Erna Handayani* | Mahfud Sholihin | Suryo Pratolo | Alni Rahmawati

© 2022 IIETA. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

Against the backdrop of financial turbulence at the start of the COVID-19 pandemic, this study examines the role of transformational leadership in leading private universities in Indonesia to achieve good financial sustainability. This study is the latest study that combines the indirect relationship of transformational leadership and financial sustainability using the mediation of accountability and transparency as part of good university governance. The study used a closed survey of 381 respondents in the financial sector from private universities in 10 provinces in Indonesia. Data processing and analysis using SPSS with various stages for an analysis endurance test. The results show that transformational leadership does not directly affect financial sustainability but through transparency and accountability. Another accepted hypothesis discusses the relationship of transformational leadership to the transparency and accountability of higher education institutions. The last accepted hypothesis is the direct relationship of the transparency variable to the financial sustainability and the accountability variable to the financial sustainability of private universities in Indonesia. Theoretical and practical recommendations are discussed densely in the discussion of this research.

transformational leadership, financial sustainability, good university governance, transparency, accountability, higher education

Part of the effects of the COVID-19 pandemic is the financial crisis that has hit many private universities in Indonesia. Empirical facts conducted in the early period of the COVID-19 pandemic on 390 private universities in Indonesia showed financial problems. This operational difficulty to the decline in the number of students was then widely discussed in the national mass media in Indonesia at that time [1-3]. It was informed that the operational difficulties of higher education institutions included several private universities having difficulty paying the salaries of lecturers and administrative staff [4-7]. The temporary decrease in the number of students causing operational difficulties shows that the financial sustainability of private universities is still not good. Financial sustainability is essential to the attention of universities because it is a condition of the sustainability of higher education operations and needs that continue to grow to the expectations of stakeholders [8]. Adoption of agency theory [9], universities are accountable to stakeholders for their sustainability performance [10].

The ability of the organization to go through a crisis and produce organizational financial performance is part of the work of leaders with the right leadership style [11]. Transformational leadership style is considered capable of taking strategic organizational policies during corporate turbulence, in this case, the hospital object [11]. Although there are not enough studies that examine the relationship of transformational leadership to financial sustainability, there is much literature on the role of transformational leadership in improving financial performance [12-14], company performance in general [15]; the performance of non-profit institutions [16] including the performance of universities [17]. Regarding sustainability, research by Jiang et al. [18] found a substantial and significant effect of transformational leadership on sustainability performance and sustainability orientation [19]. This discovery was confirmed by Abbas & Bakri [20] with similar results.

Transformational leadership has a positive effect on the development of innovation [11] and trust in the company [21], which is strongly correlated with the financial sustainability of profit institutions [22, 23] as well as non-profit organizations such as the African American church [24]. The direct influence of leadership on financial sustainability is proven in the research of Suriyankietkaew and Avery [25] and Peprah [26] as well as indirect positive effects have been demonstrated by Iqbal et al. [27] in their study using psychological security mediation.

Transformational leadership moves subordinates with inspirational, motivational, and stimulation [28] which is closely related to good governance. Several studies have linked the close relationship between transformational leadership and good governance in public organizations [29, 30], as well as in universities [31].

However, research examining the role of transformational leadership, either directly or through good governance, on financial sustainability is still limited. Therefore, this study focuses on the following reviews: 1). Examine the empirical data on the direct influence of transformational leadership as an antecedent of financial sustainability of private universities and its indirect effect through good governance; 2). Re-examine the gaps in the results of research on this study between the results of solid support for transformational leadership on financial sustainability; for example, Jundi et al. [32] found an insignificant relationship moderating transformational leadership between sustainable development and financial performance, as well as Pantouvakis and Vlachos [33] who stated that leadership did not moderate the dimensions of sustainability and financial performance.

This research contributes to developing the financial sustainability of private universities, especially in terms of university leadership. The study's results can be used to increase the influence of private universities' leadership aspects on good governance. From a theoretical perspective, the research re-examines the relationship between transformational leadership and financial sustainability gaps. In addition, this study analyzes empirical data on the relationship between leadership, good governance, and the financial sustainability of private universities, which is still very limited.

2.1 Financial sustainability

Financial sustainability is the ability to persevere towards financial goals without ongoing donor support [34, 35]. Universities need to maintain the health of their financial sustainability because the demands to continue operating and maintaining their performance are of great interest. The operational sustainability of higher education institutions is the ability of universities to cover operational costs from their operating income. Financial independence is the ability of universities to finance their activities without the help o f other parties. The independence ratio also called the dependency ratio [35], showed a negative relationship between financial sustainability and financial subsidies; if income increases due to subsidies, the company's financial sustainability decreases. The higher the dependency ratio, the lower the financial sustainability.

The financial sustainability of universities from the aspect of sustainability is the ability of universities to cover their long-term obligations or aspects of financial solvency [36-39]. The financial solvency aspect of higher education explains the compatibility between growth and long-term financial conditions [40] and good financial management to maintain financial stability [41]. Research Lan et al. [41] used solvency indicators to measure financial sustainability variables. Referring to Alshubiri [39], the solvency aspect can be explained by indicators of the long-term financial security of universities.

2.2 Transformational leadership

Before reviewing the relationship between transformational leadership roles in this study, we explain the notion of transformational leadership as a leader who inspires subordinates to achieve company targets beyond individual boundaries. The translated leadership behavior represents individual consideration, inspirational motivation, intellectual stimulation, and ideal influence on followers [42]. These behaviors include inspiring, motivating, and supporting employee innovation behavior and flexibility that fosters proactivity [43]. We review four dimensions to review transformational leadership in private universities in Indonesia [28, 44]; namely: 1). Idealized influence: the leader is respected and trusted so that subordinates follow; 2). Inspirational motivation: the leader provides motivation, a spirit of optimism, and clear direction to subordinates; 3). Intellectual Stimulation: leaders give subordinates space to be creative and innovative; 4). Individualized Consideration: the leader acts as a mentor in developing the potential of employees to excel.

