Achmad Kautsar*![]() | Ina Uswatun Nihaya

| Ina Uswatun Nihaya![]() | Tias Andarini Indarwati

| Tias Andarini Indarwati![]()

© 2023 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Against the backdrop of the existence of a dividend policy that can provide investors with a variety of signals, the objective of this study is to determine the dividend policy in the Indonesian agricultural sector, given the sector's pronounced volatility between 2014 and 2021. This is what causes the agricultural sector to experience the greatest volatility compared to other sectors. This research develops a dividend policy model with moderating variables, namely liquidity, and mediating variables, namely profitability, in response to a number of gaps in the existing literature. The method employed is quantitative explanation with purposive sampling technique. This study employs path analysis by means of the SEM method and STATA version 14. The results indicate that leverage and firm size have a negative impact on dividends, while profitability has no bearing on dividend policy. Other results indicate that leverage has no effect on profitability, while firm size has a negative effect. The failure of the moderation and mediation tests is caused by the absence of profitability's effect on dividends.

dividend policy model, liquidity, profitability, dividend payout ratio, return on assets, debt to equity ratio, current ratio, agriculture sector

The dividend policy has been demonstrated to stimulate investors. Diverse stimuli provided by the company's dividend policy can influence the decisions and interests of investors. In return for their investment in the company's shares, shareholders receive dividends, which represent a fraction of the business's profits [1]. Dividend policy refers to the determination of how much dividend will be distributed to investors and ratio of dividends paid to stockholders as a performance metric. Investors focus on dividend policy as an indicator of company performance and management's commitment to the company's long-term viability [2].

Sumber: Indonesian Stock Exchange Website.

Figure 1. Graph of the dividend payout ratio

Figure 1 depicts the evolution of the average dividend payout ratio for nine company sectors in Indonesia from 2014 to 2018. The nine company sectors exhibited fluctuations, as demonstrated by this graph. In 2015, however, the agricultural sector marked in light blue experienced extreme fluctuations, falling to -86.78% from 33.87% in 2014. This is what caused the agricultural sector to experience the greatest volatility compared to other industries.

The dividend payout ratio for agricultural businesses reached a value of -86.78 percent in 2015, despite the fact that a few of these businesses had continued to pay dividends despite experiencing a decline in profitability. Related to 2017 data from the Indonesian Ministry of Agriculture that the Indonesian government made tremendous efforts in 2017 to make the agriculture sector one of the economy's pillars and top priority. To increase agricultural exports, the Indonesian government enacted policies such as the export process policy, which allowed exports to go directly to the destination country without passing through a transit country, and increased diplomatic relations with China in order to simplify the process of obtaining an export license. Both of these policies were successful in increasing agricultural exports. The gross domestic product of the agricultural industry in 2018 was 1,005.4 trillion Indonesian rupiah, which is an increase over 2017's figure of 968.8 trillion. The agricultural sector has achieved positive growth in gross domestic product, which may have an effect on the ability of agricultural sector firms to pay dividends. As a result of these policies and efforts, greatest volatility occurred in the agricultural industry.

Leverage is one of many elements that have a role in dividend policy. In the event of liquidation, leverage is a metric used to assess the company's ability to meet all of its debts, including current and prospective [3]. According to research by Puspita [4], the dividend payout ratio improves noticeably with increased use of leverage. In contrast, Sabrina [5], provide evidence that the dividend payout ratio suffers when leverage is present.

Firm size also influences dividend policy. Large businesses typically do not experience financial challenges since they have easier access to the capital market, giving them a larger chance to obtain finance support [6]. It is easier for larger businesses to meet their funding requirements [7]. According to the findings of Nuraini [8], the dividend payout ratio does not vary much with the size of a company. Arfianny [9] suggests that dividend payout ratios are significantly impacted by firm size in a negative way.

Profitability is also mentioned as a factor that affects dividend policy. Using return on assets as a metric, profitability is quantified. The ratio of a company's earnings to its total assets demonstrates its ability to turn a profit after taxation [10]. According to the findings of Chandra and Junita [11], Increasing dividend payment ratios are one of the most direct results of increased profits. The company's performance and profitability are capable of increasing the dividend payout ratio [12-14]. In contrast, Nurwani [15] found that dividend payout ratio is significantly impacted by profitability in a manner that is counterproductive.

Profitability has significant significance for the company as a basis for evaluating its condition, performance, and performance. The company's liabilities are one of the factors that influence its profitability. There are numerous methods for determining a company's level of liability, one of which is the debt-to-equity ratio. According to the findings of another study, carried out by Wikardi and Wiyani [16], using leverage has a large and detrimental effect on return on assets. Gunde et al. [17] discovered that leverage significantly increases return on assets. The results of are in agreement with Pramesti et al. [18], who concluded that company obligations have a positive effect on company profitability.

According to research by Pradnyanita et al. [19], the size of a company is used to indicate whether the company's equity is increasing or decreasing. According to Suryati and Yetti [20] and Kausar [21], the larger a company is, the higher its profits tend to be, as measured by return on assets. These findings are supported by Pramesti et al.'s assertion that company size is capable of increasing the return on assets ratio [18]. Contrast these findings with those of Lorenza et al. [22], who found that firm size has no effect on profitability as calculated based on return on assets.

This research employs return on assets ratio (ROA) as a mediating variable. According to the findings of Rohaeni and Ma'mun [23], the return on assets ratio cannot mediate the effect of leverage on the dividend payout ratio.

This research makes use of the current ratio as a moderating variable. The current ratio is the ratio of current assets to current liabilities and is used to evaluate a company's liquidity [10]. According to research by Salsabilla and Isbanah [24], liquidity as measured by the current ratio can moderate dividend policy profitability. Different results were proposed by Yunisari and Ratnadi [25], who claimed that the current ratio, an indicator of liquidity, had no bearing on profitability to dividend policy.

