performance |

|

|

BR1 |

0.796 |

|||

|

BR2 |

0.800 |

|||

|

BR3 |

0.874 |

|||

|

EC1 |

0.781 |

|||

|

EC2 |

0.857 |

|||

|

EC3 |

0.880 |

|||

|

EC4 |

0.860 |

|||

|

EC5 |

0.741 |

|||

|

EC6 |

0.765 |

|||

|

GS1 |

0.807 |

|||

|

GS2 |

0.854 |

|||

|

GS3 |

0.859 |

|||

|

PMSMEs1 |

0.831 |

|||

|

PMSMEs2 |

0.834 |

|||

|

PMSMEs3 |

0.787 |

|||

|

PMSMEs4 |

0.915 |

|||

|

PMSMEs5 |

0.875 |

Table 8. R-square value

|

|

R Square |

R Square Adjusted |

|

Entrepreneur Competence |

0.707 |

0.700 |

|

SMEs Performance |

0.715 |

0.706 |

Table 9. Path coefficients

|

Hypothesis |

Original Sample |

Sample Mean |

Standard Deviation |

T statistics |

P values |

|

Bank Financing$\rightarrow$Entrepreneur Competence |

0.579 |

0.583 |

0.053 |

11.007 |

0.000 |

|

Bank Financing$\rightarrow$SMEs Performance |

0.139 |

0.131 |

0.081 |

1.705 |

0.089 |

|

Entrepreneur Competence$\rightarrow$SMEs Performance |

0.627 |

0.623 |

0.088 |

7.089 |

0.000 |

|

Government Support$\rightarrow$Entrepreneur Competence |

0.363 |

0.355 |

0.067 |

5.379 |

0.000 |

|

Government Support$\rightarrow$SMEs Performance |

0.141 |

0.142 |

0.110 |

1.284 |

0.200 |

|

Bank Financing à Entrepreneur Competence$\rightarrow$SMEs Performance |

0.363 |

0.363 |

0.061 |

5.939 |

0.000 |

|

Government Support à Entrepreneur Competence$\rightarrow$SMEs Performance |

0.228 |

0.222 |

0.056 |

4.085 |

0.000 |

Table 8 presents the determination's coefficient through the variance analysis (r²) to evaluate the independent variable effect on the dependent variable based on the structural model analysis.

The entrepreneur competence variable in this study has an R-square value of 0.707, indicating that the relationship between bank financing and government support can explain 70.7% of its variance. Meanwhile, other factors not covered in this study affect the remaining 29.3% of the variation. Furthermore, the R-square value of SME performance is 0.715, indicating that SME performance is influenced by bank financing relationships, government support, and entrepreneur competence by 71.5%, while other factors outside those studied influence the remaining 28.5%.

Additionally, to determine the path coefficient's value, it is imperative to conduct a hypothesis testing procedure by executing the bootstrapping process. Table 9 presents the test results for the hypothesis of this study.

The impact of bank financing on the performance of SMEs is the focus of the first hypothesis, but is refuted by the results of the hypothesis test. Specifically, the findings show that the original sample estimate of the relationship between bank financing and SME performance was 0.139. In addition, the t statistic is 1.705 with a p value > 0.05. This shows that the performance of SMEs is not directly affected by bank financing. These results indicate that bank financing does not directly affect the performance of SMEs. These findings reject the results of research [10, 12, 14] that commercial bank financing has a significant positive impact on SME performance and support previous studies such as [47] which showed that short-term loan funding from banks, leverage, and fixed asset ratios have an effect negatively on company performance. These results indicate that the relationship between SME performance and banking financing for SME actors in the regions at the new expansion stage has no direct effect. This is also due to the existence of loans, leasing, and letters of credit for SMEs which can put pressure on the return on capital so that the focus of SMEs is no longer on performance for sustainability but instead focuses on return on venture capital. Therefore, it is expected that banks will provide outreach to SMEs so that they understand carefully the procedures and strategies for loan management. In addition, it is also hoped that the government will pay attention to SMEs in tax exemption so that SMEs can focus on business strategy.

