Jianjing Li![]()

© 2024 The author. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

This study examines how top management’s environmental awareness and green innovation mediate the effects of digital transformation on sustainable development performance. The current study also looks at the institutional environment’s moderating role in the relationship between mediators (i.e., green innovation and top management’s environmental awareness) and digital transformation. The research uses regression analysis to examine hypotheses on how digital transformation affects firms’ sustainable development performance. It does this by using an imbalanced panel dataset including 1,805 Chinese publicly listed manufacturing companies from 2010 to 2021. The findings reveal that digital transformation is positively related to sustainable development performance. Besides, the relationship between digital transformation and sustainable development performance is mediated by increased green innovation and environmental awareness among top management. Furthermore, a supportive institutional environment enhances the impact of digital transformation on top management’s environmental awareness and green innovation. The study provides new insights into the mechanisms by which digital transformation promotes economic and environmental sustainability in China’s industrial sector. The findings have important implications for businesses looking to use digital technology to increase competitiveness while also achieving China’s "dual carbon" aims of green innovation and environmentally responsible leadership. Theoretical contributions include integrating an institution-based perspective to better comprehend contextual implications on long-term digital transformation.

digital transformation, corporate sustainable development, green innovation, top management’s environmental awareness, institutional environment

Characterized by groundbreaking technological advancements in harnessing resources and managing the environment, the Industrial Revolution has significantly propelled the progress of modern human civilization. However, the surging demand has triggered a rapid and previously unseen expansion in production capabilities, leading to increasingly pronounced conflicts between the demand for resources, their availability, and environmental sustainability [1]. Today, the concept of development transcends the mere expansion of economic metrics, embracing a more comprehensive vision of sustainable growth that equally weighs social, economic, and environmental considerations [2]. The World Commission on Environment and Development of the United Nations defines the term sustainable development as the individuals’ capabilities to meet their needs without compromising future generations’. Corporate sustainable development, however, requires continuous profit growth and rational utilization of resources as well as reduction in adverse effects on environment (e.g., from production activities) to gain support from a company’s internal and external stakeholders [3].

To better respond to global climate change and demonstrate responsibilities as a major country, in September 2020, China (i.e., the Chinese government) set two goals to: (a) achieve carbon neutrality by the year 2060 after (b) the estimated carbon peak by the year 2030. This policy has required Chinese enterprises to enhance green total factor productivity through energy conservation and emission reduction in their production processes to offset their carbon emissions. Setting these dual carbon goals represented a widespread and profound systemic transformation across Chinese industries. Characterized as a pillar of the national economy with a long value chain, broad industry coverage, and high externalities, the Chinese manufacturing sector has played an important role in developing the national economy and thus bears a substantial social responsibility for environmental protection and energy conservation. For instance, the application of Environmental, Social, and Governance (ESG) metrics integrates performances across these three domains into the evaluation system of high-quality corporate development, which has prompted enterprises to be more aware of environmental protection and social governance responsibilities in addition to their own interest growth.

Recent research has indicated that digital technologies may be reflected in all these definitions of disruptive innovation. They may represent innovations that are new to the world, dislocate existing processes, and open up entirely new business models. [4] The rapid development of digital technologies has provided traditional industries with momentum for innovative development. Digitalization (e.g., unique factors of production, technological system, institutional framework, development space, value philosophy) has largely affected traditional industries. Because of the substantial economic volume of the real economy, it has become a pillar industry of society, and the compatibility of the digital industry makes the integration process of China’s digital economy and real economy important aspects of economic life. To enhance sustainable development, Chinese enterprises should adapt to modern business environment and move away from traditional development models. Addressing the difficulties in upgrading digital technologies for sustainable development is an issue that has been widely discussed and researched by scholars, especially in China. Consequently, the current study aimed to answer the following research questions (hereafter: RQs):

RQ1: How does digital transformation in Chinese manufacturing enterprises affect their sustainable development performance?

RQ2: What may be the underlying mechanisms of this effect?

The current study provides value in the following ways. To begin, the study contributes to the discussion by empirically proving how digital technologies improve sustainable development performance as evaluated by ROA and ESG scores. By highlighting green innovation and top management’s environmental awareness as essential mediators, it emphasizes the internal routes that allow digital transformation to support a more sustainable business model, thereby expanding current theories.

Second, the study provides a detailed knowledge of how the institutional environment influences the success of digital transformation for promoting sustainability. It merges the institution-based view with digital transformation literature, providing a fresh perspective by demonstrating how a supportive institutional environment enhances the influence on green innovation and managerial environmental consciousness.

Furthermore, the use of an unbalanced panel dataset spanning over a decade provides a solid empirical foundation for investigating these correlations in the context of China’s manufacturing economy, given its "dual carbon" aims and growing digital world. The work adds to our theoretical understanding of the role of digital transformation in sustainability, while also providing timely insights for policymakers, practitioners, and scholars interested in digital innovation, environmental strategy, and institutional dynamics.

2.1 Digital transformation and corporate sustainable development

According to the phenomenon digital paradox, the effect of digital transformation on the company’s capability to corporate sustainable development may exhibit a "double-edged sword." This implies that when a company’s strategic positioning, external environment, and internal organization change, the effects of digital transformation may also chance. For example, digital transformation has proven to be effective only when the path of corporate development aligns with it [4]. With the continuous development of digital technologies, the gradual maturity and application of technologies (e.g., big data, artificial intelligence, blockchain, cloud computing) have accelerated the shift in corporate operational goals. Specifically, sustainable development has become an aspect of corporate competition, which focuses on operational efficiency and economic performance as well as performances in environmental and social responsibility [5]. Thus, after researching the relationship between digital transformation and corporate sustainable development in the literaute, I divided corporate sustainable development into two aspects: economic sustainability and environmental sustainability. Digital transformation can drive innovation to enhance corporate total factor productivity, which in turn boosts economic performance [6]. Also, digital transformation can promote a company’s value chain position, values in personnel management and training, research and development of projects, as well as infrastructure construction [7].

Companies may optimize their operations, save expenses, and improve decision-making processes by implementing digital technologies like artificial intelligence, blockchain, and cloud computing [8]. For example, using big data analytics allows businesses to unearth insights that lead to better product development, market targeting, and customer service, resulting in increased revenue and profitability. Furthermore, digital platforms and e-commerce have created new markets and revenue streams, highlighting how digital transformation may directly impact a company’s economic sustainability by broadening its reach and lowering entry barriers.

On the environmental front, digital transformation provides organizations with tools and mechanisms for considerably reducing their ecological impact and increasing their contributions to environmental sustainability. The Internet of Things (IoT) and smart sensors provide accurate monitoring and control of resource use, resulting in more efficient energy consumption and less waste. Furthermore, digitalization promotes the circular economy model by allowing for product life cycle management and effective material recycling. Previous study has also highlighted the importance of digital transformation in increasing environmental reporting and transparency, which not only helps businesses manage their environmental impacts more effectively but also fosters trust among stakeholders concerned about sustainability [9]. Consequently, the following hypotheses were proposed:

H1: Digital transformation can increase corporate economic performance sustainability.

H2: Digital transformation can increase corporate environmental performance sustainability.