The dividend payout ratio value in Indonesia's agricultural sector has been shown to be on the rise, according to the data presented. research gaps, and the role of liquidity profitability in influencing company dividend policy, this stimulates interest in researching the dividend policy model in agricultural companies in Indonesia by mediating profitability and liquidity moderation. The urgency of this research stems from the need to develop a dividend policy model with profitability as a mediating variable and liquidity as a moderating variable in order to expand the scope of dividend policy research topics.

2.1 Pecking order theory

Organizational funding follows pecking order theory. This model requires companies to invest and pay dividends with their own capital [26]. It balances reality [27]. Financial market asymmetric theory popularized the pecking order hypothesis. Managers and investors access information differently, creating a gap [28]. Due to information asymmetry, companies choose internal financing over external, which raises capital costs and affects dividend policies [29].

2.2 Firm life cycle theory

Mueller [30] proposed the Firm Life Cycle Theory regarding dividend payments, which proposes that a company's dividend policy should be dependent on its life cycle. Agency problems are the focal point of Firm Life Cycle Theory. Agency issues are the focus of the company's life cycle theory because agency issues are believed to arise frequently in the early phases of a company's development. During the growth phase of a business, the organization expands and the owner begins to delegate control to the management. Managers will tolerate a greater degree of delegated decision-making and will re-emerge as decision-makers. Management must be able to boost the company's development and profitability in order to maximize shareholder value. There will be agency issues if the management is incapable of delegating effectively and disregards the interests of the shareholders [31].

The life cycle theory provides insight into the emergence of the company's birth phase, growth phase, maturity phase, peak phase, and decline phase. Investors are required to understand the transformation process of companies that will become investment targets [32].

2.3 Dividend policy

Stockholders are rewarded for their investment in a firm by receiving a dividend, which is a portion of the company's profits [1]. In the end, the company's decision regarding the number of dividends to distribute to investors is known as the dividend policy, which can be quantified using the dividend payout ratio. The dividend payment dynamics in developing country markets differ from those in developed countries due to differences in ownership structures and inadequate legal protection governance [33]. A substitute for legal protection for minority investors is dividends. When a company needs capital and offers attractive terms, it must pay high dividends as a reputation-building measure to alleviate investor concerns and minimize agency issues [34].

2.4 Leverage

The leverage variable, as measured by debt-to-equity ratio which shows a company's ability to meet its obligations based on how much of its capital it uses to pay debts. A rise in debt will reduce the net profit available to shareholders, including dividends, because the obligation to pay debts takes precedence over dividend distribution [35].

Companies prefer to invest using retained earnings and other internal funding sources rather than with external funding sources, as suggested by the pecking order theory. Consequently, companies with a high level of leverage are highly dependent on retained earnings, which prevents profits from being distributed as dividends [36].

A company's debt equity ratio indicates its stability, which is determined by its ability to pay interest on its debts and pay these debts on time [37].

2.5 Firm size

Most of the time, dividends from large companies are bigger than dividends from small companies. This is because it is easier for companies with a lot of assets to get into the capital market. This is consistent with the hypothesis of the life cycle of a company, which states that after a corporation has reached maturity, it tends to have high free cash flow and a low growth rate, so mature companies pay higher dividends than young companies. How easy it is for a company to get money from the capital market can depend on how big the company is. Most small businesses can't get bonds or stocks through organized capital markets [38].

2.6 Profitability

The return on asset ratio measures how well a company can use all of its assets to make a profit after taxes. This is what the profitability variable means. Return on assets ratio indicates the efficiency with which a business generates profits. If a company is typically steady or has a higher level of profitability, it has the potential to pay out larger dividends. Nevertheless, if the company's profitability declines, it will be unable to pay dividends to its shareholders. This demonstrates a positive relationship between dividend policy and profitability [11-14]. In light of this, we can draw the conclusion that dividends rise together with the rate of return on a company's assets [39]. Following the hierarchical idea of the pecking order, the order of company funding is from cheapest to most expensive: profit, debt, and issuance of shares. To pay dividends, i.e., profits, corporations will use the cheapest funding [40].

2.7 Liquidity

In order to determine whether or not a corporation can meet its short-term obligations, analysts look at the current ratio [10]. This ratio is used as a proxy for a company's capacity to meet its short-term obligations due within a year. It is acceptable and indicative of a healthy company if the current ratio is at or above the average for its industry [41]. If a company's current ratio is high, that means it has plenty of cash on hand.

3.1 Leverage and dividend policy

The dividend payout ratio is significantly impacted favorably by leverage [4]. Companies with a high level of leverage are an indication that the company is developing and expanding, necessitating multiple funding sources for all company activities [42].

Facts and other research findings indicate that when a company has more debt or obligations that must be financed, this will automatically result in a reduction of dividends to shareholders [43]. In order to minimize external funding, companies with high levels of leverage tend to have low dividend payout policies [44]. Reduced dividend payout ratios are a direct result of increased leverage. Consequently, a larger debt-to-equity ratio has a negative impact on a company's health, and a higher debt composition reduces its dividend-paying capacity [5]. A high level of leverage indicates that a corporation is relying excessively on borrowed funds to fund its operations, it becomes a separate financial pressure, causing it to allocate funds or profits received to pay debts rather than dividends [45]. In addition, conclusive evidence to support the relationship between leverage and dividend policy has not been found [46]. Little or no influence is exerted by leverage on dividend policy [47].

H1: Leverage has a significant effect on dividend policy

3.2 Firm size and dividend policy

The dividend policy of a company tends to improve as the company grows in size [38], and raise dividend payments [48]. Companies with a large size are mature and have stable financial health, so they have easy access to external capital markets to obtain external funding and are not wholly reliant on internal funding. Ultimately, these companies can take advantage of their large profits to pay out large dividends. bigger.

Compare these results to those that indicate dividend policy is adversely affected by a company's size [49], because of the increased costs associated with expanding, many large corporations would rather reduce the amount of money they hand out in dividends to their shareholders [7]. In addition, the findings of other studies indicate that size has a favorable relationship with dividends [21]. Apart from that, further results are stated that size of the company does not have any bearing on the dividend policy [50]. There is no correlation between the total value of the assets held by the company and the number of dividends paid out to shareholders [8].