The second hypothesis examines the effect of government support on the performance of SMEs. The results of the hypothesis test show that the original sample forecast of government support for SME performance is 0.141, and the t-statistic is 1.284. With a p value > 0.05, the second hypothesis is also refuted, which shows that government support has no direct effect on the performance of SMEs. These results reject research [19, 21, 22] that government support can provide success to SMEs, but this research is consistent with research findings conducted by Zhu et al. [18], Sefiani [5], Khanal et al. [20], Mishra and Zachary [44]. In addition, this finding is in line with observations in the field that even though government support for SME performance has increased from year to year, it does not necessarily encourage business improvement for SME players. This is because government support in the form of motivation, tax breaks, and institutional structures often comes in the form of grants which can lead to complacency and a lack of creativity among SMEs. So that the government needs to pay attention to additional support for SMEs such as tax abolition, and motivation for reducing interest on loans to banks.

The third hypothesis examines the effect of bank financing on entrepreneurial competence. The results showed that the Original Sample Estimation of the Relationship between Bank Financing and Entrepreneurial Competence was 0.579, while the t-statistic was 11.007. The third hypothesis is accepted because it can be concluded from these findings that the p-value is less than 0.05. This shows that the relationship between bank financing has a significant effect on entrepreneurial competence. This finding is consistent with Mohamad and Sidek [38]. In addition to theoretical support, facts on the ground also show that every SME actor who has a financing relationship with a bank can develop the ability to take initiative, be independent, persuasive and dare to take risks so that every year SME actors always submit applications. additional cost of working capital. This means that practically bank financing for SMEs in the new expansion area (Buton Selatan Regency) can shape their entrepreneurial competence. This needs to be the concern of the banking sector that bank financing for SMEs is only for those who have entrepreneurial competence.

The fourth hypothesis examines the effect of government support on entrepreneurial competence. The results showed that the initial sample estimate of government support for entrepreneurial competence was 0.228 while the t-statistic was 5.379. The fourth hypothesis is accepted because the data shows a p-value <0.05. This shows a significant influence of government support on entrepreneurial competence. This finding concurs with Mohamad and Sidek [38]. This finding also illustrates that SMEs that receive support from the government can also develop skills in initiation, independence, persuasion, and risk taking for SMEs. Similar to the third hypothesis, in the fourth hypothesis that practically the government's support for SMEs in the new expansion area (South Buton Regency) can shape their entrepreneurial competence. This needs to be a concern of the government that bank financing for SMEs is only given to those who have entrepreneurial competence.

The fifth hypothesis examines the effect of entrepreneurial competency on SME performance. The results showed that the Original Sample Estimation of Entrepreneurial Competence on SME Performance was 0.627, while the t-statistic was 7.089. Based on these findings, the fifth hypothesis is accepted because the p-value > 0.05. This shows that entrepreneurial competence has a strong influence on the performance of SMEs. The results of this study also support the results of research from Sarwoko et al. [39]. Facts in the field are based on observations that SMEs in South Buton Regency who have entrepreneurial competence in the form of initiative, independence, confidence, and the courage to take risks can experience an increase in their business profits and an increase in the number of employees. This can provide additional support for the findings of previous studies.

The sixth hypothesis examines the mediating effect of entrepreneurial competence on the relationship between bank financing and SME performance. The test results show that the value of Specific Indirect Effects mediates entrepreneurial competency on the relationship between bank financing and SME performance of 0.363, and a t-statistic of 5.939 with a p-value <0.05. This suggests the role of entrepreneurial skills in moderating the relationship between bank financing and SME performance. This analysis also supports the findings of Mohamad and Sidek [38] that entrepreneurial competence mediates the relationship between financial services and SME growth. Furthermore, these results are also supported by the facts on the ground that SMEs who have relationships with banks can improve the performance of SMEs in terms of profitability and available resources, provided that SMEs have entrepreneurial competence. This means that from our observations in the field, SMEs that receive financing from banks and have entrepreneurial competence feel free from the pressure of loans, leases and letters of credit, but their businesses are growing.