2.3 Good university governance

For financial sustainability, it is necessary to have good organizational performance [45], which is obtained from good organizational governance or good corporate governance [46-48] and later adopted in universities into good university governance [47-50]. Financial management based on the principles of good university governance is reflected in the performance-based budget management [48] with clear measures and a straightforward work program. The principles of good university governance in financial management are information disclosure (transparency), accountability, responsibility/responsibility, independence, and fairness [51].

This study uses 2 (two) dimensions of good university governance, namely accountability and transparency, according to the basic principles of the Indonesian National Committee on Governance Policy [51] as follows: 1) Transparency is a requirement for keeping a business's objectivity; businesses must give important and relevant information in a way that is easy for stakeholders to find and understand. 2) Accountability is a condition where the entity must be able to account openly and fairly for its performance. For this reason, the entity must be managed correctly, measurably, and following the interests while considering the interests of stakeholders and other stakeholders.

3.1 Transformational leadership and financial sustainability

Leadership manages all the company's resources to achieve its goals. While the right leadership style leads resources to be ideal [11]. The transformational leadership style emphasizes the opportunity for subordinates to develop themselves, placing human resources as part of the company's investment [28]. The transformational leadership behaviors of managers have a positive impact on the financial performance of organizations [52], and there is a positive relationship between sustainable development factors (i.e. environmental, economic and social aspects) and financial performance [53].

On the other hand, collaborative leadership has a positive effect on subjective perception of financial sustainability and a negative impact on objective financial sustainability (net debt) [22]. The study by Campbell [54] focused on transformational leadership theory, and sought to study the relationship between transformational leadership elements such as (ideal influence, inspirational motivation, intellectual stimulation, and individual consideration) and financial sustainability. The results of the multiple regression analysis of this study indicated the unpredictability of financial sustainability.

Transformational leadership has underpinned the company's financial performance [55]. Transformational leadership has also been shown to have a direct positive impact on financial sustainability [26], as well as indirect effects [27]. Through research and observation, we found a dearth of studies examining transformational leadership and its impact on financial sustainability within higher education institutions. Therefore, this study develops the following hypotheses:

H1: Transformational Leadership has a significant positive direct effect on the financial sustainability of private universities.

3.2 Transformational leadership and accountability

Accountability is an important part that must be held of transformational leadership. Someone who moves subordinates based on the dimensions of inspirational motivation [28] must be able to make subordinates believe that their leader is responsible for organizational goals and the use of resources for these purposes, including the use of finance. Leaders must be able to take responsibility for their work and convince subordinates to be motivated to do more than before.

In terms of transformational leadership in higher education, rectors and deans must be able to account for the implementation of their duties to lecturers and staff in order to foster enthusiasm for performance for their universities. Accountable leaders sacrifice pride, share power and increase humility [56] to be followed by their members. Thus the leader can effectively facilitate members in overcoming future challenges the organization faces so that it continues to be sustainable, including in finance [56]. Transformational leaders encourage members to internalize and imitate the values, beliefs, and behaviors of their leaders, including mutual obligations, respect, trust, and interpersonal support, so that transformational leadership is positively related to accountability. The positive and robust relationship between transformational leadership and perceived accountability drives the innovative performance of the organization [57]. Transformational leadership has been shown to have a direct positive effect on financial sustainability [26], and accountability is a means and a mediator to move organizations to achieve financial performance [57] organizational financial sustainability. Based on the study of the relationship between transformational leadership and accountability, the following are the hypotheses of this research:

H2: Transformational Leadership has a significant positive direct effect on the accountability.

H3: Transformational Leadership has a significant positive indirect effect on the financial sustainability.

3.3 Transformational leadership and transparency

The principle of the National Committee on Governance of Indonesia [51] explains transparency as objectivity in business and organization. Transparency encourages leaders to inform all aspects of organizational management, including financial use. Information can be conveyed through routine reporting schemes and provide easy and up-to-date access to information needed by stakeholders. Financial transparency is part of the sustainability issue in universities [58, 59] that needs attention. Transparency encourages trust in leaders so that subordinates are motivated to support the organization's goals [60] entirely. In transformational leadership, the dimension of idealized influence described by Avolio [28], the leader must be respected and trusted by subordinates. Like the accountability relationship in the role of transformational leadership, this relationship is closely related to the leadership transparency aspect. Transparency fosters respect, trust, and employee motivation, which in turn promotes the organization's long-term financial performance and stability [25, 26], and accountability is a means and a mediator to move organizations to achieve financial performance [57]. The study conducted by Karyana and Aryani [61] found that teachers' perception of transformational leadership has a positive impact on transparency and accountability in school financial management. This means the school principal's transformational leadership style is an important factor in a school's financial management to increase transparency and accountability. Siti and Djumahir [62] research findings indicate that transparency positively and directly affects performance, transformational leadership has a positive and direct impact on transparency, and transformational leadership indirectly affects performance through the mediation of transparency. Based on the foregoing in previous studies, in this study will test the following hypotheses:

H4: Transformational Leadership has a significant positive direct effect on the transparency.

H5: Transformational Leadership has a significant positive indirect effect on the financial sustainability through transparency.

3.4 Accountability, transparency, and financial sustainability

The results of Almagtome et al. [38] study show that accountability and financial sustainability are intertwined, and management must provide basic financial data to enable accountability and support its operations in order to ensure adequate funding. The model university’s financial sustainability outlook is also weak, and as a result, it cannot continue to operate financially independently of the government. Further investigation reveals that the lack of financial and administrative powers is the main reason for the financial shortfall in the study's financial position. The study findings also give other government-run higher education institutions the knowledge and data they need to assess the financial viability of their schools. The study conducted by Karyana and Aryani [61] found that teachers' perception of transformational leadership has a positive impact on transparency and accountability in school financial management. This means the school principal's transformational leadership style is an important factor in a school's financial management to increase transparency and accountability.

As part of good governance, it is important to emphasize accountability and transparency in financial management in particular and organizational management in general. Research related to good governance that supports financial sustainability has been proven both in government public organizations [46] private entities [63-65], and banking [66-69]. Besides being proven to have a direct effect, good university governance can mediate the role of transformational leadership [12] on financial performance. This study complements the study of the role of the financial sustainability of private universities by using 2 (two) principles of good governance, namely accountability and transparency. This study examines the relationship with the hypothesis:

H6: Accountability has a significant positive direct effect on the financial sustainability.