H2: Firm size has a significant effect on dividend policy.

3.3 Profitability and dividend policy

Internal financing is the preferred method for financing business activities, followed by debt and equity financing [51]. When a company's profitability rises, it tends to increase dividend distribution [52]. To a large extent, the dividend payout ratio is negatively affected by the return on assets [15]. The dividend payout ratio can be increased by a company's profitability [11-14]. In terms of dividend policy, the dividend payout ratio is stated to be positively influenced by profitability, as measured by return on assets [13].

Another finding shows that dividend payout ratios tend to drop precipitously when profits rise [15], which means that the level of company profitability can affect the amount of dividends that will be distributed to shareholders.

H3: Profitability has significant effect on dividend policy.

3.4 Leverage and profitability

Therefore, companies with high leverage have a lower average performance [53] because they have a greater probability of default. According to intriguing findings [54], when it comes to local profits, leverage is detrimental, but when it comes to overseas earnings, it can be rather beneficial.

Contrast these findings with assertion that using leverage can significantly boost financial returns [17]. According to additional findings [19, 55, 56], that a large reduction in ROA might be expected if leverage is present. The more the leverage, the greater the amount of potentially harmful debt a corporation is carrying.

H4: Leverage has significant effect on profitability.

3.5 Firm size and profitability

Growing businesses tend to be more successful than smaller ones, so the larger the company, the greater its profitability [20]. The larger the corporation, the more it can accomplish economically. So that large businesses are more likely to generate greater profits [57].

The size of a company has a negative effect on profitability, according to another finding [58]. However, contrary to what was expected, business size did not significantly affect profitability as assessed by return on assets [22], we find the opposite to be true. Profitability generated by a business is unaffected by the size of the business [59].

H5: Firm size has significant effect on profitability.

3.6 Leverage, profitability, and dividend policy

The obligation to pay debts takes precedence over the distribution of dividends, so the size of the dividend will be impacted when there is an increase in the amount of debt [35]. It is generally agreed that return on assets cannot act as a buffer between leverage and the dividend payout ratio [60]. When a corporation's earnings are high enough to encourage an increase in dividend payments, with the presumption that an increase in a company's profits will serve as a trigger for the company to increase the number of dividends distributed to shareholders. Companies that are able to generate profits from the results of both internal financing and external financing in the form of debt will also have the ability to affect the size of dividend distributions [61].

H6: Profitability mediates the effect of leverage on dividend policy.

3.7 Firm size, profitability, and dividend policy

It seems that profit, as calculated by return on assets, can moderate the effect of firm size on the dividend payout ratio [62]. This contradicts the conclusion [23] that profitability assessed by return on assets cannot mediate the effect of firm size on the dividend payout ratio. This indicates that a company's size and profitability are not sufficient to guarantee that it will issue cash dividends.

H7: Profitability mediates the effect of firm size on dividend policy.

3.8 Profitability, liquidity, and dividend policy

The liquidity shown by the current ratio can mitigate the dividend payout ratio's impact on profitability [24]. Contrary to the results of research which suggests that liquidity as described by the current ratio cannot moderate profitability on dividend policy [25]. Good company liquidity conditions are expected to maintain its performance and develop its business and motivate management to pay dividends. Therefore, liquidity will be a good link between company profitability and dividend policy [63].

H8: Liquidity mediates the effect of profitability on dividend policy.

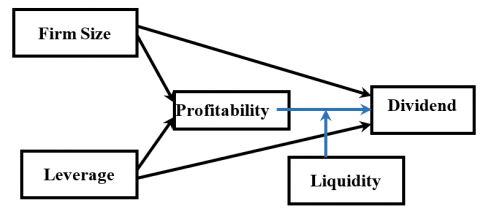

The image below depicts the study's theoretical underpinnings and key hypotheses:

Figure 2. Research framework

Figure 2 depicts the current research structure. Using data from the Indonesian agricultural sector, this study examines the moderating role of liquidity and the mediating role of profitability between the effect of firm size and leverage on dividends.

4.1 Research method

Quantitative research is defined as a research method that is based on the philosophy of positivism and is used to examine a specific population or sample, collect data using research instruments, and analyze data quantitatively and statistically to test preconceived hypotheses. This research is included in the category of conclusive research with the type of causality research. Path analysis is the analytical method chosen for efforts to solve complex research models involving not only dependent and independent, but also moderating and mediating variables. Path analysis uses STATA software version 14 to answer the relationship between the various variables investigated in this study. Path analysis is beneficial since it permits researchers to dissect or divide the numerous factors influencing a result into direct and indirect components [64].

When path analysis is used to test hypotheses, SEM offers a number of advantages not accessible with conventional techniques. Using a SEM analysis, not only can the descriptive power of alternative models be compared, but the results can also refer to further observations or crucial experiments that may boost comprehension and would not otherwise be conducted. Consequently, not only may SEM be used to assess theories, but also to assist enhance them [65].

4.2 Population and sample

This study's population consists of agricultural firms listed on the IDX (Indonesian Stock Exchange) between 2014 and 2021. This study's population consists of 25 agricultural firms. This study employs a non-probabilistic purposive sampling technique with the following sample criteria: (1) agricultural companies listed on the Indonesia Stock Exchange between 2014 and 2021; (2) companies that uploaded consecutive financial reports for 2014-2021; and (3) agricultural companies that paid dividends at least three times during 2014-2021. The purposive sampling method was selected since not all agricultural enterprises typically pay dividends during the time period of the study. As a consequence of this, the inclusion of the third criterion results in a population of 25 companies having only 10 companies left to sample. In addition, the reasons for selecting purposive sampling include its low cost, its usability, and the fact that researchers can use it to support selections made according to analytical, logical, or theoretical criteria [66].

