Tetyana Medynska![]() | Nataliia Loboda

| Nataliia Loboda![]() | Nataliia Nohinova

| Nataliia Nohinova![]() | Nadiya Oliynyk

| Nadiya Oliynyk![]() | Yuliia Borutska*

| Yuliia Borutska*![]()

© 2024 The authors. This article is published by IIETA and is licensed under the CC BY 4.0 license (http://creativecommons.org/licenses/by/4.0/).

OPEN ACCESS

The purpose of the article is to propose a new methodological approach to optimizing ecological taxation by determining its role in environmental protection. The object of study is the environment and ecological taxation. The scientific question is to establish how to optimize ecological taxation in such a way as to ensure a high level of environmental safety. For this purpose, simulation modeling and correlation and regression analysis were carried out. Based on the results, it was determined that it was the scenario of increasing revenues from emissions into the atmosphere, from discharges into water bodies, and from the ecological taxation that is levied for the generation of radioactive waste that is the best in terms of optimization. It was proposed to increase revenues from emissions into the atmosphere, from discharges into water bodies, and the ecological taxation levied for the generation of radioactive waste: a review and increase in tax rates on pollutant emissions. The study is limited by taking into account the specifics of only one country during optimization and therefore the variables are selected only after this.

ecological taxation, environmental, nature, environmental protection, modeling, optimization

Climate change is recognized as the greatest threat to nature and humanity in the 21st century. To combat climate change and overcome its negative consequences, international organizations and leading countries of the world have joined forces, so the direction of their joint work has become to prevent the consequences of environmental challenges, primarily in promoting the development of renewable energy and increasing the energy efficiency of economic sectors. A large number of international treaties and conventions of an environmental nature are evidence of the growing scale and intensity of the impact of human activity on the environment. As a result, the problems of maximizing the effectiveness of regulatory instruments, in particular ecological taxations, remain constantly relevant. To implement and reform ecological taxations, the government must first define environmental goals, i.e., a qualitatively desirable environmental standard (for example, this consists of establishing acceptable emission levels following environmental policy assumptions). Then the appropriate tax bases should be selected and a tax imposed on them that should lead to the achievement of the intended standard. After some time, it is checked to what extent the goal has been achieved, and, depending on this, the tax is increased or decreased to find the optimal rate.

As part of our research, we cannot explore and propose ways to optimize the ecological taxation of all possible countries on planet Earth. Each is an individual with its external environment. We chose Sweden, where the authors of the article had more than 5 years of experience (Figure 1).

Figure 1. Environment in Sweden [1]

The study of tax issues in the context of environmental protection is extremely relevant because it combines two critical areas of modern society: economic development and environmental sustainability. Taxation, as an effective public policy tool, can play a key role in encouraging businesses and individual consumers to behave more environmentally responsible. Placing taxes on carbon emissions, plastic use, or other environmentally harmful practices can encourage companies to adopt cleaner technologies and reduce pollution. On the other hand, tax breaks and other financial incentives can encourage the development and use of renewable energy sources such as solar and wind power, which are critical to reducing global carbon emissions. In addition, taxation can be a tool to raise funds for environmental projects and initiatives, such as the protection of natural areas, the development of environmentally friendly technologies and education in the field of sustainable development. It is also important that the tax system can ensure that the costs and benefits of environmental protection measures are shared fairly, ensuring that the financial burden does not fall solely on the poorer segments of the population.

The distribution of ecological taxations at the state level reflects the level of revenue they generate. There are many environmental barriers and counterarguments regarding the need to reform this type of tax, set higher rates, or change the object of taxation, and therefore it becomes relevant to study the evolution of ecological taxation to determine the strengths and weaknesses of its effectiveness in Sweden. All this leads us to the scientific opinion to set ourselves the goal of proposing a new methodological approach to optimizing the ecological tax by determining its role in environmental protection.

The structure of the article includes a literature review, a presentation of the main results, their discussion, and a conclusion. Modeling methods are proposed as the main ones for optimization.

The results of the analysis are reflected in Figure 2 and indicate that the topic of ecological taxation is being updated in research articles of various directions, starting as an instrument of state regulation of emissions, and ending with a necessary lever for making eco-innovative decisions.