H7: Transparency has a significant positive direct effect on the financial sustainability.

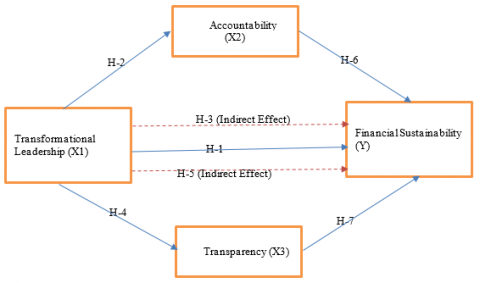

Research frameworks and hypotheses are illustrated in Figure 1 the following:

Figure 1. Research frameworks

4.1 Research methods and instruments

This study combines behavioral financial analysis with financial information that should be obtained in university financial statements. Because the financial statements of universities in Indonesia are still closed, the measurement approach uses the survey method. The study used a questionnaire to measure the relationship between variables in influencing other variables according to the research hypothesis [70, 71]; Measurements using a questionnaire instrument are carried out with the following considerations: 1). Private universities in Indonesia have not submitted financial reports openly, and there is a lack of access to research reports; 2) Research analyzes transformational leadership variables, namely manifest variables that can be measured using survey instruments [72].

This instrument's preparation follows the Podsakoff guidelines [73] and Rodríguez [74] for anticipating the biased result. The stages of preparing the questionnaire are as follows: 1). Study of the underlying theory; 2). The concept of the instrument was discussed through a closed expert forum or joint discussion involving eight finance professors, management, and financial behavior. This stage resulted in a large number of instrument improvements. Constructive inputs are incorporated into the instrument, ready to be tested via pilot test. 3). A pilot test was conducted to test the instrument before it was implemented. The pilot test was conducted on 30 respondents who were campus financial managers, accompanied by input related to instruments. The pilot test results were tested for validity and reliability, with the results being accepted and could be used further. The reliability and validity test of 30 pilot test respondents concluded that the instrument could be deployed in the field.

4.2 Research population and respondents

The research population is private universities in Indonesia with a total of 4,616 [75]. Respondents are financial managers of private universities consisting of 1). Vice-Chancellor/Chairman/Director of a private university in finance and; 2). Head of Bureau/Head of Finance for private universities in Indonesia. Based on the population of private universities, the researcher targets the number of research samples regarding Krejcie and Morgan [76], namely 380 respondents.

The research is expected to represent the entire population of private universities in Indonesia. Therefore, respondents are targeted to represent various provinces and representatives of the Lldikti region in Indonesia, namely the following ten provinces: Central Java, West Java, East Java, North Sumatra, Bengkulu, Yogyakarta, West Papua, Lampung, Palembang, and Bangka Belitung.

4.3 Data collection technique

The data collection model uses a questionnaire to the financial management leadership, carried out in collaboration with government institutions for private higher education services in Indonesia in various provinces. The data that has been collected is more than 500 respondents, who are then selected to suit the provisions of the research respondents that we have set.

4.4 Variables and measurements

The endogenous financial sustainability variable uses liquidity indicators [36, 39, 77, 78], solvency [37-39] growth and independence [79-81] universities as outlined in 7 question items. The exogenous transformational leadership variable is measured by four indicators referring to Avolio & Francis [28]: Idealized influence; Inspirational motivation; Intellectual Stimulation; Individualized Considerations. Furthermore, the accountability and transparency variables are taken from the dimensions of good corporate governance [51], measured by 7 and 8 indicators. All instruments use a 1-5 Linkert scale and are disseminated after passing validation by both experts and statistically [82].

5.1 Robustness test

We perform several steps of robustness testing of our model and data. The results of the model fit test meet the overall model validation, where the R2 value obtained is 0.655, the Q2 value is 0.405 > 0, the NFI is 0.788, and the SMRS value of the algorithm output is 0.075<0.10 [83, 84]. We examined the results of the measurements of the mean extraction of variance (AVE) and maximum joint variance (MSV) to complete the discriminant and convergent validity of [85]. The results of the AVE value of all variables are more than 0.5, with each variable being 0.568 for accountability, 0.830 for financial sustainability, 0.678 for transformational leadership, and 0.613 for transparency.

Pre-analysis tests were also carried out to meet the normality of the data, free of multicollinearity, autocorrelation, and heteroscedasticity with sig 0.127>0.05, VIF value <10, and Tolerance>0.01 in the Collinearity Statistics test, Durbin Watson obtained a value of 2.016 and a Chi-Square value of 241, 21 under the Chi-Square Table with df-1. Therefore, our analysis proceeds to the next stage.

5.2 Correlation results, AVE, Cronbach alpha, and composite reliability

Cronbach's alpha and composite reliability were employed to evaluate the inter-item consistency of our measurement items [86]. Table 4.1 demonstrates that all Cronbach alpha values above the minimum requirement of 0.6 [87], and that the composite reliability value is significantly over 0.50 [84].

We used a size of 0.7 as a valid measure of the research construct by looking at the Pearson score [84]. Some constructs had to be omitted because they did not meet our standards. The following are the results of the reliability validity, as shown in Table 1:

Table 1. Reliability validity test results

|

Variables/Indicators |

Correlation, Sig. (2-tailed) |

Results |

AVE |

Cronbach Alpha |

Composite Reliability |

|

Financial Sustainability |

|

|

0.830 |

0.896 |

0.936 |

|

College liquidity capability (FS1) |

0.724*** |

Received |

|

|

|

|

College solvency ability (FS2) |

0.778*** |

Received |

|

|

|

|

College income diversification (FS3) |

0.864*** |

Received |

|

|

|

|

Higher Education Growth (FS4) Reliance on third-party assistance (FS5) College asset ownership (FS6) Debt Expense (FS7) |