Eight years' worth of study resulted in the collection of eighty sets of panel data, all of which were then analyzed using the STATA program. Documentation, more specifically secondary data collection in the form of annual financial reports acquired from the Indonesia Stock Exchange, was the technique of choice for the data collection process.

Table 1. Description of variables and measurements

|

No |

Dependent Variable |

Measurement |

|

1. |

Dividend Policy |

Dividend Payout Ratio (DPR) = Earnings Per Share/Dividend Per Share |

|

|

Independent Variable |

|

|

2. |

Leverage |

Debt Equity Ratio (DER) = Total Debt/Total Equity |

|

3. |

Firm Size |

Size = Ln (Total Asset) |

|

|

Moderating Variable |

|

|

4. |

Profitability |

Return on Asset (ROA) = Earnings After Tax/Total Asset |

|

|

Mediating Variable |

|

|

5. |

Liquidity |

Current Ratio = Current Asset/Current Debt |

Table 1 depicts the variables utilised in the study, namely dividend policy, leverage, firm size, profitability, and liquidity, along with specific measurements for each variable.

5.1 Descriptive statistics

According to the descriptive statistics, the dividend payout ratio has an average value of 0.263, with a maximum of 10.32 and a minimum of -6.43. This value indicates that the average agricultural company distributes 26.3% of its net income as dividends. The investment variable has a standard deviation of 1.440, or 144% (above 100%), indicating that the distribution of dividend payout ratio (DPR) data between observations is variable.

The average leverage value is 1.039. The maximum leverage value is 2.68 and the minimum leverage value is 0.15. This value indicates that, on average, agricultural companies use more debt than equity to fund their operations. The investment variable has a standard deviation of 0.735, or 73.5 percent (below 100%), indicating that the distribution of leverage data between observations is not overly variable.

The average size of agricultural companies in Indonesia is 16.273, with the smallest size being 14.44 and the largest being 137.51. This indicates that agricultural companies in Indonesia are of comparable size, as the difference between the minimum and maximum values is small.

ROA has a mean value of 0.053 with a maximum value of 0.18, and a minimum value of -0.02. This value indicates that the average agricultural enterprise can generate a net profit of 5.3 percent utilizing its total assets. The investment variable has a standard deviation of 0.043, or 4.3% (below 100%), indicating that the distribution of ROA data between observations is not overly variable.

As measured by the current ratio (CR), the average liquidity of agricultural companies is 2.209, with a maximum of 7.44 and a minimum of 0.50. This demonstrates that the typical agricultural company has excellent liquidity. The investment variable has a standard deviation of 1.831, or 183.1% (above 100%), indicating that the distribution of CR data between observations varies.

Table 2. Descriptive statistics

|

Var. |

Obs. |

Mean |

St Dev. |

Min |

Max |

|

DPR |

80 |

0.263 |

1.440 |

-6.43 |

10.32 |

|

LEV |

80 |

1.039 |

0.735 |

0.15 |

2.68 |

|

SIZE |

80 |

16.273 |

0.763 |

14.44 |

17.51 |

|

ROA |

80 |

0.053 |

0.043 |

-0.02 |

0.18 |

|

CR |

80 |

2.209 |

1.831 |

0.58 |

7.44 |

Table 2 depicts descriptive statistics for the research data, including the number of observations, mean, standard deviation, minimum, and maximum values.

5.2 Regression analysis

The coefficient for the p-value of leverage on dividends is -2.34, as shown in Table 3. It is proven that leverage significantly reduces the dividend payout ratio (DPR). Al-Malkawi [67], Gonzalez et al. [68], Al-Malkawi [69], Hashemi [70], John and Muthusamy [71], Gupta and Banga [72], and Al-Shubiri [73] all found similar results. According to them, the company's operational activities that payments to shareholders are minimal. The size of the company's debt will reduce its dividend-paying capacity.

The coefficient for the p-value of firm size to dividends is -2.34, as shown in Table 3. In accordance with the findings of Banerjee [51], Al-Shubiri [73], and Afza and Mizan [74], this result is conceivable due to the fact that it is stated that large companies can allocate their funds to multiple investments or future expansion, thereby reducing the likelihood of dividend payments. Also contributing to this outcome is the fact that a larger company will incur greater operational costs as it grows, which will inevitably reduce the dividend payout to shareholders. According to Eltya et al. [75], the stakes are higher when a corporation has more assets at risk.

Profitability has no effect on dividend policy, according to the study's findings, because companies with high profits tend not to pay dividends and instead retain these profits as a future investment model. These findings are consistent with the findings of Afza and Mizan [74], Adil et al. [76], and Anil and Kapoor [77], who concluded that profitability has no effect on dividend policy, as measured by the dividend payout ratio.

The study found that using debt did not increase profits, as the size of a company's debt cannot affect profitability. According to research conducted by Maulita and Tania [78], Dissanayake [79], Velnampy and Niresh [80], and Amidu [81], leverage has no effect on profitability.

According to the findings, a company's profitability decreases as its size increases, with the explanation that companies must adjust company size and operational costs in order to increase return on assets [53, 54]. The greater the company's size, the greater its scope and economic activity. Consequently, there is a chance that large companies will generate a smaller profit as well. These findings are consistent with Bilal [82].

The fact that the p-value of the Sobel test for mediation of profitability is greater than 0.050 indicates that profitability cannot serve as a mediator between leverage and dividends. The research of Rohaeni and Ma'mun [23] indicates that ROA profitability cannot mediate the effect of firm size on the dividend payout ratio. This result cannot be separated from the absence of profitability leverage, so the mediation role of profitability cannot be demonstrated.

The fact that the p-value of the Sobel test for mediation of profitability is greater than 0.050 indicates that profitability cannot serve as a mediator between firm size and dividends. This result is consistent with the findings of Rohaeni and Ma'mun [18], who found that ROA profitability cannot mediate the effect of firm size on the dividend payout ratio. This shows that a company's size and profitability are no guarantee that it will pay dividends to shareholders in the form of cash.