2.2 The mediating role of green innovation

From the perspective of green technological innovation, studying the effect of digital transformation on corporate green innovation begins with understanding that green innovation refers to technological innovation activities related to green products or processes. It mainly includes environmental protection, pollution emission control, energy saving and emission reduction, waste utilization, as well as green product design [10]. According to the resource-based view, if a company needs green innovation, it should have a certain technological base.

Green innovation demands certain levels of innovation capability, financial resources, knowledge resources, and technical resources from a company, among which technological resources are the main driving force for green innovation and a solid foundation for corporate innovation [11]. As a form of technological resource, green innovation within the company may improve its internal operational efficiency and, thus, the level of green innovation, which in turn enhances the company’s sustainable development performance. Specifically, corporate green innovation can identify systemic issues in business operations through data mining, data analysis, and other methods, and thereby improves corporate value and aids in the improvement of modern production processes to achieve digital transformation. The effects of digital transformation on corporate green innovation include the following aspects. First, digital transformation may expand the boundaries of production possibilities and extend the boundaries of innovation possibilities, and thereby enhances the company’s green innovation capabilities [12]. Second, digital transformation can endow traditional products with digital characteristics, make them possess digital and technological attributes, as well as develop and perfect the basic usage attributes of traditional products, which in turn leads to the production’s moving towards intelligence and personalization. This enhances the derivative and added values of the products, and thereby creates more profits. Third, digital transformation can promote the innovation of business models. For example, a new business model with three components technology, manufacturing, and service, has been resultant from digital transformation and has strengthened the innovation value of manufacturing driven by service. The development of modern business forms (e.g., online live broadcasting, intelligent customer service, big data precision marketing, e-commerce) indicates that the traditional manufacturing industry is transforming into a new type of manufacturing service industry [13].

In summary, digital transformation serves as a catalyst for green innovation by providing firms with the tools, processes, and platforms they need to create sustainable solutions. It increases R&D capability, improves resource efficiency, promotes sustainable business models, assures environmental compliance, and facilitates stakeholder participation. By combining economic success with environmental care, digital transformation can greatly improve business performance sustainability.

Consequently. Hypothesis 3 was proposed:

H3: Digital transformation can enhance corporate performance sustainability through the pathway of increased green innovation.

2.3 The mediating role of top management’s environmental awareness

In the modern market environment, an awareness of digital transformation among enterprises has formed, but most enterprises have not developed a clear digital strategy or implementation path. The foci of digital transformation in many enterprises have been on how to introduce digital technology into production and operations as well as utilize digital technology information systems without a comprehensive digital layout from the strategic level of the enterprise [14]. As decision-makers in corporate strategy, top management plays a crucial role in digital transformation. Therefore, investigating the effect of digital transformation on the performance of corporate sustainable development and the role of top management factors are important for enhancing a company’s capabilities to corporate sustainable development [15].

Previous research on the relationship between corporate digital transformation and top management has primarily focused on analyzing individual attributes of top executives, such as gender [16], education level [17], and international experience [18], as well as broader characteristics such as management team diversity and consistency [19, 20]. However, there has been a significant lack in research addressing top management’s environmental consciousness. Drawing on the attention-based view, which holds that top management’s focus and cognitive engagement have a significant influence on resource allocation and regulation, it is clear that the interplay between external environmental pressures and internal managerial choices has a profound impact on firm decision-making dynamics [21]. As a result, top executives’ environmental awareness can have a significant impact on their organization’s environmental behavior and policy. When top managers place a high value on environmental awareness, it can result in a strategic orientation that supports green innovation from the top down [22]. This, in turn, stimulates a focus on improving green innovation capabilities and assures the availability of the essential resources—human, material, and financial—to develop an environmentally sustainable and innovative corporate culture. Such a strategic approach not only corresponds with the larger goals of sustainable development, but it also positions the company favorably in a competitive marketplace more sensitive to environmental concerns. Consequently, the following hypothesis was proposed:

H4: Digital transformation can enhance corporate performance sustainability through the pathway of increased levels of top management’s environmental awareness.

2.4 The moderating role of the institutional environment

New institutional economics emphasizes the role of the institutional environment in the process of economic and social development. Generally, regions with a higher level of institutional environment, due to their lower levels of information asymmetry and information transaction costs, along with a higher awareness of patent protection and intellectual property rights protection, possess a more favorable business environment [23]. The existent theories stated above have established that digital transformation can promote corporate sustainable development, but a better institutional environment can ensure the company’s effective implementation of corporate green innovation and effectively enhance top management’s environmental awareness. Specifically, although the process of digital transformation in enterprises is enabling sustainable development, it is constrained by specific social conditions and the institutional environment. Therefore, a better institutional environment can effectively transform digital transformation into productivity.

Building on the theory of institutional polycentricity, which states that power and authority are distributed across multiple centers, resulting in a complex tapestry of institutional influence at various levels, it is clear that institutional structures have a multifaceted and nuanced impact on corporate behavior [24]. This idea explains that no one institution, but rather a network of interrelated institutions, influences organizational actions and tactics. Within this complex structure, the institutional environment’s role in shaping how businesses respond to and incorporate digital transformation is very important. It emphasizes the reality that a corporation’s digital transformation journey is more than just a technological undertaking; it is profoundly enmeshed in and driven by the larger institutional framework.

In this setting, government agencies emerge as key stakeholders who actively shape the digital transformation landscape. Their impact is not uniform, but varies greatly depending on the maturity and peculiarities of the market economy in which a corporation operates [25]. This variation is significant because it implies that the effectiveness of digital transformation activities is dependent on the level of alignment and support offered by these institutional players. Recognizing the complexities of these dynamics, our approach to assessing the institutional environment employs the government-market relationship index. This measure provides a detailed view of the interplay between government policies and market dynamics, as well as a proxy for assessing institutional support for digital transformation initiatives.

The study of the interaction effects between the government-market relationship index and digital transformation efforts aims to reveal the moderating function that government support plays in the connection between digital transformation and market economy systems. It seeks to understand how varied levels of government engagement and facilitation might affect the outcomes of digital transformation, potentially accelerating or impeding a company’s ability to adapt and thrive in the digital era. By focusing on this interaction, the study acknowledges the critical role that institutional frameworks play in either enabling or constraining corporate innovation and adaptation strategies, thus offering deeper insights into the conditions under which digital transformation can most effectively contribute to corporate success and sustainability in the modern, complex institutional landscape [24, 25].

The following hypotheses were proposed:

H5: The institutional environment plays a positive moderating role in the mediating mechanism between digital transformation and green innovation.

H6: The institutional environment plays a positive moderating role in the mediating mechanism between digital transformation and top management’s environmental awareness.

3.1 Data collection and sample preprocessing

The digital transformation of the Chinese manufacturing industry was identified through textual analysis of annual reports from publicly listed companies, with the original annual report data sourced from Juchao Information. Similarly, the data on top management’s environmental awareness was derived using the textual analysis method (Li et al. [26]) on publicly listed companies’ annual reports. Data on the institutional environment were drawn from the research of Luo and Huang [27], wherein the government-market relationship index from the China Provincial Marketization Index Report (2021) was used for measurement. Additional data from databases such as Guotai’an and Wind, wherein information about Chinese A-share listed manufacturing companies between 2010 and 2022, were used. All of the data were processed as follows: (a) Samples with missing data were excluded; (b) extreme outliers were removed; (c) special treatment (ST) and *ST listed companies were excluded; and (d) all continuous variables were winsorized at the 1% and 99% levels to mitigate the influence of extreme values.