0.754*** 0.750*** 0.770*** 0.554*** |

Received Received Received Rejected |

|

|

|

|

Transformational Leadership [44] |

|

|

0.676 |

0.840 |

0.893 |

|

The formulation of a shared vision and mission (TL1) Consistent example (TL2) |

0.760*** 0.749*** |

Received Received |

|

|

|

|

Giving motivation (TL3) |

0.767*** |

Received |

|

|

|

|

M provide feedback to employees (TL4) |

0.805*** |

Received |

|

|

|

|

Award for achievement (TL5) |

0.843*** |

Received |

|

|

|

|

Responsive leadership in overcoming problems (TL6) |

0.829*** |

Received |

|

|

|

|

Always have solutions to solve problems (TL7) |

0.716*** |

Received |

|

|

|

|

Accountability [51, 88] |

|

|

0.568 |

0.849 |

0.887 |

|

Regular financial internal audit (F1) |

0.833*** |

Received |

|

|

|

|

Regular external audit (F2) |

0 753*** |

Received |

|

|

|

|

Unqualified audit results (F3) |

0.783*** |

Received |

|

|

|

|

The use of money based on a predetermined cost standard (F4) |

0.741*** |

Received |

|

|

|

|

Measurement of spending money based on performance (F5) |

0.708*** |

Received |

|

|

|

|

The use of money is reported in an orderly manner (F6) |

0.731*** |

Received |

|

|

|

|

Use of money according to Standard Fee Guidelines (F7) |

0.716*** |

Received |

|

|

|

|

Transparency [51, 88] |

|

|

0.613 |

0.920 |

0.934 |

|

A clear purpose for using money (F1) |

0.581*** |

Rejected |

|

|

|

|

Open discussion of the budget ceiling (F2) |

0.779*** |

Received |

|

|

|

|

Financial reports can be accessed quickly (F3) |

0.740*** |

Received |

|

|

|

|

Financial reports can be accessed realtime (F4) |

0.715*** |

Received |

|

|

|

|

Financial usage reports are reported regularly to stakeholders (F5) |

0.715*** |

Received |

|

|

|

|

Clear cost standards to be used as a common guideline (F6) |

0.722*** |

Received |

|

|

|

|

Commonly decided cost standards (F7) |

0.716*** |

Received |

|

|

|

|

Standard Operational Financial management procedures are carried out in an orderly manner (F8) |

0.733*** |

Received |

|

|

|

AVE: Extracted Average Variance

Correlation use-value is above 0, 7

AVE meets if the value is above 0.5 [83]

Composite Reliability meets if the value is above 0.7 [83]

Cronbach's Alpha fulfills if the value is above 0.6 0.6 [83]

5.3 Hypothesis testing results

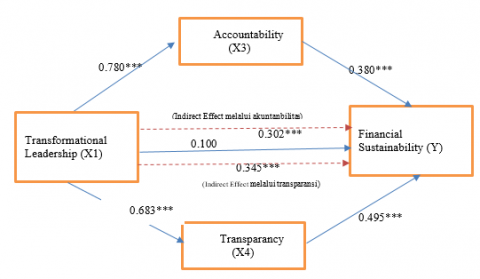

The results of hypothesis testing are presented in Figure 2 and Table 2. The hypothesis for a direct relationship is supported if the results of the statistical coefficients test are below 0.05 and are positive. To answer the hypothesis of an indirect relationship, we use the Sobel test referring to the study of Baron and Kenny [89] to prove the indirect relationship of transformational leadership to financial sustainability through accountability and transparency variables, as seen in Table 2. it was found that the mediation and Sobel tests were carried out with the provisions of t count> t table to determine the significant effect. Based on the regression analysis test, it was found that all proposed hypotheses were supported at a significance level of 0.00 (Table 2) except for the first hypothesis, namely the direct effect of transformational leadership on financial sustainability. On the other hand, a significant relationship is obtained from the indirect relationship of transformational leadership to financial sustainability through the mediating role of accountability and transparency with t counts of 5,210>1,645 and 7,486>1,645, respectively. The following figure is 2. is the result of the path analysis of each hypothesis, while Table 2. is the result of testing each hypothesis:

Figure 2. Results of path analysis of each hypothesis (processed data)

Furthermore, the results of hypothesis testing are described in Table 2.

The leadership style has been studied in many studies to ensure the organization's continuity effectively. Transformational leadership is a leadership style that emphasizes the importance of providing space for subordinates to develop by providing examples, motivation, and support to subordinates. This investment in human resources ensures the organization's survival [90, 91], including private universities, although, in this study, it has not been proven to have a significant positive effect on the financial sustainability of private universities in Indonesia. With a significance result of 0.317>0.05, the first hypothesis that transformational leadership has a direct and significant effect on financial sustainability is not accepted.

This study obtained different results from previous studies regarding the direct relationship between these two variables [25, 26] with the object of private universities. However, the relationship of transformational leadership to financial sustainability in private universities is built in an indirect relationship by using the variables of good university governance with dimensions of accountability and transparency. The results of testing the indirect relationship of transformational leadership through accountability (second hypothesis) and transparency (fifth hypothesis) are positively and significantly similar to the research of Iqbal et al. [27], although using different leadership styles.

These results indicate that transformational leadership with inspirational motivation dimensions applied in private universities needs to be proven by examples and concrete actions to move subordinates. Higher education as a nest of academics places leaders as role models by looking at the results and real work. Rector and dean will be noticed, followed by their lecturers and staff after followers believe their leader has clear goals, has precise performance, and is accountable for the responsible use of university resources. Furthermore, this trust brings motivation and joint movement towards organizational and university financial sustainability.

Transformational leadership with an emphasis on motivation and providing space for subordinates positively supports the achievement of accountability and transparency in private universities in Indonesia. This conclusion is reflected in the results of this study's second and fourth hypotheses with a significance of 0.000 <0.05. These results are closely related to the research of Vivian Chen et al. [57]. Transparency in financial management is demonstrated in the regular reporting of financial use, ease of access to information, and reliability. This transparency encourages trust, from subordinates to leaders, and a stakeholder and community trust in the organization [60]. This trust, in turn, results in the organization's ability to continue to operate independently and sustainably from the financial and business aspects [25, 26]. The results of testing the second and fifth hypotheses support the role of good university governance in improving financial sustainability as in previous studies [47, 49, 50]. This role can be a direct role as the results of the sixth and seventh hypotheses and a mediating role as support for the research results of Vivian Chen et al. [57].