The results of the moderated regression analysis (MRA) test of liquidity moderation indicate that liquidity cannot strengthen or weaken the effect of firm size on dividends. According to research conducted by Yunisari and Ratnadi [25], liquidity as described by the current ratio cannot moderate profitability in relation to the dividend payout ratio. This suggests that there will be no rise in dividend payments due to liquidity when company profitability is high and cannot decrease dividend payments when company profitability is low. So, the size of liquidity as measured using the current ratio cannot give a strengthening or weakening effect.

Table 3. Hypothesis testing and result

|

Variables |

DPR |

ROA |

||

|

|

Coef |

Sig |

Coef |

Sig |

|

LEV |

-0.075 |

-0.59 |

-0.356 |

-2.34 |

|

|

|

0.556 |

|

0.019* |

|

SIZE |

-0.389 |

-3.22 |

-0.414 |

-2.43 |

|

|

|

0.001* |

|

0.015* |

|

ROA |

|

|

-0.183 |

-1.04 |

|

|

|

|

|

0.299 |

|

LEV*ROA*DPR |

|

|

0.014 |

0.51 |

|

|

|

|

|

0.609 |

|

SIZE*ROA*DPR |

|

|

0.071 |

0.99 |

|

|

|

|

|

0.322 |

|

ROA*CR |

|

|

0.016 |

-0.042 |

|

|

|

|

|

0.074 |

|

R-Square |

0.228 |

0.494 |

||

Note: ***, **, * shows the significance of the coefficients at the level of 1%, 5%, 10%.

Table 3 depicts the findings from the study's hypothesis testing.

The findings demonstrate that there is conclusive evidence that leverage can have an adverse effect on dividend policy. If an organization has a low debt-to-equity ratio, there is a greater chance that it will pay dividends to shareholders. Investors should favor those kinds of businesses. In order for agricultural businesses to be in a position to boost their dividends, the company's debt should first be paid down. This will result in lower interest costs for the business as well as a larger portion of profits that dividends are a sort of financial compensation that may be paid out to shareholders. Because it has been demonstrated that the dividend policy of a company tends to decline as it grows larger. The findings of this study are readily apparent from the research data, which indicates that when the company's assets decrease, their dividends increase, while on the other hand, when the company's assets increase, the dividends distributed are lower than they were the year before.

6.1 Implications of study

The findings of this study imply, furthermore, that the magnitude of a company's profitability is unable to exert any influence over dividend policy. Additionally, the leverage ratio is unable to exert any influence on the magnitude of the company's profits. Several studies have found that the size of an organization has an impact on its profitability. The company's size can play a major role in how well it is able to run its business and make a profit. Due to the fact that partial profitability did not have an effect on dividends, it was determined that partial profitability could not act as a mediating factor between the effect of firm size and leverage on dividends. The results of this test were reported as being inconclusive. Another significant finding from this investigation demonstrates that liquidity cannot act as a moderator between dividend policy and profitability. The implications of this study's conclusions for agricultural businesses are that they must reduce their wasteful use of assets, which will lead to a decline in corporate profitability and dividends. In order to improve profits and dividend distribution, businesses must truly move swiftly and optimize their assets through competent management.

6.2 Limitation and further study

Indonesia's agricultural sector provides minimal data for research. Thus, the conclusions are restricted to the agricultural sector of underdeveloped nations. It is recommended that future researchers perform studies encompassing a greater number of business sectors in both emerging and wealthy nations. Future study should include profitability as the primary determinant influencing dividend policy. Future research can include other variables that can influence dividend policy, such as free cash flow, ownership structure, asset structure, and other variables outside the scope of this study, in order to investigate additional variables that can impact dividend policy. This study employs moderators and restricted mediators to examine the relationship between profitability and liquidity; therefore, it is suggested that additional factors be used to obtain more precise and meaningful findings.

[1] Rudianto. (2017). Pengantar Akuntasi Konsep & Teknik Penyusunan Laporan Keuangan, Erlangga, Jakarta.

[2] Puspitaningtyas, Z. (2017). Efek Moderasi Kebijakan Dividen Dalam Pengaruh Profitabilitas Terhadap Nilai Perusahaan. Jurnal Akuntansi, Ekonomi Dan Manajemen Bisnis, 5(2): 173-180. https://doi.org/10.30871/jaemb.v5i2.538

[3] Kasmir. (2017). Analisis Laporan Keuangan. PT Rajagrafindo Persada. Jakarta.

[4] Puspita, E. (2017). Pengaruh likuiditas, profitabilitas, leverage, dan market ratio terhadap dividend payout ratio pada perusahaan manufaktur. Ekuilibrium: Jurnal Ilmiah Bidang Ilmu Ekonomi, 12(1): 17-35. https://doi.org/10.24269/ekuilibrium.v12i1.420

[5] Sabrina, V. (2019). Pengaruh leverage dan pertumbuhan aset terhadap kebijakan dividen pada perusahaan manufaktur yang terdaftar di bei. Jurnal Pendidikan Akuntansi & Keuangan, 5(2): 89-97. https://doi.org/10.17509/jpak.v5i2.15407

[6] Siahaan, F.O. (2014). The effect of good corporate governance mechanism, leverage, and firm size on firm value. GSTF Journal on Business Review (GBR), 2(4): 137-142. https://doi.org/10.5176/2010-4804_2.4.263

[7] Beck, T., Demirgüç-Kunt, A., Maksimovic, V. (2008). Financing patterns around the world: Are small firms different?. Journal of Financial Economics, 89(3): 467-487. https://doi.org/10.1016/j.jfineco.2007.10.005

[8] Nuraini, M.W. (2021). Pengaruh leverage terhadap kebijakan dividen dengan firm size dan profitabilitas sebagai variabel mediasi pada perusahaan sektor agrikultur di bei tahun 2014-2018. Jurnal Ilmu Manajemen, 9(2): 412-425. https://doi.org/10.26740/jim.v9n2.p412-425

[9] Arfianny, A. (2020). Factors affecting payout ratio dividends with foreign ownership as moderating variables in manufacturing companies in Indonesia stock exchange. International Journal of Public Budgeting, Accounting and Finance, 3(1): 215-226.