3.2 Model design and variable characteristics

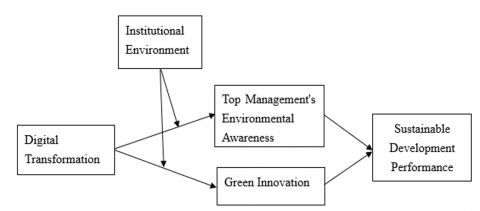

The research model of this study, as shown in Figure 1:

Figure 1. Research model

To assess the effect of digital transformation on corporate sustainable development performance, I constructed the primary regression model as follows:

$S{{D}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it}}$ (1)

$S{{D}_{it}}~$denotes the sustainable development performance of the enterprise, $Di{{g}_{it}}~$represents digital transformation, ${{X}_{it}}$ refers to various control variables, ${{\varphi }_{i~}}$indicates individual fixed effects, ${{\gamma }_{j}}$ denotes industry fixed effects, ${{\mu }_{t}}$ represents time fixed effects, and ${{\varepsilon }_{it}}$ is the random error term. ${{\alpha }_{0}}$ is the constant term, ${{\alpha }_{1}}$ represents the regression coefficient for the core explanatory variable digital transformation (Dig), and ${{\alpha }_{i}}~$represents the regression coefficients for other control variables.

To further investigate the effect of pathway of green innovation on enterprise sustainable development performance, I constructed the following mediation effect regression models:

$\text{GPaten}{{\text{t}}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it}}$ (2)

$S{{D}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}+{{\alpha }_{2}}\text{GPaten}{{\text{t}}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it}}$ (3)

$\text{GPaten}{{\text{t}}_{it}}~$refers to the level of green innovation, representing the number of green patents obtained by a listed company in the subsequent period (GPatent1) as well as the number of green patents obtained in collaboration with other entities in the subsequent period (GPatent2). The rest of the content is consistent with Eq. (1).

To further examine the effect of pathway of top management’s environmental awareness on enterprise sustainable development performance, I constructed additional mediation effect regression models as follows:

$\text{Envi}{{\text{r}}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it}}$ (4)

$S{{D}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}+{{\alpha }_{2}}\text{Envi}{{\text{r}}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it}}$ (5)

To examine the moderating role of the institutional environment (Inst) within the mediation mechanism, moderated mediation effects were established as follows:

Firstly, the moderated mediation effect of green innovation:

$\text{GPaten}{{\text{t}}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}+{{\alpha }_{2}}Ins{{t}_{it}}+{{\alpha }_{3}}Dig\text{*}Ins{{t}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it~}}$ (6)

$S{{D}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}++{{\alpha }_{2}}Ins{{t}_{it}}+{{\alpha }_{3}}Dig\text{*}Ins{{t}_{it}}+{{\alpha }_{4}}\text{GPaten}{{\text{t}}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it}}$ (7)

Secondly, the moderated mediation effect of green innovation:

$\text{Envi}{{\text{r}}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}+{{\alpha }_{2}}Ins{{t}_{it}}+{{\alpha }_{3}}Dig\text{*}Ins{{t}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it}}$ (8)

$S{{D}_{it}}={{\alpha }_{0}}+{{\alpha }_{1}}Di{{g}_{it}}++{{\alpha }_{2}}Ins{{t}_{it}}+{{\alpha }_{3}}Dig\text{*}Ins{{t}_{it}}+{{\alpha }_{4}}\text{Envi}{{\text{r}}_{it}}+{{\alpha }_{i}}{{X}_{it}}+{{\varphi }_{i}}+{{\gamma }_{j}}+{{\mu }_{t}}+{{\varepsilon }_{it}}$ (9)

Based on the regression models above, I conducted research on the relationship between digital transformation and corporate sustainable development performance. The four sections below explain the key variables involved in the models:

(1) Corporate Sustainable Development Performance

Sustainable development performance was divided into economic development performance and environmental social responsibility performance. The economic development performance was measured by the ROA in the year t+2, and the ESG was indicated by the corporate social responsibility rating score disclosed in the Hexun database for the year.

(2) Digital Transformation (Dig)

Following the approach of Wu et al. [28], the digital transformation index was constructed based on digital technologies (e.g., big data, artificial intelligence, cloud computing, blockchain). First, Python’s web scraping functionality was used to collect annual reports of Chinese A-share listed companies, and Java PDFbox library was employed to extract the full text content of each company’s annual report, serving as the text data pool [29]. Second, based on the digital transformation feature word map constructed by Wu et al. [28], the frequency of feature words in the annual report text data pool was counted. Ultimately, the aggregate frequency of these words formed the indicator system for corporate digital transformation (see Table 1).

(3) Mediating Variables

Green Innovation (GPatent): The numbers of green patents, including invention patents and utility model patents, that were obtained by the listed companies in the next period was used as a proxy for corporate green innovation.

Top management’s environmental awareness (Envir): In line with the measurement method of Li et al. [26] for top management’s environmental awareness, textual analysis was used to examine the annual reports of the listed companies. Key words were selected based on three dimensions: awareness of green competitive advantage, corporate social responsibility awareness, and perception of external environmental pressure (see Table 2).

Table 1. Digital transformation indicator system

|

Underlying Digital Technology Architecture |

Artificial Intelligence Technology |

Cloud Computing Technology |

|

Artificial Intelligence, Business Intelligence, Image Understanding, Investment Decision Support Systems, Intelligent Data Analysis, Intelligent Robots, Machine Learning, Deep Learning, Semantic Search, Biometric Technology, Face Recognition, Voice Recognition, Identity Verification, Autonomous Driving, Natural Language Processing |

Cloud Computing, Stream Computing, Graph Computing, In-Memory Computing, Multi-Party Secure Computing, Neuromorphic Computing, Green Computing, Cognitive Computing, Converged Architecture, Billion-Level Concurrency, Exabyte-Level Storage, Internet of Things, Cyber-Physical Systems |

|

|

Big Data Technology |

Blockchain Technology |

|

|

Big Data, Data Mining, Text Mining, Data Visualization, Heterogeneous Data, Credit Reporting, Augmented Reality, Mixed Reality, Virtual Reality |

Blockchain, Digital Currency, Distributed Computing, Differential Privacy Technology, Smart Financial Contracts |

|

|

Digital Application Technology |

Mobile Internet, Industrial Internet, Mobile Connectivity, Internet Healthcare, E-commerce, Mobile Payment, Third-Party Payment, NFC Payment, Smart Energy, B2B, B2C, C2B, C2C, O2O, Internet of Vehicles, Smart Wearables, Smart Agriculture, Intelligent Transportation, Smart Healthcare, Intelligent Customer Service, Smart Home, Robo-Advisors, Smart Culture and Tourism, Smart Environmental Protection, Smart Grid, Intelligent Marketing, Digital Marketing, Unmanned Retail, Internet Finance, Digital Finance, Fintech, Financial Technology, Quantitative Finance, Open Banking |

|

Table 2. Top management’s environmental awareness indicator system

|

Awareness of Green Competitive Advantage |

Energy Conservation and Emission Reduction, Environmental Protection Strategy, Environmental Protection Philosophy |

|

Corporate Social Responsibility Awareness |

Environmental Management Institutions, Environmental Education, Environmental Training, Environmental Technology Development, Environmental Auditing, Energy Conservation and Environmental Protection, Environmental Policies, Environmental Protection Departments, Environmental Inspection, Low-Carbon Environmental Protection, Environmental Protection Work |

|

Perception of External Environmental Pressure |

Environmental Governance, Environmental Protection and Environmental Management, Environmental Protection Facilities, Environmental Protection Related Laws and Regulations, Environmental Pollution Control |

The variable of top management’s environmental awareness for the listed companies was constructed based on the frequency of these terms in the company’s annual reports and was used to measure the green focus in the decision-making of corporate managers.