Table 2. Hypothesis testing results

|

H |

Model Parameters |

Coefficients |

Sig. & Decisions |

|

H-1 |

Direct Effect: Transformational LeadershipàFinancial Sustainability |

.100 |

0.317 NOT supported |

|

H-2 |

Direct Effect: Transformational Leadership àAccountability |

.780 |

0.000*** Supported |

|

H-3 |

Indirect Effect: Transformational LeadershipàAccountability àFinancial Leadership |

.302 |

0.000*** Supported |

|

H-4 |

Direct Effect: Transformational Leadership àTransparency Indirect Effect: Transformational Leadershipà |

.683 |

0.000*** Supported |

|

H-5 |

Transparency àFinancial Sustainability |

.345 |

0.000*** Supported |

|

H-6 |

Direct Effect: Accountability àFinancial Sustainability |

.380 |

0.000*** Supported |

|

H-7 |

Direct Effect: Transparency àFinancial Sustainability |

.495 |

0.000*** Supported |

1. Number of samples: 381

2. ***Sig<0.05

3. Sobel Test: t count>t table at 1.645

6.1 Conclusion

This study examines the role of the transformational leadership style as an inspirational style, motivator, and stimulator for subordinates to develop and develop positively to support the sustainability of private universities that represent financial sustainability. This study shows that the role of transformational leadership is not obtained from a direct relationship but requires the mediation of good university governance with transparency and accountability. A leader can influence his subordinates as an inspiration, motivator, and stimulator by setting an example for his subordinates. In financial management, this example aspect can be demonstrated by the dimensions of transparency and accountability. Thus, the aspects of transparency and accountability facilitate the influence of inspirational leadership, motivators, and stimulators that can effectively move all lines of higher education, both operationally and financially.

To previous research, transformational leadership supports the formation of good governance [61, 62] this study supports the relationship between the role of leadership with transformational style and good governance in private higher education institutions. As part of the principles of good governance, transparency and accountability in financial management significantly enhance the transformational role in improving the finances of private universities. Good governance of private universities affects efficiency and appropriate spending of funds to support the performance of private universities, which ultimately supports the financial sustainability of private universities. This conclusion supports the research of Peter and Kamanzi [92] and Arslan and Alqatan [93], which examine the relationship between good corporate governance and financial sustainability. Therefore, these results can be a reference for higher education leaders to focus on transparency and accountability in higher education management to inspire, motivate, and improve all universities to move towards financially stable and long-term goals.

6.2 Weaknesses and recommendations for further research

This study uses a survey method to assess financial sustainability. Despite the difficulties encountered, researchers understand that the best way to assess the financial aspect is to look directly at the financial statements. Research that relies on questionnaires has the potential to bias the results. Although this research has used methods to overcome research bias in instruments, researchers still include this element as a potential weakness of this study. Furthermore, future research needs to consider aspects of the study of financial statements in examining the variables of transparency, accountability, and financial sustainability combined with aspects of transformational leadership studies. Future researchers can also consider other principles of good university governance to complement studies on this theme.

[1] Suryanto, A. (2020). Terimbas-pandemi-maba-di-pts-menurun-drastis. https://radarlampung.online/2020/09/17/terimbas-pandemi-maba-di-pts-menurun-drastis.

[2] Republika. (2020). Ragam Cara PTS Hadapi Pandemi. https://www.republika.id/posts/9336/ragam-cara-pts-hadapi-pandemi.

[3] Putra, R. (2020). Skenario ‘New Normal’ Perguruan Tinggi. https://news.detik.com/kolom/d-5039862/skenario-new-normal-perguruan-tinggi.

[4] Wijaya, E.P.E. (2020). Pandemi COVID 19 minat daftar PTS di Yogyakarta menurun. https://jogja.suara.com/read/2020/08/22/192210/pandemi-covid-19-minat-daftar-ke-pts-di-jogja-menurun.

[5] Haryadi, R. (2020). Kesulitan Menggaji Dosen, Kemendikbud Diminta Bantu PTS. https://uai.ac.id/kesulitan-menggaji-dosen-kemendikbud-diminta-bantu-pts/?utm_source=rss&utm_medium=rss&utm_campaign=kesulitan-menggaji-dosen-kemendikbud-diminta-bantu-pts.

[6] Ikhsan, M. (2020). Corona, 80 Persen PTS di DKI Mulai Kesulitan Bayar Gaji Dosen. https://www.cnnindonesia.com/nasional/20200426092855-20-497345/corona-80-persen-pts-di-dki-mulai-kesulitan-bayar-gaji-dosen.

[7] Jawa Pos Kesulitan Bayar SPP, Mahasiswa di PTS Terancam Drop Out. https://www.jawapos.com/nasional/25/07/2020/kesulitan-bayar-spp-mahasiswa-di-pts-terancam-drop-out/, accessed on Nov. 19, 2020.

[8] Cernostana, Z. (2018). Measuring financial sustainability of private higher education institutions. Engineering for Rural Development, 1173-1178. https://doi.org/10.22616/ERDev2018.17.N343

[9] Jensen, M.C. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Value Summit Power VE.

[10] Ceulemans, K., Moderez, L., Liedekerke, L.V. (2015). Sustainability reporting in higher education: A comprehensive review of the recent literature and paths for further research. Journal of Cleaner Production, 106: 127-143. https://doi.org/10.1016/j.jclepro.2014.09.052

[11] Kiyak, M. Bozaykut, T., Güngör, P., Aktaş, E. (2011). Strategic leadership styles and organizational financial performance: A qualitative study on private Hospitals. Procedia - Social Behavior Science, 24: 1521-1529. https://doi.org/10.1016/j.sbspro.2011.09.090

[12] Sudarsana, I.N., Budiasih, I.G.A. (2019). Pengaruh gaya kepemimpinan dan budaya organisasi pada kinerja keuangan dengan penerapan good corporate governance sebagai variabel moderasi. E-Journal Akuntansi, 29(1): 78-95. https://doi.org/10.24843/EJA.2019.v29.i01.p06 orang

[13] Burawat, P. (2019). The relationships among transformational leadership, sustainable leadership, lean manufacturing and sustainability performance in Thai SMEs manufacturing industry. International Journal of Quality and Reliability Management, 36(6): 1014-1036. https://doi.org/10.1108/IJQRM-09-2017-0178

[14] Son, T.T., Phong, L.B., Loan, B.T.T. (2020). Transformational leadership and knowledge sharing: determinants of firm’s operational and financial performance. SAGE Open, 10(2). https://doi.org/10.1177/2158244020927426

[15] Patiar, A., Wang, Y. (2016). The effects of transformational leadership and organizational commitment on hotel departmental performance. International Journal of Contemporary Hospitality Management, 28(3): 586-608. https://doi.org/10.1108/IJCHM-01-2014-0050

[16] Adriani, Z. (2019). Improving performance through transformational leadership and utilization of information technology: A survey in mosque-based Islamic cooperatives in Indonesia. Academy of Strategic Management Journal, 18(2): 1-13.