[10] Sudana, I.M. (2011). Manajemen Keuangan Perusahaan Teori & Praktik. Erlangga. Jakarta.

[11] Chandra, B., Junita, N. (2021). Tata kelola perusahaan dan manajemen laba terhadap kebijakan dividen di Indonesia. Jurnal Ekonomi Modernisasi, 17(1): 15-26. https://doi.org/10.21067/jem.v17i1.5188

[12] Silviana, W., Adi, S.W. (2021). Impact of liquidity, solvency, profitability, company growth, and size of the company against the dividend policy. In Annual Conference of Ihtifaz: Islamic Economics, Finance, and Bankin, pp. 367-380.

[13] Romus, M., Anita, R., Abdillah, M.R., Zakaria, N.B. (2020). Selected firms environmental variables: Macroeconomic variables, performance and dividend policy analysis. In IOP Conference Series: Earth and Environmental Science, 469(1): 012047. https://doi.org/10.1088/1755-1315/469/1/012047

[14] Kautsar, A. (2019). Profitability is a mediation variable of debt on dividend payout indonesian agriculture companies. Journal Scholars Journal of Economics, Business and Management, 6(2): 143-146.

[15] Nurwani. (2017). Pengaruh rasio likuiditas dan profitabilitas terhadap kebijakan dividen: Studi pada perusahaan manufaktur yang terdaftar di bursa efek Indonesia. Jurnal Riset Finansial Bisnis, 1(1): 1-8. https://doi.org/10.5281/zenodo.1066324

[16] Wikardi, L.D., Wiyani, N.T. (2017). Pengaruh debt to equity ratio, firm size, inventory turnover, assets turnover dan pertumbuhan penjualan terhadap profitabilitas (Studi kasus pada industri makanan dan minuman yang terdaftar di bei periode 2011-2015). Jurnal Online Insan Akuntan, 2(1): 99-118.

[17] Gunde, Y.M., Murni, S., Rogi, M.H. (2017). Analisis pengaruh leverage terhadap profitabilitas pada perusahaan manufaktur sub industri food and beverages yang terdaftar di bei (Periode 2012-2015). Jurnal EMBA: Jurnal Riset Ekonomi, Manajemen, Bisnis Dan Akuntansi, 5(3). https://doi.org/10.35794/emba.5.3.2017.18382

[18] Pramesti, D., Wijayanti, A., Nurlaela, S. (2016). Pengaruh rasio likuiditas, leverage, aktitivitas dan firm size terhadap profitabilitas. Jurnal Seminar Nasional IENACO, 810-817.

[19] Pradnyanita Sukmayanti, N.W., Triaryati, N. (2018). Pengaruh struktur modal, likuiditas dan ukuran perusahaan terhadap profitabilitas pada perusahaan property dan real estate. E-Jurnal Manajemen Universitas Udayana, 8(1): 172-202. https://doi.org/10.24843/ejmunud.2019.v08.i01.p07

[20] Suryati, D., Yetti, F. (2019). Pengaruh firm size, debt ratio dan capital adequacy ratio terhadap profitabilitas. Equity, 18(2): 153. https://doi.org/10.34209/equ.v18i2.465

[21] Kautsar, A. (2014). Analisis pengaruh firm size, der, dan sales growth terhadap dividend payout ratio dengan roe sebagai variabel intervening pada perusahaan non keuangan yang listed di bei tahun 2009-2011. Jurnal Bisnis Strategi, 23(2): 1-13. https://doi.org/10.14710/jbs.23.2.1-13

[22] Lorenza, D., Kadir, M.A., Sjahruddin, H. (2020). Pengaruh struktur modal dan ukuran perusahaan terhadap profitabilitas pada perusahaan otomotif yang terdaftar di bursa efek Indonesia. Jurnal Ekonomi Manajemen, 6(1): 13-20.

[23] Rohaeni, N., Ma’mun, A.S. (2020). Pengaruh likuiditas dan ukuran perusahaan terhadap kebijakan dividen tunai dengan profitabilitas sebagai variabel intervening pada perusahaan index idx high dividen 20. Jurnal Bina Bangsa Ekonomika, 13(1): 38-46. https://doi.org/10.46306/jbbe.v13i1.30

[24] Salsabilla, N.F., Isbanah, Y. (2020). Pengaruh profitabilitas dan risiko bisnis terhadap dividend payout ratio melalui likuiditas sebagai variabel moderasi. Jurnal Ilmu Manajemen, 8(4): 1301. https://doi.org/10.26740/jim.v8n4.p1301-1311

[25] Yunisari, N.W., Ratnadi, N.M.D. (2018). Pengaruh profitabilitas dan kepemilikan manajerial pada kebijakan dividen dengan likuiditas sebagai variabel moderasi. E-Jurnal Akuntansi, 23: 379. https://doi.org/10.24843/eja.2018.v23.i01.p15

[26] Donaldson, G. (1961). Corporate debt capacity. A study of corporate debt policy and the determination of corporate debt capacity. (Second Printing). Division of Research, Graduate School of Business Administration, Harvard Univ.

[27] Myers, S. (1984). The capital structure puzzle. Journal of Finance, 39(3): 575-592. https://doi.org/10.3386/w1393

[28] Khalaf, B.A. (2022). An empirical investigation of the impact of firm life cycle using the pecking order theory. Academy of Entrepreneurship Journal, 28(1): 1-9.