(4) Moderating Variable

Institutional Environment (Inst): In line with the research by Luo and Huang [27], this was measured using the "Government-Market Relationship Index" from the "China Provincial Marketization Index Report (2021)".

Table 3. Variable characteristics and corresponding codes

|

Description of Variables |

Variable Name |

Variable Code |

|

Dependent Variable |

Return on Total Assets in Year t+2 |

ROA |

|

Environmental Social Responsibility Performance in Year t+2 |

ESG |

|

|

Independent variable |

Digital Transformation |

Dig |

|

Mediating Variables |

Green Innovation |

GPatent |

|

|

Top Management’s Environmental Awareness |

Envir |

|

Moderating Variable |

Institutional Environment |

Inst |

|

Control Variables |

Company Size |

Size |

|

Debt-to-Asset Ratio |

Lev |

|

|

Company Growth |

Growth |

|

|

Company Age |

Age |

|

|

Tobin’s Q |

Tbq |

|

|

Cash Holding Level |

Cash |

|

|

CEO-Chair Duality |

Dual |

|

|

Big Four Audit |

Aud |

|

|

Equity Concentration of the Largest Shareholder |

Top1 |

|

|

Industry |

Ind |

|

|

Year |

Year |

Table 4. Descriptive statistics

|

Variable |

Obs |

Mean |

Std. Dev. |

Min |

Max |

|

f2ROA |

13254 |

5.293 |

7.234 |

-24.711 |

25.488 |

|

f2ESG |

13254 |

20.887 |

13.755 |

-3.75 |

72.93 |

|

Dig |

13254 |

5.543 |

12.91 |

0 |

83 |

|

GPatent1 |

13254 |

1.051 |

3.815 |

0 |

29 |

|

Envir |

13254 |

3.05 |

4.199 |

0 |

22 |

|

Inst |

13254 |

6.89 |

1.378 |

2.04 |

8.96 |

|

Size |

13254 |

21.911 |

1.158 |

19.781 |

25.38 |

|

Lev |

13254 |

39.361 |

20.524 |

4.965 |

93.63 |

|

Growth |

13254 |

14.546 |

28.623 |

-48.78 |

141.226 |

|

Age |

13254 |

18.101 |

5.231 |

8 |

35 |

|

Tbq |

13254 |

2.626 |

1.855 |

0 |

10.6 |

|

Cash |

13254 |

4.355 |

6.617 |

-14.975 |

22.621 |

|

Dual |

13254 |

.3 |

.458 |

0 |

1 |

|

Aud |

13254 |

.043 |

.203 |

0 |

1 |

|

Tpatentop1 |

13254 |

34.329 |

14.231 |

8.98 |

74.02 |

(5) Control Variables

To control for other variables’ effects on corporate sustainable development performance, I selected company size (Size), debt-to-asset ratio (Lev), company growth (Growth), return on equity (Roe), company age (Age), company value (Tbq), cash holdings level (Cash), CEO-Chair duality (Dual), whether audited by the Big Four (Aud), and equity concentration (Top1) as covariates. Additionally, I considered the effects of industry and year (i.e., fixed effects of industry and year, respectively; See Table 3). Table 3 shows the variables and their corresponding codes; Table 4 shows the descriptive statistics among these variables.

4.1 Regression results analysis

Table 5 shows the results of regression models wherein digital transformation (Dig) was the explanatory variable and indices of corporate sustainable development were the outcome variables. The regression coefficient of digital transformation was statistically significantly positive in both models (1) (0.0191, p < 0.05) and (2) (0.0310, p < 0.05), indicating that digital transformation enhanced the economic sustainable development performance and environmental sustainable development performance. Therefore, digital transformation had a main effect on the sustainable development of enterprises, which supported our H1 and H2.

Table 5. Regression results of digital transformation and corporate sustainable development

|

VARIABLES |

(1) F2.ROA |

(2) F2.ESG |

|

Dig |

0.0191*** |

0.0310*** |

|

(4.262) |

(3.567) |

|

|

Size |

-3.603*** |

-1.155*** |

|

(-22.05) |

(-3.632) |

|

|

Lev |

0.0158*** |

-0.0254** |

|

(2.867) |

(-2.369) |

|

|

Growth |

0.0150*** |

0.0227*** |

|

(7.670) |

(5.942) |

|

|

Age |

-0.181 |

-0.917** |

|

(-0.840) |

(-2.181) |

|

|

Tbq |

0.000426 |

0.331*** |

|

(0.00937) |

(3.738) |

|

|

Cash |

0.0490*** |

0.0718*** |

|

(4.924) |

(3.705) |

|

|

Dual |

-0.0883 |

-0.181 |

|

(-0.465) |

(-0.490) |

|

|

Aud |

0.203 |

-2.059* |

|

(0.326) |

(-1.700) |

|

|

Top1 |

0.0462*** |

0.0639*** |

|

(4.587) |

(3.258) |

|

|

Constant |

83.26*** |

65.01*** |

|

(17.87) |

(7.173) |

|

|

Year |

Y |

Y |

|

Ind |

Y |

Y |

|

Observations |

13,254 |

13,254 |

|

R-squared |

0.075 |

0.144 |

t-values in parentheses *** p < .01, ** p < . 05, * p < .1

4.2 Endogeneity test

Considering the potential endogeneity issues due to omitted variables and the reciprocal causality between digital transformation of Chinese manufacturing enterprises and corporate sustainable development variables, I employed the instrumental variable (IV) method for correction. Through the IV method, I created a variable Dig_IV, whcih was the cube root of the difference between the company’s level of digital transformation and the average level of digital transformation across all companies in the same industry and province. Afterwards, the endogeneity issue was tested through a two-stage regression.

Table 6 shows the specific regression results, where models (1) (0.0134, p < 0.05) and (2) (0.0262, p < 0.05), indicate a positive association between digital transformation and corporate sustainable development performance, suggesting that digital transformation effectively promotes corporate sustainable development performance. The Cragg-Donald Wald F statistic of 3029.84 was significantly greater than the critical value, and thus the null hypothesis was rejected. The F-robust or Kleibergen-Paap rk LM (Kleibergen-Paap, 2006) statistic of 2268.118 (p < .01) showed that the null hypothesis should be rejected, and thus confirmed that the chosen instrument variable effectively addresses the endogeneity of variables.