[17] Nurtjahjani, F., Noermijati, N., Hadiwidjojo, D., Irawanto, D.W. (2019). Transformational leadership higher education: A study in Indonesian Universities. Aicmbs, 135: 95-101. https://doi.org/10.2991/aebmr.k.200410.015

[18] Jiang, W., Zhao, X., Ni, J. (2018). The impact of transformational leadership on employee sustainable performance: The mediating role of organizational citizenship behavior. Sustainability, 9(9): 1567. https://doi.org/10.3390/su9091567

[19] Obal, M., Morgan, T., Joseph, G. (2020). Integrating sustainability into new product development: The role of organizational leadership and culture. Journal of Small Business Strategy, 30(1): 43-57.

[20] Abbas, S., Bakri, N. (2020). Transformational leadership, organizational culture and sustainability at the property development companies in Malaysia. International Journal of Recent Technology Engineering, 8(3S2): 640-644. https://doi.org/10.35940/ijrte.c1209.1083s219

[21] Purvee, A., Enkhtuvshin, D. (2015). Leadership Behaviors, trustworthiness, and managers’ ambidexterity. International Journal of Innovatif Management Technology, 6(2): 109-113. https://doi.org/10.7763/ijimt.2015.v6.584

[22] Kim, J. (2018). Collaborative leadership and financial sustainability in local government. Local Government Studies, 44(6): 874-893. https://doi.org/10.1080/03003930.2018.1512490

[23] Stanovci, M.K., Metin, H., Ademi, B. (2019). Financial sustainability of NGOs: An empirical study of kosovo NGOs. IFAC-PapersOnLine, 52(25): 113-118. https://doi.org/10.1016/j.ifacol.2019.12.457

[24] Munford, J. (2016). Transformational leadership and fiscal sustainability in African American Churches. Ph.D. Dissertation. Walden University, Minnesota, USA.

[25] Suriyankietkaew, S., Avery, G. (2016). Sustainable leadership practices driving financial performance: Empirical evidence from Thai SMEs. Sustaibility, 8(4): 1-14. https://doi.org/10.3390/su8040327

[26] Peprah, W.K. (2018). The relationship between sustainable leadership and financial sustainability: A key to transforming agricultural financing. Proceeding: 4th Research Conference on Sustainable Development Goals: Transforming AfricaAt: Adventist University of Africa, Nairobi, 13th - 15th September, 2018.

[27] Iqbal, Q., Ahmad, N.H., Nasim, A., Khan, S.A.R. (2020). A moderated-mediation analysis of psychological empowerment: Sustainable leadership and sustainable performance. Journal of Cleaner Production, 262: 121429. https://doi.org/10.1016/j.jclepro.2020.121429

[28] Avolio, B.J., Yammarino, F.J. (2013). Introduction to, and overview of, transformational and charismatic leadership Transformational and Charismatic Leadership: The Road Ahead 10th Anniversary Edition. https://doi.org/10.1108/S1479-357120130000005005

[29] Mohamad, M., Daud, Z., Yahya, K. (2014). Impact on employees’good governance characterisrtics, the role of transformational leadership as determinant factor. International Journal of Environmental Science and Technology, 3(1): 320-338.

[30] Elmasry, M., Bakri, N. (2019). Behaviors of transformational leadership in promoting good governance at the palestinian public sector. International Journal of Organizational Leadership, 8(1): 1-12. https://doi.org/10.33844/ijol.2019.60265

[31] Indrianawati, U. (2010). The effect of leadership on performance management, good governance, internal and external satisfaction in study programs. Business Review, 9(5): 8-28.

[32] Jundi, K., Ghazalat, A., Yahya, S. (2019). The sustainable development practices role and transformational leadership: interaction and impact on the financial performance. Journal of Reviews on Global Economics, 8: 591-603. https://doi.org/10.6000/1929-7092.2019.08.51

[33] Pantouvakis, A., Vlachos I. (2020). Talent and leadership effects on sustainable performance in the maritime industry. Transportation Research Part D: Transport and Environment, 86: 102440. https://doi.org/10.1016/j.trd.2020.102440

[34] Anthony, K. (2014). Effect of microfinance lending on the financial performance of businesses: A case study of small and medium enterprises in nakuru east sub. International Journal of Science and Research, 3(10): 2304-2308.

[35] Dunford, C. (2003). The holy grail of microfinance: Helping the poor and sustainable: Microfinance evolution, achievements and challenges. ITDG, London.

[36] Al-Kharusi, S., Murthy, S.R. (2017). Financial sustainability of private higher education institutions: The case of publicly traded educational institutions. Investment Management and Financial Innovations, 14(3): 25-38. https://doi.org/10.21511/imfi.14(3).2017.03

[37] Di Carlo, F., Modugno, G., Agasisti, T., Catalano, G. (2019). Changing the accounting system to Foster Universities’ financial sustainability: First evidence from Italy. Sustainability, 11(21): 16151. https://doi.org/10.3390/su11216151

[38] Almagtomea, A., Shaker, A., Al-Fatlawi, A., Bekheet, H. (2019). The integration between financial sustainability and accountability in higher education institutions: An exploratory case study. International Journal of Innovation, Creativity and Change, 8(2): 202-221.