Figure 2. Results of bibliometric analysis of keyword matches for the query - ecological taxation

For example, Omodero et al. [2] and Borutska et al. [3] focus on assessing the environmental safety of regions and optimizing their overall constraints. In such works, one can find parallels in the context of the impact of ecological taxation on the economy, and also consider how the introduction of such taxes can stimulate or suppress investment in environmental projects. Scientists consider ecological taxation as a tool for managing the impact on the environment, especially in areas that directly interact with natural resources. environment, for example in ecotourism.

Other literature, Xu et al. [4], Singh et al. [5], and Salamatov et al. [6] focus on environmental security and ecosystem services in response to land use changes in the coastal zone. Information from these sources can be useful in understanding how ecological taxation optimization can influence the environmental assessment of land resources and contribute to more sustainable land use.

In doing so, Deswanto and Siregar [7], Kovács‐Hostyánszki et al. [8], and Feng et al. [9] examine the relationship between companies' environmental reports and their financial performance, environmental performance, and company value. This can help to understand the importance of transparency in environmental performance and its impact on financial performance, which is important in the context of ecological taxation optimization. Considering ecological intensification methods to mitigate the negative impacts of intensive land use on pollinators. The results can be used to argue for the importance of ecological taxation as an incentive for more sustainable land use.

Also note that Venkateswarlu et al. [10], Zhan et al. [11], Bommarco et al. [12], and Abramova et al. [13] emphasize the use of ecosystems to ensure food security through environmental intensification and assessing environmental security based on functionality, organization, and stability. This may highlight the role of ecological taxation in financing approaches that promote sustainable development.

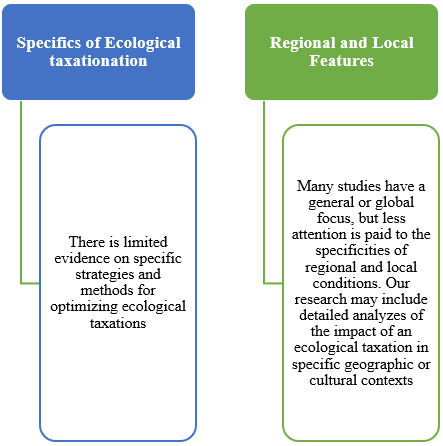

Taking all this into account, key gaps in the literature today can be identified (Figure 3).

Figure 3. Gaps in the literature are relevant to our research topic

Thus, the scientific question is to establish how to optimize ecological taxation in such a way as to ensure a high level of environmental safety.

The key method we will use is called simulation modeling. Simulation modeling is the process of using models to simulate real processes or systems to analyze their behavior. This allows researchers to experiment with these models in a controlled virtual environment. This method makes it possible to demonstrate the impact of a green tax on environmental protection to properly optimize it. This requires additional methods. One such method is correlation regression analysis. Correlation and regression analysis is an important addition to simulation modeling, especially when it comes to studying the impact of a green tax on environmental protection. While simulation modeling allows complex processes to be reproduced and analyzed under controlled conditions, correlation and regression analysis adds depth and rigor to this research. The selection of correlation regression analysis in the context of simulation modeling, particularly for studying the impact of a green tax on environmental protection, is rooted in its ability to uncover and quantify the intricate relationships between variables. This method is pivotal for understanding how various levels of green taxation (the independent variables) influence different environmental outcomes (the dependent variables). The theoretical basis for choosing this method centers on its proficiency in analyzing complex, multifaceted relationships within datasets. It is a statistical technique used to study the strength and nature of the relationship between two or more variables. The input variables are Revenues from emissions into the atmospheric air, million US dollars - x1, Revenues from discharges into water bodies, million US dollars - x2, Revenues from waste disposal, million US dollars - x3, Tax levied for the generation of radioactive waste, million US dollars - x4, Integral indicator of environmental protection, units - y. Input data is given in Table 1.

Table 1. Input data for identifying connections

|

Year |

x1 |

x2 |

x3 |

x4 |

y |

|

2018 |

1185 |

111 |

684 |

709 |

0.48 |

|

2019 |

3132 |

142 |

935 |

777 |

0.65 |

|

2020 |

2562 |

144 |

1014 |

976 |

0.68 |

|

2021 |

2581 |

159 |

153 |

1027 |

0.77 |

|

2022 |

3610 |

155 |

1254 |

1071 |

0.81 |

The Coefficient of Determination, denoted as R2, measures the proportion of the variance in the dependent variable that is predictable from the independent variable(s) in a regression model. The Fisher Criterion, commonly known as the F-Statistic, is used in the context of an overall significance test in regression analysis. It tests whether there is a relationship between the dependent and independent variables.