The Heckman two-stage model was used to address the sample selection bias (or the corresponding endogeneity). In the current study, selection bias could be present when companies, especially those who were concerned about their environmental sustainable development performances, chose not to disclose their information. In the first stage, a probit model was used to regress the factors affecting the selection process on the tentative outcome variable (i.e., the obtained estimates of this selection probability, represented by the IMR value), which was later used to correct sample bias. In the second stage, the IMR variable was included in the original regression model to obtain the results from the Heckman regression model (see Table 6). The regression results from models (3) (0.0191, p < 0.05) and (4) (0.0308, p < 0.05) indicated a statistically significant positive association between digital transformation and corporate sustainable development performance, which corroborated the validity of the main regression results of the current study.

4.3 Robustness test

To ensure the validity of the regression results above, I conducted a series of robustness tests. First, the number of lag periods was changed, which extended the lag by one more period to examine if the results would still hold. Second, I located enterprises that had not undergone digital transformation (i.e., some enterprises did not undergo digital transformation) during the time period, identified those with a digital transformation index value of zero, and excluded them from the robustness testing. The results of this testing are shown in Table 7, wherein the regression coefficients for the digital transformation were statistically significantly positive in the lagged period (0.0150, p < 0.05; 0.0264, p < 0.05),indicating that digital transformation promoted the sustainable development performance of enterprises in the following year. Models (3) (0.016, p < 0.05) and (4) (0.0224, p < 0.05) indicated that digital transformation positively affected corporate sustainable development performance. The results of the robustness testing showed that our previous regression results were credible.

4.4 The mediating role of green innovation

I used a mediation effect model to test the mechanism of green innovation (see Table 8). Model (1) indicated a statistically significant positive association between digital transformation and green innovation (0.0254, p < 0.05). The results of Model (2) demonstrated a statistically significant positive association between green innovation and sustainable development economic performance (0.0294, p < 0.05). Model (3) showed a statistically significant positive association between green innovation and sustainable development environmental performance (0.0994, p < 0.05). This shows that green innovation capability played a mediating role between digital transformation and corporate sustainable development performance. Digital transformation appeared to bring in stronger capabilities of green innovation to enterprises (e.g., more quality resources, talents for green product innovation) and in turn improve sustainable development of enterprises by enhancing both corporate financial performance and environmental performance.

4.5 The mediating role of top management’s environmental awareness

In Table 9, the results of Model (1) indicated a statistically significant positive association between digital transformation and top management’s environmental awareness (0.0110, p < 0.05). Model (2) showed a statistically significant positive association between top management’s environmental awareness and sustainable development economic performance (0.0626, p < 0.05). Model (3) showed a statistically significant positive association between top management’s environmental awareness and sustainable development environmental performance (0.102, p < 0.05). This indicated that top management’s environmental awareness played a mediating role between digital transformation and corporate sustainable development performance.

4.6 The moderating role of the institutional environment

By adding the mediating variables and the interaction by digital transformation and the institutional environment into the baseline regression model, the moderation effect on the association between digital transformation and corporate sustainable development performance was tested (see Table 10). Models (1) to (3) showed the moderated mediation effect of green innovation. The regression results indicated a statistically significant positive interaction effect by corporate digital transformation and the institutional environment on the association between corporate digital transformation and green innovation (0.00113, p < 0.05). Furthermore, this interaction also had a statistically significant positive effect on corporate sustainable economic (0.00689, p < 0.05) and environmental performance (0.0113, p < 0.05).

In regions with better institutional environments, green innovation can better support the effect of digital transformation on corporate sustainable development. Models (4) to (6) in Table 10 showed the moderated mediation effect models via top management’s environmental awareness (see Figure 1). These results showed a statistically significant positive interaction by corporate digital transformation and the institutional environment on the association between digital transformation and top management’s environmental awareness (0.00419, p < 0.05), suggesting that in regions with a higher institutional environment, digital transformation promoted top management’s environmental awareness. This interaction also had a statistically significant positive effect on corporate sustainable development performance (0.00741, p < 0.05; 0.0108, p < 0.05), indicating that the institutional environment served as a positive moderating role in the mediating effect of top management’s environmental awareness on the association between digital transformation and institutional environment. Additionally, the tests for the mediating variables green innovation capability and top management’s environmental awareness also showed statistically significant effects on corporate sustainable development performance.

Table 6. Instrumental variable method two-stage least squares (2SLS) and heckman tests