The seventh hypothesis discusses the role of entrepreneur competence in mediating the relationship between government support and SME performance. The test results show that the value of Specific Indirect Effects or the mediation path coefficient of entrepreneurial competency on the relationship between government support and SME performance is 0.363. The t-statistic is 4.085, and the p-value is <0.05. These results indicate that the relationship between government support and SME performance is mediated by entrepreneurial competence. This is in line with the observation that SMEs that have received encouragement from the government have developed and some have stagnated. Further investigation confirms that only developing SMEs have entrepreneurial competence, while those that are not developing do not, which is in line with the second hypothesis. This finding is in line with research by Sarwoko et al. [39] which shows that entrepreneurial competence has a mediating effect on SME performance. Furthermore, these results are also supported by the facts on the ground that SMEs who receive government support can improve the performance of SMEs in terms of profitability and available resources, provided that SMEs have entrepreneurial competence.

Based on the results of hypothesis testing conducted on 115 SME owners, it can be concluded that the impact of bank financing and government support does not have a direct effect on SME performance, but the relationship between bank financing and government support has a significant effect on entrepreneurial competence, then entrepreneurial competence has a strong influence on performance. SMEs so that when viewed from an indirect or mediating effect, it shows that the relationship between bank financing and government support on the performance of SMEs can be mediated by entrepreneurial competence. This can provide an explanation that the relationship between bank financing and government support will affect the performance of SMEs if the SMEs have entrepreneurial competence.

This research is predicted to accommodate various benefits for related parties, such as:

This study has limitations that need to be noted as follows:

[1] Ulya, N.U., Musyarri, F.A. (2020). Reformulation of regulations regarding financial technology in positive law in Indonesia. Legal Arena, 13(3): 479-500. https://doi.org/10.21776/ub.arenahukum.2020.01303.5

[2] Mitchelmore, S., Rowley, J. (2010). Entrepreneurial competencies: A literature review and development agenda. International Journal of Entrepreneurial Behavior & Research, 16(2): 92-111. https://doi.org/10.1108/13552551011026995

[3] Man, T.W.Y., Lau, T., Chan, K.F. (2002). The competitiveness of small and medium enterprises: A conceptualization with focus on entrepreneurial competencies. Journal of Business Venturing, 17(2): 123-142. https://doi.org/10.1016/S0883-9026(00)00058-6

[4] Bhutta, N.T., Ali Shah, S.Z. (2015). Do behavioural biases impact corporate entrepreneurship, agency cost and firm performance: Evidence from developed and developing economies? Pakistan Journal of Commerce and Social Sciences, 9(3): 761-798.

[5] Sefiani, Y. (2013). Factors for success in SMEs: A perspective from Tangier. Doctoral Dissertation. University of Gloucestershire, Gloucestershire, England.

[6] Ferejo, M.N., Ahmed, H.M.S., Muzeyin, J.R., Amde, S.J, Thomran, M., Mamuye, F. (2022). Exploring factors affecting growth of micro and small enterprises: Evidence from Ethiopia. International Journal of Sustainable Development and Planning, 17(5): 1523-1533. https://doi.org/10.18280/ijsdp.170516

[7] Reichel, A., Haber, S. (2005). A three-sector comparison of the business performance of small tourism enterprises: An exploratory study. Tourism Management, 26(5): 681-690. https://doi.org/10.1016/j.tourman.2004.03.017

[8] Bendary, A., Minyawi, E. (2015). Entrepreneurial Competencies effect on Small and Medium Enterprises Performance through the mediation effect of Psychological Contracting of Outsourcing. International Journal of Business, and Economic Development, 3(2): 243-254.

[9] Oraya, N.A., Maina, S. (2023). Entrepreneurial competencies and organizational performance of micro and small enterprises in Machakos County, Kenya. International Academic Journal of Human Resource and Business Administration, 4(2): 257-272.