[39] Alshubiri, F.N. (2020). Analysis of financial sustainability indicators of higher education institutions on foreign direct investment: Empirical evidence in OECD countries. International Journal of Sustainability in Higher Education, 22(1): 77-99. https://doi.org/10.1108/IJSHE-10-2019-0306

[40] Gómez-Bezares, F. Przychodzen, W., Przychodzen, J. (2016). Corporate sustainability and shareholder wealth-evidence from British companies and lessons from the crisis. Sustainability, 8(3): 276. https://doi.org/10.3390/su8030276

[41] Lan, S., Yang, C., Tseng, M.L. (2019). Corporate sustainability on causal financial efficiency model in a hierarchical structure under uncertainties. Journal of Cleaner Production, 237: 117769. https://doi.org/10.1016/j.jclepro.2019.117769

[42] Ran, S. (2017). Are transformational leaders sustainable? The role of organizational culture. Wayne State University.

[43] McCormick, B.W., Guay, R.P., Colbert, A.E., Stewart, G.L. (2019). Proactive personality and proactive behaviour: Perspectives on person–situation interactions. Journal of Occupational and Organizational Psychology, 92(1): 30-51. https://doi.org/10.1111/joop.12234

[44] Bass, B.M., Avolio, B.J. (1993). Transformational leadership and organizational culture. Public Administration Quarterly, 112-121.

[45] Godday, O., Billyaminu, A. (2020). Risk management strategies and banks’ financial sustainability in the ace of the recent global pandemi. International Journal of Business and Management Review, 8(6): 1-12.

[46] Adegbite, E. (2015). Good corporate governance in Nigeria: Antecedents, propositions and peculiarities. International Business Review, 24(2): 319-330.

[47] Sabandar, S.Y., Tawe, A., Musa, C.I. (2018). The implementation of good university governance in the private universities in makassar (Indonesia). Espacios, 39(2).

[48] Pratolo, S., Sofyani, H., Anwar, M. (2020). Performance-based budgeting implementation in higher education institutions: Determinants and impact on quality. Cogent Business & Management, 7(1): 1786315. https://doi.org/10.1080/23311975.2020.1786315

[49] Wahyudin, A., Nurkhin, A. (2017). Keuangan perguruan tinggi. Jurnal Keuangan dan Perbankan, 21(40): 60–69.

[50] Kawedar, W., Handayani, R.S., Purwanto, A. (2019). Good governance, sistem pengendalian internal, dan kinerja keuangan organisasi sektor publik. Matrik: Jurnal Manajemen, Strategi Bisnis dan Kewirausahaan, 13(2): 214. https://doi.org/10.24843/matrik:jmbk.2019.v13.i02.p09

[51] Komite Nasional Kebijakan Governance. (2006). Pedoman Umum Good Corporate Governance Indonesia.

[52] Ocak, M., Ozturk, A. (2018). The Role of transformational leadership behaviours effects on corporate entrepreneurship behaviours and financial performance of firms. International Review of Management and Marketing, 8(4): 45-55.

[53] Jundi, K., Ghazalat, A., Yahya, S. (2019). The sustainable development practices role and transformational leadership: interaction and impact on the financial performance. Journal of Reviews on Global Economics, 8: 591-603. https://doi.org/10.6000/1929-7092.2019.08.51

[54] Campbell, T.R. (2020). Relationship Between transformational leadership style and financial sustainability. Dissertation, Walden University. USA.

[55] Sahaya, N. (2012). A learning organization as a mediator of leadership style and firms’ financial performance. International Journal Business Management, 7(14): 113. https://doi.org/10.5539/ijbm.v7n14p96

[56] Tucker, B.A., Russell, R.F. (2004). The influence of the transformational leader. Journal of Leadership and Organizational Studies, 10(4): 103-111. https://doi.org/10.1177/107179190401000408

[57] Chen, C.H.V., Yuan, M.L., Cheng, J.W., Seifert, R. (2016). Linking transformational leadership and core self-evaluation to job performance: The mediating role of felt accountability. North Am. J. Econ. Financ., 35: 234-246. https://doi.org/10.1016/j.najef.2015.10.012

[58] Kuo, C.C., Ni, Y.L., Wu, C.H., Duh, R.R., Chen, M.Y., Chang, C. (2021). When can felt accountability promote innovative work behavior? The role of transformational leadership. Personnel Review. https://doi.org/10.1108/PR-03-2021-0174

[59] Tabucanon, A.S., Sahavacharin, A., Rathviboon, S., Lhaetee, H., Pakdeesom, D., Xue, W., Charmondusit, K. (2021). Investigating the critical issues for enhancing sustainability in higher education institutes in Thailand. International Journal of Sustainable Development and Planning, 16(3): 503-514. https://doi.org/10.18280/ijsdp.160311

[60] Yue, C.A., Men, L.R., Ferguson, M.A. (2019). Bridging transformational leadership, transparent communication, and employee openness to change: The mediating role of trust. Public Relations Review, 45(3): 101779. https://doi.org/10.1016/j.pubrev.2019.04.012

[61] Karyana, J.P.J., Aryani, Y.A. (2021). Teacher perception of head of school transformational leadership, transparency, and accountability of school financial management. In Corporate Leadership and Its Role in Shaping Organizational Culture and Performance, pp. 279-295. https://doi.org/10.4018/978-1-5225-8266-3.ch013

[62] Nawangsari, L.C., Sudarma, M., Aisjah, S., Djumahir, A. (2015). The role of transformational leadership, monitoring and transparency on performance. European Journal of Business and Management Research, 7(5): 61-79.

[63] Janggu, T., Darus, F., Zain, M.M., Sawani, Y. (2014). Does good corporate governance lead to better sustainability reporting? an analysis using structural equation modeling. Procedia - Social Behavior Science, 145: 138-145. https://doi.org/10.1016/j.sbspro.2014.06.020

[64] Omri, A., Ben Mabrouk, N. (2020). Good governance for sustainable development goals: Getting ahead of the pack or falling behind? Environmental Impact Assessment Review, 83: 106388. https://doi.org/10.1016/j.eiar.2020.106388

[65] Tjahjadi, B., Soewarno, N., Mustikaningtiyas, F. (2021). Good corporate governance and corporate sustainability performance in Indonesia: A triple bottom line approach. Heliyon, 7(3): e06453. https://doi.org/10.1016/j.heliyon.2021.e06453

[66] Kinde, B.A. (2012). Financial sustainability of microfinance institutions (MFIs) in Ethiopia. European Journal of Business and Management Research, 4(15): 1-11.