Both of these methods play a key role in solving complex analytical problems and help optimize the target object. All calculations will be made through Microsoft Excel. Moving on to simulation modeling of the impact of ecological taxation on environmental protection, we will use the AnyLogic Personal Learning Edition software application. This software product allows you to model, optimize, and visualize system dynamics processes and processes in various industries. Using AnyLogic Personal Learning Edition to simulate the effects of ecological taxation on environmental protection involves a systematic approach that integrates data analysis, model building, and simulation testing. All necessary data were obtained through Eurostat and the Swedish State Tax Administration.

Having carried out calculations in Microsoft Excel, we obtained the results of constructing a multiple regression equation shown in Table 2.

Table 2. Results of constructing a multifactor regression model

|

|

C |

Standard Error |

T |

P |

Lower 95% |

Upper 95% |

|

Intercept |

-0.184 |

0.16 |

-1.15 |

0.3 |

-0.62 |

0.26 |

|

x1 |

0.0000001 |

0.000001 |

0.8 |

0.4 |

0.0000002 |

0.000004 |

|

x2 |

0.000002 |

0.000003 |

0,6 |

0.6 |

-0.00001 |

0.00001 |

|

x3 |

-0.00001 |

0.00001 |

-0.9 |

0.4 |

-0.000003 |

0.000001 |

|

x4 |

0.0000012 |

0.000005 |

2.2 |

0.08 |

-0.0000003 |

0.000003 |

Thus, we obtain the following regression Eq. (1):

$y=-0.184+0,0000001 \times 1+0,000002 \times 2-0.00001 \times 3+0.0000012 \times 4$ (1)

According to Eq. (1), if you increase the flow from emissions into the atmospheric air by 100,000 thousand US, then the integral indicator of environmental protection will increase by 0.01 units, and if you increase the flow from discharges into water bodies by 100,000 thousand US, the integral indicator environmental protection in Sweden will increase by 0.2 units. In turn, if revenues from waste disposal increase by 100,000 thousand US dollars, then the integral indicator of environmental protection will decrease by 0.01 units. And if ecological taxation levied for the generation of radioactive waste increases by 100,000 thousand US dollars, the integral indicator of environmental protection will increase by 0.12 units.

Analyzing the adequacy of the constructed model, it can be noted that the relationship between the factors and the resulting variable is close - the coefficient of determination R2 is equal to 0.873, and significant - the value of the Fisher Criterion is equal to 6.873 and is in the critical region, respectively, the null hypothesis about the absence of influence of factors on the resulting variable is rejected.

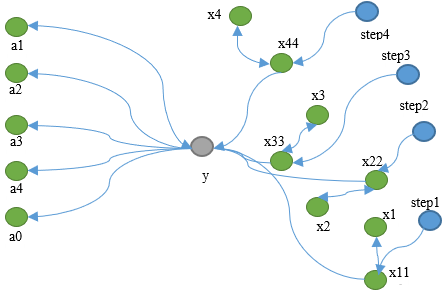

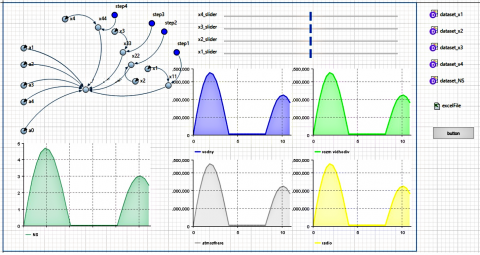

First, we create a project in the program and add all the necessary controls from the system dynamics panel. Following the task, the best tools would be System Dynamics for studying relationships and Statistics for the visual presentation of data. The general view of the constructed simulation model is shown in Figure 4.