[29] Kwak, G. (2021). Financing decision of high-tech SMEs in Korea: A revisitation to pecking order theory. Applied Economics Letters, 28(16): 1400-1406. https://doi.org/10.1080/13504851.2020.1820437

[30] Mueller, D.C. (1972). A life cycle theory of the firm. The Journal of Industrial Economics, 20(3): 199-219. https://doi.org/10.2307/2098055

[31] Miller, D., Friesen, P.H. (1984). A longitudinal study of the corporate life cycle. Management Science, 30(10): 1161-1183. https://doi.org/10.1287/mnsc.30.10.1161

[32] Primc, K., Kalar, B., Slabe-Erker, R., Dominko, M., Ogorevc, M. (2020). Circular economy configuration indicators in organizational life cycle theory. Ecological Indicators, 116: 106532. https://doi.org/10.1016/j.ecolind.2020.106532

[33] Khan, A. (2022). Ownership structure, board characteristics and dividend policy: Evidence from Turkey. Corporate Governance: The International Journal of Business in Society, 22(2): 340-363. https://doi.org/10.1108/CG-04-2021-0129

[34] Sun, J., Yuan, R., Cao, F., Wang, B. (2017). Principal–principal agency problems and stock price crash risk: Evidence from the split‐share structure reform in China. Corporate Governance: An International Review, 25(3): 186-199. https://doi.org/10.1111/corg.12202

[35] Gustian, H., Bidayati, U. (2011). Analysis of the influence of cash position, debt to equity ratio, and return on assets on dividend payout ratio in manufacturing companies listed in bei. Jurnal Fokus Manajemen Bisnis, 1(1): 1. https://doi.org/10.12928/fokus.v1i1.1294

[36] Silaban, C.N., Pengestuti, I.R.D. (2017). Analisis faktor-faktor yang mempengaruhi kebijakan dividen dengan firm size sebagai variabel kontrol (Studi pada Perusahaan Manufaktur yang Terdaftar di BEI Tahun 2011- 2015). Diponegoro Journal of Management, 6(3): 1-15. https://doi.org/10.31603/bisnisekonomi.v15i1.1002

[37] Santoso, I. (2009). Akuntansi Keuangan Menengah (Intermediate Accounting). PT. Refika Aditama. Bandung. https://doi.org/10.7476/9788523212100

[38] Ranajee, R., Pathak, R., Saxena, A. (2018). To pay or not to pay: What matters the most for dividend payments? International Journal of Managerial Finance, 14(2): 230-244. https://doi.org/10.1108/IJMF-07-2017-0144

[39] Nidar, S.R. (2016). Manajemen Keuangan Perusahaan Modern, Pustaka Reka Cipta, Bandung.

[40] Septiana, M., Prasetyo. (2015). Analisis pengaruh cash ratio, debt to total asset, asset growth, firm size dan return on asset terhadap dividend payout ratio. Diponegoro Journal of Management, 4: 1-13.

[41] Wójtowicz, P. (2022). Questing benchmarks for the current ratio: An analysis of the Warsaw Stock Exchange firms. International Entrepreneurship Review, 8(4): 83-97. https://doi.org/10.15678/IER.2022.0804.06

[42] Al-Fasfus, F.S. (2020). Impact of free cash flows on dividend pay-out in Jordanian banks. Asian Economic and Financial Review, 10(5): 547-558. https://doi.org/10.18488/journal.aefr.2020.105.547.558

[43] Ghasemi, M., AB Razak, N., Muhamad, J. (2018). Dividends, leverage and endogeneity: A simultaneous equations study on Malaysia. Australasian Accounting, Business and Finance Journal, 12(1): 47-64. http://dx.doi.org/10.14453/aabfj.v12i1.4

[44] Rajesh Kumar, B., Sujit, K.S. (2018). Determinants of dividends among Indian firms—An empirical study. Cogent Economics & Finance, 6(1): 1423895. https://doi.org/10.1080/23322039.2018.1423895

[45] Lotto, J. (2020). Towards extending dividend puzzle debate: What motivates distribution of corporate earnings in Tanzania? International Journal of Financial Studies, 8(1): 18. https://doi.org/10.3390/ijfs8010018

[46] Thakur, B.P.S., Kannadhasan, M. (2018). Determinants of dividend payout of Indian manufacturing companies: A quantile regression approach. Journal of Indian Business Research, 10(4): 364-376. https://doi.org/10.1108/JIBR-02-2018-0079

[47] Le, T.T.H., Nguyen, X.H., Tran, M.D. (2019). Determinants of dividend payout policy in emerging markets: Evidence from the ASEAN region. Asian Economic and Financial Review, 9(4): 531-546. https://doi.org/10.18488/journal.aefr.2019.94.531.546

[48] Shafai, N.A., Nassir, A.M., Kamarudin, F., Rahim, N.A., Ahmad, N.H. (2019). Dynamic panel model of dividend policies: Malaysian perspective. Contemporary Economics, 13(3): 239-253. https://doi.org/10.6007/IJARAFMS/v10-i3/7845

[49] Yousaf, I., Ali, S., Hassan, A. (2019). Effect of family control on corporate dividend policy of firms in Pakistan. Financial Innovation, 5(1): 1-13. https://doi.org/10.1186/s40854-019-0158-9

[50] Bhayani, S., Ajmera, B. (2019). Dividend policy decision: Panel data analysis for selected cement companies in India. Journal of Commerce and Accounting Research, 8(4): 79-85.

[51] Banerjee, A., De, A. (2015). Capital structure decisions and its impact on dividend payout ratio during the pre-and post-period of recession in Indian scenario: An empirical study. Vision, 19(4): 366-377. https://doi.org/10.1177/0972262915610956

[52] Budiarso, N.S. (2019). Agent, steward, and dividend policy. European Research Studies, 22(3): 83-94. https://doi.org/10.35808/ersj/1458

[53] Gharsalli, M. (2019). High leverage and variance of SMEs performance. The Journal of Risk Finance, 20(2): 155-175. https://doi.org/10.1108/JRF-02-2018-0011

[54] Vithessonthi, C., Tongurai, J. (2015). The effect of leverage on performance: Domestically-oriented versus internationally-oriented firms. Research in International Business and Finance, 34: 265-280. https://doi.org/10.1016/j.ribaf.2015.02.016

[55] Senarathne, C.W., Perera, T.R. (2021). Explaining the impact of financial leverage on firm performance in the healthcare sector in sri lanka by fixed cost coverage ratio. Organizacijø Vadyba: Sisteminiai Tyrimai, (86): 77-91.