|

VARIABLES |

(1) 2SLS F2.ROA |

(2) 2SLS F2.ESG |

(1) Heckman F2.ROA |

(2) Heckman F2.ESG |

|

Dig |

0.0134** |

0.0262** |

0.0191*** |

0.0308*** |

|

(2.380) |

(2.359) |

(4.271) |

(3.537) |

|

|

Imr |

|

|

7.405 |

-51.39*** |

|

|

|

(1.207) |

(-4.307) |

|

|

Size |

0.493*** |

2.485*** |

-4.673*** |

6.270*** |

|

(7.346) |

(18.82) |

(-5.184) |

(3.577) |

|

|

Lev |

-0.0523*** |

-0.124*** |

0.0427* |

-0.212*** |

|

(-15.68) |

(-18.89) |

(1.861) |

(-4.751) |

|

|

Growth |

0.0220*** |

0.0267*** |

0.00181 |

0.114*** |

|

(10.85) |

(6.689) |

(0.162) |

(5.287) |

|

|

Age |

0.00329 |

-0.148*** |

-0.247 |

-0.462 |

|

(0.291) |

(-6.630) |

(-1.108) |

(-1.067) |

|

|

Tbq |

0.493*** |

0.228*** |

-0.326 |

2.597*** |

|

(13.90) |

(3.269) |

(-1.188) |

(4.868) |

|

|

Cash |

0.318*** |

0.350*** |

0.0723*** |

-0.0897** |

|

(35.01) |

(19.58) |

(3.331) |

(-2.126) |

|

|

Dual |

-0.108 |

-0.638** |

-1.065 |

6.597*** |

|

(-0.848) |

(-2.546) |

(-1.281) |

(4.081) |

|

|

Aud |

0.714** |

3.552*** |

0.986 |

-7.491*** |

|

(2.380) |

(6.016) |

(1.096) |

(-4.286) |

|

|

Top1 |

0.0401*** |

0.0680*** |

0.0555*** |

-0.000231 |

|

(9.615) |

(8.294) |

(4.383) |

(-0.00938) |

|

|

Constant |

-7.805*** |

-30.66*** |

101.4*** |

-61.10** |

|

(-5.482) |

(-10.95) |

(6.435) |

(-1.994) |

|

|

Cragg-Donald Wald F |

6189.539 |

6189.539 |

|

|

|

Kleibergen-Paap rk LM |

4221.587(0.000) |

4221.587(0.000) |

|

|

|

Observations |

13,254 |

13,254 |

13,254 |

13,254 |

|

R-squared |

0.175 |

0.117 |

0.075 |

0.145 |

z-scores in parentheses *** p < .01, ** p < .05, * p < .1

Table 7. Results of robustness tests

|

VARIABLES |

(1) Lagged by one more period F.ROA |

(2) Lagged by one more period F.ESG |

(3) Excluding Non-Digitalized Enterprises F.ROA |

(4) Excluding Non-Digitalized Enterprises F.ESG |

|

Dig |

0.0150*** |

0.0264*** |

0.0160*** |

0.0224** |

|

(3.260) |

(2.679) |

(3.138) |

(2.457) |

|

|

Size |

-2.651*** |

0.551 |

-3.633*** |

-1.798*** |

|

(-14.97) |

(1.456) |

(-13.07) |

(-3.620) |

|

|

Lev |

0.00665 |

-0.0439*** |

0.0112 |

-0.0103 |

|

(1.100) |

(-3.397) |

(1.169) |

(-0.603) |

|

|

Growth |

0.0354*** |

0.0348*** |

0.0135*** |

0.0116** |

|

(17.48) |

(8.044) |

(4.655) |

(2.228) |

|

|

Age |

-0.315 |

-0.978* |

-0.494 |

-1.054* |

|

(-1.233) |

(-1.793) |

(-1.638) |

(-1.956) |

|

|

Tbq |

0.387*** |

0.298*** |

-0.103 |

0.239** |

|

(7.786) |

(2.811) |

(-1.610) |

(2.095) |

|

|

Cash |

0.124*** |

0.119*** |

0.0340** |

0.0286 |

|

(11.53) |

(5.200) |

(2.238) |

(1.052) |

|

|

Dual |

0.118 |

-0.469 |

-0.149 |

0.0153 |

|

(0.574) |

(-1.072) |

(-0.530) |

(0.0305) |

|

|

Aud |

0.892 |

0.566 |

0.852 |

-2.241 |

|

(1.325) |

(0.394) |

(0.903) |

(-1.328) |

|

|

Top1 |

0.0421*** |

0.0760*** |

0.0439*** |

0.0240 |

|

(3.928) |

(3.317) |

(2.678) |

(0.819) |

|

|

Constant |

64.59*** |

30.54*** |

89.26*** |

83.62*** |

|

(11.79) |

(2.608) |

(12.15) |

(6.367) |

|

|

Year |

Y |

Y |

Y |

Y |

|

Ind |

Y |

Y |

Y |

Y |

|

Observations |

11,077 |

11,077 |

7,003 |

7,003 |

|

R-squared |

0.107 |

0.147 |

0.074 |

0.156 |

t-values in parentheses *** p < .01, ** p < .05, * p < .1

Table 8. Test of the mediating effect of green innovation

|

VARIABLES |

(1) GPatent |

(2) F2.ROA |

(3) F2.ESG |

|

Dig |

0.0254*** |

0.0208*** |

0.0381*** |

|

(9.764) |

(6.233) |

(5.818) |

|

|

GPatent |

|

0.0294* |

0.0994*** |

|

|

(1.829) |

(3.140) |

|

|

Size |

1.024*** |

0.518*** |

2.512*** |

|

(28.00) |

(7.439) |

(18.34) |

|

|

Lev |

-0.00213 |

-0.0503*** |

-0.114*** |

|

(-1.175) |

(-14.98) |

(-17.17) |

|

|

Growth |

-0.00132 |

0.0214*** |

0.0255*** |

|

(-1.215) |

(10.64) |

(6.438) |

|

|

Age |

-0.0208*** |

-0.0101 |

-0.171*** |

|

(-3.407) |

(-0.894) |

(-7.652) |

|

|

Tbq |

0.113*** |

0.498*** |

0.172** |

|

(5.891) |

(13.92) |

(2.451) |

|

|

Cash |

0.00162 |

0.297*** |

0.322*** |

|

(0.326) |

(32.28) |

(17.82) |

|

|

Dual |

0.214*** |

-0.0735 |

-0.701*** |

|

(3.121) |

(-0.579) |

(-2.808) |

|

|

Aud |

1.978*** |

0.705** |

3.359*** |

|

(12.24) |

(2.341) |

(5.668) |

|

|

Top1 |

-0.0115*** |

0.0424*** |

0.0766*** |

|

(-5.082) |

(10.09) |

(9.265) |

|

|

Constant |

-21.72*** |

-7.457*** |

-29.53*** |

|

(-26.96) |

(-4.871) |

(-9.802) |

|

|

Year |

Y |

Y |

Y |

|

Ind |

Y |

Y |

Y |

|

Observations |

13,254 |

13,254 |

13,254 |

|

R-squared |

0.153 |

0.191 |

0.133 |

t-values in parentheses *** p < .01, ** p < .05, * p < .1

Table 9. Test of the mediating effect of top management's environmental awareness

|

VARIABLES |

(1) Envir |

(2) F2.ROA |

(3) F2.ESG |

|

Dig |

0.0110*** |

0.0184*** |

0.0299*** |

|

(5.285) |

(4.104) |

(3.434) |

|

|

Envir |

|

0.0626*** |

0.102** |

|

|

(3.065) |

(2.574) |

|

|

Size |

0.108 |

-3.610*** |

-1.166*** |

|

(1.421) |

(-22.10) |

(-3.668) |

|

|

Lev |

-0.00825*** |

0.0163*** |

-0.0246** |

|

(-3.214) |

(2.961) |

(-2.290) |

|

|

Growth |

0.000903 |

0.0150*** |

0.0226*** |

|

(0.990) |

(7.644) |

(5.919) |

|

|

Age |

0.309*** |

-0.201 |

-0.949** |

|

(3.072) |

(-0.929) |

(-2.256) |

|

|

Tbq |

-0.0206 |

0.00172 |

0.333*** |

|

(-0.972) |

(0.0377) |

(3.763) |

|

|

Cash |

0.0207*** |

0.0477*** |

0.0697*** |

|

(4.465) |

(4.792) |

(3.594) |

|

|

Dual |

-0.00169 |

-0.0882 |

-0.181 |

|

(-0.0191) |

(-0.464) |

(-0.489) |

|

|

Aud |

-0.228 |

0.217 |

-2.035* |

|

(-0.788) |

(0.349) |

(-1.681) |

|

|

Top1 |

0.00123 |

0.0462*** |

0.0638*** |

|

(0.262) |

(4.581) |

(3.253) |

|

|

Constant |

-4.337** |

83.53*** |

65.46*** |

|

(-2.001) |

(17.94) |

(7.222) |

|

|

Year |

Y |

Y |

Y |

|

Ind |

Y |

Y |

Y |

|

Observations |

13,254 |

13,254 |

13,254 |

|

R-squared |

0.107 |

0.075 |

0.144 |

t-values in parentheses *** p < .01, ** p < .05, * p < .1

Table 10. Moderating effect of institutional environment in the mediation mechanism