In Figure 4, the parameters a0-a4 represent the coefficients of the regression equation. Parameters x1-x4 retain the original value of the system, which corresponds to the value of ecological taxation. To collect statistical data, we use the “Data Set” element and assign them the names dataset_x1-dataset_x4 and dataset_NS to collect and store information about the state and dynamics of x11-x44 variables. To visually represent dynamic changes in the simulation, we will place five elements of the “Time Graph” type, which will display the variables x11-x44 and “environmental protection”, respectively.

Accordingly, Figure 5 shows controls of the “ExcelFile” and “Button” types, which implement the export of statistical data to the MS Excel format. Moving on to the actual simulation modeling, it is necessary to determine the step at which it is expected that taxes will rise naturally, without making additional budget decisions. To achieve our goals, we assume that the volume of revenue from ecological taxation will grow annually by the absolute average increase in these indicators. The initial step is to assess the validity of the underlying assumption itself. This involves examining whether there is a logical and empirically supported basis for expecting that the growth in ecological tax revenue will correlate with the growth of the specified indicators. For instance, if the indicators are directly related to activities that are taxed or incentivized by the ecological tax, this assumption might be more credible. Bypassing and skipping intermediate calculations, we note that in this case the environmental protection indicator in Sweden will increase next year from 0.804 to 0.834, and the expected value in 5 years is 1.322. After increasing the x1 indicator (receipt from emissions into the atmosphere) by 20%, the environmental protection indicator will increase in the first year to 0.898 units, and after 5 years it will reach 1.386 units.

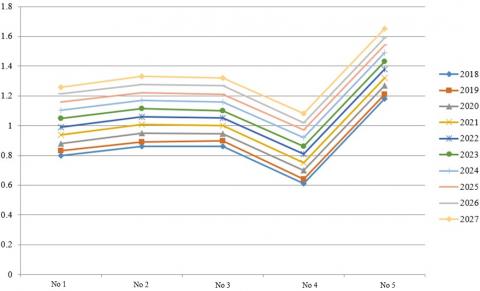

A total of 20 simulation tests were carried out, but for simplicity, we will present the first 5 (Table 3).

According to the results, the best one will provide an increase in revenues from emissions into the atmospheric air, from discharges into water bodies, and from the ecological taxation levied for the generation of radioactive waste (experiment No. 5). The worst result will be with an increase in revenue from waste disposal (experiment No. 4). A graphical display of the simulation results is presented in Figure 6.

Table 3. Results of a simulated experiment

|

No. |

Result |

|

1 |

All revenues should be increased by the corresponding average absolute increase for the period under study |

|

2 |

The effect of experiment 1 and x1 increase by 20% |

|

3 |

The effect of experiment 1 and x2 increased by 20% |

|

4 |

The effect of experiment 1 and x3 increase by 20% |

|

5 |

The effect of experiment 1 and increase x1, x2, x4 by 20% |

Figure 4. General view of the simulation model of system dynamics

Figure 5. General view of the constructed model

Figure 6. The value of the environmental protection indicator in accordance with the simulation experiments carried out

To optimize the budget and ecological taxation in Sweden to improve environmental protection, based on the results of simulation modeling, it is possible to propose an increase in revenues from air emissions, from discharges into water bodies, and from the ecological taxation levied on the generation of radioactive waste: review and increase tax rates on pollutant emissions This can encourage enterprises to introduce cleaner technologies; introducing differentiated rates for different types of pollutants, especially those that have a greater negative impact on the environment.

In the context of the simulation model presented in the study, control mechanisms serve to ensure the validity and accuracy of the results. First, the model validation process ensures that it adequately reproduces real-world conditions and processes based on comparison with historical data or scientifically based hypotheses. Calibrating the model allowed the parameters to be adjusted so that they best match the actual conditions or expected behavior of the system. This helped refine the model and make its predictions more accurate. Sensitive analysis, on the other hand, was used to identify how changes in input data affect the model's output. This is especially important for identifying those factors that have the greatest influence on the results, as well as for defining the boundaries of the model.

Let's compare our study with others that are involved in our results. For example, studies like Abramova et al. [13], and Rainaldi [14] highlight the importance of regulatory policies for the efficiency of tax revenues. This indicates the need to take into account regulatory devices when developing ways to optimize ecological taxation. At the same time, it is possible to protect the environment by ensuring environmental safety, where taxation is already part and parcel of it [15].