[67] Abdelbadie, R.A., Salama, A. (2010). Corporate governance and financial stability in US banks: Do indirect interlocks matter. The Journal of Business Research, 104: 85-105. https://doi.org/10.1016/j.jbusres.2019.06.047

[68] Aksoy, M., Yilmaz, M.K., Tatoglu, E., Basar, M. (2020). Antecedents of corporate sustainability performance in Turkey: The effects of ownership structure and board attributes on non-financial companies. Journal of Cleaner Production, 276: 124284. https://doi.org/10.1016/j.jclepro.2020.124284

[69] Correa-Garcia, J.A., Garcia-Benau, M.A., Garcia-Meca, E. (2020). Corporate governance and its implications for sustainability reporting quality in Latin American business groups. Journal of Cleaner Production, 260: 121142. https://doi.org/10.1016/j.jclepro.2020.121142

[70] Cooper, D.R., Schindler, P.S. (2014). Business research methods 12th edition.

[71] Creswell, J.W. (2012). Research design: Qualitative, quantitative and mixed methods approach. Sage Publications.

[72] Sholihin, M., Ratmono, D. (2021). Analisis SEM_PLS dengan WarpPLS 7.0 untuk Hubungan Nonlinier dalam Penelitian Sosial dan Bisnis. 2nd ed. Yogyakarta.

[73] Podsakoff, P.M., MacKenzie, S.B., Lee, J.Y., Podsakoff, N.P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5): 879-903. https://doi.org/10.1037/0021-9010.88.5.879

[74] Rodríguez-Ardura, A., Meseguer-Artola, A. (2020). Editorial: How to prevent, detect and control common method variance in electronic commerce research. Journal of Theoretical and Applied Electronic Commerce Research, 15(2): I-V. https://doi.org/10.4067/S0718-18762020000200101

[75] Pddikti.kemendikbud.go.id. Data Perguruan Tinggi. https://pddikti.kemdikbud.go.id/pt.

[76] Krejcie, R.V., Morgan, D.W. (1970). Determining sample size for research activities. Educational and Psychological Measurement, 30(3): 607-610.

[77] Sazonov, S.P., Kharlamova, E.E., Chekhovskaya, I.A., Polyanskaya, E.A. (2015). Evaluating financial sustainability of higher education institutions. Asian Social Science, 11(20): 34-40. https://doi.org/10.5539/ass.v11n20p34

[78] Booth, M., Irvine, H., Ryan, C., McGregor-Lowndes, M. (2017). Spenders or savers? An examination of the reserves of Australian NGOs. Australian Accounting Review, 27(3): 248-262. https://doi.org/10.1111/auar.12152

[79] Achtenhagen, L., Naldi, L., Melin, L. (2010). “Business growth”—Do practitioners and scholars really talk about the same thing? Entrepreneurship Theory and Practice, 34(2): 289-316. https://doi.org/10.1111/j.1540-6520.2010.00376.x

[80] Gupta, P., Guha, S., Krishnaswami, S. (2013). Firm growth and its determinants. The Journal of Innovation and Entrepreneurship, 2(1): 15. https://doi.org/10.1186/2192-5372-2-15

[81] Supplee, J.L. (2014). Enrollment pathways to financial sustainability: Choosing the road less traveled. Christian Higher Education, 13(4): 250-265. https://doi.org/10.1080/15363759.2014.924889

[82] Haryono, S. (2017). Metode SEM untuk Penelitian dengan AMOS Lisrel PLS. Luxima Metro Media.

[83] Hair, J.F., Ringle, C.M., Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2): 139-152. https://doi.org/10.2753/MTP1069-6679190202

[84] Hair, J.F., Sarstedt, M., Hopkins, L., Kuppelwieser, C.G. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review, 26(2): 106-121. https://doi.org/ 10.1108/EBR-10-2013-0128

[85] Fornell, C., Larcker, D.F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research, 18(3): 382. https://doi.org/10.2307/3150980

[86] Zahro, S., Mustikasari, H., Mukti, Y.P., Wardhana, A.P. (2022). Developing comfortable cloth face masks: An experiment with four-ply cloth. International Journal of Sustainable Development and Planning, 17(7): 2229-2237. https://doi.org/10.18280/ijsdp.170723

[87] Chin, W.W., Marcolin, B.L., Newsted, P.R. (2003). A partial least squares latent variable modeling approach for measuring interaction effects: Results from a Monte Carlo simulation study and an electronic-mail emotion/adoption study. Information Systems Research, 14(2): 189-217. https://doi.org/10.1287/isre.14.2.189.16018

[88] Rhoades, L., Eisenberger, R. (2002). Perceived organizational support: A review of the literature. Journal of Applied Psychology, 87(4): 698-714. https://doi.org/10.1037//0021-9010.87.4.698

[89] Baron, R.M., Kenny, D.A. (1986). The moderator-mediator variabel distinction in social psychological research: Conseptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6): 1173-1182. https://doi.org/10.1177/1350506818764762

[90] Cabras, I., Goumagias, N.D., Fernandes, K., Cowling, P., Li, F., Kudenko, D., Devlin, S., Nucciarelli, A. (2017). Exploring survival rates of companies in the UK video-games industry: An empirical study. Technological Forecasting and Social Change, 117: 305-314. https://doi.org/10.1016/j.techfore.2016.10.073

[91] Lo, F.Y., Liao, P.C. (2021). Rethinking financial performance and corporate sustainability: Perspectives on resources and strategies. Technological Forecasting and Social Change, 162: 120346. https://doi.org/10.1016/j.techfore.2020.120346

[92] Peter, N.A., Kamanzi, S.M. (2019). Own-income generation: A pilar of financial sustainability in institutions of higher learning. World Voice Nexus, 3(3).

[93] Arslan, M., Alqatan, A. (2020). Role of institutions in shaping corporate governance system: Evidence from emerging economy. Heliyon, 6(3): e03520. https://doi.org/10.1016/j.heliyon.2020.e03520