|

VARIABLES |

(1) Green Innovation GPatent2 |

(2) Green Innovation F2.ROA |

(3) Green Innovation F2.ESG |

(4) Top Management's Environmental Awareness Envir |

(5) Top Management's Environmental Awareness F2.ROA |

(6) Top Management's Environmental Awareness F2.ESG |

|

Dig |

0.00572*** |

0.0249*** |

0.0579*** |

0.0218*** |

0.0272*** |

0.0548*** |

|

(9.088) |

(6.766) |

(7.850) |

(10.03) |

(7.667) |

(7.189) |

|

|

Inst |

0.0266*** |

0.256*** |

0.939*** |

-0.101*** |

0.134*** |

1.104*** |

|

(4.633) |

(5.861) |

(9.243) |

(-3.855) |

(3.126) |

(10.70) |

|

|

Dig*inst |

0.00113*** |

0.00689** |

0.0113* |

0.00419** |

0.00741** |

0.0108* |

|

(3.036) |

(2.321) |

(1.816) |

(2.311) |

(2.500) |

(1.735) |

|

|

GPatent |

|

0.0271* |

0.280** |

|

|

|

|

|

(1.685) |

(2.034) |

|

|

|

|

|

Envir |

|

|

|

|

0.0305** |

0.0633** |

|

|

|

|

|

(2.151) |

(1.995) |

|

|

Size |

0.179*** |

0.551*** |

1.752*** |

0.514*** |

0.675*** |

1.928*** |

|

(19.58) |

(7.906) |

(11.53) |

(12.29) |

(9.837) |

(12.62) |

|

|

Lev |

-0.000885** |

-0.0492*** |

-0.0971*** |

0.00940*** |

-0.0555*** |

-0.0883*** |

|

(-1.977) |

(-14.59) |

(-13.12) |

(4.586) |

(-16.58) |

(-11.90) |

|

|

Growth |

-1.15e-05 |

0.0210*** |

0.0244*** |

-0.00240* |

0.0234*** |

0.0233*** |

|

(-0.0419) |

(10.44) |

(6.407) |

(-1.909) |

(11.39) |

(6.132) |

|

|

Age |

-0.00146 |

-0.0131 |

-0.297*** |

-0.00877 |

0.0290** |

-0.316*** |

|

(-0.917) |

(-1.154) |

(-11.33) |

(-1.204) |

(2.441) |

(-12.08) |

|

|

Tbq |

0.0172*** |

0.501*** |

0.120* |

-0.244*** |

0.633*** |

0.0729 |

|

(3.314) |

(14.04) |

(1.706) |

(-10.25) |

(16.26) |

(1.032) |

|

|

Cash |

-0.000522 |

0.293*** |

0.247*** |

0.0332*** |

0.314*** |

0.226*** |

|

(-0.430) |

(31.90) |

(13.69) |

(5.968) |

(34.62) |

(12.44) |

|

|

Dual |

0.0745*** |

-0.132 |

-0.844*** |

-0.368*** |

-0.0496 |

-0.901*** |

|

(4.366) |

(-1.038) |

(-3.071) |

(-4.715) |

(-0.389) |

(-3.302) |

|

|

Aud |

0.562*** |

0.565* |

3.389*** |

-0.823*** |

0.419 |

3.376*** |

|

(14.03) |

(1.872) |

(4.819) |

(-4.491) |

(1.401) |

(4.859) |

|

|

Top1 |

-0.00309*** |

0.0417*** |

0.0846*** |

0.00277 |

0.0362*** |

0.0870*** |

|

(-5.573) |

(9.939) |

(8.786) |

(1.094) |

(8.737) |

(9.019) |

|

|

Constant |

-3.880*** |

-9.682*** |

-19.08*** |

-7.660*** |

-12.02*** |

-21.50*** |

|

(-19.12) |

(-6.155) |

(-5.701) |

(-8.261) |

(-7.920) |

(-6.214) |

|

|

Year |

Y |

Y |

Y |

Y |

Y |

Y |

|

Ind |

Y |

Y |

Y |

Y |

Y |

Y |

|

Observations |

13,254 |

13,254 |

13,254 |

13,254 |

13,254 |

13,254 |

|

R-squared |

0.083 |

0.193 |

0.226 |

0.096 |

0.189 |

0.256 |

t-statistics in parentheses *** p < .01, ** p < .05, * p < .1

Based on data from Chinese A-share listed companies from 2010 to 2021, I constructed corporate digitalization indicators and top management’s green awareness indicators using Python technology. I employed analyses with data obtained from the Wind and CSMAR databases to explore the relationship between digital transformation and corporate sustainable development performance, which yields the following conclusions. First, digital transformation promotes both the economic sustainable development performance and the environmental sustainable development performance among Chinese enterprises. The validity of these results was confirmed through endogeneity and robustness testing. Second, the association between digital transformation and corporate sustainable development include the mediating mechanisms via two pathways: green innovation and top management’s environmental awareness. I found that digital transformation improved corporate sustainable development performance levels through the pathways of enhancing corporate green innovation capabilities and top management’s awareness levels. Third, the institutional environment plays a positive moderating role in the mediation effect between digital transformation and corporate sustainable development. The results indicate that in regions with better and more robust institutional environments, the effects of digital transformation on green innovation and top management’s environmental awareness are greater. This suggests that improvements in the institutional environment may effectively enhance the role of digital transformation in promoting corporate green innovation and elevating top management’s environmental consciousness.

The implications of this study are as follows: First, businesses are encouraged to expedite their digital transformation, with a focus on sustainability goals. This includes making significant investments in digital technologies like as big data analytics, cloud computing, and the Internet of Things (IoT). These technologies should be used to optimize resource utilization, improve energy efficiency, and promote green production innovation. Adopting IoT for real-time monitoring of energy consumption could be a practical step toward identifying and reducing inefficiencies. Enterprises should also devise a detailed digital transformation plan that specifies benchmarks and objectives for green development, such as decarbonizing manufacturing processes through technological advancements.

Furthermore, it is critical to regard green development as a strategic priority. Enterprises should embed green development goals within their long-term strategic planning. This includes setting clear, measurable targets for reducing the environmental footprint of their manufacturing processes, developing new eco-friendly technologies, and optimizing existing processes to curtail pollution and energy use. Seeking certification for environmental standards, such as ISO 14001, can also help the company demonstrate its commitment to sustainable operations and improve its reputation.

Another critical area is strengthening collaborative innovation. Manufacturing companies should collaborate with research institutions and other businesses to create environmentally friendly new products and materials. This could include organizing or joining industrial consortiums focusing on green innovation, as well as investing in R&D projects targeted at developing sustainable product lines or improving the environmental performance of existing products.

Increasing business environmental awareness and incorporating sustainability into corporate strategy are also important ideas. This includes providing frequent training to leaders and employees to foster a culture of environmental awareness and sustainable development. Sustainable development goals should be integrated into the fabric of company strategy and decision-making, with projects and investments prioritized according to their environmental impact.

Finally, it is vital to capitalize on external opportunities and adapt to regulatory changes. Enterprises should be aware about and respond to changes in the external institutional environment, such as new legislation and policy incentives for sustainability. Participating in government sustainability initiatives and using governmental incentives for green technology investments can help an organization’s sustainability efforts.

Chinese manufacturing businesses can greatly improve their performance in terms of sustainable development by implementing these practical guidelines. This not only coincides with the Chinese government’s sustainable development goals, but also provides a competitive edge in the marketplace, establishing these businesses as leaders in green innovation and corporate social responsibility.