[56] Papadimitri, P., Pasiouras, F., Tasiou, M. (2021). Financial leverage and performance: The case of financial technology firms. Applied Economics, 53(44): 5103-5121. https://doi.org/10.1080/00036846.2021.1915949

[57] Junaidi, M. (2021). Effect of debt to equity ratio and firm size of return on assets on manufacturing company in indonesia stock exchange. The Review of Finance and Banking, 13(2): 99-108. https://doi.org/10.24818/rfb.21.13.02.01

[58] Irom, I.M., Joshua, O., Ahmed, M.N., Emmanuel, A.T. (2018). Effect of firm attributes on return on asset of listed manufacturing companies in Nigeria. Journal of Accounting, Finance and Auditing Studies, 4(3): 223-240.

[59] Sudrajat, J., Daud, Z.M. (2020). The effect of firm’s size on corporate performance. International Journal of Advanced Computer Science and Applications, 11(5). https://doi.org/10.14569/IJACSA.2020.0110536

[60] Cahyani, N.L.A.P., Badjra, I.B. (2017). Pengaruh Leverage dan likuiditas terhadap kebijakan dividen dengan profitabilitas sebagai variabel intervening di BEI. Doctoral dissertation, Udayana University.

[61] Anvari, E., Askari, S.M. (2015). Analysis the most effective factors on the policy of share dividends in the Tehran Stock Exchange companies. WALIA journal, 31(4): 211-215.

[62] Widana, I.N.A., Suardana, I.B.R. (2018). Determinan kebijakan dividen dengan profitabilitas sebagai variabel mediasi. Jurnal Ilmiah Akuntansi & Bisnis, 3(1): 108-117. https://doi.org/10.38043/jiab.v3i1.2103

[63] Hakeem, S.A.A., Bambale, A.J.A. (2016). Mediating effect of liquidity on firm performance and dividend payout of listed manufacturing companies in Nigeria. Journal of Economic Development, Management, IT, Finance & Marketing, 8(1): 15-35.

[64] Lleras, C. (2005). Path analysis. Encyclopedia of Social Measurement, 3(1): 25-30. https://doi.org/10.1016/B0-12-369398-5/00483-7

[65] Mitchell, R.J. (1992). Testing evolutionary and ecological hypotheses using path analysis and structural equation modelling. Functional Ecology, 6(2): 123-129. https://doi.org/10.2307/2389745

[66] Berndt, Andrea E. "Sampling methods." Journal of Human Lactation 36, no. 2 (2020): 224-226.

[67] Al-Malkawi, H. (2008). Factors influencing corporate dividend decision: Evidence from Jordanian panel data. International Journal of Business, 13(2): 177-195.

[68] González, M., Molina, C., Pablo, E. (2010). Dividend policy and ownership structure in Latin America. Universidad de Los Andes. Facultad de Administración. School of Management.

[69] Nizar Al-Malkawi, H. (2007). Determinants of corporate dividend policy in Jordan: An application of the tobit model. Journal of Economic & Administrative Sciences, 23(2): 44-70. https://doi.org/10.1108/10264116200700007

[70] Hashemi, S.A., Zadeh, F.Z. (2012). The impact of financial leverage operating cash flow and size of company on the dividend policy (case study of Iran). Interdisciplinary Journal of Contemporary Research in Business, 3(10): 264-270.

[71] John, S.F., Muthusamy, K. (2010). Leverage, growth and profitability as determinants of dividend payout ratio-evidence from indian paper industry. Asian Journal of Business Management Studies, 1(1): 26-30.

[72] Gupta, A., Banga, C. (2010). The determinants of corporate dividend policy. Decision, 37(2).

[73] Al-Shubiri, F.N. (2011). Determinants of changes dividend behavior policy: Evidence from the amman stock exchange. Far East Journal of Psychology and Business, 4(1).

[74] Afza, T., Mizan, H.H. (2010). Ownership structure and cash flows as determinants of corporate dividend policy in Pakistan. International Business Research, 3(3): 210-221. https://doi.org/10.5539/ibr.v3n3p210

[75] Eltya, S. (2014). Pengaruh leverage, likuiditas, profitabilitas dan ukuran perusahaan terhadap kebijakan dividen (Studi pada Perusahaan Perbankan yang Terdaftar di Bursa Efek Indonesia Tahun 2010-2013). Jurnal Administrasi Bisnis S1 Universitas Brawijaya, 15(1): 84510.

[76] Adil, M., Zafar, N., Yasen, N. (2011). Empirical analysis of determinants of dividend payout: Profitability and liquidity. Interdisciplinary Journal of Contemporary Research in Business, 3(1): 289-300.

[77] Anil, K., Kapoor, S. (2008). Determinants of dividend payout ratios-a study of Indian information technology sector. International Research Journal of Finance and Economics, 15(1): 63-71.

[78] Maulita, D., Tania, I. (2018). Pengaruh Debt to equity ratio (DER), debt to asset ratio (DAR), dan long term debt to equity ratio (LDER) terhadap profitabilitas. JAK (Jurnal Akuntansi) Kajian Ilmiah Akuntansi, 5(2): 132-137. http://doi.org/10.5281/zenodo.1311575

[79] Dissanayake. (2012). The determinants of return on equity: Evidences from Sri Lankan microfinance institutions. Journal of Arts, Science & Commerce, 3(22).

[80] Velnampy, T., Niresh, J.A. (2012). The relationship between capital structure & profitability global. Journal of Management and Business Research, 12(13).

[81] Amidu, M. (2007). How does dividend policy affect performance of the firm on ghana tock Exchange? Investment Management and Financial Innovations, 4(2): 103-112.

[82] Bilal, A.R., Naveed, M., Taliv, N.A. (2011). Impact of working capital on profitability of cement sector of Pakistan. Interdisciplinary Journal of Contemporary Research in Business, 3(7): 661-666.