[10] Ibor, B.I., Offiong, A.I., Mendie, E.S. (2017). Financial inclusion and performance of micro, small and medium scale enterprises in Nigeria. International Journal of Research Granthaalayah, 5(3): 104-122. https://doi.org/10.5281/zenodo.439557

[11] Cámara, N., Tuesta, D. (2014). Measuring financial inclusion: A muldimensional index. BBVA Research Paper(14/26): 1-56. http://doi.org/10.2139/ssrn.2634616

[12] De la Torre, A., Martínez Pería, M.S., Schmukler, S.L. (2010). Bank involvement with SMEs: Beyond relationship lending. Journal of Banking & Finance, 34(9): 2280-2293. https://doi.org/10.1016/j.jbankfin.2010.02.014

[13] Nguyen, T., Tripe, D., Ngo, T. (2018). Operational efficiency of bank loans and deposits: A case study of vietnamese banking system. International Journal of Financial Studies, 6(1): 14. https://doi.org/10.3390/ijfs6010014

[14] Ayuba, B., Zubairu, M. (2015). Impact of banking sector credit on the growth of small and medium enterprises (SME’s) in Nigeria. Journal of Resources Development and Management, 15: 1-9.

[15] Kozolchyk, B. (1992). National law center/select advisory group rules and commentary on standby letters of credit: Presentation on the section devoted to the work of the national law center of inter-American free trade. Arizona Journal of International and Comparative Law, 9: 361.

[16] Kraemer, H., Lang, F. (2012). The importance of leasing for SME finance. Working Paper 2012/15 EIF Research & Market Analysis, Luxembourg.

[17] Deloof, M., Lagaert, I., Verschueren, I. (2007). Leases and Debt: Complements or substitutes? Evidence from Belgian SMEs. Journal of Small Business Management, 45(4): 491-500. https://doi.org/10.1111/j.1540-627X.2007.00224.x

[18] Zhu, Y., Wittmann, X., Peng, M.W. (2012). Institution-based barriers to innovation in SMEs in China. Asia Pacific Journal of Management, 29(4): 1131-1142. https://doi.org/10.1007/s10490-011-9263-7

[19] Zindiye, S., Chiliya, N., Masocha, R. (2012). The impact of government and other institutions' support on the performance of small and medium enterprises in the manufacturing sector in Harare, Zimbabwe. International Journal of Business Management & Economic Research, 3(6): 655-667.

[20] Khanal, A.R., Mishra, A.K., Koirala, K.H. (2015). Access to the Internet and financial performance of small business households. Electronic Commerce Research, 15(2): 159-175. https://doi.org/10.1007/s10660-015-9178-3

[21] Smallbone, D., Welter, F. (2001). The role of government in SME development in transition economies. International Small Business Journal, 19(4): 63-77. https://doi.org/10.1177/0266242601194004

[22] Mckinney, P. (2010). What is the role of the government to encourage small business innovation? Retrieved 23 April, 2023.

[23] Scott, W.R. (2008). Institutions and Organizations: Ideas and Interests: Sage.

[24] Boyatzis, R.E., Goleman, D., Rhee, K. (2000). Clustering competence in emotional intelligence: Insights from the Emotional Competence Inventory (ECI). Handbook of emotional intelligence, 99(6): 343-362.

[25] Zubaidah, R., Haryono, S., Udin, U. (2021). The effects of principal leadership and teacher competence on teacher performance: The role of work motivation. Quality – Access to Success, 22(180): 91-96.

[26] Boyatzis, R.E. (2008). Competencies in the 21st century. Journal of Management Development, 27(1): 5-12. https://doi.org/10.1108/02621710810840730

[27] Hazlina Ahmad, N., Ramayah, T., Wilson, C., Kummerow, L. (2010). Is entrepreneurial competency and business success relationship contingent upon business environment? International Journal of Entrepreneurial Behavior & Research, 16(3): 182-203. https://doi.org/10.1108/13552551011042780

[28] Shahab, M.A., Putra, M.A., Udin, U. (2022). Strengthening social capital to increasing farmers' entrepreneurial ability. Quality – Access to Success, 23(187): 200-208. https://doi.org/10.47750/QAS/23.187.25

[29] Udin, U. (2022). Knowledge sharing and innovative work behavior: Testing the role of entrepreneurial passion in distribution channel. Journal of Distribution Science, 20(2): 79-89. http://doi.org/10.15722/jds.20.02.202202.79