The author would like to express their gratitude to the anonymous reviewer for offering constructive comments on the manuscript.

[1] Ghobakhloo, M. (2020). Industry 4.0, digitization, and opportunities for sustainability. Journal of Cleaner Production, 252: 119869. https://doi.org/10.1016/j.jclepro.2019.119869

[2] Ford, S., Despeisse, M. (2016). Additive manufacturing and sustainability: An exploratory study of the advantages and challenges. Journal of Cleaner Production, 137: 1573-1587. https://doi.org/10.1016/j.jclepro.2016.04.150

[3] Jamal, T., Zahid, M., Martins, J.M., Mata, M.N., Rahman, H.U., Mata, P.N. (2021). Perceived green human resource management practices and corporate sustainability: Multigroup analysis and major industries perspectives. Sustainability, 13(6): 3045. https://doi.org/10.3390/su13063045

[4] Nadkarni, S., Prügl, R. (2021). Digital transformation: A review, synthesis and opportunities for future research. Management Review Quarterly, 71: 233-341. https://doi.org/10.1007/s11301-020-00185-7

[5] Zajac, E.J., Kraatz, M.S., Bresser, R.K. (2000). Modeling the dynamics of strategic fit: A normative approach to strategic change. Strategic Management Journal, 21(4): 429-453. https://doi.org/10.1002/(SICI)1097-0266(200004)21:4<429:AID-SMJ81>3.0.CO;2-%23

[6] Liu, F., Wu, W. (2023). Digital transformation and ESG performance of enterprises under the double carbon goal effect and impact mechanism. Science & Technology Progress and Policy, 12(28): 1-9. https://doi.org/10.6049/kjjbydc.H202307135

[7] Zhao, C., Wang, W., Li, X. (2021). How does digital transformation affect the total factor productivity of enterprises? Finance & Trade Economics, 42(7): 114-129. https://doi.org/10.19795/j.cnki.cn11-1166/f.20210705.001

[8] Tan, K.H., Ji, G., Lim, C.P., Tseng, M.L. (2017). Using big data to make better decisions in the digital economy. International Journal of Production Research, 55(17): 4998-5000. https://doi.org/10.1080/00207543.2017.1331051

[9] Feroz, A.K., Zo, H., Chiravuri, A. (2021). Digital transformation and environmental sustainability: A review and research agenda. Sustainability, 13(3): 1530. https://doi.org/10.3390/su13031530

[10] Chen, Y.S., Lai, S.B., Wen, C.T. (2006). The influence of green innovation performance on corporate advantage in Taiwan. Journal of Business Ethics, 67: 331-339. https://doi.org/10.1007/s10551-006-9025-5

[11] Diaz-Moriana, V., Clinton, E., Kammerlander, N., Lumpkin, G.T., Craig, J.B. (2020). Innovation motives in family firms: A transgenerational view. Entrepreneurship Theory and Practice, 44(2): 256-287. https://doi.org/10.1177/1042258718803051

[12] Guo, M., Du, C. (2019). Mechanism and effect of information and communication technology on enhancing the quality of China’s economic growth. Statistical Research, (3): 3-16. https://doi.org/10.19343/j.cnki.11-1302/c.2019.03.001

[13] Qi, P., Song, W. (2024). Digital transformation, and innovation-driven development and high-quality development of the manufacturing value chain. Journal of Guangdong University of Finance & Economics, (1): 4-18.

[14] Lv, T. (2019). The trend and path of digital transformation of traditional industries. People’s Forum Academic Frontiers, (18): 13-19. https://doi.org/10.16619/j.cnki.rmltxsqy.2019.18.002

[15] Wrede, M., Velamuri, V.K., Dauth, T. (2020). Top managers in the digital age: Exploring the role and practices of top managers in firms’ digital transformation. Managerial and Decision Economics, 41(8): 1549-1567. https://doi.org/10.1002/mde.3202

[16] Zhao, K., Zhang, K. (2024). The impact of gender diversity in the board of directors on digital transformation of enterprises. Management and Administration, (5): 1-12. https://doi.org/10.16517/j.cnki.cn12-1034/f.20240015.005

[17] Wang, Y. (2023). Executive academic capital and enterprise digital transformation. Science Technology and Industry, (15): 102-107.

[18] Cao, H., Ma, Y., Ding, Y. (2023). Overseas executives and corporate digital transformation-Empirical evidence from Chinese a-share listed companies. Journal of Financial Development Research, (9): 22-30. https://doi.org/10.19647/j.cnki.37-1462/f.2023.09.003

[19] Zhou, Z., Liu, L., Sun, X. (2023). Heterogeneity of executive teams, digital transformation, and enterprise R&D investment. Friends of Accounting, (24): 115-122.

[20] Wang, H., Lu, Y., Song, T. (2023). Seeking change in stability? TMT stability and enterprise digital transformation. R&D Management, (2): 97-110. https://doi.org/10.13581/j.cnki.rdm.20220674

[21] Zhang, M., Lan, H., Chen, W. (2018). A literature review of attention-based view of the firm: Knowledge base, evolution process, and research front. Business Management Journal, (9): 189-208. https://doi.org/10.19616/j.cnki.bmj.2018.09.012

[22] Dragomir, V.D., Dragomir, V.D. (2020). Ethical aspects of environmental strategy. Corporate Environmental Strategy: Theoretical, Practical, and Ethical Aspects, 75-113. https://doi.org/10.1007/978-3-030-29548-6_3

[23] Yin, X., Wei, M. (2023). Technology finance investment, digital transformation, and transformation of new and old driving forces: Based on the perspective of institutional environment. Statistics & Decision, (23): 150-155. https://doi.org/10.13546/j.cnki.tjyjc.2023.23.027

[24] Ostrom, E. (2009). Understanding Institutional Diversity. Princeton University Press. https://doi.org/10.1515/9781400831739

[25] Hanelt, A., Bohnsack, R., Marz, D., Antunes Marante, C. (2021). A systematic review of the literature on digital transformation: Insights and implications for strategy and organizational change. Journal of Management Studies, 58(5): 1159-1197. https://doi.org/10.1111/joms.12639

[26] Li, Y., Xia, Y., Zhao, Z. (2023). The relationship between executives’ green perception and firm performance in heavy-pollution industries: A moderated mediating effect model. Science & Technology Progress and Policy, (7): 113-123. https://doi.org/10.6049/kjjbydc.2022030266

[27] Luo, E., Huang, Z. (2023). Executive incentives, institutional environment and exploratory innovation in high tech enterprises executive incentives, institutional environment and exploratory innovation in high tech enterprises. Management and Administration, (1): 90-97. https://doi.org/10.16517/j.cnki.cn12-1034/f.20230216.003

[28] Wu, F., Hu, H., Lin, H., Ren, X. (2021). Enterprise digital transformation and capital market performance: Empirical evidence from stock liquidity. Journal of Management World, (7): 130-144+10. https://doi.org/10.19744/j.cnki.11-1235/f.2021.0097

[29] Zhang, S., Balog, K. (2020). Web table extraction, retrieval, and augmentation: A survey. ACM Transactions on Intelligent Systems and Technology (TIST), 11(2): 1-35. https://doi.org/10.1145/3372117