Other scientists, for example, Jørgensen [16] and Chaplin-Kramer et al. [17] focus on the application of ecological models to assess sustainability or the formation of mechanisms of cooperation and competition in networked information ecological chains. This can help to understand the interactions between different stakeholders in the context of ecological taxation. When other scholars and practitioners model the balance in ecosystem supply chains [18-21], which applies to the development of models for ecological taxation optimization, or focus on farmers' participation in decision-making on environmental protection of water resources, which can provide important lessons for engaging the public and different stakeholder groups in the process of ecological taxation optimization.

Unlike others, we have presented a comprehensive modeling approach. Introducing differentiated rates for different types of pollutants, especially those that hurt the environment. Unlike static analytical models, simulation modeling can reflect changing conditions and system adaptation to different scenarios in real-time.

The effects of changes in the level of environmental protection achieved as a result of applying different scenarios for implementing ecological taxation reform in Sweden were modeled. The optimal scenario for ecological taxation reform in Sweden is confirmed through simulation modeling using the AnyLogic toolkit. It is substantiated that for Sweden, the optimal reform scenario will be an increase in the level of taxation for emissions into the atmospheric air, from discharges into water bodies, and from the ecological taxation levied for the generation of radioactive waste. At the same time, increasing ecological taxation for waste disposal will not have an effective result in ensuring environmental protection, which requires the use of other waste control tools.

As a result, the visual representation of models helps to better understand the impact of ecological taxation and facilitates a more effective perception of information by different groups of stakeholders. We have proven that simulation modeling is an important tool in studying the environmental impact of green taxes, allowing for the consideration of a wide range of factors and providing more accurate and informed environmental policy recommendations.

The study is limited by taking into account the specifics of only one country during optimization and therefore the variables are selected only after that.

As a result, it should also be noted that in the context of intensifying global environmental threats, accompanied by an increase in destructive anthropogenic impact on the environment, the development and implementation of effective environmental policies aimed not only at directly neutralizing environmental threats but also at eliminating their transmission effect is of strategic importance on the environmental, energy and economic security of the country. In particular, it is quite natural that the aggravation of environmental problems associated with emissions of pollutants into the air, water bodies, and soil, and the lack of effective tools for managing household and industrial waste (especially radioactive) hurt the state of the country’s environmental safety, but this influence is not point and static, but continues its transmission into other important components of environmental protection. All this should be taken into account in further research.

[1] One planet. Naturum - visitor centres in nature. https://www.oneplanetnetwork.org/news-and-events/news/naturum-visitor-centres-nature, accessed on January 9, 2022.

[2] Omodero, C.O., Ujah, P.I., Iyoha, F.O. (2022). Foreign direct investment and information communication technology taxation effects on tax income growth. Revue d'Intelligence Artificielle, 36(3): 387-393. https://doi.org/10.18280/ria.360306

[3] Borutska, Y., Vashchyshyn, M., Zhurba, I., Leskiv, H., Taranenko, H., Panteleiev, M. (2023). State environmental impact management in ecological tourism development. International Journal of Design & Nature and Ecodynamics, 18(5): 1247-1254. https://doi.org/10.18280/ijdne.180527

[4] Xu, C.Y., Pu, L.J., Zhu, M., Li, J.G., Chen, X.J., Wang, X.H., Xie, X.F. (2016). Ecological security and ecosystem services in response to land use change in the coastal area of Jiangsu, China. Sustainability, 8(8): 816. https://doi.org/10.3390/su8080816

[5] Singh, A.K., Jyoti, B., Kumar, S., Lenka, S.K. (2021). Assessment of global sustainable development, environmental sustainability, economic development and social development index in selected economies. International Journal of Sustainable Development and Planning, 16(1): 123-138. https://doi.org/10.18280/ijsdp.160113

[6] Salamatov, A., Gordeeva, D., Agapov, A. (2021). Sociocultural dynamics of sustainable development: Formation of human potential in the process of integrated ecological and economic training. International Journal of Environmental Impacts, 4(1): 62-76. https://doi.org/10.2495/EI-V4-N1-62-76

[7] Deswanto, R.B., Siregar, S.V. (2018). The associations between environmental disclosures with financial performance, environmental performance, and firm value. Social Responsibility Journal, 14(1): 180-193. https://doi.org/10.1108/SRJ-01-2017-0005