[30] Wang, J.X., Mangmeechai, A. (2022). Impact of entrepreneurship knowledge literacy curriculum on college graduates’ sustainable entrepreneurial competence based on entrepreneurial learning theory. International Journal of Sustainable Development and Planning, 17(4): 1309-1316. https://doi.org/10.18280/ijsdp.170428

[31] Muafi, Sanusi, Z.M., Roostika, R. (2023). Digital skills, digital entrepreneurship, job satisfaction, and sustainable performance of MSMEs: A survey on MSMEs in Indonesia. International. Journal of Sustainable Development and Planning, 18(2): 465-473. https://doi.org/10.18280/ijsdp.180215

[32] Segal, G., Borgia, D., Schoenfeld, J. (2005). The motivation to become an entrepreneur. International Journal of Entrepreneurial Behavior & Research, 11(1): 42-57. https://doi.org/10.1108/13552550510580834

[33] Draksler, T.Z., Širec, K. (2018). Conceptual research model for studying students’ entrepreneurial competencies. Naše Gospodarstvo/Our Economy, 64(4): 23-33.

[34] Sánchez, J.C. (2013). The Impact of an Entrepreneurship Education Program on Entrepreneurial Competencies and Intention. Journal of Small Business Management, 51(3): 447-465. https://doi.org/10.1111/jsbm.12025

[35] Hadi, N., Udin, U. (2020). Testing the effectiveness of CSR dimensions for small business entrepreneurs. Journal of Open Innovation: Technology, Market, and Complexity, 7(1): 6. https://doi.org/10.3390/joitmc7010006

[36] Gerli, F., Gubitta, P., Tognazzo, A. (2011). Entrepreneurial competencies and firm performance: An empirical study. Paper presented at the VIII International Workshop on Human Resource Management.

[37] Gadi Djou, L., Udin, U., Lukiastuti, F., Filatrovi, E.W. (2020). The contingency approach of digitalization and entrepreneurial orientation on smes performance in metal and machinery industry. International Journal of Criminology and Sociology, 9: 2235-2249.

[38] Mohamad, M.R., Sidek, S. (2013). The role of entrepreneurial competencies as a mediator in the relationship between microfinance and small business growth. Journal of Entrepreneurship and Business, 1(1): 21-31.

[39] Sarwoko, E., Surachman, A., Hadiwidjojo, D. (2013). Entrepreneurial characteristics and competency as determinants of business performance in SMEs. IOSR journal of Business and Management, 7(3): 31-38.

[40] Sekaran, U., Bougie, R. (2016). Research Methods for Business: A Skill Building Approach. John Wiley & Sons.

[41] Williams, B., Onsman, A., Brown, T. (2010). Exploratory factor analysis: A five-step guide for novices. Australasian Journal of Paramedicine, 8: 1-13. https://doi.org/10.33151/ajp.8.3.93

[42] Lingesiya, Y. (2012). Identifying factors to indicate the business performance of small scale industries: Evidence from Sri Lanka. Global Journal of Management and Business Research, 12(21): 75-82.

[43] Kyndt, E., Baert, H. (2015). Entrepreneurial competencies: Assessment and predictive value for entrepreneurship. Journal of Vocational Behavior, 90: 13-25. https://doi.org/10.1016/j.jvb.2015.07.002

[44] Mishra, C.S., Zachary, R.K. (2015). The theory of entrepreneurship. Entrepreneurship Research Journal, 5(4): 251-268. https://doi.org/10.1515/erj-2015-0042

[45] Yazdanfar, D., Öhman, P. (2015). Debt financing and firm performance: An empirical study based on Swedish data. The Journal of Risk Finance, 16(1): 102-118. https://doi.org/10.1108/JRF-06-2014-0085

[46] Kline, R.B. (2023). Principles and Practice of Structural Equation Modeling. Guilford publications.

[47] Tam, L.T., Ngan, N.P., Trung, N.T., Minh, C.P. (2020). Banking relationship ties to firm performance: Evidence from food and beverage firms in Vietnam. Journal of Economics and Business, 3(2): 602-616. https://doi.org/10.31014/aior.1992.03.02.224