[8] Kovács‐Hostyánszki, A., Espíndola, A., Vanbergen, A. J., Settele, J., Kremen, C., Dicks, L.V. (2017). Ecological intensification to mitigate impacts of conventional intensive land use on pollinators and pollination. Ecology Letters, 20(5): 673-689. https://doi.org/10.1111/ele.12762

[9] Feng, Y.J., Yang, Q.Q., Tong, X.H., Chen, L.J. (2018). Evaluating land ecological security and examining its relationships with driving factors using GIS and generalized additive model. Science of the Total Environment, 633: 1469-1479. https://doi.org/10.1016/j.scitotenv.2018.03.272

[10] Venkateswarlu, K., Nirola, R., Kuppusamy, S., Thavamani, P., Naidu, R., Megharaj, M. (2016). Abandoned metalliferous mines: Ecological impacts and potential approaches for reclamation. Reviews in Environmental Science and Bio/Technology, 15: 327-354. https://doi.org/10.1007/s11157-016-9398-6

[11] Zhan, L.K., Guo, X.H., Li, T.Z., Liu, X., Lu, C.D., Zhang, N., Lu, Z.H. (2022). Ecological security measurement based on functionality-organization-stability in inland of Three Gorges Reservoir area. Journal of Environmental Engineering and Landscape Management, 30(3): 433-449. https://doi.org/10.3846/jeelm.2022.17408

[12] Bommarco, R., Kleijn, D., Potts, S.G. (2013). Ecological intensification: Harnessing ecosystem services for food security. Trends in Ecology & Evolution, 28(4): 230-238. https://doi.org/10.1016/j.tree.2012.10.012

[13] Abramova, A., Chub, A., Kotelevets, D., Lozychenko, O., Zaichenko, K., Popov, O. (2022). Regulatory policy of tax revenues efficiency assurance as the dominant of state economic security. International Journal of Sustainable Development & Planning, 17(6): 1727-1736. https://doi.org/10.18280/ijsdp.170606

[14] Rainaldi, M. (2023). Digital optimization of public assets for enhanced resilience to socioeconomic and environmental disruptions. International Journal of Environmental Impacts, 6(3): 129-134. https://doi.org/10.18280/ijei.060305

[15] Ruan, W.Q., Li, Y.Q., Zhang, S.N., Liu, C.H. (2019). Evaluation and drive mechanism of tourism ecological security based on the Dpsir-Dea model. Tourism Management, 75: 609-625. https://doi.org/10.1016/j.tourman.2019.06.021

[16] Jørgensen, S.E. (2016). Application of ecological models for assessment of sustainability. International Journal of Design & Nature and Ecodynamics, 11(3): 153-167. https://doi.org/10.2495/DNE-V11-N3-153-167

[17] Chaplin‐Kramer, R., Jonell, M., Guerry, A., Lambin, E.F., Morgan, A.J., Pennington, D., Smith, N., Franch, J.A., Polasky, S. (2015). Ecosystem service information to benefit sustainability standards for commodity supply chains. Annals of the New York Academy of Sciences, 1355(1): 77-97. https://doi.org/10.1111/nyas.12961

[18] Lou, C.Q., Gui, X.M., Yan, G. (2013). Study on operation mechanism of network information ecological chain: Cooperative competition mechanism. Information Science, 31(8): 6-12.

[19] Jian, T, Zuogong, W., Jiang, G.Q. (2018). Modelling and simulation of the balance of supply chain ecosystem. Journal Européen des Systèmes Automatisés, 51(4-6): 273-281. https://doi.org/10.3166/JESA.51.273-281

[20] Sylkin, O., Krupa, O., Borutska, Y., Todoshchuk, A., Zhurba, I. (2023). Exploring the impact of international tourism on regional sustainable development: A methodological approach for enhancing effectiveness. International Journal of Sustainable Development & Planning, 18(7): 2089-2096. https://doi.org/10.18280/ijsdp.180711

[21] Levchenko, O., Levchenko, A., Kolisnichenko, R., Tsumariev, M., Zaverbnyj, A. (2023). Formation of a model of legal protection of competitive advantages in the system of innovation management of sustainable development and planning. International Journal of Sustainable Development & Planning, 18(4): 1227-1233. https://doi.org/10.18280/ijsdp.180427